allianz se

TRANSCRIPT

FINANCIAL INSTITUTIONS

CREDIT OPINION26 April 2021

Update

RATINGS

Allianz SEDomicile MUNICH, Germany

Long Term Rating Aa3

Type Insurance FinancialStrength - Fgn Curr

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Christian Badorff +49.69.70730.961VP-Senior [email protected]

Irina Dimitrova +49.69.86790.2106Associate [email protected]

Antonello Aquino +44.20.7772.1582Associate Managing [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Allianz SEUpdate including FY 2020 results

SummaryMoody's rates Allianz SE Aa3 for insurance financial strength (IFSR) and senior debt witha stable outlook. The rating reflects the group’s very strong franchise as well business andgeographic diversification, very strong and stable profitability, and very strong capitalisationand financial flexibility. Partially offsetting these strengths is the sensitivity of Allianz to thelow interest rate environment, which hampered its capitalisation over 2020 and which weexpect to put some pressure on the group's profitability going forward, in line with Europeanpeers. While Allianz' exposure to Italian assets and, more specifically, to Italian sovereignbonds, has meaningfully reduced over recent years, there remains some concentration risk.Furthermore, Allianz is taking on more asset risk in response to low interest rates.

Exhibit 1

Net Income and Return on Capital (1 yr. avg. ROC)1

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2016 2017 2018 2019 2020

Re

turn

on

avg

. Ca

pita

l (1 y

r. avg

RO

C)

Ne

t In

com

e

Net Income (Loss) Attributable to Common Shareholders Return on Average Capital (ROC)

[1] Net Income as adjusted by Moody'sSource: Company reports and Moody's Investors Service

Credit profile of significant subsidiariesFor more information1 on the credit profiles of: 1) Allianz Versicherungs-AG and AllianzLebensversicherungs-AG, collectively referred to as Allianz Deutschland (rated Aa2 IFSR,stable); 2) Allianz's Italian operations (Allianz S.p.A. rated A3 IFSR, stable); 3) Allianz's US lifeoperations (Allianz Life Insurance Company of North America rated A1 IFSR, stable), 4) EulerHermes SA (rated Aa3 IFSR, stable).

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Credit strengths

» Very strong global franchise and market positions in all markets Allianz is operating in

» Strong degree of diversification between P&C and life, with asset management providing additional diversification benefit

» High and low volatility profitability

» Very strong capitalisation, despite some recent weakening

» Very strong financial flexibility

Credit challenges

» Relatively high exposure to guaranteed rate business and high dependence on investment results in life

» Anticipated pressure on investment returns from continuously low interest rates

» Elevated high risk asset exposure compared to peers

» Concentration risk in Italy

» Smaller pockets of underperformance, e.g. Allianz Global Corporate and Specialty (AGCS) and Latin America

Rating outlookThe outlook for Allianz SE ratings is stable reflecting our expectation that Allianz’s business profile will remain very strong, that itsprofitability will prove resilient despite macroeconomic headwinds and that Allianz will maintain its capitalisation close to the currentlevels.

Factors that could lead to an upgradePositive rating pressure could arise from:

» Group Solvency II ratio sustainably in excess of 220% and proven resilience to a prolonged low interest rate scenario,

» Return on Capital (Moody's definition, with capital comprising shareholders' equity, free RfB reserve and hybrid capital) of at least6% through the economic and underwriting cycle, and,

» Maintaining current levels of earnings diversification and reducing the product risk inherent in the group's life product portfolio.

