b2b softwaare days: startups – investment, valuation and exit

TRANSCRIPT

Startups – Investment, Valuation and Exit

www.i5invest.com

2 | 28/04/2015

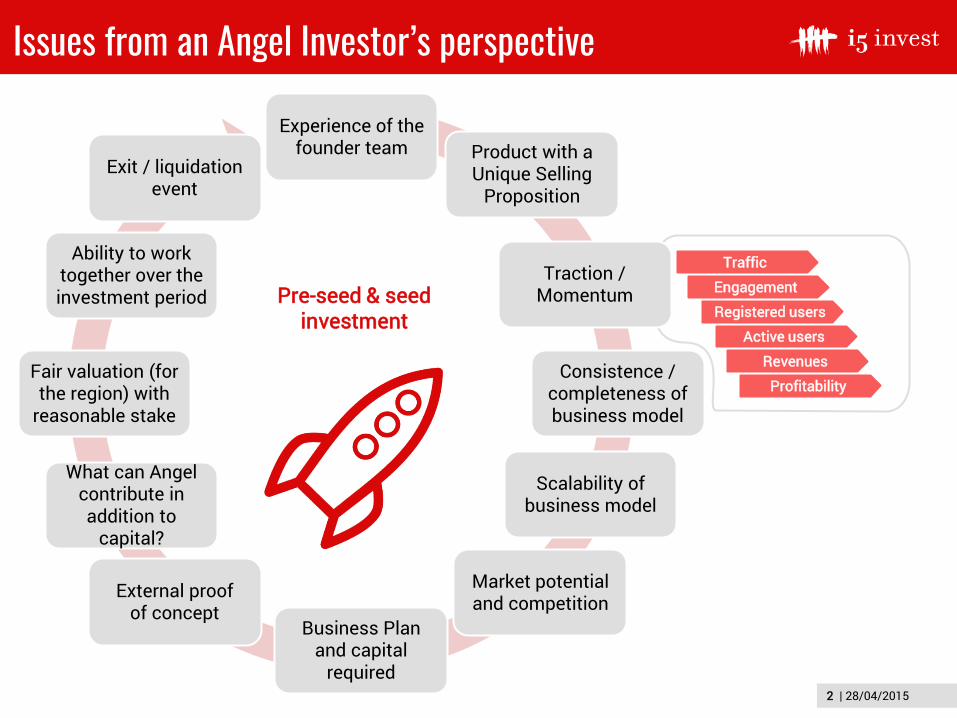

Experience of the founder team Product with a

Unique Selling Proposition

Traction / Momentum

Consistence / completeness of business model

Scalability of business model

Market potential and competition

Business Plan and capital

required

External proof of concept

What can Angel contribute in addition to

capital?

