analyze this, analyze that: a reversing entry … · analyze this, analyze that: a reversing entry...

TRANSCRIPT

1

ANALYZE THIS, ANALYZE THAT: A REVERSING ENTRY CASE

Ting Jie (TJ) Wang, Ph.D. §

Associate Professor of Accounting

College of Business

Governors State University

Phone: 708-534-4965 / Fax: 708-534-8457

1 University Parkway

University Park, Illinois 60484

Xinghua Gao, Ph.D.

Assistant Professor of Accounting

College of Business

Governors State University

Phone: 708-235-7624 / Fax: 708-534-8457

1 University Parkway

University Park, Illinois 60484

Email: [email protected]

Jun Zhan, Ph.D.

Assistant Professor of Accounting

David Nazarian College of Business and Economics

Department of Accounting and Information Systems

California State University, Northridge

Phone: 818-677-4505

18111 Nordhoff Street

Northridge, CA 91330

Email: [email protected]

§ Corresponding author.

2

ANALYZE THIS, ANALYZE THAT: A REVERSING ENTRY CASE

INTRODUCTION

Analytical and problem solving skills are essential for not only forensic accountants but also

traditional accountants (Davis, Farrel, and Ogilby 2014). The American Institute of Certified

Public Accountants (AICPA) will in its tests increase focus on higher-order cognitive skills

starting April 1, 2017. Those skills include, but are not limited to, analytical ability, critical

thinking, problem solving, and professional skepticism, due to ongoing changes in the business

world and impacts on the accounting profession from advancements in technology (AICPA,

2015). It is therefore important and imperative for accounting educators to cultivate an interest in

learning among students, and grow their ability in analysis and problem-solving.

The AICPA will adopt the modified Bloom’s Taxonomy of Educational Objectives in

constructing its new tests in 2017. Based on the modified Bloom’s Taxonomy, there are four

categories of skill levels, namely, Remembering & Understanding, Application, Analysis, and

Evaluation. Currently, the AICPA incorporates Remembering & Understanding and Application

equally in each of its four sections of the CPA exam – auditing and attestation (AUD), business

environment and concepts (BEC), financial accounting and reporting (FAR), and regulation

(REG). In 2017, the AICPA will include 15~25% of analysis and 5~15% of evaluation in AUD,

20~30% of analysis in BEC, 25~35% of analysis in FAR, and 25~35% of analysis in REG,

according to its new blueprints (AICPA, 2015). Based on its new blueprints, the AICPA includes

the following key words (or verbs) in the representative task: (1) identify, recognize, understand,

explain, define, summarize, and recall (Remembering & Understanding), (2) apply, perform,

document, prepare, use, calculate, inquire, test, assist, describe, conduct, measure, determine, and

adjust (Application), (3) develop, analyze, compare, detect, interpret, reconcile, investigate,

review, and derive (Analysis), and (4) conclude, evaluate, observe, and verify (Evaluation).

This paper presents a case that can be used to enhance accounting students’ analytical and

problem solving skills. This case focuses on reversing entries and requires students to identify

and define the types/characteristics of year-end adjustments that are applicable and suitable for

reversing entries through deductive and inductive reasoning. By going through these two

approaches in finding the solution for this case, students will be exposed to fundamental

concepts in accounting at a different level, such as accruals and deferrals, year-end adjusting

entries, the process of closing, and changes of account balances at different stages of the

accounting cycle. Students need to integrate these concepts, understand their relationships, and

observe patterns of transactions along the process, in order to arrive at the solution. Students will

be going through all four levels of higher-order cognitive skills in this case, namely,

Remembering & Understanding, Application, Analysis, and Evaluation.

Although reversing entries may be discussed in introductory and/or intermediate accounting

courses, this case will be best implemented in senior or graduate/master level of accounting

courses subsequent to students’ mastery of accruals and deferrals involved in year-end

adjustments. However, educators are encouraged to apply this case in any way they think may fit.

3

We structure the case into three steps: Step 1-understanding reversing entries (remembering

& understanding); Step 2-applying deductive reasoning (remembering & understanding, apply,

and analysis); and Step 3-applying inductive reasoning (apply, analysis, and evaluate). In Step 1,

we help students understand the process of year-end adjusting entries and closing, and

application procedure of reversing entries. In Step 2, we help students understand different types

of year-end adjusting entries and applicability of reversing entries by requiring them to apply

their understanding of reversing entries acquired from Step 1. In Step 3, we require students to

identify and define the types of year-end adjusting entries that are applicable and suitable for

reversing entries by deriving patterns of entries based on their observations of the work obtained

from Step 2.

We strongly urge that educators instruct and guide students through each one of the steps.

We compose the case below in such a way so that educators can easily adopt the materials in

their classroom. In addition, we share some teaching notes to educators at the end of the paper.

STEP 1: UNDERSTANDING REVERSING ENTRIES

This case requires students to identify and define the types/characteristics of year-end journal

entries which can be used as reversing entries. In order to find the solution for this case, students

first need to understand the purpose of a reversing entry and how it works. Therefore, in the first

step we help students review the process of year-end adjusting entries and understand the

application of reversing entries. We adopt a common textbook example below to demonstrate

how a reversing entry works. Educators can add additional materials as needed.

Purpose of Reversing Entries

The purpose of reversing entries, as indicated in the textbooks, is to ease the process of

recording for some of the routinely occurred transactions that are involved in year-end adjusting

entries as if these adjusting entries had not taken place or as if the fiscal year-end had not

occurred (Kieso, Weygandt, and Warfield 2013; Scott 2013; Walther 2000, and Weygandt,

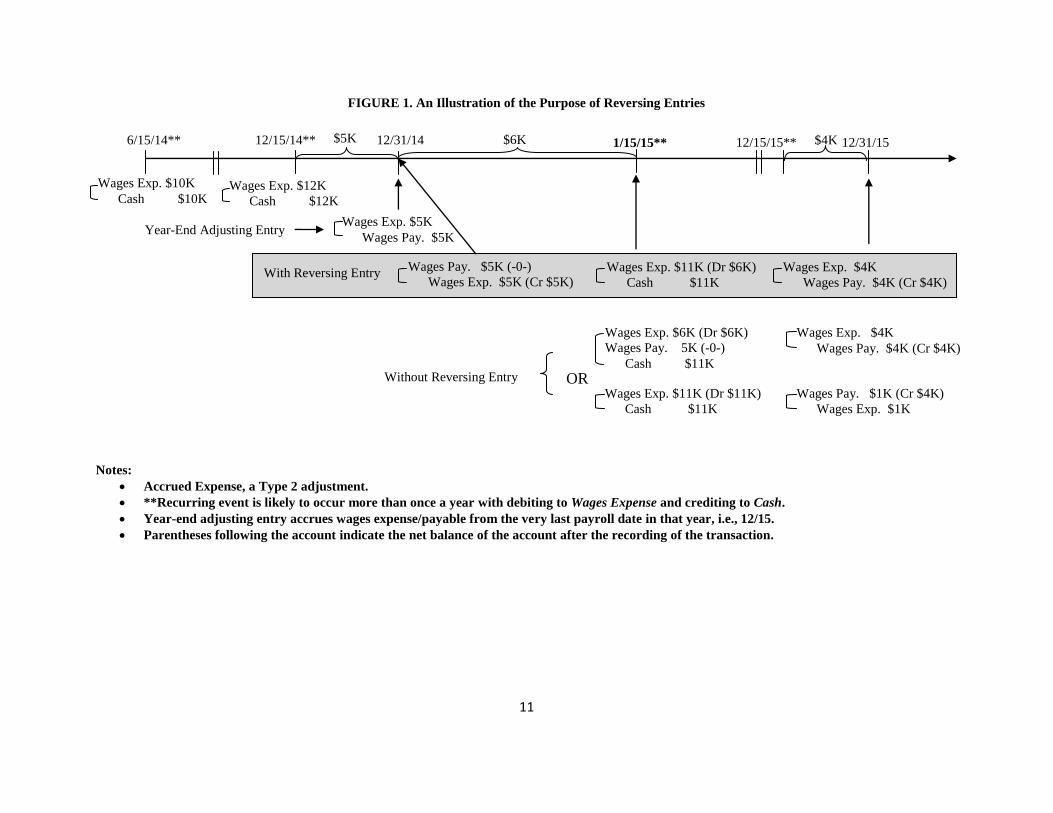

Kimmel and Kieso 2014). Figure 1 illustrates a commonly adopted example from the textbooks,

i.e., payroll transaction. In the example, the company processes and records its payroll on the

fifteenth of each month. The illustration shows that a routinely occurred monthly payroll

transaction involves a debit to Wages Expense and a credit to Cash with a monthly incurred

payroll amount (e.g., $10K for the month of May 15 – June 14 paid on June 15, $12K for

November 15 – December 14 paid on December 15, and $11K for December 15 – January 14

paid on January 15).

