2006:217 civ master's thesis1028633/fulltext01.pdf · as the world’s largest automation...

TRANSCRIPT

2006:217 CIV

M A S T E R ' S T H E S I S

Cutting Logistics Costs with a CentralizedDistribution Model for ABB’s Distribution

of LV Products in Asia Pacific

Anna Fröderberg

Luleå University of Technology

MSc Programmes in Engineering Industrial Business Administration

Department of Business Administration and Social SciencesDivision of Industrial Logistics

2006:217 CIV - ISSN: 1402-1617 - ISRN: LTU-EX--06/217--SE

Preface

PREFACE This master’s thesis has been written during the fall of 2005 as a final part of my university degree MSc in Industrial Management and Engineering, Lulea University of Technology, division of Industrial Logistics. The thesis has been conducted at ABB’s Logistics Centre Asia Pacific, located in Singapore. Fulfilling this study was made possible thanks to the support from a range of people that I would like to thank. I owe the biggest thanks to my supervisors at ABB Singapore, Isabel Chong and Heri Setiabudi. Their guidance and knowledge about logistics have helped me many times during the study. I would also like to thank Isabel for giving me the opportunity to write my thesis at the Logistics Centre. I am grateful for the experience of working in Singapore and the chance to expand my knowledge about logistics. I would also like to thank my supervisor Anders Sörqvist at Lulea University of Technology who has assisted me with his practical knowledge. Anna Ivarsson, your comments about my report have been utmost helpful. Finally, I would like to give my appreciation to all the people I have meet in Singapore that has made my stay here such a memorable time. It has been an interesting period here at ABB Singapore and I have had the opportunity to apply my education on an important issue in the industry. I am very pleased with the result and it is my hope that this report will contribute to an improved logistics performance at ABB. Singapore, December 2005. Anna Fröderberg

Abstract

ABSTRACT As the world’s largest automation supplier, ABB has built a value chain geared to the singular goal of achieving results for the customer. Every day ABB ships more than 1,000,000 automation products. Hence, logistics plays an important part for ABB to gain a substantial competitive edge in the global market place. The company must be able to deliver their products at shortest time possible to meet customer demands. If ABB wants to increase their market share and enhance its performance they must determine their competitive priorities. Both pricing and availability of the products are closely linked with the distribution channel. If the distribution channel is efficient then the products will be available in right quantities at the right time to customers. If the distribution channel is also cost efficient then the price of the products can be lowered. The objective of this study is to understand how the different logistics costs affect ABB’s distribution model and to find the most optimum model to support the Asia Pacific region in order to prevent a sub optimization. Today ABB have a decentralized distribution and the sales units keep their own stock to support local requirements. The total logistics costs constitute of 17.5 percent of the transfer price. A centralized distribution model will create a saving of X MUSD and lower the total logistics cost to 12.6 percent of the transfer price. In order to fulfil the purpose the author has done a broad literature review about distribution and cost models. The evaluation of today’s distribution model is based on information from a survey sent to concerned production and sales units during October 2005. The simulations for the regional distribution centre are based on parameters from the situation today. The conclusion of the thesis is that ABB will benefit from a centralized distribution model. Using a model with a regional distribution centre will not just save costs, it will also increase the service level by providing the customers with higher product availability. However, local stocking have its benefits since ABB will be close to customer location and can, if the right products are available, offer a faster delivery than a regional distribution centre. The disadvantage with a longer lead time can be avoided by using investing in new IT infrastructure or use existing technologies for order handling and use direct distribution to large end customers.

Sammanfattning

SAMMANFATTNING ABB är världens största leverantör av automationsprodukter och företaget skickar dagligen över 1,000,000 produkter. Det gör att logistiken spelar en avgörande roll för att nå konkurrensfördelar på marknaden. ABB måste kunna leverera sina produkter med korta ledtider för att möta kundernas krav. Konkurrensfördelar som är relaterade till distributionsmodellen är priset på produkten och produktillgängligheten. Om distributionsmodellen är effektiv kommer rätt produkter att vara på rätt plats enligt kunderna önskemål. Om distributionen också är kostnadseffektiv kan även priset på produkten sänkas. Syftet med denna studie är att förstå hur de olika logistikkostnaderna påverkar ABBs distributionsmodell och att finna den mest optimala modellen för att försörja Asia Pacific regionen. Idag har ABB en decentraliserad distributionsmodell med en total logistikkostnad på 17.5 procent i relation till transfer priset. En centraliserad distributionsmodell kommer att generera en besparing på X MUSD och sänka den totala logistikkostnaden till 12.6 procent av transfer priset. För att uppnå syftet har författaren genomfört en litteraturstudie inom ämnet distributions- och kostnadsmodeller. Utvärderingen av dagens distributionsmodell är baserad på information från en enkät skickad till berörda fabriker och säljbolag under oktober 2005. Simuleringarna för det regionala distributionscentret är baserat på parametrar från dagens situation. Slutsatsen är att ABB borde centralisera sin distributionsmodell. Att ha ett regionalt distributionscenter kommer inte bara att sänka kostnaden, det kommer också att öka servicenivån genom en högre produkttillgänglighet. Dock kommer ABB att vara närmare sina kunder om de har kvar lagren hos säljbolagen och de kan, om rätt produkter är tillgängliga, erbjuda en snabbare ledtid än regionalt distributionscenter. Nackdelen med utökad ledtid kan hanteras genom att investera in ny IT infrastruktur för orderhantering samt genom direkt distribution till kunderna.

Abbreviations

ABBREVIATIONS ATAP Automation Technology Automation Products AS-IS AS the situation IS today BA Business Area BU Business Unit DDU Delivered Duty Unpaid KPI Key Performance Indicator LCA Logistics Centre Asia LV products Low voltage products PU Production Unit RDC Regional distribution centre SU Sales unit SECRL ABB Cewe-Control, Västerås, Sweden ITSCE ABB Sace, Bergamo, Italy NOCRL ABB Control, Skien, Norway FRENT ABB Entrelec, Chassieu, France DEBJE Busch-Jager, Lüdenscheid, Germany DESTO ABB Stotz, Heidleberg, Germany FICON ABB OY, Vaasa, Finland

Table of Contents

1 INTRODUCTION .......................................................................................................................... 1

1.1 PROBLEM BACKGROUND .......................................................................................................... 1 1.2 PROBLEM DEFINITION............................................................................................................... 1 1.3 SPECIFYING THE PURPOSE ....................................................................................................... 2 1.4 EXCLUSIONS............................................................................................................................ 2 1.5 READING DIRECTIVES............................................................................................................... 3

2 RESEARCH METHODOLGY....................................................................................................... 4

2.1 RESEARCH ALIGNMENT............................................................................................................ 4 2.2 RESEARCH APPROACH............................................................................................................. 4 2.3 DATA COLLECTION METHODS................................................................................................... 4 2.4 VALIDITY AND RELIABILITY........................................................................................................ 5 2.5 COURSE OF ACTION................................................................................................................. 6

3 ABB FACTS................................................................................................................................. 8

3.1 ABB GROUP ........................................................................................................................... 8 3.1.1 Brief history .................................................................................................................... 8 3.1.2 ABB today ...................................................................................................................... 8

3.2 AUTOMATION PRODUCTS ......................................................................................................... 9 3.3 ABB SINGAPORE ................................................................................................................... 10

3.3.1 Logistic Centre Asia..................................................................................................... 10 3.4 LOW VOLTAGE PRODUCTS ..................................................................................................... 11