Fair valuation (for the region) with

reasonable stake

Ability to work together over the investment period

Exit / liquidation event

Issues from an Angel Investor’s perspective

28/04/2015

Traffic

Engagement

Registered users

Active users

Revenues

Profitability

Pre-seed & seed investment

3 | 28/04/2015

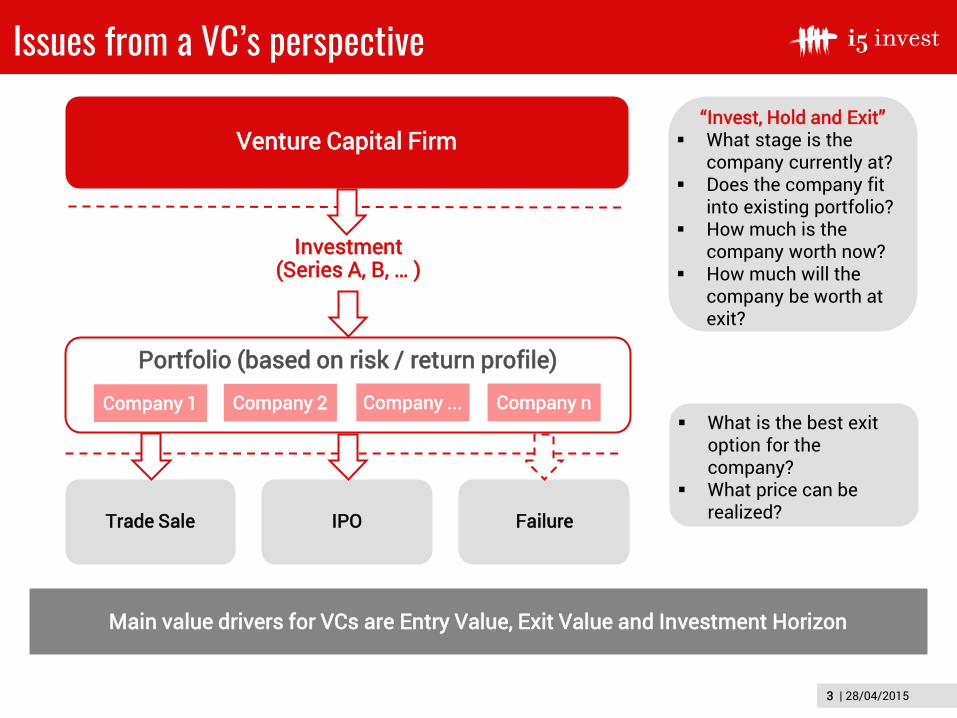

Issues from a VC’s perspective

28/04/2015

Venture Capital Firm

Portfolio (based on risk / return profile)

Failure IPO Trade Sale

What is the best exit option for the company?

What price can be realized?

“Invest, Hold and Exit”

What stage is the company currently at?

Does the company fit into existing portfolio?

How much is the company worth now?

How much will the company be worth at exit?

Main value drivers for VCs are Entry Value, Exit Value and Investment Horizon

Investment (Series A, B, … )

Company 1 Company 2 Company ... Company n

4 | 28/04/2015

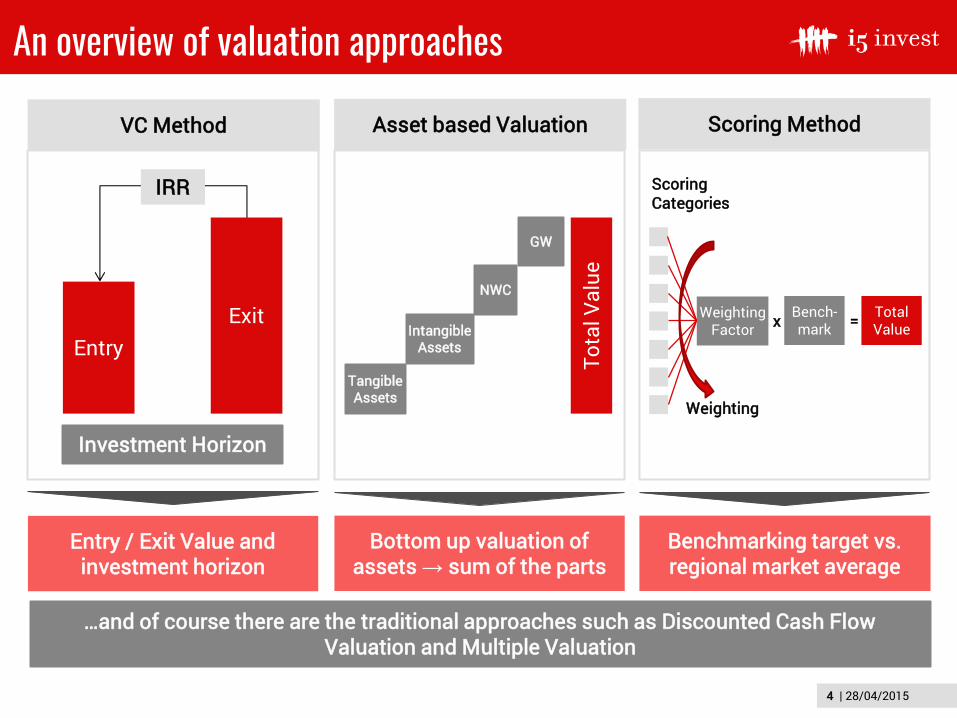

An overview of valuation approaches

VC Method Asset based Valuation Scoring Method

Entry / Exit Value and investment horizon

Bottom up valuation of assets → sum of the parts

Benchmarking target vs. regional market average

Entry Exit

IRR

Investment Horizon

Tangible Assets

NWC

Intangible Assets

GW

Tota

l Val

ue

Scoring Categories

Weighting Factor

Bench- mark

Total Value x =

Weighting

…and of course there are the traditional approaches such as Discounted Cash Flow Valuation and Multiple Valuation

