1 q15 results

TRANSCRIPT

1

Marzo 2014

1Q 2015 Results

April 2015

2

Operating structure

Note: The percentages of control are updated as of 31 March and are calculated net of treasury shares

€644 m €1.35 Bio €392 m

All Media sectors from

dailies and periodicals

to radio, Internet, and

advertising

Global automotive

components supplier

(filters, engine air and

cooling systems and

suspensions)

Nursing homes,

rehabilitation and

hospital management

Private equity

Education

Revenues

2014

Businesses

Competitive

position

Leader in circulation of Italian dailies

N.1 news magazine

N.1 Italian information website

Third Italian radio network

Leader in its core

businesses (filters and

suspensions) in

Europe and South

America

--

Leader in Italian long

term care (nursing

homes and

rehabilitation)

Non-core investments

56.1% 57.7% 51.3%

Total € 2.4 Bio

3

• Founded in 1976 by Carlo De Benedetti; controlled (45.8%) by COFIDE-Gruppo

De Benedetti

• Long term investment strategy, with focus on controlling stakes

• Balanced portfolio of businesses, with leading positions in their respective

businesses

• Active role in governance and in strategic decision making of portfolio

companies

• No leverage and significant liquidity available at holding company level

• Commitment to low cost structure

CIR Group profile

4

• On July 23, 2014 CIR, Sorgenia Holding and VERBUND AG signed an

agreement with creditors for the restructuring of Sorgenia’s debt. At the same

time, Sorgenia signed a standstill agreement with the lending banks

• The debt restructuring process followed the “182 bis” court procedure, which

was concluded on February 25, 2015, when the Court of Milan approved the

debt restructuring plan

• On March 27 2015 the lending banks subscribed to a capital increase in

Sorgenia of approximately € 400 million and a convertible loan of about € 200

million through the conversion of receivables. CIR simultaneously sold its

stake in Sorgenia and no longer owns any shares in the energy company

Exit from Sorgenia

5

• Consolidated net income: € 21.2 million (vs. -€ 2.6 million in 1Q 2014).

Contribution of industrial businesses (Espresso, Sogefi and KOS) is + € 13

million, vs. a loss of €1.2 million in 1Q 2014

• Consolidated net financial position of the CIR Group at March 31, 2015:

- €157.4 million (vs. - €112.8 million at 31 December 2014), including:

- A net financial surplus at holding level of €370.1 million

- A net debt of consolidated subsidiaries of - €527.5 million (vs. - €492.3

at 31 December 2014)

1Q 2015 consolidated financial highlights

6

Consolidated income statement

Group net result (2.6) 21.2

€ m

Income taxes (8.8) (8.9)

(14.0) Financial expense/income 5.6

22.1

1Q 2014 1Q 2015

EBIT

EBITDA 46.0 61.4

36.2

Revenues 588.7 628.0

Loss on assets held for sale (1.1) --

(1) Net of third party interests (equal to €11.7 million in 1Q 2015)

(1)

7

Consolidated income statement by business sector

€ m

(2) Including Treasury and non core investments

1Q 2014 1Q 2015

CIR holding level (1.4) 8.2

Net result (2.6) 21.2

(2)

1.3 KOS Group 1.9

(3.6) Sogefi Group

Espresso Group 1.1 6.7

4.4

(1.2) Total industrial companies 13.0 (1)

(1) Pro-rata share of subsidiaries’ net income

8

Consolidated balance sheet – main group assets

€ m

Group equity in consolidated balance sheet 31 Dec. 2014 31 Mar. 2015

129.5 KOS 131.5

95.1 Sogefi

Espresso 347.9 357.2

107.3

(1) Including Cir Ventures, Education and other minor investments

Fixed assets 18.1 17.9

572.5 Total industrial companies 596.0

NPLs 49.3 49.2

Private equity 67.7 72.8

Other investments 33.9 35.7

Other assets/liabilities

Net cash

(16.5)

379.5

(14.0)

370.1

(1)

1,104.5 1,127.7 Consolidated shareholders’equity

532.0 Total CIR and non industrial companies 531.7

(2) Non Performing Loans portfolios

(2)

9

Consolidated net financial position

€ m

31 Dec. 2014 31 Mar. 2015

(157.0) KOS Group (195.5)

(304.3)

CIR holding level 379.5 370.1

Sogefi Group

Espresso Group (34.2) (11.2)

(327.5)

(492.3) Total subsidiaries (527.5)

Consolidated net financial indebtedness (112.8) (157.4)

3.2 Other subsidiaries 6.7

Total shareholders’ equity 1,573.2 1,613.5

Consolidated net invested capital 1,686.0 1,770.9

(1) Including third party interests

(1)

10

379.5 + 6.4+ 2.5 - 3.9- 14.4

370.1

0

50

100

150

200

250

300

350

400

Net financial surplus

at Dec.31, 2014

Shares buyback Net divestitures Financial income Other costs Net financial surplus

at Mar. 31, 2015

(€ m)

• Decrease of net cash at holding system level is mainly due to purchases of

treasury shares

Net financial position at “holding system” level

Evolution of net financial position

(1)

(1) Fair value of securities + securities income, trading

(2) Operating costs, extraordinary costs, taxes, etc.