Factors that could lead to a downgradeNegative rating pressure could arise from one or a combination of the following factors:

» Group Solvency II ratio sustainably below 180%,

» Deterioration in profitability as evidenced by a Return on Capital (Moody's definition, with capital comprising shareholders' equity,free RfB reserve and hybrid capital) below 5%, and/or,

» Significant increase in investment risk, as reflected in an increase of the high risk asset ratio (Moody's definition) to more than180%.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

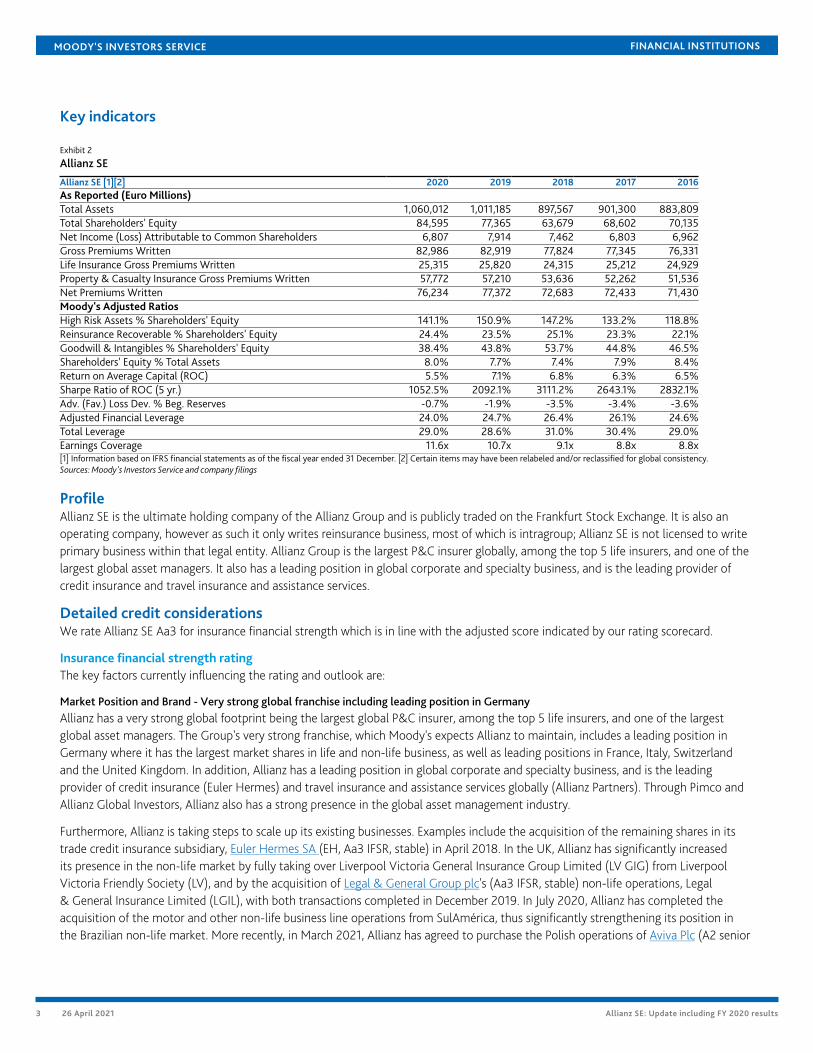

Key indicators

Exhibit 2

Allianz SE

Allianz SE [1][2] 2020 2019 2018 2017 2016As Reported (Euro Millions)Total Assets 1,060,012 1,011,185 897,567 901,300 883,809Total Shareholders' Equity 84,595 77,365 63,679 68,602 70,135Net Income (Loss) Attributable to Common Shareholders 6,807 7,914 7,462 6,803 6,962Gross Premiums Written 82,986 82,919 77,824 77,345 76,331Life Insurance Gross Premiums Written 25,315 25,820 24,315 25,212 24,929Property & Casualty Insurance Gross Premiums Written 57,772 57,210 53,636 52,262 51,536Net Premiums Written 76,234 77,372 72,683 72,433 71,430Moody's Adjusted RatiosHigh Risk Assets % Shareholders' Equity 141.1% 150.9% 147.2% 133.2% 118.8%Reinsurance Recoverable % Shareholders' Equity 24.4% 23.5% 25.1% 23.3% 22.1%Goodwill & Intangibles % Shareholders' Equity 38.4% 43.8% 53.7% 44.8% 46.5%Shareholders' Equity % Total Assets 8.0% 7.7% 7.4% 7.9% 8.4%Return on Average Capital (ROC) 5.5% 7.1% 6.8% 6.3% 6.5%Sharpe Ratio of ROC (5 yr.) 1052.5% 2092.1% 3111.2% 2643.1% 2832.1%Adv. (Fav.) Loss Dev. % Beg. Reserves -0.7% -1.9% -3.5% -3.4% -3.6%Adjusted Financial Leverage 24.0% 24.7% 26.4% 26.1% 24.6%Total Leverage 29.0% 28.6% 31.0% 30.4% 29.0%Earnings Coverage 11.6x 10.7x 9.1x 8.8x 8.8x[1] Information based on IFRS financial statements as of the fiscal year ended 31 December. [2] Certain items may have been relabeled and/or reclassified for global consistency.Sources: Moody's Investors Service and company filings