4 THEORETICAL FRAME OF REFERENCE............................................................................... 12

4.1 THE TOTAL COST CONCEPT ................................................................................................... 12 4.1.1 The Total Cost Model................................................................................................... 12

4.2 CUSTOMER SERVICE.............................................................................................................. 12 4.2.1 Availability .................................................................................................................... 13 4.2.2 Order cycle................................................................................................................... 14 4.3.2 Communication ............................................................................................................ 14

4.3 DISTRIBUTION ACTIVITIES AND COSTS .................................................................................... 14 4.3.1 Warehousing................................................................................................................ 14 4.3.2 Inventories ................................................................................................................... 14 4.3.3 Transport...................................................................................................................... 16 4.3.4 Order Processing ......................................................................................................... 17 4.3.5 Lot Quantity Costs ....................................................................................................... 18

4.4 DISTRIBUTION........................................................................................................................ 18 4.4.1 Intermediaries .............................................................................................................. 18 4.4.2 Centralized Distribution................................................................................................ 19 4.4.3 Product Characteristics................................................................................................ 20

4.5 MEASURING LOGISTICS.......................................................................................................... 21 4.5.1 Measuring distribution models ..................................................................................... 22

5 RESULTS FROM EMPIRICAL RESEARCH ............................................................................. 23

5.1 THE SALES ORGANISATION ..................................................................................................... 23 5.1.1 LV Products ................................................................................................................. 24 5.1.2 Customer Service ........................................................................................................ 25 5.1.3 Warehouse................................................................................................................... 25 5.1.4 Inventories ................................................................................................................... 25 5.1.5 Transport...................................................................................................................... 26 5.1.6 Order handling ............................................................................................................. 27 5.1.7 Measuring Logistics ..................................................................................................... 28

5.2 TOTAL COST MODEL.............................................................................................................. 28 5.2.1 Flows............................................................................................................................ 29

Table of Contents

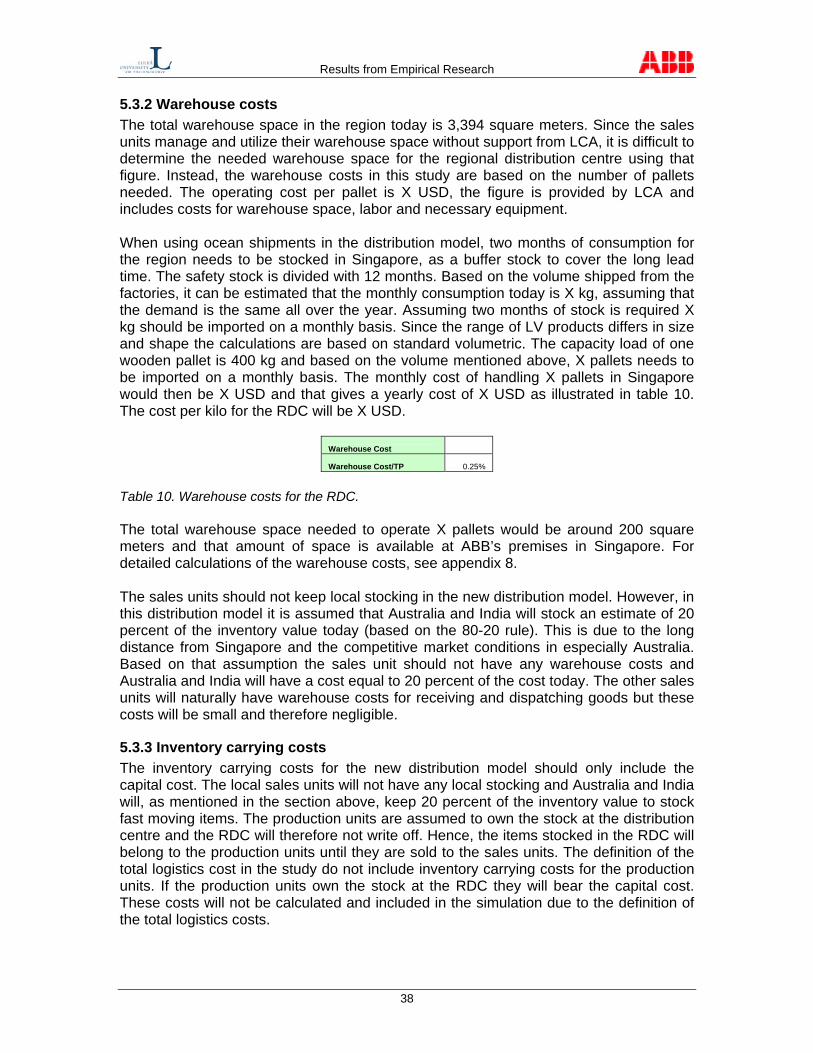

5.2.2 Warehouse Costs ........................................................................................................ 30 5.2.3 Inventory Carrying Costs ............................................................................................. 31 5.2.4 Transportation Costs.................................................................................................... 32 5.2.5 Order handling Costs................................................................................................... 33 5.2.6 Lot quantity Costs ........................................................................................................ 34 5.2.7 Performance measurement ......................................................................................... 34 5.2.8 Total Logistics Costs.................................................................................................... 36

5.3 REGIONAL DISTRIBUTION CENTRE .......................................................................................... 37 5.3.1 Flows............................................................................................................................ 37 5.3.2 Warehouse costs ......................................................................................................... 38 5.3.3 Inventory carrying costs............................................................................................... 38 5.3.4 Transportation costs .................................................................................................... 39 5.3.5 Order processing cost.................................................................................................. 40 5.3.6 Lot quantity costs ......................................................................................................... 41 5.3.7 Performance ................................................................................................................ 41 5.3.8 Total logistics costs...................................................................................................... 41

6 ANALYSIS.................................................................................................................................. 43

6.1 WAREHOUSE COSTS.............................................................................................................. 43 6.2 INVENTORY CARRYING COSTS................................................................................................ 44 6.3 TRANSPORTATION COSTS ...................................................................................................... 46 6.4 ORDER HANDLING COSTS ...................................................................................................... 47 6.5 LOT QUANTITY COSTS ........................................................................................................... 48 6.6 PERFORMANCE...................................................................................................................... 49 6.7 REGIONAL DISTRIBUTION CENTRE .......................................................................................... 51

7 CONCLUSIONS ......................................................................................................................... 52

7.1 TOTAL LOGISTICS COSTS ....................................................................................................... 52 7.2 RECOMMENDATIONS .............................................................................................................. 53 7.3 CRITICAL VIEWPOINT ............................................................................................................. 55

REFERENCES .............................................................................................................................. 57 APPENDIX 1 – LOCATION OF SALES UNITS/PRODUCTION UNITS APPENDIX 2 – SURVEY TO SALES UNITS APPENDIX 3 – SURVEY TO PRODUCTION UNITS APPENDIX 4 – TRANSPORTATION COSTS, AS-IS APPENDIX 5 – TOTAL CYCLE TIME, AS-IS APPENDIX 6 – ON TIME DELIVERY, AS-IS APPENDIX 7 – TOTAL LOGISTICS COSTS, AS-IS APPENDIX 8 – WAREHOUSE COSTS AND ICC, RDC APPENDIX 9 – IMPORT COSTS, RDC APPENDIX 10 – EXPORT COSTS, RDC APPENDIX 11 – ORDER HANDLING COSTS, RDC APPENDIX 12 – TOTAL LOGISTICS COSTS, RDC

Introduction

1

1 INTRODUCTION This chapter will introduce the reader to the subject of distribution models and present reasons for ABB Singapore’s need to investigate if a centralized distribution model would be to prefer. This discussion leads to the purpose of the thesis and the exclusions. Finally the structure of the thesis is presented.