5 | 28/04/2015

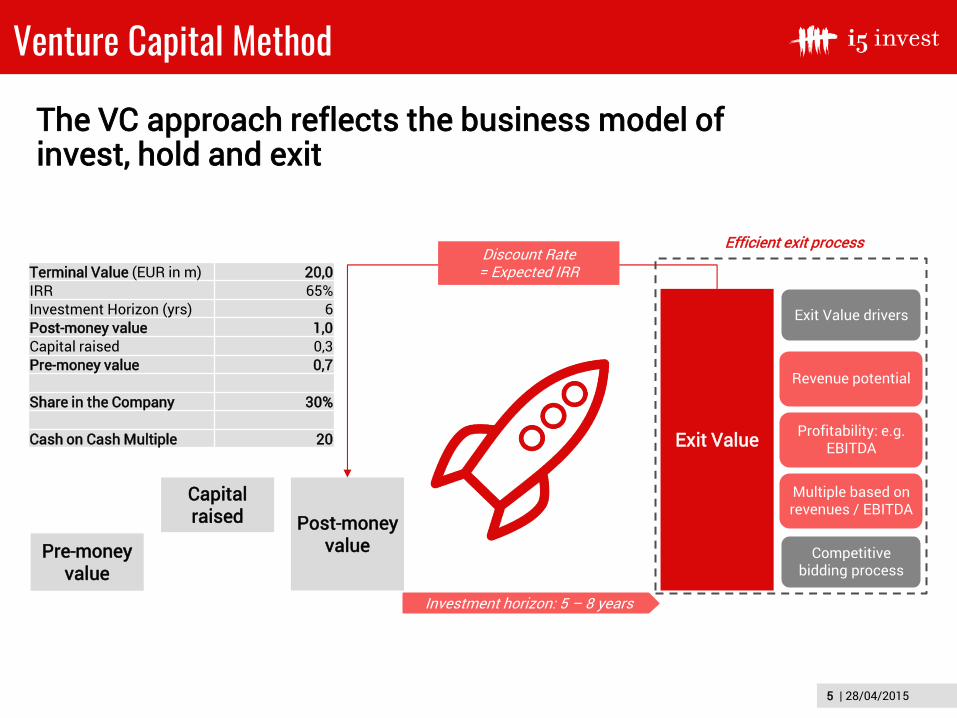

Venture Capital Method

The VC approach reflects the business model of invest, hold and exit

Pre-money value

Post-money value

Capital raised

Exit Value

Discount Rate = Expected IRR

Exit Value drivers

Revenue potential

Profitability: e.g. EBITDA

Multiple based on revenues / EBITDA

Competitive bidding process

Investment horizon: 5 – 8 years

Terminal Value (EUR in m) 20,0 IRR 65% Investment Horizon (yrs) 6 Post-money value 1,0 Capital raised 0,3 Pre-money value 0,7

