amm aerospace materials conference. pittsburgh, pa. airbus … · 2012-04-27 · airbus market...

TRANSCRIPT

Airbus market update and 20 year forecast

PR1206581_v1

Simon F. Pickup

Director - Business Operations, Airbus Americas

AMM Aerospace Materials Conference. Pittsburgh, PA.

Presentation agenda

•Commercial review

•Global Market Forecast (GMF)

•Airbus product line update

2011 was a record year for Airbus

To December 31st, 2011

Airbus record

Airbus deliveries 534

Industry records

Airbus orders 1,608 gross

1,419 net

Airbus year-end backlog 4,437 aircraft

Sales of a new model 1,226 A320neo

Airbus and Boeing orders over the last 15 years

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Airbus

Boeing

Gross units

Both Airbus and Boeing have seen significant backlog growth since 2005. 2011 saw the industry sales record broken by Airbus.

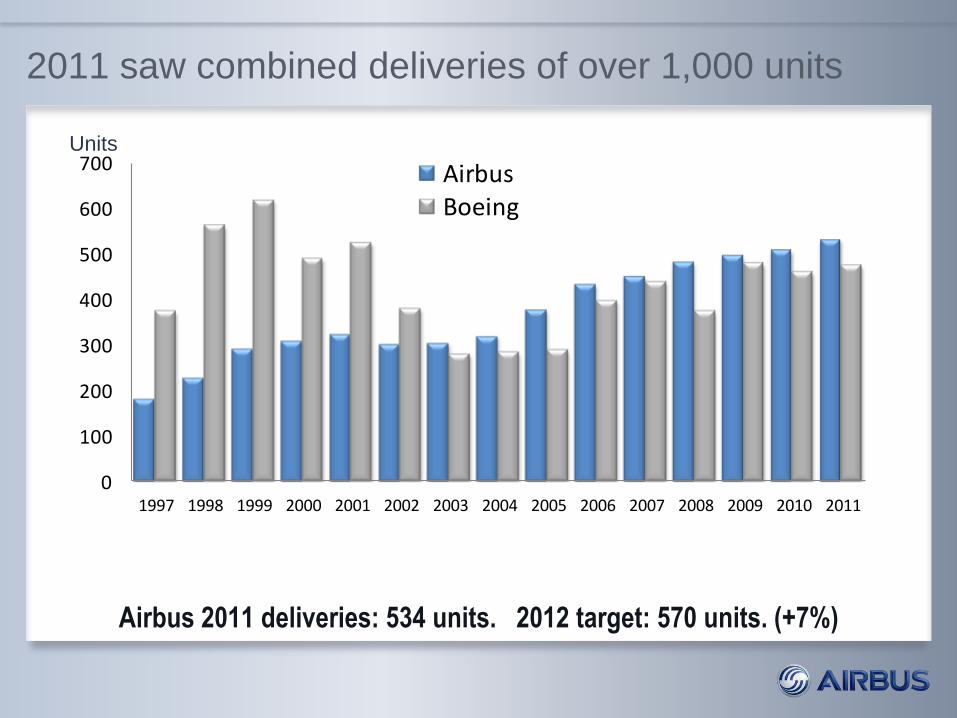

2011 saw combined deliveries of over 1,000 units

Airbus 2011 deliveries: 534 units. 2012 target: 570 units. (+7%)

0

100

200

300

400

500

600

700

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

AirbusBoeing

Units

Airbus deliveries over the last 15 years

Airbus’ measured production rate increases have obviated the need for drastic output changes

0

100

200

300

400

500

600

700

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Asian Crisis

9/11 Attack SARS

Global Financial Crisis

The Airbus and Boeing combined backlog stands at almost 8,400 units

Airbus 4,491 units

Boeing 3,881 units

Airbus’ backlog represents around 7 years of production

46% 54%

End January 2012

2,477 70

373 865 96

737: 767: 777: 787: 747-8:

A320:

A330/A340:

A350XWB:

A380:

3,406

345

555

185

Airbus backlog by geographical region

Airbus’ backlog is well balanced by region

North America

493 aircraft

11%

Asia-Pacific

1,642 aircraft

37%

Latin America

315 aircraft

7%

Europe

526 aircraft

12%

Middle East

456 aircraft

11%

Lessors

895 aircraft

19%

Africa

78 aircraft

2%

Corporate, Military

32 aircraft

1%

At December 31st, 2011

Current and planned monthly production rates

40 42 per month

A320 Family

10 per month A350XWB

Family

3 3.5 per month A380

A330 Family

9 10 per month

Air travel has proved to be resilient to external shocks

Gulf Crisis Oil Crisis

World annual traffic (RPKs - trillions) Asian Crisis 9/11 Oil Crisis SARS Recession

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1970 1975 1980 1985 1990 1995 2000 2005 2010

+ 45%

growth

45% growth from 2000 to 2010

2011 saw impressive passenger traffic growth

2011

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep. Oct. Nov. Dec.

Record high oil price throughout the year (US$95 for WTI and US$110 for Brent)

MENA unrest

Japanese earthquake

Eurozone debt crisis

4

4.25

4.5

4.75

5

5.25

2010 2011

+5.8%

World annual passenger traffic (RPKs - trillions)

Despite major external

shocks throughout the

year, world passenger

traffic grew 5.8% in 2011

Outlook for 2012, according to IATA

“While we have seen some improvements in

economic prospects, any further significant rise in

fuel price will almost certainly turn weak profits into

losses,"

Tony Tyler, IATA Director General,

March 2012.

IATA’s current global

forecast:

2012 net industry

profit: $3 Billion

Top performing

regions: Asia-Pacific,

North America and

Middle East

Jet fuel price volatility

Source: US Energy Information Administration, US Gulf Coast Jet Fuel Spot Prices

Global Market Forecast 2011 - 2030

Market Outlook

September 2011

0

2

4

6

8

10

12

1970 1980 1990 2000 2010 2020 2030

0

2

4

6

8

10

12

1970 1980 1990 2000 2010 2020 2030

Air travel remains a robust growth market

World annual traffic (RPKs - trillions)

20-year world annual traffic growth

4.8% ICAO

total traffic

Airbus

GMF 2011

Air traffic has doubled

every 15 years

Traffic will

double again

in the next 15

years

Page 16

20-year demand for almost 27,800 new passenger and freighter aircraft

Market value of $3.5 trillion Source: Airbus GMF

Passenger aircraft (≥ 100 seats) Jet freight aircraft (>10 tons)

1,680 very large aircraft

6,920 twin-aisle aircraft

19,170 single-aisle aircraft

The in-service passenger fleet will more than double in size by 2030

Fleet size (units)

15,002

Passenger aircraft 100 seats (excluding freighters)

31,424

26,900

2011 2030

Page 18

Air transport growth is highest in expanding regions

Population growth, urbanization and economic prosperity will all drive air travel demand in the developing regions

China

India

Middle East

Asia

Africa

CIS

Latin America

Eastern Europe Exp

an

din

g r

eg

ion

s

Western Europe

North America

Japan

1 billion people 2011

6 billion

people 2011

Yearly RPK growth

2011 -2030

“Global middle class” expected to rise to 4.9 billion people by 2030

In 2030, two thirds of the global middle class will be in Asia-Pacific Source: Kharas and Gertz, Airbus

* Households with daily expenditures between $10 and $100 per person (at PPP)

Millions of people

664 703 680

338 333 322

525

1,740

3,228

318

473

654

0

1,000

2,000

3,000

4,000

5,000

2010 2020 2030

Other

Asia-Pacific

North America

Europe

1,845

6,900

3,249

7,600

4,884

8,300 World pop. (M)

X 6

0 1,000 2,000 3,000 4,000 5,000

Asia-Pacific

Europe

North America

Middle East

Latin America

CIS

Africa

Asia-Pacific to lead in world traffic by 2030

2010 traffic 2010-2030 traffic

World Traffic by airline domicile (RPK billions)

Page 20

33%

23%

20%

11%

6%

4%

3%

% of 2030

world RPK

Asia-Pacific to take one third of deliveries North America and Europe take 22 percent each

Asia-Pacific

34%

Europe 22%

North America

22%

Latin America

8%

Middle East 7%

Africa 4%

CIS 3%

26,921 passenger aircraft delivery demand

Forecast deliveries (units)

