4 q15 earnings presentation

TRANSCRIPT

Fourth Quarter 2015 Earnings Conference Call

February 18, 2016

This presentation contains forward-looking statements, including our belief in the

benefits to be achieved from the business unit realignment, expectations for

annualized cost savings achieved from our cost optimization program and resulting

restructuring charges, expectations for revenue, adjusted EBITDA and capital

expenditures in 2016 and our ability to further improve margin profile and generate

positive levered free cash flow for the full-year 2016. Because such statements are not

guarantees of future performance and involve risks and uncertainties, there are

important factors that could cause Internap's actual results to differ materially from

those in the forward-looking statements. These include statements related to our

expectations regarding performance of our IT infrastructure services and the benefits

we expect our customers to receive from them, customer adoption rates of our

performance-based product offerings, our ability to execute our strategy, deliver growth

and generate cash, our ability to correctly forecast anticipated cost savings and

restructuring charges, our ability to leverage data center expansions and continue to

build positive operating leverage in the business model, our ability to sell into available

data center capacity, our ability to renegotiate key IP transit contracts on favorable

terms and our ability to increase our utilization of our data center space. Internap

discusses these factors in its filings with the Securities and Exchange Commission.

Given these risks and uncertainties, investors should not place undue reliance on

forward-looking statements as a prediction of future results. Internap undertakes no

obligation to update, amend, or clarify any forward-looking statement for any reason. 2

Forward-looking Statements

• In 2015, the Board of Directors created a Strategy Committee of independent

directors

• Hired Morgan Stanley and Greenberg Traurig to assist in evaluation of strategic

alternatives

• Internap contacted a wide range of financial and strategic parties

• Internap received several preliminary, non-binding indications of interest with respect

to a potential acquisition of the Company

• Due to a variety of factors, including the inability to obtain financing and volatility in

the credit markets, no agreement was reached

• The Board remains open to all alternatives that would maximize shareholder value

• Having conducted a thorough review, the Board has determined that accelerating

Internap’s business unit realignment best positions the Company for value creation

as a standalone entity and also best facilitates the possibility of other value creating

combinations

Strategic Review Process Summary

Strategic Review

3

• Accelerate transition into two integrated business units: Data Center and Network

Services and Cloud and Hosting Services

• The business unit realignment will facilitate more effective and efficient business

operations, improve customer and product focus and increase long-term

shareholder value

• Cost optimization program expected to result in approximately $4 million - $5

million of annualized cost savings beginning in 2Q16

• Savings will be generated primarily by optimizing the Company’s cost structure

during the business realignment, as well as reduced discretionary spending and

marketing program efficiencies

• Record a one-time, below the line, restructuring charge of approximately $2.5

million - $3.0 million

Business Realignment and Associated

Cost Optimization Initiative

Strategic Review

4

5

Business Alignment

2Q13Percentages not to scale.

Data Center

and

Network

Services

67%

Company-

Controlled Colo

28%~55%-60%

IP Services

26%

~55%-60%

Service

Partner Colo

13%~25%-30%

Cloud and

Hosting

Services

33%

Bare-Metal Cloud

11% ~70%

Dedicated Hosting

20%~70%

Other

2%~ 80%

Services/% Total Pro Forma Revenue

• Market growth rate 8%-10%

• Regional and global competitors (Colo/REIT’s)

• Differentiate on power dense platform

• Market growth rate (2)%-(5)%

• Price declines partially offset by traffic growth

• Global carrier competitors

• Patented technology enables and differentiates colo

and cloud/hosting services

• Customer convenience play

• Geographic reach and “fill in”

• Market growth rate 20%-25%

• Differentiate on superior price/performance value

proposition for high performance applications

• Bare metal and virtual cloud provider competitors

• Custom hosting represents 40%

• Market growth rate 10%-15%

• Dedicated servers represents 60%

• Market growth rate 5%-6%

• Managed services and compliance value proposition

• Hosting provider competitors

• Software and shared hosting

GM % Market Dynamic/Competitive Positioning

• Consolidated revenue of $78.8M increased 1% Q/Q and decreased 7% Y/Y

• Core data center services revenue of $49.1M increased 1% Q/Q and decreased 1% Y/Y

