artigo em ingles - bcu.gub.uy de economa... · regime has changed, with a tendency to lower selic...

TRANSCRIPT

A New Structural Change in the Reaction Function of the Brazilian Central Bank*

Paulo Chananeco F. de Barcellos Neto**

Tatiana Silva F. de Barcellos***

Abstract

Brazil has been adopting the successful inflation targeting regime for over a decade and since 2011 the Central Bank is under the command of Alexandre Tombini. Despite the commitment made for inflation control, the level of interest rate has been constantly reduced in recent years, reaching the lowest level since the implementation of the system. Thus, this paper aims to investigate, using the Taylor Rule (1993), if the country is with the real opportunity to reduce the interest rate or if it is taking a risk behavior that could lead to future problems. In fact, the estimated results show that the conduct of the regime has changed, with a tendency to lower Selic rate. The characteristics of this trend, however, are subjective and recent, so they can’t be considered permanent.

Key words: Monetary Policy; inflation targeting regime; interest rate; Taylor’s Rule. JEL Classification: E4, G1.

1. Introduction

The way as central banks determine its interest rates awakens the attention of economic agents, for the impacts on different sectors of the economy. Its importance is evidenced both in fact that many central banks use the benchmark interest rate as the main monetary policy instrument and the impact that it causes on consumption decisions, capital flows into the country, activity level and supply and credit demand in the economy.

In the 1980s and 1990s, Brazil had a hyperinflationary reality which had been discontinued with the introduction of the Real Plan (1994). In 1999, the country stopped using the fixed exchange rate regime and has adopted the inflation targeting regime, which provided a better economic stability from this determination. However, its interest rates are still in higher levels than developed countries that adopt the same system. * The authors would like to thank the comments of the economists Marcelo Portugal, Alexandre Barbosa

and Luiz Gustavo Furlani. **

PhD in Economics (UFRGS), Banco Cooperativo SICREDI S/A. ***

Economist (UFRGS), Badesul Desenvolvimento S/A.

2

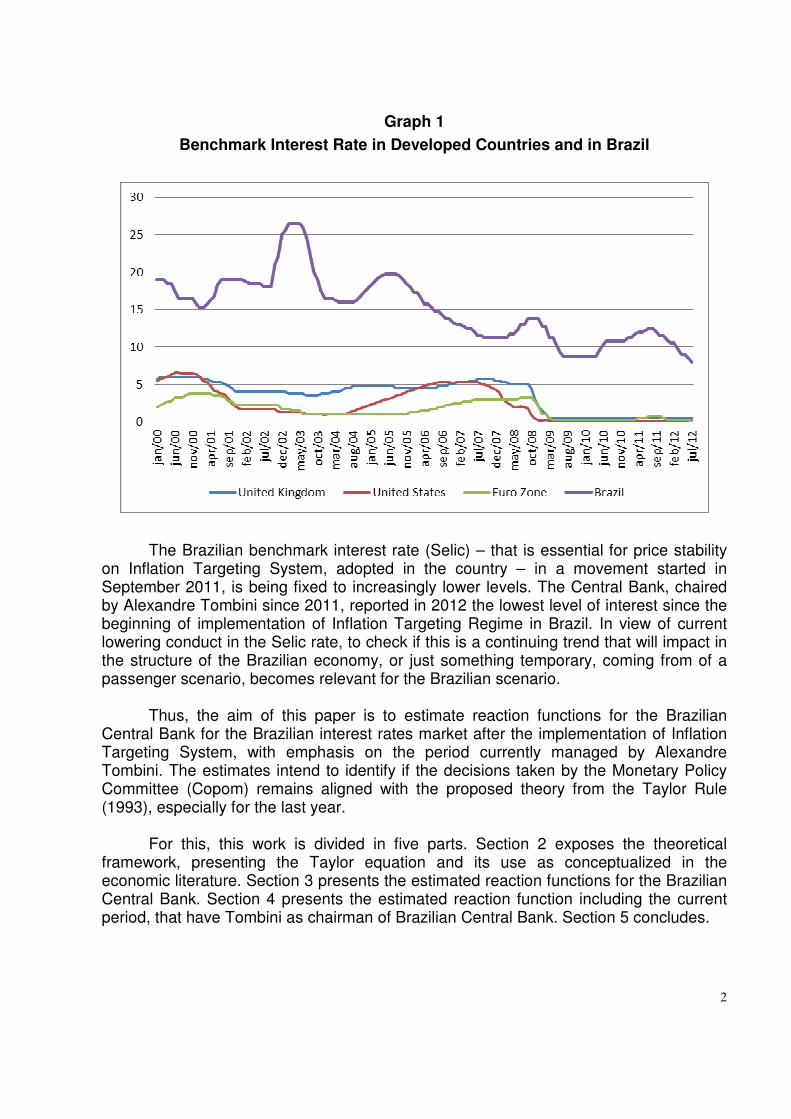

Graph 1

Benchmark Interest Rate in Developed Countries and in Brazil

The Brazilian benchmark interest rate (Selic) – that is essential for price stability on Inflation Targeting System, adopted in the country – in a movement started in September 2011, is being fixed to increasingly lower levels. The Central Bank, chaired by Alexandre Tombini since 2011, reported in 2012 the lowest level of interest since the beginning of implementation of Inflation Targeting Regime in Brazil. In view of current lowering conduct in the Selic rate, to check if this is a continuing trend that will impact in the structure of the Brazilian economy, or just something temporary, coming from of a passenger scenario, becomes relevant for the Brazilian scenario.

