1. icv kongres controllera srbije 2013, dragan vještica, head of controlling, metro

TRANSCRIPT

METRO Cash & Carry Serbia Member of

ICV Serbia

KPI’s in Retail Industries

Belgrade

May 17th , 2013

METRO Cash & Carry Serbia Member of Page 2

METRO GROUP

Retail vs. Manufacturing

Classification of KPI

Summary

CCC

Monitoring P&L KPI’s

METRO Cash & Carry Serbia Member of Page 3

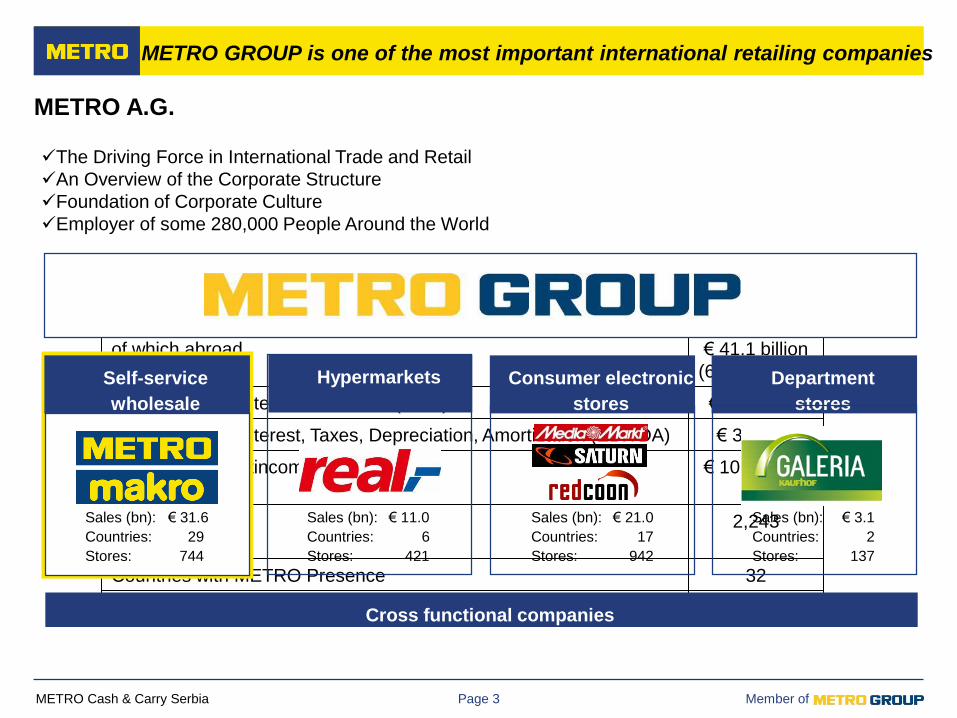

The Driving Force in International Trade and Retail

An Overview of the Corporate Structure

Foundation of Corporate Culture

Employer of some 280,000 People Around the World

METRO A.G.

METRO GROUP is one of the most important international retailing companies

Fiscal Year 2012

Sales € 66.7 billion

of which abroad € 41.1 billion

(61.6 percent)

Earning before Interest and Taxes (EBIT) € 1.4 billion

Earning before Interest, Taxes, Depreciation, Amortization (EBITDA) € 3 billion

Consolidated Netincome € 101 million

Locations 2,243

Countries with METRO Presence 32

Number of Staff on Annual Average Total 282,989

Sales (bn): € 21.0

Countries: 17

Stores: 942

Cross functional companies

Hypermarkets

Sales (bn): € 11.0

Countries: 6

Stores: 421

Self-service

wholesale

Sales (bn): € 31.6

Countries: 29….

