annual report 2007 - | nbb.be

TRANSCRIPT

Report 2007Corporate Report

© National Bank of Belgium

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

Foreword 5

Guy Quaden

Governor

The Bank’s report on its activities has undergone a radical revision for this 2007 edition, and its presentation has been modernised. The content focuses on the main events of the past fi nancial year and, on this occasion, on two important aspects of the life of the institution : human resources management and the sustainable development policy.

This is the report on a company whose special character was confi rmed once again by a ruling handed down on 9 March 2007 by the Brussels Commercial Court : “the tasks entrusted to the National Bank of Belgium in the general interest and for the public economic benefi t (…) have made the Bank a special legal entity obeying its own specifi c rules”. The special status of the Bank as the central bank of Belgium, and a member of the Eurosystem, is spelt out in its governance statement.

In 2007, the Bank developed a number of projects with a European dimension in various areas of activity. These projects form part of the process which is gradually establishing a new way of working within the Eurosystem, with closer cooperation between the various central banks and efforts to achieve economies of scale.

Outside the Eurosystem, the Bank also performs a range of services for the Belgian economy. That work consists mainly in collecting and analysing macroeconomic and microeconomic data, and managing the payment and securities settlement systems.

Thus, the Central Balance Sheet Offi ce, which celebrates its thirtieth anniversary in 2008, collects the annual accounts of most enterprises active in Belgium. The compilation and publication of standardised annual accounts was designed as a tool for corporate management, communication with the public, staff information, and protection of the rights of third parties. The easing of the burden on businesses is a laudable aim which the Bank supports and promotes, for instance by improving its statistics collection procedures and by simplifying the fi ling of annual accounts. However, this must not lead to any deterioration in the quality and availability of corporate fi nancial information.

FOREWORD

6 Corporate Report 2007

There have also been further improvements to this report’s presentation of financial information on the Bank itself, with a distinction between the accounting rules imposed by the European System of Central Banks, those based on Belgian legislation and those laid down by the Council of Regency. The financial information is preceded by a management report describing the main developments which have influenced the result and the main risks confronting the Bank.

While severe turmoil is affecting many financial institutions around the world, and sometimes making it difficult for them to maintain their dividend policy, the Bank – which has always been prudently managed – will again pay its shareholders a dividend whose purchasing power has been preserved, i.e. a coupon with a nominal increase in value.

Contents 7

FOREWORD 5

INTRODUCTION 9

CHAPTER 1 : KEY EVENTS OF THE PAST YEAR 13

Major progress in payment systems 14

The Bank, service provider within the Eurosystem 16

Facilities for fi ling and consulting annual accounts 18

CHAPTER 2 : HUMAN RESOURCES MANAGEMENT 21

A changing environment, changing activities 21

Changing personnel needs 21

New emphasis on management 21

Employment trends 24

CHAPTER 3 : SUSTAINABLE MANAGEMENT 27

Air and water 29

Noise 29

Energy 29

Mobility 32

Waste management 33

Communication 34

Projects 34

CHAPTER 4 : GOVERNANCE 37

Governor 37

Board of Directors 40

Council of Regency 43

Board of Censors 45

Budget Committee and Remuneration Committee 45

Representative of the Minister of Finance 46

General meeting 46

Auditor 46

Disclosure of posts held and assets 46

Governance statement and rules of procedure 46

Amendment of the Organic Law and the Statutes 48

Organisation chart 50

Obituaries and retirement 51

CHAPTER 5 : DIRECTORS’ REPORT, ANNUAL ACCOUNTS

AND AUDITOR’S REPORT 52

Directors’ report 53

Presentation of annual accounts as at 31 December 2007 57

Notes to the annual accounts 67

Comparison over fi ve years 91

Auditor’s report 97

ANNEXES 100

1. Approval by the Council of Regency 101

2. Governance statement 103

3. Rules of procedure 117

4. List of articles published in 2007 in the Economic Review and the Working Papers 121

5. Opening hours and addresses 123

The National Bank of Belgium A central bank at your service

Introduction 9

With its euro area colleagues and the European Central Bank, the National Bank of Belgium is one of the components of the Eurosystem.

INTRODUCTION

The Eurosystem acts as the central bank of the euro area. The Treaty establishing the European Community assigned to it the primary objective of ensuring price sta-bility in the euro area. It performs that task by implement-ing monetary policy, which thus promotes growth and employment. Indeed, a monetary policy which preserves the purchasing power of the currency is the only way to improve the economic prospects and the standard of liv-ing. Experience has shown that a general and persistent increase in prices (inflation) and falling prices (deflation) are both damaging.

Other functions, such as the conduct of foreign exchange transactions, the holding and management of the official foreign exchange reserves of the Member States, and the promotion of the smooth operation of the pay-ment systems are among the Eurosystem’s activities, as is the collection of a mass of statistical information. The European System of Central Banks (ESCB) comprises the European Central Bank (ECB) and all the central banks of the European Union Member States, including those which have not adopted the euro. Questions concerning the stability of the European financial system are handled at ESCB level.

The Eurosystem… and beyond

Much of the National Bank’s work is connected with the tasks assigned to the supranational entities : the Eurosystem and the ESCB. The governor of the Bank par-ticipates in the meetings of the ECB Governing Council, which takes decisions on monetary policy. The Bank devotes a great deal of expertise to the preparation and implementation of those decisions.

In addition, it holds and manages Belgium’s official for-eign exchange reserves. It oversees the smooth opera-tion of the financial system as a whole, and that of the payment and securities settlement systems in particular. To limit the risks of a crisis, it contributes to the establish-ment of national standards and rules on that subject, and takes part in the work of the competent international institutions. This work of supervising the financial sec-tor is performed in close collaboration with the Banking, Finance and Insurance Commission. The Bank shares with the other central banks of the Eurosystem the right to issue euro banknotes. For Belgium, it is also responsible for placing the banknotes and coins in circulation, their withdrawal from circulation and quality monitoring.

10 Corporate Report 2007

The Bank is a recognised centre for analysis and economic research. The results of its work appear in various publications.

A monetary policy which preserves the currency’s purchasing power is the only way of improving the economic prospects and the standard of living.

the Economic Review, the Financial Stability Review and the Working Papers publish more specific studies. The Bank’s researchers are members of international networks and collaborate with their counterparts in Belgian univer-sities. The Bank initiates and supports research projects, and organises specialist seminars on macroeconomics and internship programmes for young researchers. Its scientific library is one of Belgium’s most important economic librar-ies. Its museum, totally refurbished in 2002, offers the general public – and especially schools – the opportunity to learn about money and how it works.

Within its area of responsibility, the Bank is a valued adviser of the government. It is represented in many national bodies, such as the High Council of Finance, the High Council of Employment, and the Central Economic Council. At international level, it takes part in the activi-ties of the International Monetary Fund (IMF), whose aims include the promotion of international monetary coopera-tion. It is one of the founding members of the Bank for International Settlements (BIS), which acts as the bank of the central banks and fosters international cooperation in monetary and financial matters. It joins in the work of the discussion forum constituted by the Organisation for Economic Cooperation and Development, and is involved in the groups of experts set up by the Council of the European Union and in the European Commission committees when their work falls within its sphere of competence. It advises the government in negotiations conducted by the World Trade Organisation on the liber-alisation of financial services. At the request of national or

Like most other central banks, it has also been entrusted with specifically national tasks unconnected with its par-ticipation in the Eurosystem. These represent a substantial part of its activities and occupy a considerable proportion of its staff. The Bank compiles and analyses the majority of Belgium’s economic statistics : in particular, it produces the balance of payments, and the consumer and business confidence indicators.

On behalf of the National Accounts Institute, it compiles the national and regional accounts and the foreign trade statistics. Many of these data are published, or sent to the international organisations which Belgium is required to supply with data.

In addition, the Bank acts as State Cashier, centralising the State’s revenue and expenditure and the balance of the Post Office transactions. It also plays a role in the issue and redemption of government loans. Finally, it is in charge of the routine management of the Securities Regulation Fund, which supervises the secondary market in public debt securities and regulates the price of government loans by intervening on the Stock Exchange.

A centre of excellence

The Bank is a recognised centre for analysis and economic research. The results of its work appear in various publi-cations : the Annual Report presents Belgium’s economic and financial situation in its international context, while

Introduction 11

The Bank has been printing banknotes since 1850, and continues to do so as a member of the Eurosystem.

Much of the National Bank’s work is connected with the tasks assigned to the Eurosystem.

the central credit registers enable the Bank to publish studies on economic sectors.

The Bank manages the Belgian interbank clearing sys-tem. It is the contact point for Belgian banks using the European payment system TARGET2. It is taking part in the establishment of the Single Euro Payments Area, which aims to ensure that card payments and payments in the form of transfers and direct debits can be arranged anywhere in the European Union just as easily as in one country.