ProfileAllianz SE is the ultimate holding company of the Allianz Group and is publicly traded on the Frankfurt Stock Exchange. It is also anoperating company, however as such it only writes reinsurance business, most of which is intragroup; Allianz SE is not licensed to writeprimary business within that legal entity. Allianz Group is the largest P&C insurer globally, among the top 5 life insurers, and one of thelargest global asset managers. It also has a leading position in global corporate and specialty business, and is the leading provider ofcredit insurance and travel insurance and assistance services.

Detailed credit considerationsWe rate Allianz SE Aa3 for insurance financial strength which is in line with the adjusted score indicated by our rating scorecard.

Insurance financial strength ratingThe key factors currently influencing the rating and outlook are:

Market Position and Brand - Very strong global franchise including leading position in GermanyAllianz has a very strong global footprint being the largest global P&C insurer, among the top 5 life insurers, and one of the largestglobal asset managers. The Group's very strong franchise, which Moody's expects Allianz to maintain, includes a leading position inGermany where it has the largest market shares in life and non-life business, as well as leading positions in France, Italy, Switzerlandand the United Kingdom. In addition, Allianz has a leading position in global corporate and specialty business, and is the leadingprovider of credit insurance (Euler Hermes) and travel insurance and assistance services globally (Allianz Partners). Through Pimco andAllianz Global Investors, Allianz also has a strong presence in the global asset management industry.

Furthermore, Allianz is taking steps to scale up its existing businesses. Examples include the acquisition of the remaining shares in itstrade credit insurance subsidiary, Euler Hermes SA (EH, Aa3 IFSR, stable) in April 2018. In the UK, Allianz has significantly increasedits presence in the non-life market by fully taking over Liverpool Victoria General Insurance Group Limited (LV GIG) from LiverpoolVictoria Friendly Society (LV), and by the acquisition of Legal & General Group plc's (Aa3 IFSR, stable) non-life operations, Legal& General Insurance Limited (LGIL), with both transactions completed in December 2019. In July 2020, Allianz has completed theacquisition of the motor and other non-life business line operations from SulAmérica, thus significantly strengthening its position inthe Brazilian non-life market. More recently, in March 2021, Allianz has agreed to purchase the Polish operations of Aviva Plc (A2 senior

3 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

unsecured debt rating, stable). The acquisition will make Allianz the fifth-largest insurer in Poland and serves to consolidate its leadingposition in central and eastern Europe (CEE).

Allianz is also stepping up its efforts to further digitalize and to simplify its business model to increase customer satisfaction, improvecost efficiency and to strengthen growth momentum.

Distribution - Strong diversity and controlAllianz's distribution is viewed as strong, with access to a variety of channels in many of the countries in which it operates. For its lifebusiness, there is a strong focus on tied agents, especially in Germany, which is the Group's largest distribution channel. The othersignificant channels are brokers, as well as bancassurance, which is growing and where the Group has exclusive distribution agreementsin various regions such as with HSBC in Asia for life insurance, with UniCredit in Italy and several CEE countries for life and P&C, withSantander and HypoVereinsbank in Germany for both life and P&C, and effective from December 2020 with BBVA in Spain for P&C.

