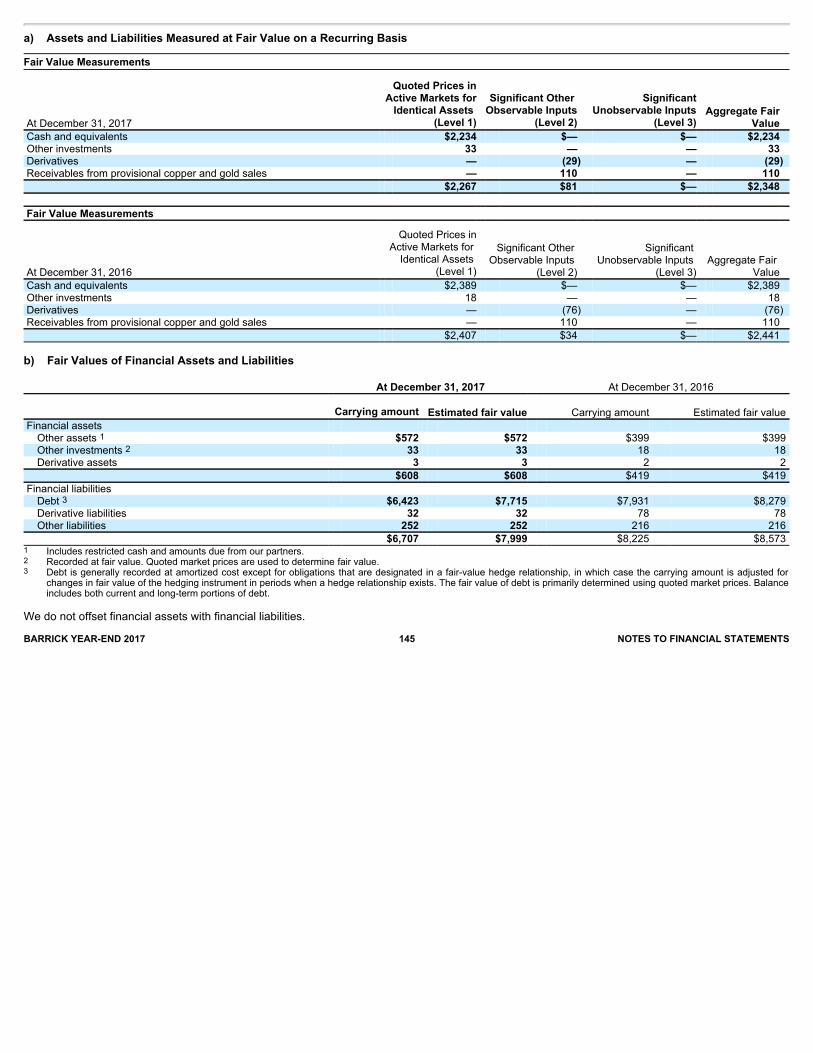

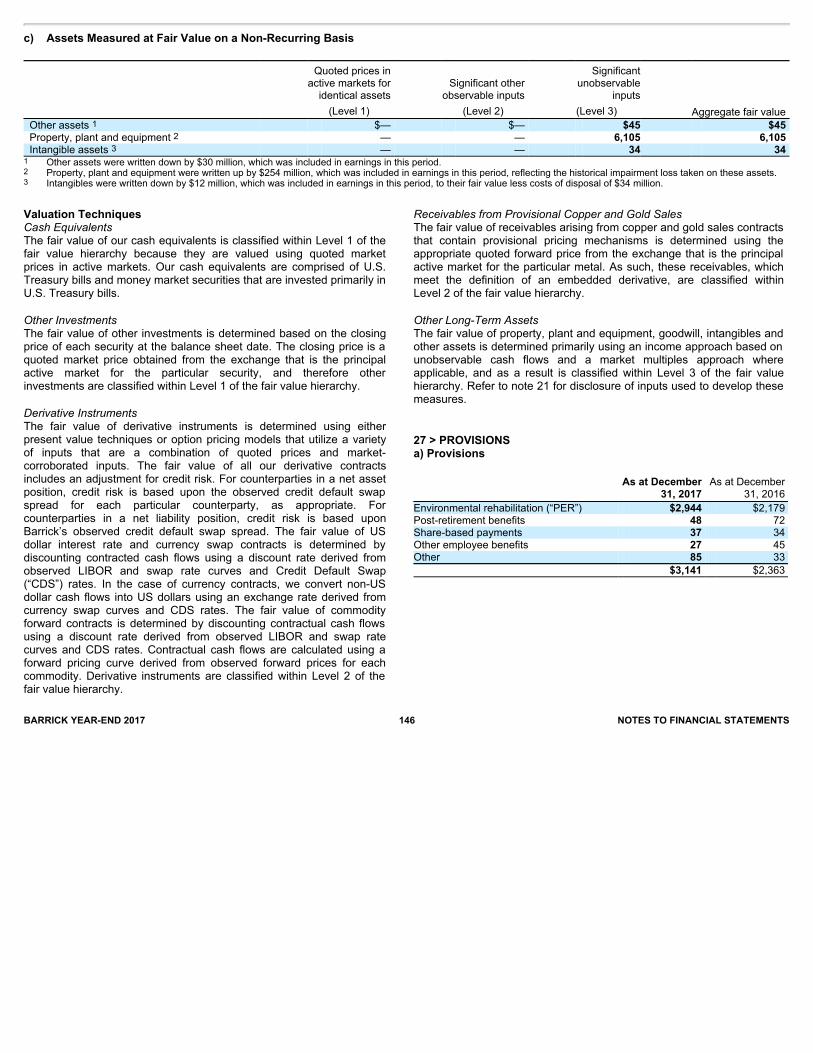

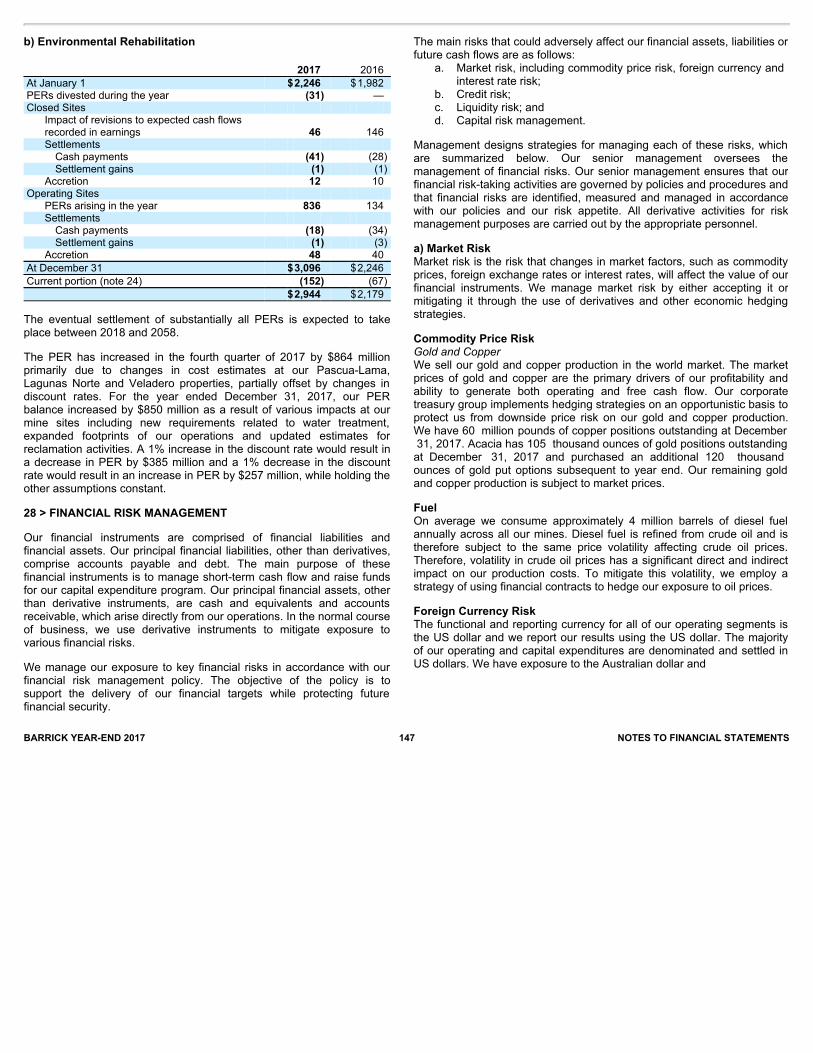

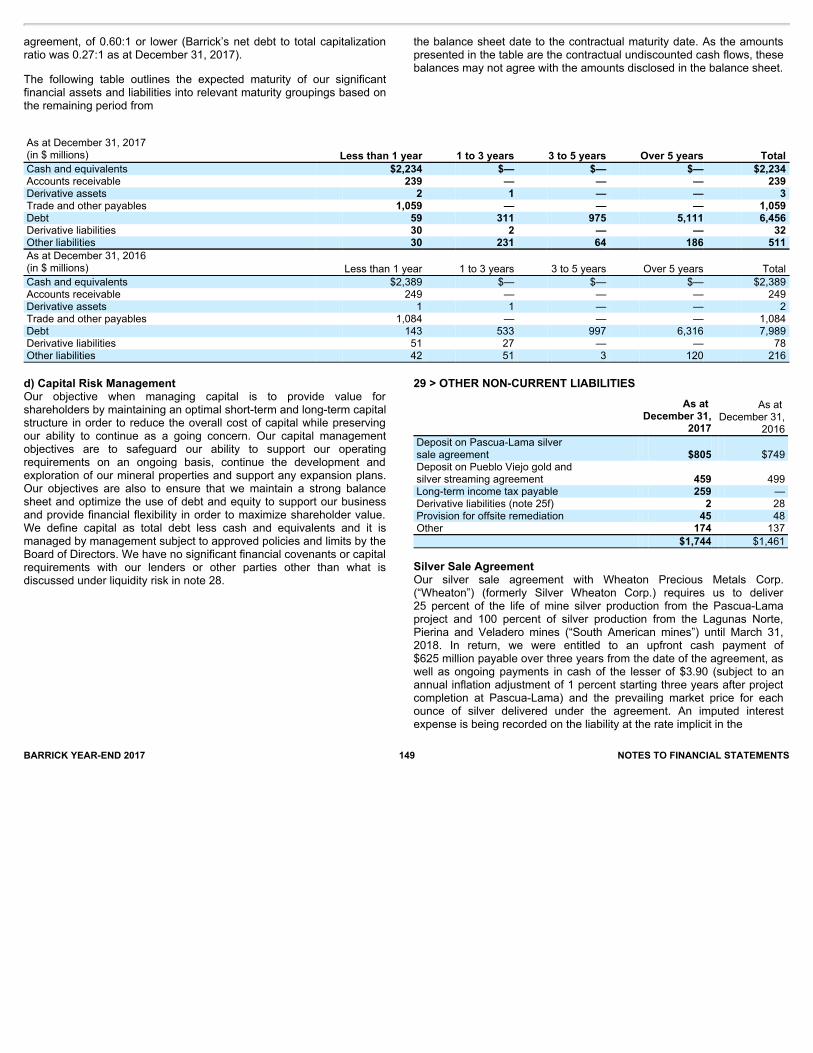

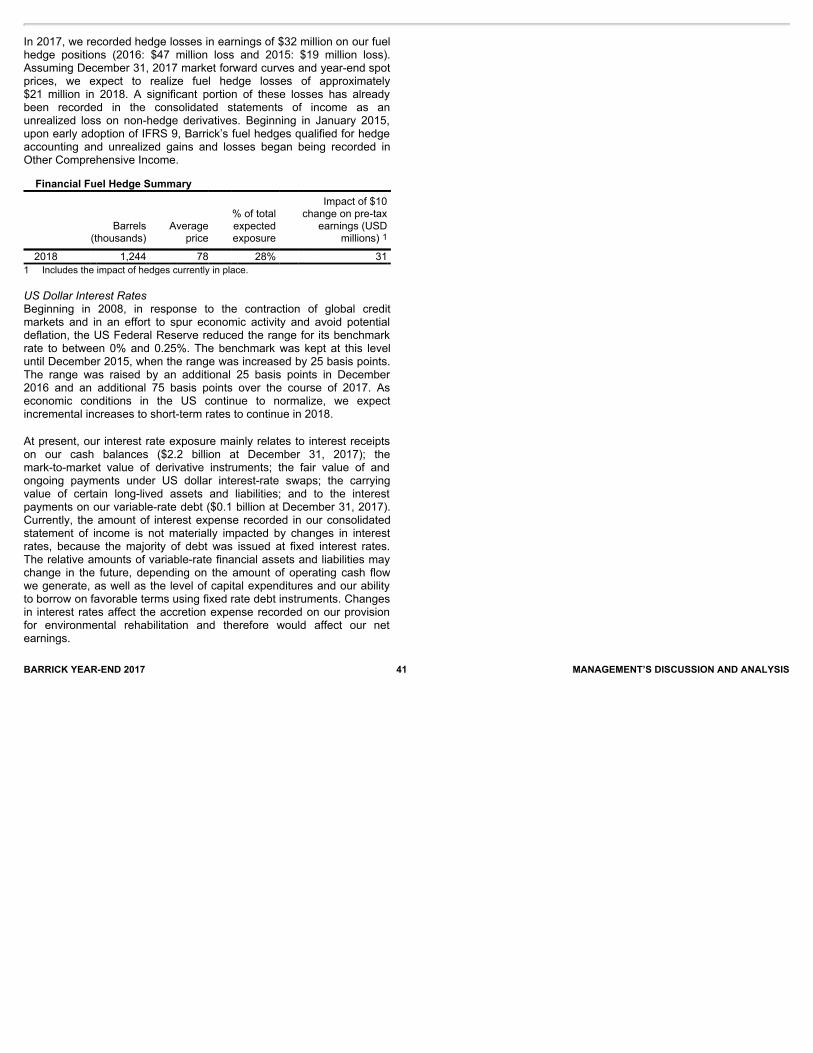

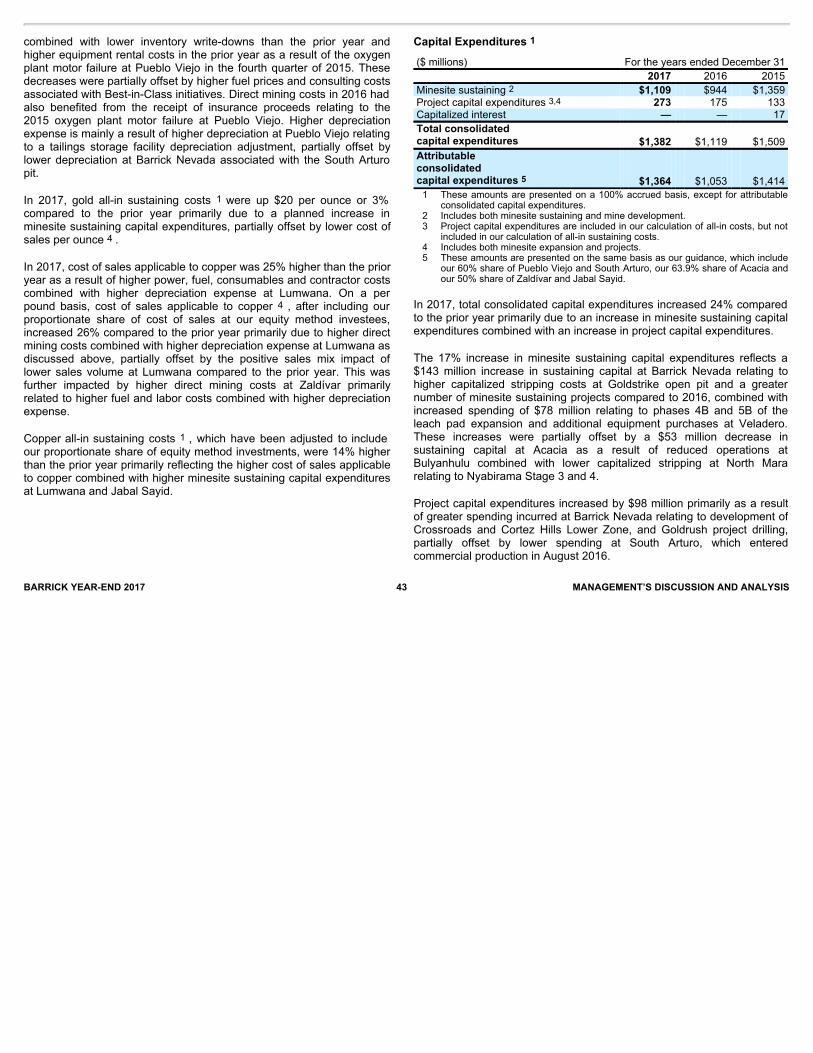

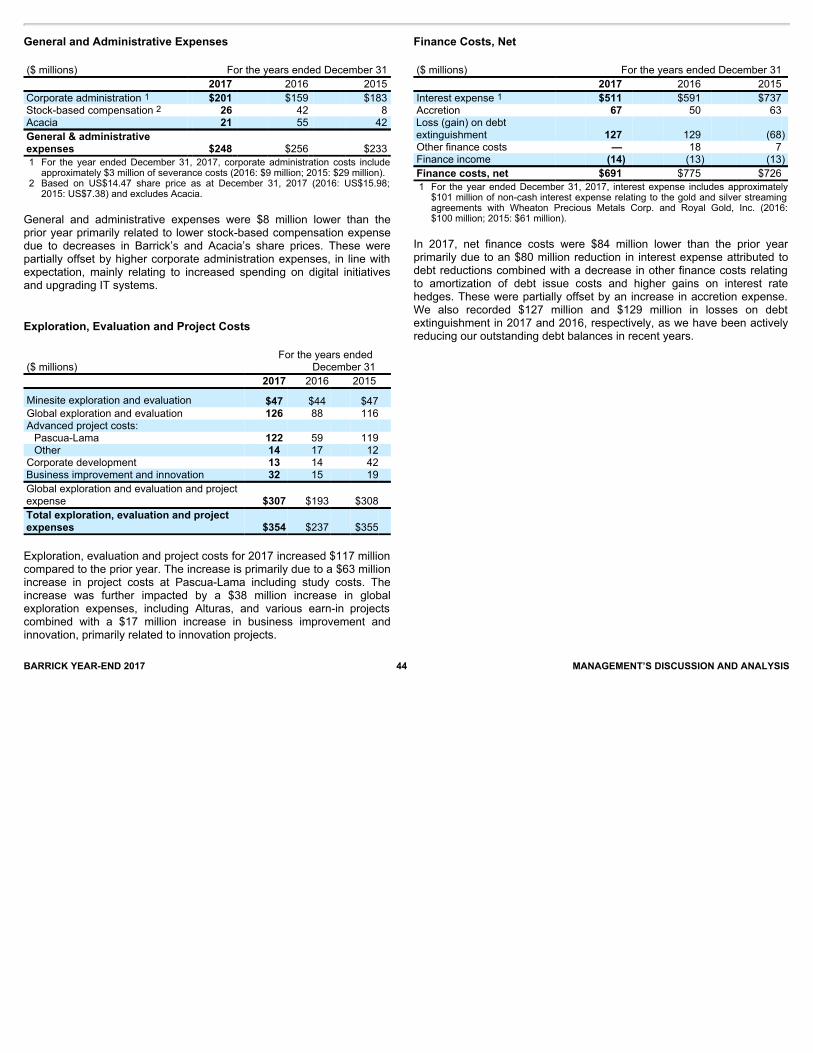

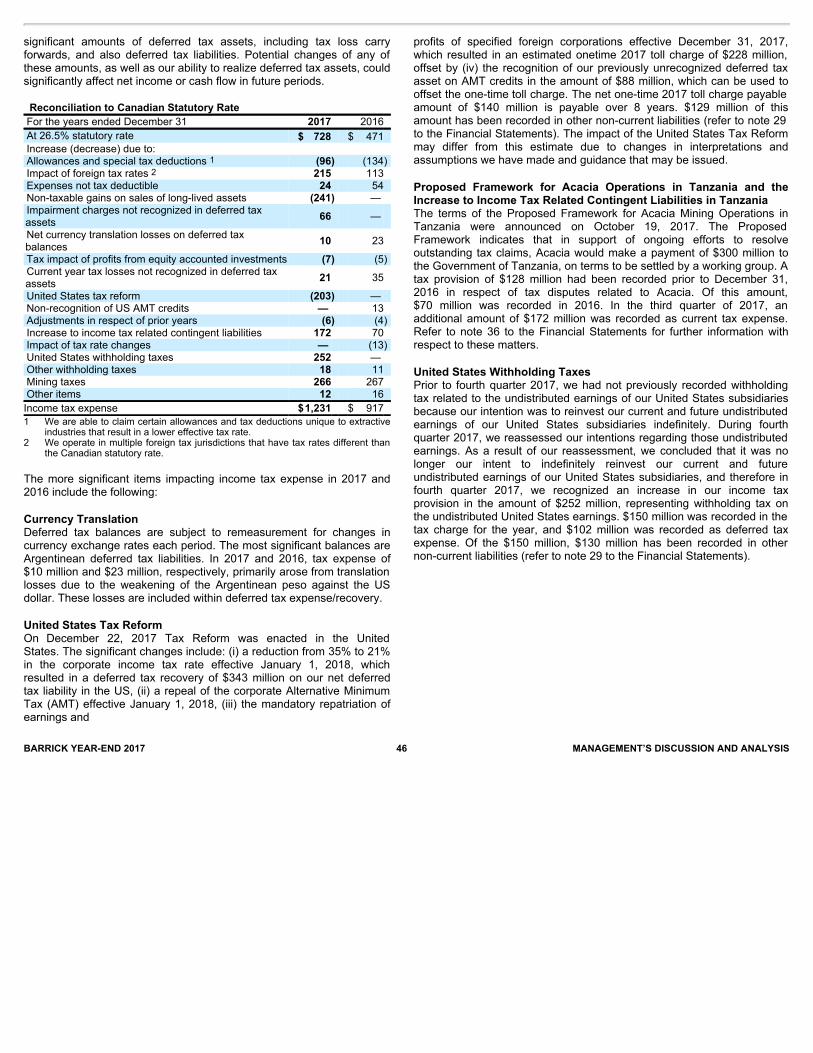

barrickgoldcorporationd18rn0p25nwr6d.cloudfront.net/cik-0000756894/196eac0b-e021-42e6-b..., in the...