Finally, the Bank performs a large number of highly specialised IT services for the Eurosystem community. Those services are described in more detail in chapter 1.

international institutions, it provides technical assistance for certain emerging or transition countries, and for the Democratic Republic of Congo.

Other services for the economy

Like some of its colleagues, and at the request of the legislator, the Bank centralises and circulates a large amount of microeconomic information. The Central Balance Sheet Office receives the annual accounts of almost all enterprises active in Belgium, processes them and makes them available to the public. The internet plays an increasing role in these operations. On the basis of these data, the Bank publishes sectoral statistics and documentation enabling firms to compare themselves with other firms in their sector.

The Bank also centralises data on credit granted to indi-viduals and firms – in the latter case, only if the loan exceeds 25,000 euro – thus enabling the banks to achieve a more accurate assessment of the credit risks which they are incurring. Since the beginning of 2005, the data on this subject have been exchanged with the central regis-ters of six other euro area Member States. The registra-tion of all consumer credit and mortgage loan contracts concluded by individuals is intended to prevent excessive debt : before granting a new loan, lenders have to consult the database of the Central Individual Credit Register. The statistics compiled for the National Accounts Institute and the data from the Central Balance Sheet Office and

Like most other central banks, the Bank has also been entrusted with specifically national tasks unconnected with its participation in the Eurosystem.

The National Bank helps decision-makers and business leaders to gain a better understanding of their economic environment.The National Bank helps decision-makers and business leaders

Without confidence, our economy would not have the same ambitions.

Key events of the past year 13

KEY EVENTS OF THE PAST YEAR

The European Central Bank will celebrate its 10th anniversary in 2008. The National Bank will therefore have been a member of the Eurosystem and the European System of Central Banks for ten years.

1.

In 2004, the Governing Council approved the Eurosystem mission statement and a series of organisational principles endorsed by all its members. While decentralisation is still the basic principle governing the performance of the various tasks of the Eurosystem, the ECB and the national central banks (NCBs) of the euro area undertake to per-form those tasks in a spirit of cooperation and teamwork. The Eurosystem is committed to identifying potential synergies and economies of scale, and to exploiting them to the extent feasible. It also aims to avoid unnecessary duplication of work and resources at functional levels, and to make intensified use of the experience available both at the ECB and at the NCBs. The operation of the Eurosystem is gradually adapting, and it is becoming increasingly com-mon for NCBs to get together to offer services to other members or other systems. The key events of the year under review illustrate how the Bank is participating in this process.

The year 2007 brought some notable developments in the field of payment systems, which are steadily becoming attuned to the context of the Eurosystem. More generally, the Bank intends to play a proactive role in this interna-tionalisation process by offering services geared to the new situation in Europe.

The activities connected with the Eurosystem are not the only focus of attention for the Bank, which is also concerned to perform with maximum efficiency the tasks entrusted to it by the legislator for the benefit of the Belgian economy. By way of example, we shall mention the measures taken during the year under review to make it easier to file and consult annual accounts, and thus con-tribute to the simplification of administrative formalities.

14 Corporate Report 2007

The operation of the Eurosystem is evolving : central banks are increasingly offering services jointly to other members.

The National Bank is responsible for placing banknotes and coins in circulation for Belgium, withdrawing them from circulation and monitoring their quality. It also manages the interbank payment systems.

Major progress in payment systems

The Bank manages the interbank payment systems for Belgium. The advent of the euro and the new European monetary policy had, and continue to have, a significant influence on non-cash payment systems and securities management and settlement systems.

The Eurosystem launched TARGET when the non-cash euro was introduced in 1999. That system enabled the European banks to effect urgent or large-value payments in real time throughout the euro area. It was there-fore an indispensable instrument for implementing the Eurosystem’s monetary policy. TARGET also offered the infrastructure necessary for the settlement of transactions by peripheral systems (retail payment systems and securi-ties settlement systems). However, since it was based on the existing national systems, it generated high costs for the Eurosystem and the banks.

TARGET2

It was therefore decided to develop a new system, TARGET2, based on a single technical platform offering a range of standardised services for the banks and the par-ticipating peripheral systems. New services are offered for the banking sector, for instance in liquidity management and the settlement of peripheral system transactions. The business continuity provisions adopted will probably serve as a benchmark for the other interbank infrastructures identified as critical for the smooth operation of the

financial system. Moreover, the charges have been aligned throughout, and the legal and regulatory frameworks have been harmonised as far as possible. TARGET2 there-fore enables the banks to achieve economies of scale and to offer a better service. It also provides an opportunity for international banks to rationalise their internal services in depth.

This system was successfully launched on 19 November 2007 in an initial group of countries. Belgium is in the second group, which migrated on 18 February 2008.

The TARGET2 platform is a fine example of a combined range of services conforming to the organisational princi-ples set out above : it is a joint technical infrastructure pro-vided by a group of NCBs comprising the Banca d’Italia, the Banque de France and the Deutsche Bundesbank, and piloted by the Eurosystem under the aegis of the ECB Governing Council. The Bank took part in its construc-tion : in the past year, for instance, it organised a series of tests and finalised the legal framework ; it also made the preparations for the Belgian banks and peripheral systems to migrate to the new platform.

The Eurosystem also conceived a project for unifying the infrastructure for the settlement of transactions in securi-ties. Known as TARGET2-Securities (T2S), this project involves creating a technical platform for the settlement of securities in central bank money, to which all securi-ties settlement systems can be connected. T2S aims to harmonise securities transaction settlement practices in

Key events of the past year 15

The year 2007 brought some major developments in payment systems : TARGET2 is the new system enabling banks in the euro area to exchange urgent or large-value payments. SEPA establishes a European area for non-cash payments in euro.

order to achieve substantial economies of scale. The sys-tem – which would be based in particular on the existing TARGET2 infrastructure – is currently being discussed by the parties concerned ; a final decision on its development should be taken by mid 2008.

SEPA

The Single Euro Payments Area – SEPA will really take shape in 2008 : since 28 January it has been possible to effect transfers throughout that area using a partly standardised form, the “single model”. From 2008, the Belgian market will also be open to other payment card systems, while keeping the Bancontact/Mistercash sys-tem for the time being. The European direct debit will be introduced when the Directive on payment services in the single market (Payment Services Directive – PSD) has been transposed into Belgian law (in principle, in November 2009). The PSD provides SEPA with the legal basis vital for its implementation.

SEPA is based essentially on agreements drawn up within the banking sector. The European Payments Council has developed European standards for transfers and direct debits, and a common framework for card payments. All economic agents (businesses, public authorities and consumers) will be able to use these payment instruments throughout SEPA.

The Eurosystem actively supports the creation of SEPA. In a monetary union where the same coins and banknotes can be used for cash payments, the absence of European non-cash payment instruments is an obvious defect. It is one of the obstacles to be eliminated in order to create a genuine European market in payment services. SEPA is therefore in line with the Lisbon strategy, which aims to make the European Union the most competitive and dynamic knowledge-based economy by 2010.

The transition to SEPA is being organised mainly at national level. The Belgian banking sector has drawn up a detailed migration plan with the support of the Bank. The latter is also very committed to consultation with the other parties concerned (businesses, public authorities and consumer organisations). That consultation takes place in the Steering Committee on the future of means of payment. On 12 December 2007, that committee published an initial progress report outlining the migra-tion plan and assessing the state of preparation of the players concerned. This revealed that Belgian credit insti-tutions are well-prepared for the transition to SEPA. The European transfer was launched on the Belgian market on 28 January 2008. However, it will be phased in gradually, and – according to the forecasts – Belgian transfers will have largely disappeared by the end of 2010. The public authorities will circulate the new European transfer form among the general public at the end of 2008. Large cor-porations generating a substantial number of transfers are expected to do the same. Details of the transition to the European direct debit have yet to be defined.

(1) It comprises the Member States of the European Union plus Iceland, Liechtenstein, Norway and Switzerland.

(2) Available at www.nbb.be/sepa.

16 Corporate Report 2007

The Cash system designed by the National Bank is enjoying international success. It gives central banks a secure, automated system for managing flows of banknotes and coins.

SEPA is not confined to the introduction of European standards. It aims to create a European market in retail non-cash payments. This should mean keener competi-tion between the players ; companies and credit institu-tions should benefit from the increased standardisation and achieve economies of scale ; in all SEPA countries, consumers will enjoy equivalent protection, significantly strengthened by the PSD. This unified market will also offer new opportunities for suppliers of payment instru-ments and electronic invoicing.