Stores: 744

Sales (bn): € 3.1

Countries: 2

Stores: 137

Consumer electronic

stores

Department

stores

METRO Cash & Carry Serbia Member of Page 4

Retail vs. Manufacturing

METRO GROUP

Classification of KPI

Summary

CCC

Monitoring P&L KPI’s

METRO Cash & Carry Serbia Member of

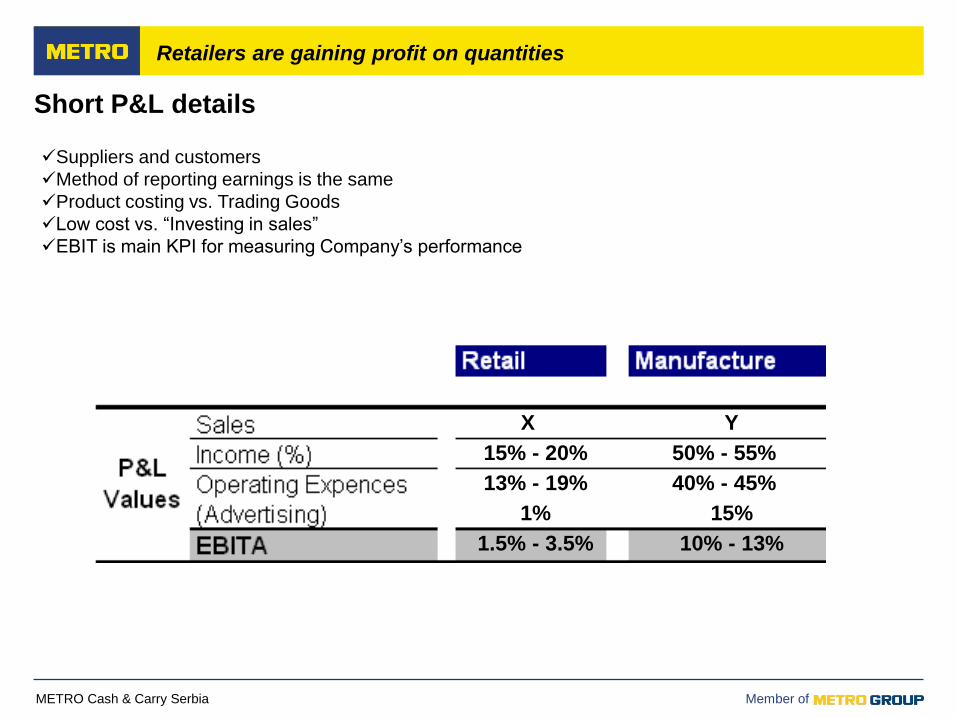

Short P&L details

Retailers are gaining profit on quantities

X Y

15% - 20% 50% - 55%

13% - 19% 40% - 45%

1% 15%

1.5% - 3.5% 10% - 13%

Suppliers and customers

Method of reporting earnings is the same

Product costing vs. Trading Goods

Low cost vs. “Investing in sales”

EBIT is main KPI for measuring Company’s performance

METRO Cash & Carry Serbia Member of Page 6

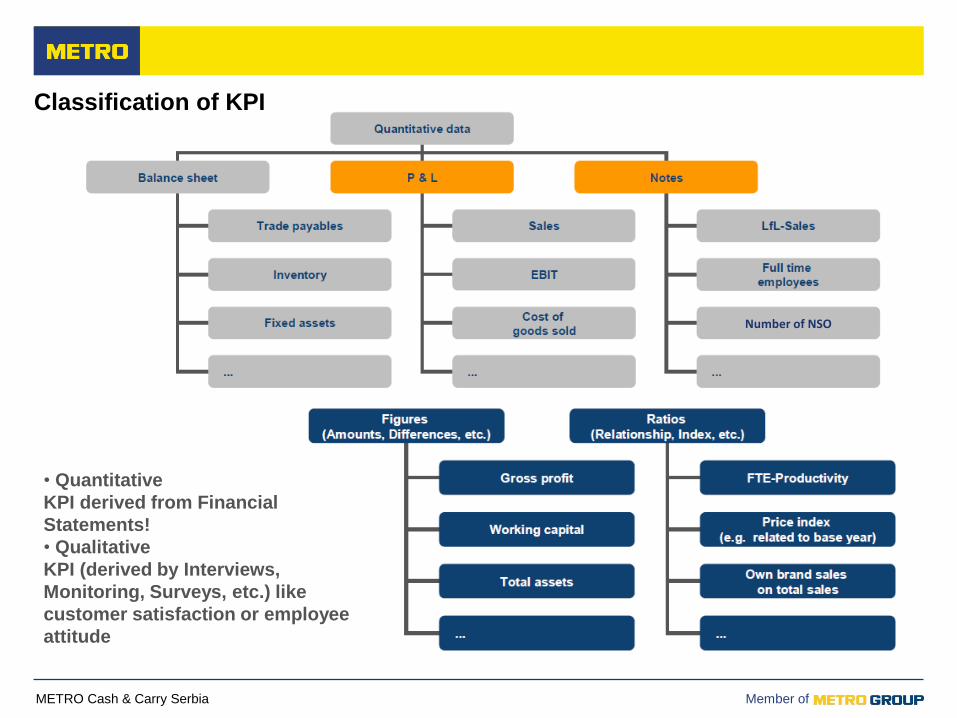

Classification of KPI

METRO GROUP

Retail vs. Manufacturing

Summary

CCC

Monitoring P&L KPI’s

METRO Cash & Carry Serbia Member of

• Quantitative

KPI derived from Financial

Statements!