1.1 Problem background The need for having goods physically moved between the place where they are produced and the places where they are consumed, have rapidly increased during the last decade. The exchange process has become a cornerstone of economic activity, and channels of distribution develop when many exchanges take place between producers and consumers. (Lambert el al, 1999) The scope and role of logistics have changed over the years and more recently logistics has become more prominent and is recognised as a critical factor of competitive advantage, instead of having a supportive role to functional areas as marketing and production. The growing importance of logistics arises from companies going global to access new markets. (Sum et al, 2001) In today’s market, with rising oil prices, it has become important to continuously review the company’s logistics performance. A major concern for companies is to which extent a channel of distribution creates an efficient flow of products from producer to consumers. The manufacture’s objective is to obtain optimum performance of the vital functions in the channel of distribution; warehousing, transportation and physical handling. (Lambert et al, 1999) Due to the dynamic nature of business environment, companies must frequently evaluate and monitor the performance of their distributions channels. When performance goals are not met, other possible channel alternatives must be evaluated and changes must be implemented. Lambert et al (1999) claims that distribution channels are recognized as one of the least managed areas in companies.

1.2 Problem definition Suppose a customer is going to build an industrial project that needs a 24/7 support and continuity to avoid a plant down situation. The customer will try to estimate the cost of buying such a product, the reliability of the product and the availability of after sales support. In today’s environment it is no longer enough to evaluate the cost merely based on buying the quality product at the lowest cost. To ensure the running of the business there are far more to take in account, including faster delivery times and the availability of the products from the supplier. As the world’s largest automation supplier, ABB has built a value chain geared to the singular goal of achieving results for the customer. Every day more than 1,000,000 automation products are shipped meeting customers need for motion, measurement, power, protection control and optimization. Logistics plays an important part for ABB to gain a substantial competitive edge in the global market place. The company have to be close to customer location wherever it may be to give the assurance to the customer that they will always be there for them. If a customer is in need of their support ABB wants to be sure they can deliver the products at shortest time possible to meet their demands. ABB’s objective is to increase market shares in Asia Pacific and that can among others

Introduction

2

be achieved by improved logistics performance. To reach these objectives ABB has to focus on developing an efficient value chain, hence the importance of the distribution model in Asia Pacific. In today’s competitive market ABB also need to focus on stable service levels in order to keep their position and to expand. ABB have sales units in 12 countries in Asia Pacific and they keep their own stock to support the local requirements. The sales units are required to keep minimum stock of various products in the warehouses in order to lower the costs. But due to the request of short delivery times, long lead times from the manufacturers and the level of competitiveness of similar products available in the market, the sales units are struggling with their inventory levels. Every product that is stocked is at risk at becoming obsolete. When large quantities are stocked there is an increased risk for the material becoming of no use. Cost for shortage and delays occur when products can not be delivered to customer. Besides the actual cost of not being able to deliver, failing to maintain a stable service level can have the impact of loosing a customer. Thus, poor delivery performance implies that both existing and future customers are lost. Since ABB wants to expand its market share in Asia Pacific it is important that they always are able to deliver their products according to customer requirement. A decentralized distribution model, like the one ABB is having in Asia Pacific, can lead to increased cost and less efficiency performance of the sales units. One way to cut logistic costs and improve delivery performance can be to use a regional distribution centre. A centralized distribution model can lead to better delivery performance, better customer service and less inventory carrying and transportation cost. (Lambert et al, 1999) At this point ABB has not done a thorough evaluation of the costs and performance of the distribution model. Since ABB lacks a holistic view over the costs and performance, a study to investigate the current distribution model is needed.

1.3 Specifying the purpose The objective of this study is to understand how the different logistics costs affect ABB’s distribution model and to find the most optimum model to support the Asia Pacific region, in order to prevent a sub optimization. The study will give ABB a recommendation how the company should move forward and enhance its performance regarding their distribution model. The objective can be summarized in two major points

• To conduct a study for the current distribution model • To conduct a feasibility study to see if converting the decentralized model to a

centralized model with the needs of a regional distribution centre would be to prefer

The regional distribution centre will hereafter be referred to as RDC.

1.4 Exclusions The scope of the study will be limited to Low voltage products. The area of LV products covers four of Automation Technologies Automation Products (ATAP) business units.

Introduction

3

This study will include the distribution costs/performance from seven incoming factories sited in Europe to the costs/performance at seven sales units in Asia Pacific. For location of factories and sales units, see appendix 1. The sales units in Korea and Japan were formed in 2004 and are excluded from the study due to lack of data. The sales unit in New Zealand was formed in 2003 and sat up its local stock in 2004 and is excluded since the figures would be misleading. The sales units in China and Hong Kong are also excluded from this study due to the volume and growth of their business. Vietnam and Indonesia will become sales units in 2006. The definition for the total logistics costs in this study is illustrated in figure 1. As shown in the figure the inventory carrying cost and warehouse cost for the producers are excluded in this study. They are excluded since they are assumed not to differ significantly with a centralized distribution model and since the accurate cost for LV products shipped to Asia Pacific are difficult to obtain from the producers.

Figure 1. Exclusions.

1.5 Reading directives The structure of the report is to some extent similar to the authors work procedure. The disposition of the master’s thesis can be divided into three main parts, presented in figure 2.

Figure 2. The disposition of the report. The first three chapters of the report are connected since they provide the reader with the background of the problem, company and the course of action. The first part of the thesis is the base of the report. The second part of the thesis is the main part and includes the theoretical frame of reference, results from the empirical research and the analysis. All chapters in the thesis leads to the third part, conclusion. In the last chapter the reader will be provided with recommendations on how ABB should proceed to enhance its distribution model. All figures stated in this report is from full year 2004, if not otherwise is stated. All costs are expressed in USD. This report is printed in two versions, one official and one confidential. Figures and information of confidential nature will be replaced by an X in the official version.

Introduction

Method Company Info

Conclusion

Theory Empirical research

Analysis

1 2 3

PU

Warehouse/ICC

LABB

Warehouse/ICC Transportation Transportation

Research Methodology

4

2 RESEARCH METHODOLGY To ensure a high quality study, well-established and scientific methods have been used by the author. This chapter aims at giving the reader an understanding of the methods that have been applied and the course of action.

2.1 Research Alignment According to Lekvall & Wahlbin (2001) the alignment of a research must be adapted to the aim of the purpose. The purpose of a research can be classified into two directions; explanatory and descriptive. When using the explanatory approach the author studies a problem in order to explain the relationship between variables. In a descriptive study the researcher does not draw conclusions from the collected data, but only describes the material. The difference between an explanatory and descriptive study can be subtle, a descriptive study must to some extent provide explanation and vice versa. The purpose of this thesis is to conduct a study for the current distribution model and to conduct a feasibility study to see if converting the decentralised model to a centralised model would be to prefer. In order to fulfil this purpose logistics costs must be analyzed and distributed among the sales companies. This method requires detailed information regarding the cost drivers and underlying factors. In order to investigate the different logistics costs the author searched for relationship between different parameters affected by creating a distribution centre. The author also drew conclusions from the evaluation of the result of the sales companies. Therefore, both explanatory and descriptive alignment will be used jointly in this thesis.