The Bank, service provider within the Eurosystem

With the advent of the Eurosystem and the resulting progressive integration of financial systems and markets, a number of IT applications designed for and with the Bank’s user services underwent significant international development. The Bank has played a particularly active role in this area, entirely in line with the organisational changes whereby it is becoming increasingly common for several NCBs to offer services jointly. A few examples illustrate how the Bank is implementing the principles promoted by the Eurosystem.

The first example concerns the management of the fidu-ciary euro. Like the other NCBs, the Bank is responsible for placing banknotes and coins in circulation, and for their withdrawal and quality monitoring at national level. The introduction of euro banknotes and coins in 2002 was

the occasion for the Bank to develop an IT tool permitting more efficient and secure management of banknotes. By means of the Cash application, banknotes are handed in and withdrawn in sealed packs, following prior electronic notification. Data communication, payment recording and invoicing are effected automatically on completion of the physical operations.

The success of this tool in Belgium encouraged the Bank to offer it to other NCBs. Thus, the Bank concluded a partnership with the Nederlandsche Bank and the Banque centrale du Luxembourg permitting them to use the Cash Single Shared Platform (CashSSP) to manage their flows of banknotes and coins, both internally and in dealings with credit institutions (or cash transport firms) established in their country. The Bank of Finland has joined this partnership : CashSSP has been operational there, too, since February 2008. This development shows that the proactive attitude of NCBs wishing to cooperate helps to create synergies of benefit to the other parties involved.

Another partnership was concluded in connection with the implementation of the Eurosystem’s monetary policy, for the settlement of lending transactions and the management of the associated collateral. Conduct of monetary policy operations is decentralised : each NCB is responsible for monitoring loans to banks estab-lished in its country, and the collateral backing the loans. Management of the collateral is essential in the context of the implementation of monetary policy, since the loans

Key events of the past year 17

With the advent of the Eurosystem, a number of IT applications underwent significant international development. The Bank has played a particularly active role in this area.

granted must be backed by security. Apart from market-able assets, bank loans have been eligible as collateral since January 2007. For the purpose of managing this collateral and settling credit operations, the Bank put into production a new IT application, the Eurosystem Collateral Management System (ECMS). A partnership was concluded with the Nederlandsche Bank, which has been using ECMS since December 2006.

Collateral management also has a transnational dimen-sion : each central bank acts as a correspondent for the other NCBs in the Eurosystem. One central bank can thus make available to another NCB the collateral lodged with it by a credit institution, as security for obtain-ing credit from the latter. The Correspondent Central Banking Model (CCBM) is the system which facilitates the cross-border use of collateral to guarantee all types of Eurosystem credit operation. Thus, as at 31 December 2007, as a correspondent, the Bank held around 147 bil-lion euro on behalf of other NCBs. In 2006, the important role which the Bank performed here placed it in third posi-tion, in terms of amounts, among ESCB correspondent central banks. On a reciprocal basis, the other central banks held around 22 billion euro as correspondents of the Bank as at 31 December 2007.

At the request of the market operators, a single platform is to be established for the settlement of Eurosystem credit operations and collateral management, for both national and cross-border transactions. It should enable the NCBs to harmonise the procedures for implementing

the common monetary policy, while maintaining decentra-lised management. The ECB has announced that this new platform, known as CCBM2, will be based on existing systems such as ECMS. The Bank and the Nederlandsche Bank have therefore invested heavily in this project. Following an initial market consultation in 2007, work has begun on defining the technical characteristics of the new version of the CCBM.

In line with the Eurosystem’s mission statement, Eurosystem members have undertaken to promote and encourage the exchange of personnel, know-how and experience. The examples below show how the Bank is making a contribution here, positioning itself as a service provider for the Eurosystem.

The first example concerns banknotes. Since the intro-duction of the fiduciary euro, the ECB and the other Eurosystem members have had an IT application which monitors the number of banknotes placed in circula-tion, validated, rejected or destroyed. This central data-base (CIS – Currency Information System) is updated monthly by the NCBs. In 2006, in view of the impending enlargement of the euro area and the introduction of a new series of banknotes, the ECB decided to replace it with a more efficient system. The Bank was commissioned to develop the new application. It is thus placing the rel-evant know-how which it has acquired at the service of the Eurosystem, in both functional and IT terms. The new database will be delivered to the ECB and the other NCBs in stages during the first half of 2008.

18 Corporate Report 2007

The National Bank is taking on the role of provider of specialist IT services for its peers.

The National Bank participates in the on-going process which aims to share knowledge and know-how within the Eurosystem.

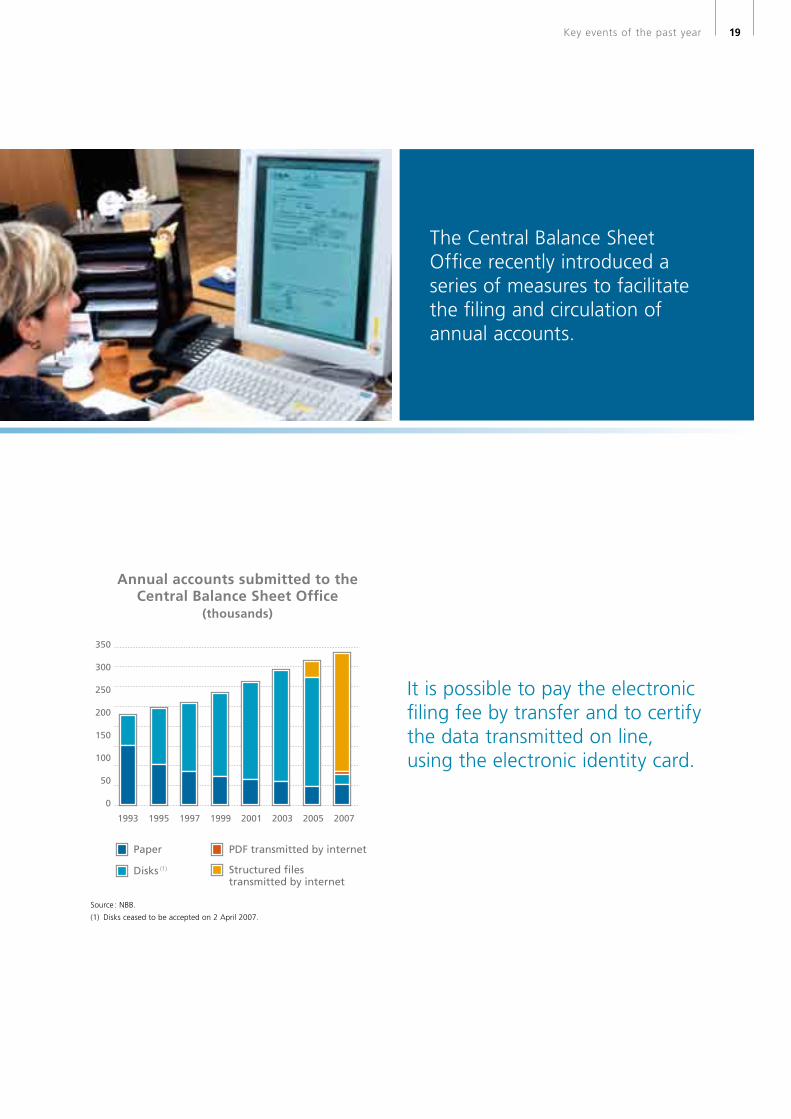

Sheet Office since it was established in 1978. The obli-gation to publish annual accounts was first imposed on limited liability companies. It was then extended to large and very large non-profit organisations and private foun-dations. A supplement, the social balance sheet, which gives information on employment, was added to the annual accounts in 1996.

The Central Balance Sheet Office recently introduced a series of measures to facilitate the filing and circulation of annual accounts. Since mid February 2008, the accounts for the current year and the five preceding years have been available free of charge on the Bank’s website.

Also, since 1 April 2007, commercial companies have been able to file their annual accounts via the internet, in XBRL or PDF format. From mid March 2008, non-profit organisations and private foundations also have the option of filing their accounts in XBRL format via the internet. XBRL is the new international standard for the exchange of financial data via the internet. It offers many advantages. It gives the items in the annual accounts a single code and links them together via a rational struc-ture, avoiding the need to encode the same data several times. This standard also facilitates the exchange, transfer and analysis of the data, which can be selected, re-used and reformatted according to the type of statement required. An advantageous rate is charged to encourage use of this new standard for filing accounts.

The second example concerns information and commu-nication technologies, equally essential for central banks and all financial institutions. By judicious investment, the Bank has developed robust IT infrastructures for the benefit of the Belgian economic and financial community. The Centre for Exchange and Clearing and the two central credit registers are the best-known examples. For some years now, the Bank has specialised in the use of internet technologies. The expertise thus acquired in the secure exchange of data has been put to good use in the interna-tionalisation of internal applications (CashSSP and ECMS). It is now shared with the ECB and the other NCBs. Thus, in 2007, the Bank invested heavily in the development of the ESCB XML Data Interchange (EXDI) network, which enables ESCB members to exchange data between applications in a standardised form.