Since the fiscal year-end of the company is on December 31, 2014, the company accrues its

payroll from December 15 to December 31 in its year-end adjustments by debiting to Wages

Expense and crediting to Wages Payable for $5K. The Wages Expense account will be closed out

in the closing process at the year-end (i.e., to a zero balance in the account), leaving a credit

balance in the amount of $5K in the Wages Payable account before the beginning of the next

fiscal year, a new accounting cycle, assuming this is their first year of operations (i.e., there is no

prior balance in the account). Without making a reversing entry, the company will have Wages

4

Payable and Wages Expense accounts overstated in the system after they process and record their

payroll on January 15 until the year end in 2015 when they prepare and record year-end adjusting

entries, if they record the payroll transaction in the same way as in 2014. The company needs to

take into account the overstatements in these two accounts and the accrued payroll from

December 15 to December 31, instead of just the latter, when they make year-end adjustments in

the second year in 2015.

The company may make an adjustment to the recording of the payroll on January 15, 2015, if

they are able to, instead of just following their routine payroll entries, to offset the

overstatements in Wages Payable and Wages Expense accounts. For example, they can debit

Wages Expense for $6K and Wages Payable for $5K, and credit Cash for $11K. This way, the

overstatements in Wages Payable and Wages Expense are offset in the recurring transaction, and

the ending adjusting entry for the second year will follow the same routine; that is, to accrue for

the payroll from December 15 to December 31, 2015.

It will be more efficient and effective for the company to adopt the reversing entry process

right after they close the book and begin another new accounting cycle, especially when the

recording of payroll entries and year-end adjustments are performed by two different

departments/employees (i.e., making an adjustment to the payroll entry on January 15, 2015 is

not realistic). When the reversing entry procedure is followed, the overstatement in Wages

Payable will be offset and a reduction in Wages Expense equal to the amount that was accrued in

the year-end adjustment previously will be entered into the book at the beginning of a new cycle.

The Wages Expense account will end up with a correct amount equal to the wages accrued from

January 1 to January 14 when the payroll transaction is recorded as usual on January 15, 2015

(Figure 1). In addition, in the year-end adjustments of the second year, the company only needs

to accrue for the payroll that is accrued between their last payroll transaction and the end of the

fiscal year as they have done in 2014. They do not need to deal with any overstatements from the

beginning of the year in their year-end adjustments as indicated previously. As a result, it is

efficient and effective when we follow the procedure of recording reversing entries depicted in

this example.

Based on the illustration in Figure 1, we can help students recognize two necessary

conditions when reversing entries are applicable and suitable: (1) the recording of the

repeating/recurring entry stays the same way as previously, and (2) the recording of the fiscal

year-end adjusting entry in the subsequent year stays the same way as previously as well. Both

conditions are required if a reversing entry is to be applicable.

STEP 2: APPLYING DEDUCTIVE REASONING (ANALYZE THIS)

Only year-end adjusting entries are subject to reversing entries, but not all of them are

applicable and suitable for reversing entries. In order to identify and define types/characteristics

of these year-end adjusting entries that are applicable for reversing entries, students need to

understand all types of year-end adjusting entries to begin with. Thus, in this step we require

students to get familiar with all types of year-end adjusting entries by following a deductive

reasoning approach. That is, we work from a general rule (applicability of reversing entries from

5

Step 1) to a more specific knowledge/situation (several year-end adjusting entries, e.g., supplies,

A/R, etc.).

We will help students review the year-end adjusting entries first.

Types of Year-End Adjusting Entries

Basically, there are seven possible types of year-end adjusting entries as follows:

1) Accrued Revenue (recognition before cash flows):

In a simple form, it means that revenue is recognized before cash is received. Revenues

such as interests, rental, etc. are examples of accounts that will be accrued in the year-

end adjustments.

2) Accrued Expense (recognition before cash flows):

In a simple form, it means that expense is recognized before cash is paid. Expenses

such as interests, rental, utilities, payroll, etc. are examples of accounts that will be

accrued in the year-end adjustments.

3) Deferred Revenue (recognition after cash flows):

In a simple form, it means that cash for a revenue account is received before the

company performs and completes the revenue event (e.g., delivering the products or

providing the services). Deposits/advances from customers or tenants are examples of

revenues that will be deferred in the year-end adjustments.

4) Deferred Expense (recognition after cash flows):

In a simple form, it means that cash for an expense is paid before the company uses it.

Deposits or prepayments made by the company to utility/insurance companies or

landlords are examples of expenses that will be deferred in the year-end adjustments.

5) Changes in Estimates/Asset Valuation Adjustments/Expirations:

There are estimates used for fixed and other assets (e.g., number of useful years,

salvage value, etc.). The company may change estimates on the recording of

depreciation, amortization, and depletion, as well as accounts receivable/bad debt.

There are also asset valuation adjustments (Baskerville 2011) made to reflect values of

assets according to GAAP (e.g., supplies, accounts receivable, inventory, fair value

reporting). In addition, there are expirations on certain assets and liabilities

(FinanceReading.com), such as expirations on unearned revenues, prepaid

insurance/rent, depreciation on assets, etc. All the changes/adjustments/expirations will

result in year-end adjustments. These definitions may be overlapping and are not

mutually exclusive.

6) Changes in Principle:

The company may want to change its way of recording inventory (e.g., average cost to

LIFO) and/or revenues from long-term contracts (e.g., completed-contract to

percentage-of-completion). Thus the company needs to make an adjusting entry at the

year-end.

7) Corrections of Errors

The company also needs to correct any errors in reporting in its year-end adjustments.

6

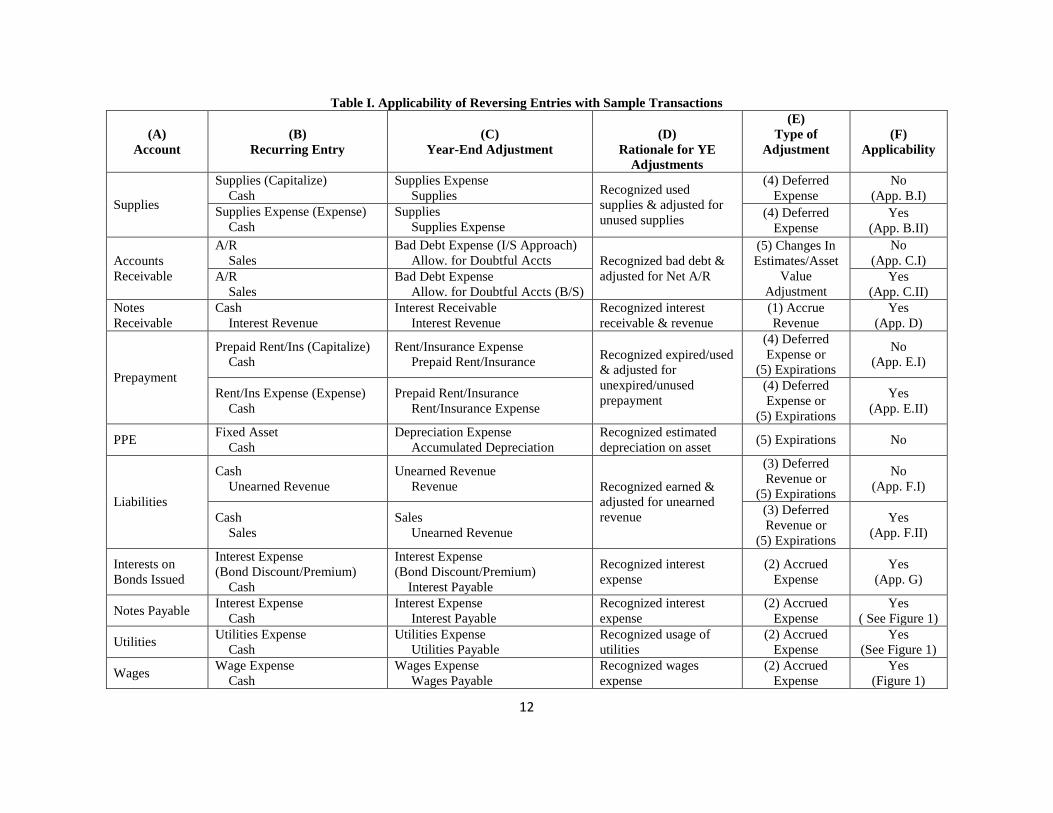

Table I shows a sample list of adjusting entries that accounting students learned from

intermediate accounting courses. Along with each account (column A), recurring entry (column

B), and year-end adjustment (column C), Table I also provides rationale (column D), type of

adjustments (column E), and applicability of a reversing entry (column F). Students will first

apply their general understanding of reversing entries to these year-end adjusting entries by

filling out columns B-F. Table I contains suggested answers from the authors. Educators will

need to decide on how much to reveal to students. Students need to come up with the recurring

entries, year-end adjusting entries, rationale for year-end adjustments, type of each year-end

adjusting entry, and applicability of reversing entries. Students should be encouraged to create

work as shown in Figure 1 for each year-end adjustment.

STEP 3: APPLYING INDUCTIVE REASONING (ANALYZE THAT)

As of the end of Step 2, students should have a comprehensive understanding of the concepts

such as accruals and deferrals, types of adjusting entries, the processes of year-end adjusting

entries and closing, and application of reversing entries. However, students may not be able to

come up with the types/characteristics of year-end adjusting entries for reversing entries yet, i.e.,

the solution of the case, even though they have recognized some entries that are applicable and

others that are not applicable in Table I from Step 2. Therefore, students will work from specific

observations to a broader generalization and theory in this step, that is, apply inductive reasoning.