TRANSCRIPT

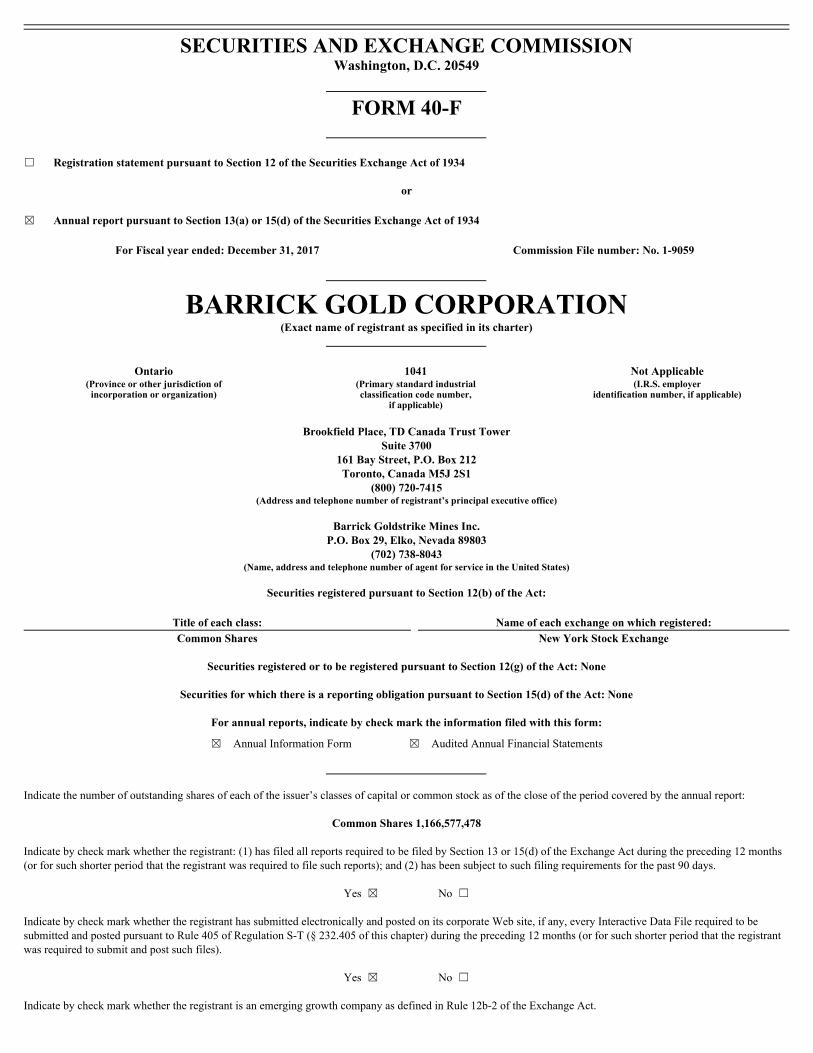

SECURITIESANDEXCHANGECOMMISSIONWashington,D.C.20549

FORM40-F

☐ RegistrationstatementpursuanttoSection12oftheSecuritiesExchangeActof1934

or☒ AnnualreportpursuanttoSection13(a)or15(d)oftheSecuritiesExchangeActof1934

ForFiscalyearended:December31,2017 CommissionFilenumber:No.1-9059

BARRICKGOLDCORPORATION(Exactnameofregistrantasspecifiedinitscharter)

Ontario 1041 NotApplicable(Provinceorotherjurisdictionofincorporationororganization)

(Primarystandardindustrialclassificationcodenumber,

ifapplicable)

(I.R.S.employeridentificationnumber,ifapplicable)

BrookfieldPlace,TDCanadaTrustTowerSuite3700

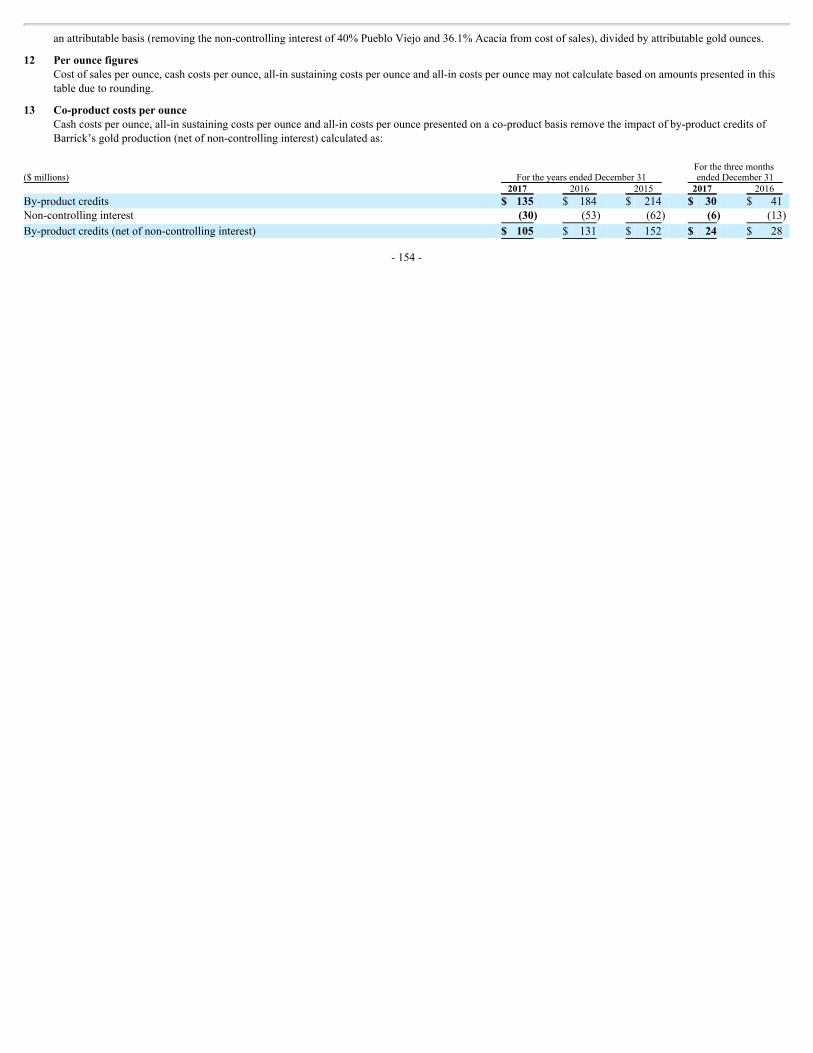

161BayStreet,P.O.Box212Toronto,CanadaM5J2S1

(800)720-7415(Addressandtelephonenumberofregistrant’sprincipalexecutiveoffice)

BarrickGoldstrikeMinesInc.P.O.Box29,Elko,Nevada89803

(702)738-8043(Name,addressandtelephonenumberofagentforserviceintheUnitedStates)

SecuritiesregisteredpursuanttoSection12(b)oftheAct:

Titleofeachclass: Nameofeachexchangeonwhichregistered:

CommonShares NewYorkStockExchange

SecuritiesregisteredortoberegisteredpursuanttoSection12(g)oftheAct:None

SecuritiesforwhichthereisareportingobligationpursuanttoSection15(d)oftheAct:None

Forannualreports,indicatebycheckmarktheinformationfiledwiththisform:

☒AnnualInformationForm☒AuditedAnnualFinancialStatements

Indicatethenumberofoutstandingsharesofeachoftheissuer’sclassesofcapitalorcommonstockasofthecloseoftheperiodcoveredbytheannualreport:

CommonShares1,166,577,478

Indicatebycheckmarkwhethertheregistrant:(1)hasfiledallreportsrequiredtobefiledbySection13or15(d)oftheExchangeActduringthepreceding12months(orforsuchshorterperiodthattheregistrantwasrequiredtofilesuchreports);and(2)hasbeensubjecttosuchfilingrequirementsforthepast90days.

Yes☒No☐

IndicatebycheckmarkwhethertheregistranthassubmittedelectronicallyandpostedonitscorporateWebsite,ifany,everyInteractiveDataFilerequiredtobesubmittedandpostedpursuanttoRule405ofRegulationS-T(§232.405ofthischapter)duringthepreceding12months(orforsuchshorterperiodthattheregistrantwasrequiredtosubmitandpostsuchfiles).

Yes☒No☐

IndicatebycheckmarkwhethertheregistrantisanemerginggrowthcompanyasdefinedinRule12b-2oftheExchangeAct.

Emerginggrowthcompany☐

IfanemerginggrowthcompanythatpreparesitsfinancialstatementsinaccordancewithU.S.GAAP,indicatebycheckmarkiftheregistranthaselectednottousetheextendedtransitionperiodforcomplyingwithanyneworrevisedfinancialaccountingstandardsprovidedpursuanttoSection13(a)oftheExchangeAct.☐

INTERNALCONTROLOVERFINANCIALREPORTINGANDDISCLOSURECONTROLSANDPROCEDURES

Thedisclosureprovidedunder“InternalControlOverFinancialReportingandDisclosureControlsandProcedures”onpages150and151ofExhibit99.1,Barrick’sAnnualInformationForm,isincorporatedbyreferenceherein.

MANAGEMENT’SREPORTONINTERNALCONTROLOVERFINANCIALREPORTING

Barrick’s“Management’sReportonInternalControlOverFinancialReporting”containedinExhibit99.2isincorporatedbyreferenceherein.

ATTESTATIONREPORTOFTHEREGISTEREDPUBLICACCOUNTINGFIRM

Thedisclosureprovidedunder“ReportofIndependentRegisteredPublicAccountingFirm”onpages95through96ofExhibit99.3,Barrick’sAuditedConsolidatedFinancialStatements,isincorporatedbyreferenceherein.

AUDITCOMMITTEE

Thedisclosureprovidedunder“CompositionoftheAuditCommittee”onpage148ofExhibit99.1,Barrick’sAnnualInformationForm,isincorporatedbyreferenceherein.Barrickhasaseparately-designatedstandingauditcommitteeestablishedinaccordancewithSection3(a)(58)(A)oftheSecuritiesExchangeActof1934,asamended.

CODEOFETHICS

Barrickhasadoptedacodeofethicsentitled,“BarrickGoldCorporationCodeofBusinessConductandEthics.”TheCodeofBusinessConductandEthicsappliestoalldirectors,officersandemployeesofBarrick,includingBarrick’sprincipalexecutiveofficer,principalfinancialofficerandprincipalaccountingofficer.TheCodeofBusinessConductandEthicsisavailableatBarrick’sInternetwebsite,www.barrick.com,intheCompany—GovernancesectionandisavailableinprinttoanyshareholderuponwrittenrequesttotheCorporateSecretaryofBarrick.

PRINCIPALACCOUNTANTFEESANDSERVICES

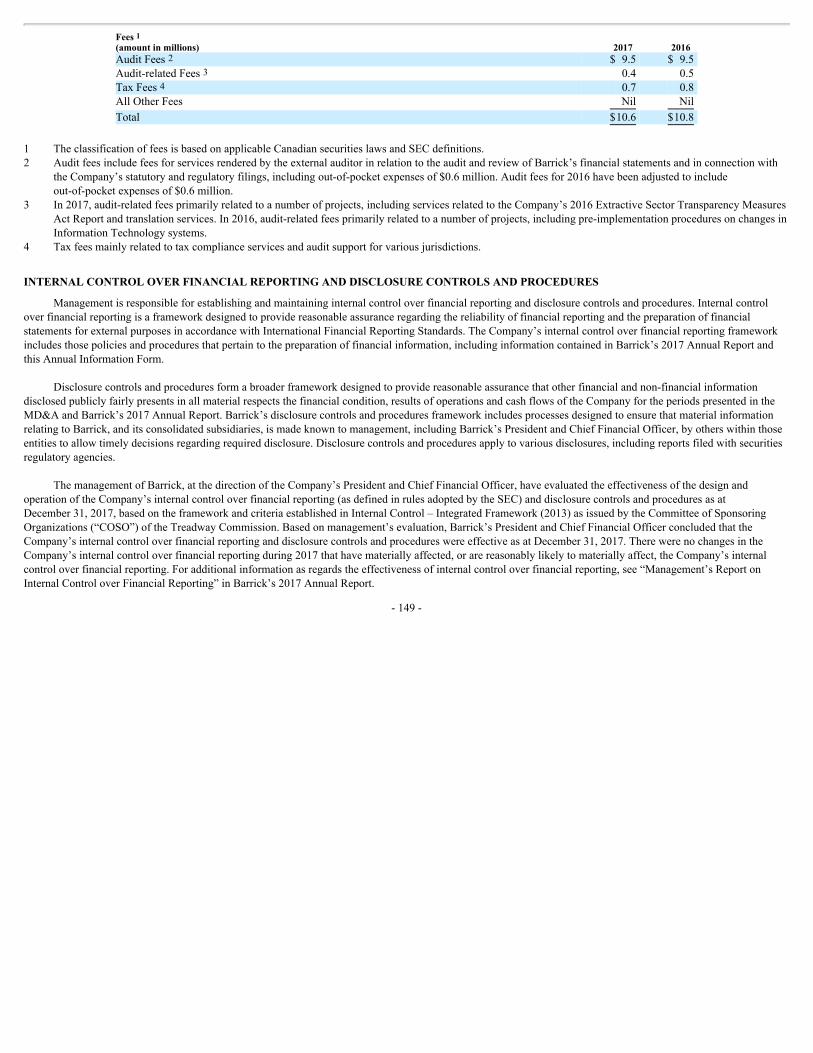

Thedisclosureprovidedunder“ExternalAuditorServiceFees”onpages149and150ofExhibit99.1,Barrick’sAnnualInformationForm,isincorporatedbyreferenceherein.

AUDITCOMMITTEEPRE-APPROVALPOLICIESANDPROCEDURES

Thedisclosureprovidedunder“AuditCommitteePre-ApprovalPoliciesandProcedures”onpage149ofExhibit99.1,Barrick’sAnnualInformationForm,isincorporatedbyreferenceherein.Noaudit-relatedfees,taxfeesorothernon-auditfeeswereapprovedbytheAuditCommitteepursuanttoparagraph(c)(7)(i)(C)ofRule2-01ofRegulationS-X.

OFF-BALANCESHEETARRANGEMENTS

Barrickhasnooff-balancesheetarrangementsthathave,orarereasonablylikelytohave,amaterialeffectonBarrick’sfinancialcondition,changesinfinancialcondition,revenuesorexpenses,resultsofoperations,liquidity,capitalexpendituresorcapitalresources.

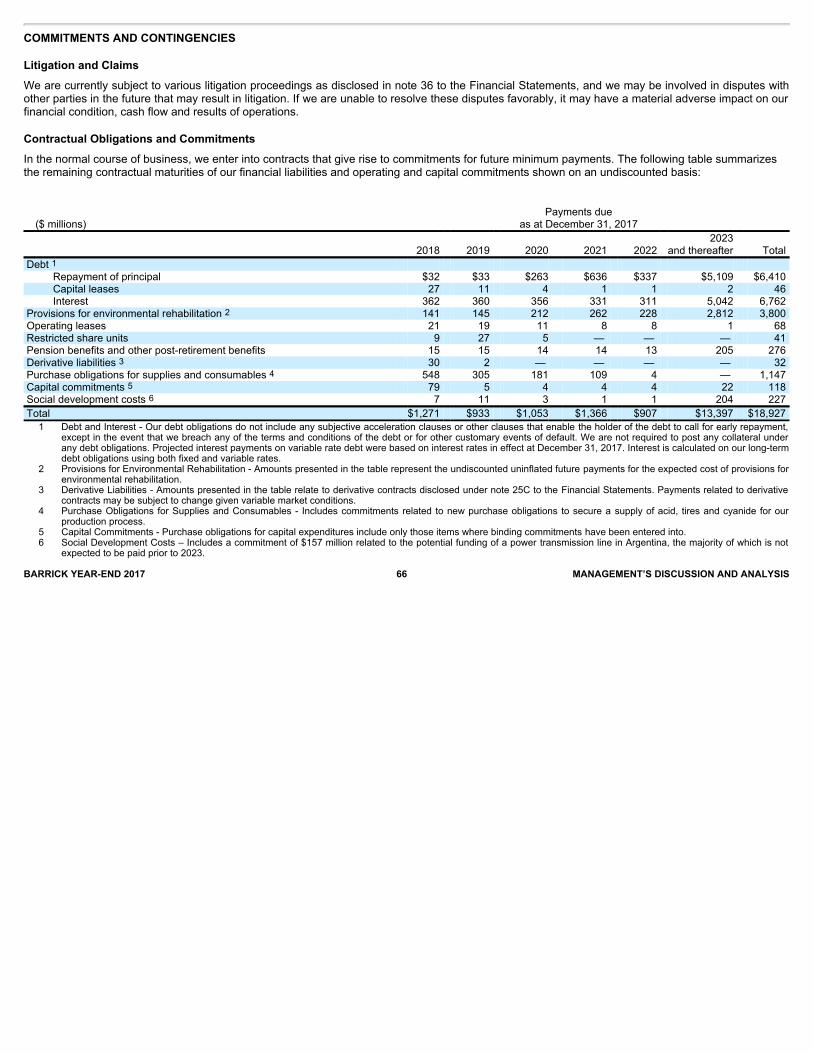

CONTRACTUALOBLIGATIONS

Thedisclosureprovidedunder“ContractualObligationsandCommitments”onpage66ofExhibit99.4,Management’sDiscussionandAnalysisofFinancialandOperatingResults,isincorporatedbyreferenceherein.

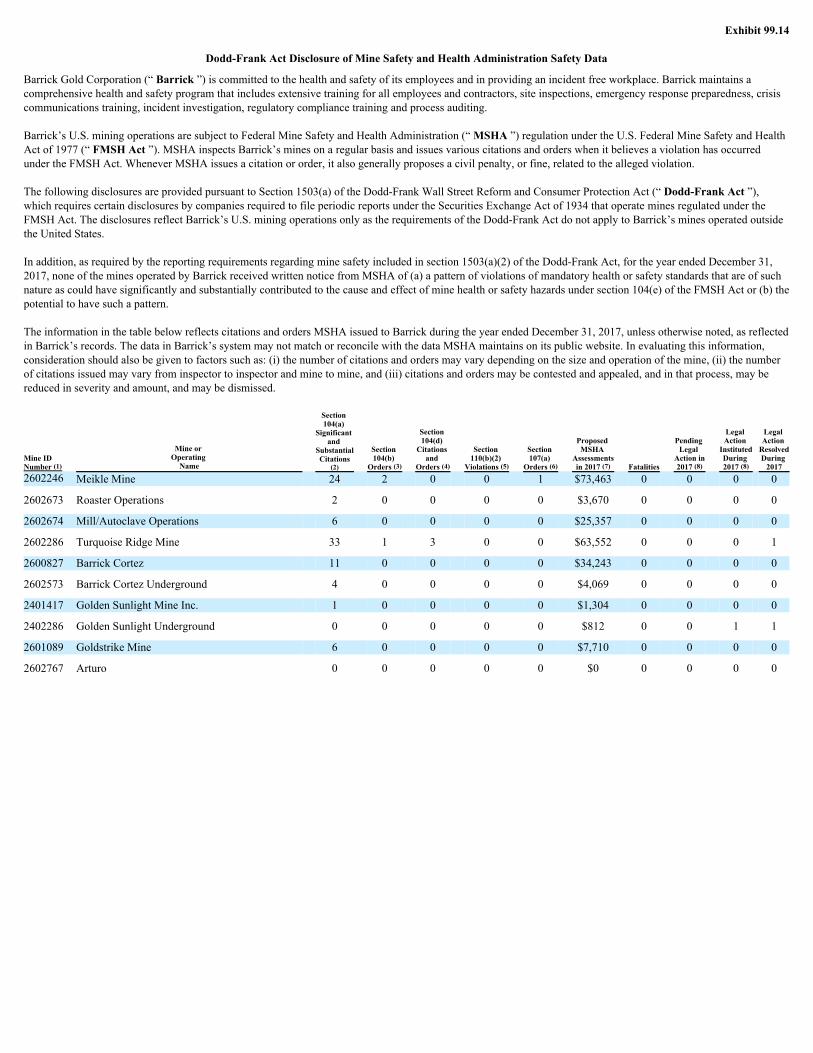

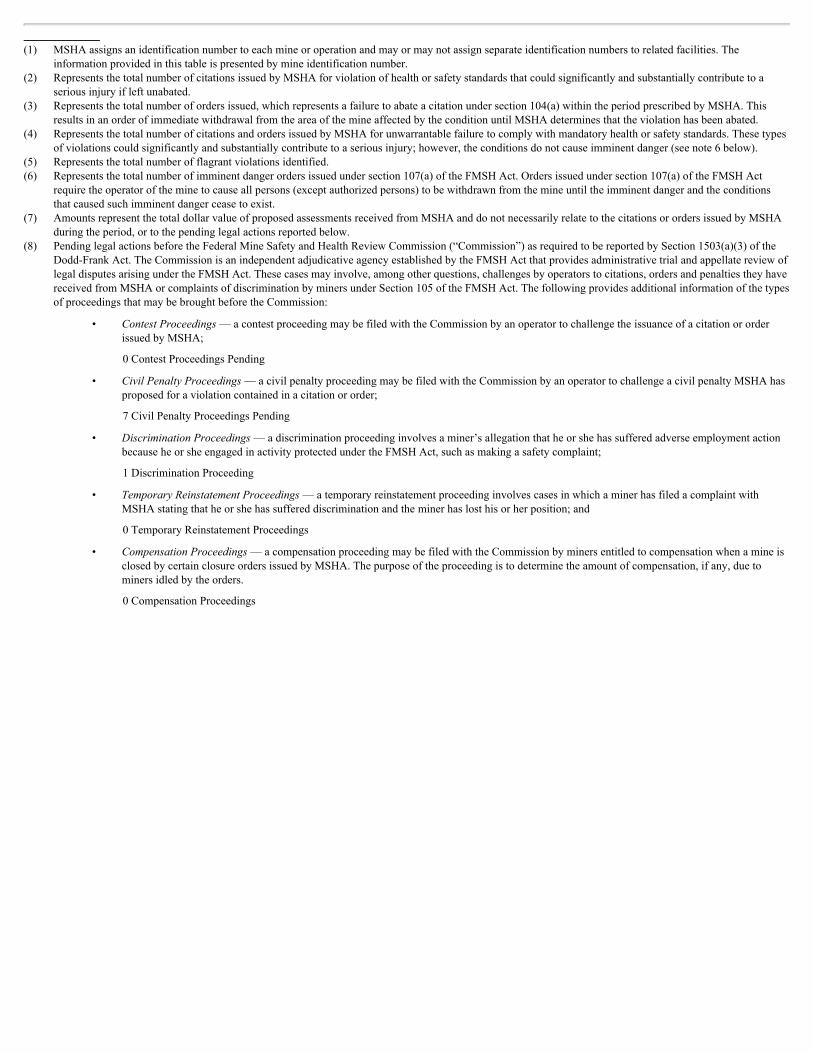

MINESAFETYDISCLOSURE

BarrickisrequiredtoreportcertainminesafetyviolationsorotherregulatorymattersrequiredbySection1503(a)oftheDodd-FrankWallStreetReformandConsumerProtectionAct,andthatrequiredinformationisincludedinExhibit99.14.

UNDERTAKINGANDCONSENTTOSERVICEOFPROCESS

A.Undertaking

Registrantundertakestomakeavailable,inpersonorbytelephone,representativestorespondtoinquiriesmadebytheCommissionstaff,andtofurnishpromptly,whenrequestedtodosobytheCommissionstaff,informationrelatingto:thesecuritiesregisteredpursuanttoForm40-F;thesecuritiesinrelationtowhichtheobligationtofileanannualreportonForm40-Farises;ortransactionsinsaidsecurities.

B.ConsenttoServiceofProcess

RegistranthaspreviouslyfiledwiththeCommissionaFormF-XinconnectionwiththeCommonShares.

INCORPORATIONBYREFERENCE

Barrick’sannualreportonForm40-F(otherthanthesectionentitled“Ratings”inExhibit99.1)isincorporatedbyreferenceintoBarrick’sRegistrationStatementsonFormS-8(FileNos.333-121500,333-131715,333-135769),FormF-3(FileNo.333-206417)andFormF-10(FileNo.333-216099).

SIGNATURES

PursuanttotherequirementsoftheExchangeAct,theregistrantcertifiesthatitmeetsalloftherequirementsforfilingonForm40-Fandhasdulycausedthisannualreporttobesignedonitsbehalfbytheundersigned,theretodulyauthorized.

BARRICKGOLDCORPORATION

Dated:March23,2018 By: /s/RichieHaddock Name: RichieHaddock Title: SeniorVicePresidentandGeneralCounsel

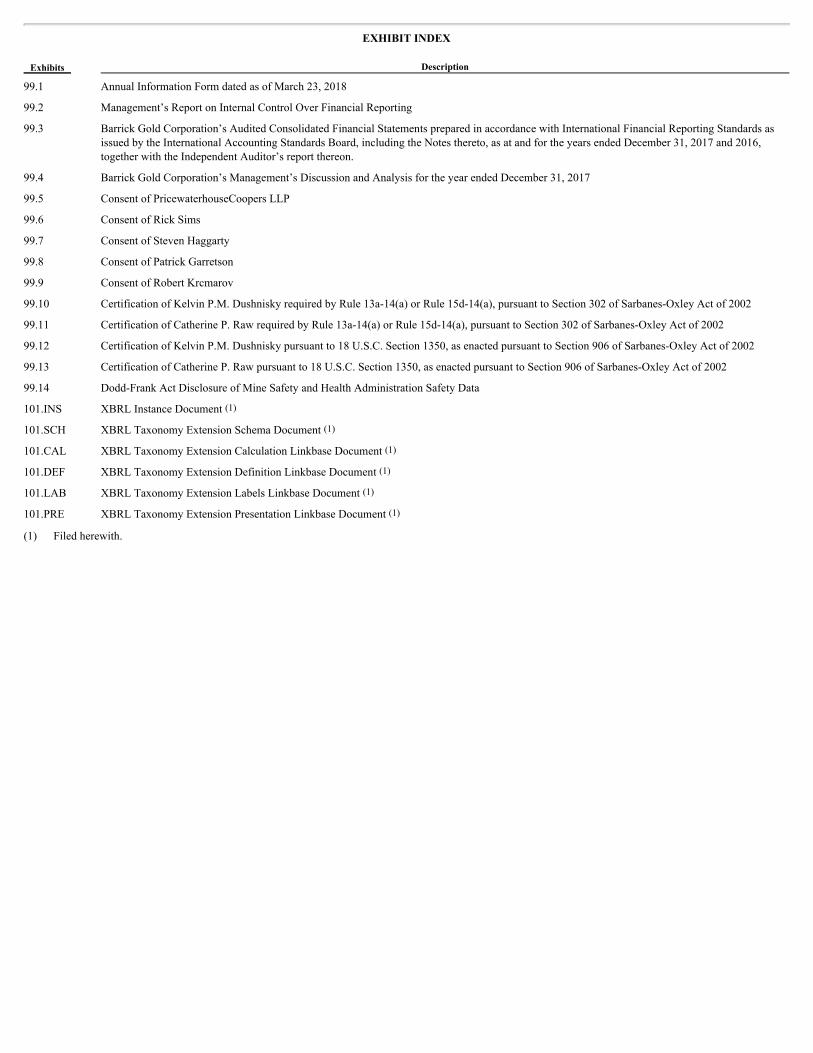

EXHIBITINDEXExhibits Description

99.1 AnnualInformationFormdatedasofMarch23,2018

99.2 Management’sReportonInternalControlOverFinancialReporting

99.3

BarrickGoldCorporation’sAuditedConsolidatedFinancialStatementspreparedinaccordancewithInternationalFinancialReportingStandardsasissuedbytheInternationalAccountingStandardsBoard,includingtheNotesthereto,asatandfortheyearsendedDecember31,2017and2016,togetherwiththeIndependentAuditor’sreportthereon.