Allianz is also developing new digital distribution models and its new Pan-European direct insurance brand has become operational inlate 2019.

Product Focus and Diversification - Very strong diversification partially offset by risks from life bookAllianz benefits from very strong diversification by business lines. In 2020, operating profits were well balanced between non-life (38%of operating profit excluding corporate, consolidation and other), life & health (38%) and asset management (25%). The Group'sgeographic diversification is also very strong, with the majority of operating profits being generated in European businesses and sizablecontributions from other regions, as well as by global lines and asset management, which are well diversified geographically in theirown right.

Allianz's key product risk is in the life segment, which has relatively high guarantees in many core markets, notably Germany, and forwhich low interest rates are especially challenging. For FY 2020, Allianz reported a spread between the current yield (2.86%, based onaverage book values of assets) and the average guaranteed rate (1.85%, based on technical reserves) of c.100bps, compared to c.150bpsfor FY 2014. Yields on re- and new investments have deteriorated in 2020 and we expect this to reduce the spread going forward,despite strong asset-liability management. Allianz is actively reducing this type of risk by further reducing guaranteed rates on newbusiness, but given the long duration of its inforce book, this will take time. In some jurisdictions, Allianz is speeding up this process bydisposing of back-books as well.

The risk in P&C is more limited with the book well-balanced between commercial and retail business although the relatively largeglobal corporate and specialty business meaningfully exposes the Group to large claims and reserving risk.

Asset Quality - good quality, well managed but risk exposure is gradually increasingAllianz's asset quality is good, including 33% of government bonds, 8% covered bonds, 32% of corporate bonds and 9% of equities asat YE 2020. The average quality of the fixed income securities also remained good at YE 2020 with 65% of debt securities rated A orabove. The high risk assets as a % of shareholders’ equity ratio (which includes equities, investment property, and below investmentgrade/unrated debt securities) was relatively high at 141% at YE 2020 (151% at YE 2019) but this is mitigated to some extent by theGroup’s ability to share losses with policyholders by managing its crediting rates, and also by hedging.

In line with European peers, Allianz has been increasing its exposure to alternative investments, such as mortgages, real estate, privateplacements, infrastructure and private equity. During 2020, these investments grew by 10% to €176.5 billion (c.61% of this amountcomprising mortgages and real estate) representing about 21% of the investment portfolio. Whilst enhancing yield and matching wellwith the Group's illiquid liabilities, Moody's believes that these investments also add more risk to the Group's investment portfolio. Inview of continuously low interest rates, we expect that Allianz will continue to gradually increase investment risk.

Allianz's exposure to Italian sovereign bonds (Government of Italy, Baa3, stable outlook) has significantly reduced over past years, from52% of the Group’s reported shareholders’ equity at year-end 2014 to 24% at year-end 2020.

The Allianz Group's goodwill and intangibles to adjusted equity at 38.4% at YE 2020 (YE 2019: 43.8%) has decreased driven by boththe decline in deferred acquisition costs and the rise in shareholder's equity. The ratio appears relatively high but this is mainly drivenby deferred acquisition costs, where Allianz has no track record of meaningful impairments. Excluding these from the calculation wouldresult in a ratio of around 16%.

4 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

The Group’s reinsurance recoverables are low, representing around 24.3% of shareholders' equity at YE 2020.