• Qualitative

KPI (derived by Interviews,

Monitoring, Surveys, etc.) like

customer satisfaction or employee

attitude

Classification of KPI

Number of NSO

METRO Cash & Carry Serbia Member of Page 8

Monitoring P&L KPI’s

METRO GROUP

Retail vs. Manufacturing

Summary

CCC

Classification of KPI

METRO Cash & Carry Serbia Member of

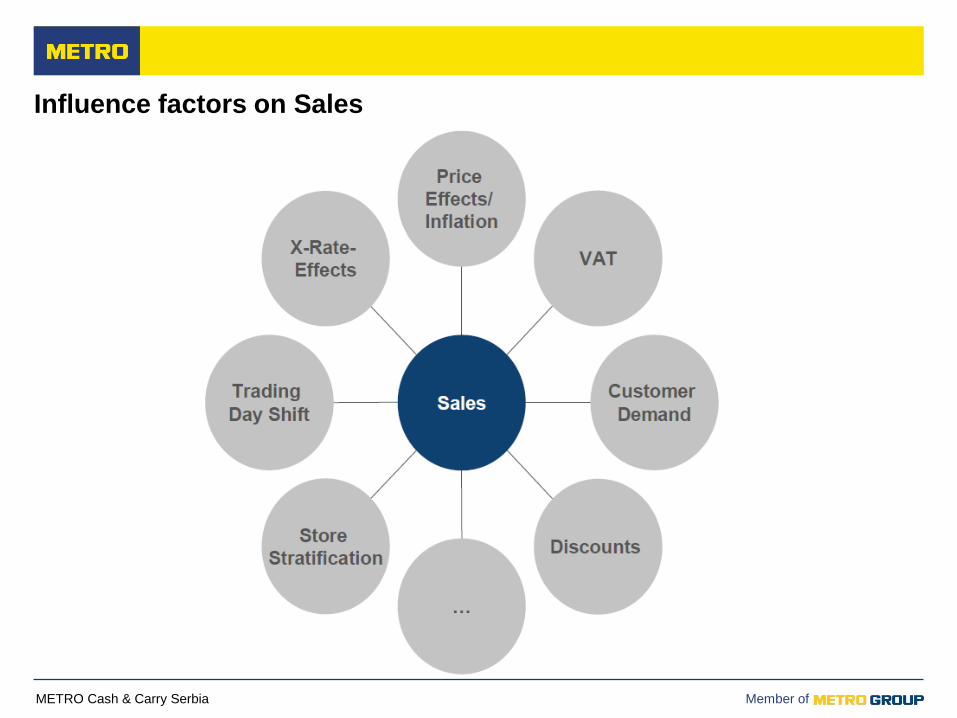

Influence factors on Sales

METRO Cash & Carry Serbia Member of

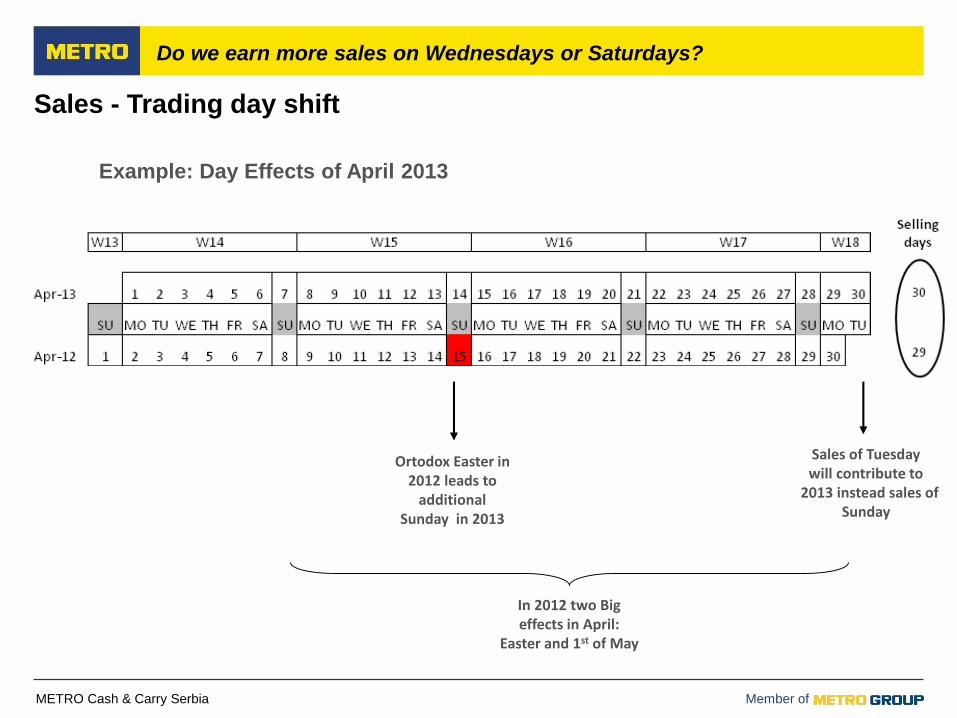

Sales - Trading day shift (I)

Example: Day Effects of April 2013

Sales - Trading day shift

Do we earn more sales on Wednesdays or Saturdays?