2.2 Research Approach There are two ways, with several differences, of research approaches; quantitative and qualitative. The approach should be determined with regard to the purpose of the study. (Lekvall & Whalbin, 2001). In a qualitative approach the researcher collects, analyse and interpret data that is soft; i. e. can not easily be quantified and expressed in numbers. The researcher present plain text, in an order, that provides meaning of the studied problem. Quantitative data is expressed in terms of numbers and figures that are analyzed with mathematical and/or statistical methods. According to Lekvall & Whalbin (2001) most studies tend to be of qualitative nature, but exceptions exist. To fulfil the purpose of this study both qualitative and quantitative have been used. The result of the cost evaluation has a quantitative approach and is presented in hard data, numbers and figures, while qualitative studies was conducted to analyse the costs. A qualitative study was also necessary to understand how the different cost drivers are linked. Understanding how soft aspect like customer service will be affected also required a qualitative approach. This implies that the study has a quantitative approach with qualitative features.

2.3 Data Collection Methods When performing a study like this thesis, amounts of data can be collected. In order to screen the data it is important to distinguish between essential and non-essential data. Data can be collected and categorised in two different ways; primary and secondary data. Primary data consist of data the researcher gathers through observations, surveys

Research Methodology

5

and interviews. Secondary data, on the other hand, consists of data that has been collected in another context; it has been produced by someone else. Secondary data can be found, for example, in books, journals and on internet. It is important that the researcher understands that secondary data is collected with another purpose than the actual research. (Wiedersheim-Paul & Eriksson, 1999) The methods used to gather data should be carefully selected for each individual study. In order to fulfil this study, primary and secondary data are used jointly in this thesis. Primary data has been collected through interviews and surveys with employees at ABB Singapore, the sales units in Asia Pacific and European factories. Secondary data was found in libraries and on ABB’s internal web pages. Source of the information will be from past history data, full year 2004. The literature used in the theoretical frame of references was mainly found on LIBRIS, a national system for searching literature at libraries in Sweden. Articles and journals has been found by searching the databases Emerald and Elite using keywords such as “distribution model”, “logistics” and “performance measurement”.

2.4 Validity and Reliability Validity and reliability are important aspects since analysis based on incorrect data provides false conclusion and will mislead the reader. According to Lekvall & Whalbin (2001) it is important to reflect upon possible errors in the collected data in order to achieve a trustworthy study. Validity is whether the method of measurement actually measures what it is intend to measure. Validity can be divided into internal and external validity. The internal validity is how well the research results correspond to what is being studied. External validity concerns the ability to generalize from the results. (Wiedersheim-Paul & Eriksson, 1999) Reliability concerns whether the method of measurement gives a stabile and reliable result. For example, will the measure yield the same result if it was measured again? The study excludes lot quantity costs but that will affect the result of the model. A centralized distribution model will lower the lot quantity costs since discounts will be given when purchasing larger volumes. If the capital binding for the production units would be included in the study the total saving with a RDC would be less, due to the increased lead time with ocean shipments. The author has not taken into consideration costs for damage and humidity problems during ocean shipments. When closing the sales units’ warehouses they can have difficulties of finding usage of the space, which has not been taken into consideration by the author. Further, the author has not investigated how the procedure for invoicing will affect the model. It is assumed that the information gathered through books and articles is reliable and trustworthy. Data collected from internal web pages is also assumed to be up to date. To assure high validity and reliability regarding primary data, all data need to be defined to make them easy to compare. In order to minimize the errors and assure that the respondents interpreted the questions in the survey equally everyone received the same survey. To assure high validity and reliability the answers from the survey some of the answers have been verified with the help of information from similar surveys. The information given by the respondents have also been verified through telephone conferences.

Research Methodology

6

Respondents at ABB Singapore have also reviewed the report repeatedly during the study to ensure that the author have perceived the information correctly. Interviews and telephone conferences have been booked in advance so the respondent could dedicate time and to avoid stressful situations.

2.5 Course of Action The structure of this report is shaped in a manner that easily will communicate how the purpose is defined, approached and solved. The thesis assignment was to do research, analysis and present the final result in a written report within 20 weeks. Figure 3 outline the authors’ way of conduct.

Figure 3.The authors course of action. The purpose has been defined together with the mentor at Luleå University of Technology respectively ABB Singapore. The author approached the study by dividing the purpose into four phases, see figure 4.

Figure 4. The four phases.

Thorough literature studies have been conducted in order to outline the theoretical frame of references and to understand the first phase. With the theoretical frame of reference

Phase 2

Phase 3

Phase 4

Phase 1

What are the cost elements involved in distributing goods from factories to final consumption?

How is the current distribution model working and how effective is it?

How would a distribution model with a RDC work?

What is the most optimum cost / performance model of distributing goods?

Lite

ratu

re S

tudi

es

Model AS-IS

Model with a RDC

Model AS-IS

Model with a RDC

Qua

litat

ive

Em

piric

al

Res

earc

h Q

uant

ativ

e

Em

piric

al R

esea

rch

Con

clus

ion

Analysis

Writing the report

Research Methodology

7

in mind the author has done the empirical research. The theoretical frame of reference has continuously been used during the study in order to keep a discussion around the problem. Both phase two and three is found in the empirical research. The empirical research is based on input from the literature study, respondents at ABB and the surveys sent to the sales and production units. The second phase, how the current distribution model is working is mainly outlined from respondents at ABB and the survey. In phase three the author conducted a feasibility study for the need of a RDC and she identified the major costs involved to set-up and operate a RDC. The analysis has been conducted with the theoretical frame of reference and empirical research in mind and with consideration of the purpose. In the analysis the current cost structure is being reviewed and compared to the estimated cost of a centralised model. Alongside with reviewing the cost structure the author has also taken in consideration the performance of the distribution models. Finally, a recommendation of which model would be more effective and efficient to support the regional customers needs is given. The recommendation is based on the analysis of the two different distribution models and represents the fourth and final phase of the study. In order to ensemble a critical evaluation of the result the validity and reliability of the authors work is discussed at the end of the report. The author reflects over the study and points out several sources of error that eventually can have affected the result.

ABB Facts

8

3 ABB FACTS This chapter will introduce the reader to the ABB Group and ABB in Singapore. A brief background and explanation of the organisation in which this study is conducted will also be given.

3.1 ABB Group ABB is a leader in power and automation technologies that enable utility and industry customers to improve performances while lowering environmental impacts. The company’s goal is to “create value for all their stakeholders by meeting the needs of theirs customers, employees and the communities where they do business”.

3.1.1 Brief history ABB was formed 1988 as a merge from the Swedish company Asea and the Swiss company Brown Boveri et Cie, BBC. Asea was formed 1980 by a fusion of two Swedish companies and BBC was formed in 1891. In the beginning Asea was focusing on producing generators, transformers and motors while BBC's business idea was to manufacture generators. Until the fusion with Asea, steam turbines were the most important product for BBC. The fusion between Asea and BBC was introduced in 1987 but they didn’t merge until the turn of year 1987. After the merge the company had about 160,000 employees.