(2)

11

Composition of liquid assets and gross financial debt

Liquid assets at 31 March 2015

€ m

Hedge funds

Other (stocks, equity funds)

382.1

96.0

95.1

30.1

370.1

80.9

32.0

31 Dec.

2014

31 Mar.

2015

Cash and time deposits

Corporate bonds

Government bonds

57.9

5.7

68.6

58.0

7.6

99.3

Total liquid assets

31 Dec.

2014

31 Mar.

2015

CIR S.p.A. 2004/2024 -- --

2.6 -- Gross finanacial debt

Other debt 2.6 --

Fixed income funds 94.0 123.0

12

1Q 2015 Subsidiaries’ financial and operational highlights

Key strategic objectives 1Q 2015 Highlights

Expansion of digital platforms, leveraging on

leadership in traditional media

Further efficiency improvement

Selective growth in emerging industry sectors, with

international focus

Further consolidation in Italian nursing and

rehabilitation

Geographical expansion (India)

Completion of global footprint, through growth in

non-European countries

Further efficiency improvement and restructuring of

manufacturing footprint

Product innovation

Decrease of press advertising revenues (-6.9%), vs. -8.0% of the market

Still, in such challenging market, Espresso reported positive net results, stable EBITDA and decreasing net debt (€11.2 m vs. €34.2m at 4Q2014), thanks to continuing efforts on efficiency improvement

La Repubblica is the top daily newspaper for newsstand sales and readership

Repubblica.it confirms its leadership among Italian news sites with 1.6 million unique users per day

Espresso

Sogefi

KOS

Non-core

investments

Positive performance of Education business

Continuing growth of revenues (+11.8%) and EBITDA (+23.4%) thanks to

ongoing organic and external growth

Laurent Hebenstreit selected as the new CEO; formal appointment

expected in June

Revenues growth of 10% at consolidated level (+5.9% at constant

exchange rates):

- Double digit growth in North America (+15.1%) and Asia (+39.7%);

- + 7.7% in Europe

- Continuing weakness in Latin America

Improving EBITDA and net income thanks to higher volumes, favourable

exchange rates and lower restructuring costs

13

Espresso - overview

1Q 2015 Revenues breakdown

NATIONAL PRESS

DIGITAL

ADVERTISING

National daily newspaper

18 Regional newspapers throughout Italy

Group websites

Three national radio stations

LOCAL

NEWSPAPERS

RADIO

Collection of advertising

€ m

1Q 2014 1Q 2015

Revenues 152.3 146.6

Net income 2.1 12.0

EBITDA 14.2 13.9

Key financials Operating structure

1Q 2015 Performance and outlook

• Circulation revenues at € 55.7 million, decreasing by 3.8%, in a

market down 9.8%. Advertising revenues were down 2.8%, less

than the market (-5.2% in February). Radio advertising grew

+2.6%; internet was in line (+0.1%)