Share in the Company 30%

Cash on Cash Multiple 20

Efficient exit process

6 | 28/04/2015

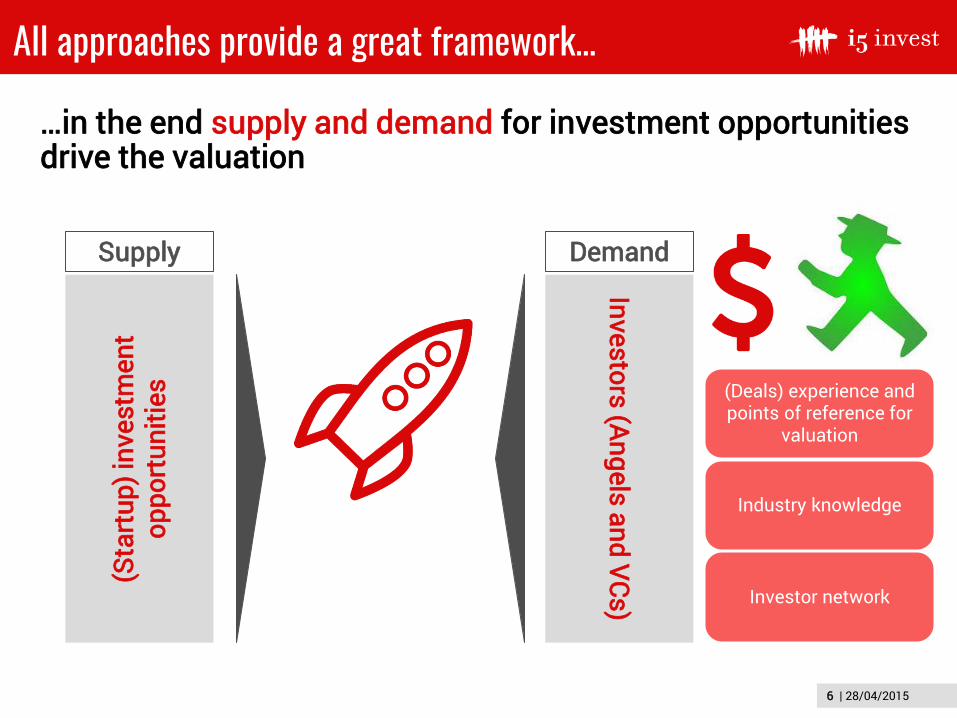

All approaches provide a great framework…

…in the end supply and demand for investment opportunities drive the valuation

(Sta

rtup

) inv

estm

ent

oppo

rtun

ities

Investors (Angels and VCs)

(Deals) experience and points of reference for

valuation

Industry knowledge

Investor network

Supply Demand

7 | 28/04/2015

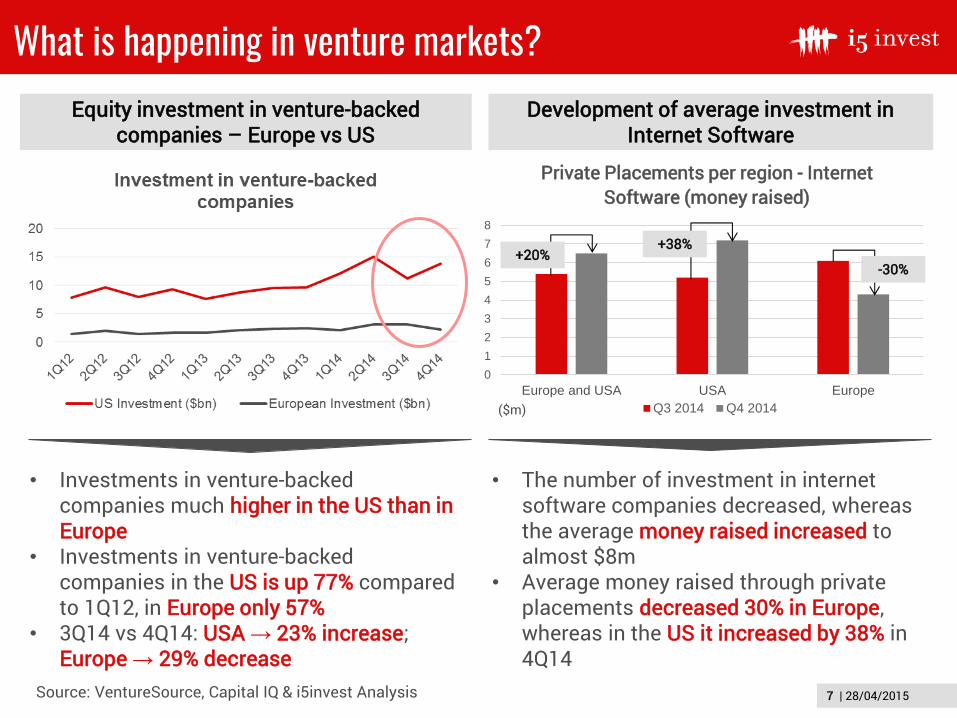

What is happening in venture markets?