3.1.2 ABB today Today ABB operates in over 100 countries and they have about 102,000 employees. The revenues for 2004 were 20,721 MUSD. ABB Ltd shares are traded on the stock exchanges in New York, Stockholm, Frankfurt and London/Zurich. ABB’s head office is located in Zurich. During the time of this study the ABB group was divided into three divisions; automation technologies, power technologies and down stream business. ABB Power Technologies serves electric, gas and water utilities to as well industrial and commercial customers. ABB Automation Technologies delivers solutions for control, motion, protection and plant integration to process and utility industries. ABB Downstream business supplies process technologies and construction services to the oil and gas industries. Every division constitutes of different Business Areas (BA) and every business area consists of different business units (BU), for an organizational chart see figure 5. BU’s shall develop the different parts of the common product range of the BA with special focus on development, investments and production allocations but also on marketing support. The manufacturing facilities are organized under the BU’s. This study is performed under the division Automation Technologies and Business Area Automation Products (ATAP). Business units included in the study are Breakers & Switches, Control Products, Enclosures & DIN Rail Products and Wiring Accessories. The BU Low Voltage System is specialized towards system solutions and provides the whole Low Voltage range and mainly caters to projects.

ABB Facts

9

Figure 5.Organizational chart.

3.2 Automation Products The Business Area Automation Products employees about 27,000 people worldwide and have 110 manufacturing sites in 50 countries. The BA is the market leader in most of its business and during 2003 the sales reached 4.3 billion USD. ATAP serves customers with building blocks to improve plant performance, including motors, drives, instrumentation, low voltage devices and power electronics. Sales of ATAP Products and Systems via local ABB sales companies or channel partners cover over 100 countries of the world. For a figure of the BA’s transformation, see figure 6. ATAP is facing a logistic challenge since more than 1,000,000 products are shipped daily to end customers around the globe. The BA’s mission is to create exceptional growth

• without destroying price structures • with innovation in marketing and products • with strategic acquisitions

Figure 6. The transformation of ATAP over the last four years.

Drives, Motors and Power Electronics

Low Voltage products & Instruments

Low-Voltage

Instrumentation

Electrical Machines

Drives and Power Electronics

2003: Two BA’s in original AT division

2002: Four BA’s in two divisions

2004: One single BA in a simplified AT Division

Automation Products

Automation TechnologiesPower Technologies

ABB Group

Down Stream Business

ATMA ATAP ATPA

3 Business Areas

10 Business Units

3 Divisions

1. BU 3101 LV Systems 5. BU 3121 Wiring Accessories 9. BU 4130 Machines 2. BU 3106 Breakers& Switches 6. BU 3128 Instrumentation 10. BU 4141 LV Motors 3. BU 3111 Control Products 7. BU 4120 LV Drives 4. BU 3118 Enclosures & DIN Rail Products 8. BU 4128 PE & MV Drives

ABB Facts

10

3.3 ABB Singapore ABB Singapore is a part of the ABB group with its head office at Ayer Rajha Crescent in Singapore. The company was locally established 1971 and are currently having about 700 employees. They support the ABB group with the range of system and products within each industry and market. ABB Singapore is also the centre for engineering, products and spares distribution within the Asia Pacific Region. ABB Singapore have one feeder factory that manufactures Wiring Accessories, located in Jakarta.

3.3.1 Logistic Centre Asia Logistic Centre Asia (LCA) is located in Singapore and has been in operation for the past five years. Their responsibilities are to manage the distribution logistics for ABB products in the Asia Pacific region and to provide logistic support to the region. Their current services include among others order management, transportation planning and control and IT Infrastructure. LCA is also operating a regional distribution centre, located in Singapore, for LV Drives. The product lines that are being handled by LCA is LV Motors, Spare parts, Robots and AC Drives. LCA’s vision is “to be a world class logistic centre for ABB Products” and their mission is “to give ABB and her customers a competitive advantage by ensuring timely delivery of our products at the lowest possible cost”. For an organizational chart of LCA, see figure 7.

Figure 7. LCA Organization.

Logistics Manager (14)

Biz Development

Operations (11)

Customer Service (9)

Logitics IT (2)

ABB Facts

11

3.4 Low Voltage Products The Business Area ATAP cover the full range of Low Voltage Products, hereafter referred to as LV products. Belonging to the range of LV products are products with 1,000 voltages and below, for a picture of some of the products included in the LV product range, see figure 8.

Figure 8. A selection of the major production lines belonging to LV products. The products are foremost aimed at three different applications, industry, machine building and distribution. Products belonging to the different business units included in this study are illustrated in figure 9. Business Unit Product Line Production Unit Breakers & Switches Air Circuit Breaker (ACB) ITSCE 3105 Moulded Case Circuit Breaker ITSCE Load Break Switch FICON Fuse Switch FICON Enclosures and safety switch FICON Control Products Contactors FRENT/SECRL/DESTO 3111 (3108+3109) Soft starters SECRL Pilot devices SECRL Manual Motor Starters DESTO Relays, Sensors, Timer, PLC FRENT/DESTO Terminal block FRENT Electronic products DESTO Enclosures & DIN Rail Products Miniature Circuit Breakers (MCB) DESTO 3118 Residual Current Devices (RCD) DESTO/ITSCE Accessories DESTO MDRC DESTO/ITSCE EIB DESTO Consumer Unit ITSCE/IDIIM Distribution Board ITSCE Multi-purpose Enclosure ITSCE Busbar Assemblies IDIIM Electrical Energy Meters ITSCE/DESTO Surge Arrestors FRENT Wiring Accessories Electrical Wiring Accessories (EWA) SGIND 3121 Dimmers, Speed Controller DEBJE Infrared Control System DEBJE Industrial Plugs and Sockets DEBJE/CEWE Figure 9. Business units/Product lines/Production unit.

Theoretical Frame of Reference

12

4 THEORETICAL FRAME OF REFERENCE This chapter will provide the reader with a summary of the theoretical frame of reference that has been used while conducting this study.

4.1 The Total Cost Concept For a company the goal with the distribution model is to improve overall efficiency by reallocation functions, and therefore costs among its members. The level of customer service offered by the manufacturer, for example, will have a significant impact on other members in the distribution channel. A manufacturer whose product availability is poor and whose order cycle time is inconsistent may force wholesalers to carry more inventory as safety stock in order to keep an acceptable service level to end customers. Lambert et al (1999) stress the importance that customer service solely do not provide customer satisfaction since customer satisfaction represents the customers overall assements of all elements in the marketing mix (right product, at the right price, with proper promotion available at the right price). The additional values can be achieved through improvements in customer service. Customer service is the output of the logistics system. In order to achieve a set level of customer service a number of trade-offs must be evaluated in terms of their impact on service levels. This evaluation should be conducted with respect to the total cost model.

4.1.1 The Total Cost Model The total cost concept is a key to effectively reduce the total cost of logistics activities rather than focusing on minimising each activity in isolation. (Lambert et al, 1999) The total concept is important seeing logistics decision will affect different areas of the organisation. Attempt to reduce individual costs in one area may be offset by increased costs in other areas; a trade off situation, see figure 10. The figure implies that measures that increase the cost for one activity can be motivated if the total cost decreases. The Total Cost Model by Lambert et al (1999) presents five major logistics costs categories that are driven by a number of key logistics activities required to facilitate the flow of a product from the point of origin to the point of consumption. According to the authors the activities included in the cost model depends on the outline of the logistics organisation. In some situations some components of the model needs to be removed whereas in other situations further components need to be added. Apart from providing understanding how different areas could be affected by changes within the organisation, the total cost model provides a structure to identify activities that support the logistics process.

4.2 Customer Service Customer service represent the output of the logistics system, it is a measure of the effectiveness of the logistics system in creating time and place utility for a product, including after sales support. The level of customer service not only determines whether existing customers will remain customers, but also how many potential customers the company can attract. Thus, the customer service level a company provides has a direct impact on its market share; its total logistics cost and ultimately its profitability. (Lambert et al, 1999) The cost associated with customer service is the cost of lost sales, since

Theoretical Frame of Reference

13

measuring this cost is very difficult companies should strive to minimize the total cost of the other cost components at a given service level.