• The increase in net income was due to lower income taxes (by €

2.0 million), to the reorganization of television activities (impact

+€ 1.1 million) and to the capital gain of € 6.1 million related to

the sale of All Music (Deejay TV) to Discovery Italy

• FY 2015 outlook is highly dependent on the performance of the

advertising market, which at present is still uncertain, despite

late signs of improvement

14

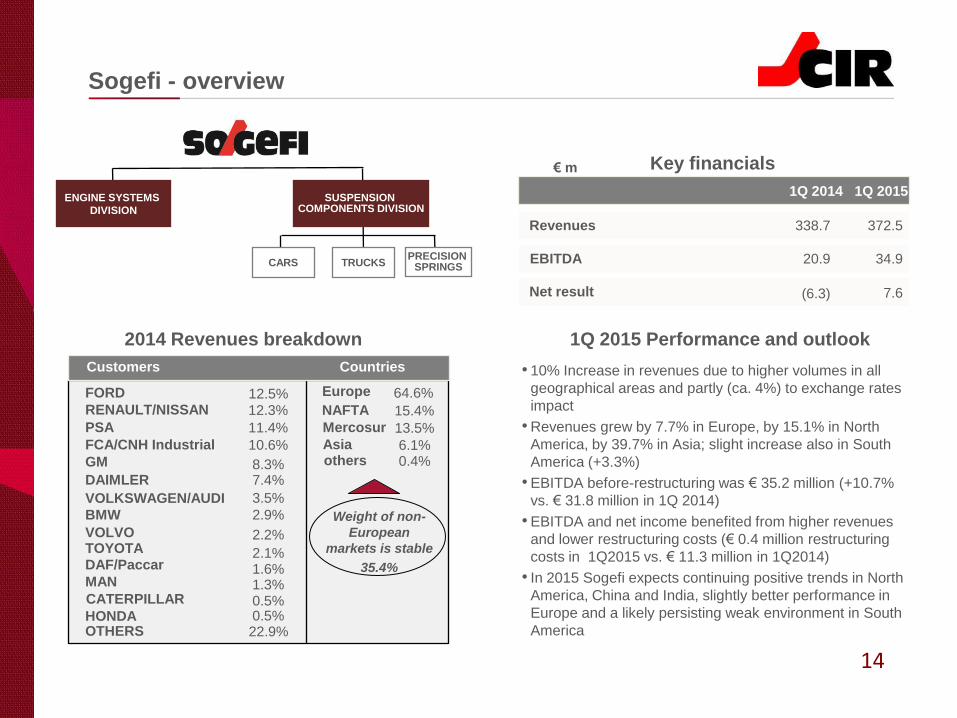

Sogefi - overview

Revenues 338.7 372.5

Net result (6.3) 7.6

EBITDA 20.9 34.9

Key financials

ENGINE SYSTEMS

DIVISION

SUSPENSION COMPONENTS DIVISION

PRECISION SPRINGS TRUCKS CARS

€ m

1Q 2014 1Q 2015

• 10% Increase in revenues due to higher volumes in all

geographical areas and partly (ca. 4%) to exchange rates

impact

• Revenues grew by 7.7% in Europe, by 15.1% in North

America, by 39.7% in Asia; slight increase also in South

America (+3.3%)

• EBITDA before-restructuring was € 35.2 million (+10.7%

vs. € 31.8 million in 1Q 2014)

• EBITDA and net income benefited from higher revenues

and lower restructuring costs (€ 0.4 million restructuring

costs in 1Q2015 vs. € 11.3 million in 1Q2014)

• In 2015 Sogefi expects continuing positive trends in North

America, China and India, slightly better performance in

Europe and a likely persisting weak environment in South

America

1Q 2015 Performance and outlook

FORD

RENAULT/NISSAN

PSA

FCA/CNH Industrial

GM

DAIMLER

VOLKSWAGEN/AUDI

BMW

VOLVO TOYOTA

DAF/Paccar

2014 Revenues breakdown

MAN

CATERPILLAR

HONDA

OTHERS

12.5% 12.3%

10.6%

11.4%

8.3% 7.4%

3.5%

2.9%

2.2%

2.1% 1.6% 1.3% 0.5% 0.5% 22.9%

64.6%

15.4%

Europe

NAFTA

Mercosur 13.5%

6.1% 0.4%

Weight of non-

European

markets is stable

35.4%

Countries Customers

Asia others

15

KOS - overview

€ m 2011 2012

Revenues 95.5 106.8

Net income 2.5 3.7

EBITDA 12.4 15.3

Key financials

SHAREHOLDERS

HOSPITAL

MANAGEMENT NURSING HOMES REHABILITATION

CIR (51.3%)

ARDIAN (46.7%)

Management and others (2.0%)

Operating structure

1Q 2014 1Q 2015

5.2

2.3

5.7

10.2

36.6

114.3 7.6 23.5

45.4

107.1

18.8

Revenues breakdown by region (2014)

4.5

• Increase in revenues (+11.8%), thanks to relevant acquisitions

in the nursing home/rehabilitation area and to organic growth

across all businesses lines.

• Contributions to EBITDA increase were:

- €1.1 million from revenue growth and efficiency

improvement, at constant 2013 perimeter

- €1.8 million from acquisitions and greenfields of 2014/1Q

2015

• Diagnostic and therapeutic technology operations and

development are continuing in India, as well as in the UK

• The company now has 75 nursing homes in the centre and

north of Italy with more than 7,100 beds, plus ca. 200 under

construction

• Main objectives are to pursue market consolidation in core

businesses and to selectively expand internationally, with a

primary focus on India

1Q 2015 Performance and outlook

16

• Education

- CIR has an interest of 17.4% in SEG (Swiss Education Group), a world

leader in education for hospitality management (hotels, restaurants, etc.).

The book value of the investment at March 31, 2015 was €21.1 million

• Private equity

- Diversified portfolio of private equity funds and direct minority private equity

investments, with a fair value of € 72.8 million at March 31, 2015. The

portfolio is reaching its maturity phase as limited investments were added in

the recent past

• NPL

- At the end of March 2015 the net value of CIR investment in the non-

performing loan portfolios amounted to €49.2 million.

- CIR no longer owns operating companies in this industry and is currently in

the process of collecting the existing receivables, with no further investments

Non-core investments

17

• This document has been prepared by CIR for information purposes only and for use

in presentations of the Group’s results and strategies.

• For further details on CIR and its Group, reference should be made to publicly

available information, including the Annual Report, the Semi-Annual and Quarterly

Reports

• Statements contained in this document, particularly the ones regarding any CIR

Group possible or assumed future performance, are or may be forward looking

statements and in this respect they involve some risks and uncertainties

• Any reference to past performance of CIR Group shall not be taken as an indication

of future performance

• This document does not constitute an offer or invitation to purchase or subscribe for

any shares and no part of it shall form the basis of or be relied upon in connection

with any contract or commitment whatsoever

Disclaimer

18

www.cirgroup.com