These examples demonstrate that the Eurosystem’s mis-sion statement is steadily being implemented and that the knowledge and expertise of the members are being shared. The Bank aims to play a key role in that process.

Facilities for filing and consulting annual accounts

Apart from its work for the Eurosystem, the Bank per-forms specific services for the community, and particularly for businesses. Thus, it has managed the Central Balance

Key events of the past year 19

The Central Balance Sheet Office recently introduced a series of measures to facilitate the filing and circulation of annual accounts.

Annual accounts submitted to the Central Balance Sheet Office

(thousands)

Paper

Disks (1)

PDF transmitted by internet

Structured files transmitted by internet

1995 1997 1999 2001 2003 2005 20071993

0

50

200

150

100

250

300

350

Source : NBB.

(1) Disks ceased to be accepted on 2 April 2007.

It is possible to pay the electronic filing fee by transfer and to certify the data transmitted on line, using the electronic identity card.

The National Bank watches over the quality of means of payment, from banknotes to electronic systems.The National Bank watches over the quality of means of

Without confidence, paying for things would not be so easy.

Human resources management 21

HUMAN RESOURCES MANAGEMENT

The aim of human resources management is to enable the institution to optimise its strategic choices in a changing environment.

2.

A changing environment, changing activities

The Bank’s integration into the Eurosystem did not only change its institutional framework, it also modified its technological and social environment.

On the occasion of the second strategic exercise conduct-ed by the Board of Directors, a master plan was drawn up for each department for a period ending in 2009. It places the emphasis on activities which come under the ESCB, the quality of the services provided for the community, and cost control.

Changing personnel needs

The changing environment in which the institution is evolving and the resulting adjustments have greatly altered its personnel needs. The Bank now requires more skills and increased mobility. To meet these challenges, the Human Resources department drew up an action plan.

Those changing needs are also reflected in recruitment. In 2007, the Bank took on some young economists spe-cialising in questions relating to financial stability, and some IT personnel. The Bank’s participation in employ-ment exchanges such as Talentum has proved that it still attracts young graduates. An internal survey conducted among managerial and supervisory staff with less than five years’ seniority reveals that, for half of them, career opportunities are a key reason for applying to the Bank. Reputation, prestige and job security are the next reasons cited by almost half of respondents. One-third of them are attracted by the work-life balance which the institu-tion offers.

New emphasis on management

During the past year, while preserving its own social model the Bank has introduced new points of emphasis in its human resources policy. They include skills manage-ment, career development – with a greater role for the managerial capabilities of supervisory and managerial staff – and the promotion of mobility.

22 Corporate Report 2007

In 2007, the Bank took on twelve new staff members on permanent contracts, the great majority being IT staff and economists.

Skills management

A few years ago, the Bank introduced a skills manage-ment model which represents the cornerstone of its human resources policy (recruitment, training, assess-ment promotion and change). This model aims to match individual skills as closely as possible to the objectives and strategy of the institution. A number of generic skills were identified, plus a series of specific skill profiles. During the annual staff appraisal interviews, a professional develop-ment plan was drawn up with each member of staff, enabling all employees to do their job better and acquire useful skills in the medium term. This augmented staff mobility.

Managers and experts

A new collective labour agreement was concluded in 2007 concerning the career structure for managerial and supervisory staff. Two streams were created : one for “managers” (administration) and one for “experts” (staff functions). It is crucial for the Bank to have managers and experts capable of facing the challenges presented by a changing environment. In accordance with their new status, heads of service and heads of department, and potential applicants for those positions, will attend a Development Centre. This external development centre will enable the persons concerned to conform to the man-agement style defined by the Bank. Training programmes will be organised for that purpose.

A project concerning the career structure of the other categories of staff is also in the pipeline. It concerns the design of a new promotion system enabling staff to take advantage of career opportunities corresponding to the needs which the Bank encounters in the future, accord-ing to a system based mainly on skill levels and quality of performance.

Mobility

The ability to respond quickly to new needs requires great internal mobility. The Bank therefore intends to encourage that. It must be possible to make changes flexibly and speedily, within a maximum period set at three months. Mobility is also a favoured development instrument. That is why the Bank enables young managerial staff, in the first five years of their career, to learn about various activi-ties. It is also possible to complete an internship with the European Central Bank or with another central bank of the Eurosystem.

Technical assistance

The Bank also makes the skills of its staff in certain areas available to other central banks, primarily via technical assistance programmes.

Human resources management 23

Thus, it provides support for other ESCB central banks in their preparations for the introduction of the single currency. In 2007, the Bank took part in the twinning programmes organised by the European Commission for the Czech Republic and Slovenia. A second programme with Slovenia has been announced for 2008, and another with Latvia. The Bank also received numerous delegations on working visits.

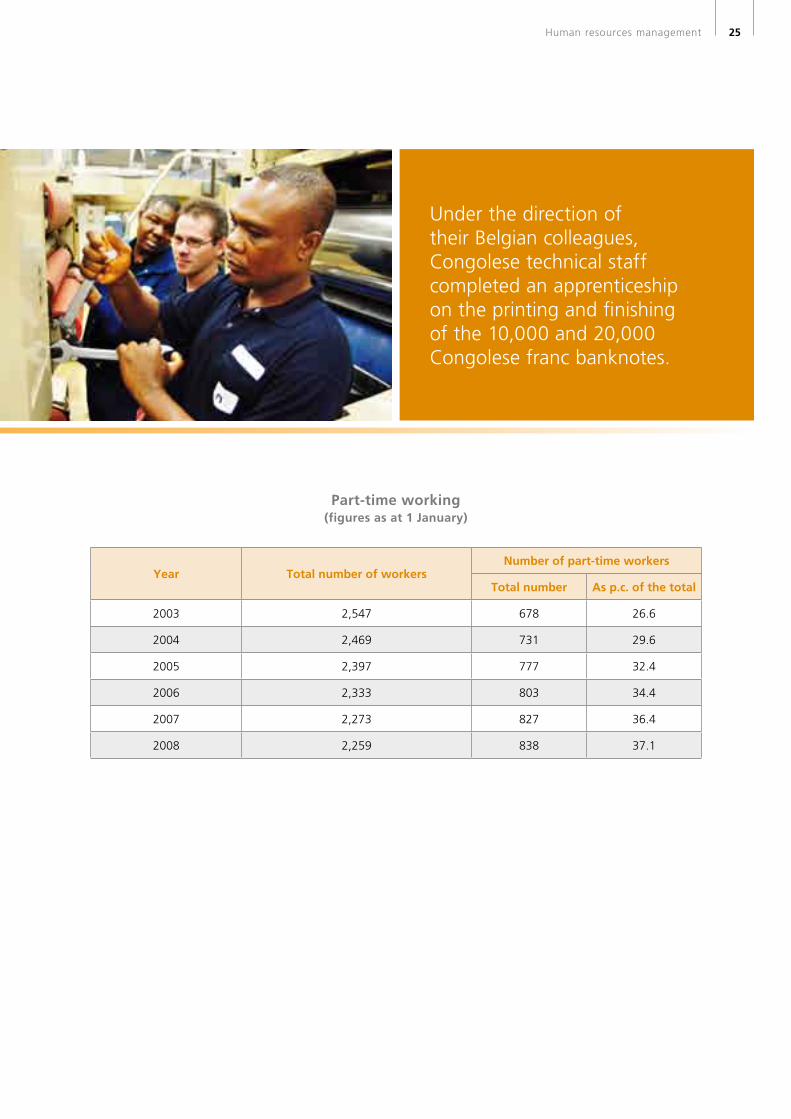

As part of the bilateral cooperation between Belgium and the Democratic Republic of Congo, and in consultation with the International Monetary Fund, the Bank also pro-vided technical assistance for its Congolese counterpart. Technical staff from the Central Bank of Congo completed an internship to assist them in the manufacture of the new 10,000 and 20,000 Congolese franc banknotes. The Bank also lent its expertise under a training and consultancy programme organised in Kinshasa, concern-ing not only payment systems but also financial markets, information technology, monetary policy and facility management.

Training

The purpose of training is to match the institution’s needs as closely as possible to the skills of its staff.

The Bank offers a broad array of training schemes in order to ensure the availability of the skills which it considers necessary. It has recognised the importance of training by including the entitlement to training in a sectoral collective labour agreement. Flexible formulas are offered : courses during school holidays, video training, coached learning, etc.

One of the main trends of recent years is the improvement in tailoring training programmes to the specific needs of the services. Managerial and supervisory staff also take part in training schemes organised by the ESCB, in par-ticular to align the various corporate cultures.