Thus, the aim of this paper is to estimate reaction functions for the Brazilian Central Bank for the Brazilian interest rates market after the implementation of Inflation Targeting System, with emphasis on the period currently managed by Alexandre Tombini. The estimates intend to identify if the decisions taken by the Monetary Policy Committee (Copom) remains aligned with the proposed theory from the Taylor Rule (1993), especially for the last year.

For this, this work is divided in five parts. Section 2 exposes the theoretical framework, presenting the Taylor equation and its use as conceptualized in the economic literature. Section 3 presents the estimated reaction functions for the Brazilian Central Bank. Section 4 presents the estimated reaction function including the current period, that have Tombini as chairman of Brazilian Central Bank. Section 5 concludes.

3

2. The Taylor Rule and further studies about the reaction function

To analyze the behavior of interest rates, we will use the rule proposed by Taylor (1993), which purports to explain the interest rate that compensates U.S. treasuries through a linear equation, which is called Taylor Rule.

The Taylor Rule argues that credible and transparent rules should be used to

guide monetary policy, because this is the most effective way to measure better performance results - that is essential for the Inflation Targeting System. The work is known, however, by using the reaction function - an information structure that can adequately represent the evolution of interest rates by central banks along the time - to the behavior of domestic interest rates in the U.S. over the period 1987 and 1992. This function, which is already widely used and known in the economic literature, has the following form:

)(5,0*)(5,0* tttt yri +−++= πππ (1)

Where,

i = interest rates of U.S. Federal Funds;

r* = equilibrium interest rate;

π = inflation rate (measured by GDP deflator);

π* = inflation target;

y = percentage deviation of real output from potential output.

Using as reference the work of Taylor, many authors estimated empirical reaction functions. Clarida, Galí and Gertler (1998) estimate reaction functions for France, Germany, Italy, Japan, UK and USA, seeking to characterize how central banks conducted their monetary policies since 1979. The study includes lagged explanatory variables and agents expectations regarding the evolution of output and inflation.

Judd and Rudebusch (1998) analyzed the monetary policy of the United States

between 1970 and 1997 by applying a dynamic version of the Taylor Rule. In this paper, there was different reaction functions, considering that during the period the Fed was chaired by three presidents: Arthur Burns, Paul Volcker and Alan Greenspan. The authors found that results relate movements in interest rates with a monetary policy that aims at low inflation and economic growth around its potential in the short term. It was found also that the period for which the Taylor Rule is best adapted was in the decision made by Allan Greenspan. However, as in other studies, the results differ from the original specifications of Taylor in two aspects: interest rates react more strongly to deviations of GDP than the original article supposed and the adjustment speed seems to be softer than Taylor proposed.

4

Regarding the case of Brazil, Garcia, Medeiros and Salgado (2002) conducted a

study on the behavior of the Brazilian monetary authority from 1994 to 2000, before the adoption of inflation targeting regime in the country. In addition to the traditional variables, the authors used the percentage change in international reserves component of explanatory Selic rate. Therefore, the choice to insert this variable is related with the fact that the country uses the exchange rate band system as the mains monetary policy instrument before Inflation Targeting System, and the fact that the monetary authorities have the primary function inflation through different elements than at the current regime.

The work of Modenezi (2008) estimates a reaction function for Brazil in the period

between 2000 and 2007. The model investigates the existence of conservatism in the Brazilian monetary policy, preventing a considerable reduction of the Selic rate. The estimated reaction function brings, differing from the original model, the incidence of two inflation rates – the free and the administrated - to verify whether the Brazilian monetary authority responds differently to these variables. The observation made is that the central bank reacts more strongly against free inflation rates than the administrated rate. Furthermore, the author notes that the rising and the falling on inflation are reflected in interest rate in a too soft way.

Minella and Souza-Sobrinho (2009) conducted a study for the Brazilian economy

during the period of inflation targeting. The model investigates the monetary policy transmission mechanisms and brings features of the Brazilian economy. The monetary channels are presented: the family’s interest rate, the firm’s interest rate and the exchange rate. The authors found that the interest rate channel of the families is the most important mechanisms to explain the dynamic of the output. Both the interest rate on families, as the exchange rate are important for the transmission. For inflation, the best indicator is a proxy for expectations. Thus, the authors conclude that interest rates in the domestic market are significantly sensitive to monetary policy.

Aragon and Portugal (2009) investigated the preferences of the Brazilian Central

Bank on the conduct of monetary policy on inflation targeting system. The authors seek to estimate the preferences of the Brazilian monetary authority, which they consider to be something very important since it allows checking if the economic results are consistent with the structure of optimal monetary policy. The authors assume that the Central Bank of Brazil uses past expectations to solve the intertemporal optimization problem. The calculation of the optimal rule for determining the benchmark interest rate by the Central Bank is estimated by a function of the monetary authority from the choice of preference parameters that minimize the deviation between the optimal way and the way of the observed Selic. The result shows that the Central Bank of Brazil adopts a flexible inflation targeting system, with emphasis on stabilizing inflation and interest rate mitigation.