Sales of Tuesdaywill contribute to

2013 instead sales of Sunday

Ortodox Easter in 2012 leads to

additional Sunday in 2013

In 2012 two Big effects in April:

Easter and 1st of May

METRO Cash & Carry Serbia Member of

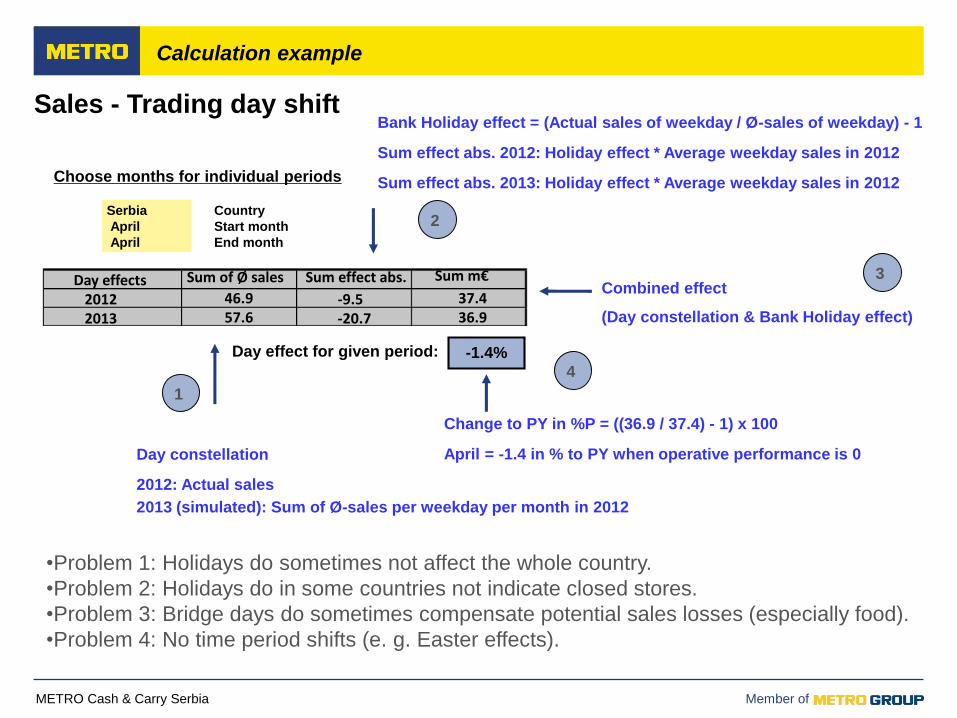

Bank Holiday effect = (Actual sales of weekday / Ø-sales of weekday) - 1

Choose months for individual periods

Serbia

April

April

Country

Start month

End month

Sum effect abs. 2012: Holiday effect * Average weekday sales in 2012

Sum effect abs. 2013: Holiday effect * Average weekday sales in 2012

Combined effect

(Day constellation & Bank Holiday effect)

Day constellation

Change to PY in %P = ((36.9 / 37.4) - 1) x 100

April = -1.4 in % to PY when operative performance is 0

2012: Actual sales

2013 (simulated): Sum of Ø-sales per weekday per month in 2012

•Problem 1: Holidays do sometimes not affect the whole country.

•Problem 2: Holidays do in some countries not indicate closed stores.

•Problem 3: Bridge days do sometimes compensate potential sales losses (especially food).

•Problem 4: No time period shifts (e. g. Easter effects).

Sales - Trading day shift

Calculation example

2

1

3

4

Day effect for given period:

Day effects20122013

Sum of Ø sales Sum effect abs. Sum m€

46.957.6

-9.5-20.7

37.436.9

-1.4%

METRO Cash & Carry Serbia Member of

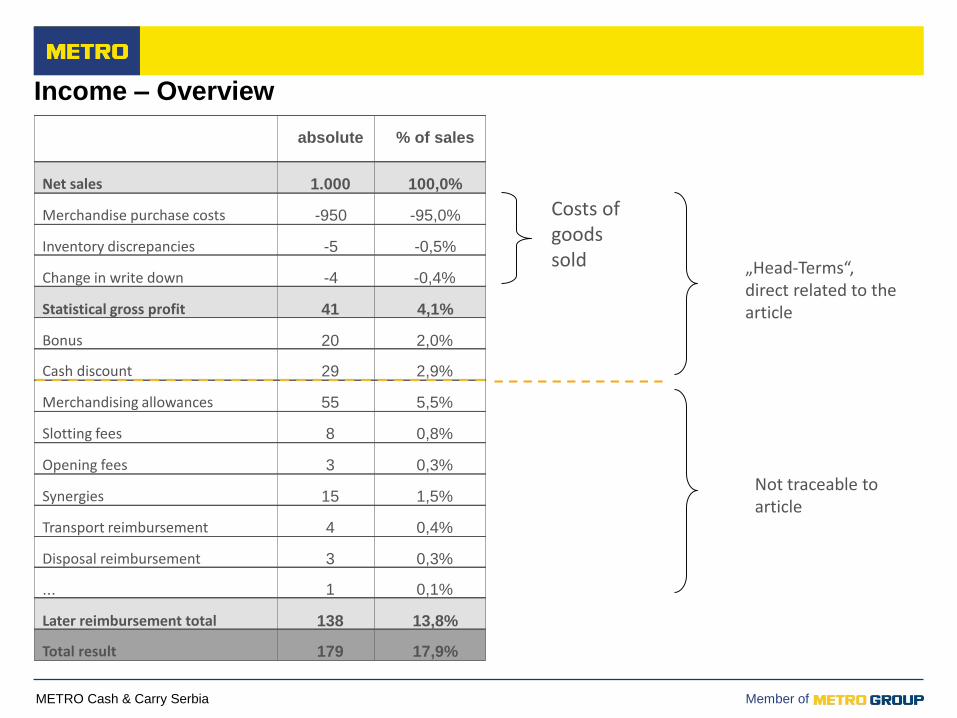

absolute

Net sales

% of sales

100,0%1.000

Merchandise purchase costs -95,0%-950

Inventory discrepancies -0,5%-5

Change in write down -0,4%-4

Statistical gross profit 4,1%41

Bonus

Cash discount

Merchandising allowances

Slotting fees

Opening fees

Synergies

Transport reimbursement

Disposal reimbursement

...

2,0%

2,9%

5,5%

0,8%

0,3%

1,5%

0,4%

0,3%

0,1%

20

29

55

8

3

15

4

3

1

Later reimbursement total 13,8%138

Total result 17,9%179

„Head-Terms“,direct related to thearticle

Not traceable toarticle

Income – Overview

Costs ofgoodssold

METRO Cash & Carry Serbia Member of

Income: t0: 8,8% x 1.000 = 88 €

Marginin % o.s.

t1: 10,2% x 1.300 = 132,6 € : 44,6 €

10,2%

Margin-related variance:Sales-related and margin-

related variance:

(10,2% - 8,8%) x 1.000 = €14

8,8%

t0Sales-related

variance:

t1(10,2% - 8,8%) x

(1.300 -1.000) = 4,2

(1.300 – 1.000)

x 8,8% = €26,4

1.000Sales

1.300

Calculation of income variances

Income Variance

METRO Cash & Carry Serbia Member of

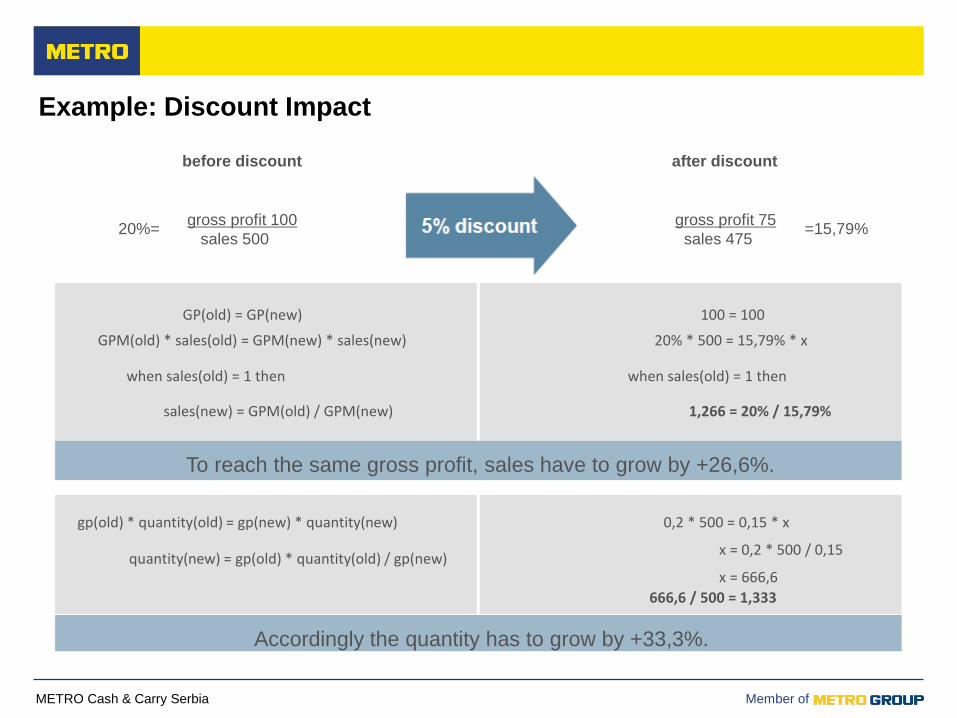

Example: Discount Impact

ABC Trading company has weekly sales of 500 € (quantity 500 with a price of 1 €).

The gross profit margin is 20%.

For one week there is a special promotion campaign which is offering 5% discount.

What is the necessary quantity growth to reach the same gross profit as

before?