Recruitment of permanent staff between 1 January 2003 and 31 December 2007

17

11

10

7

4

4

41

IT

Research

Legal service

Financial stability

International coordination and Eurosystem

Statistics

Communication and secretariat

Microeconomic analysis

The Bank’s integration into the Eurosystem has changed not only its institutional framework but also its technological and social environment.

24 Corporate Report 2007

Encouraging mobility includes offering internships at other central banks, among them the ECB.

Employment trends

As a result of changing functions in a constantly changing environment, some jobs disappear and new ones are cre-ated, generally requiring a higher level of training.

As at 31 December 2007, the Bank had a workforce of 2,032 “full-time equivalents”, of whom 351 were managerial or supervisory staff and 1,681 clerical staff. Employment, which had already fallen by 22 p.c. over the past ten years as a result of network restructuring and productivity gains in the Bank’s various spheres of activity, declined by a further 17 full-time equivalents in 2007.

Change in staff numbers, 1997 to 2007(full-time equivalents as at 31 December)

0

500

1,000

1,500

2,000

2,500

2,59

9

2,51

8

2,44

5

2,40

6

2,41

8

2,31

9

2,25

0

2,17

4

2,12

0

2,04

8

2,03

2

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

The changing environment in which the institution is evolving and the resulting adjustments have greatly modified its personnel needs.

Source : NBB.

Human resources management 25

Under the direction of their Belgian colleagues, Congolese technical staff completed an apprenticeship on the printing and finishing of the 10,000 and 20,000 Congolese franc banknotes.

Part-time working(figures as at 1 January)

Year Total number of workersNumber of part-time workers

Total number As p.c. of the total

2003 2,547 678 26.6

2004 2,469 731 29.6

2005 2,397 777 32.4

2006 2,333 803 34.4

2007 2,273 827 36.4

2008 2,259 838 37.1

The National Bank protects your purchasing power by guaranteeing price stability.The National Bank protects your purchasing power

Without confidence, your everyday life would not have the same flavour.

Sustainable management 27

SUSTAINABLE MANAGEMENT

A company serving society : that is the motto under which the Bank aims to combine its multiple tasks.

3.

The Bank also intends to reflect this mission to serve society in its corporate ethos : it encourages its staff to adopt an ethical approach and social commitment as cardinal values.

Those values are displayed, for instance, in the desire to improve the institution’s environmental record. Located right in the city centre and engaging in both admin-istrative and industrial activities, the Bank is aware of its particular responsibility on this subject. That is one reason why it has initiated the necessary action to gain, in the near future, the “ecodynamic enterprise” label awarded by the Brussels Institute of Environmental Management (IBGE/BIM). It is a demanding procedure which concerns a number of aspects, and all sectors of the Bank’s activity. Clearly, recent years have already seen a spate of environmental projects, covering a very wide range of aspects : selective waste collection, reductions in

energy consumption, incentives to use public transport, etc.

The Bank pursues numerous activities which come under the heading of Corporate Social Responsibility. We shall confine ourselves here to describing the effort which it is making on the aspects which the IBGE/BIM consid-ers when defining an ecodynamic enterprise. Thus, we shall see how the Bank takes account of the environ-ment within its actual operating processes. One example is the ISO14001: 2004 certification which the Printing Works gained for its environmental management system. Admittedly, this is not a certificate granted to opera-tors causing the least pollution, but it has the merit of introducing the concept of environmental manage-ment into the activity of the institution and forcing it to make constant improvements in its performance on that subject.

28 Corporate Report 2007

The Bank’s Printing Works has gained an environmental management certificate.

At the end of 2007, the Bank’s Printing Works gained the ISO 14001: 2004 certificate. Awarded following an audit by Lloyds (LRQA), this certification is the culmination of a major team effort. To gain this certificate it is necessary to have identified the environmental impact of the operator’s activities, the processes used and the products made – in terms of air, water and soil pollution, waste management, energy consumption, etc. –, and to have developed a manage-ment system for those aspects.

Awarded for three years with twice-yearly checks, this certificate also requires the operator to make progress, by setting targets and constantly improving its environmental performance.

Obtaining this certification is part of the Bank’s general policy on sustainable development. Having already obtained certificates concerning quality (ISO 9001) and security management (CWA 14641: 2003), its Printing Works now has fully integrated management systems.

Recent years have seen a spate of environmental projects covering a very wide range of aspects: selective waste collection, reductions in energy consumption, incentives to use public transport, etc.

Sustainable management 29

reverse osmosis filter, reducing the amount of chemicals, water and energy used. In addition, a highly efficient technical facility management system gives an electronic indication of the smallest leak in the steam circulation system, so that it can be rectified without delay.

Noise

Working right in the city centre means paying particular attention to the noise nuisance which the activity may cause. During the past year, silencers have been installed in the Printing Works’ ventilation and cooling equipment. Their effect is assessed both by measurement and by surveys among staff and neighbours.

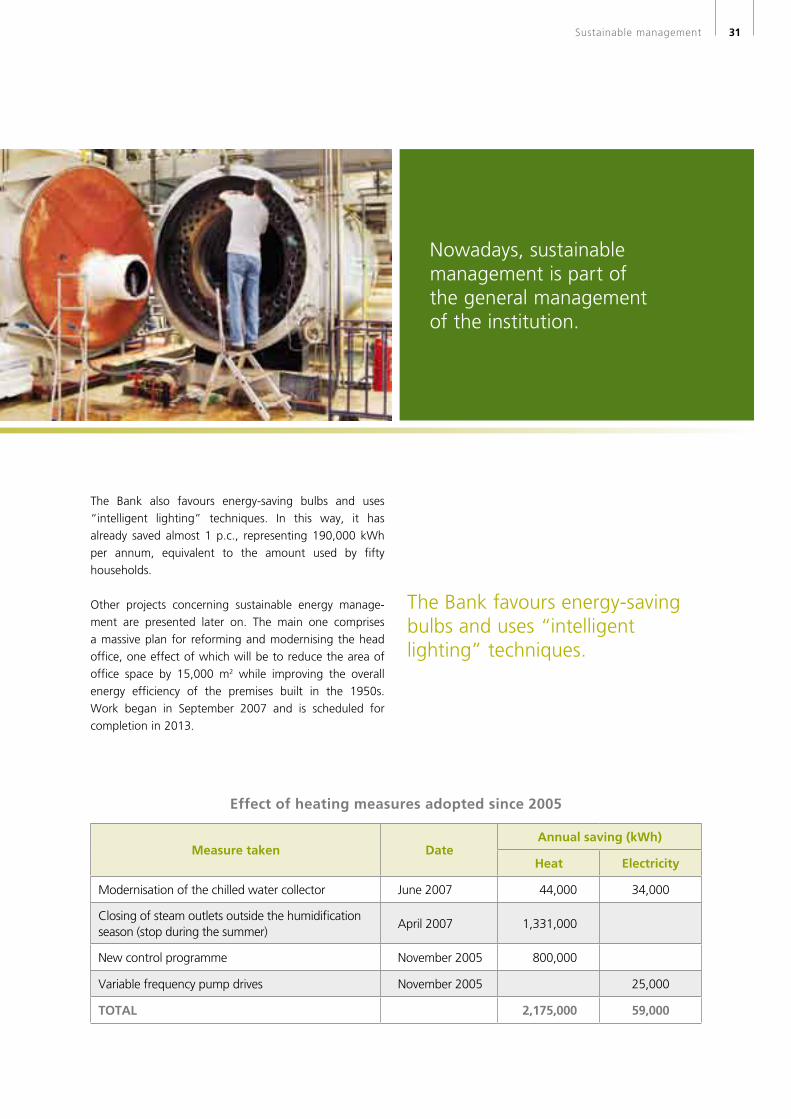

Energy

Nowadays, energy management is regarded as an inte-gral part of the institution’s general management. For many years, the Bank has taken accurate measurements of its energy consumption, having installed around three hundred meters for the purpose. Since 1994, the annual report on energy published by its Equipment and Techniques service has presented a medium-term picture of progress on that subject. During last autumn, the staff developed an energy accounts programme which can be used to perform highly sophisticated analyses and thus to seek ways of cutting consumption.

Air and water

The Printing department’s industrial activities are associ-ated with specific environmental risks. That is why a pro-gramme was devised to reduce atmospheric emissions of volatile organic compounds. Since 2002, the installations have included a biofilter in which bacteria break down the polluting molecules produced by the serigraphic presses and ink driers. An approved agency is responsible for monitoring the waste air.

For an activity such as that of the Printing Works, water purity is a primary environmental concern. The water used in the production process undergoes ultrafiltration so that it can be reused ; dirty water is taken away by a specialist firm. These liquids are therefore never mixed with other waste water ; the latter is subjected to internal checks every two months, and to an annual audit conducted by an approved laboratory checking, in particular, for heavy metals.