Caetano, Silva Jr and Correa (2011) investigate - through a discrete non stationary approach in modeling the Brazilian interest rate - the Monetary Policy

5

Committee interventions in the prime interest rate. The authors examine the decisions of the Monetary Policy Committee in accordance with the decisions of high, low, or maintenance of the Selic rate as a discrete variable rather than continuous, as commonly studied. The proposed model is shown parsimonious and allows the estimated parameters that define the initial decisions taken by the committee are asymmetrical and cannot find significant differences between the high and the low thresholds.

3. Reaction Function in Inflation Targeting Regime

The estimative of a reaction function for the Central Bank was performed based on sub-optimal structure proposed by Taylor (1993), with adaptations to the estimated empirical realities of Brazil. In particular, the estimates investigated the entire period with the inflation targeting regime in Brazil, started in 1999 and in force in the country. The purpose of the estimates was to investigate whether there was a change behavior of the monetary authority in the new government, in view of the current level in the basic interest rate (Selic), the lowest in Brazil since the scheme was implemented.

For the realization of the estimates, the variables used were mostly the traditional in articles with the same purpose, as well as in Barcellos (2008). Initially, the Selic rate was used to estimate with the time lags necessary, as the exchange rate. Additionally, a variable dummy was used for October 2002 in some estimates, because of the atypical economic context which had marked the end of Arminio Fraga's presidency1. Thus, among the group used, three variables deserve further explanations.

The first variable to clarify is the form to use the inflation expectations in the

reaction function model. As in Barcellos (2008), before the existence of an intertemporal behavior for the monetary authority in its decisions, the desired inflation target, although annual, must not be fixed until the end of the year, earning a treatment proposal. It is very probable that at each meeting of the monetary authority in the beginning of the year, it takes its decisions seeking to reach the target of the current year. However, this issue is no longer trivial when seeking to explain how the monetary authority is acting, for example, a decision by mid-year. Certainly, in the last meeting of the year, the current inflation has less importance than the trends for inflation of the next year.

In this context, it was used a series called Dj, which is a linear combination of the

market expectations for inflation gap (IPCA) in relation to the mark of mixed form between the present year (t) composed with the behavior expected for next year (t +1). This composition is performed using a weighted average of deviations from expectation in relation to targets set by the monetary authority. The purpose of the variable is to obtain a number that reflects the actual search of the monetary authority over time for inflation. Thus, this indicator can be interpreted as an index that reflects the deviations of 1 For more informations, read Barcellos (2008).

6

expected inflation from the target of this year, which goes losing value in relevance to potential deviations of the following year. Mathematically, we have:

( ) ( )11 *

12*

12

12++ −

+−

−= ttjttj E

jE

jDj ππππ (2)

Where,

Dj: weighted deviation of expected inflation from the target inflation;

Ejπt: expectation of the month j for the IPCA of the year t;

πt*: center of the target inflation for the year t;

Ejπt+1: expectation of the month j for the IPCA of the year t+1;

πt+1*: center of the target inflation for the year t+1;

The second series that was treated in a special way is the economic activity and their gap. Although recent data that aim to measure the monthly activity2 in Brazil, due to the broad term, was retained for use as a proxy of the product series of monthly industrial production (IBGE) seasonally adjusted, and as potential product, the series obtained using the Hodrick-Prescott filter.

Finally, with the main purpose of to measure whether there was some change in the structure of the reaction function from Tombini’s mandate in the monetary authority of Brazil, it was added to the model a dummy variable. Thus, the variable that began in January 2011, aims to identify whether their falls in the benchmark interest rate was a natural movement of the regime, or reflect of any change in the conduction form by the Central Bank on monetary policy regime.

In this context, the first estimate had the objective to measure the broad reaction function since the beginning of the inflation targeting regime (2000) until the recent period (July 2012), representing the base of controlling inflation and being one of the comparisons in Tombini management. Estimates performed followed the following structure:

1542321 2002_ −−− ++++= toutttjtt CDyDjii βββββ (3)

Where,

it : benchmark interest rate Selic monthly; 2 Although the series IBC-BR is very interesting to measure the Brazilian GDP, as it started to be conducted in 2003, it wasn’t used because doesn’t include the hole period that this study encompasses.