• Segment profit of $47.3M increased 6% Q/Q and decreased 3% Y/Y

• Segment margin of 60.1% expanded 310 bps Q/Q and 220 bps Y/Y

• Adjusted EBITDA of $22.8M increased 15% Q/Q and flat Y/Y

• Adjusted EBITDA margin of 29.0% expanded 380 bps Q/Q and 200 bps Y/Y

• Levered free cash flow of $1.4 million (second consecutive positive quarter)

Record Financial Results

4Q15 Highlights

6

Core data center services defined as company-controlled colocation, hosting and cloud services.

Segment profit, segment margin, adjusted EBITDA, adjusted EBITDA margin and levered free cash flow are non-GAAP measures. Segment profit is segment revenues less

direct costs of network, sales and services, exclusive of depreciation and amortization. Segment profit does not include direct costs of customer support, direct costs of

amortization of acquired technologies or any other depreciation or amortization associated with direct costs. Segment margin is segment profit as a percentage of segment

revenues. Adjusted EBITDA is loss from operations plus depreciation and amortization, (loss) gain on disposals of property and equipment, exit activities, restructuring and

impairments, stock-based compensation, acquisition costs and strategic alternatives and related costs. Adjusted EBITDA margin is adjusted EBITDA as a percentage of

revenues. Levered free cash flow is adjusted EBITDA less capital expenditures, net of equipment sale-leaseback transactions and cash paid for interest. A presentation of

segment profit and segment margin and a reconciliation of adjusted EBITDA to GAAP loss from operations and levered free cash flow can be found in the attachment to our

fourth quarter 2015 earnings press release, which is available on our website and furnished to the Securities and Exchange Commission.

.

Financial Summary: Revenue

Revenue

7$ in millions.

• Consolidated revenue increased 1% Q/Q and decreased 7% Y/Y

• Data center services revenue increased 1% Q/Q and decreased 4% Y/Y

• Strategic mix shift to data center services 75% of consolidated revenue

• IP services revenue flat Q/Q and decreased 14% Y/Y

• Churn mitigation program yielding positive results

Data Center Services Drive Sequential Top Line Growth

Revenue Churn

Data Center Churn 1.8% 1.7% 3.0% 2.3% 2.1% 2.4% 2.1% 1.6%

IP Revenue Churn 1.2% 1.2% 1.8% 1.4% 1.9% 1.8% 1.6% 1.7%

Total Revenue Churn 1.6% 1.6% 2.7% 2.0% 2.1% 2.3% 2.0% 1.6%

71% 73% 73% 73% 73% 74% 75% 75%

29% 27% 27% 27% 27% 26% 25% 25%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

IP ServicesData Center Services

$84.1 $84.7 $84.3 $80.8 $80.4 $78.3 $78.8$82.0

8

Strategic Mix Shift Engine for Growth

Favorable Revenue Mix

Profitable Growth

$ in millions. Core data center services defined as company-controlled colocation, hosting and cloud services. Legacy revenue defined as IP services and partner colocation data

center services. CAGR is compound annual growth rate.

• 15% 3-year adj. EBITDA CAGR

• Adjusted EBITDA margin expanded

750 basis points over the same time-

frame

Solid Adj. EBITDA Growth and

Margin Expansion

• Core increased 1% Q/Q and

decreased 1% Y/Y

• Core revenue represents 83% of data

center services revenue and 62% of

consolidated revenue

• 17% 3-year revenue CAGR

Core Data Center Services

Resume Sequential Growth

$39.4

$29.7 $30.4

$49.1

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

Core Legacy

$15.0

$22.8

21.5%

29.0%

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

Adj. EBITDA Margin

Data Center Services Segment Profit and

Segment Margin

9

Data Center Services Segment Profit

• Data center segment profit increased 5% Q/Q and flat Y/Y

• Data center segment margin expanded 270 basis points Q/Q and 230 basis points Y/Y

• Core segment profit increased 5% Q/Q and 2% Y/Y

• Core segment margin expanded 220 basis points Q/Q and 240 basis points Y/Y

Core Data Center Services Engine for Long-Term Profitable Growth

$ in millions.