But at the Bank, it is not only this industrial department that uses water. Saving water is everyone’s responsibil-ity, and is an everyday issue. Thus, the premises are now cleaned by a dry method, limiting the quantity of water and cleaning products needed.

In the steam-production plants, water and energy savings go hand in hand : the water is demineralised to prevent lime scale formation and thus cut fuel consumption. Nowadays, that operation is effected by means of a

In the Printing Works, volatile organic compounds produced by various installations are broken down by bacteria in a biofilter.

Silencers have been installed in the Printing Works’ ventilation and cooling equipment.

30 Corporate Report 2007

Improvements to the main boiler have cut electricity and heat consumption by 825,000 kWh per annum since the end of 2005.

The large number of very recent, on-going or forthcoming changes in this area will therefore come as no surprise. We shall confine ourselves here to reviewing the most important of them.

The improvement in the main boiler control system and the other measures adopted since the end of 2005 have brought savings, in normalised values, of over 1,700,000 kWh in 2006 and over 1,850,000 kWh in 2007, or 9.5 p.c. and 8.5 p.c. respectively of the Bank’s consumption. Combined with the grant from the Brussels Capital Region, these savings meant that the investments paid for themselves in fourteen months.

Since 1 January 2007, the proportion of the Bank’s electric-ity obtained from renewable energy sources has increased from 15 p.c. to 100 p.c. The institution has achieved the objective of carbon-neutral electricity consumption.

During the past year, the Bank simplified and modernised the chilled water collector in one of the complexes of head office buildings. This will cut the Bank’s energy consumption by 34,000 kWh per annum.

CO2 emissions, 1997-2006 (kilotonnes)

1999 2000 20011998 2002 2003 2004 2005 20061997

Gas

Heating oil

0

1

2

3

4

5

6

Emission rights

Source : NBB.

Sustainable management 31

Nowadays, sustainable management is part of the general management of the institution.

The Bank also favours energy-saving bulbs and uses “intelligent lighting” techniques. In this way, it has already saved almost 1 p.c., representing 190,000 kWh per annum, equivalent to the amount used by fifty households.

Other projects concerning sustainable energy manage-ment are presented later on. The main one comprises a massive plan for reforming and modernising the head office, one effect of which will be to reduce the area of office space by 15,000 m2 while improving the overall energy efficiency of the premises built in the 1950s. Work began in September 2007 and is scheduled for completion in 2013.

Measure taken DateAnnual saving (kWh)

Heat Electricity

Modernisation of the chilled water collector June 2007 44,000 34,000

Closing of steam outlets outside the humidification season (stop during the summer)

April 2007 1,331,000

New control programme November 2005 800,000

Variable frequency pump drives November 2005 25,000

TOTAL 2,175,000 59,000

Effect of heating measures adopted since 2005

The Bank favours energy-saving bulbs and uses “intelligent lighting” techniques.

32 Corporate Report 2007

Mobility

A very large proportion of the staff are commuters. In regard to incentives for responsible mobility, the Bank goes much farther than the law requires, refunding the full cost of staff season tickets for public transport (train, bus or metro). 73 p.c. of its staff travel by public transport.

The Bank hopes that these various measures will reduce the percentage of staff who still travel to work by car. Moreover, a company car is not among the fringe benefits offered. A pilot teleworking project has also been set up. Its assessment should open the way to new ideas on mobility.

Finally, the Bank has a fleet of company vehicles : cars, vans and lorries, which tend to be used less and less. Furthermore, new vehicles purchased have diesel engines fitted with particulate filters.

Since joining the Eurosystem, the Bank has seen a consid-erable increase in the number of foreign trips by its mana-gerial and supervisory staff. In 2007 alone, that involved around 700 flights to Frankfurt. Once the high-speed rail link begins operating to Frankfurt, the Bank’s travel service will promote journeys by train.

73 p.c. of the Bank’s staff use public transport.

Walk, take the train... or cycle !

A large percentage of the staff live less than 20 km from the office where they work.

The Bank therefore decided to encourage cycling to work. To do that, it not only pays an allowance per kilometre, it has also provided special facilities at its head office, comprising cycle racks, specially ventilated changing rooms and showers. These facilities were improved and extended during 2007.

Sustainable management 33

The Forest Stewardship Council (FSC) label.

Waste management

The materials used and the waste produced by the Printing Works and the Central Cash Office are precisely recorded and carefully monitored.

However, like any administrative institution, the Bank also consumes large amounts of ordinary paper. Its “ printing charter” provides for the use of 100 p.c. totally chlorine free (TCF) paper, bearing the Forest Stewardship Council (FSC) label.

Moreover, there are many projects which have already had, and will continue to have, an impact in reducing the volume of paper produced by working procedures. For some years now, the development of intranet sites has permitted a great reduction in the circulation in paper form of official notices and other forms. The aboli-tion of the paper press review has cut consumption by 12,000 pages per day. The Enterprise Resource Planning software – whereby invoices can be scanned once instead of copied multiple times – and especially the DMS (docu-ment management system), also appreciably reduce the consumption, handling and storage of paper. During 2007, printers were reconfigured to print on both sides of the paper as the default setting. Similarly, the replacement of individual printers by multi-function devices, initiated in 2007, should reduce their number by two hundred units.

Paper consumption (millions of sheets)

For some years now, the development of intranet sites has greatly reduced the circulation of information in paper form.

20

21

22

23

24

25

26

27

28

2003 2004 2005 2006 200720022000 2001

Source : NBB.

34 Corporate Report 2007

In 2003, the in-house magazine, Connect, devoted two lengthy articles to the position of businesses in regard to the environment. On that occasion, the staff Médiatheque decided to set up a battery collection point, which has become increasingly successful. Between 2005 and 2007, some fifty messages relating to environmental questions were published in that magazine or on the intranet. Most of them were practical hints, equally applicable at home (electricity consumption of appliances on stand-by, ways of saving water, etc.). The plan is to circulate this type of message systematically.

Projects

The Accommodation Master Plan adopted by the Bank will have a major effect in environmental terms : it will reduce the area of office space by 15,000 m² at head-quarters, and will be accompanied by many improvements in heat and sound insulation, heating technology, etc.

The Bank has applied for permission to replace all the win-dows in the main building with soundproof glass offering a high level of insulation. The external walls are to be insu-lated and areas refurbished, with cooling ceilings ; ventila-tion will therefore cease to be used except to air the prem-ises. These measures should save up to 1,370,000 kWh (= 137,000 m³ of gas) per annum on heating and achieve the K45 index for the level of insulation of the refurbished areas. Also, the asbestos still in situ behind six hundred metres of metal panels is to be removed.

In regard to the management of office waste, selec-tive collection came into general use at the beginning of 2007 : a paper bin by the office, bins for PET bottles and cans near the drink dispensers, and bins for non-recyclable waste in the toilets. This operation has doubled the proportion of recycled waste and brought a 40 p.c. reduction in the volume of non-recyclable waste.

There is an obligation on suppliers to take back the pack-aging of cleaning products (containers, boxes, palettes). Supplies for the kitchen have to be packed in recyclable materials, reducing the waste by 90 p.c.

Waste production is monitored increasingly closely with a view to introducing an appropriate management system. Each type of waste is collected and treated by a specialist firm. The Printing department has launched a programme aimed at reducing industrial waste and waste packaging.

Communication

The Nobel Peace Prize for 2007, awarded to persons engaged in research on global warming, reflects the importance attached to respect for the environment and sustainable development. The staff of large corporations also take these issues to heart, and the information on the subject published via the Bank’s internal communication channels generates a considerable response.

Water used by the Printing Works in the production process undergoes ultrafiltration.

Sustainable management 35

Finally, a research agency has been commissioned to con-duct an energy audit. Its terms of reference entail prepara-tion of an overall project enabling the Bank to develop an investment programme designed to achieve the optimum combination of heat, cold and steam production, with a view to renovating the central energy plant in 2009. The feasibility of installing solar power units on the roofs of the head office buildings will also be examined.

The Accommodation Master Plan adopted by the Bank will have a major impact in environmental terms. It involves refurbishment and considerable improvements to the energy efficiency of the central building.

Some measurable targets

Apart from the projects mentioned here, the Bank has set itself some measurable targets, defined in figures, for the next five years :

➔ average reduction in electricity consumption : 2 p.c. per annum ;

➔ average reduction in consumption of gas (and heating oil) : 4 p.c. per annum ;

➔ average reduction in the use of paper by printers and photocopiers : 6 p.c. per annum ;

➔ average reduction in the number of journeys by air : 4 p.c. per annum.

The National Bank contributes to international economic and financial stability.The National Bank contributes to international economic and

Without confidence, international relations would not count for much.