Capital Adequacy - Very Strong capitalisation despite recent weakening affected by the coronavirus-related market volatilityAllianz's capitalisation weakened over 2020, with the Group Solvency II ratio decreasing by 5%points to 207% (YE 2019: 212%),with the increase in solvency capital requirement (SCR) only partly offset by the increase in own funds. The ratio has deterioratedpredominantly due to unfavourable market movements resulting from the coronavirus outbreak, notably the low interest rates(-27%points), but was also negatively impacted by tax and other changes (-8%points). The overall decrease was only partly offset bythe strong pre-tax operating capital generation (+23%points) and the positive effects from model changes (+1%point) and from capitalmanagement actions (+7%points) (including the issuance of subordinated debt in May and November 2020 and various de-riskingmeasures such as reduction of equity exposure and duration management). It is noteworthy, that Allianz, in contrast to most Europeanpeers, did not stop or reduce its dividend payment out of the 2019 earnings.

Reported sensitivities of Allianz' Solvency II coverage to external factors are moderately high, but a broader market stress - such asthe one experienced in the first half of 2020 - tends to exceed the combined sensitivities to single market movements. At YE 2020,the largest sensitivity was against 50bps increase in credit spreads on government bonds (-15%points, YE 2019: -10%p), followedby 30% fall in equity markets (-14%points, YE 2019: -15%points) and a decrease in interest rates by 50bps (-9%points, YE 2019:-9%points). We expect Allianz to maintain its Solvency II ratio within the target range, however in an event of economic downturnscenario and negative financial market movements, a fall in equities or a fall in interest rates to even lower levels would hurt theGroup's capitalisation.

In its updated set of targets for 2019-2021, Allianz has committed itself to maintain Group Solvency II above 180%, moving away fromthe range of 180-220% it had stated previously. At the same time Allianz committed to maintain a disciplined approach to capitalmanagement and to payout capital identified as being excess capital to shareholders via dividend payments and share buybacks unlessit can be invested in growing the business while meeting strict hurdles. In Q2 2020, Allianz announced the introduction of the technicalprovision transitional measures for its German life and health insurance operations for its reported regulatory Solvency II position,based on which the Group Solvency II ratio was 240%. Allianz's capital management will continue to be based on the more economicbasis excluding these transitional measures.

Profitability - Strong and very stable operating performance to be maintained in the long-term but increasing pressure from low interestratesAllianz's profitability has been strong on average in the last five years, with a Return on Capital (Moody's definition, with capitalcomprising shareholders' equity, free RfB reserve and hybrid capital) of 6.4%. Furthermore, volatility of earnings has been low.

In 2020, the Group's performance was adversely affected by the coronavirus pandemic and recorded a 9.3% decrease in operatingprofit to €10.8 billion (YE 2019: €11.9 billion). While in P&C and in Life and Health operating profits decreased by 13.4% and 7.4%respectively, the Asset Management segment recorded a growth in operating profit of 5.5%. Net income fell by 14.1% to €7.1 billion (YE2019: €8.3 billion), reflecting the fall in operating profit and negative non-operating variances including restructuring expenses, whereasthe negative effect of increasing impairments and lower realized gains on investments was partially offset by a gain on the sale of theAllianz Popular bancassurance partnership.

In P&C, the operating result declined to €4.4 billion at YE 2020 (YE 2019: €5.0 billion) driven by the decrease in underwriting result andinvestment income. The drop in underwriting result was mainly due to coronavirus claims in business interruption, event cancellationand credit insurance, partially offset by lower claims frequency in other lines of business. In addition, reserve releases were lower andnatural catastrophe claims higher than in 2019. Despite the significant improvement of the expense ratio by 0.7%points, the Group'scombined ratio deteriorated to 96.3% (YE 2019: 95.5%). The weaker operating investment result was prompted by lower yields anddividend income.

In Life and Health, operating profit declined to €4.4 billion (YE 2019: 4.7 billion) mainly due to lower loadings and fees following thedeconsolidation of Allianz Popular in Spain and lower new business, as well as due to loss recognition and a positive prior-year impactin the United States. These negative developments have been only partly compensated by the increase in investment margin andreduced acquisition expenses. The new business margin decreased to 2.8% at YE 2020 (YE 2019: 3.2%) driven by negative impacts

5 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

from lower interest rates. The new business value dropped by 19.6% to €1.7 billion reflecting both lower volumes and decreasedmargins.