$32.4 $34.8 $33.9 $35.3 $34.9 $35.1

$33.5 $35.3

55.6%56.7%

55.0%

57.6%58.9% 59.0%

57.2%

59.9%63.4%

64.8%62.3%

64.2%65.6% 66.4% 64.4%

66.6%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Partner Colo Segment Profit Core Segment Profit

DC Segment Margin % Core Segment Margin %

IP Services Segment Profit and Segment Margin

10

IP Services Segment Profit

Solid Profitability and Cash Generation

$ in millions.

• IP segment profit increased 8% Q/Q and decreased 11% Y/Y

• IP segment margin expanded 420 basis points Q/Q and 200 basis points Y/Y

• Enabler for high-performance, hybrid Internet infrastructure service offerings

$13.8 $12.7

$13.6 $13.5 $12.6

$12.4 $11.1

$12.0

58.3%

55.9%

59.0%58.7%

58.1%58.9%

56.5%

60.7%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Segment Margin %

11

Record High Adjusted EBITDA and Adjusted EBITDA Margin

Adjusted EBITDA

$ in millions.

• Adjusted EBITDA increased 15% Q/Q and flat Y/Y

• Adjusted EBITDA margin expanded 380 bps Q/Q and 200 bps Y/Y

• Positive results reflect impact of favorable product mix shift

• Tight operational controls and positive operating leverage support margin expansion

Record Adjusted EBITDA Results

$17.8 $18.5 $19.7

$22.7

$17.9 $19.1 $19.8

$22.8

21.7% 22.0%23.3%

27.0%

22.2%

23.8%

25.2%

29.0%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Adj. EBITDA Margin

Financial Review: Cash Flow and Balance Sheet

12

Levered Free Cash Flow

4Q15 3Q15 4Q14

Cash & Cash Equivalents $17.8 $18.3 $20.1

Less: Debt (net of discount) 318.5 318.8 299.0

Less: Capital Leases 57.1 57.5 60.1

Equals: Net Debt $(357.8) $(358.0) $(339.0)

Net Debt to Adj. EBITDA (LQA)* 3.9x 4.5x 4.7x

Balance Sheet Summary

$ in millions * LQA = Last Quarter Annualized.

$(13.5)

$(0.7) $(0.2)

$(9.2)$(4.2)

$(3.3)

$2.2 $1.4

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Adj. EBITDA $17.8 $18.5 $19.7 $22.7 $17.9 $19.1 $19.8 $22.8

Less: Capex $(25.5) $(13.1) $(13.7) $(25.1) $(15.7) $(15.8) $(10.9) $(14.7)

Less: Cash Interest Exp. $(5.8) $(6.1) $(6.2) $(6.8) $(6.4) $(6.6) $(6.7) $(6.7)

Equals: Levered FCF $(13.5) $(0.7) $(0.2) $(9.2) $(4.2) $(3.3) $2.2 $1.4

$(40.0)

$(30.0)

$(20.0)

$(10.0)

$-

$10.0

$20.0

$30.0

2016 Financial Guidance

13

Revenue

Adjusted EBITDA

$310 - $320

$80 - $90

Range

(in millions)

Financial guidance constitutes forward-looking statements which involve risks and uncertainties. Please refer to slide 2 for more information

regarding forward-looking statements.