Figure 10. The Total Cost Model (Lambert et al, 1999) In most companies customer service is defined as a performance measurement such as the ability to ship 95 percent of the orders received within 48 hours. Customer service can be used to differentiate the product or influence the market price, if customers are willing to pay more for better service. Management should establish customer service levels after studying customers need. Industrial companies must identify potential users and determine how these consumers will make their purchase decision. (ibid.) Customer service is a complex subject and is usually measured in terms of

• level of product availability • speed and consistency of the customer’s order cycle • communication that takes place between seller and customer

4.2.1 Availability The most important measure of customer service is inventory availability within a specified order cycle time. Availability is usually expressed in terms of

• Number of items out of stock compared to the total number of items in inventory • Items shipped as a percentage of the number of items ordered • Number of orders shipped complete as a percentage of total orders received.

Place/ Customer

service

Order Processing

Cost

Transportation costs

Warehousing costs

Inventory carrying costs

Lot quantity costs

Product

Promotion

Price LO

GIS

TICS

MAR

KETIN

G

Theoretical Frame of Reference

14

4.2.2 Order cycle The order cycle is the time that elapses between the customer’s order placement and the time the product is received. The ability to consistently achieve the targeted order cycle time influences the amount of inventory held throughout the distribution channel. Most customers prefer consistent service to fast service, since the former allows them to plan inventory levels to a greater extent than is possible with a fast but highly variable order cycle.

4.3.2 Communication In order to achieve the increased demands of reliable customer service the information flow between supplier and customer has become a focus area for companies. Communication refers to the company’s ability to frequently supply information regarding such factors as order status, order tracking, back order status, order confirmation and product shortages etc. The use of automated information systems usually results in fewer errors in shipping, picking, labelling and documentation.

4.3 Distribution Activities and Costs Logistics activities generate costs that need to be considered while computing the total logistics cost. Activities and costs that will be described in this section are found in Lamberts total logistics cost model that is explained in section 4.1.

4.3.1 Warehousing Warehousing plays a vital role in providing a desired level of customer service at the lowest possible total cost. Warehousing is used for storing inventories during all phases in the logistics process (from raw materials to finished goods). Warehouses can be used to support manufacturing, to mix products from multiple producers to a single customer, to subdivide a larger shipment to many customers etcetera. Warehousing costs compromise costs that change with the number of warehouse facilities and include fixed cost such as rent, heat, personnel, depreciation in investments and necessary equipment. Costs such as labour have a fixed and a variable component, for example if the product flows in the warehouse increases additional labour might be needed. Most warehousing costs will not change with the level of inventory stocked but rather with the number of stocking locations. This implies that warehousing cost exist independently from the levels of inventory.

4.3.2 Inventories According to Lambert et al (1999) inventories represent the largest single investment in assets for most companies. During recent years most customers in the industry have been accustomed to high level of product availability resulting in higher inventory levels for companies. Because capital invested in inventories must compete with other investments opportunities inventory management has become very important. When determining the right inventory levels several conflicting aspects need to be evaluated. Full knowledge of the cost of different inventory levels and how to they will affect the total logistics cost and delivery service needs to be taken in consideration. The pros and cons of high respective low inventory levels must be considered and most important of all, the inventory levels must be in line with the company’s competitive strategy. High levels of inventories enable for fast delivery to customer and avoid stock

Theoretical Frame of Reference

15

outs and cost for loss sales, but it is often a costly option. As opposed to high inventory levels, the primary reason for keeping levels low is the capital invested in the goods, an opportunity cost on which a company forego the opportunity to invest the capital elsewhere. Inventory carrying costs (ICC) is the costs associated with the quantity of inventory stored, it includes a number of different cost components and generally represents one of the highest costs of logistics. (Lambert et al, 1999) Inventory carrying costs should include only those costs that vary with the quantity of inventories and is categorized into following groups

1. Capital costs. Holding inventories ties up capital that could be used for other types of investments. Consequently, the company’s opportunity cost of capital, the rate of return that could be realized from some other use of the money, should be used in order to reflect the true cost. The company must consider what rate of return it is sacrificing on the cash invested in inventory.

2. Inventory service costs. Inventory service costs consist of taxes and insurances

that emerge due to holding inventories. Insurances are used as a mean to avoid financial loss in case of an accident. In general taxes vary directly with inventory levels. Insurance rates are not strictly proportional with inventory levels since insurance is usually purchased to cover a certain value of product for a specified time.

3. Storage space costs. Storage space cost is the variable cost incurred due to e.g.

replenishing and dispatching from inventory, heating and renting.

4. Inventory risk costs. This cost varies from company to company but usually include costs for obsolesces, damage and shrinkage.

Inventory levels constantly vary depending on customer demand and how often they are replenished. Inventory turnover rate is a good measure of inventory performance, a high ratio is to prefer since it indicates that inventories move through the company quickly. (Lambert et al, 1999) Inventory Turnover Rate = Annual sales value [Times/year] [1] Average inventory value

The throughput time is also of interest when measuring inventory performance. The ratio expresses the time required for goods to move through a certain section. Throughput time = 365 [Days] [2]

Inventory turnover rate If a company is experiencing a low inventory turnover rate and long throughput time the ICC is high, for an illustration of the relationship between ICC and inventory turns, see figure 11.

Theoretical Frame of Reference

16

Figure 11. The relationship between ICC and inventory turns. (Lambert et al, 1999) 4.3.2.1 ABC Analysis The number of items held in inventory at a company is often very large, but management should pay extra attention and control on only a small percentage of the items. ABC analysis is the process of dividing items into three classes according to their dollar usage, management focus should be on the items with highest value. This method is equivalent of creating a Pareto chart. A items typically represent about 20 percent of the items but account for 80 percent of the dollar usage. Class B item account for 30 percent of the items but only account for 15 percent of the dollar usage. Finally, 50 percent of the items fall in class C, representing a mere 5 percent of the dollar usage. (Krajewski et al, 2002) The goal of ABC analysis is to identify inventory levels of class A items and enable management to control them tightly. Class A items should be able to be delivered with a short delivery time and have a high stock availability. Since inventory cost for class C items are lower, much looser control is appropriate. For class C items longer delivery times and a lower stock availability is motivated. (ibid)

4.3.3 Transport A product produced at one point has little value to the prospective customer unless it is moved to the point where it will be consumed, transportation achieves this movement. The movement creates place utility but transportation is also a factor in time utility since it determines how fast and consistently a product moves from one point to another. The activity of transporting goods drive the transportation cost and the cost vary depending on weights, volumes, distance and the point of origin and destination. Transportation costs for e.g. raw material with low value per tonnage can account for a large part of the total logistics costs. For other products, e.g. high tech equipment, with high value per tonnage, the transportation cost constitute only a small part of the total logistics cost. Cost associated with transportation can be identified in total and by segment, i.e. inbound, outbound, by mode, by customer etc. (Lambert et al, 1999) Nowadays most companies have outsourced the transportation services to a third part in order to focus on its core competence. Transportation cost and delivery service is closely connected and aiming for decreased transportation cost might imply a lowered delivery service. A lowered service level can eventually lead to increased cost incurred by larger safety stocks or loss of sales. According to Gunasekaran et al (2001) the cost

ICC

Inventory turns

Theoretical Frame of Reference

17

for transportation should be treated as a metric of high priority when trying to reduce the total delivery cost. 4.3.3.1 INCO Terms The INCO terms represent a set of international rules for interpretation of delivery terms used in trade contracts. Thus, uncertainties of different interpretations of such terms can be avoided. The INCO terms were established by the International Chamber of Commerce in 1953 and are regularly updated. The scope of the INCO terms is limited to matters relating to the rights and obligation of the parties with respect to the delivery of the goods. There are in total 13 INCO terms and they are grouped in four categories, see figure 12.