4/28/2015

Equity investment in venture-backed companies – Europe vs US

Source: VentureSource, Capital IQ & i5invest Analysis

Development of average investment in Internet Software

0

1

2

3

4

5

6

7

8

Europe and USA USA Europe

Private Placements per region - Internet Software (money raised)

Q3 2014 Q4 2014

+20% +38%

-30%

($m)

• Investments in venture-backed companies much higher in the US than in Europe

• Investments in venture-backed companies in the US is up 77% compared to 1Q12, in Europe only 57%

• 3Q14 vs 4Q14: USA → 23% increase; Europe → 29% decrease

• The number of investment in internet software companies decreased, whereas the average money raised increased to almost $8m

• Average money raised through private placements decreased 30% in Europe, whereas in the US it increased by 38% in 4Q14

8 | 28/04/2015

+18%

+13% +15% +11%

+33% +12%

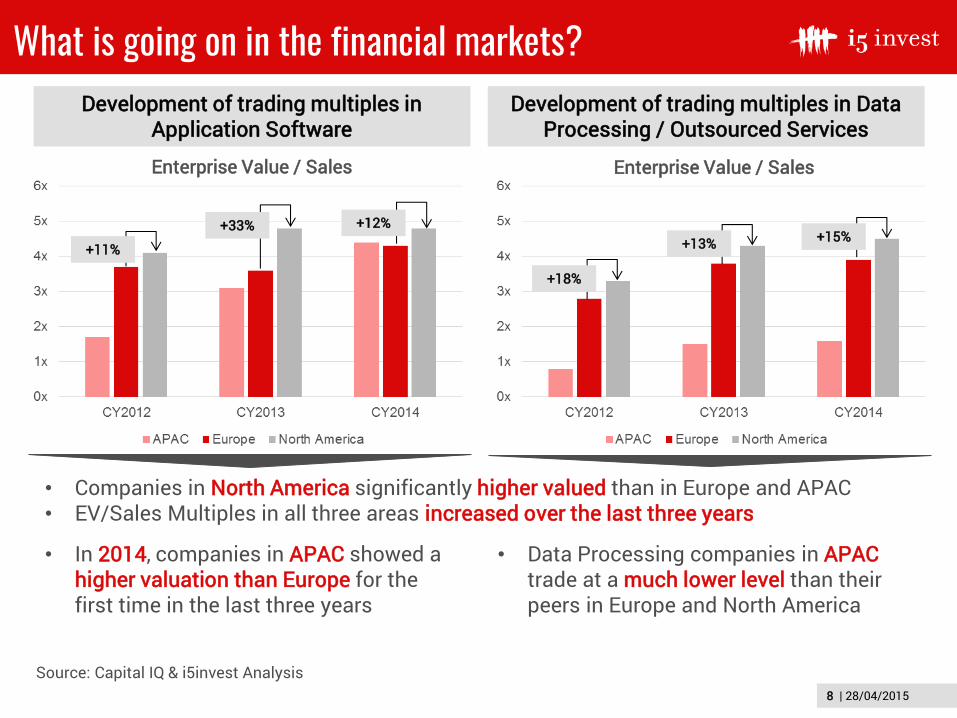

What is going on in the financial markets? Development of trading multiples in

Application Software Development of trading multiples in Data

Processing / Outsourced Services

Source: Capital IQ & i5invest Analysis

Enterprise Value / Sales

• In 2014, companies in APAC showed a higher valuation than Europe for the first time in the last three years

• Data Processing companies in APAC trade at a much lower level than their peers in Europe and North America

• Companies in North America significantly higher valued than in Europe and APAC • EV/Sales Multiples in all three areas increased over the last three years