7

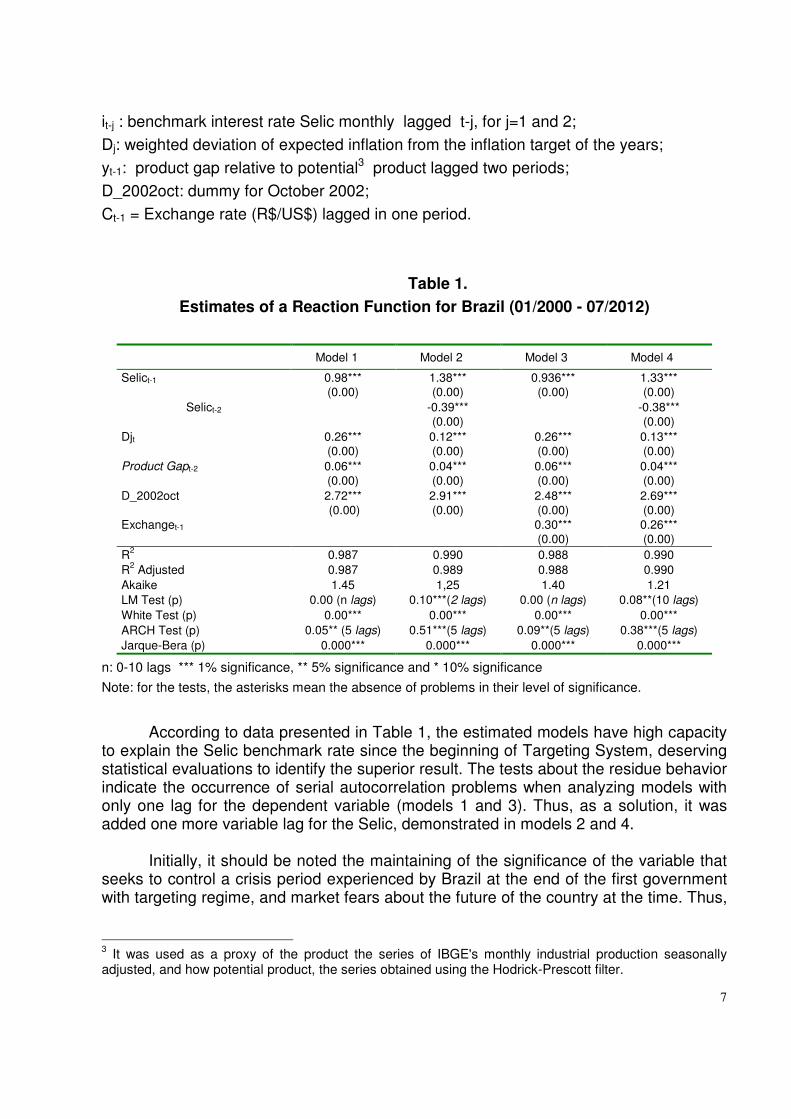

it-j : benchmark interest rate Selic monthly lagged t-j, for j=1 and 2;

Dj: weighted deviation of expected inflation from the inflation target of the years;

yt-1: product gap relative to potential3 product lagged two periods;

D_2002oct: dummy for October 2002;

Ct-1 = Exchange rate (R$/US$) lagged in one period.

Table 1.

Estimates of a Reaction Function for Brazil (01/2000 - 07/2012)

Model 1 Model 2 Model 3 Model 4

Selict-1 0.98*** (0.00)

1.38*** (0.00)

0.936*** (0.00)

1.33*** (0.00)

Selict-2 -0.39*** (0.00)

-0.38*** (0.00)

Djt 0.26*** (0.00)

0.12*** (0.00)

0.26*** (0.00)

0.13*** (0.00)

Product Gapt-2 0.06*** (0.00)

0.04*** (0.00)

0.06*** (0.00)

0.04*** (0.00)

D_2002oct Exchanget-1

2.72*** (0.00)

2.91*** (0.00)

2.48*** (0.00) 0.30*** (0.00)

2.69*** (0.00) 0.26*** (0.00)

R2 0.987 0.990 0.988 0.990 R2 Adjusted 0.987 0.989 0.988 0.990 Akaike 1.45 1,25 1.40 1.21 LM Test (p) 0.00 (n lags) 0.10***(2 lags) 0.00 (n lags) 0.08**(10 lags) White Test (p) 0.00*** 0.00*** 0.00*** 0.00*** ARCH Test (p) 0.05** (5 lags) 0.51***(5 lags) 0.09**(5 lags) 0.38***(5 lags) Jarque-Bera (p) 0.000*** 0.000*** 0.000*** 0.000***

n: 0-10 lags *** 1% significance, ** 5% significance and * 10% significance

Note: for the tests, the asterisks mean the absence of problems in their level of significance.

According to data presented in Table 1, the estimated models have high capacity to explain the Selic benchmark rate since the beginning of Targeting System, deserving statistical evaluations to identify the superior result. The tests about the residue behavior indicate the occurrence of serial autocorrelation problems when analyzing models with only one lag for the dependent variable (models 1 and 3). Thus, as a solution, it was added one more variable lag for the Selic, demonstrated in models 2 and 4.

Initially, it should be noted the maintaining of the significance of the variable that

seeks to control a crisis period experienced by Brazil at the end of the first government with targeting regime, and market fears about the future of the country at the time. Thus,

3 It was used as a proxy of the product the series of IBGE's monthly industrial production seasonally adjusted, and how potential product, the series obtained using the Hodrick-Prescott filter.

8

the dummy variable for October 2002 remained significant in the estimated models, despite being relatively far from today.

The significance of the exchange rate behavior as an explanatory variable is the

differential of the models presented in the Table 1, as already observed in Barcellos (2008), making the models 3 and 4 present higher statistical results and demonstrating the exchange rate as an important variable in the Brazilian monetary policy conduct.

In the functional structure of the model 3, it is noteworthy that the deviation of the

weighted expectations (Dj) and the exchange rate appear as exogenous variables with important weights for decision of Monetary Policy Committee, with values of 0.26 and 0.30, respectively, and accepted with 1% significance level. Besides Barcellos (2008), these characteristics had been already observed in earlier Brazilian works, as Minella, Freitas, Goldfajn and Muinhos (2002).

Because of the statistical tests applied to models, model 4 managed all elements of accessibility, more successfully illustrating the behavior of the Central Bank along the years since the adoption of inflation targeting. In this case, the exchange rate appeared as major variable in the decision making process. However, deviations of inflation expectations in relation the target remain relevant, being monitored in a hybrid form in a two years moving horizon. The models estimated in this way presented a very stable regime in Brazil over the last twelve years, but may be omitting some change with the arrival of new team, factor estimated.