99.4 BarrickGoldCorporation’sManagement’sDiscussionandAnalysisfortheyearendedDecember31,2017

99.5 ConsentofPricewaterhouseCoopersLLP

99.6 ConsentofRickSims

99.7 ConsentofStevenHaggarty

99.8 ConsentofPatrickGarretson

99.9 ConsentofRobertKrcmarov

99.10 CertificationofKelvinP.M.DushniskyrequiredbyRule13a-14(a)orRule15d-14(a),pursuanttoSection302ofSarbanes-OxleyActof2002

99.11 CertificationofCatherineP.RawrequiredbyRule13a-14(a)orRule15d-14(a),pursuanttoSection302ofSarbanes-OxleyActof2002

99.12 CertificationofKelvinP.M.Dushniskypursuantto18U.S.C.Section1350,asenactedpursuanttoSection906ofSarbanes-OxleyActof2002

99.13 CertificationofCatherineP.Rawpursuantto18U.S.C.Section1350,asenactedpursuanttoSection906ofSarbanes-OxleyActof2002

99.14 Dodd-FrankActDisclosureofMineSafetyandHealthAdministrationSafetyData

101.INS XBRLInstanceDocument(1)

101.SCH XBRLTaxonomyExtensionSchemaDocument(1)

101.CAL XBRLTaxonomyExtensionCalculationLinkbaseDocument(1)

101.DEF XBRLTaxonomyExtensionDefinitionLinkbaseDocument(1)

101.LAB XBRLTaxonomyExtensionLabelsLinkbaseDocument(1)

101.PRE XBRLTaxonomyExtensionPresentationLinkbaseDocument(1)

(1) Filedherewith.

Exhibit99.1

BarrickGoldCorporationBrookfieldPlace,TDCanadaTrustTowerSuite3700,161BayStreet,P.O.Box212Toronto,ONM5J2S1AnnualInformationFormFortheyearendedDecember31,2017DatedasofMarch23,2018

BARRICKGOLDCORPORATIONANNUALINFORMATIONFORM

TABLEOFCONTENTSGLOSSARYOFTECHNICALTERMS 4

REPORTINGCURRENCY,FINANCIALANDRESERVEINFORMATION 10

FORWARD-LOOKINGINFORMATION 10

SCIENTIFICANDTECHNICALINFORMATION 13

GENERALINFORMATION 13

OrganizationalStructure 13Subsidiaries 14AreasofInterest 16GeneralDevelopmentoftheBusiness 16

History 16Strategy 16ResultsofOperationsin2017 18

NARRATIVEDESCRIPTIONOFTHEBUSINESS 22

Production 22ReportableOperatingSegments 22

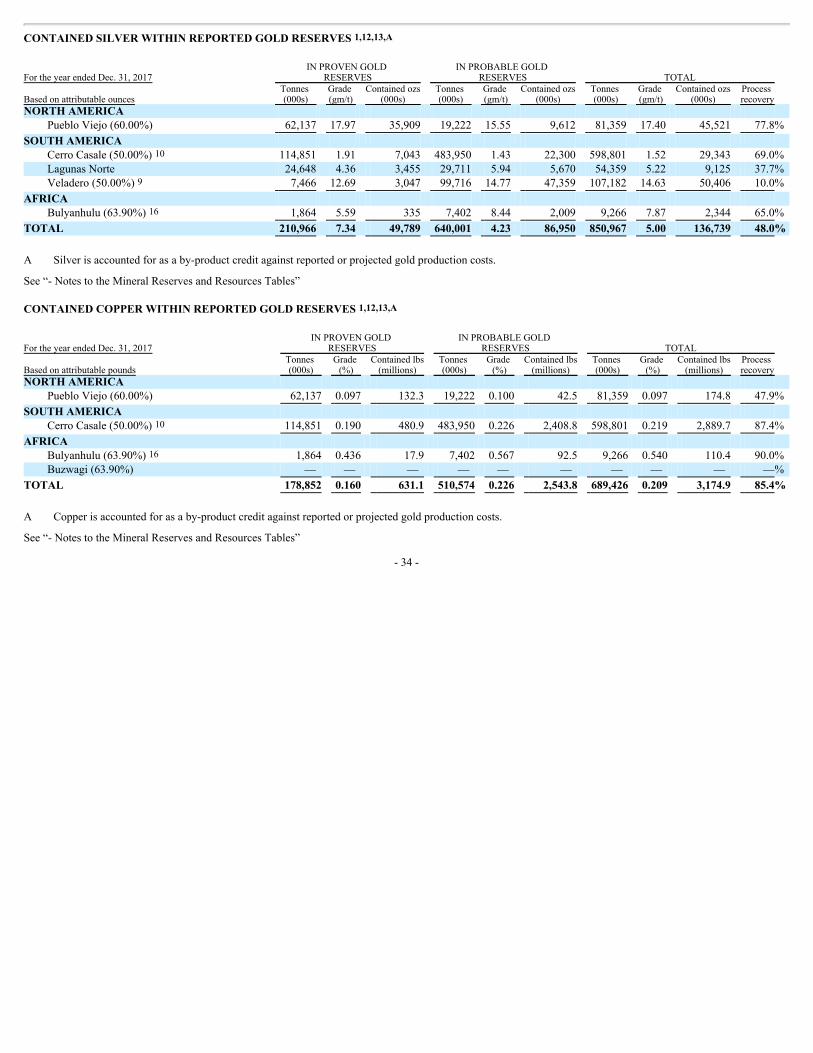

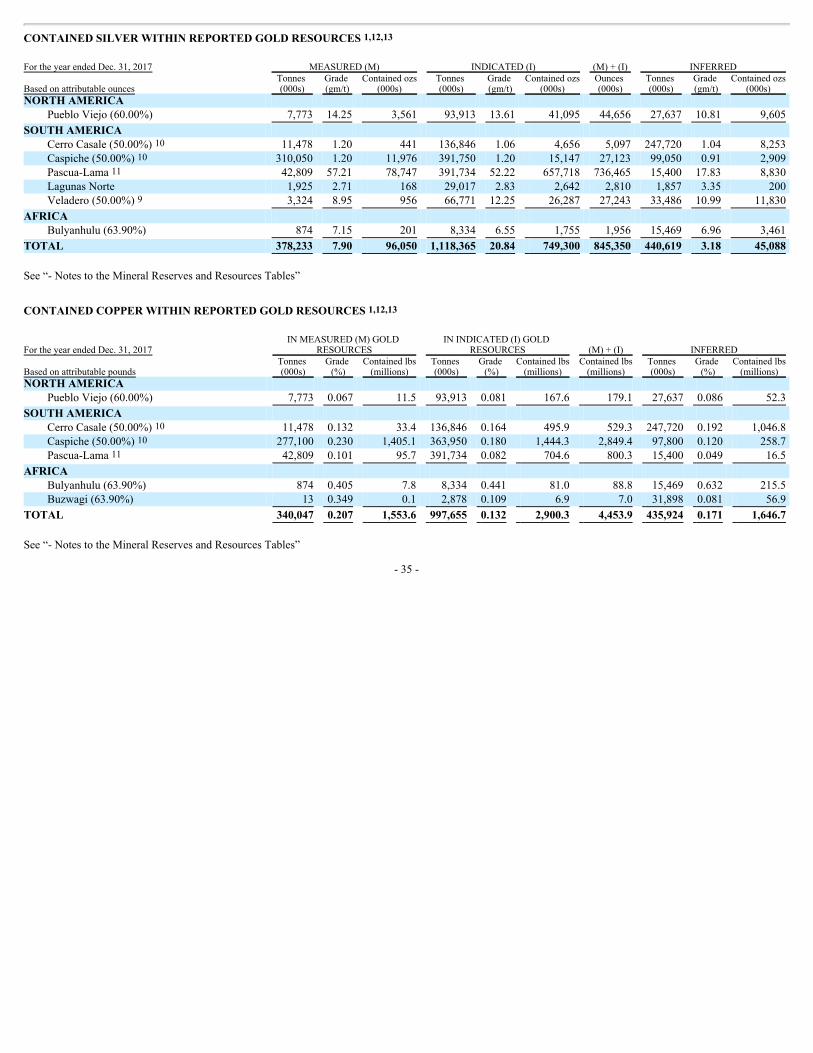

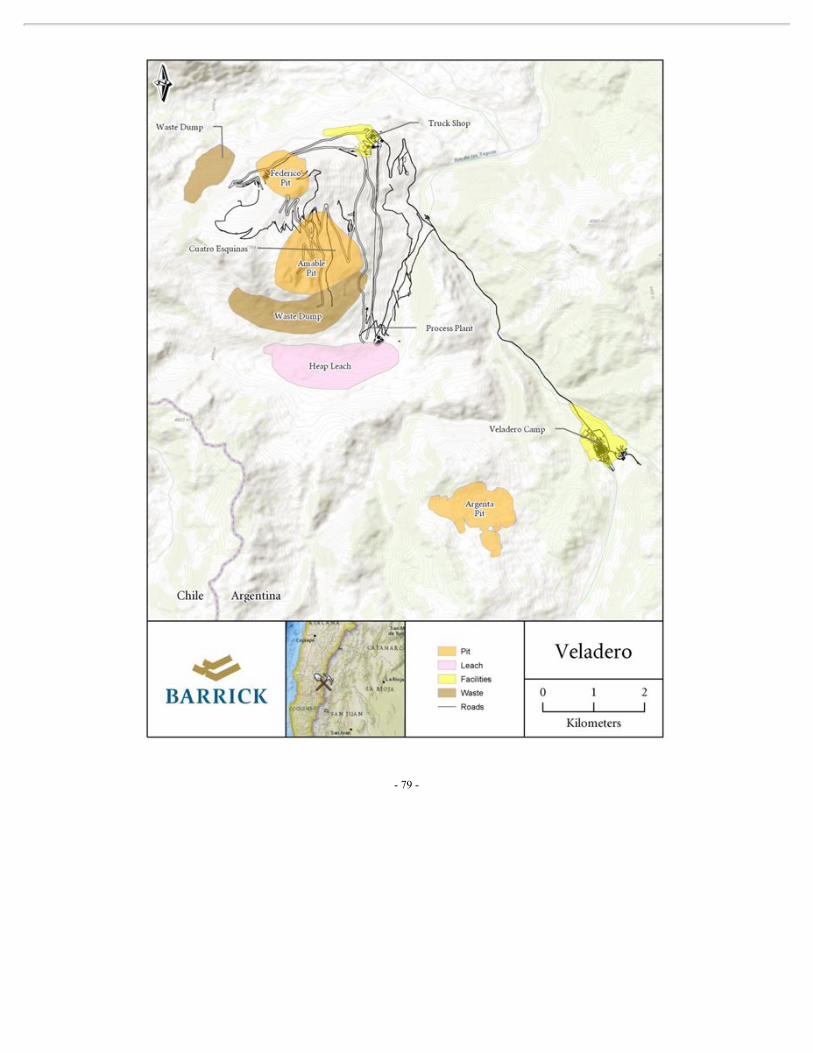

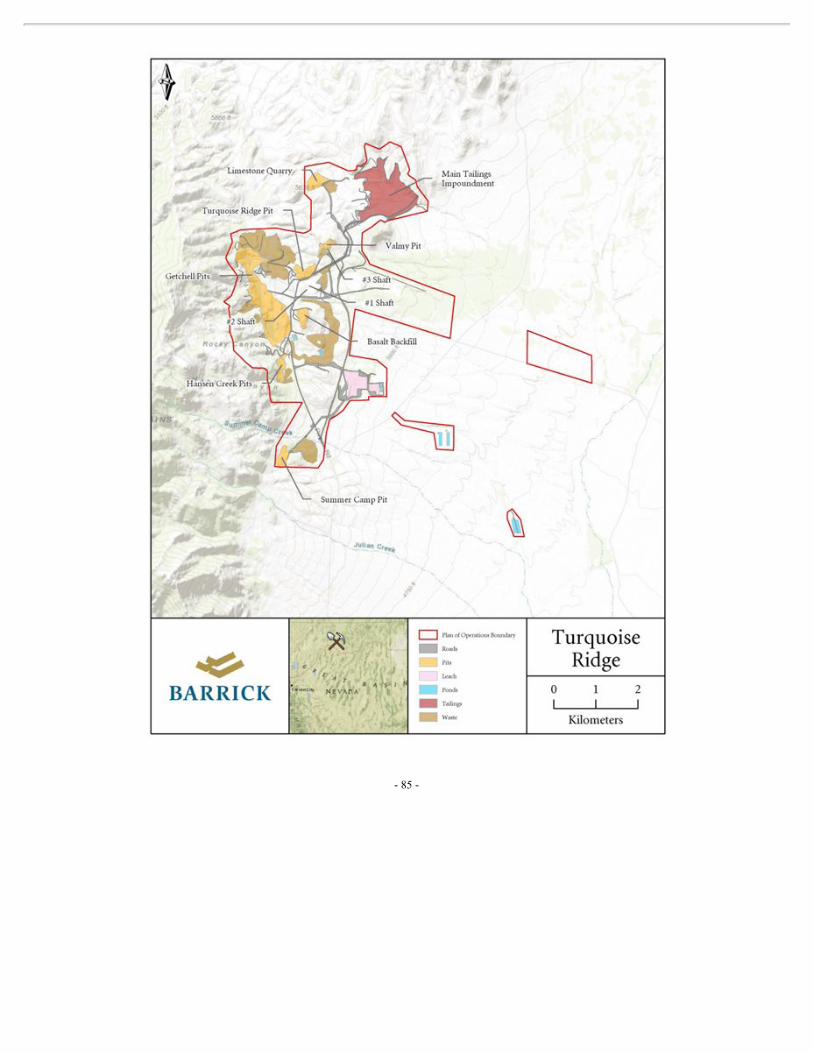

BarrickNevada 23PuebloViejo(60%basis) 24LagunasNorte 24Veladero 25TurquoiseRidge(75%basis) 26AcaciaMiningplc(63.9%basis) 27Pascua-LamaProject 28

MineralReservesandMineralResources 29MarketingandDistribution 39EmployeesandLaborRelations 41Competition 41CorporateSocialResponsibility 41OperationsinEmergingMarkets:CorporateGovernanceandInternalControls 42

BoardandManagementExperienceandOversight 43Communications 44InternalControlsandCashManagementPractices 44ManagingCulturalDifferences 45BooksandRecords 45

MATERIALPROPERTIES 45

CortezProperty 45GoldstrikeProperty 52PuebloViejoMine 58

-i-

LagunasNorteMine 65VeladeroMine 71TurquoiseRidgeMine 80

EXPLORATIONANDEVALUATIONS 86

ENVIRONMENT 91

LEGALMATTERS 94

GovernmentControlsandRegulations 94LegalProceedings 97

RISKFACTORS 110

MANAGEMENT’SDISCUSSIONANDANALYSISOFFINANCIALCONDITIONANDRESULTSOFOPERATIONS 129

CONSOLIDATEDFINANCIALSTATEMENTS 129

CAPITALSTRUCTURE 129

RATINGS 132

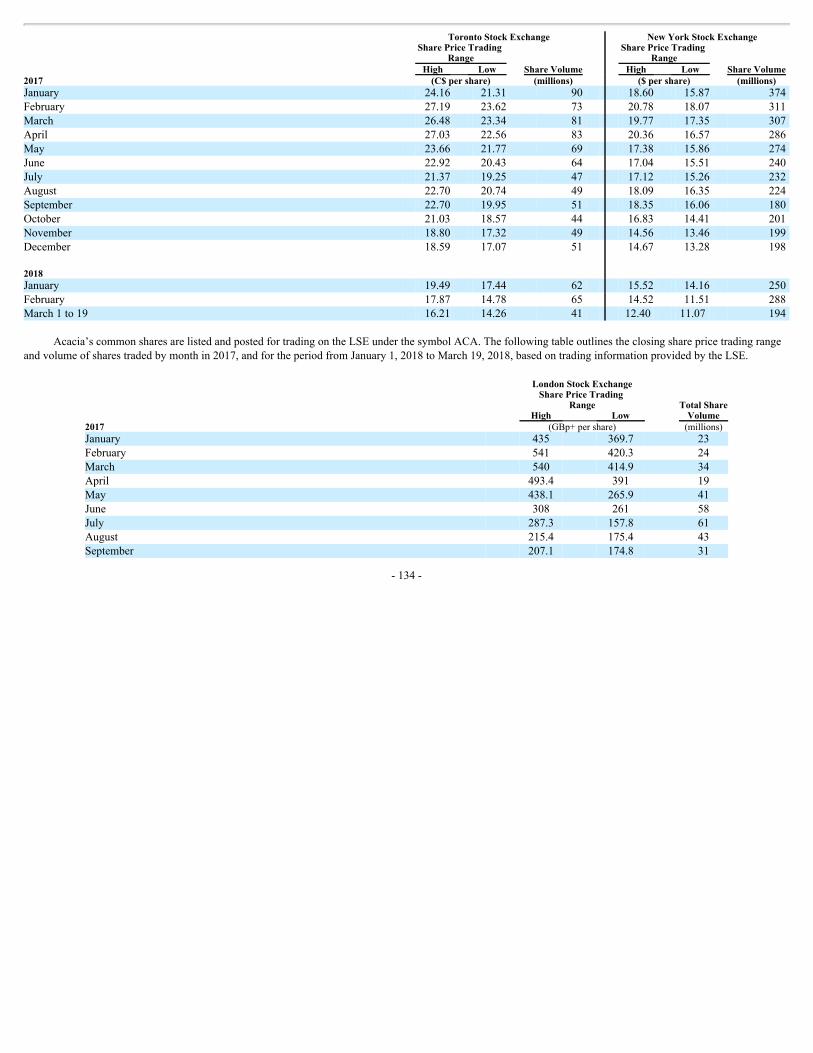

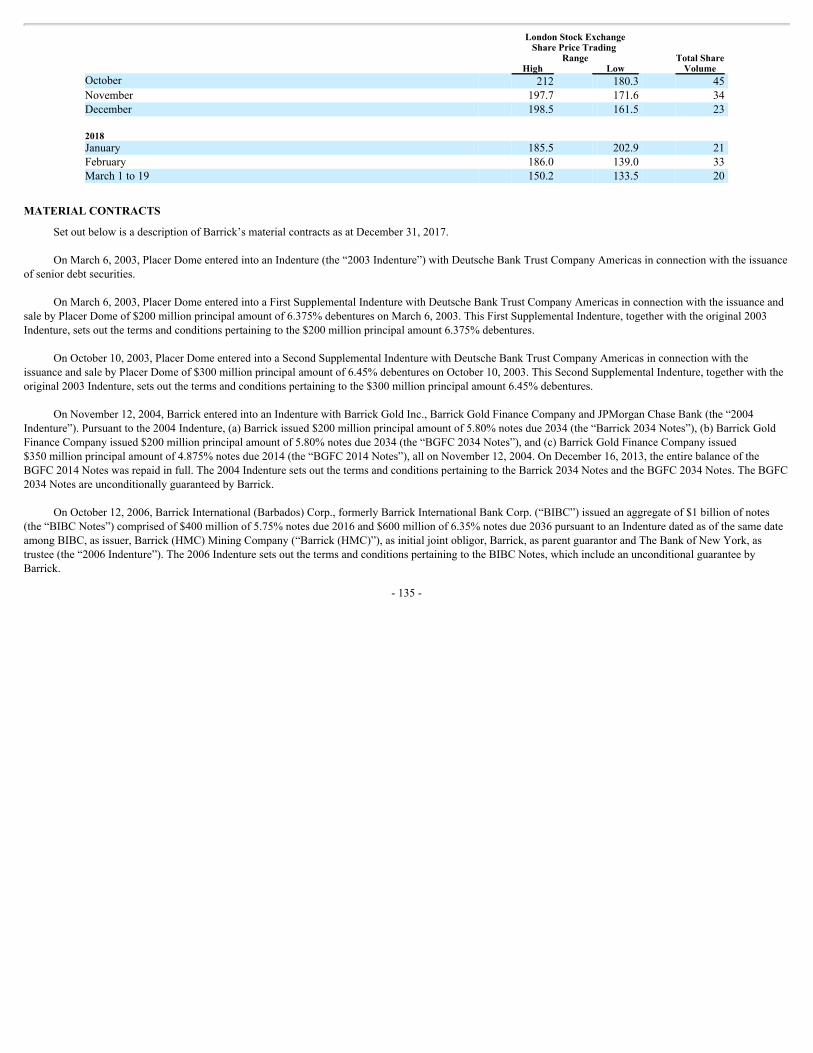

MARKETFORSECURITIES 133

MATERIALCONTRACTS 135

TRANSFERAGENTSANDREGISTRARS 137

DIVIDENDPOLICY 137

DIRECTORSANDOFFICERSOFTHECOMPANY 137

AUDITCOMMITTEE 147

AuditCommitteeMandate 147CompositionoftheAuditCommittee 147RelevantEducationandExperience 147ParticipationonOtherAuditCommittees 148AuditCommitteePre-ApprovalPoliciesandProcedures 148ExternalAuditorServiceFees 148

INTERNALCONTROLOVERFINANCIALREPORTINGANDDISCLOSURECONTROLSANDPROCEDURES 149

NON-GAAPFINANCIALMEASURES 150

INTERESTSOFEXPERTS 167

ADDITIONALINFORMATION 168

-ii-

SCHEDULE“A”AUDITCOMMITTEEMANDATE A-1

-iii-

GLOSSARYOFTECHNICALTERMS

Assay

Achemicalanalysistodeterminetheamountorproportionoftheelementofinterestcontainedwithinasample,typicallybasemetalsorpreciousmetals.

Autoclave

Oxidationprocessinwhichhightemperaturesandpressuresareappliedwithinapressurizedclosedvesseltoconvertrefractorysulfidemineralizationintoamenableoxideore.

BlockCaving

Anon-selectivebulkminingmethodwherematerialiscausedtocavetowardsundergroundextractionpointsfollowingtheengineereddrillingandremovalofmaterialfromanundercutthatcreatesapatternofbreakageandcollapsewithintherockmass.

By-product

Apayablesecondarymetalormineralproductthatisrecoveredalongwiththeprimarymetalormineralproductduringtheconcentrationprocess.

Carbonaceous

Naturallyoccurringcarbonpresentintheorefromthedecayoforganicmaterialwhichcanresultinaninadvertentlossofpreciousmetalsduringthecyanidationprocess.

Carbon-in-leach(CIL)

Arecoveryprocessinwhichpreciousmetalsaredissolvedfromfinelygroundoreduringcyanidationandsimultaneouslyadsorbedonrelativelycoarseactivatedcarbon(burntcoconutshell)granules.Theloadedcarbonparticlesareseparatedfromtheslurryandrecycledintheprocessfollowingpreciousmetalremovalandreactivationthroughchemicalandthermalmeans.

Carbon-in-column(CIC)

Amethodofrecoveringgoldandsilverfromsolutionfollowingcyanidationintheprocessbyadsorptionofthepreciousmetalsontopreparedcarbon(burntcoconutshell).

Concentrate

Aproductfromamineralprocessingfacilitysuchasgravityseparationorflotationinwhichthevaluableconstituentshavebeenupgradedandunwantedganguematerialsrejectedaswaste.

Containedounces

Ameasureofin-situorcontainedmetalbasedonanestimateoftonnageandgrade.

Crushing

AunitoperationthatreducesthesizeofmaterialdeliveredasRunofMineOreforfurtherprocessing.

Cut-and-fill

Amethodofstopinginwhichoreisremovedinslices,orlifts,andthentheexcavationisfilledwithrockorotherwastematerial(backfill),beforethesubsequentsliceisextracted.

Cut-offgrade

Acalculatedminimummetalgradeatwhichmaterialcanbeminedandprocessedatbreak-evencost.