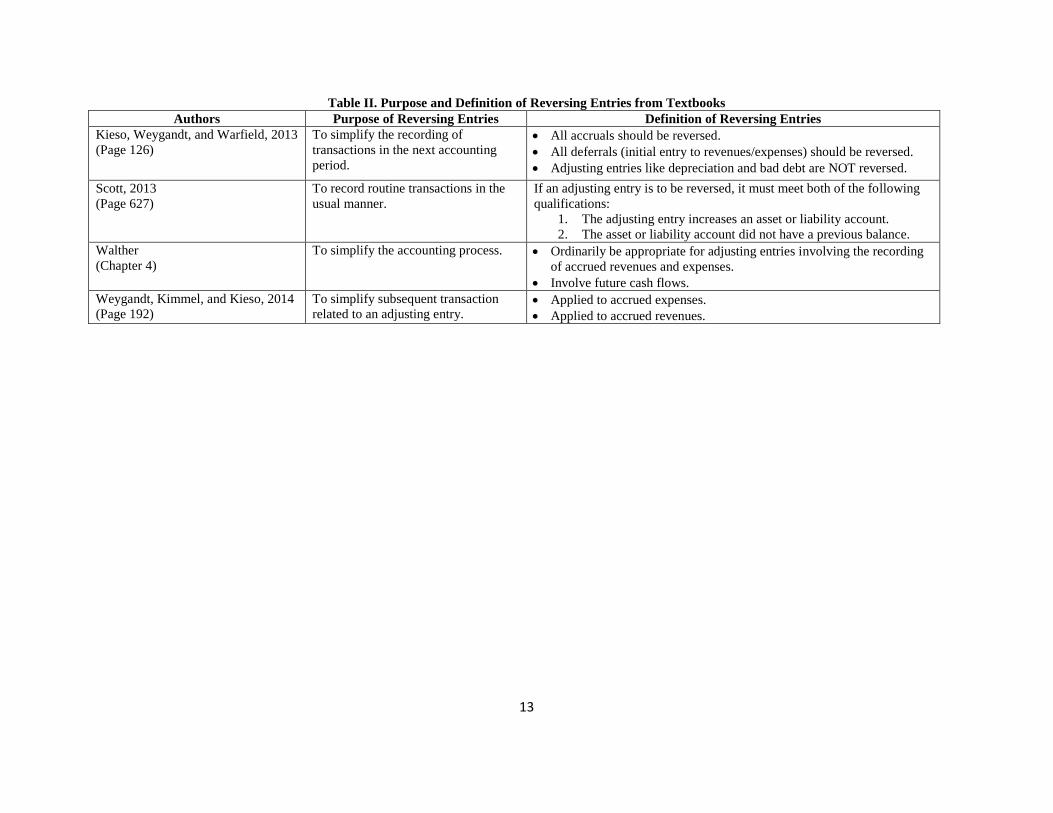

We will ask students to apply definitions of reversing entries from the textbooks to their

work in Table I. Table II provides a list of definitions for reversing entries from the textbooks.

Educators should remind students that definitions from textbooks may not be completely

applicable, and that they need to know the reasons why these definitions are and are not

applicable.

We will then require students to come up with their own definition for the application of

reversing entry by summarizing their observations of the patterns of transactions from sample

transactions in Table I. Students may detect and derive patterns such as the frequency and type of

recurring entry, the basis of its recurring, the frequency of recurring, types of year-end adjusting

entries, whether cash flow is involved, etc., along with the applicability of reversing entry.

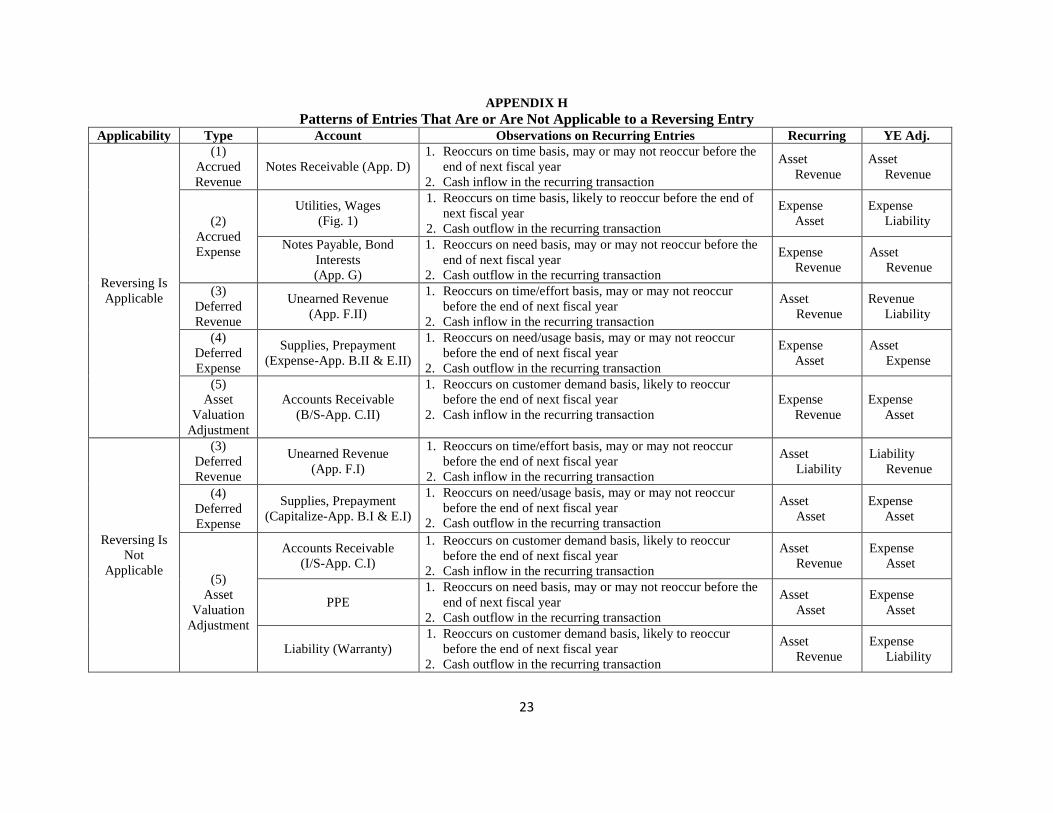

Appendix H shows an example of patterns in which observations can be gathered together based

on (1) if reversing entry is applicable and (2) type of adjusting entry. Students may point out

different patterns/categories and gather things differently, which is perfectly alright.

Students need to find a solution for the case. They should be motivated to create a list of

conditions/findings based on their analysis from Steps 2 and 3. They should also be encouraged

to discuss and debate with others about their findings. Educators can use the list of findings that

we provide here to guide students.

7

CONCLUDING REMARKS

The accounting profession has called for more high-order cognitive skills on its workforces

due to ongoing changes in the business world and advancements in technology. As a result, the

AICPA will be incorporating more questions requiring high-order skills in it examination in

2017. This case focuses more on advanced tasks involving high-order skills such as application,

analysis, and evaluation. It will help students develop high-order skills and give them an

opportunity to integrate their knowledge of the accounting cycle.

Recording reversing entries is an optional procedure in the accounting cycle. Yet we believe

this procedure has non-trivial educational values to accounting students due to its close

relationship with year-end adjusting entries. By going through two different analyses, i.e.,

deductive and inductive reasoning, in order to identify and define the types/characteristics of

year-end adjusting entries for reversing entries, students will get a chance to improve their

analytical and problem-solving skills along with the opportunity to integrate their understanding

of the concepts of accruals and deferrals, types of adjusting entries, the processes of year-end

adjusting entries and closing, and application of reversing entries.

The optimal timing for covering the case will be at the topic of accounting changes and errors

in an intermediate accounting course or at a master-level financial accounting course. A team

project will also be ideal because it provides a cooperative learning environment to students. We

took a survey from a small group of graduate accounting students after administering the case

and found that 39 percent of the correspondents regard this case easy to follow, 61 percent

indicate they enjoy doing this exercise, and 93 percent believe this exercise strengthens their

understanding of accounting concepts. We share our experience and provide tasks and objectives

of each step in the Teaching Notes below.

8

TEACHING NOTES

The following are some suggestions for implementing this case in the classroom. We will go over

them step by step and then provide suggested solution for the case.

STEP 1: Understanding Reversing Entries

Higher-Order Skills Involved

Remembering &

Understanding Understand Recall Recognize

In this step, students will understand the purpose of reversing entries and how it is applicable.

Students should realize that two conditions must exist when revering entries are applicable and suitable,

such as (1) the recording of the repeating/recurring entry stays the same way as previously recorded and

(2) the recording of the fiscal year-end adjusting entry in the subsequent year stays the same way as

previously recorded as well.

The objective for this step is:

to help students remember and understand how reversing entries work in the wages example

(Figure 1), which involves with the following:

1. recalling and understanding how a payroll transaction is recorded,

2. recalling and understanding how the year-end adjusting entry works for the wages example,

3. recalling and understanding how the year-end closing works for the wages example, and

4. recognizing the two conditions determining whether reversing entries are applicable or not in

the wages example.