Enterprise Value / Sales

9 | 28/04/2015

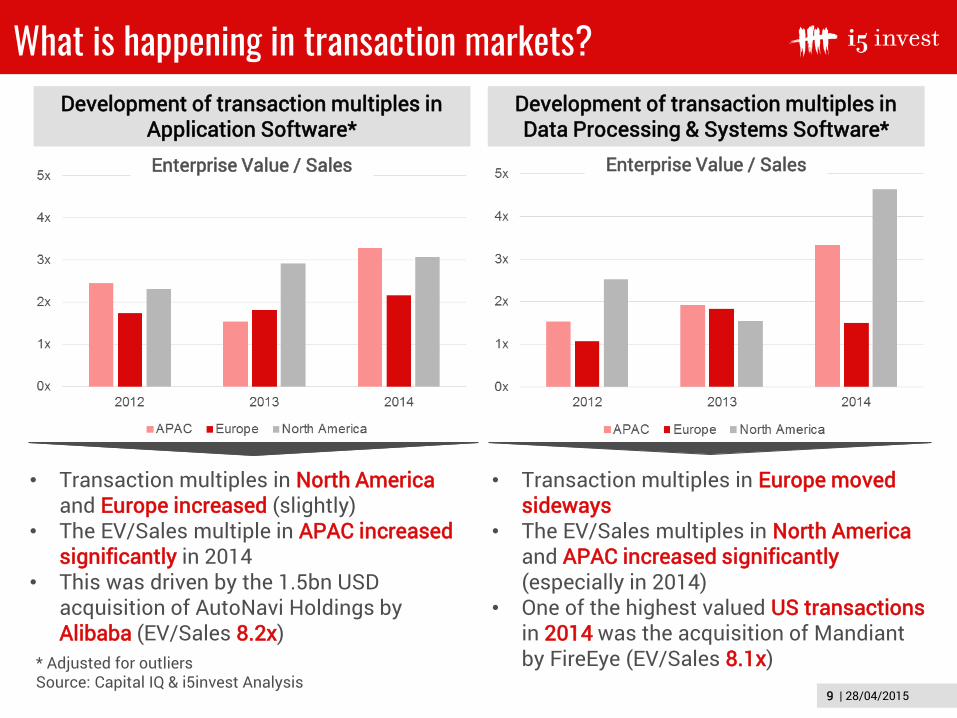

What is happening in transaction markets?

4/28/2015

Development of transaction multiples in Application Software*

Development of transaction multiples in Data Processing & Systems Software*

Enterprise Value / Sales Enterprise Value / Sales

* Adjusted for outliers Source: Capital IQ & i5invest Analysis

• Transaction multiples in North America and Europe increased (slightly)

• The EV/Sales multiple in APAC increased significantly in 2014

• This was driven by the 1.5bn USD acquisition of AutoNavi Holdings by Alibaba (EV/Sales 8.2x)

• Transaction multiples in Europe moved sideways

• The EV/Sales multiples in North America and APAC increased significantly (especially in 2014)

• One of the highest valued US transactions in 2014 was the acquisition of Mandiant by FireEye (EV/Sales 8.1x)

10 | 28/04/2015

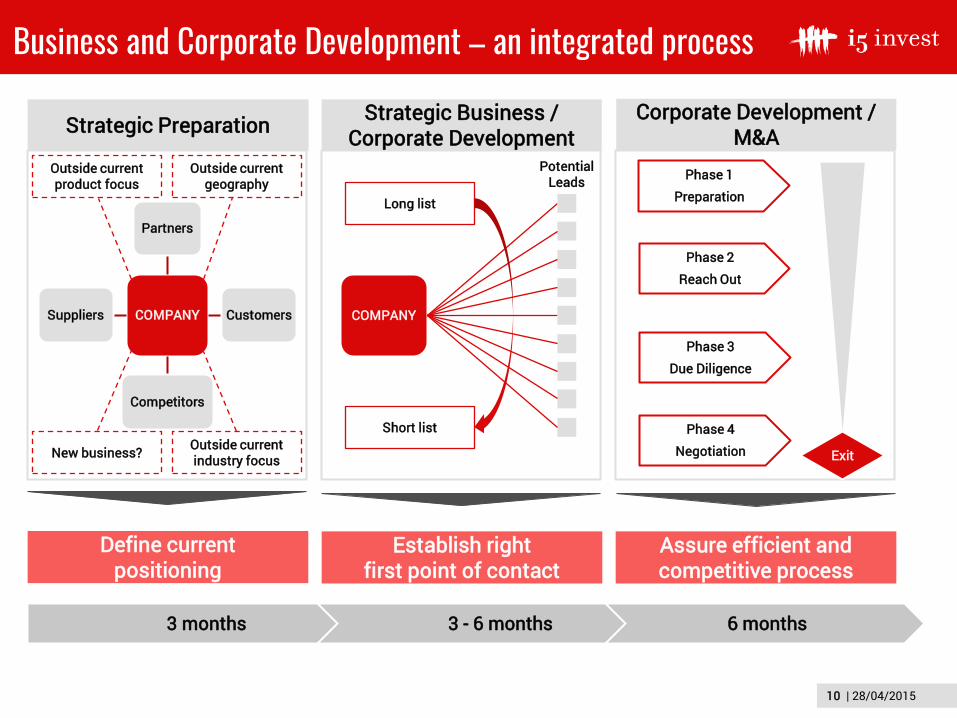

COMPANY

Partners

Customers

Competitors

Suppliers

Outside current product focus

Outside current industry focus

Outside current geography

New business?