Applicable for sea transport only

Applicable for all modes of transport

Departure term EXW Shipment term, main carriage unpaid FAS / FOB FCA Shipment term, main carriage paid CFR / CIF CPT / CIP Delivery term DES / DEQ DAF / DDU / DDP

Figure 12. INCO terms. From EXW down to DDP the point of transfer in the transport moves from the sellers premises to the buyers place. For the first three groups the risk of loss or damage during transportation are with the buyer of the goods, whereas for the fourth group all risks up to delivery are with the seller of the goods. (P&O Nedlloyd, http://www.ponl.com)

4.3.4 Order Processing According to Lambert et al (1999) the order processing system is the nerve of the logistic system since it sets the logistic process in motion. The customer order cycle compromises all activities, and all time elapsed, from a customer’s placement of an order to the receipt of the product. The speed and quality of the information flows has a direct impact on cost and efficiency of the entire operation. The total order cycle time usually involves activities mentioned in figure 13. The order handling process is usually facilitated through an ERP system that is aimed at ease the interface between different departments involved in the order cycle. (Krajewski & Ritzman, 2002)

Figure 13. Total order cycle time from a customer’s perspective. (Lambert et al, 1999) Order processing costs include the cost of order transmittal, order entry, order processing and other related handling costs. The cost for the information system is also

1. Order placment 6. Order delivery 5. Order shipped

2. Order received

3.Order processed

4. Order completion

Theoretical Frame of Reference

18

included in this order processing costs. When establishing these costs, only those costs that will change with the decision being made should be included. (Lambert et al, 1999)

4.3.5 Lot Quantity Costs Lot quantity costs are production and purchasing related costs that will change as a result of a change in the logistics system. Production lot quantity cost usually includes production preparation costs and capacity costs due to changeover and materials handling. The lot quantity costs associated with purchasing are the costs of buying in various quantities.

4.4 Distribution A channel of distribution is defined as the collection of organization units, either internal or external to the manufacturer, which performs the function involved in product marketing. (Lambert et al, 1999) The marketing functions include for example buying, selling, transporting, storing, financing and bearing market risk. Any organizational unit that perform one or more of the marketing activities is a member of the channel of distribution. Some channel members perform single marketing functions, for example, forwarders transport products and warehouses store them. While other, such as wholesalers perform multiple activities. Channel structures affect the control over the performance of functions; the speed of delivery, communication and the cost of the operations. While a direct manufacturer-to-user channel gives management greater control over the performance distribution cost are generally higher than for other channels. It is necessary for companies using that channel structure to have substantial sales volumes or market concentrations. (ibid)

4.4.1 Intermediaries Marketing channels develop because intermediaries, for example distributors, can make the marketing process more efficient by reducing the number of market contacts, see figure 14. Intermediaries provide possession, time and place utility. They create possession utility through the process of exchange and provide time utility by holding inventory available for sale. Finally, they provide place utility by physically moving goods to the market. The assortment of goods and services held by a producer and the assortment demanded by the customer often differs, the intermediaries can provide the customers with a broader range of products from multiple producers.

Theoretical Frame of Reference

19

Figure 14. The number of market contacts with and without an intermediary. According to Lambert et al (1999) the use of an intermediary can reduce following costs

• Selling cost (fewer marker contacts are required) • Transportation cost (fewer but larger volume shipments) • Inventory carrying costs (if the intermediary takes ownership) • Storage costs • Order processing costs

4.4.2 Centralized Distribution Large scale benefits have during recent years lead to a centralization of distribution models and warehouses. By having only a few stock points at centralized locations the increase in volume gives greater prerequisite to develop efficient warehouse operations. Another type of large scale benefits is that less capital binding is needed to achieve a certain service level than in a decentralized distribution model. Mattson (2002) argues that a centralized structure leads to decreased cost and also increased customer service levels and he pinpoints at following

• Economies of scale. With fewer stock points the material flows will get larger at the centralized warehouse. The prerequisite to invest in efficient automated technology to handle the goods becomes greater and investments in automatic processes pay off faster. When handling all warehouse operations at the same place savings in for example personnel can be done.

Producer

Customer

Intermediary

13 market contacts

Producer

Customer

30 market contacts

Theoretical Frame of Reference

20

• The fewer stock points in the distribution model the less stock is required to maintain a certain service level. The relation between service level and stock size is illustrated in figure 15.

• Savings in learning. Fast introduction of new components and less scrapping

costs when replacing old articles. • Reduction of the bullwhip effect. The bullwhip effect is directly correlated to the

number of stocking points in the supply chain. Estimates indicate the bullwhip effect is amplified to the double for every level of warehouse.

• Reduced risk for material shortage and obsolete material. Wrong dimensions of

the stock is reduced and risk for shortage of material can be minimised, i.e. if a local stock can not supply its market (they do not have enough stock to satisfy the market demand) while another market is not in need of the product.

• The product flows through a centralized warehouse is much easier to control.

The safety stock can be decreased and thereby the cost of tied capital in inventory, since the demand from the customers is never 100 percent correlated.

• Decreased cost for transportation. The cost for transportation increase when

the number of stock points increases.

Figure 15. Service level and stock size. A decentralized distribution model is to prefer for products that require fast deliveries. It is also important for products that require after-sales services and for companies that need to be close to customer location. A low degree of centralization is to prefer when having high costs for transportation in relationship to the value of the product. However, the main reason for a multiple stock points is to be close to customer location and provide fast deliveries.

4.4.3 Product Characteristics The characteristics of the products are an important consideration when designing a channel of distribution. Factors that ought to be analysed are the products value; technicality; degree of market acceptance; degree of substitutability; the product’s bulk;

Service level

Stock size

100 %

Centrazlied distributionmodel

Decentrazlied distributionmodel

Theoretical Frame of Reference

21

degree of market concentration; seasonality and width and depth of the product line. The product’s value influences its inventory carrying cost and the desirability of premium transportation. High value products may be shipped by air freight to minimize in-transit inventories and inventory carrying costs can be reduced by holding inventories at a central location. (Lambert et al, 1999)