MADE TO TRADE. Retail Key Figures. Financial Management Training June 2012 | © METRO AG 2012 21

METRO Cash & Carry Serbia Member of

before discount after discount

20%=gross profit 100

sales 500

gross profit 75

sales 475=15,79%

GP(old) = GP(new) 100 = 100

GPM(old) * sales(old) = GPM(new) * sales(new) 20% * 500 = 15,79% * x

when sales(old) = 1 then when sales(old) = 1 then

sales(new) = GPM(old) / GPM(new) 1,266 = 20% / 15,79%

To reach the same gross profit, sales have to grow by +26,6%.

gp(old) * quantity(old) = gp(new) * quantity(new) 0,2 * 500 = 0,15 * x

quantity(new) = gp(old) * quantity(old) / gp(new)x = 0,2 * 500 / 0,15

x = 666,6

666,6 / 500 = 1,333

Accordingly the quantity has to grow by +33,3%.

Example: Discount Impact

METRO Cash & Carry Serbia Member of

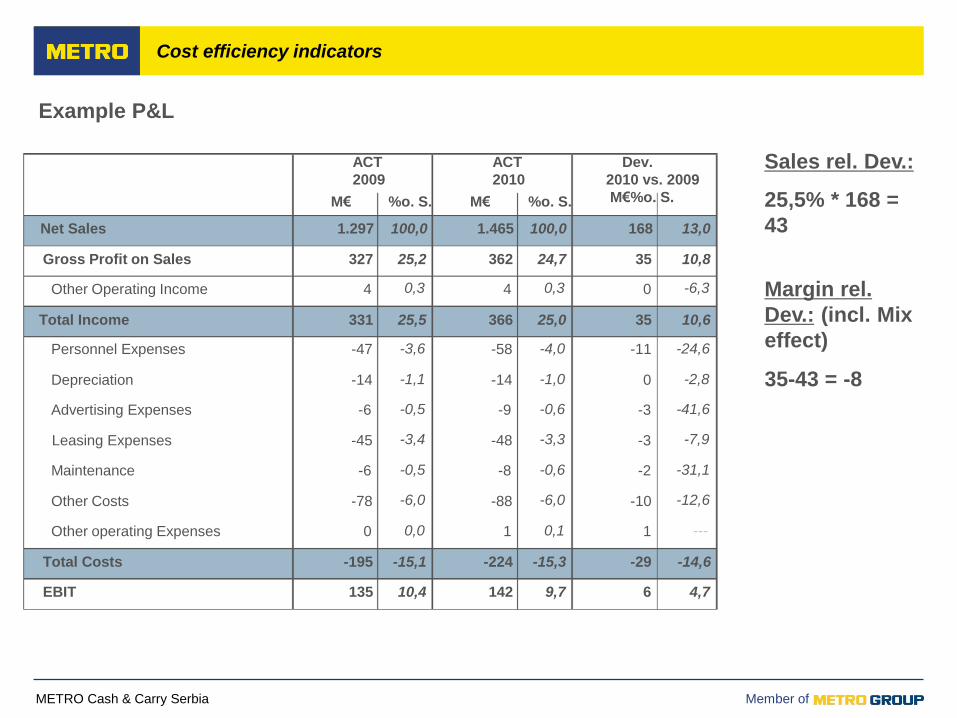

Example P&L

ACT

2009

M€

Net Sales

Gross Profit on Sales

Other Operating Income

Total Income

Personnel Expenses

Depreciation

Advertising Expenses

Leasing Expenses

Maintenance

Other Costs

Other operating Expenses

Total Costs

EBIT

1.297

327

4

331

-47

-14

-6

-45

-6

-78

0

-195

135

%o. S.

100,0

25,2

0,3

25,5

-3,6

-1,1

-0,5

-3,4

-0,5

-6,0

0,0

-15,1

10,4

M€

1.465

362

4

366

-58

-14

-9

-48

-8

-88

1

-224

142

ACT

2010

%o. S.

100,0

24,7

0,3

25,0

-4,0

-1,0

-0,6

-3,3

-0,6

-6,0

0,1

-15,3

9,7

Dev.

2010 vs. 2009

M€%o. S.

168

35

0

35

-11

0

-3

-3

-2

-10

1

-29

6

13,0

10,8

-6,3

10,6

-24,6

-2,8

-41,6

-7,9

-31,1

-12,6

---

-14,6

4,7

Sales rel. Dev.:

25,5% * 168 =

43

Margin rel.