The Asset Management business segment demonstrated strong resilience with operating profit increasing to €2.9 billion at YE 2020 (YE2019: €2.7 billion) driven by higher average assets under management and related revenues. The Group reported third party net inflowsof €32.8 billion in 2020 (FY 2019: €75.8 billion) and a decrease in its cost-income ratio to 61.2% (YE 2019: 62.3%).

We expect that the low interest rates will continue to gradually reduce Allianz’s investment returns. While we anticipate this to havenegative implications for both Allianz's life and P&C segment, the implications for its life segment will likely be more pronounced.

Looking forward, Moody’s expects that Allianz will be able to gradually return to pre-crisis profitability levels, thanks mainly to graduallyimproving P&C underwriting profitability offsetting pressure by low interest rates on life earnings. Allianz continues to take steps toturn around its commercial business, written into AGCS, which recently has been a drain of profitability. Pricing in commercial linescontinues to develop favourably, providing tail-winds, whereas we anticipate the positive pricing momentum to level out somewhat,given the economic environment.

Liquidity & Asset Liability Management - Low liquidity risk and strong ALM capabilities, but nature of life business poses challengesWe view Allianz's ALM capabilities as strong, and the Group at YE 2020 operates with low duration gap of around -0.1 years (-0.1 yearsat YE 2019). However, the Group still has a relatively high although decreasing average guaranteed rate of 1.85% (1.93% at YE 2019) forits life business, and the long, though reduced duration of Life & Health liabilities and pressured interest rate environment makes ALMmore challenging, particularly in Germany (reported weighted average guaranteed rate of 1.8% at YE 2020). The sensitivity of the Group'sSolvency II ratio (-9%points reduction in scenario of a decrease in interest rates by 50bps at YE 2020) illustrates this risk.

In 2020, Allianz reported a spread between the current yield (2.9%, based book values of assets) and the average guaranteed rate(1.9%, based on technical reserves) of c.100bps, compared to c.150bps in 2014. Yields on re- and new investments have furtherdeteriorated in 2020 and Moody’s anticipates the spread to reduce further going forward. This will likely prompt Allianz to take onadditional asset risk in search for yields, although Moody’s expects this to occur only gradually and under strict observation of asset-liability management and capital management requirements.

Liquidity of the Group is very strong (also see section Liquidity Profile below).

Reserve Adequacy - Consistently favourable reserve developmentThe overall reserve adequacy of Allianz, which has consistently released reserves, is considered strong. Over the last ten years, theGroup's prior year releases have benefited its combined ratio by a meaningful average of around 3.4%points. During 2020, thereported run-off ratio reduced to 0.8% (YE 2019: 2.1%) largely driven by reserve strengthening at AGCS, but also due to lower reserverelease from Allianz's operations in Reinsurance, Australia and Italy. Allianz's reserving risk benefits from its very diversified book ofbusiness, although the proportion of commercial/specialised risks is meaningful, and going forward we expect the Group to continue toreport reserve releases.

Financial Flexibility - Very strong access and healthy leverage and coverage ratiosAllianz's adjusted financial leverage decreased in 2020 to 24.0% (YE 2020: 24.7%) driven by the increase in shareholders' equity morethan offsetting the increase in total borrowings. However, the total leverage slightly increased to 29.0% at YE 2020 (YE 2019: 8.6%)reflecting the issuance of restricted Tier 1 bonds of €2.3 billion.

In Q1 2020, Allianz issued senior debt amounting to €1.25 billion via two issuances with 5 and 11 year maturities respectively and calleda €750 million senior bond. In Q2, the Group concluded the placement of a €1.0 billion subordinated bond. Furthermore, in Q4 2020,Allianz issued a dual tranche RT1 (€1.25 billion and US$1.25 billion) and called another senior bond of €500 million. Recently, in March2021, Allianz called two subordinated bonds of €800 million and US$1.0 billion.