4.5 Measuring Logistics The aim by logistics is to improve delivery performance and at the same time reduce cost. In order to realise what type of improvements are feasible it is important to obtain insight and knowledge regarding the present situation in the company. (Aronsson et al, 2003). The first step to realise feasible improvements is to map the flows and costs within the company. Consequently the mapping should facilitate the development of performance measurement that can determine the company’s present performance. The actual mapping must be customized for every company according to how the information is structured and available within the company. More resources will be consumed when conducting a detailed mapping, hence it is important to only focus on the vital part necessary for the study. According to Tangen (2004), performance measurement is defined as the process of quantifying the efficiency and effectiveness of action. A performance measurement should be derived from the companies’ strategic objectives; otherwise the performance measurement may support activities that have opposite effect of those implied in the strategy. Further Tangen states that it is important to remember that strategies usually changes over a time and therefore the performance measurement should continuously be renewed. There is a need for flexibility in the performance measurement to ensure that they are coherent with the objectives of the company. Moreover, it is important that the performance measurement is appropriately balanced and is not solely conducted on a financial basis. The performance measurement system must consist of different types of measures that encompass all important aspects agreed as representing the success of the company. Since the performance measure influence the behavior of the employees it is important to have a proper set of measurements. According to Tangen (2004) it is not rare that an improvement in one area leads to deterioration in another and that can result in a decline in overall performances. A performance measurement must therefore guard against sub-optimization to ensure that employee behavior is consistent with corporate goals. It is also important to focus on a limited number of performances since more measurement demands more analysis and it is a waste of collected data if they are ignored. The resources to gather and analyze large number of data could offset the expected benefits. According to Chow (1994), logistics performance may be viewed as a part of the large notion of organizational performance. When measuring logistics performance, effectiveness and efficiency must be distinguished. Effectiveness can be defined “as the extent to which an objective has been achieved” while efficiency is defined as “the degree to which resources have been used economically”. That means that efficiency is “doing things right” while effectiveness is “doing the right thing”. Logistics is a broad area and the objective for management must be to find a set of measures that capture most of the performance dimensions considered to be important. The use of e.g. two

Theoretical Frame of Reference

22

measures of performance can be justified for researcher whose study only addresses customer satisfaction or cost efficiency.

4.5.1 Measuring distribution models The design of a company’s distribution channel is often a result of old decision that rarely is updated. Thus, Storhagen (1997) argues that the distribution channel should continuously be evaluated. When conducting the evaluation several aspects must be considered

• Volumes. Map the flows, in volumes, and calculate the future volumes based on the companies forecasts. How does the trend look like for delivery sizes, shipment frequencies etc?

• Product flow. Where are the present and future customers located? How many customer and stock points exist?

• Types of products. How many product variation exist and what character do they have; weight; volume etc?

• Cost. How large are the cost for transportation and warehousing? • Variation. How is the variation on flow; is it stable or depends on season? • Customer service. What is the level of service aimed at? What do the

customers need and what do competitors offer? Measuring distribution models performance is difficult since some aspects of channel performance may be difficult to quantify, making a unified index of performance difficult to achieve. One measure of channel performance is the extent to which the company’s target market is being satisfied, given the companies goals. Examples of measurement of distribution model effectiveness that consider customer satisfaction are

• is the product available in desired quantities? • is the product available when needed? • is the product delivered in time?

Companies should set objectives for the distribution model and then measure actual performance against planned performance. (Lambert et al, 1999)

Results from Empirical Research

23

5 RESULTS FROM EMPIRICAL RESEARCH This chapter will provide the reader with a summary of the theoretical frame of reference that has been used while conducting this study.

5.1 The sales organisation Every business area, in this case ATAP, consists of several sales units. ATAP have sales units located in 12 countries in Asia Pacific. Some of the sales units have been excluded in the study due to reasons stated in section 1.5. Outside Western Europe the sales organisation is split into six territories under the responsibilities of five territorial managers. Their main task is to manage, develop and expand the local BA products sales organisation in the territory. Further, their task is to ensure appropriate local know-how and resources to reach the targets sat by the management. The sales units are strategically located around Asia Pacific in order to be as close to customer location as possible. They are each individually shaped and equipped to supply a specific market with LV products. The function of the sales unit, apart from sales involves marketing, order placement and provide the customers with know-how and after sales support. The sales units differ in size depending on the size of the market they are covering, in Singapore the sales teams consist of 14 persons and they are specialised towards different segments. The sales units are also equipped with local warehouses in order to be able to reduce the time from order placement to despatch. The production units sell their products to the local sales units around the world, and the sales units then resell them to end customers. Hence, it is the sales units that are in contact with the end customers. For a schematic view over the sales organisation, see figure 16.

Figure 16. ABB’s sales organisation.

The sales unit in Singapore has both local and overseas end customers. The local end customers purchase all products that are being offered while the overseas end customers only purchase products from Wiring Accessories, since one of the feeder factories for the business unit is handled by the sales unit in Singapore (the factory is located in Jakarta). The definition of end customer in this study is an external non-ABB customer. As illustrated in the figure above end customer and end user is not necessary

Production U

nits

Sales Units

Distributors

Large OEM

Large panel builders

Industry; end users

OEM Panel builders

Results from Empirical Research

24

the same. Locally the sales units have sales to a few segments that will be explained below.

• Distributors. The distributors are important for ABB since they make it possible to offer a high availability of the products. Availability is important for the market of LV products and it would be difficult for ATAP to build this distribution network themselves.

• Channel partners. The largest customers together with the distributors.

• Panel builders. Panel builders assemble components into a system. The panel

builders often supply products to OEM customers. • Original Equipment Manufacturer, OEM. OEM customer use ABB’s products in

their own constructions, for example in elevators and robots. Long term deals are negotiated with the large OEM customers and they purchase ABB products for a lower price than purchasing from distributors.

• Internal customers. The sales unit in Singapore has internal customer that

purchase Wiring Accessories, as mentioned above. Some of ABB’s main competitors on the Asian market are Schneider Electric (Germany), Siemens (Germany), Soco Mec (France) and Mitsubishi (Japan). Most of the companies compete with ABB in different product ranges, but Schneider cover the same range of LV Products as ABB. In Singapore ABB has an estimate 10 percent market share, the major actor on the market is Schneider with almost a 50 percent market share. Regarding the price level ABB is considered a midrange option between Siemens and Schneider. Schneider is the cheapest offer and they are carrying a large inventory in Singapore and can therefore promise a faster delivery than ABB. According to the sales department in Singapore the price is most important for the customer closely followed by a fast delivery. The sales units report that all their major competitors are keeping regional stocking in the region. For overall market shares for LV products see figure 17.

Figure 17. Overall market share for LV Products 2003, please note that it is not only for the Asian market.

5.1.1 LV Products The Business Area ATAP consists of 10 business units of which four consists of LV products. The business units and their major production units are listed in figure 18. (For a list of product lines belonging to the business units, see section 3.4). One production unit can manufacture different products belonging to different business units.

SchneiderLegrand ABB Siemens GE

13.6%12.0%

9.0%9.0%

6.2%

Results from Empirical Research

25

LV products are considered being high tech electrical equipment and the value of the products differs depending on the product. LV products constitutes of several products line of different width. The demand during the year is stable and do not fluctuate. Business Unit Production Unit Breakers & Switches ITSCE FICON Control Products SECRL FRENT DESTO Enclosures & DIN Rail Products DESTO ITSCE FRENT SGIND (IDIIM) Wiring Accessories DEBJE SECRL (CEWE) SGIND

Figure 18. Business units and production units.

5.1.2 Customer Service The overall purpose of the supply process is to cost efficient produce and deliver LV products to customers in accordance with their requirements. ABB has to ensure that a high level of delivery performance is maintained and that favourable conditions for the distribution to customers are built. According to the ABB logistics handbook (an internal guideline aimed at assisting production and sales unit in logistics matters) the most important level of customer value is an increased connection between the sales units and the customers, that can be achieved by a jointly learning relationship process. ABB encourage their sales units to try to shorten order lead times and in stock-availability. They should always monitor feed back from customers and provide action when improvement is needed. It is also important for customers to be updated about information such as inventory status, expected delivery dates, back orders etc. The target for on time delivery to customers requested date for all ABB sales units is 96 percent. The aim for the production units is to have a 100 percent acknowledge on time delivery.