4. Reaction Function with Alexandre Tombini

In 2010, after the presidential elections that happened in Brazil, the president of the Central Bank was changed, leading Alexandre Tombini to take charge of the monetary authority in January 2011. The new president, being a career officer of the institution since 1998, followed and participated of the implementation of the inflation targeting regime in Brazil. Thus, the expectations were of continuity in the conduct of policy determining interest rate.

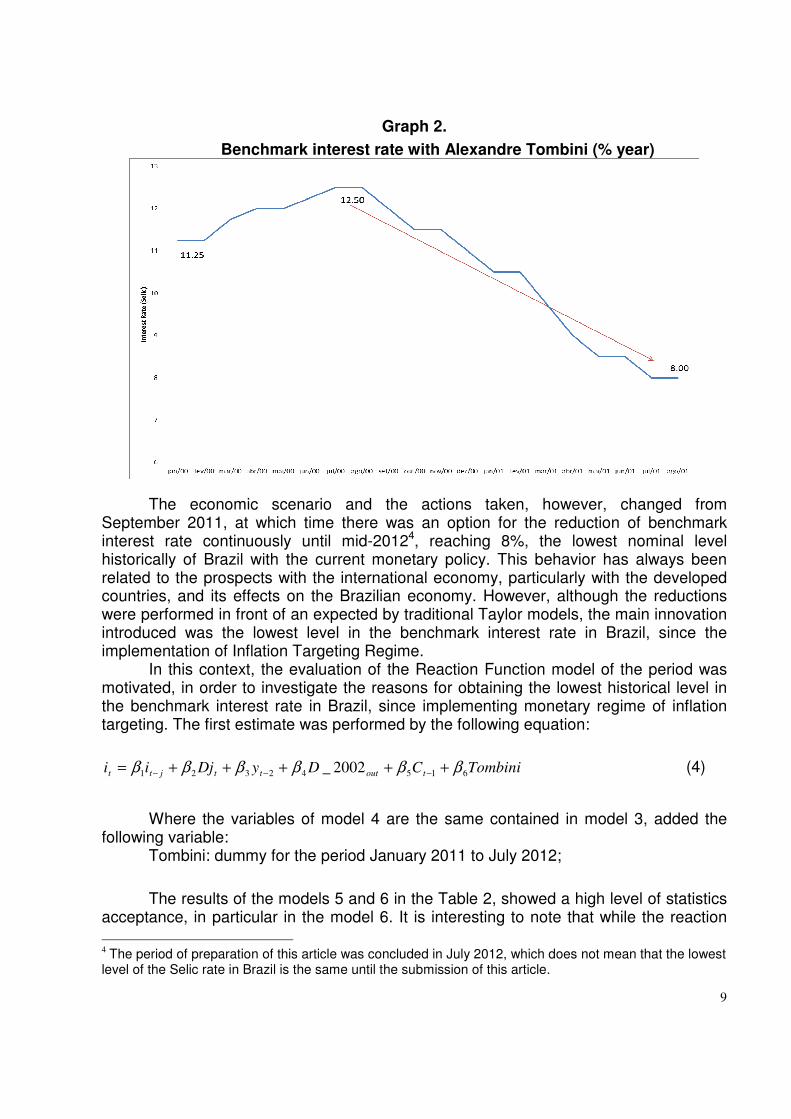

In 2010, inflation in Brazil (IPCA) was close to the target ceiling, reaching 5.91%,

and market expectations were of high movements in the Selic rate in the first months of the new governor. In fact, in January 2011, Copom decided to raise the prime rate Selic to 11.25% per year, marking the beginning of the high process, which after some elevations made the monetary authority reach 12.5% per year in July. Thus, the initial attitudes of the monetary authority followed the historical behavior of monetary policy in Brazil.

9

Graph 2.

Benchmark interest rate with Alexandre Tombini (% year)

The economic scenario and the actions taken, however, changed from September 2011, at which time there was an option for the reduction of benchmark interest rate continuously until mid-20124, reaching 8%, the lowest nominal level historically of Brazil with the current monetary policy. This behavior has always been related to the prospects with the international economy, particularly with the developed countries, and its effects on the Brazilian economy. However, although the reductions were performed in front of an expected by traditional Taylor models, the main innovation introduced was the lowest level in the benchmark interest rate in Brazil, since the implementation of Inflation Targeting Regime.

In this context, the evaluation of the Reaction Function model of the period was motivated, in order to investigate the reasons for obtaining the lowest historical level in the benchmark interest rate in Brazil, since implementing monetary regime of inflation targeting. The first estimate was performed by the following equation:

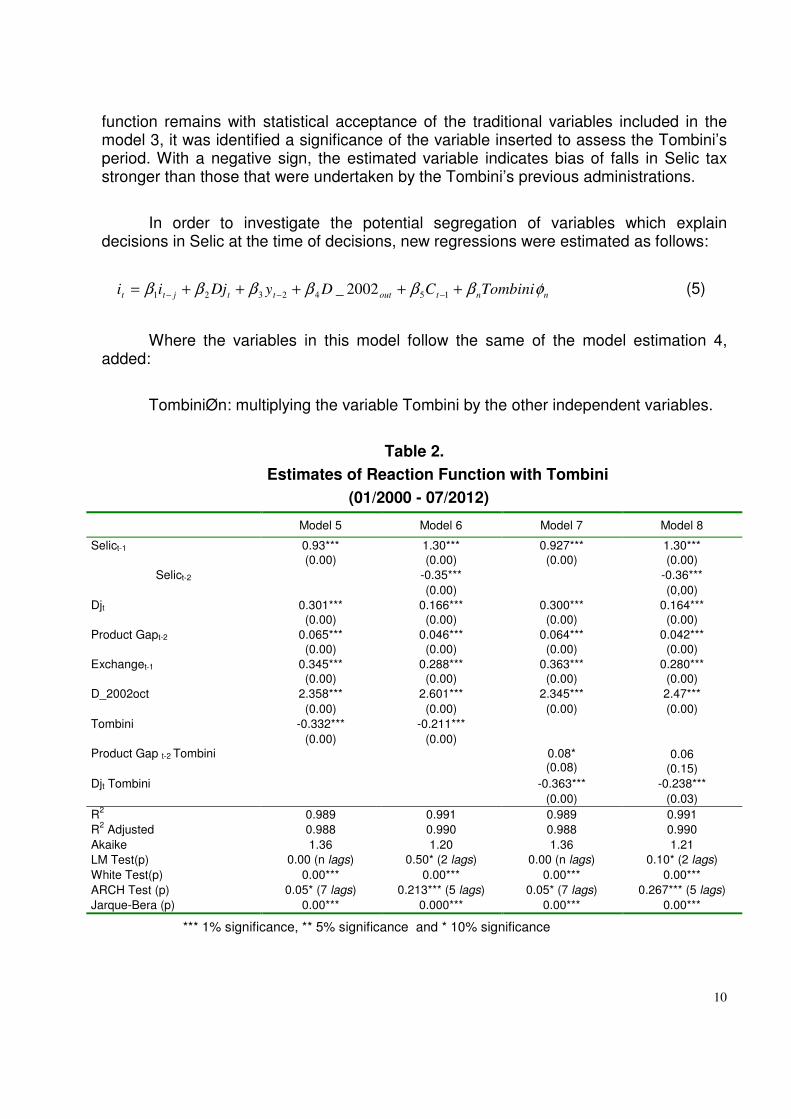

TombiniCDyDjii toutttjtt 61542321 2002_ ββββββ +++++= −−− (4)

Where the variables of model 4 are the same contained in model 3, added the following variable:

Tombini: dummy for the period January 2011 to July 2012;

The results of the models 5 and 6 in the Table 2, showed a high level of statistics acceptance, in particular in the model 6. It is interesting to note that while the reaction 4 The period of preparation of this article was concluded in July 2012, which does not mean that the lowest

level of the Selic rate in Brazil is the same until the submission of this article.

10

function remains with statistical acceptance of the traditional variables included in the model 3, it was identified a significance of the variable inserted to assess the Tombini’s period. With a negative sign, the estimated variable indicates bias of falls in Selic tax stronger than those that were undertaken by the Tombini’s previous administrations.

In order to investigate the potential segregation of variables which explain decisions in Selic at the time of decisions, new regressions were estimated as follows:

nntoutttjtt TombiniCDyDjii φββββββ +++++= −−− 1542321 2002_ (5)

Where the variables in this model follow the same of the model estimation 4, added:

TombiniØn: multiplying the variable Tombini by the other independent variables.

Table 2.

Estimates of Reaction Function with Tombini

(01/2000 - 07/2012)

Model 5 Model 6 Model 7 Model 8

Selict-1 0.93*** (0.00)

1.30*** (0.00)

0.927*** (0.00)

1.30*** (0.00)

Selict-2 -0.35*** -0.36*** (0.00) (0,00) Djt 0.301***

(0.00) 0.166*** (0.00)

0.300*** (0.00)

0.164*** (0.00)

Product Gapt-2 0.065*** (0.00)

0.046*** (0.00)

0.064*** (0.00)

0.042*** (0.00)

Exchanget-1 0.345*** (0.00)

0.288*** (0.00)

0.363*** (0.00)

0.280*** (0.00)

D_2002oct 2.358*** 2.601*** 2.345*** 2.47*** (0.00) (0.00) (0.00) (0.00) Tombini -0.332*** -0.211*** (0.00) (0.00) Product Gap t-2 Tombini

0.08* (0.08)

0.06 (0.15)

Djt Tombini -0.363*** -0.238*** (0.00) (0.03) R2 0.989 0.991 0.989 0.991 R2 Adjusted 0.988 0.990 0.988 0.990 Akaike 1.36 1.20 1.36 1.21 LM Test(p) 0.00 (n lags) 0.50* (2 lags) 0.00 (n lags) 0.10* (2 lags) White Test(p) 0.00*** 0.00*** 0.00*** 0.00*** ARCH Test (p) 0.05* (7 lags) 0.213*** (5 lags) 0.05* (7 lags) 0.267*** (5 lags) Jarque-Bera (p) 0.00*** 0.000*** 0.00*** 0.00***

*** 1% significance, ** 5% significance and * 10% significance

11

The results presented in models 7 and 8 reflect the estimated equations with acceptance of the econometrics tests, indicating that two variables started to present different weights in the meetings of the Monetary Policy Committee. The significant and positive behavior of the Variable Product Gap t-2 Tombini started to demonstrate that the decline in economic activity that occurred during the period analyzed, encouraged the decisions of reductions in the Selic. Thus, the daredevil ambient of the Brazilian activity during this period contributed to the reductions decisions in the Selic more than the behavior that had been observed in the country.