-4-

Development

Workcarriedoutforthepurposeofpreparingamineraldepositforproduction.Inanundergroundmine,developmentincludesshaftsinking,crosscutting,driftingandraising.Inanopenpitmine,developmentincludestheremovalofoverburdenand/orwasterock.

Dilution

Theeffectofwasteorlow-gradeorewhichisunavoidablyincludedintheminedore,loweringtherecoveredgrade.

Doré

Compositegoldandsilverbullionusuallyconsistingofapproximately90%preciousmetalsthatwillbefurtherrefinedtoseparatepuremetals.

Drift

Ahorizontaltunnelgenerallydrivenwithinoralongsideanorebodyandalignedparalleltothelongdimensionoftheore.

Drift-and-fill

Amethodofundergroundminingusedforflat-lyingmineralizationorwheregroundconditionsarelesscompetent.

Drilling

Core:adrillingmethodthatusesarotatingbarrelandanannular-shaped,diamond-impregnatedrock-cuttingbittoproducecylindricalrockcoresandliftsuchcorestothesurface,wheretheymaybecollected,examinedandassayed.

Reversecirculation:adrillingmethodthatusesarotatingcuttingbitwithinadouble-walleddrillpipeandproducesrockchipsratherthancore.Airorwateriscirculateddowntothebitbetweentheinnerandouterwallofthedrillpipe.Thechipsareforcedtothesurfacethroughthecenterofthedrillpipeandarecollected,examinedandassayed.

Conventionalrotary:adrillingmethodthatproducesrockchipssimilartoreversecirculationexceptthatthesampleiscollectedusingasingle-walleddrillpipe.Airorwatercirculatesdownthroughthecenterofthedrillpipeandreturnschipstothesurfacearoundtheoutsideofthepipe.

In-fill:thecollectionofadditionalsamplesbetweenexistingsamples,usedtoprovidegreatergeologicaldetailandtoprovidemoreclosely-spacedassaydata.

Exploration

Prospecting,sampling,mapping,diamond-drillingandotherworkinvolvedinlocatingthepresenceofeconomicdepositsandestablishingtheirnature,shapeandgrade.

Flotation

Aprocesswhichconcentratesmineralsbytakingadvantageofspecificsurfacepropertiesandapplyingchemicalssuchascollectors,depressants,modifiersandfrothersinthepresenceofwaterandfinelydispersedairbubbles.

Grade

Theconcentrationofanelementofinterestexpressedasrelativemassunits(percentage,partspermillion,ouncesperton,gramspertonne,etc.).

-5-

Grinding(Milling)

Involvesthesizereductionofmaterialfedtoaprocessplantthoughabrasionorattritiontoliberatevaluablemineralsforfurthermetallurgicalprocessing.

Heapleaching

Aprocesswherebypreciousorbasemetalsareextractedfromstackedmaterialplacedontopofanimpermeableplasticlinerandafterapplyingleachsolutionswhichdissolveandtransportvaluesforrecoveryintheprocessplant.

Lode

Amineraldeposit,consistingofazoneofveins,veinletsordisseminations,inconsolidatedrockasopposedtoaplacerdeposit.

Long-holeopenstoping

Amethodofundergroundmininginvolvingthedrillingofholesupto30metersorlongerintoanorebearingzoneandthenblastingasliceofrockwhichfallsintoanopenspace.Thebrokenrockisextractedandtheresultingopenchambermayormaynotbebackfilledwithsupportingmaterial.

MetricconversionTroyounces × 31.10348 = GramsTroyouncespershortton × 34.28600 = GramspertonnePounds × 0.00045 = TonnesTons × 0.90718 = TonnesFeet × 0.30480 = MetersMiles × 1.60930 = KilometersAcres × 0.40468 = HectaresFahrenheit (°F-32)×5÷9 = Celsius

Mill

Afacilitywhereoreisfinelygroundandthereafterundergoesphysicalorchemicaltreatmenttoextractthevaluablemetals.

Mineralreserve

Theeconomicallymineableportionofameasuredorindicatedmineralresourcedemonstratedbyatleastapreliminaryfeasibilitystudy.Thisstudymustincludeadequateinformationonmining,processing,metallurgical,economicandotherrelevantfactorsthatdemonstrate,atthetimeofreporting,thateconomicextractioncanbejustified.Amineralreserveincludesdilutingmaterialsandallowancesforlossesthatmayoccurwhenthematerialismined.Mineralreservesaresub-dividedinorderofincreasingconfidenceintoprobablemineralreservesandprovenmineralreserves.

Probablemineralreserve:theeconomicallymineableportionofanindicatedand,insomecircumstances,ameasuredmineralresourcedemonstratedbyatleastapreliminaryfeasibilitystudy.Thisstudymustincludeadequateinformationonmining,processing,metallurgical,economicandotherrelevantfactorsthatdemonstrate,atthetimeofreporting,thateconomicextractioncanbejustified.

Provenmineralreserve:theeconomicallymineablepartofameasuredmineralresourcedemonstratedbyatleastapreliminaryfeasibilitystudy.Thisstudymustincludeadequateinformationonmining,processing,metallurgical,economicandotherrelevantfactorsthatdemonstrate,atthetimeofreporting,thateconomicextractionisjustified.

-6-

Mineralresource

Aconcentrationoroccurrenceofdiamonds,naturalsolidinorganicmaterial,ornaturalsolidfossilizedorganicmaterialincludingbaseandpreciousmetals,coal,andindustrialmineralsinorontheEarth’scrustinsuchformandquantityandofsuchagradeorqualitythatithasreasonableprospectsforeconomicextraction.Thelocation,quantity,grade,geologicalcharacteristicsandcontinuityofamineralresourceareknown,estimatedorinterpretedfromspecificgeologicalevidenceandknowledge.Mineralresourcesaresub-divided,inorderofincreasinggeologicalconfidence,intoinferred,indicatedandmeasuredcategories.

Inferredmineralresource:thatpartofamineralresourceforwhichquantityandgradeorqualitycanbeestimatedonthebasisofgeologicalevidenceandlimitedsamplingandreasonablyassumed,butnotverified,geologicalandgradecontinuity.Theestimateisbasedonlimitedinformationandsamplinggatheredthroughappropriatetechniquesfromlocationssuchasoutcrops,trenches,pits,workingsanddrillholes.

Indicatedmineralresource:thatpartofamineralresourceforwhichquantity,gradeorquality,densities,shapeandphysicalcharacteristicscanbeestimatedwithalevelofconfidencesufficienttoallowtheappropriateapplicationoftechnicalandeconomicparameters,tosupportmineplanningandevaluationoftheeconomicviabilityofthedeposit.Theestimateisbasedondetailedandreliableexplorationandtestinginformationgatheredthroughappropriatetechniquesfromlocationssuchasoutcrops,trenches,pits,workingsanddrillholesthatarespacedcloselyenoughforgeologicalandgradecontinuitytobereasonablyassumed.

Measuredmineralresource:thatpartofamineralresourceforwhichquantity,gradeorquality,densities,shapeandphysicalcharacteristicsaresowellestablishedthattheycanbeestimatedwithconfidencesufficienttoallowtheappropriateapplicationoftechnicalandeconomicparameters,tosupportproductionplanningandevaluationoftheeconomicviabilityofthedeposit.Theestimateisbasedondetailedandreliableexploration,samplingandtestinginformationgatheredthroughappropriatetechniquesfromlocationssuchasoutcrops,trenches,pits,workingsanddrillholesthatarespacedcloselyenoughtoconfirmbothgeologicalandgradecontinuity.

Miningclaim

Afootprintoflandthatapartyhasstakedormarkedoutinaccordancewithapplicablemininglawstoacquiretherighttoexploreforand,inmostinstances,exploitthemineralsunderthesurface.

Netprofitsinterestroyalty

Aroyaltybasedontheprofitremainingafterrecaptureofcertainoperating,capitalandothercosts.

Netsmelterreturnroyalty

Aroyaltybasedonapercentageofvaluablemineralsproducedwithsettlementmadeeitherinkindorincurrencybasedonthesaleproceedsreceivedlessalloftheoffsitesmelting,refiningandtransportationcostsassociatedwiththepurificationoftheeconomicmetals.

Openpitmine

Aminewherematerialsareremovedinanexcavationfromsurface.

Ore

Materialcontainingmetallicornon-metallicmineralswhichcanbeminedandprocessedataprofit.

Orebody

Asufficientlylargeamountoforethatiscontiguousandcanbeminedeconomically.

-7-

Oxideore

Mineralizedrockinwhichsomeofthehostrockororiginalmineralizationhasbeenoxidized.

QualifiedPerson

See“ScientificandTechnicalInformation”.

Reclamation

Theprocessbywhichlandsdisturbedasaresultofminingactivityaremodifiedtosupportbeneficiallanduse.Reclamationactivitymayincludetheremovalofbuildings,equipment,machineryandotherphysicalremnantsofmining,closureoftailingsstoragefacilities,leachpadsandotherminefeatures,andcontouring,coveringandre-vegetationofwasterockandotherdisturbedareas.

Reclamationandclosurecosts

Thecostofreclamationplusothercosts,includingwithoutlimitationcertainpersonnelcosts,insurance,propertyholdingcostssuchastaxes,rentalandclaimfees,andcommunityprogramsassociatedwithclosinganoperatingmine.

Recoveryrate

Atermusedinprocessmetallurgytoindicatetheproportionofvaluablematerialphysicallyrecoveredintheprocessingofore.Itisgenerallystatedasapercentageofthematerialrecoveredcomparedtothetotalmaterialoriginallypresent.

Refining

Thefinalstageofmetalproductioninwhichimpuritiesareremovedfromamoltenmetal.

Refractorymaterial

Mineralizedmaterialfromwhichmetalisnotamenabletorecoverybyconventionalcyanidemethodswithoutanypre-treatment.Therefractorynaturecanbeduetoeithersilicaorsulfideencapsulationofthemetalorthepresenceofnaturallyoccurringcarbonorotherconstituentsthatreducegoldrecovery.

Roasting

Thetreatmentofsulfideorebyheatandair,oroxygenenrichedair,inordertooxidizesulfidesandremoveotherelements(carbon,antimonyorarsenic).

Shaft

Averticalpassagewaytoanundergroundmineforventilation,movingpersonnel,equipment,suppliesandmaterialincludingoreandwasterock.

Tailings

Thematerialthatremainsafterprocessing.

Tailingsstoragefacility

Anareaconstructedforlongtermstorageofmaterialthatremainsafterprocessing.

Tons

Shorttons(2,000poundsorapproximately907kilograms).

Tonnes

Metrictonnes(1,000kilogramsorapproximately2,205pounds).

-8-

Underhandcut-and-fill

Acut-and-fillmethodofundergroundminingthatworksdownward,withcementedfillplacedabovetheworkingarea;bestsuitedwheregroundconditionsarelesscompetent.

-9-

REPORTINGCURRENCY,FINANCIALANDRESERVEINFORMATION

AllcurrencyamountsinthisAnnualInformationFormareexpressedinUnitedStatesdollars,unlessotherwiseindicated.Referencesto“C$”aretoCanadiandollars.Referencesto“A$”aretoAustraliandollars.Referencesto“CLP”aretoChileanpesos.Referencesto“ARS”aretoArgentineanpesos.ForCanadiandollarstoU.S.dollars,theaverageexchangeratefor2017andtheexchangerateasatDecember31,2017wereoneCanadiandollarper0.77and0.80U.S.dollars,respectively.ForAustraliandollarstoU.S.dollars,theaverageexchangeratefor2017andtheexchangerateasatDecember31,2017wereoneAustraliandollarper0.77and0.78U.S.dollars,respectively.ForChileanpesostoU.S.dollars,theaverageexchangeratefor2017andtheexchangerateasatDecember31,2017wereoneU.S.dollarper649and615Chileanpesos,respectively.ForArgentineanpesostoU.S.dollars,theaverageexchangeratefor2017andtheexchangerateasatDecember31,2017wereoneU.S.dollarper16.56and18.61Argentineanpesos,respectively.

FortheyearendedDecember31,2017andforthecomparativepriorperiodsidentifiedinthisAnnualInformationForm,BarrickGoldCorporation(“Barrick”orthe“Company”)prepareditsfinancialstatementsinaccordancewithInternationalFinancialReportingStandardsasissuedbytheInternationalAccountingStandardsBoard(“IFRS”).TheauditedconsolidatedfinancialstatementsoftheCompanyfortheyearendedDecember31,2017(the“ConsolidatedFinancialStatements”)areavailableelectronicallyfromtheCanadianSystemforElectronicDocumentAnalysisandRetrieval(“SEDAR”)atwww.sedar.comandfromtheU.S.SecuritiesandExchangeCommission’s(the“SEC”)ElectronicDocumentGatheringandRetrievalSystem(“EDGAR”)atwww.sec.gov.

Mineralreserves(“reserves”)andmineralresources(“resources”)havebeenestimatedasatDecember31,2017inaccordancewithNationalInstrument43-101–StandardsofDisclosureforMineralProjects(“NationalInstrument43-101”),asrequiredbyCanadiansecuritiesregulatoryauthorities.ForUnitedStatesreportingpurposes,IndustryGuide7(undertheSecuritiesandExchangeActof1934),asinterpretedbytheStaffoftheSEC,appliesdifferentstandardsinordertoclassifymineralizationasareserve(seeNote8of“–NotestotheMineralReservesandResourcesTables”in“NarrativeDescriptionoftheBusiness–MineralReservesandMineralResources”).Inaddition,whiletheterms“measured”,“indicated”and“inferred”mineralresourcesarerequiredpursuanttoNationalInstrument43-101,theSECdoesnotrecognizesuchterms.CanadianstandardsdiffersignificantlyfromtherequirementsoftheSEC,andmineralresourceinformationcontainedhereinisnotcomparabletosimilarinformationregardingmineralreservesdisclosedinaccordancewiththerequirementsoftheSEC.Readersshouldunderstandthat“inferred”mineralresourceshaveagreatamountofuncertaintyastotheirexistenceandastotheireconomicandlegalfeasibility.Inaddition,readersarecautionednottoassumethatalloranypartofBarrick’smineralresourcesconstituteorwillbeconvertedintoreserves.