Asia-Pacific: 9,160

Europe: 5,950

North America: 5,901

of which:

USA: 5,389

P.R. China: 4,041

Significant replacement market

4,500 aircraft to be replaced by a more eco-efficient generation Source: Ascend and Airbus GMF, for end 2010 in-service fleets

Old : A300B, 707, 727, 737-100/200, 747-100/200,

Mid: A300-600/A310, 737-300/400/500, 747-300, 757, 767, F100, MD11, MD90/90

New: A320, A300/A340, A380, 717, 737NG, 747-400, 777, ERJ190

North America 1,657 Old and mid generation

aircraft in service

41%

Latin America 226 Old and mid generation

aircraft in service

33%

Europe 1,070 Old and mid

generation

aircraft in service

25%

Africa &

Middle East 802 Old and mid generation

aircraft in service

37%

Asia-Pacific 745 Old and mid generation

aircraft in service

21%

A320 Family

A320 Family – best selling single aisle family Data to end March 2012

8,380 firm orders

5,051 deliveries

3,329 order backlog

The A320neo Family

A real step in efficiency:

15% less fuel burn and CO2 emissions

15% more range

While maintaining the Family values:

Building on proven programme with over 8,300 sales

Minimum change, maximum commonality

Maturity from service entry, with low industrial/technical risk

The A320neo will enter service in 2015

A320neo worldwide success

A320 Family is the leader in all market segments

30

100 36 80

60

40

45

33

22

20

30

30

150

200

72

80 6

30

10

1,289 Firm orders from 24 customers

130

8

78

30

50

50 30

100

A330 and A350XWB: complimentary twins

Data to end March 2012

The A330 and A350XWB Families offer a complete fleet solution

A330: 1,188 firm orders

328 order backlog

89 customers

A350XWB: 555 firm orders

34 customers

A350 XWB: an „Intelligent Airframe‟ by design

CFRP

Wings

Centre wing box and keel beam

Tail cone (Section 19)

Skin panels

Frames, stringers and doublers

Doors (Passenger & Cargo)

No corrosion & fatigue tasks

Titanium

High load frames

Door surroundings

Landing gear

Pylons

No corrosion tasks

Al/Al-Li

19%

Titanium

14%

Steel 6%

Misc.

8%

Composite

53%

MSN 5000 (static test) front and centre fuselage join-up

A350 XWB final assembly started Toulouse France – 5th April 2012

Trent XWB engine flying test bed

First flight 18th February 2012, over one year before A350 first flight

The A380 orderbook – a continuing growth story

253 firm orders from

19 Customers

17 A380

10 A380

12 A380

19 A380

1 A380

12 A380

2 A380

6 A380

6 A380

5 A380

6 A380

10 A380

90 A380

10 A380

20 A380

5 A380

6 A380

6 A380

Private

Customer

Data as at January 17th 2012

10 A380

71 A380s delivered to date to 7 customers Around 100 will be in service by year‟s end

Malaysia Airlines and Thai will join the operator base this year In-service fleet as of end March 2012

Page 32

Incomparable popularity

“A380 flights are almost

always full. In all of my 40

years in the business, I’ve

never known an aircraft to

be so popular. People are

especially keen to fly in the

A380”. Tim Clark

Emirates CEO

interviewed by Süddeutsche Zeitung – 16th December 2011

Page 33

Airbus has sold 11,569 aircraft to 337 customers

To end March 2012

Total sales include A330, A310 and A340 models

A350 Family

A380 Family

A330 Family

A320 Family

The only large scale manufacturer with an all fly-by-wire product line

New standards. Together.

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. This document and all information contained herein is the sole property of AIRBUS S.A.S. No intellectual property rights are granted by the

delivery of this document or the disclosure of its content. This document shall not be reproduced or disclosed to a third party without the express written consent of AIRBUS S.A.S. This document and its content shall not be

used for any purpose other than that for which it is supplied. The statements made herein do not constitute an offer. They are based on the mentioned assumptions and are expressed in good faith. Where the supporting

grounds for these statements are not shown, AIRBUS S.A.S. will be pleased to explain the basis thereof.

AIRBUS, its logo, A300, A310, A318, A319, A320, A321, A330, A340, A350, A380, A400M are registered trademarks.

Page 35