Another variable that was significant in the model changed was the center of the inflation target. The variable Djt Tombini was negative, indicating minor importance to the inflation gap relative to the target center. Therefore, inflation expectations above the target center lost the power of affect the monetary authority decisions in the period analyzed, governed by Tombini. Only the exchange rate doesn’t show a significance effect, indicating the maintenance of this variable in the decisions of the Monetary Policy Committee.

5. Conclusion

Maintaining the original work of Taylor (1993) as a structural reference, and evaluating the latest articles in Brazil, this study aimed to estimate reaction functions for the Central Bank of Brazil on the context of obtaining the lowest level of the benchmark interest rate (Selic), since the adoption of Inflation Targeting System. For this, the presentation of a literature review was necessary in the first moment, aiming at outlining how the recent literature has addressed the issue.

In the estimates of Reaction Function over targeting regime, it was noted that the traditional variables for the Brazilian case were kept and statistically relevant. However, the analysis performed from the segregation of the period of the three presidents of the monetary authority identified that the current management of Tombini, begun in 2011 and evaluated until July 2012, left to pursue the center of the inflation target, keeping the exchange rate importance similar to previous periods and passing to appreciate the behavior of economic activity so superior to the standard that was being observed.

In order to understand the changes identified, it is possible to raise four

hypotheses to explain this behavior. The first is related to the fact that during the period identified for Tombini, the international scenario has undergone a strong retractions in developed and developing countries, in such a way that the central bank would be acting with that attitude of retraction facing a new context. Another evaluation that is possible is that the central bank was enjoying this context seek to reduce the prime rate in order to break the paradigm of coexistence of high levels in the Selic rate in Brazil compared to other countries. Thus, the external context of many economic difficulties

12

would, on the other hand, allowing the Brazilian Central Bank to test a lower level on your interest rate in a secure way.

On the other hand, inflation ended the year 2011 at 6.5%, the upper limit of the

target assumed, and tends to end 2012 above the central target (4.5%). In this context, the change identified in the reaction function of Tombini estimated illustrates that the actions of decrease in benchmark interest rate gave very little attention to the center of the inflation target. In this case, the center of the inflation target would, in fact, being undervalued, which present high risks to the inflation targeting regime in the medium term and characterize a mismanagement of the regime in the country.

Considering these facts, the regressions performed become very interesting for

identifying behavioral changes and allow the emergence of hypotheses for the recent behaviors of inflation targeting regime in Brazil.

13

References

ARAGÓN, E.K.; PORTUGAL, M.S. Central Bank preferences and monetary rules under the inflation targeting regime in Brazil. Revista de Economia Brasileira, Rio de Janeiro, v.29, n.1, 2009.

BANCO CENTRAL DO BRASIL. Política Monetária. Relatório de Inflação, Brasília, v.1, n.3, p.21-30, dez. 1999.

BARCELLOS, P. C. F. N.. Structural Changes in the Reaction Function of the Brazilian Central Bank. XIII Jornadas Anuales de Economia. Banco Central do Uruguai, Montevidéu, 2008.

BERNANKE, B.; BLINDER, A. The Federal Funds Rate and the Channels of Monetary Transmission. American Economic Review, Nashville, v.82, p.901-921, 1992.

BUTTIGLIONE, L; TRISTANI, O. Monetary Policy Actions and the Term Structure of Rates: A Cross-Country Analysis, Roma: Banco da Itália, 1996. Mimeografado.

CAETANO, S.M.; CORREA, W.L.R.;SILVA JR., G. E. Abordagem discreta para a dinâmica da taxa Selic. Economia Aplicada.Ribeirão Preto, v.15, n. 2, 2011.

CLARIDA, R.; GALÍ, J.; GERTLER, M. Monetary Policy Rules in Practice: Some International Evidence. European Economic Review, v. 42, p.1033-1067, 1998.

COOK, T.; HAHN, T. The Effect of Changes in the Federal Funds Rate Target on Market Interest Rates in the 1970’s. Journal of Monetary Economics, Rochester, v.24, n.3, p.331-351, 1989.

DAVIDSON, R; MACKINNON, J. Estimation and Inference in Econometrics. Oxford, Oxford University Press, 1993.

ENGLE, R.; GRANGER, C. ARCH: Selected Readings. Oxford ,Oxford University Press, 1995.

FRAGA, A. Comment on Chapter 8. In: GIAVAZZI, F., GOLDFAJN, I., E HERRERA, S. (Ed.). Inflation Targeting, Debt and the Brazilian Experience, 1999 to 2003. London: MIT Press, p. 295-297, 2005.

GARCIA, M.; MEDEIROS, M.; SALGADO, M. Monetary Policy During Brazil’s Real Plan: Estimating the Central Bank’s Reaction Function. São Paulo: Departamento de Economia, FEA, USP, 2002. (Texto para Discussão, seminário n. 18).

HALDANE, A.; READ, V. Monetary Policy Surprises and the Yield Curve. Bank of England Working Paper, London, n. 106, p. 1-42, 2000.

HAMILTON, J. Time Series Analysis. Princeton: Princeton University Press, 1994.