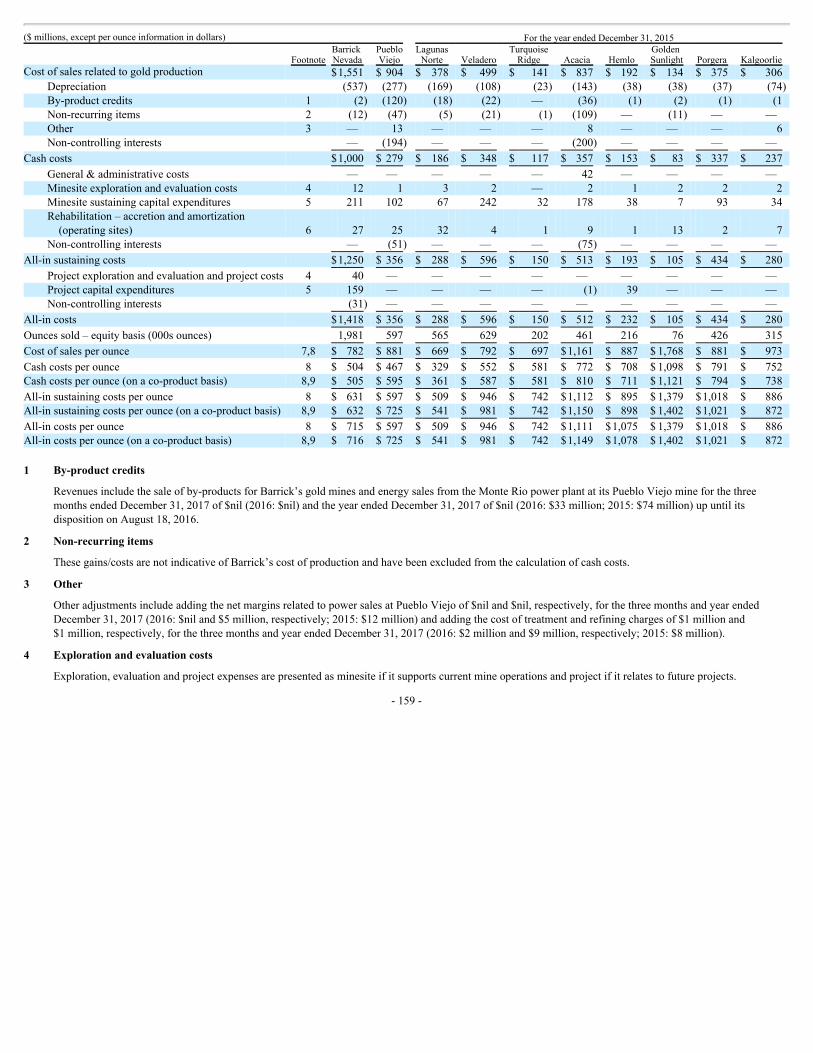

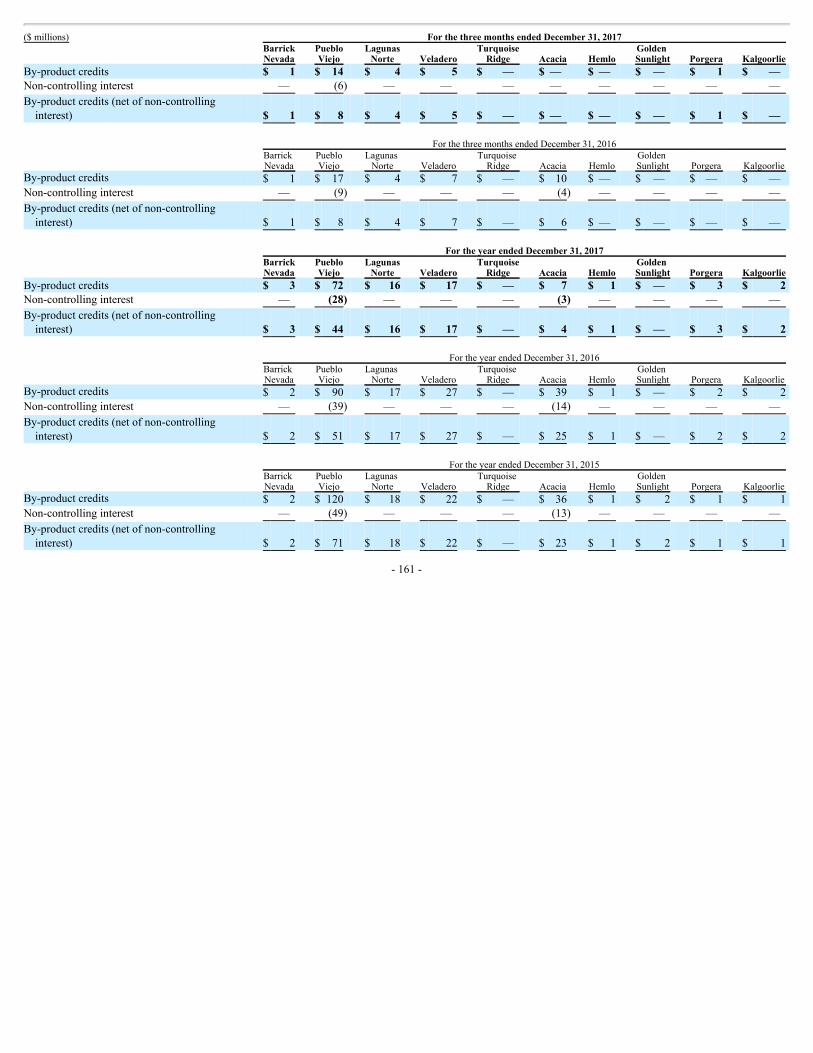

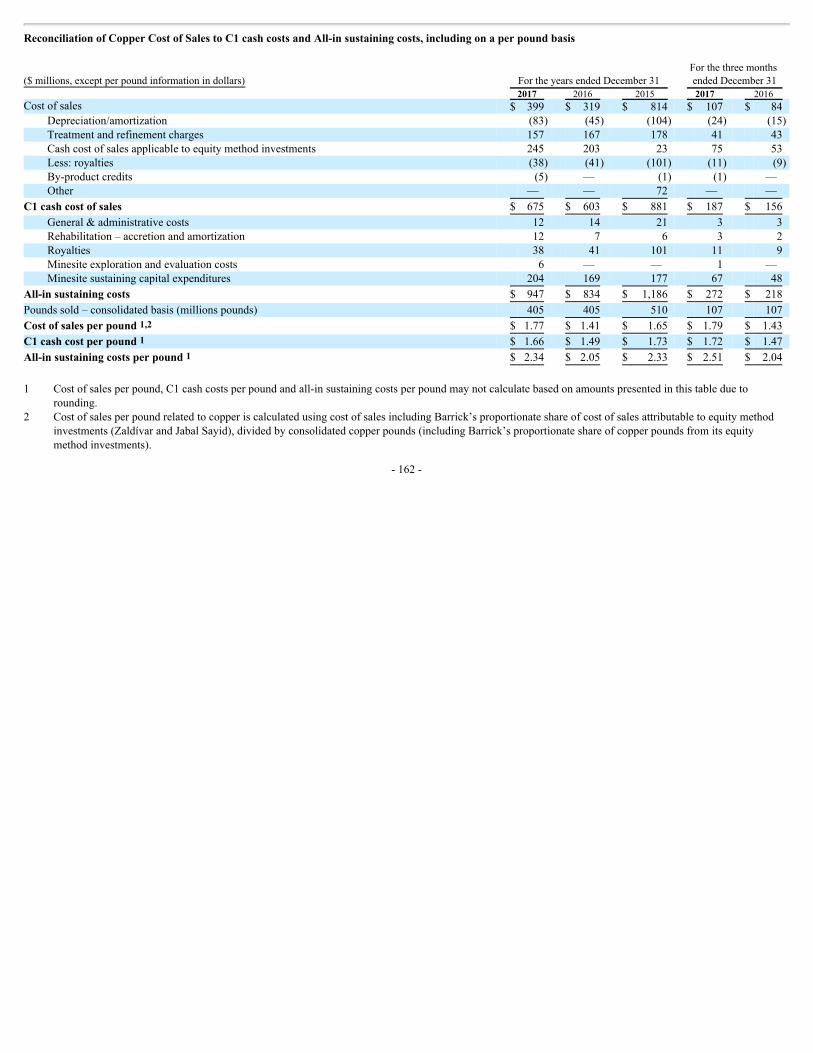

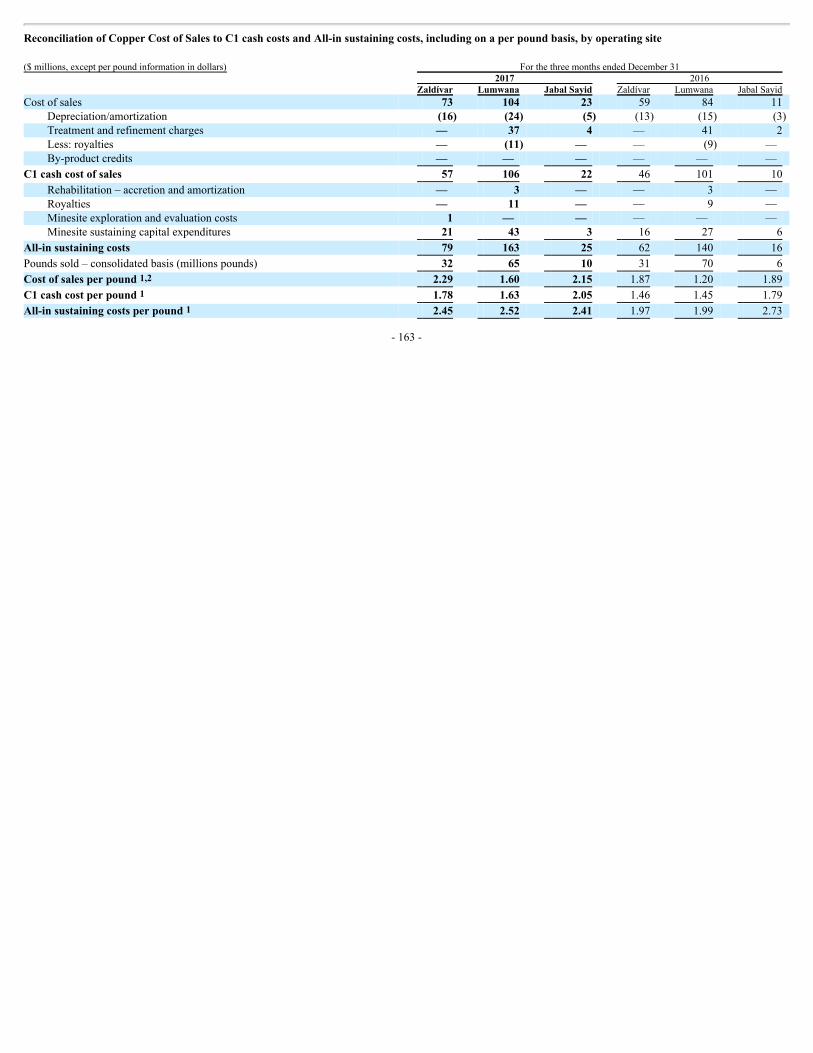

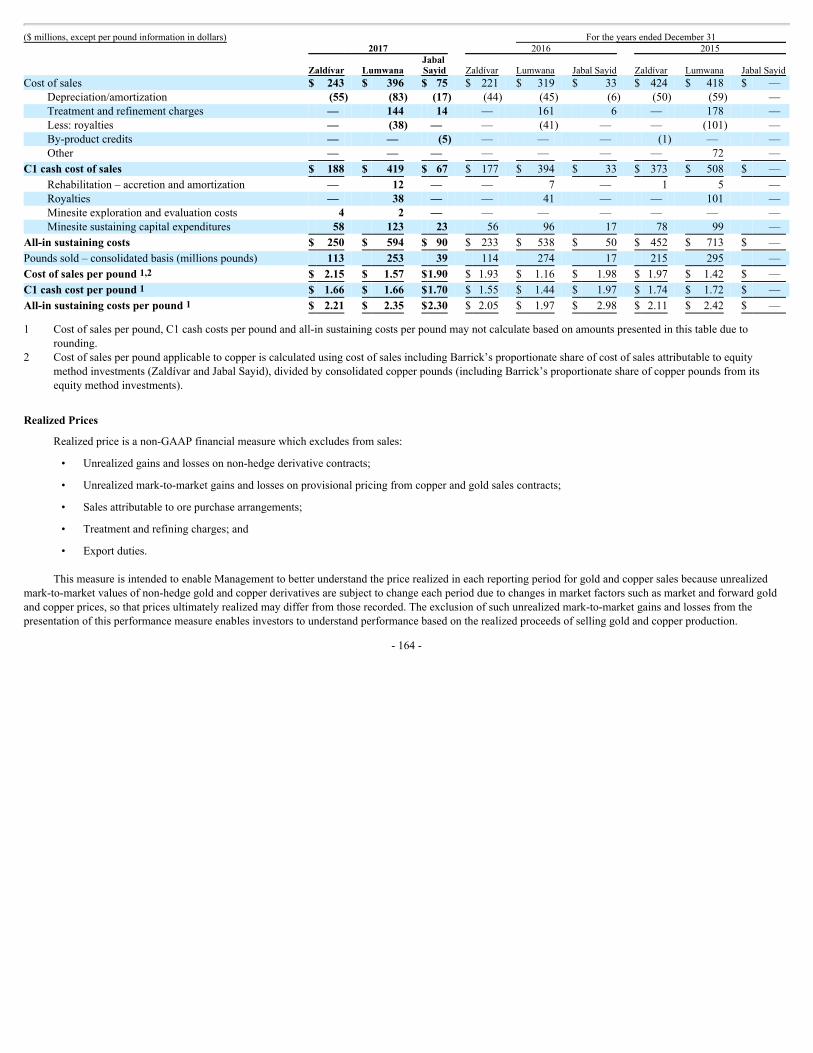

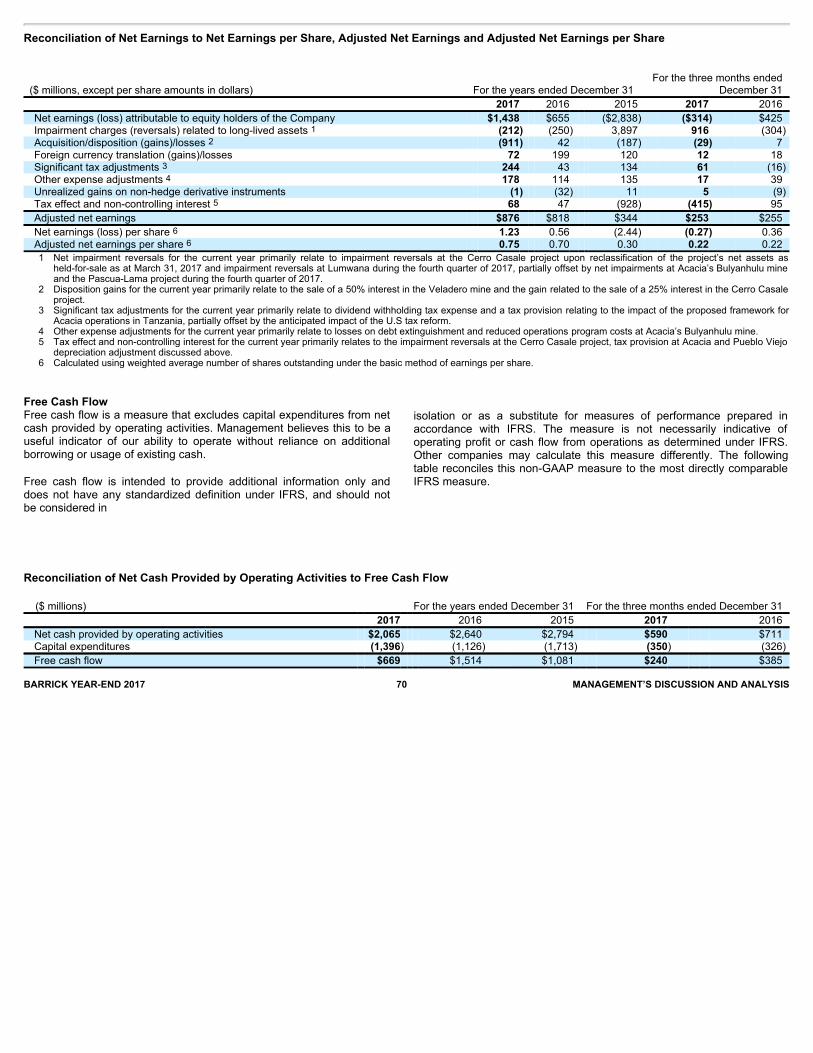

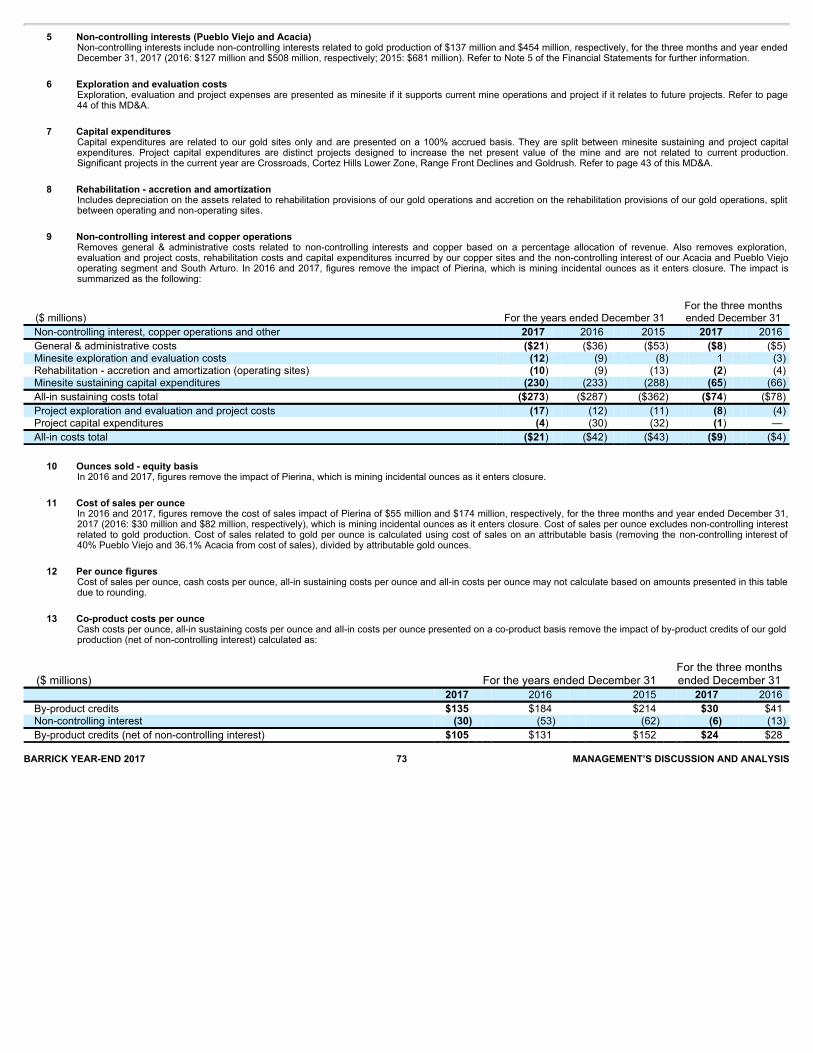

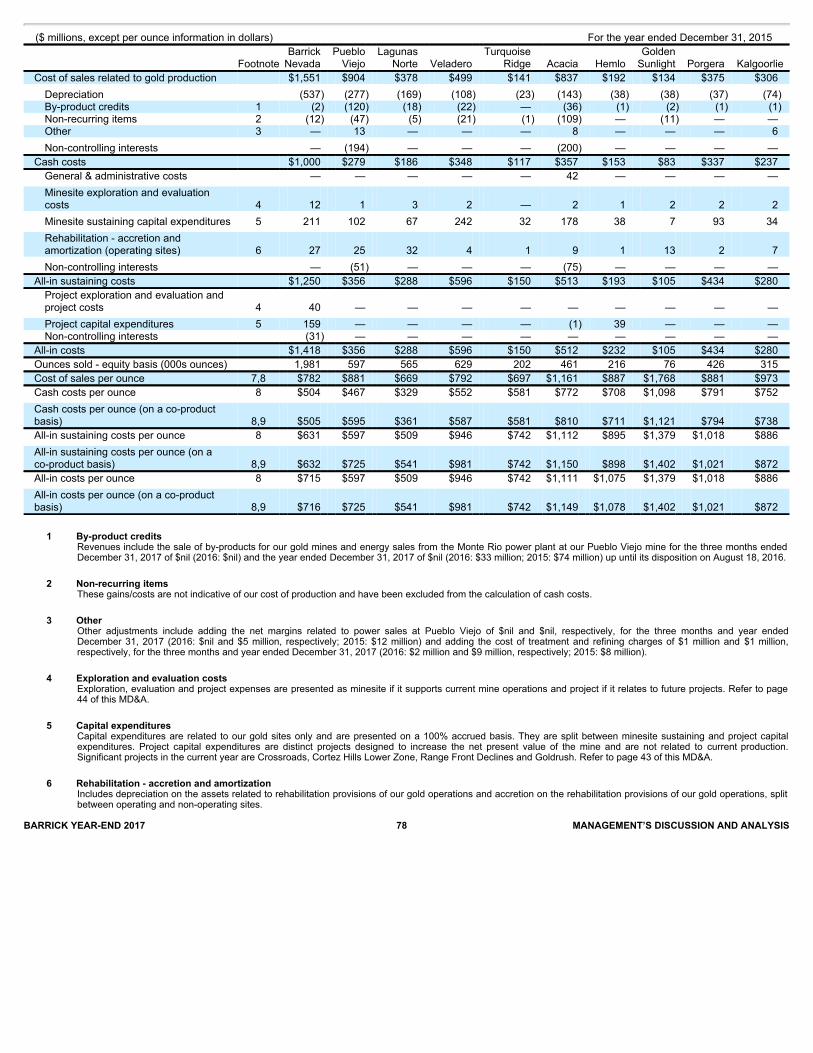

Barrickusescertainnon-GAAPfinancialperformancemeasuresinitsfinancialreports,includingcashcostsperounce,all-insustainingcostsperounce,all-incostsperounce,C1cashcostsperpoundandall-insustainingcostsperpound.Foradescriptionandreconciliationofeachofthesemeasures,pleaseseepages69to84ofBarrick’sManagement’sDiscussionandAnalysisofFinancialandOperatingResultsfortheyearendedDecember31,2017containedinBarrick’s2017AnnualReport(the“MD&A”).Seealso“Non-GAAPFinancialMeasures”atpages150to167foradetaileddiscussionofeachofthenon-GAAPmeasuresusedinthisAnnualInformationForm.

FORWARD-LOOKINGINFORMATION

CertaininformationcontainedinthisAnnualInformationForm,includinganyinformationastoBarrick’sstrategy,projects,plansorfuturefinancialoroperatingperformance,constitutes“forward-lookingstatements”.Allstatements,otherthanstatementsofhistoricalfact,areforward-looking

-10-

statements.Thewords“believe”,“expect”,“anticipate”,“contemplate”,“target”,“plan”,“goal”,“aim”,“intends”,“continue”,“budget”,“estimate”,“may”,“will”,“can”,“could”,“should”,“schedule”andsimilarexpressionsidentifyforward-lookingstatements.Forward-lookingstatementsarenecessarilybaseduponanumberofestimatesandassumptionsrelatedtothefactorssetforthbelowthat,whileconsideredreasonablebyBarrickasatthedateofthisAnnualInformationForminlightofmanagement’sexperienceandperceptionofcurrentconditionsandexpecteddevelopments,areinherentlysubjecttosignificantbusiness,economicandcompetitiveuncertaintiesandcontingencies.Knownandunknownfactorscouldcauseactualresultstodiffermateriallyfromthoseprojectedintheforward-lookingstatementsandunduerelianceshouldnotbeplacedonsuchstatementsandinformation.Suchfactorsinclude,butarenotlimitedto:

• fluctuationsinthespotandforwardpriceofgold,copperorcertainothercommodities(suchassilver,dieselfuel,naturalgasandelectricity);

• changesinnationalandlocalgovernmentlegislation,taxation,controlsorregulationsand/orchangesintheadministrationoflaws,policies,andpractices,expropriationornationalizationofpropertyandpoliticaloreconomicdevelopmentsinCanada,theUnitedStates,DominicanRepublic,Australia,PapuaNewGuinea,Chile,Peru,Argentina,Tanzania,Zambia,SaudiArabia,UnitedKingdomorBarbadosorothercountriesinwhichBarrickdoesormaycarryonbusinessinthefuture;

• failuretocomplywithenvironmentalandhealthandsafetylawsandregulations;

• timingofreceiptof,orfailuretocomplywith,necessarypermitsandapprovals;

• increasedcostsandphysicalrisks,includingextremeweathereventsandresourceshortage,relatedtoclimatechange;

• diminishingquantitiesorgradesofreserves;

• increasedcosts,delays,suspensionsandtechnicalchallengesassociatedwiththeconstructionofcapitalprojects;

• risksassociatedwiththeimplementationofBarrick’sdigitaltransformationinitiative,andtheabilityoftheprojectsunderthisinitiativetomeetBarrick’scapitalallocationobjectives;

• risksassociatedwiththefactthatcertainBest-in-Classinitiativesarestillintheearlystagesofevaluation,andadditionalengineeringandotheranalysisisrequiredtofullyassesstheirimpact;

• theultimateresolutionofadisputerelatingto(i)theimpositionbytheTanzaniangovernmentofabanonmineralconcentrateexportscurrentlyimpacting

theoperationsofAcaciaMiningplc(“Acacia”),(ii)allegationsbytheGovernmentofTanzaniathatAcaciaunder-declaredthemetalcontentofconcentrateexportsfromTanzania,and(iii)certaintaxre-assessmentsofAcaciabytheTanzaniangovernment;

• thebenefitsexpectedfromrecenttransactionsbeingrealized;

• uncertaintywhethersomeoralloftheBest-in-ClassinitiativesandtargetedinvestmentswillmeettheCompany’scapitalallocationobjectives;

• lackofcertaintywithrespecttoforeignlegalsystems,corruptionandotherfactorsthatareinconsistentwiththeruleoflaw;

• theimpactofgloballiquidityandcreditavailabilityonthetimingofcashflowsandthevaluesofassetsandliabilitiesbasedonprojectedfuturecashflows;

• adversechangesintheCompany’screditratings;

• theimpactofinflation;

• risksassociatedwithworkingwithpartnersinjointlycontrolledassets;

-11-

• operatingortechnicaldifficultiesinconnectionwithminingordevelopmentactivities,includinggeotechnicalchallenges,anddisruptionsinthemaintenanceorprovisionofrequiredinfrastructureandinformationtechnologysystems;

• damagetoBarrick’sreputationduetotheactualorperceivedoccurrenceofanynumberofevents,includingnegativepublicitywithrespecttoBarrick’shandlingofenvironmentalmattersordealingswithcommunitygroups,whethertrueornot;

• thespeculativenatureofmineralexplorationanddevelopment;

• changesinmineralproductionperformance,exploitationandexplorationsuccesses;

• riskoflossduetoactsofwar,terrorism,sabotageandcivildisturbances;

• fluctuationsinthecurrencymarkets(suchasCanadianandAustraliandollars,Chilean,ArgentineanandDominicanpesos,Britishpound,Peruviansol,Zambiankwacha,SouthAfricanrand,TanzanianshillingandPapuaNewGuineankinaversustheU.S.dollar);

• changesinU.S.dollarinterestratesthatcouldimpactthemark-to-marketvalueofoutstandingderivativeinstrumentsandongoingpayments/receiptsunderinterestrateswapsandvariableratedebtobligations;

• risksarisingfromholdingderivativeinstruments(suchascreditrisk,marketliquidityriskandmark-to-marketrisk);

• litigationandlegalandadministrativeproceedings;

• contestsovertitletoproperties,particularlytitletoundevelopedproperties,oroveraccesstowater,powerandotherrequiredinfrastructure;

• businessopportunitiesthatmaybepresentedto,orpursuedby,theCompany;

• theCompany’sabilitytosuccessfullyintegrateacquisitionsorcompletedivestitures;

• employeerelations,includinglossofkeyemployees;

• availabilityandincreasedcostsassociatedwithmininginputsandlabor;and

• theorganizationofBarrick’spreviouslyheldAfricangoldoperationsandpropertiesunderaseparatelistedcompany.

Inaddition,therearerisksandhazardsassociatedwiththebusinessofmineralexploration,developmentandmining,includingenvironmentalhazards,industrialaccidents,unusualorunexpectedformations,pressures,cave-ins,floodingandgoldbullion,coppercathodeorgoldorcopperconcentratelosses(andtheriskofinadequateinsurance,orinabilitytoobtaininsurance,tocovertheserisks).ManyoftheseuncertaintiesandcontingenciescanaffecttheCompany’sactualresultsandcouldcauseactualresultstodiffermateriallyfromthoseexpressedorimpliedinanyforward-lookingstatementsmadeby,oronbehalfof,theCompany.Readersarecautionedthatforward-lookingstatementsarenotguaranteesoffutureperformance.Alloftheforward-lookingstatementsmadeinthisAnnualInformationFormarequalifiedbythesecautionarystatements.Specificreferenceismadeto“NarrativeDescriptionoftheBusiness–MineralReservesandMineralResources”and“RiskFactors”andtotheMD&A(whichisavailableonSEDARatwww.sedar.comandonEDGARatwww.sec.govasanexhibittoBarrick’sForm40-F)foradiscussionofsomeofthefactorsunderlyingforward-lookingstatementsandtherisksthatmayaffectBarrick’sabilitytoachievetheexpectationssetforthintheforward-lookingstatementscontainedinthisAnnualInformationForm.

TheCompanymay,fromtimetotime,makeoralforward-lookingstatements.TheCompanyadvisesthattheaboveparagraphandtheriskfactorsdescribedinthisAnnualInformationFormandintheCompany’sotherdocumentsfiledwiththeCanadiansecuritiesregulatoryauthoritiesandtheSECshouldbereadforadescriptionofcertainfactorsthatcouldcausetheactualresultsoftheCompanytomateriallydifferfromthoseintheoralforward-lookingstatements.TheCompanydisclaimsanyintentionor

-12-

obligationtoupdateorreviseanyoralorwrittenforward-lookingstatementswhetherasaresultofnewinformation,futureeventsorotherwise,exceptasrequiredbyapplicablelaw.

SCIENTIFICANDTECHNICALINFORMATION

Unlessotherwiseindicated,scientificortechnicalinformationinthisAnnualInformationFormrelatingtomineralreservesormineralresourcesisbasedoninformationpreparedbyemployeesofBarrick,itsjointventurepartnersoritsjointventureoperatingcompanies,asapplicable,ineachcaseunderthesupervisionof,orfollowingreviewby,RickSims,VicePresident,ReservesandResources,StevenHaggarty,SeniorDirector,MetallurgyorPatrickGarretson,SeniorDirector,LifeofMinePlanning.

ScientificortechnicalinformationinthisAnnualInformationFormrelatingtothegeologyofparticularpropertiesandexplorationprogramsisbasedoninformationpreparedbyemployeesofBarrick,itsjointventurepartnersoritsjointventureoperatingcompanies,asapplicable,ineachcaseunderthesupervisionofRobertKrcmarov,ExecutiveVicePresident,ExplorationandGrowth.

EachofMessrs.Sims,Haggarty,GarretsonandKrcmarovisa“QualifiedPerson”asdefinedinNationalInstrument43-101.A“QualifiedPerson”meansanindividualwhoisanengineerorgeoscientistwithatleastfiveyearsofexperienceinmineralexploration,minedevelopmentoroperationormineralprojectassessment,oranycombinationofthese,hasexperiencerelevanttothesubjectmatterofthemineralproject,andisamemberingoodstandingofaprofessionalassociation.

EachofMessrs.Sims,Haggarty,GarretsonandKrcmarovisanofficeroremployeeofBarrickand/oranofficer,directororemployeeofoneormoreofitsassociatesoraffiliates.NosuchpersonreceivedorwillreceiveadirectorindirectinterestinanypropertyofBarrickoranyofitsassociatesoraffiliates.Asofthedatehereof,eachsuchpersonownsbeneficially,directlyorindirectly,lessthan1%ofanyoutstandingclassofsecuritiesofBarrickandlessthan1%ofanyoutstandingclassofsecuritiesofBarrick’sassociatesoraffiliates.

GENERALINFORMATION

OrganizationalStructure

BarrickisacorporationgovernedbytheBusinessCorporationsAct(Ontario)resultingfromtheamalgamation,effectiveJuly14,1984,ofCamfloMinesLimited,Bob-ClareInvestmentsLimitedandtheformerBarrickResourcesCorporation.ByarticlesofamendmenteffectiveDecember9,1985,theCompanychangeditsnametoAmericanBarrickResourcesCorporation.EffectiveJanuary1,1995,asaresultofanamalgamationwithawholly-ownedsubsidiary,theCompanychangeditsnamefromAmericanBarrickResourcesCorporationtoBarrickGoldCorporation.OnDecember7,2001,inconnectionwithitsacquisitionofHomestakeMiningCompany(“Homestake”),theCompanyamendeditsarticlestocreateaspecialvotingshare,whichhasspecialvotingrightsdesignedtopermitholdersofBarrickGoldInc.(formerlyHomestakeCanadaInc.)(“BGI”)exchangeablesharestovoteasasingleclasswiththeholdersofBarrickcommonshares.InMarch2009,inconnectionwithBarrick’sredemptionofalloftheoutstandingBGIexchangeableshares,thesingleoutstandingspecialvotingsharewasredeemedandcancelled.InconnectionwithitsacquisitionofPlacerDomeInc.(“PlacerDome”),BarrickamalgamatedwithPlacerDomepursuanttoarticlesofamalgamationdatedMay9,2006.InconnectionwiththeacquisitionofArizonaStarResourceCorp.(“ArizonaStar”),BarrickamalgamatedwithArizonaStarpursuanttoarticlesofamalgamationdatedJanuary1,2009.Barrick’sheadandregisteredofficeislocatedatBrookfieldPlace,TDCanadaTrustTower,161BayStreet,Suite3700,Toronto,Ontario,M5J2S1.