Allianz Group has historically been an active user of debt. Allianz SE either guarantees or directly issues most of the Group's debt, withthe majority of the debt issued through the vehicle Allianz Finance II B.V. Going forward, we expect Allianz adjusted financial leverageto remain below 30%.

6 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

The 5 year average earnings coverage for FY 2020 of 9.8x, which is within Moody's expectations for Aa rated companies, improvedfrom 9.3x for FY 2019. The 1 year earnings coverage ratio increased to 11.6x in 2020 from 10.7x in 2019 benefitting from lower fundingcosts. Moody's expects Allianz to achieve earnings coverage of at least 6x-8x.

Moody's considers the refinancing risk to be limited in the coming few years, given Allianz's well balanced debt profile, cash positionand access to capital markets.

Exhibit 3

Financial Flexibility

Sources: Moody's Investors Service and company filings

Liquidity analysisAllianz SE's primary source of cash-flow is from its directly and indirectly held participations in insurance operations (please note: allfigures in this paragraph are based on the local GAAP single legal entity annual reports). In 2020, Allianz SE received from its directlyheld participations about €4.5 billion (YE 2019: €4.0 billion) of dividends, as well as €2.4 billion (YE 2019: €2.6 billion) of income fromprofits transfer agreements, while it reported a negative net technical result from reinsurance business of €-223 million (YE 2018:€-225 million). At the same time, Allianz SE incurred €0.9 billion of interest expense (YE 2019: €1 billion) and the total dividends paid in2020 for 2019 were €4.0 billion (dividend paid in 2019 for 2018 was €3.8 billion). Allianz ultimately plans and manages the Allianz SEresult (net earnings of €4.4 billion in 2020 and €4.5 billion in 2019) in line with the liquidity needs of the Group.

Allianz SE maintains a USD CP programme and Euro CP programme. US CP (through a USD5.0 billion programme) is issued via vehicleAllianz Finance Corporation, whose very strong liquidity is supported by an unconditional and irrevocable guarantee from Allianz SE.The US CP stood at USD0.2 billion as of YE 2020. The majority of US CP issuance is issued on a 2-day settlement basis. The Group'Euro CP issuance programme (€5.0 billion maximum) is issued directly through Allianz SE and the outstanding amount as at YE 2020was around €0.9 billion.

Allianz SE as the Group holding company and reinsurer for the Group maintains a significant level of high liquidity assets (cash, bonds,tradable equities) on its own balance sheet, in respect of shareholder funds and policyholder obligations, which could be used tosupport short-term liquidity needs at Allianz SE or its financing subsidiaries. Allianz SE also manages a cash pool which includes allGerman operating companies and the majority of European entities, such that liquid assets could be made available to the holdingcompany from certain key subsidiaries at short notice. In addition, Allianz SE benefits from substantial committed, long-term bankcredit lines and LOC facilities. Therefore, in Moody's opinion, the Group is able to unambiguously meet all its near-term maturingobligations.

7 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Structural considerationsAllianz SE is the ultimate holding company of the Group and is also an operating company, however as such it only writes reinsurancebusiness, most of which is intragroup; Allianz SE is not licensed to write primary business within that legal entity. As a result of thisspecial status, Allianz SE's insurance financial strength and senior debt ratings are assigned at the same level, Aa3, and the subordinateddebt rating at A2. This is consistent with Moody's standard notching approach for reinsurance operating companies.

Environmental, Social and Governance (ESG)Allianz Group is taking into account ESG considerations in their decision making, for example by applying ESG criteria in investmentmanagement. Allianz also reports regularly on its approach and its progress. At this stage, we do not consider this to result in materialcredit implications for Allianz SE or its subsidiaries.

EnvironmentalLike its P&C insurance peers, Allianz is exposed to the economic consequences of climate change, primarily through the unpredictableeffect of climate change on the frequency and severity of weather-related catastrophic events, such as floods, storms, drought andwildfires. Compared to some similarly rated peers, Allianz has lower exposure to natural catastrophes and in addition it has adequatereinsurance cover in place and is able to reprice its products regularly which helps in mitigating these risks to a certain extent.