STEP 2: Applying Deductive Reasoning (Analyze This)

Higher-Order Skills Involved

Evaluation Verify

Analysis Detect Determine

Application Apply Perform

Remembering and

Understanding Understand Recall Recognize

In this step, students will enhance their understanding of reversing entries by applying their

knowledge of reversing entries obtained from Step 1 to several year-end adjusting entries which they have

acquired from previous courses.

Instructors can provide a few initial/recurring entries to students in order to help them start the project.

Instructors can demonstrate that there may be different ways to record initial/recurring entries, e.g.,

capitalize versus expense, and different estimation methods for the year-end adjustments, e.g., Income

Statement versus Balance Sheet. As a result, students may come up with different year-end adjusting

entries, rationales, types of adjustment, and/or applicability of reversing entry. Students may or may not

remember what/how year-end adjustments should be made, but instructors may provide hints or reveal

more examples.

In order to enhance their understanding of the concepts of accruals and deferrals, students need to be

reminded to follow the classifications of types of year-end adjusting entries, i.e., Accrued Revenue,

9

Accrued Expense, Deferred Revenue, Deferred Expense, etc. Students may need to be aware of possible

overlapping classifications.

Students do not have to create diagrams exactly like those shown in the figures in this case. They

should be encouraged to create their own diagrams or tables. They should be required to

demonstrate/document on how they come up with their decisions, i.e. their reasoning.

The objective of this step is

to provide students an opportunity to apply their understanding of the applicability of reversing

entries acquired previously to several other accounts, which involves with the following:

1. understanding different types of year-end adjusting entries, such as accruals and deferrals,

etc.

2. recalling a recurring entry for each account, and its related year-end adjusting entry (Table I),

3. recognizing its rationale for the adjustment and type of year-end adjustment made previously

(Table I),

4. performing and documenting their work as shown in the figures in the paper for each

account,

5. detecting and determining if a reversing entry is applicable or not under each account, and

6. verifying their work in terms of the decision they made in the previous task above in 4.

STEP 3: Applying Inductive Reasoning (Analyze That)

Higher-Order Skills Involved

Evaluation Observe Evaluate Conclude

Analysis Develop Analyze Compare

Application Apply

In this step, students will have an opportunity to enhance their high-order skills, such as application,

analysis and evaluation. Students will first apply definitions of reversing entries from textbooks (and may

need to reconcile for the differences), and then develop a way for comparison and evaluation of their

work before they can make a conclusion.

The objective of this step is

to give students an opportunity to first integrate their understanding of reversing entry within the

accounting cycle and then develop high-order skills, which involves the following:

1. applying and reconciling the definitions of reversing entry from the textbooks to their work

in Table I,

2. observing the patterns of their work from diagrams and Table I and developing a way to

organize them for comparison below,

3. comparing and analyzing the patterns from the above, and

4. concluding the findings based on their work above.

Suggested Solution-Applicability of Reversing Entry

Based on their observations from Step 3, students may conclude that reversing entries are applicable

when the year-end adjustments are accrued revenues and accrued expenses, i.e., Type 1 and Type 2

adjustments (Notes Receivable, Notes Payable, Utilities, and Wages). Students may also conclude that

reversing entries under certain circumstances will be applicable for deferred revenues and deferred

expenses, i.e., Type 3 and Type 4 adjustments, especially when the recurring entries of the related year-

end adjustments involve revenue/expense account (Unearned Revenue, Supplies, and Prepayment).

10

Students should be encouraged to look into the reasons and circumstances of the applicability of reversing

entries.

In sum, reversing entries will be applicable and suitable for those year-end adjustments which

interrupt the recognition cycle of the revenue or expense recorded at recurring entries. If the company

records, in recurring entries before the fiscal year-end, revenue after its earning process (i.e., earned)

when they received cash or expense after its consumption when they paid, applying reversing entries will

undo the interruption on the recognition cycle from the year-end adjustments, such as accrued revenues

and accrued expenses. If the company records, in recurring entries before the fiscal year-end, revenue

before the completion of its earning process or expense before it fully uses up the service/resource,

applying reversing entries will also undo the interruption on the recognition cycle from the year-end

adjustments such as deferred revenue and deferred expense. However, if the company records

asset/liability in the recurring entry, i.e., capitalization method, for deferred revenues or deferred expenses,

the year-end adjustments will complete the recognition cycle for the revenue or expense. As a result,

reversing entries are not applicable because applying reversing entries in these cases will undo the

recognition cycle of revenues and expenses from the previous period.

11

FIGURE 1. An Illustration of the Purpose of Reversing Entries

Notes:

Accrued Expense, a Type 2 adjustment.

**Recurring event is likely to occur more than once a year with debiting to Wages Expense and crediting to Cash.

Year-end adjusting entry accrues wages expense/payable from the very last payroll date in that year, i.e., 12/15.

Parentheses following the account indicate the net balance of the account after the recording of the transaction.

Wages Exp. $10K

Cash $10K

6/15/14** 12/15/14**

Wages Exp. $12K

Cash $12K

Wages Exp. $5K

Wages Pay. $5K

Wages Exp. $11K (Dr $11K)

Cash $11K

1/15/15** 12/31/14 12/31/15

Wages Pay. $1K (Cr $4K)

Wages Exp. $1K

$5K 12/15/15** $4K

Without Reversing Entry

Wages Pay. $5K (-0-)

Wages Exp. $5K (Cr $5K) Wages Exp. $4K

Wages Pay. $4K (Cr $4K) With Reversing Entry

Year-End Adjusting Entry

Wages Exp. $6K (Dr $6K)

Wages Pay. 5K (-0-)

Cash $11K

OR

Wages Exp. $4K

Wages Pay. $4K (Cr $4K)

Wages Exp. $11K (Dr $6K)

Cash $11K

$6K

12

Table I. Applicability of Reversing Entries with Sample Transactions

(A)

Account

(B)

Recurring Entry

(C)

Year-End Adjustment

(D)

Rationale for YE

Adjustments

(E)

Type of

Adjustment

(F)

Applicability

Supplies

Supplies (Capitalize)

Cash

Supplies Expense

Supplies Recognized used

supplies & adjusted for

unused supplies

(4) Deferred

Expense

No

(App. B.I)

Supplies Expense (Expense)

Cash

Supplies

Supplies Expense (4) Deferred

Expense

Yes

(App. B.II)

Accounts

Receivable

A/R

Sales

Bad Debt Expense (I/S Approach)

Allow. for Doubtful Accts Recognized bad debt &

adjusted for Net A/R

(5) Changes In

Estimates/Asset

Value

Adjustment

No

(App. C.I)

A/R

Sales

Bad Debt Expense

Allow. for Doubtful Accts (B/S)

Yes

(App. C.II)

Notes

Receivable

Cash

Interest Revenue

Interest Receivable

Interest Revenue

Recognized interest

receivable & revenue

(1) Accrue

Revenue

Yes

(App. D)

Prepayment

Prepaid Rent/Ins (Capitalize)

Cash

Rent/Insurance Expense

Prepaid Rent/Insurance Recognized expired/used

& adjusted for

unexpired/unused

prepayment

(4) Deferred

Expense or

(5) Expirations

No

(App. E.I)

Rent/Ins Expense (Expense)

Cash

Prepaid Rent/Insurance

Rent/Insurance Expense

(4) Deferred

Expense or

(5) Expirations

Yes

(App. E.II)

PPE Fixed Asset

Cash

Depreciation Expense

Accumulated Depreciation

Recognized estimated

depreciation on asset (5) Expirations No

Liabilities

Cash

Unearned Revenue

Unearned Revenue

Revenue Recognized earned &

adjusted for unearned

revenue

(3) Deferred

Revenue or

(5) Expirations

No

(App. F.I)

Cash

Sales

Sales

Unearned Revenue

(3) Deferred

Revenue or

(5) Expirations

Yes

(App. F.II)

Interests on

Bonds Issued

Interest Expense

(Bond Discount/Premium)

Cash

Interest Expense

(Bond Discount/Premium)

Interest Payable

Recognized interest

expense

(2) Accrued

Expense

Yes

(App. G)

Notes Payable Interest Expense

Cash

Interest Expense

Interest Payable

Recognized interest

expense

(2) Accrued

Expense

Yes

( See Figure 1)

Utilities Utilities Expense

Cash

Utilities Expense

Utilities Payable

Recognized usage of

utilities

(2) Accrued

Expense

Yes

(See Figure 1)

Wages Wage Expense

Cash

Wages Expense

Wages Payable

Recognized wages

expense

(2) Accrued

Expense

Yes

(Figure 1)

13

Table II. Purpose and Definition of Reversing Entries from Textbooks

Authors Purpose of Reversing Entries Definition of Reversing Entries

Kieso, Weygandt, and Warfield, 2013

(Page 126)

To simplify the recording of

transactions in the next accounting

period.

All accruals should be reversed.

All deferrals (initial entry to revenues/expenses) should be reversed.

Adjusting entries like depreciation and bad debt are NOT reversed.

Scott, 2013

(Page 627)

To record routine transactions in the

usual manner.