Governance 37

GOVERNANCE

In view of the particular functions of the Bank and its specific, unique role in Belgium, it has been endowed by law with its own particular legal framework and specific system of governance.

4.

The Bank’s governance statement, which describes its special legal framework and its operating rules and the powers of its organs, appears in Annex 2 to this report and on the Bank’s website. (1) Below is a description of the Bank’s governance in 2007.

Governor

Mr Guy Quaden has held the office of governor since 1 March 1999. Mr Quaden’s term of office was renewed for a further five years, with effect from 1 March 2004. The governor’s curriculum vitae is available on the Bank’s website.

The governor can prove ownership of fifty registered shares in the Bank, as required by Article 34, 3° of the Statutes. He holds no share options and no rights to acquire shares. During the past year, he has not purchased or sold any Bank shares or other financial instruments relating to such shares.

He also holds the following offices :

Member of the Governing Council and of the General Council of the ECB ;

Director of the BIS ;

Governor of the IMF ;

Alternate governor of the International Bank for Reconstruction and Development, the International Development Association and the International Finance Corporation ;

Chairman of the Financial Stability Committee, the Supervisory Board of the Financial Services Authority, the Professional Association of Public Credit Institutions and the Study Group on Ageing (High Council of Finance) ;

Vice-chairman of the High Council of Finance ;

Member of the Bureau of the High Council of Finance, member of the Board of Directors of the National Accounts Institute and of the Carnegie Hero Fund Administrative Committee.

(1) Cf. www.nbb.be, Our enterprise – Our organisation – Governance statement.

38 Corporate Report 2007

Legal proceedings

On 9 March 2007, the Brussels Commercial Court passed judgment in an action brought by a group of twenty-four shareholders seeking a ruling ordering the Bank and the State jointly, or in solidum, to pay the applicants the sum of € 9,333.67 per share in the Bank, plus interest. (1) The shareholders claimed that, between 1996 and 2002, the State wrongfully appropriated the capital gains realised by the Bank on the sale of gold reserves.

The Court ruled that the applicants’ plea was unfounded. It confirmed that the shareholders have no right to the capital gains made by the Bank on the sale of gold, and that under the Organic Law and the Statutes, the capital gains realised are deducted from the profits to be distributed among the shareholders. It also ruled that the Bank had not committed any offence in transferring those capital gains to the State pursuant to the laws of 26 July 1996, 18 December 1998 and 10 December 2001.

As a central bank, the Bank has special status

As Belgium’s central bank, the Bank is an integral part of the Eurosystem, whose main objective is to maintain price stability for the benefit of the community. It also performs numerous other tasks in the general interest which have been entrusted to it by law. Its situation is therefore very different from that of an ordinary commercial company, whose main objective is to maximise its profits.

The pre-eminence of the Bank’s tasks in the public interest, present from the start and now anchored in the Treaty establishing the European Community, justifies its special status. In particular, it accounts for the methods of appointing the members of its organs, the specific composition and role of the Council of Regency, the limited powers of the general meeting of shareholders and the special arrangements for organising supervision. It also accounts for the provisions governing the financial aspects of the Bank’s activity, which provide it with a sound financial basis and attribute to the State, as a sovereign State, part of the income which the Bank obtains from its activities as a central bank (see in particular Articles 29, 30, 31 and 32 of the law of 22 February 1998 establishing the Organic Statute of the National Bank of Belgium, known as the Organic Law).

It was also the Bank’s tasks in the public interest, inherent in its role as a central bank, that caused the legislator to endow it with a special legal framework. The provisions on public limited liability companies apply to it only additionally, i.e. in regard to matters not governed by the Treaty establishing the European Community, the Protocol on the Statutes of the ESCB and the ECB attached to the Treaty, the Organic Law and the Statutes of the Bank, and provided that the provisions on public limited liability companies do not conflict with those priority rules. Moreover, as a member of the Eurosystem, the Bank is subject to special accounting rules and enjoys special status regarding the information disclosure obligations.

(1) The amount claimed in the initial citation was € 5,784 per share. The applicants increased it to € 9,333.67 per share during the proceedings.

Governance 39

It considered that, in respecting the will of the legislator, the Bank had exercised all due care, and that it cannot have acted illegally, and certainly cannot be held liable.

Twenty shareholders lodged an appeal against this judgment before the Brussels Court of Appeal. The final claims must be submitted by no later than 30 June 2008. The date of the hearing has not yet been fixed.

On 21 March 2007, an application for interim measures was filed against the Bank before the President of the Brussels Commercial Court, at the request of twenty-two shareholders. Taking the view that the judgment of 9 March 2007 implied that the gold held by the Bank belonged to State, which in their opinion meant that the Bank should have recorded a debt to the State on its balance sheet, or formed a provision, they claimed that the Bank’s annual accounts had not been correctly drawn up. In the light of these points, they demanded suspension of the ordinary general meeting scheduled for 26 March 2008 and its postponement for one month, rectification of the accounts for 2006 and the convening of an extraordinary general meeting if the corrected annual accounts showed that the net assets represented less than 50 p.c. of the share capital.

By an order issued on 23 March 2007, the court hearing the application for interim measures rejected the demand for suspension of the general meeting scheduled for 26 March 2007. It decided that, contrary to the applicants’ assertions, the Commercial Court had not given any ruling, in its judgment of 9 March 2007, on the legal regime governing the gold reserves, be it in regard to their ownership or the accounting law. It also pointed out that the ordinary general meeting has no power to approve the accounts, to decide on the administration and management or to grant a discharge to the administrative bodies. Since the applicants had not taken appropriate steps to obtain a decision from the court on the other claims, the latter were referred to the case list.

Two other actions are still pending before the Brussels Court of Appeal.

The first concerns the appeal brought by a group of shareholders against the ruling handed down by the Brussels Commercial Court on 27 October 2005. The date of the hearing has not yet been fixed. The date of May 2009 is indicated as a guide on the Court of Appeal’s website.

The applicant shareholders demanded liquidation of the Bank’s reserve fund on the grounds that the Bank had lost its right of issue following the transition to Economic and Monetary Union. The Brussels Commercial Court confirmed the view that, since that transition, the Bank has shared the right of issue with the European Central Bank and the central banks of the other countries which have adopted the euro. Consequently, it still has the right of issue and there is no reason to liquidate its reserve fund. The Court of Arbitration had already confirmed the maintenance of the Bank’s right of issue in 2003.

The second legal action concerns the appeal brought by a group of shareholders against the ruling handed down by the Brussels Commercial Court on 2 February 2006. The date of the hearing has not yet been fixed. The date of April 2009 is indicated as a guide on the Court of Appeal’s website.

The applicant shareholders were seeking cancellation of the decision by the Council of Regency which, at the end of the 2003 financial year, approved an additional write-back on the provision for future exchange losses, supplementing the write-back necessary to cover the exchange losses for the year, and approved the inclusion of that additional write-back in the proceeds to be shared between the Bank and the State pursuant to the rule laid down in Article 29 of the Organic Law and in Article 53 of the Bank’s Statutes. The Brussels Commercial Court declared the action unfounded and ruled that the foreign exchange gains realised, forming the subject of an additional write-back, were correctly included in the sharing between the Bank and the sovereign State under the rule laid down by those two provisions.

40 Corporate Report 2007

Board of Directors

The Board of Directors met 44 times in 2007.

Members :Term of office expiry date

Mr Guy Quaden, governor 28 February 2009

Mr Luc Coene, vice-governor and secretary 3 August 2009

Mrs Marcia De Wachter, director 28 February 2011

Mr Jan Smets, director 28 February 2011

Mrs Françoise Masai, director 28 February 2011

Mr Jean Hilgers, director and treasurer 28 February 2011

Mr Peter Praet, director 29 October 2012

Mr Norbert De Batselier, director 31 August 2012

The curriculum vitæ of the directors is available on the Bank’s website.

Each of the directors can prove ownership of twenty-five registered shares in the Bank, as required by Article 34, 3° of the Statutes. The directors do not hold any share options or any rights to acquire shares. During the past year, they have not purchased or sold any Bank shares or other financial instruments relating to such shares.

The vice-governor and the directors also hold the follow-ing offices :

Mr Coene

Member of the EU Economic and Financial Committee, the ECB International Relations Committee, the Financial Stability Committee, the High Council of Finance and its Bureau, and Working Group No 3 of the OECD Economic Policy Committee ;

Alternate member of the Governing Council and General Council of the ECB, the G10 Committee of Governors and the International Monetary and Financial Committee ;

Head of the Public sector borrowing requirements section of the High Council of Finance.

Mrs De Wachter

Member of the Board of Directors of the CBFA, the Financial Stability Committee, the Belgian Institute of Public Finances and the Insurance Commission ;

Alternate member of the General Committee of the Professional Association of Public Credit Institutions ;

Adviser to the BIS Financial Stability Institute.