Dev.: (incl. Mix

effect)

35-43 = -8

Cost efficiency indicators

METRO Cash & Carry Serbia Member of

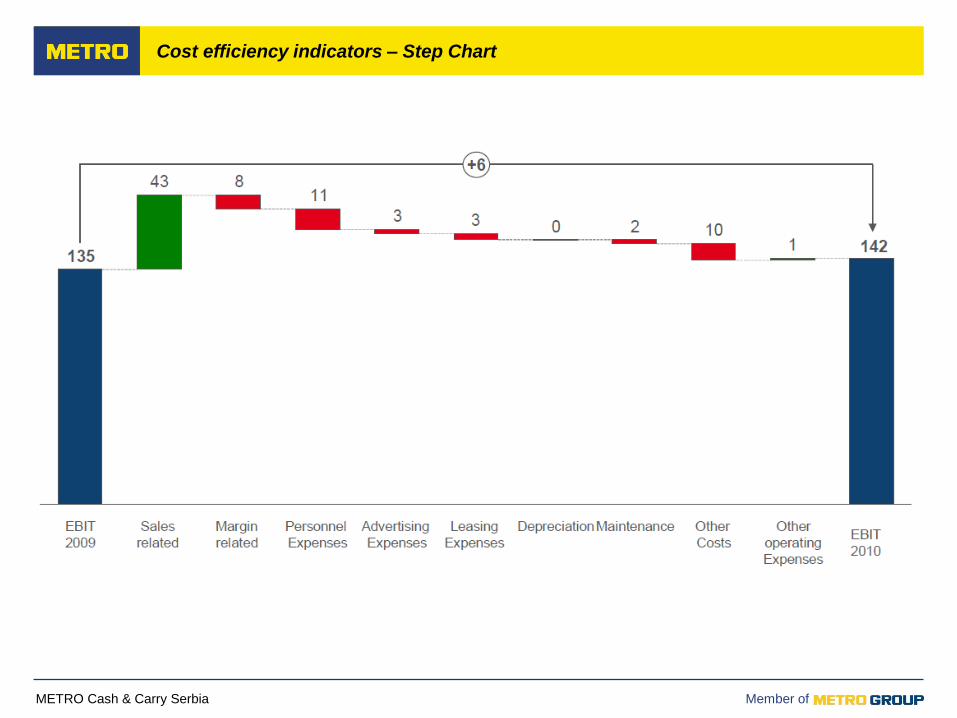

Cost efficiency indicators – Step Chart

METRO Cash & Carry Serbia Member of Page 18

Summary

METRO GROUP

Retail vs. Manufacturing

Monitoring P&L KPI’s

CCC

Classification of KPI

METRO Cash & Carry Serbia Member of

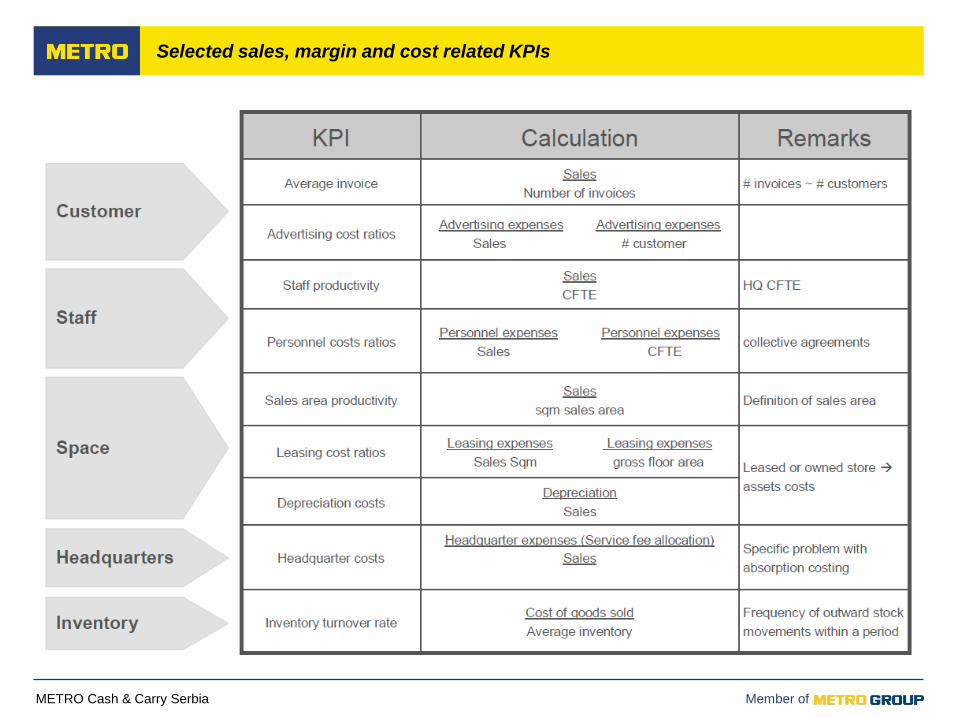

Selected sales, margin and cost related KPIs

METRO Cash & Carry Serbia Member of Page 20

CCC

METRO GROUP

Retail vs. Manufacturing

Monitoring P&L KPI’s

Summary

Classification of KPI

METRO Cash & Carry Serbia Member of