Business and Corporate Development – an integrated process

Strategic Preparation Strategic Business / Corporate Development

Corporate Development / M&A

COMPANY

Potential Leads

Long list

Short list

3 months 3 - 6 months 6 months

Define current positioning

Establish right first point of contact

Assure efficient and competitive process

Phase 1

Preparation

Phase 3

Due Diligence

Phase 2

Reach Out

Phase 4

Negotiation Exit

11 | 28/04/2015

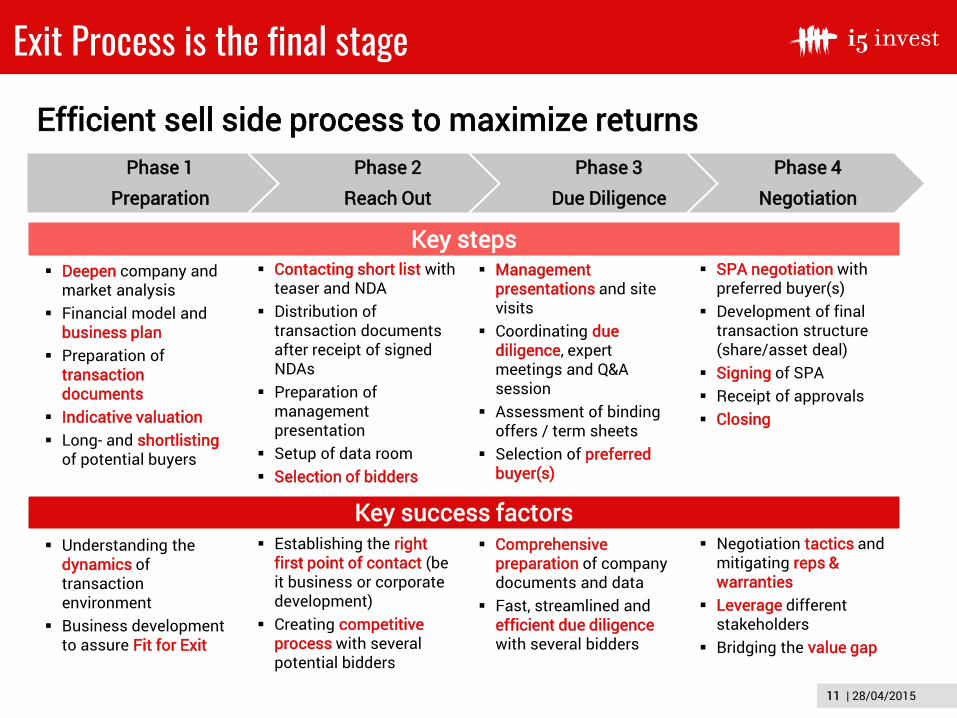

Exit Process is the final stage

Deepen company and market analysis

Financial model and business plan

Preparation of transaction documents

Indicative valuation Long- and shortlisting

of potential buyers

Contacting short list with teaser and NDA

Distribution of transaction documents after receipt of signed NDAs

Preparation of management presentation

Setup of data room Selection of bidders

SPA negotiation with preferred buyer(s)

Development of final transaction structure (share/asset deal)

Signing of SPA Receipt of approvals Closing

Management presentations and site visits

Coordinating due diligence, expert meetings and Q&A session

Assessment of binding offers / term sheets

Selection of preferred buyer(s)

Phase 1 Preparation

Phase 2 Reach Out

Phase 3 Due Diligence

Phase 4 Negotiation

Key steps

Key success factors Understanding the

dynamics of transaction environment

Business development to assure Fit for Exit

Establishing the right first point of contact (be it business or corporate development)

Creating competitive process with several potential bidders

Negotiation tactics and mitigating reps & warranties

Leverage different stakeholders

Bridging the value gap

Comprehensive preparation of company documents and data

Fast, streamlined and efficient due diligence with several bidders

Efficient sell side process to maximize returns

Thank you!