-13-

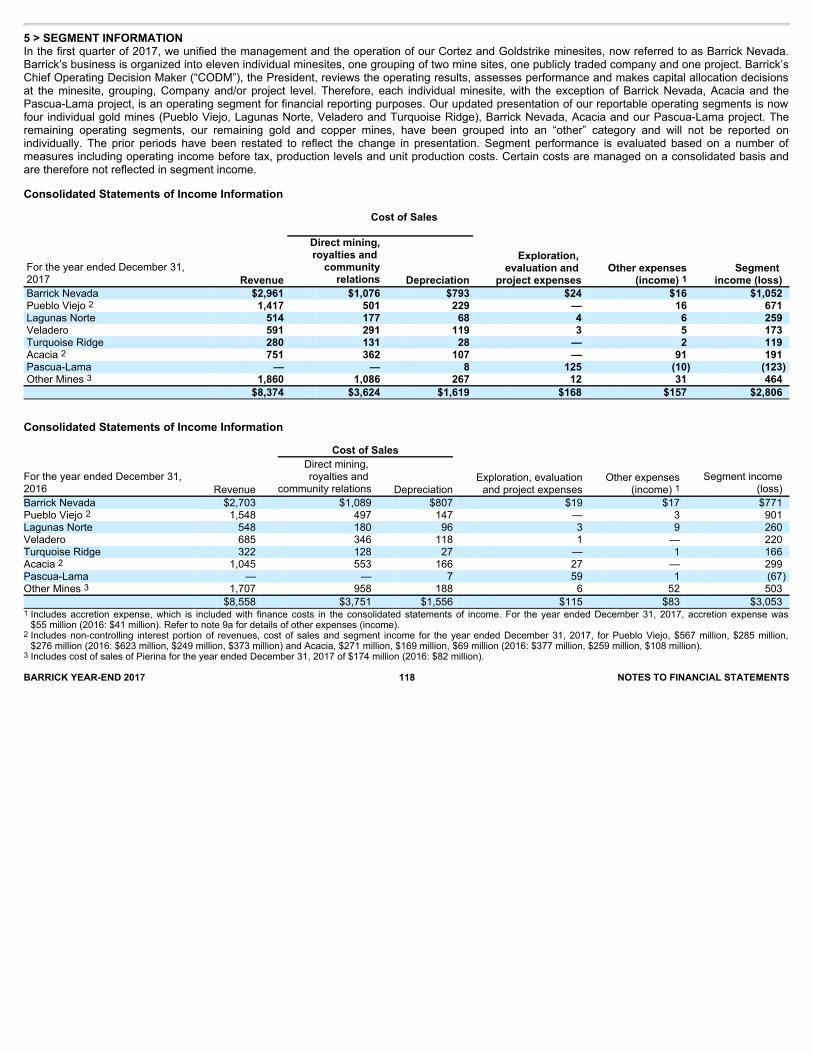

Barrick’sbusinessisorganizedintooperatingsegmentsforfinancialreportingpurposes,comprisingelevenindividualminesites,BarrickNevada(composedoftheCortezandGoldstrikepropertiesasdescribedinfurtherdetailbelow),onepubliclytradedcompany(Acacia)andoneproject(Pascua-Lama).Barrick’sreportableoperatingsegmentsareBarrickNevada,PuebloViejo,LagunasNorte,Veladero,TurquoiseRidge,AcaciaandPascua-Lama.Inthefirstquarterof2017,BarrickunifiedthemanagementandoperationofitsCortezandGoldstrikeproperties,nowreferredtoasBarrickNevada.Forfinancialreportingpurposes,theCompany’sremainingoperatingsegmentsthatarenotreportableoperatingsegmentsaregroupedintoan“other”categoryandarenotreportedonindividually.ThematerialpropertiespresentedinthisAnnualInformationFormare:Cortez,Goldstrike,PuebloViejo,LagunasNorte,VeladeroandTurquoiseRidge.See“NarrativeDescriptionoftheBusiness–ReportableOperatingSegments”.

Subsidiaries

AsignificantportionofBarrick’sbusinessiscarriedonthroughitssubsidiaries.AchartshowingBarrick’smines,projects,relatedoperatingsubsidiaries,othersignificantsubsidiariesandcertainassociatedsubsidiariesasatMarch19,2018andtheirrespectivelocationsorjurisdictionsofincorporation,asapplicable,issetoutbelow.Allsubsidiaries,minesandprojectsreferredtointhechartare100%owned,unlessotherwisenoted.

-14-

-15-

AreasofInterest

AmapshowingBarrick’sminingoperationsandprojectsasatMarch19,2018,includingthoseminesheldthroughBarrick’sequityinterestinAcacia,issetoutattheendofthis“GeneralInformation”section.

GeneralDevelopmentoftheBusiness

History

Barrickenteredthegoldminingbusinessin1983andisaleadinginternationalgoldcompany.TheCompanyhasinterestsinoperatingminesorprojectsinCanada,theUnitedStates,theDominicanRepublic,Peru,Chile,Argentina,Tanzania,Zambia,Australia,PapuaNewGuineaandSaudiArabia.TheCompany’sprincipalproductsandsourcesofearningsaregoldandcopper.

Duringitsfirsttenyears,BarrickfocusedonacquiringanddevelopingpropertiesinNorthAmerica,notablytheCompany’sGoldstrikepropertyontheCarlinTrendinNevada.Since1994,BarrickhasstrategicallyexpandedbeyonditsNorthAmericanbaseandnowoperatesonfivecontinents.

Strategy

Barrick’sstrategyisfocusedongrowingfreecashflowpershareoverthelongterm.TheCompanyaimstoachievethisby:(i)maintainingindustryleadingmargins,drivenbyoperationalexcellence,technologicalinnovationandsuperiorexecution;(ii)maintainingasuperiorportfolioofassetsandallocatingcapitalwithdisciplineandrigor;(iii)maintainingarobustbalancesheetthatcanwithstandgoldpricevolatilityandsupportinvestmentthroughmetalpricecycles;and(iv)leveragingtheCompany’stalentanddistinctivepartnershipcultureascompetitiveadvantages.

BarrickisfocusedoncontinuouslyimprovingtheproductivityandefficiencyoftheCompany’sexistingoperations,whilepursuingstepchangesinperformanceoverthelong-termthroughinvestmentsindigitalsystemsandinnovation.Startinginlate2016andthroughout2017,BarricklaidthefoundationforitsdigitaltransformationthroughaseriesofpilotprojectsprimarilyfocusedattheCortezpropertyinNevada.ThisallowedBarricktoevaluatedigitalsolutionsandtheirpotentialeconomicreturnsinacontrolledenvironmentwithrigorousoversight.In2018,Barrick’sdigitalstrategywillfocusoncompletingthefirstiterationofanenterprise-grade,dataanalyticsplatform,referredtoasthe“BarrickDataFabric”.Barrickwillalsoacceleratetheimplementationofdigitalprojectsacrossitsotheroperations,withaninitialfocusinNevada.

TheCompanyisalsoadvancingfourfeasibility-levelprojectsthathavethepotentialtocontributemorethanonemillionouncesofannualproductiontoBarrick,withinitialcontributionsbeginningin2021.ProjectsinNevadaatCortezDeepSouth,Goldrush,andTurquoiseRidgehavebeenapprovedandareinexecution(finalBoardapprovalforthestartofmajorconstructionatGoldrushremainspending).OptimizationworkonasequencedprojecttopotentiallyextendthelifeoftheLagunasNortemineinPeruremainsunderway.Barrick’sportfolioalsocontainsanumberofundevelopedgreenfieldgolddeposits,providingfurtheroptionalityandleveragetogoldprices.TheseincludeAlturas,DonlinGold,NorteAbiertoandPascua-Lama.Foradditionalinformation,see“MaterialProperties–CortezProperty”,“MaterialProperties–LagunasNorteMine”,“MaterialProperties–TurquoiseRidgeMine”,and“ExplorationandEvaluations”.

AllprojectsundergorigorousscrutinybytheCompany’sInvestmentCommitteeateverystageofevaluationanddevelopment,prioritizingfreecashflowgeneration,risk-adjustedreturns,andcapital

-16-

efficiency.Eachprojectisbenchmarkedagainsta15%hurdlerateusingalong-termgoldpriceassumptionof$1,200perounceandrankedaccordingly.

Barrick’sexplorationprogramsstrikeabalancebetweenhigh-qualitybrownfieldprojects,greenfieldexploration,andemergingdiscoveriesthathavethepotentialtobecomeprofitablemines.InlinewithBarrick’sfocusongrowingitsexplorationportfolio,theCompanyhasalsocultivatedactivepartnershipswithanumberofjuniorexplorationanddevelopmentcompaniesastheCompanyseekstoidentifypotentialnewcoremineraldistrictsfortheCompany.ThesepartnershipsincludeATACattheOrionprojectintheYukon,OsiskoattheKanpropertyinnorthernQuébec,andPremierGoldatCoveMcCoyinNevada.

ForadditionalinformationregardingBarrick’sexplorationprogramsandnewdiscoveries,see“ExplorationandEvaluations”.

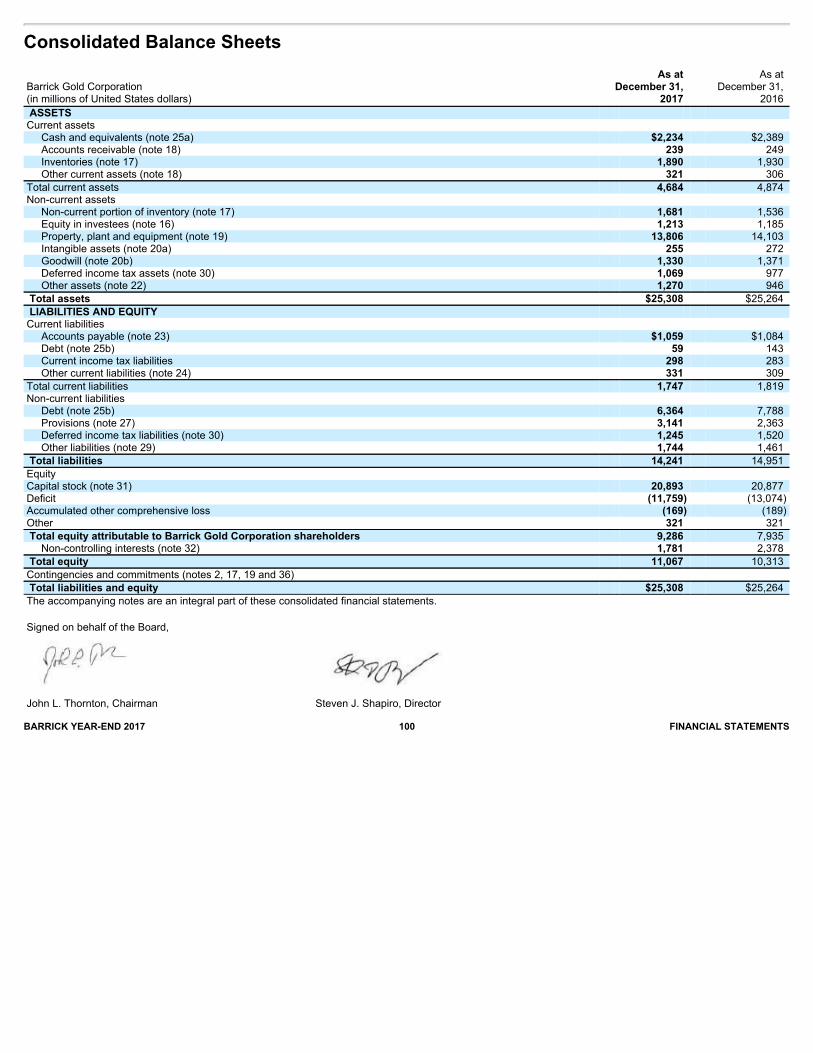

Insupportofmaintainingarobustbalancesheet,BarrickistargetingareductionoftheCompany’stotaldebtfrom$6.4billionasofyear-end2017toaround$5billionbytheendof2018.TheCompanyexpectstoachievethisprimarilybyusingcashflowfromoperationsandcashonhand,andpotentiallythroughfurtherportfoliooptimization.Barrickintendstocontinuetopursuedebtreductionwithdiscipline,takingonlythoseactionsthataresensiblefortheCompany,ontermsfavourabletoshareholders.

DrivinganownershipcultureacrosstheCompanyisanotherkeyelementofBarrick’sstrategy.In2016,theCompanycreatedtheGlobalEmployeeSharePlan,whichawardsBarrickcommonsharestoemployeesbasedonoverallCompanyperformance.ThesesharesarepurchasedbyBarrickontheopenmarketandmustbeheldforaslongasanemployeeremainswiththeCompany.AsofMarch19,2018,Barrickemployeesnowownmorethan1.5millionsharesoftheCompanyasaresultoftheGlobalEmployeeSharePlan,fosteringacultureofownershipacrosstheorganization.

Barrickalsocarriedoutthefollowinginitiativesin2015,2016,and2017tooptimizeitsportfolioandstrengthenitsbalancesheet:

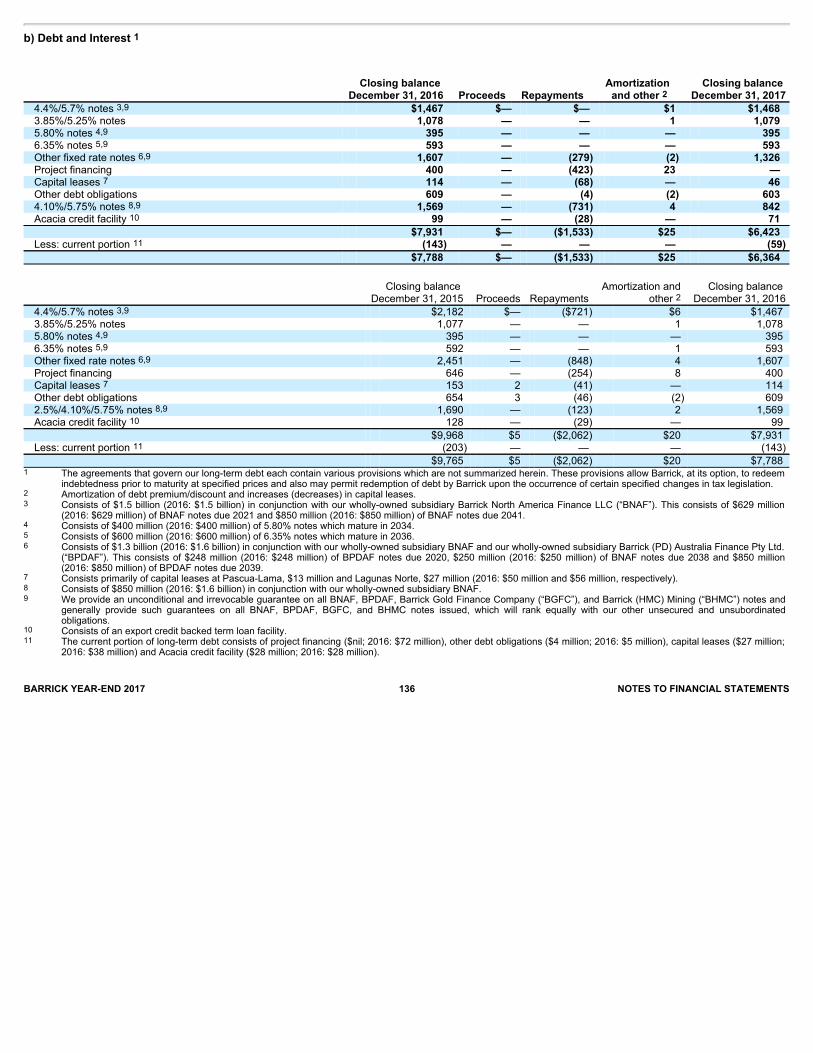

• In2015,Barrickreduceditstotaldebtby$3.1billion,exceedinganoriginaldebtreductiontargetof$3billionfortheyear,throughacombinationofnormalcourserepaymentsandearlydebtretirements.Barrickcompletedthefollowingtransactionsin2015aspartofthisdebtreductionstrategy.OnJuly23,2015,BarrickcompletedthesaleoftheCowalmineinAustraliaforcashconsiderationof$550million.OnAugust31,2015,Barrickcompletedthesaleof50%ofitsinterestinthePorgeramineinPapuaNewGuineatoZijinMiningGroupCompanyforcashconsiderationof$298million.OnSeptember29,2015,BarrickclosedagoldandsilverstreamingtransactionwithRoyalGold,Inc.(“RoyalGold”)forproductionlinkedtoBarrick’s60%interestinthePuebloViejomineintheDominicanRepublic.RoyalGoldmadeanupfrontcashpaymentof$610millionandwillcontinuetomakecashpaymentsforgoldandsilverdeliveredundertheagreement(formoreinformationaboutthePuebloViejostreamingtransaction,see“MaterialProperties–PuebloViejoMine”).OnDecember1,2015,Barrickcompletedthesaleof50%ofitsZaldívarcoppermineinChiletoAntofagastaplc.InAugust2016,Barrickfinalizedtheworkingcapitaladjustmentsresultinginfinalconsiderationof$950million.OnDecember17,2015,BarrickcompletedthesaleoftheRubyHillmineandBarrick’s70%interestintheSpringValleyproject,bothinNevada,toWatertonPreciousMetalsFundIICayman,LPforcashconsiderationof$110million.

• In2016,Barrickreduceditstotaldebtby$2.04billion,or20%,from$9.97billionto$7.93billion,exceedingitsoriginaltargetof$2billion,throughacombinationofnormalcourserepaymentsandearlydebtretirements,includingcompletionoftwocashtenderoffers.On

-17-

January11,2016,BarrickcompletedthesaleoftheBaldMountainmineandits50%interestintheRoundMountainmine,bothinNevada,toKinrossGoldCorporation(“Kinross”)forcashconsiderationof$610million,subjecttocertainclosingadjustments.

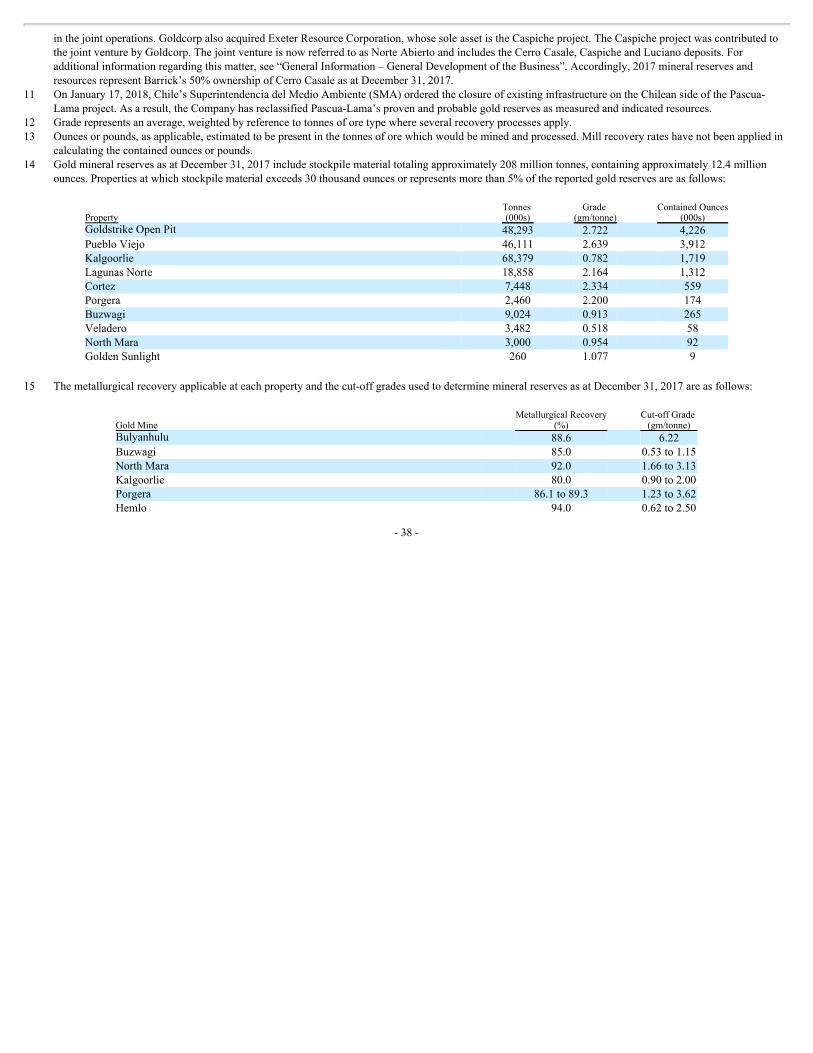

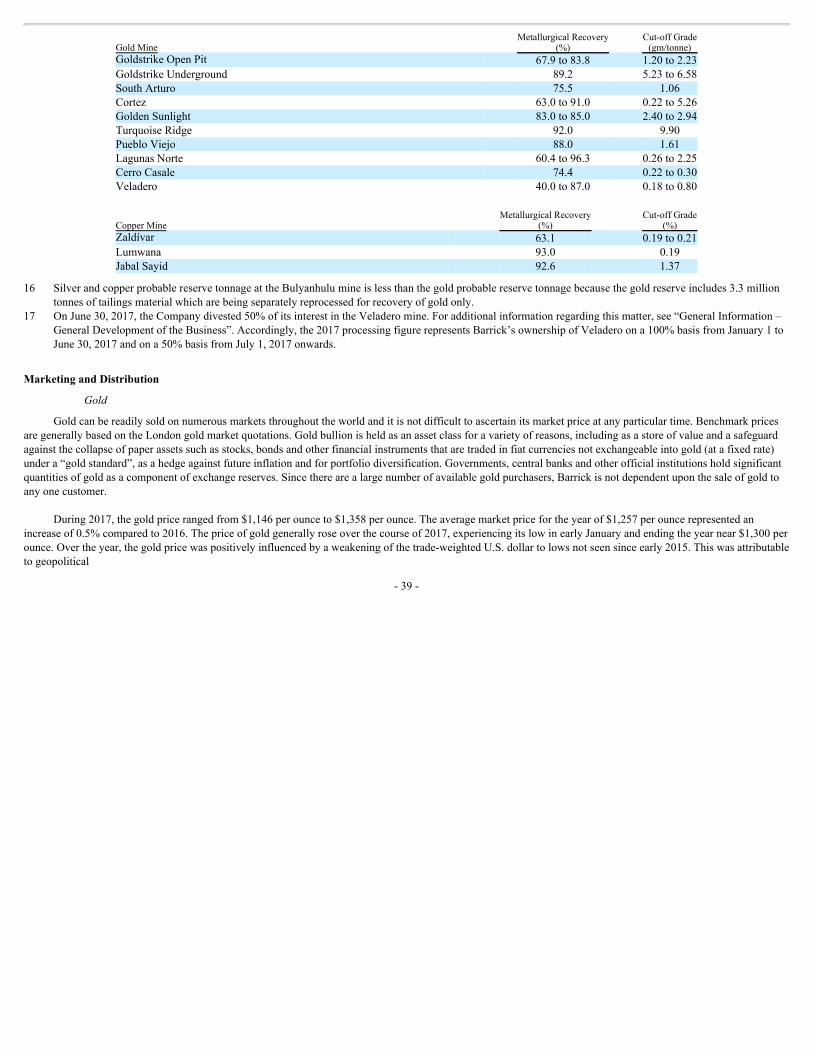

• OnJune9,2017,BarrickcompletedatransactionwithGoldcorpInc.(“Goldcorp”)toformanewjointventureattheCerroCasaleprojectinChile.Pursuanttothetransaction,Goldcorpacquireda25%interestinCerroCasalefromBarrick.Thetransaction,coupledwiththeconcurrentpurchasebyGoldcorpofKinross’s25%interestinCerroCasale,resultedinBarrickandGoldcorpeachholdinga50%interestinthejointoperations.GoldcorpenteredintoaseparateagreementfortheacquisitionofExeterResourceCorporation,whosesoleassetwastheCaspicheproject,locatedapproximately10kilometersnorthofCerroCasale.TheCaspicheprojectwascontributedtothejointventurebyGoldcorp.ThejointventureisnowreferredtoasNorteAbiertoandincludestheCerroCasale,CaspicheandLucianodeposits.

• OnJune30,2017,Barrickcompletedthesaleof50%ofitsinterestintheVeladeromineinArgentinatoShandongGoldMiningCo.,Ltd.(“Shandong”)forcashconsiderationof$960million,pluspost-closingworkingcapitaladjustmentsofapproximately$30millionreceivedinthefourthquarterof2017(fortotalproceedsofapproximately$990million).ThetwocompaniesalsoformedaworkinggrouptoexplorethejointdevelopmentofthePascua-Lamadeposit,andwillevaluateadditionalinvestmentopportunitiesonthehighlyprospectiveElIndiogoldbeltontheborderofArgentinaandChile.

• In2017,theCompanyreduceditstotaldebtby$1.51billion,or19%,exceedingtheoriginal2017debtreductiontargetof$1.45billion.