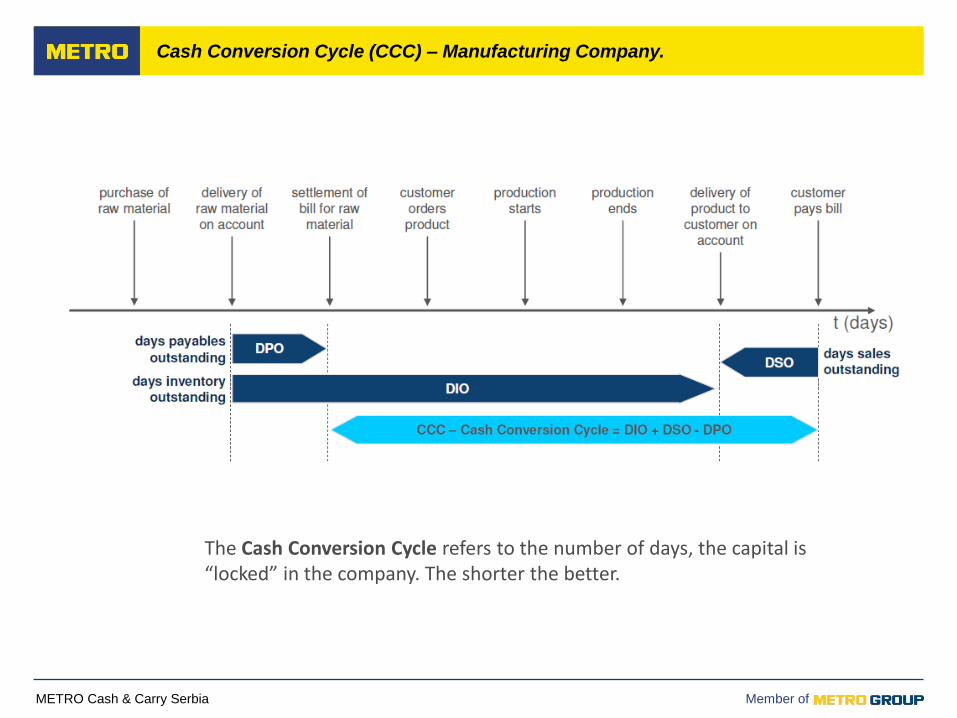

Cash Conversion Cycle (CCC) – Manufacturing Company.

The Cash Conversion Cycle refers to the number of days, the capital is“locked” in the company. The shorter the better.

Cash Conversion Cycle (CCC) – Manufacturing Company.

METRO Cash & Carry Serbia Member of

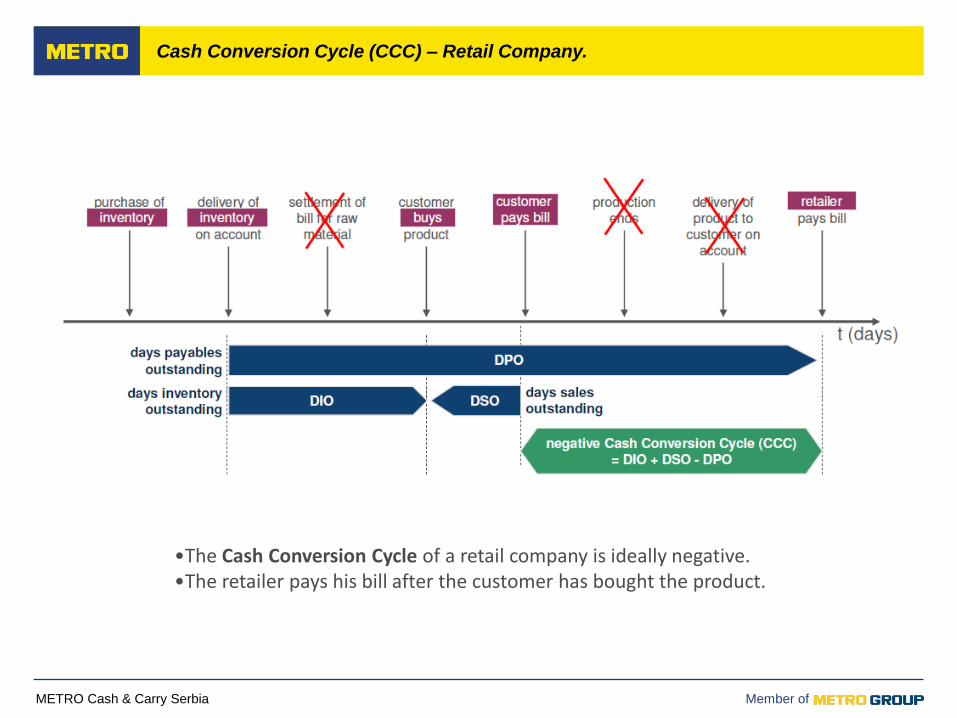

Cash Conversion Cycle (CCC) – Retail Company.

negative Cash Conversion Cycle (CCC)

= DIO + DSO - DPO

•The Cash Conversion Cycle of a retail company is ideally negative.•The retailer pays his bill after the customer has bought the product.

Cash Conversion Cycle (CCC) – Retail Company.