OUR EUROPE OFFICE i5invest Beratungs GmbH

(CEO Herwig Springer) Spengergasse 37-39

A-1050 Vienna Austria/Europe

OUR US OFFICE i5growth Inc.

(CEO Markus Wagner) 460 S California Ave, #304 Palo Alto, California 94306

United States

Herwig Springer CEO Corp. Dev.,

+43 650 530 8976

13 | 28/04/2015

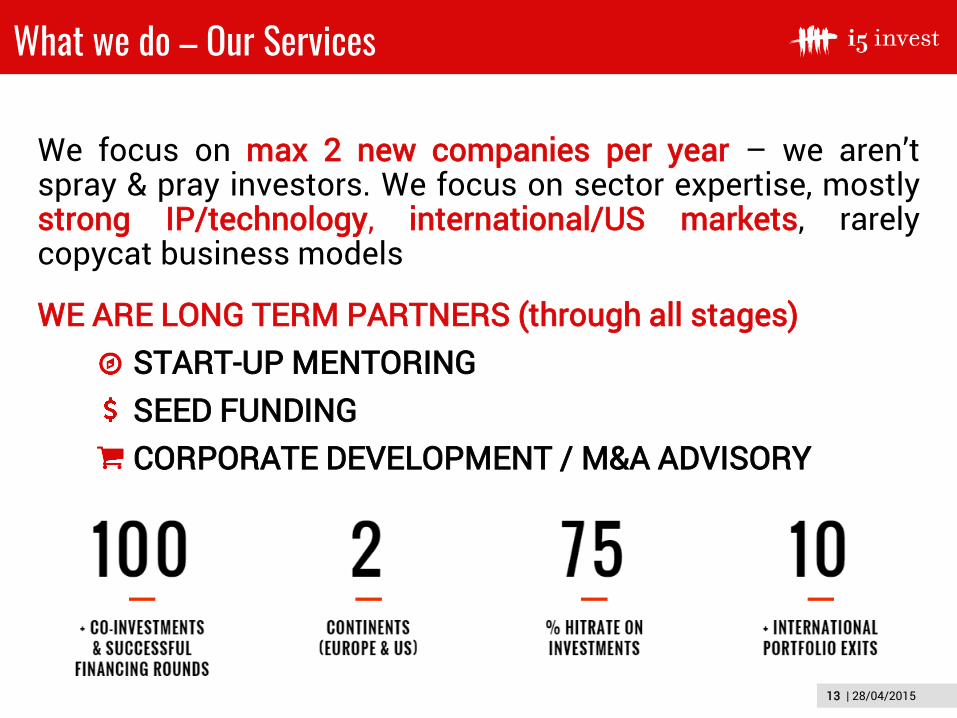

What we do – Our Services

WE ARE LONG TERM PARTNERS (through all stages) START-UP MENTORING SEED FUNDING CORPORATE DEVELOPMENT / M&A ADVISORY

We focus on max 2 new companies per year – we aren’t spray & pray investors. We focus on sector expertise, mostly strong IP/technology, international/US markets, rarely copycat business models

14 | 28/04/2015

Who we are – Our Team Founded 2007, Vienna - partner i5growth Inc. in Palo Alto

28/04/2015

- PARTNERS & FRIENDS – OUR ECOSYSTEM-

Herwig Springer CEO Corp. Dev.,

+43 650 530 8976

Patrick Prokesch Director Corp. Dev.,

+43 676 303 4854

Paul Weinberger

Partner

Markus Wagner Chairman of

Advisory Board, CEO - i5growth

Inc./ USA

Alexander Igelsboeck

Partner

Martin Brunthaler

Partner

Bernhard Lehner Partner

Vlad Gozman Partner Ad

viso

ry B

oard

/ Pa

rtne

r

Part

ner

Johannes Raidl Director Corp. Dev.,

+43 664 167 7577

Georg Novak Executive Assistant

+43 676 841 282 150

15 | 28/04/2015

Portfolio Overview

#inspire, #innovate, #incubate, #invest, #internationalize