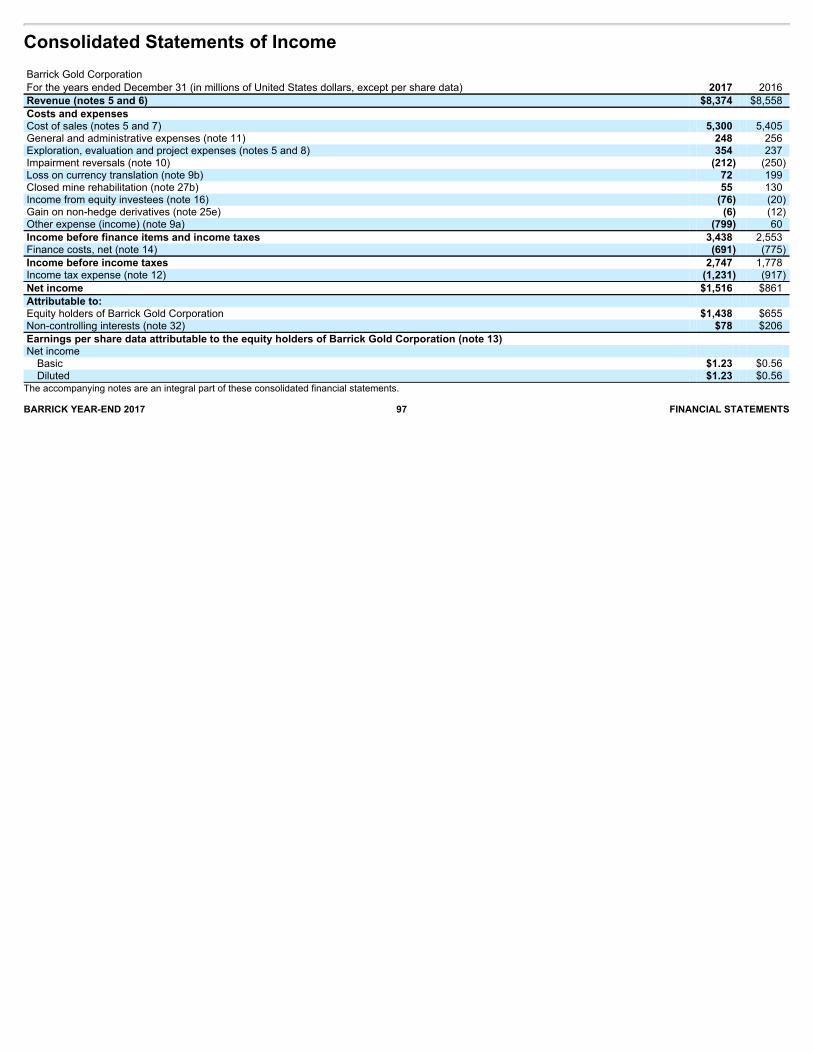

Results of Operations in 2017

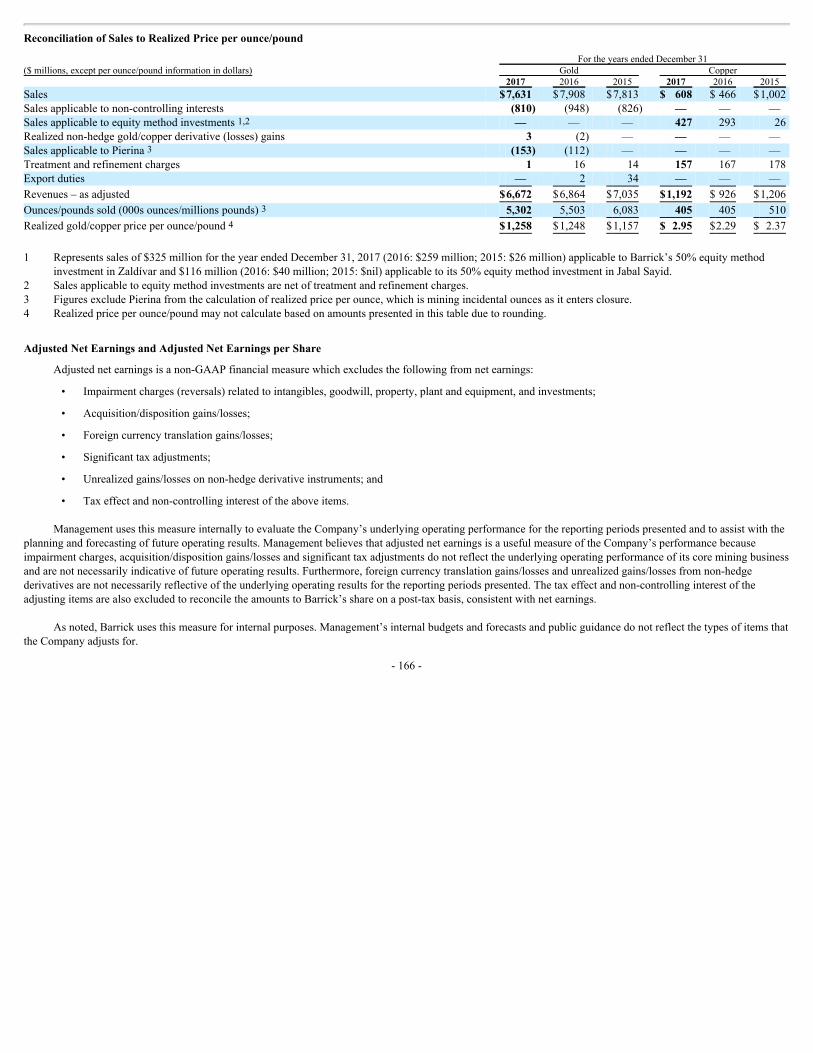

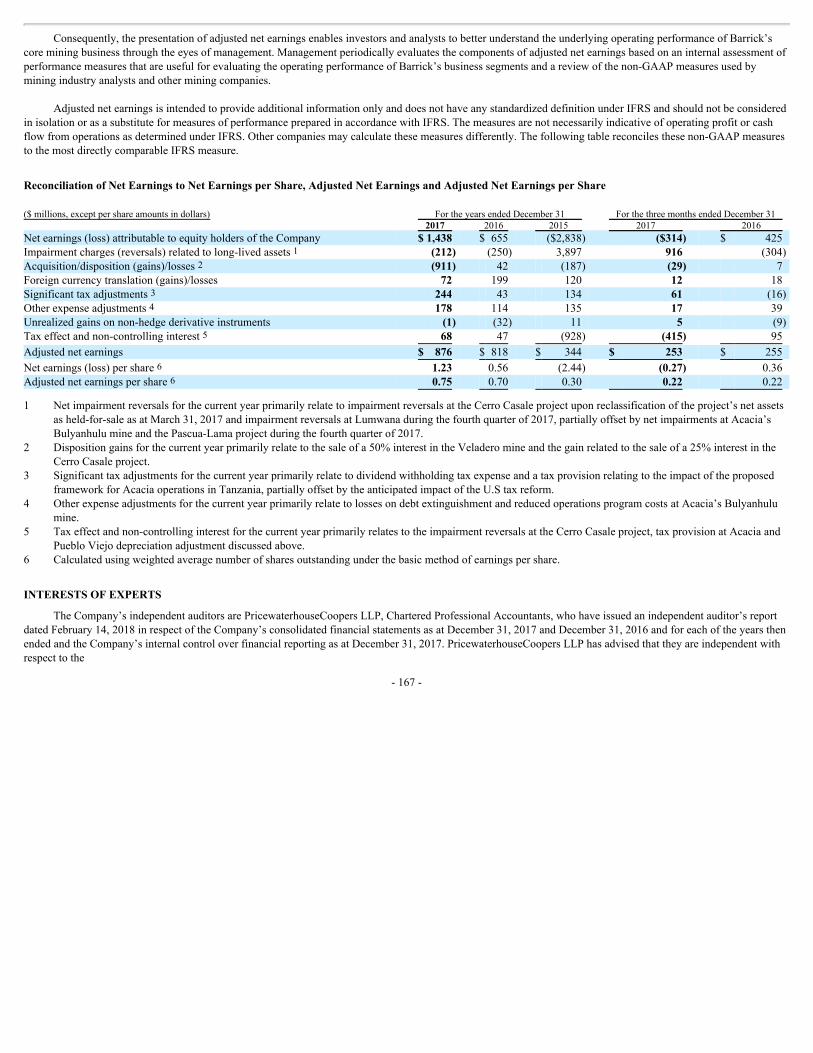

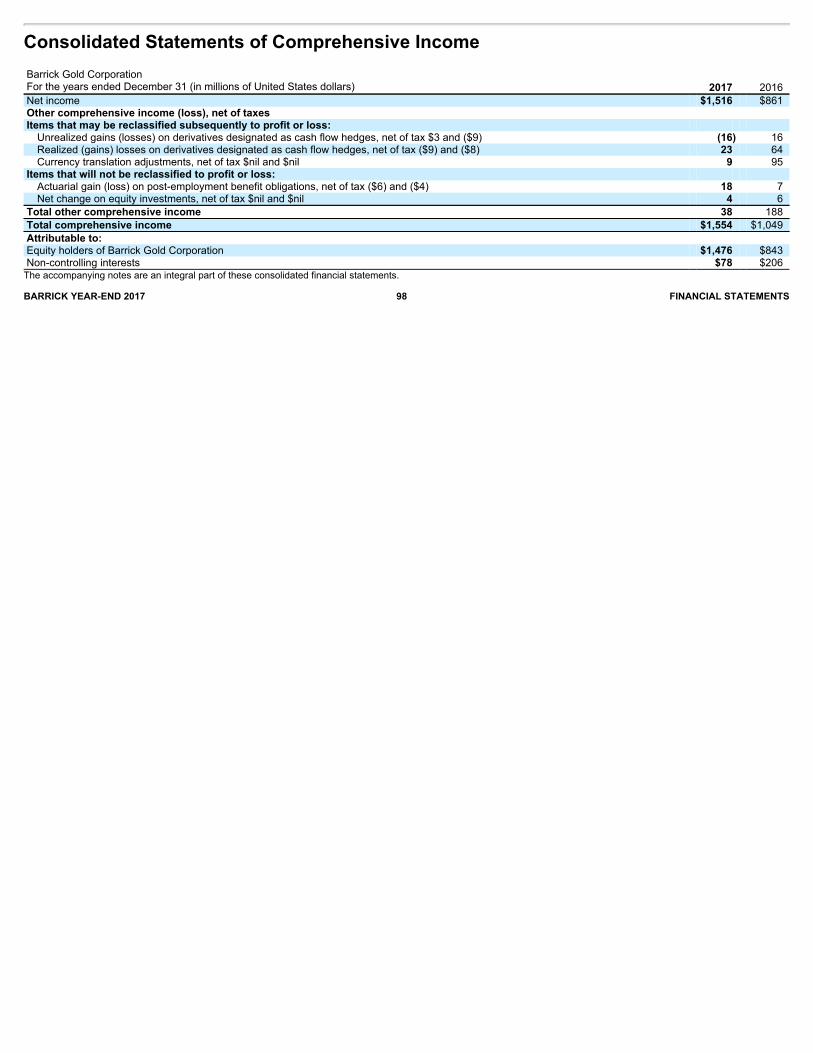

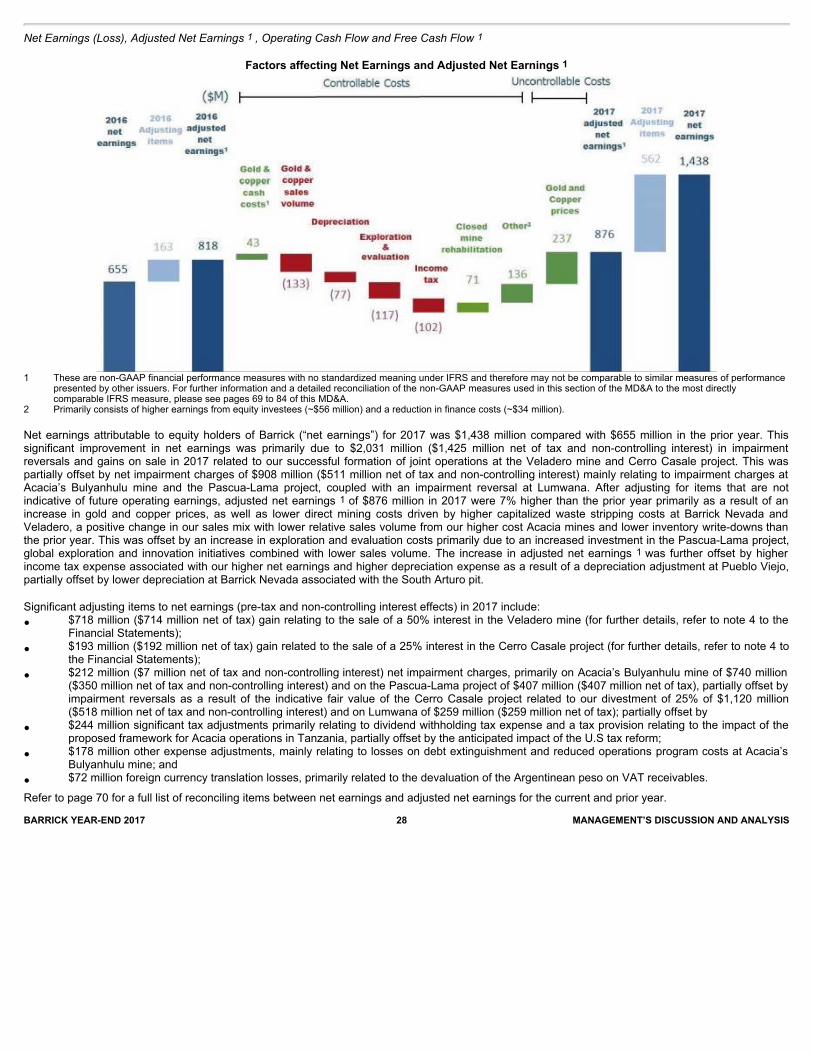

Totalrevenuesin2017were$8.4billion,adecreaseof$0.2billion,or2%,comparedto2016,primarilyduetolowergoldsalesvolume,partiallyoffsetbyhigherrealizedgoldandcopperprices.In2017,goldandcopperrevenuestotaled$7.6billionand$0.6billion,respectively,withgolddown4%,comparedtotheprioryearduetoadecreaseingoldsalesvolume,partiallyoffsetbyhigherrealizedprices,andcopperup30%comparedtotheprioryearduetohigherrealizedprices.Realizedgoldpricesof$1,258perouncein2017wereup1%comparedtotheprioryear,principallyduetohighermarketprices.Realizedcopperpricesfor2017were$2.95perpound,up29%comparedtotheprioryearduetohighermarketprices.Foranexplanationofrealizedprice,see“Non-GAAPFinancialMeasures–RealizedPrices”.In2017,Barrickreportednetearningsof$1.438billion,includingafter-taxnet$1.425billioninimpairmentreversalsandgainsonsalein2017relatedtoitssuccessfulformationofnewjointoperationsattheVeladeromineandCerroCasaleproject.Thiswaspartiallyoffsetbynetimpairmentchargesof$511millionnetoftaxandnon-controllinginterestmainlyrelatingtoimpairmentchargesatAcacia’sBulyanhulumineandthePascua-Lamaproject,coupledwithanimpairmentreversalatLumwana,comparedtonetearningsof$655millionin2016.Adjustednetearningswere$876million,comparedtoadjustednetearningsof$818millionin2016(foranexplanationofadjustednetearnings,see“Non-GAAPFinancialMeasures–AdjustedNetEarningsandAdjustedNetEarningsperShare”).Thesignificantadjustingitems(pre-taxandnon-controllinginteresteffects)in2017include:$718milliongainrelatingtothesaleofa50%interestintheVeladeromine;$193milliongainrelatedtothesaleofa25%interestintheCerroCasaleproject;$212millionnetimpairmentcharges,primarilyonAcacia’sBulyanhulumineof$740millionandonthePascua-Lamaprojectof$407million,partiallyoffsetbyimpairmentreversalsasaresultoftheindicativefairvalueoftheCerroCasaleprojectrelatedtoBarrick’sdivestmentof25%of$1.12billionandonLumwanaof$259million;partiallyoffsetby$244millionsignificanttaxadjustmentsprimarilyrelatingtodividendwithholdingtaxexpenseandataxprovisionrelatingtotheimpactoftheproposedframeworkforAcaciaoperationsinTanzania,partiallyoffsetbytheanticipatedimpactoftheU.Staxreform;$178millionotherexpenseadjustments,mainlyrelatingtolossesondebtextinguishmentandreducedoperationsprogramcostsatAcacia’sBulyanhulu

-18-

mine;and$72millionforeigncurrencytranslationlosses,primarilyrelatedtothedevaluationoftheArgentineanpesoonVATreceivables.