If an adjusting entry is to be reversed, it must meet both of the following

qualifications:

1. The adjusting entry increases an asset or liability account.

2. The asset or liability account did not have a previous balance.

Walther

(Chapter 4)

To simplify the accounting process. Ordinarily be appropriate for adjusting entries involving the recording

of accrued revenues and expenses.

Involve future cash flows.

Weygandt, Kimmel, and Kieso, 2014

(Page 192)

To simplify subsequent transaction

related to an adjusting entry. Applied to accrued expenses.

Applied to accrued revenues.

14

REFERENCES

American Institute of Certified Public Accountants. 2015. “Exposure Draft: Maintaining the

Relevance of the Uniform CPA Examination”

Baskerville, Peter. http://www.saylor.org/site/wp-content/uploads/2011/12/BUS103-

ENDOFPERIODADJUSTMENTS.pdf

Davis, Charles, Ramona Farrell, and Suzanne Ogilby. 2009. Characteristic and Skills of the

Forensic Accountant. American Institute of Certified Public Accountants.

Financereading.com, http://financereading.com/types_of_accounting_adjustments.htm.

Kieso, Donald E., Jerry J. Weygandt, and Terry D. Warfield. 2013. “Intermediate Accounting”,

15th

edition, Wiley.

Scott, Cathy J. 2013. “College Accounting: A Career Approach”, 12th

edition, Cengage Learning.

Walther, Larry M. 2010. “Financial Accounting: Principles of Accounting.com”, CreateSpace

Independent Publishing Platform.

Weygandt, Jerry J., Paul D. Kimmel, and Donald E. Kieso. 2014. “Financial Accounting”, 9th

edition, Wiley.

15

APPENDIX A

Supplement of Sample Year-End Adjusting Entries

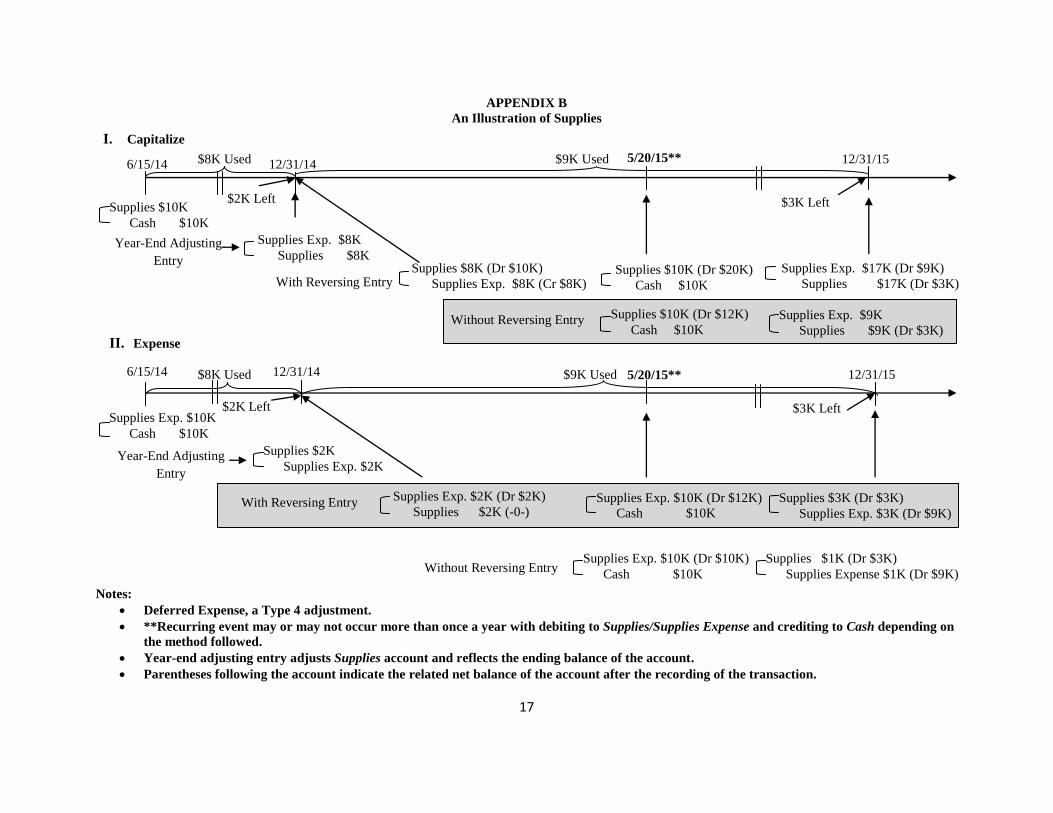

Supplies (see Appendix B)

Appendix B shows two illustrations involving supplies. There are two ways to record supplies, i.e.,

Capitalization or Expense method. In Appendix B.I, we can see that the original entry is a debit to an asset, i.e.,

Supplies, following the capitalizing method, and in Appendix B.II a debit to an expense, i.e., Supplies Expense,

following the expensing method. Both are Type 4 year-end adjustment—Deferred Expense because cash is paid for

an expense before the company uses it.

In the example, there are $8K of supplies used in 2014 and $2K of supplies left at the end of 12/31/14, and $9K

of supplies used in 2015 and $3K left at the end of 12/31/15. Under the capitalization method as shown in Appendix

B.I, we will record (1) the purchase of supplies by debiting Supplies and crediting Cash with the amount purchased,

and (2) the total use of supplies (i.e., $8K) in 2014 by debiting Supplies Expense and crediting Supplies in the year-

end adjustment on 12/31/2014. The Supplies Expense account will be closed in the closing process, leaving $2K of

supplies in the Supplies account after the closing. If reversing entries will be applicable and suitable, these two

conditions must be met. Otherwise, reversing entries will not be applicable.

The diagram in Appendix B.I, i.e., the capitalization method, shows that these two conditions are not met with a

reversing entry but they are met without a reversing entry. Although the recording stays the same for the purchase

on 5/20/15 as on 6/15/14 with a reversing entry, but the recording for the year-end adjustment on 12/31/15 differs

than the one on 12/31/14 since it needs to count for the usage in 2014, the previous year. As a result, reversing

entries are not applicable in this case. However, these two conditions are met with a reversing entry when we follow

the expense method, as shown in Appendix B.II.

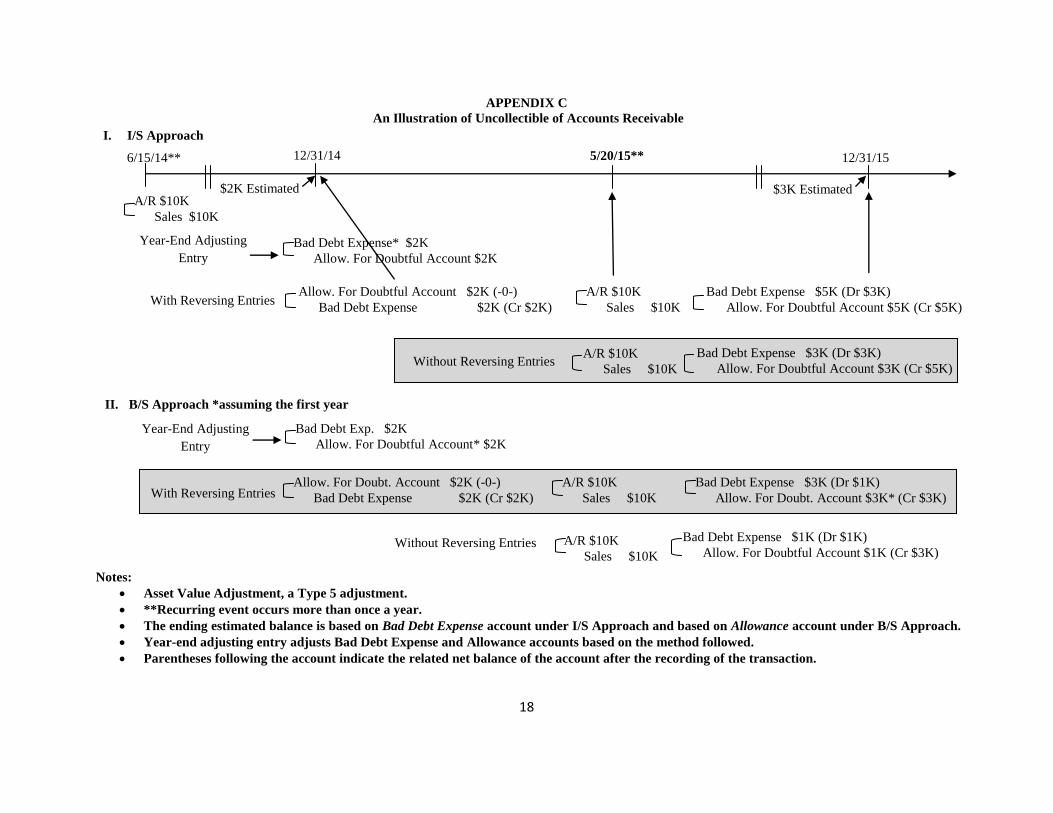

Accounts Receivable (see Appendix C)

When we record a sale with Accounts Receivable, we accrue the revenue. As collections for these receivables

are made, we offset the accrual of revenues. We will then estimate uncollectible in the year-end adjustments. For the

purpose of this article, the estimate for the uncollectible will be classified as adjustments to asset value, i.e., a Type 5

adjustment—Asset Valuation Adjustment. There are two ways to estimate the uncollectible, i.e., the Income

Statement and Balance Sheet method.