14

JUDD, J.; RUDEBUSCH, G. Taylor´s Rule and the FED: 1970 - 1997. Federal Reserve Bank of San Francisco Economic Review, San Francisco, v.ø, p. 3-16, 1998.

McCALLUM, B. Recent Developments in The Analysis of Monetary Policy Rules. Federal Reserve Bank of St. Louis. Review, St. Louis, v. 81, p. 3-11, 1999.

McCALLUM, B.; NELSON, E. Nominal Income Targeting In An Open-Economy Optimizing Model. Journal of Monetary Economics, Rochester, v.43, p.553-578, 1999.

MEIRELLES, H. The Challenge of Economic Growth With Social Justice. Brasília: Banco Central do Brasil, 2003.

MINELLA, A. et al. Inflation Targeting in Brazil: Lessons and Challenges. Banco Central do Brasil Working Paper Series, Brasília, nº 53, p.1-48, 2002.

MINELLA, A.; SOUZA-SOBRINHO,N. Monetary Channels in Brazil throught the lens of a semi-structural model. Banco Central do Brasil, Working Paper Series, Brasília, n.181, p-1-57, 2009.

MODENESI, A.M. Convenção e Rigidez na Política Monetária:uma estimativa da função de reação do BCB (2000-2007). XXVI Encontro Nacional de Economia da ANPEC, Salvador, 2008.

MOHANLY, M.; KLAU, M. Monetary Policy Rules in Emerging Market Economies: Issues and Evidence. Bank for International Settlements Working Paper, Basel, n. 149, p.1-24, 2004.

MUINHOS, M.; ALVES, S. Modelo Macroeconômico de Médio Porte para a Economia Brasileira, Brasília: Banco Central do Brasil, 2002.

OLIVEIRA, A. Modelo de Estrutura a Termo de Taxas de Juros: Um Teste Empírico, 2003. Dissertação de Mestrado em Economia - Função Getúlio Vargas, Rio de Janeiro.

ROLEY, V.; GORDON, S. Monetary Policy Actions and Long Term Interest Rates. Federal Reserve Bank of Kansas City Economic Review, Kansas City, v.80, p.73-89, 1995.

TAYLOR, J. Discretion versus Policy Rules in Practice. Carnegie-Rochester Conference Series on Public Policy, Rochester, n.39, p. 195-214, 1993.

15

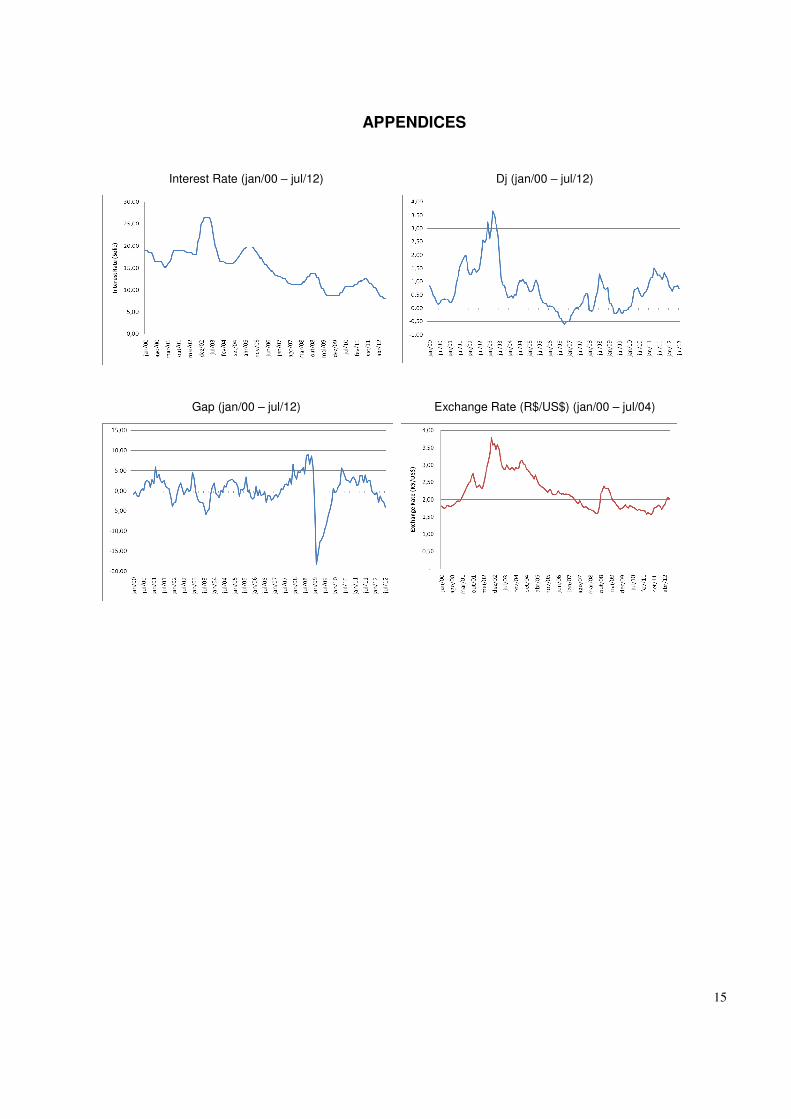

APPENDICES

Interest Rate (jan/00 – jul/12) Dj (jan/00 – jul/12)

Gap (jan/00 – jul/12) Exchange Rate (R$/US$) (jan/00 – jul/04)