Mr Smets

Chairman of the Belgian Financial Forum Steering Committee and the Irving Fisher Committee on Central-Bank Statistics ;

Owing to the tasks in the public interest entrusted to it, the Bank is a special legal entity obeying its own particular rules.

Governance 41

Vice-chairman of the High Council of Employment ;

Director of the Belgian Institute of Public Finances ;

Alternate director of the BIS ;

Member of the Financial Stability Committee, the Securi-ties Regulation Fund Committee, the Board of Directors of the Deposits and Financial Instruments Protection Fund, the Study Group on Ageing (High Council of Finance), the OECD Economic Policy Committee and the Editorial Board of the International Journal of Central Banking ;

Alternate member of the Board of Directors of the National Accounts Institute.

Mrs Masai

Chairman of the Administrative Board of the Credit and Debt Observatory ;

Member of the CBFA Board of Directors, the Financial Stability Committee, the Administrative Board of the Ageing Fund and the Administrative Board of the Royal Institute of International Relations.

Mr Hilgers

Member of the Financial Stability Committee, the Securi-ties Regulation Fund Committee, the Board of Directors of the Deposits and Financial Instruments Protection Fund, the Belgian Institute of Public Finances, and the Public sector borrowing requirements section of the High Council of Finance.

Mr Praet

Chairman of the ECB Banking Supervision Committee ;

Member of the CBFA Board of Directors, the Financial Stability Committee, the Public sector borrowing require-ments section of the High Council of Finance, the Bureau of the High Council of Finance, the Committee of European Banking Supervisors, the Committee on the Global Financial System, the Basel Committee on Banking Supervision and the Committee on Payment and Settlement Systems ;

Alternate director of the BIS ;

Co-chairman of the Basel Committee on Banking Super-vision Research Task Force ;

Alternate member of the G10 Board of Governors and the International Monetary and Financial Committee ;

Member of the Board of the Brussels European and Global Economic Laboratory (BRUEGEL).

Mr De Batselier

Member of the Financial Stability Committee, the High Council of Finance and its Public sector borrowing requirements section, and the Board of Directors of the National Accounts Institute.

42 Corporate Report 2007

Council of Regency1

2

3

4

57

8

6

9

1418

19

10 13

11

1215

17

16

Governance 43

Council of Regency

The Council of Regency is composed of the governor, the directors and ten regents.

Members :Term of office expiry date

Mr Noël Devisch (1) : 30 March 2009

Mr Gérald Frère (2) : 29 March 2010

Mr Jacques Forest (1) : 31 March 2008

Mr Luc Cortebeeck (3) : 30 March 2009

Mrs Martine Durez (2) : 29 March 2010

Mr Rudi Thomaes (1) : 30 March 2009

Mr Christian Van Thillo (2) : 31 March 2008

Mr Didier Matray (2) : 31 March 2008

Mr Rudy De Leeuw (3) : 29 March 2010

Mr Pierre Wunsch (2) : 30 March 2009

On 14 March 2007, Mr Christian Dumolin resigned as regent. The most senior Dutch-speaking regent appointed by the Minister of Finance, he took that decision in the interests of the Bank, to permit the nomination of

1 Rudi Thomaes, regent2 Didier Matray, regent3 Luc Cortebeeck, regent4 Jean Hilgers, director5 Pierre Wunsch, regent6 Luc Coene, vice-governor7 Christian Van Thillo, regent8 Norbert De Batselier, director9 Marcia De Wachter, director10 Peter Praet, director

(1) On the proposal of the most representative organisations from industry and commerce, from agriculture and from small and medium-sized enterprises and traders.

(2) On the proposal of the Minister of Finance.

(3) On the proposal of the most representative labour organisations.

11 Rudy De Leeuw, regent12 Jean-Pierre Arnoldi, representative of the

Minister of Finance13 Jacques Forest, regent14 Guy Quaden, governor15 Martine Durez, regent16 Jan Smets, director17 Gérald Frère, regent18 Françoise Masai, director19 Noël Devisch, regent

Mr Rudy De Leeuw to represent one of the labour organi-sations legally entitled to a representative on the Council of Regency. The statutory obligation requiring the Council of Regency to comprise equal numbers of French and Dutch speakers prevented the nomination of Mr De Leeuw, a Dutch speaker, to replace Mr Mordant, a French speaker. The Bank thanked Mr Dumolin for taking this action, which enables the labour organisations to maintain their top-level representation on the Council of Regency, but it regretted the loss of an active and competent member who has always devoted so much effort on behalf of the Bank and the public interest.

The ordinary general meeting on 26 March 2007 renewed the terms of office of the regents, Mr Gérald Frère and Mrs Martine Durez. Messrs Rudy De Leeuw and Pierre Wunsch were elected as regents to replace Messrs André Mordant and Christian Dumolin respectively. The term of office of Mr Wunsch, who replaces Mr Dumolin, will end at the close of the ordinary general meeting in 2009. The other terms of office will end at the close of the ordinary general meeting in 2010. The meeting on 26 March 2007 conferred the title of honorary regent on Messrs André Mordant and Christian Dumolin.

In practice, the Council of Regency meets at least three times a month, except during July and August, when it meets only once. It met thirty-three times in 2007.

44 Corporate Report 2007

Board of Censors

1

23 6

7

4

5

8 10

9

Governance 45

Board of Censors

Members :Term of office expiry date

Baron Paul Buysse 29 March 2010

Mr Philippe Grulois 30 March 2009

Mr Rik Branson 31 March 2008

Mr Jean-François Hoffelt 30 March 2009

Mr Guy Haaze 31 March 2008

Mr Bernard Jurion 30 March 2009

Mr Luc Carsauw 26 March 2010

Mrs Michèle Detaille 31 March 2008

Mr Michel Moll 31 March 2008

Mr Jean-François Cats 29 March 2010

The ordinary general meeting on 27 March 2007 renewed the terms of office Baron Paul Buysse and Mr Luc Carsauw. Mr Jean-François Cats was elected censor to replace Mr Maurice Charloteaux. These three terms of office will expire at the close of the ordinary general meeting in 2010. The meeting conferred the title of honorary censor on Mr Maurice Charloteaux.

The Board of Censors met eight times in 2007.

Budget Committee and Remuneration Committee

Since 14 February 2007, the former Committee for the budget and directors’ remuneration has been replaced by the Budget Committee and the Remuneration Committee.

The Budget Committee is composed as follows :

Chairman : Baron Paul Buysse, censor ;

Mr Luc Coene, vice-governor ;

Mr Gérald Frère, regent ;

Mrs Martine Durez, regent ;

Mr Philippe Grulois, censor ;

Mr Jean-Pierre Arnoldi, representative of the Minister of Finance.

This Committee met once in 2007.

The Remuneration Committee is composed as follows :

Chairman : Mr Gérald Frère, regent ;

Mrs Martine Durez, regent ;

Baron Paul Buysse, censor ;

Mr Philippe Grulois, censor ;

Mr Jean-Pierre Arnoldi, representative of the Minister of Finance.

This Committee did not meet in 2007.

1 Luc Carsauw2 Jean-François Hoffelt3 Bernard Jurion4 Michel Moll5 Michèle Detaille

6 Jean-François Cats7 Rik Branson8 Baron Paul Buysse, president9 Guy Haaze10 Philippe Grulois, secretary

46 Corporate Report 2007

out that the ordinary general meeting of the Bank has no power to approve the annual accounts, decide on the administration and management, or grant a discharge to the Bank’s administrative organs.

Auditor

The firm Ernst & Young Bedrijfsrevisoren/Réviseurs d’entreprises, represented by Mr Marc Van Steenvoort, acts as the Bank’s auditor and was appointed by the ordi-nary general meeting on 29 March 2005 for a renewable term of three years. The renewal of the appointment of Ernst & Young Bedrijfsrevisoren/Réviseurs d’entreprises for a three-year term will be proposed at the ordinary general meeting on 31 March 2008.

Disclosure of posts held and assets

The members of the Board of Directors and the regents and censors are subject to the obligations arising from the laws of 2 May 1995 and 26 June 2004 concerning the disclosure of posts held and assets.

Governance statement and rules of procedure

The Council of Regency approved the amendments to the governance statement and the Bank’s rules of procedure.

In accordance with Article 20.2 of the Organic Law, the rules of procedure include basic rules on the activities of

In view of the particular functions of the Bank connected with its role as a central bank, it has been endowed by law with its own particular legal framework.

Representative of the Minister of Finance

Since 1 September 2005, the post of representative of the Minister of Finance has been filled by Mr Jean-Pierre Arnoldi, Treasury director general and acting chairman of the Board of Directors of the Federal Public Service Finance.

General Meeting