As shown in Appendix C.I, i.e., the Income Statement approach, we don’t need a reversing entry because the

two conditions (same recording for the recurring and year-end adjustment) are not met. If we record a reversing

entry, it will require an additional calculation for the amount of bad debt expense (i.e., adding the estimates from the

previous years).

However, we will benefit from the reversing entry procedure when we adopt the Balance Sheet method as

shown in Appendix B.II. After we record the reversing entry, i.e., debiting Allowance for Doubtful Account and

crediting Bad Debt Expense, we can just record the same year-end adjusting entry for the Allowance with the

estimate from the Accounts Receivable on both 12/31/14 and 12/31/15 in the example (assuming the estimate is $3K

at the end of 2015), as well as the recurring entry on 5/20/2015. If we don’t make a reversing entry, we will need to

perform an additional calculation for the Allowance account, i.e., subtract the previous balance in the Allowance

account from the current estimate.

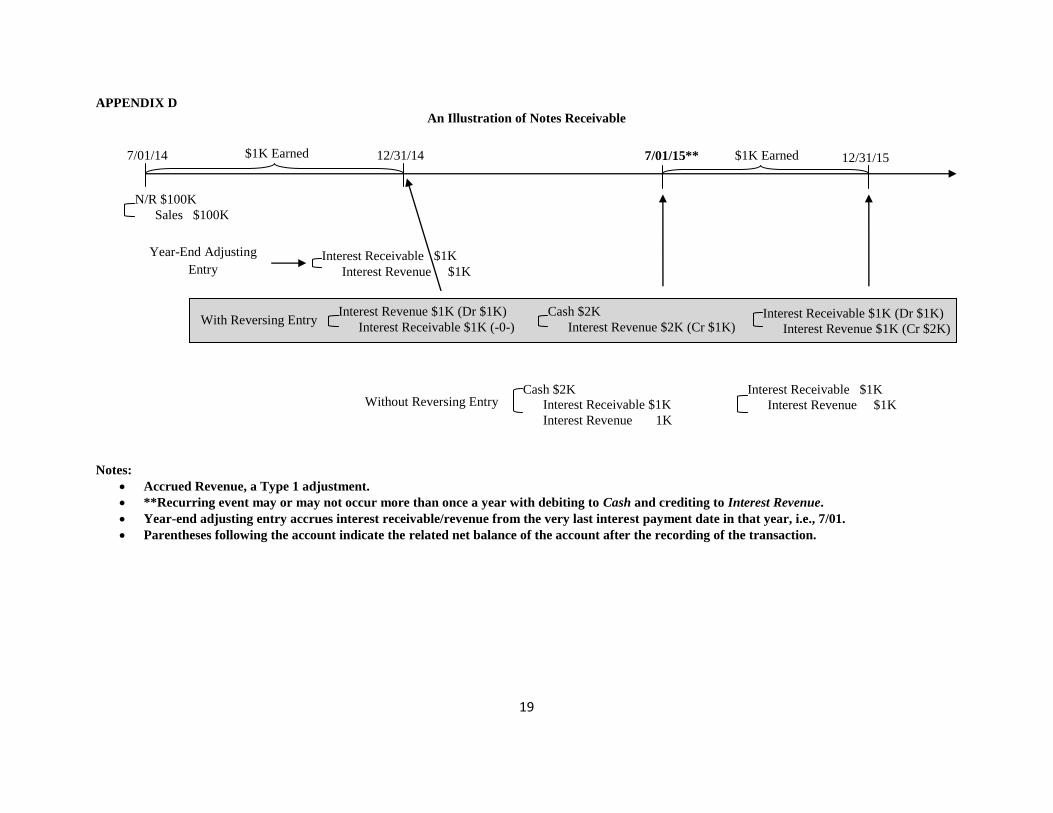

Notes Receivable (see Appendix D)

The adjustment for accruing interests on notes receivable is a Type 1 adjustment—Accrued Revenue, as shown

in Appendix D. The diagram shows that the two conditions are met with a revering entry. We will ease the recording

for the interest on notes receivable when we follow the reversing entry procedure. We can record the same entries

for the receipt of cash, i.e., the recurring entry, as well as the year-end adjustment, i.e., accruing the interest for the

period from the last receipt of payment to the end of the year. However, we will need to make an adjustment to the

16

recurring entry (to Interest Receivable and Interest Revenue accounts) when we receive the interest payment if we

do not make the reversing entry.

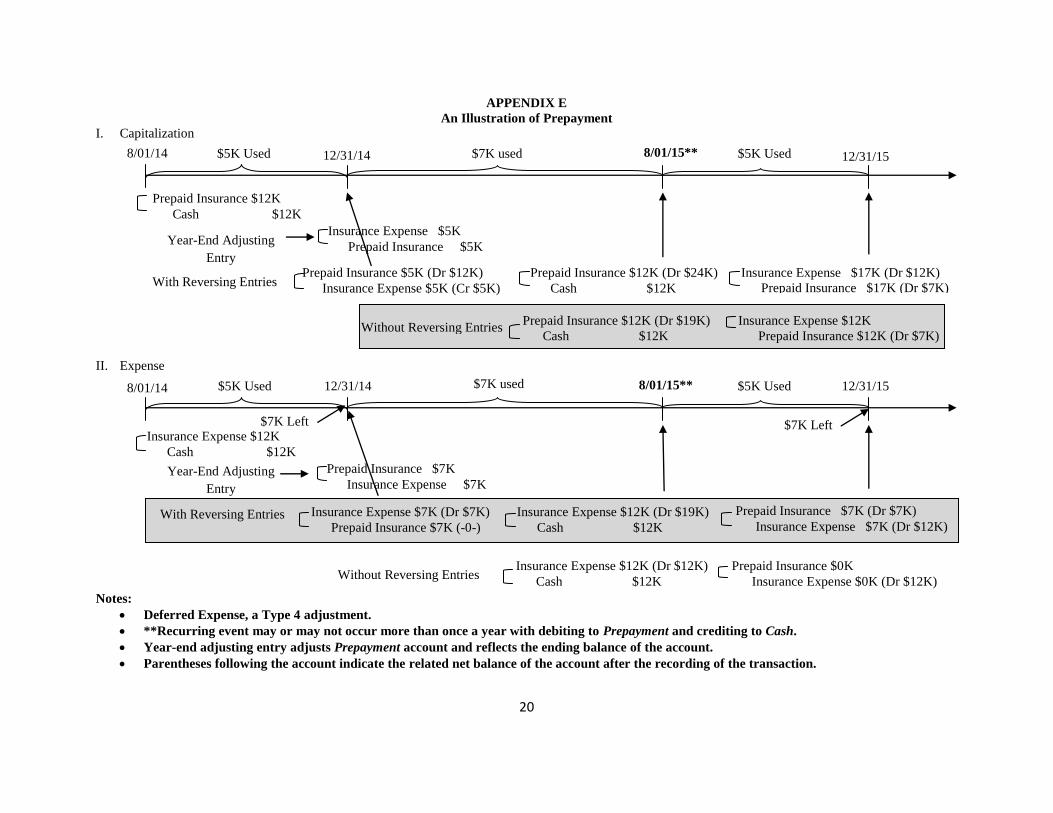

Prepayment (see Appendix E)

The adjustment for prepayment is a Type 4 adjustment—Deferred Expense, as shown in Appendix E. The

illustrations show that reversing entries will not be applicable under the Capitalization method but will be applicable

under the Expense method. The illustration in Appendix E.I, the Capitalization method, shows that we will need to

recognize and adjust for the amount of expired insurance, i.e., Insurance Expense and Prepaid Insurance, in the

year-end adjustment regardless of whether we will adopt the reversing entry procedure or not later on. However, in

the subsequent year the calculation of the amount of expired insurance will need to go back to the original amount of

the prepayment from the previous period if we adopt the reversing entry procedure (i.e., $12K + $12K - $5K in the

example). As a result, following a reversing entry in this case will not achieve the two conditions.

On the other hand, the illustration in Appendix E.II, i.e., Expense method, shows that we will meet the two

conditions when we adopt a reversing entry. In this case, we need to recognize and adjust for the amount of unused

insurance, i.e., Prepaid Insurance and Insurance Expense, in the year-end adjustment. By following a reversing

entry, we will be recording the recurring entry and year-end adjusting entry the same way for all years.