SocialLike its peers, Allianz faces social risks through the handling of customer information, the underwriting and business growthimplications (positive and negative) of changing demographics, and the impact of changing consumer preferences on distributionchannels. Furthermore, Allianz's social risks arise primarily from underwritten exposures to a wide range of liability claims againstindividuals and corporations (e.g. industrial accidents, health & safety issues, product recalls).

GovernanceLike all other corporate credits, the credit quality of Allianz is influenced by a wide range of governance-related issues, relating tofinancial, managerial, ownership or other factors, all of which can be exacerbated by regulatory oversight and intervention. Allianz is alarge and complex group and has adequate corporate governance practices in place.

8 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Rating methodology and scorecard factors

Exhibit 4

Allianz SE

Financial Strength Rating Scorecard [1][2] Aaa Aa A Baa Ba B Caa ScoreAdj ScoreBusiness Profile Aa AaMarket Position and Brand (20%) Aaa Aa

-Relative Market Share Ratio XDistribution (5%) Baa Aa

-Distribution Control X-Diversity of Distribution X

Product Focus and Diversification (10%) Aa Aa-Product Risk - P&C X-Product Risk - Life X-Product Diversification X-Geographic Diversification X

Financial Profile Aa AaAsset Quality (10%) A A

-High Risk Assets % Shareholders' Equity 141.1%-Reinsurance Recoverable % Shareholders' Equity 24.4%-Goodwill & Intangibles % Shareholders' Equity 38.4%

Capital Adequacy (15%) Aa Aa-Shareholders' Equity % Total Assets 8.0%

Profitability (15%) Aa Aa-Return on Capital (5 yr. avg.) 6.4%-Sharpe Ratio of ROC (5 yr.) 1052.5%

Liquidity and Asset/Liability Management (5%) Aa Aa-Liquid Assets % Liquid Liabilities X

Reserve Adequacy (5%) Aa Aa-Adv. (Fav.) Loss Dev. % Beg. Reserves (5 yr. wtd. avg.) -2.1%

Financial Flexibility (15%) Aa Aa-Adjusted Financial Leverage 24.0%-Total Leverage 29.0%-Earnings Coverage (5 yr. avg.) 9.8x

Operating Environment Aaa - A Aaa - APreliminary Standalone Outcome Aa3 Aa3[1] Information based on IFRS financial statements as of fiscal year ended December 31, 2020. [2] The Scorecard rating is an important component of the company's published rating,reflecting the standalone financial strength before other considerations (discussed above) are incorporated into the analysis.Source: Moody’s Investors Service

Ratings

Exhibit 5

Category Moody's RatingALLIANZ SE

Rating Outlook STAInsurance Financial Strength Aa3Senior Unsecured MTN (P)Aa3Commercial Paper P-1Subordinate A2 (hyb)Junior Subordinate A2 (hyb)

Source: Moody's Investors Service

Endnotes1 Please note: the ratings and outlooks stated here are the current ones at the time of publication but might have changed since then

9 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2021 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDITCOMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY,“PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUALFINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’SRATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SCREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICEVOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOTSTATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK ANDRELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHEROPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHEROPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDITRATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR.MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDINGTHAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE,HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESSAND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENTDECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIEDOR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USEFOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTENCONSENT.MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM ISDEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing its Publications.To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating,agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $5,000,000. MCO and Moody’sInvestors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regardingcertain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publiclyreported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance —Director and Shareholder Affiliation Policy.”Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and servicesrendered by it fees ranging from JPY125,000 to approximately JPY550,000,000.MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1259941

10 26 April 2021 Allianz SE: Update including FY 2020 results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

11 26 April 2021 Allianz SE: Update including FY 2020 results