Capital Expenditures

Growth

Maintenance

$40 - $50

$30 - $35

$10 - $15

14

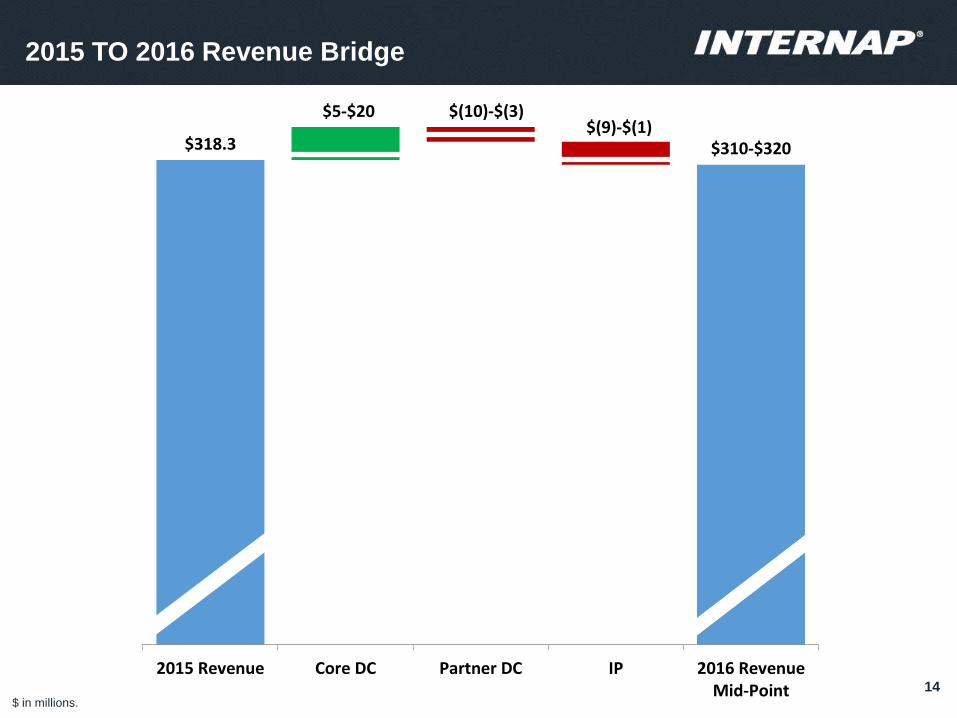

2015 TO 2016 Revenue Bridge

2Q13$ in millions.

$318.3 $310-$320

$5-$20 $(10)-$(3)$(9)-$(1)

2015 Revenue Core DC Partner DC IP 2016 RevenueMid-Point

15

2015 TO 2016 Adjusted EBITDA Bridge

2Q13$ in millions.

$79.6

$80-$90

$2-$7 $(7)-$(2) $1-$3 $1-$3

$3-$6

2015 Adj. EBITDA GrowthInitiatives

Churn MIRO C COGS Savings Opex Benefits 2016 Adj. EBITDAMid-Point

Product

MarketExecution

Building a Great Company

16

1. Salesforce productivity initiatives

Bookings increased sequentially during 4Q15

2. Proactive churn mitigation and account management

Total churn rate the lowest level in 6 quarters

3. Targeted data center utilization

Largest quarterly leasing increase in Dallas data center since facility opening

4. Channel programs – sales force multiplier

Positive momentum with second-half 2015 channel bookings up significantly from first-half

2015

5. Lead generation and targeted marketing initiatives

Marketing sourced new logos MRR accelerate considerably over the previous 2 quarters

6. New/enhanced product and service offerings

Gaining traction for Managed Internet Routing Optimizer (MIRO) Controller with $0.5M in sales

in 4Q15

Focus on Growth

17

Growth Initiatives Yielding Positive Results

Results:

• Record results for 4Q15 and FY 2015

– Highest quarterly and annual levels of adjusted EBITDA, adjusted EBITDA margin and

segment margin

• Adjusted EBITDA increased 15% and adjusted EBITDA margin expanded 380 bps Q/Q

• Second consecutive quarter of positive levered free cash flow

Looking Forward:

• Business unit realignment designed to facilitate more effective and efficient business

operations, to improve customer and product focus and increase long-term

shareholder value

• Cost optimization program expected to result in approximately $4 million - $5 million

of annualized cost savings beginning in 2Q16, primarily a result of optimizing cost

structure around the business unit realignment

• Further improve margin profile

• Expect to generate positive levered free cash flow for the full-year 2016

Improved Operational and Financial Results

4Q15 Summary

18