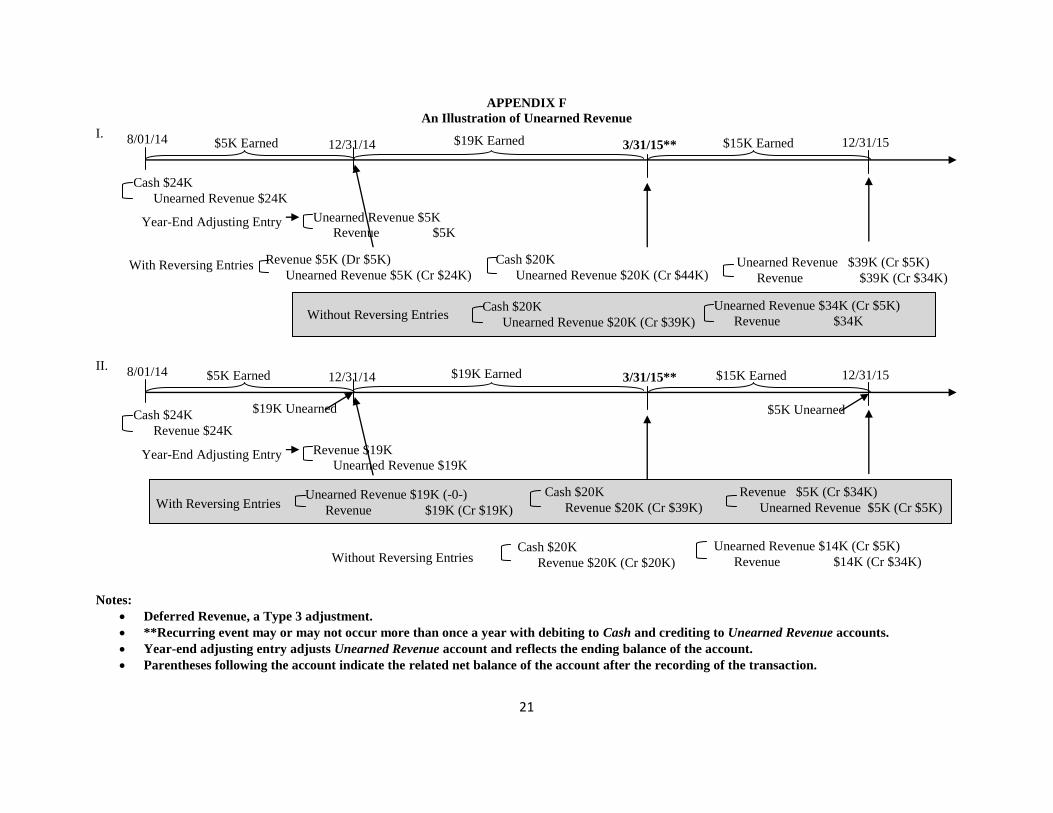

Liabilities (see Appendix F)

The adjustment for unearned revenue is a Type 3 adjustment—Deferral Revenue. There are two ways to record

this unearned revenue. We can record the receipt of cash as unearned revenue and then adjust for the amount earned

in the year-end adjustment (Appendix F.I) or we can record the receipt of cash as revenue to begin with and then

adjust for the amount of unearned in the year-end adjustment (Appendix F.II). The illustrations show that reversing

entry will not be applicable when we record the receipt of cash as unearned revenue but will be applicable when we

record the receipt of cash as revenue in the recurring entry.

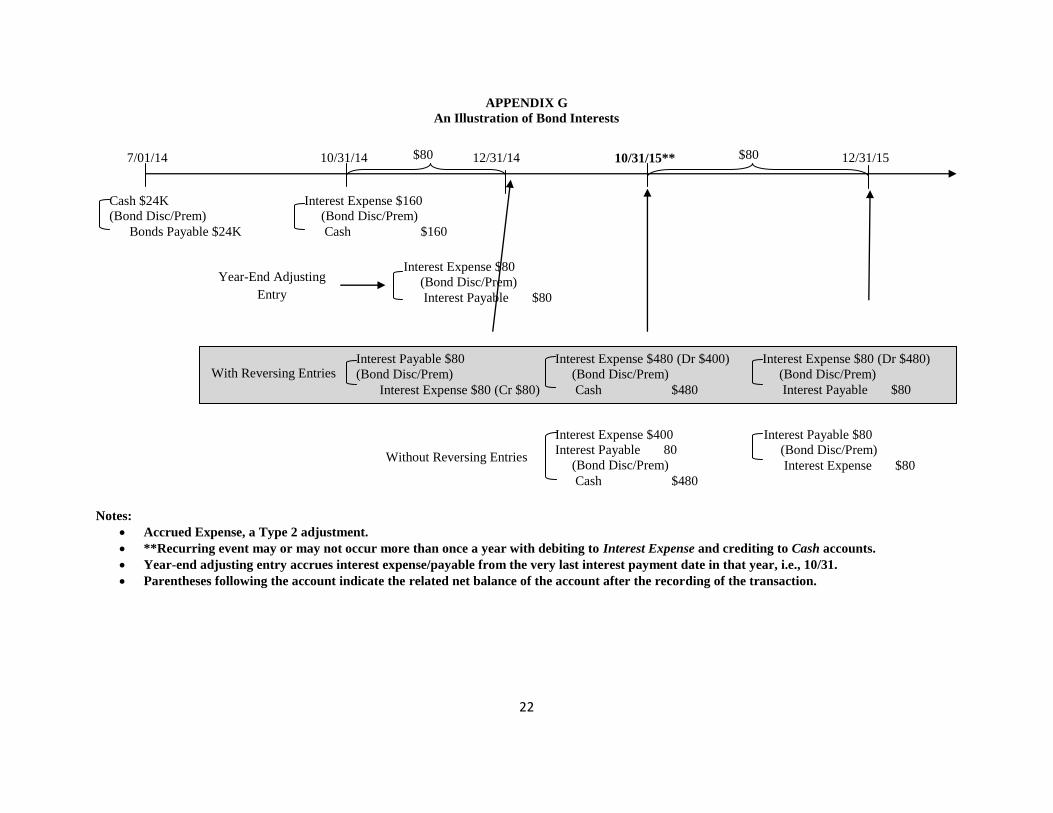

Interests on Bonds Issued (see Appendix G)

The adjustment for interest expense for bonds is a Type 2 adjustment—Accrued Expense. We will be meeting

the two conditions when we follow a reversing entry. With a reversing entry, we will record the same entries when

we make interest payments on the interest dates and the same entries when we record year-end adjustments. If we do

not follow with a reversing entry, however, we will make an adjustment to the entry when we pay the interest on the

interest dates.

17

APPENDIX B

An Illustration of Supplies

Notes:

Deferred Expense, a Type 4 adjustment.

**Recurring event may or may not occur more than once a year with debiting to Supplies/Supplies Expense and crediting to Cash depending on

the method followed.

Year-end adjusting entry adjusts Supplies account and reflects the ending balance of the account.

Parentheses following the account indicate the related net balance of the account after the recording of the transaction.

Supplies $10K

Cash $10K

6/15/14

Supplies Exp. $8K

Supplies $8K

Supplies $10K (Dr $12K)

Cash $10K

5/20/15** 12/31/14 12/31/15

Supplies Exp. $9K

Supplies $9K (Dr $3K)

$2K Left $3K Left

Without Reversing Entry

Supplies $8K (Dr $10K)

Supplies Exp. $8K (Cr $8K)

Supplies Exp. $17K (Dr $9K)

Supplies $17K (Dr $3K) With Reversing Entry

Year-End Adjusting

Entry

6/15/14 5/20/15** 12/31/14 12/31/15

Supplies Exp. $10K

Cash $10K

$2K Left $3K Left

Year-End Adjusting

Entry

Supplies $3K (Dr $3K)

Supplies Exp. $3K (Dr $9K)

Without Reversing Entry

Supplies Exp. $2K (Dr $2K)

Supplies $2K (-0-)

Supplies $1K (Dr $3K)

Supplies Expense $1K (Dr $9K)

With Reversing Entry

Supplies $2K

Supplies Exp. $2K

Supplies Exp. $10K (Dr $12K)

Cash $10K

$8K Used

$8K Used $9K Used

$9K Used

I. Capitalize

II. Expense

Supplies $10K (Dr $20K)

Cash $10K

Supplies Exp. $10K (Dr $10K)

Cash $10K

18

APPENDIX C

An Illustration of Uncollectible of Accounts Receivable

Notes:

Asset Value Adjustment, a Type 5 adjustment.

**Recurring event occurs more than once a year.

The ending estimated balance is based on Bad Debt Expense account under I/S Approach and based on Allowance account under B/S Approach.

Year-end adjusting entry adjusts Bad Debt Expense and Allowance accounts based on the method followed.

Parentheses following the account indicate the related net balance of the account after the recording of the transaction.

A/R $10K

Sales $10K

6/15/14**

Bad Debt Expense* $2K

Allow. For Doubtful Account $2K

A/R $10K

Sales $10K

5/20/15** 12/31/14 12/31/15

$2K Estimated $3K Estimated

Without Reversing Entries

Allow. For Doubtful Account $2K (-0-)

Bad Debt Expense $2K (Cr $2K) With Reversing Entries

Year-End Adjusting

Entry

I. I/S Approach

Bad Debt Expense $3K (Dr $3K)

Allow. For Doubtful Account $3K (Cr $5K)

Bad Debt Expense $5K (Dr $3K)

Allow. For Doubtful Account $5K (Cr $5K)

II. B/S Approach *assuming the first year

Bad Debt Exp. $2K

Allow. For Doubtful Account* $2K

Without Reversing Entries

Allow. For Doubt. Account $2K (-0-)

Bad Debt Expense $2K (Cr $2K) With Reversing Entries

Year-End Adjusting

Entry

Bad Debt Expense $1K (Dr $1K)

Allow. For Doubtful Account $1K (Cr $3K)

Bad Debt Expense $3K (Dr $1K)

Allow. For Doubt. Account $3K* (Cr $3K)

A/R $10K

Sales $10K

A/R $10K

Sales $10K

A/R $10K

Sales $10K

19

APPENDIX D

An Illustration of Notes Receivable

Notes:

Accrued Revenue, a Type 1 adjustment.

**Recurring event may or may not occur more than once a year with debiting to Cash and crediting to Interest Revenue.

Year-end adjusting entry accrues interest receivable/revenue from the very last interest payment date in that year, i.e., 7/01.

Parentheses following the account indicate the related net balance of the account after the recording of the transaction.

N/R $100K

Sales $100K

7/01/14

Interest Receivable $1K

Interest Revenue $1K

Cash $2K

Interest Receivable $1K

Interest Revenue 1K

7/01/15** 12/31/14 12/31/15

Without Reversing Entry

Interest Revenue $1K (Dr $1K)

Interest Receivable $1K (-0-) With Reversing Entry

Year-End Adjusting

Entry

Interest Receivable $1K (Dr $1K)

Interest Revenue $1K (Cr $2K)

Interest Receivable $1K

Interest Revenue $1K

Cash $2K

Interest Revenue $2K (Cr $1K)

$1K Earned $1K Earned

20

APPENDIX E

An Illustration of Prepayment

I. Capitalization

II. Expense

Notes:

Deferred Expense, a Type 4 adjustment.

**Recurring event may or may not occur more than once a year with debiting to Prepayment and crediting to Cash.

Year-end adjusting entry adjusts Prepayment account and reflects the ending balance of the account.

Parentheses following the account indicate the related net balance of the account after the recording of the transaction.

Prepaid Insurance $12K

Cash $12K

8/01/14

Insurance Expense $5K

Prepaid Insurance $5K

Prepaid Insurance $12K (Dr $19K)

Cash $12K

8/01/15** 12/31/14 12/31/15

Without Reversing Entries

Prepaid Insurance $5K (Dr $12K)

Insurance Expense $5K (Cr $5K) With Reversing Entries

Year-End Adjusting

Entry

Insurance Expense $12K

Prepaid Insurance $12K (Dr $7K)

Insurance Expense $17K (Dr $12K)

Prepaid Insurance $17K (Dr $7K)

Prepaid Insurance $12K (Dr $24K)

Cash $12K

$5K Used $7K used $5K Used

Insurance Expense $12K

Cash $12K

8/01/14

Prepaid Insurance $7K

Insurance Expense $7K

Insurance Expense $12K (Dr $12K)

Cash $12K

8/01/15** 12/31/14 12/31/15

Without Reversing Entries

Insurance Expense $7K (Dr $7K)

Prepaid Insurance $7K (-0-) With Reversing Entries

Year-End Adjusting

Entry

Prepaid Insurance $0K

Insurance Expense $0K (Dr $12K)

Prepaid Insurance $7K (Dr $7K)

Insurance Expense $7K (Dr $12K) Insurance Expense $12K (Dr $19K)

Cash $12K

$5K Used $7K used $5K Used

$7K Left $7K Left

21

APPENDIX F

An Illustration of Unearned Revenue

I.

II.

Notes:

Deferred Revenue, a Type 3 adjustment.

**Recurring event may or may not occur more than once a year with debiting to Cash and crediting to Unearned Revenue accounts.

Year-end adjusting entry adjusts Unearned Revenue account and reflects the ending balance of the account.

Parentheses following the account indicate the related net balance of the account after the recording of the transaction.

Cash $24K

Unearned Revenue $24K

8/01/14

Unearned Revenue $5K

Revenue $5K

12/31/14 12/31/15

Without Reversing Entries

Revenue $5K (Dr $5K)

Unearned Revenue $5K (Cr $24K) With Reversing Entries

Year-End Adjusting Entry

Unearned Revenue $34K (Cr $5K)

Revenue $34K

Unearned Revenue $39K (Cr $5K)

Revenue $39K (Cr $34K)

$5K Earned $19K Earned $15K Earned 3/31/15**

Cash $20K

Unearned Revenue $20K (Cr $39K)

Cash $20K

Unearned Revenue $20K (Cr $44K)

Cash $24K

Revenue $24K

8/01/14

Revenue $19K

Unearned Revenue $19K

12/31/14 12/31/15

Without Reversing Entries

Unearned Revenue $19K (-0-)

Revenue $19K (Cr $19K) With Reversing Entries

Year-End Adjusting Entry

Unearned Revenue $14K (Cr $5K)

Revenue $14K (Cr $34K)

Revenue $5K (Cr $34K)

Unearned Revenue $5K (Cr $5K)

$5K Earned $19K Earned $15K Earned 3/31/15**

Cash $20K

Revenue $20K (Cr $20K)

Cash $20K

Revenue $20K (Cr $39K)

$5K Unearned $19K Unearned

22

APPENDIX G

An Illustration of Bond Interests

Notes:

Accrued Expense, a Type 2 adjustment.

**Recurring event may or may not occur more than once a year with debiting to Interest Expense and crediting to Cash accounts.

Year-end adjusting entry accrues interest expense/payable from the very last interest payment date in that year, i.e., 10/31.

Parentheses following the account indicate the related net balance of the account after the recording of the transaction.

Cash $24K

(Bond Disc/Prem)

Bonds Payable $24K

7/01/14 12/31/14 12/31/15

Without Reversing Entries

Interest Payable $80

(Bond Disc/Prem)

Interest Expense $80 (Cr $80)

With Reversing Entries

Year-End Adjusting

Entry

Interest Expense $160

(Bond Disc/Prem)

Cash $160

10/31/14 10/31/15**

Interest Expense $400

Interest Payable 80

(Bond Disc/Prem)

Cash $480

Interest Expense $80

(Bond Disc/Prem)

Interest Payable $80

Interest Payable $80

(Bond Disc/Prem)

Interest Expense $80

Interest Expense $80 (Dr $480)

(Bond Disc/Prem)

Interest Payable $80

Interest Expense $480 (Dr $400)

(Bond Disc/Prem)

Cash $480

$80 $80

23

APPENDIX H

Patterns of Entries That Are or Are Not Applicable to a Reversing Entry Applicability Type Account Observations on Recurring Entries Recurring YE Adj.

Reversing Is

Applicable

(1)

Accrued

Revenue

Notes Receivable (App. D)

1. Reoccurs on time basis, may or may not reoccur before the

end of next fiscal year

2. Cash inflow in the recurring transaction

Asset

Revenue

Asset

Revenue

(2)

Accrued

Expense

Utilities, Wages

(Fig. 1)

1. Reoccurs on time basis, likely to reoccur before the end of

next fiscal year

2. Cash outflow in the recurring transaction

Expense

Asset

Expense

Liability

Notes Payable, Bond

Interests

(App. G)

1. Reoccurs on need basis, may or may not reoccur before the

end of next fiscal year

2. Cash outflow in the recurring transaction

Expense

Revenue

Asset

Revenue

(3)

Deferred

Revenue

Unearned Revenue

(App. F.II)

1. Reoccurs on time/effort basis, may or may not reoccur

before the end of next fiscal year

2. Cash inflow in the recurring transaction

Asset

Revenue

Revenue

Liability

(4)

Deferred

Expense

Supplies, Prepayment

(Expense-App. B.II & E.II)

1. Reoccurs on need/usage basis, may or may not reoccur

before the end of next fiscal year

2. Cash outflow in the recurring transaction

Expense

Asset

Asset

Expense

(5)

Asset

Valuation

Adjustment

Accounts Receivable

(B/S-App. C.II)

1. Reoccurs on customer demand basis, likely to reoccur

before the end of next fiscal year

2. Cash inflow in the recurring transaction

Expense

Revenue

Expense

Asset

Reversing Is

Not

Applicable

(3)

Deferred

Revenue

Unearned Revenue

(App. F.I)

1. Reoccurs on time/effort basis, may or may not reoccur

before the end of next fiscal year

2. Cash inflow in the recurring transaction

Asset

Liability

Liability

Revenue

(4)

Deferred

Expense

Supplies, Prepayment

(Capitalize-App. B.I & E.I)

1. Reoccurs on need/usage basis, may or may not reoccur

before the end of next fiscal year

2. Cash outflow in the recurring transaction

Asset

Asset

Expense

Asset

(5)

Asset

Valuation

Adjustment

Accounts Receivable

(I/S-App. C.I)

1. Reoccurs on customer demand basis, likely to reoccur

before the end of next fiscal year

2. Cash inflow in the recurring transaction

Asset

Revenue

Expense

Asset

PPE

1. Reoccurs on need basis, may or may not reoccur before the

end of next fiscal year

2. Cash outflow in the recurring transaction

Asset

Asset

Expense

Asset

Liability (Warranty)

1. Reoccurs on customer demand basis, likely to reoccur

before the end of next fiscal year

2. Cash outflow in the recurring transaction

Asset

Revenue

Expense

Liability