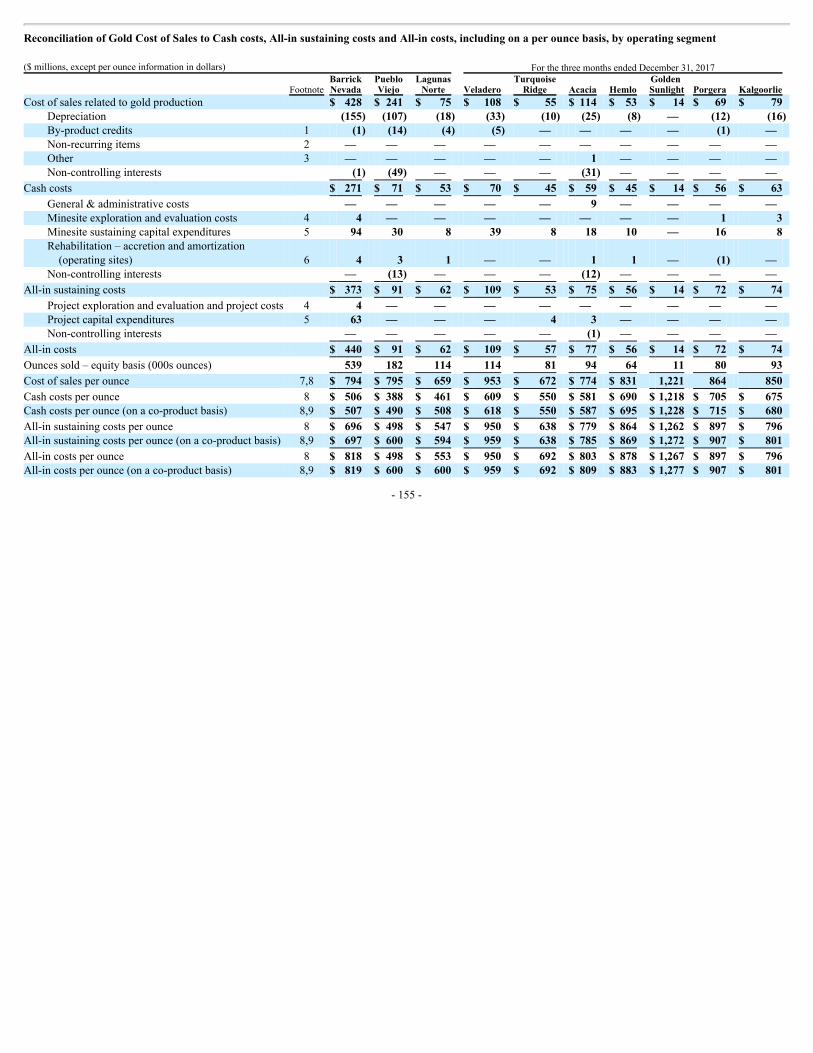

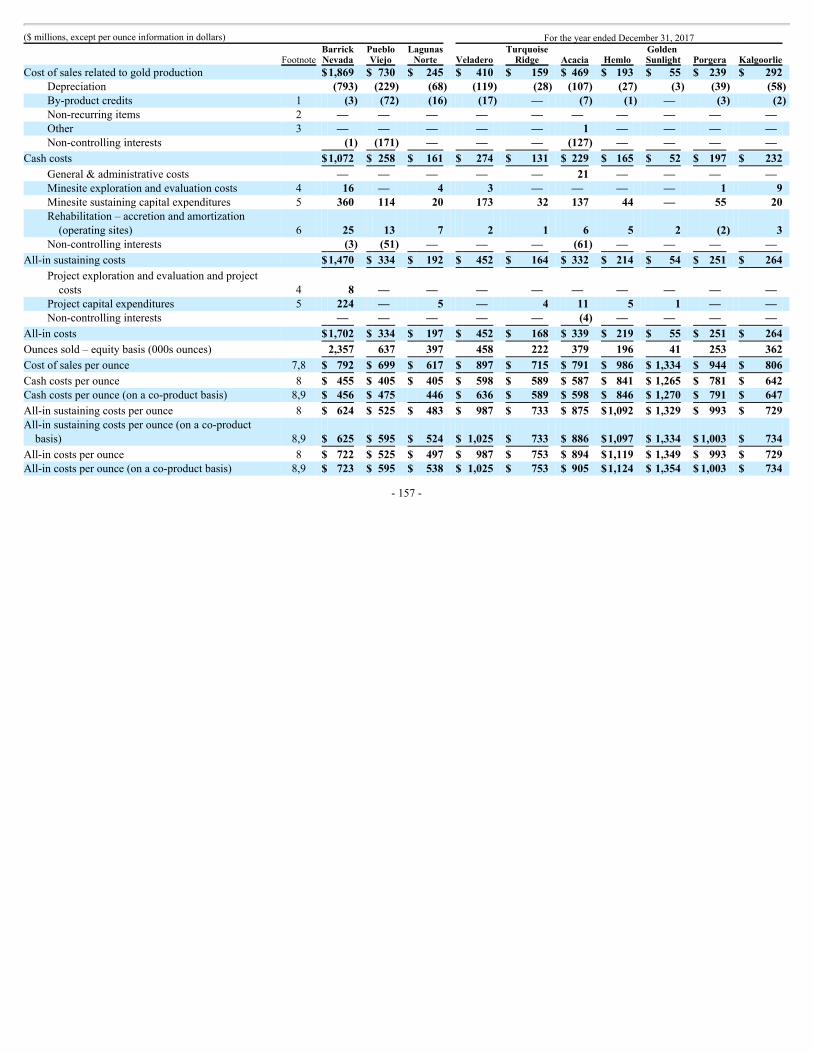

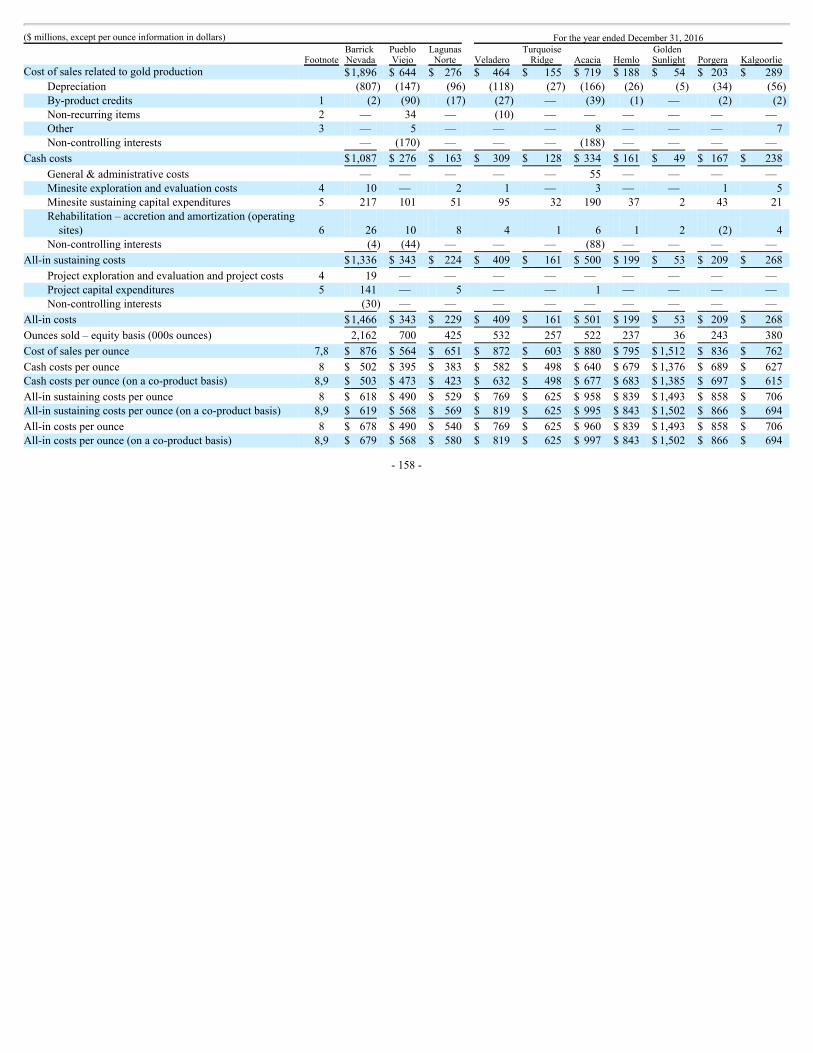

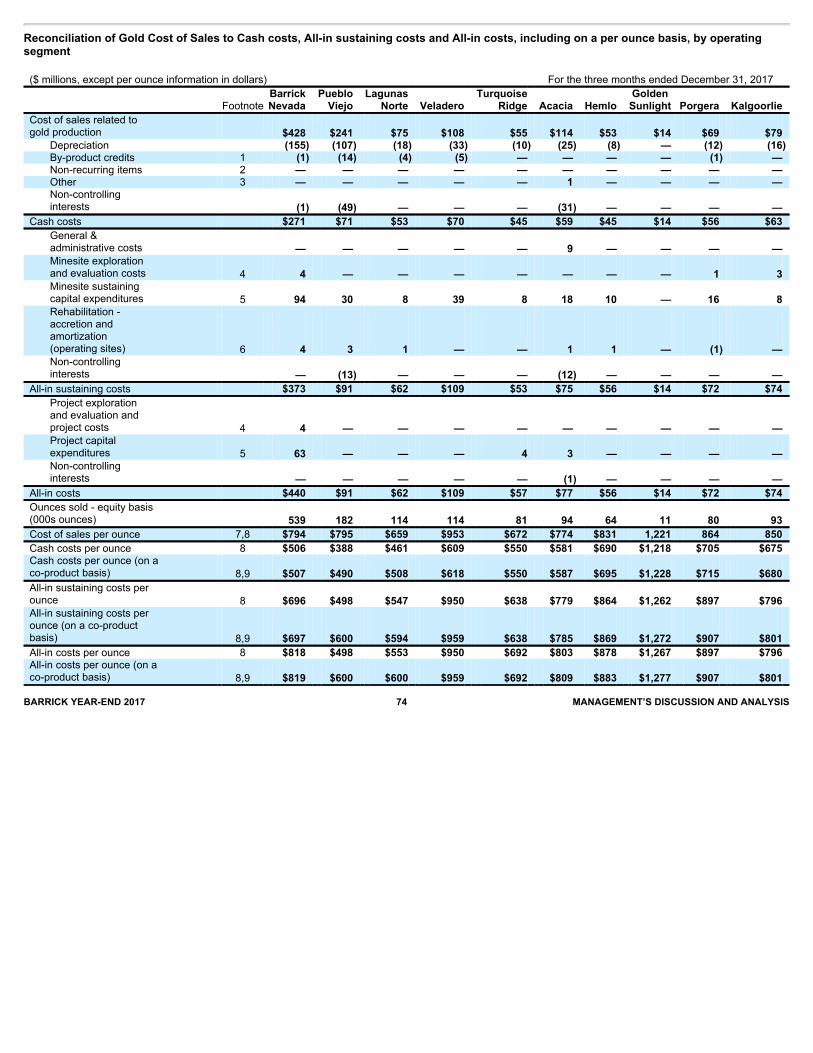

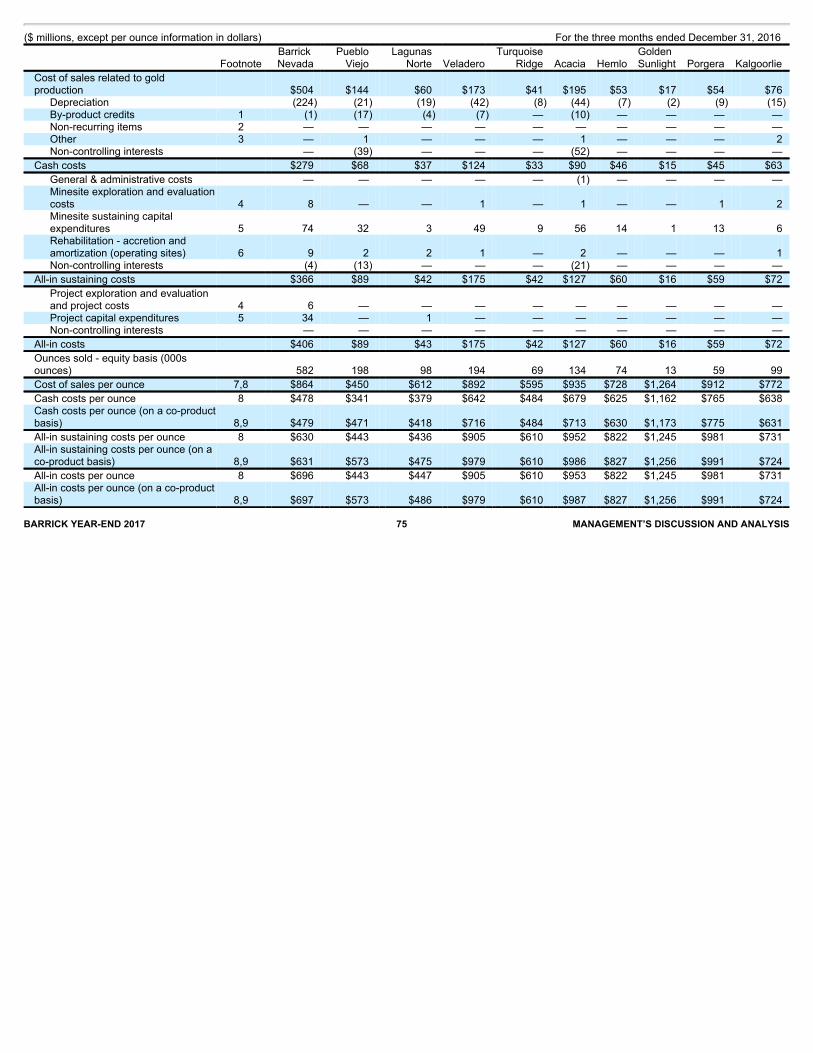

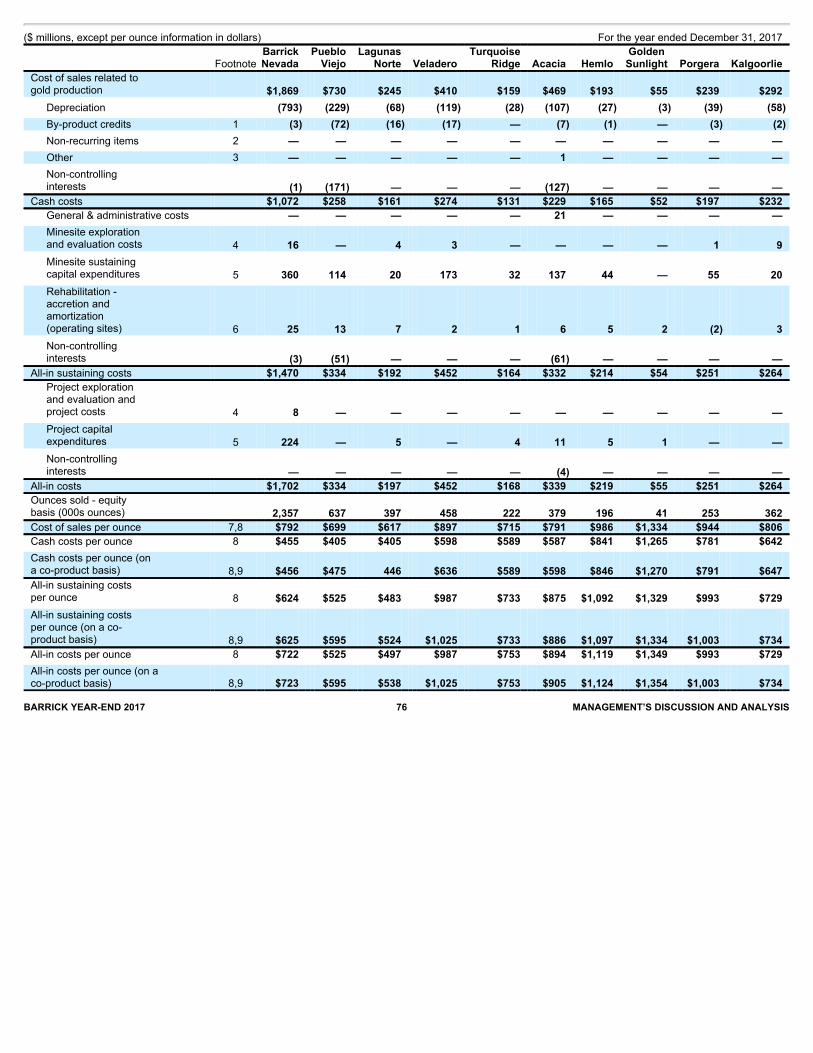

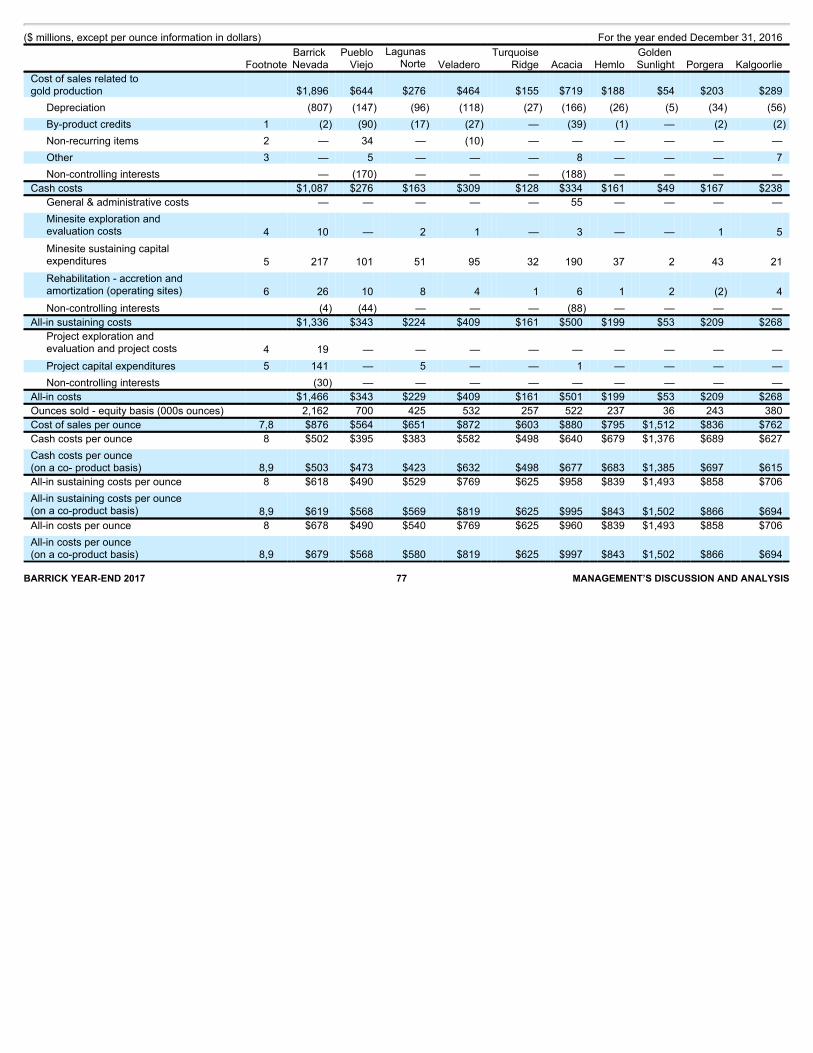

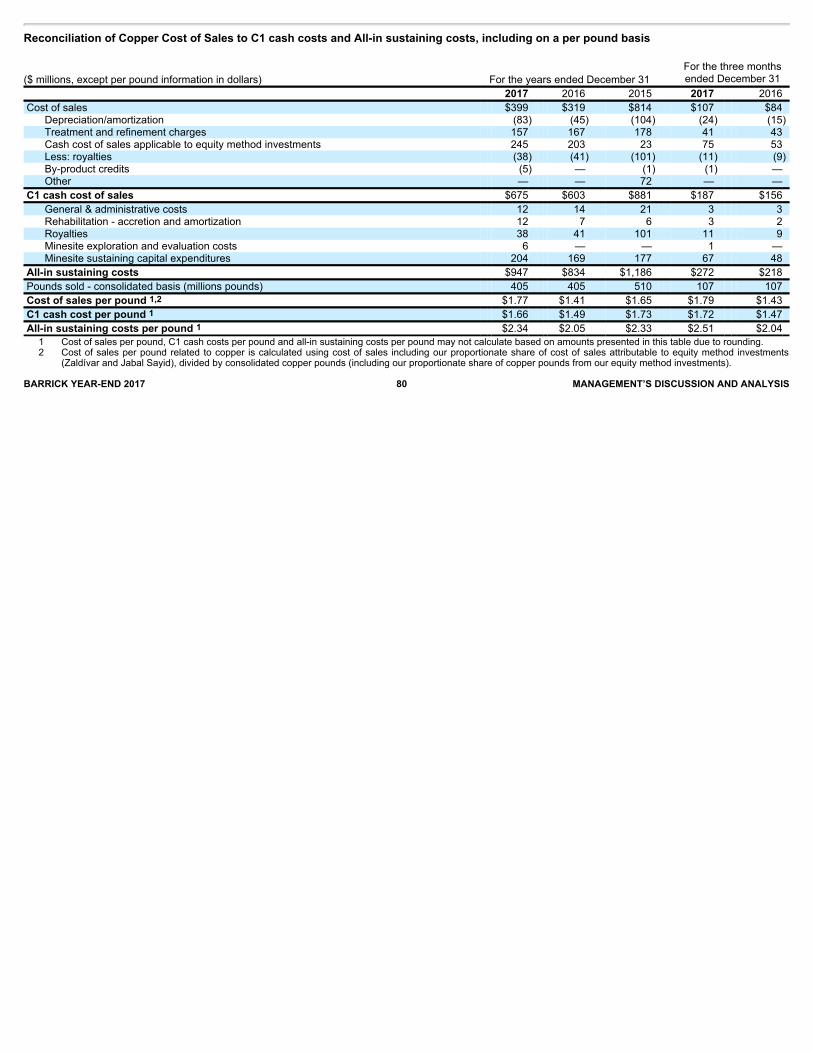

In2017,Barrick’sgoldproductionwas5.3millionounces,4%lowerthan2016goldproduction,withcostsofsalesapplicabletogoldof$794perounce,all-insustainingcostsof$750perounceandcashcostsof$526perounce.Barrick’scopperproductionin2017was413millionpoundsofcopper,inlinewith2016copperproduction,withcostofsalesapplicabletocopperof$1.77perpound,all-insustainingcostsof$2.34perpoundandC1cashcostsof$1.66perpound.In2016,Barrickproduced5.52millionouncesofgold,withcostsofsalesapplicabletogoldof$798perounce,all-insustainingcostsof$730perounceandcashcostsof$546perounce,and415millionpoundsofcopper,withcostofsalesapplicabletocopperof$1.41perpound,all-insustainingcostsof$2.05perpoundandC1cashcostsof$1.49perpound.“All-insustainingcosts”and“Cashcosts”perounceand“All-insustainingcosts”and“C1cashcosts”perpoundarenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsperounce,cashcostsperounce,all-insustainingcostsperpoundandC1cashcostsperpound,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

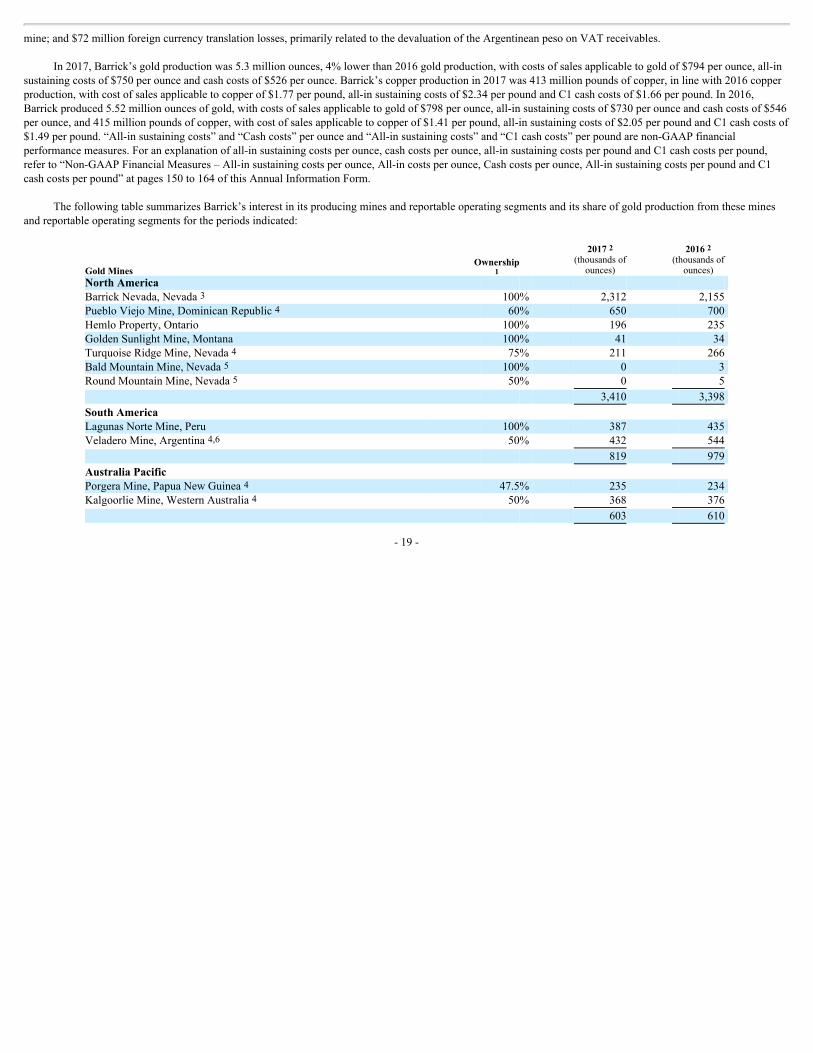

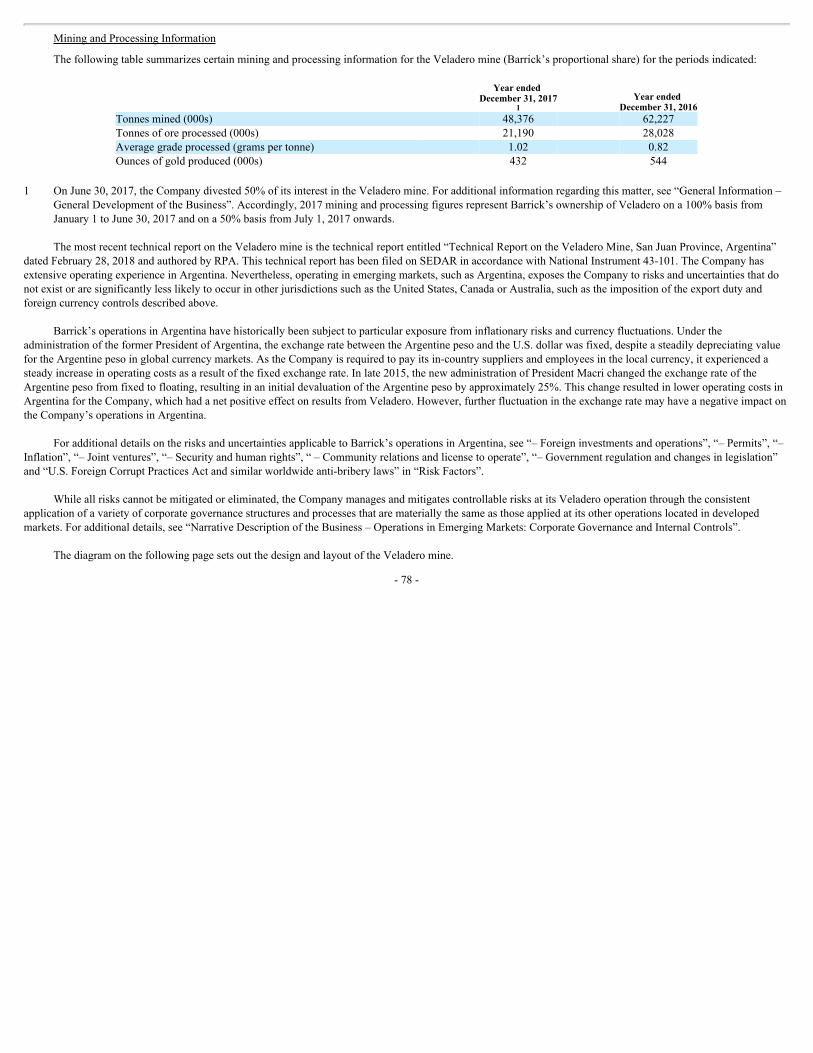

ThefollowingtablesummarizesBarrick’sinterestinitsproducingminesandreportableoperatingsegmentsanditsshareofgoldproductionfromtheseminesandreportableoperatingsegmentsfortheperiodsindicated:

GoldMines Ownership

1

20172(thousandsof

ounces)

20162(thousandsof

ounces) NorthAmerica BarrickNevada,Nevada3 100% 2,312 2,155PuebloViejoMine,DominicanRepublic4 60% 650 700HemloProperty,Ontario 100% 196 235GoldenSunlightMine,Montana 100% 41 34TurquoiseRidgeMine,Nevada4 75% 211 266BaldMountainMine,Nevada5 100% 0 3RoundMountainMine,Nevada5 50% 0 5

3,410 3,398

SouthAmerica LagunasNorteMine,Peru 100% 387 435VeladeroMine,Argentina4,6 50% 432 544

819 979

AustraliaPacific PorgeraMine,PapuaNewGuinea4 47.5% 235 234KalgoorlieMine,WesternAustralia4 50% 368 376

603 610

-19-

GoldMines Ownership

1

20172(thousandsof

ounces)

20162(thousandsof

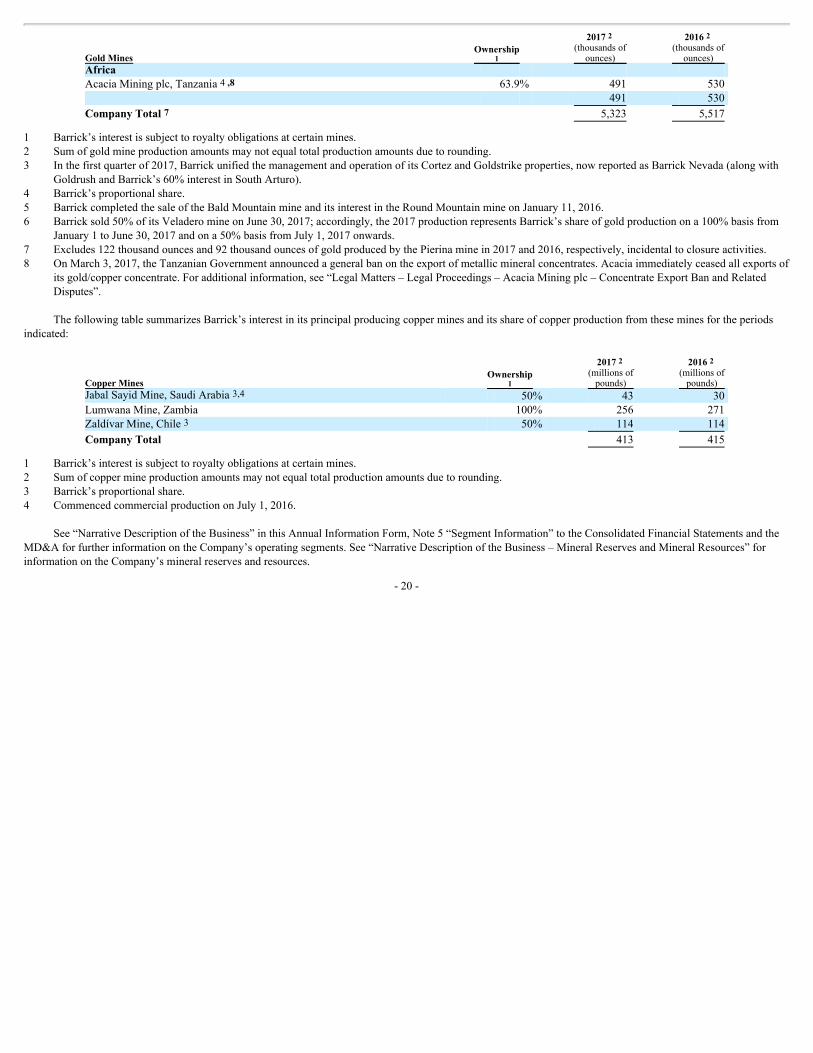

ounces) Africa AcaciaMiningplc,Tanzania4,8 63.9% 491 530

491 530

CompanyTotal7 5,323 5,517

1 Barrick’sinterestissubjecttoroyaltyobligationsatcertainmines.2 Sumofgoldmineproductionamountsmaynotequaltotalproductionamountsduetorounding.3 Inthefirstquarterof2017,BarrickunifiedthemanagementandoperationofitsCortezandGoldstrikeproperties,nowreportedasBarrickNevada(alongwith

GoldrushandBarrick’s60%interestinSouthArturo).4 Barrick’sproportionalshare.5 BarrickcompletedthesaleoftheBaldMountainmineanditsinterestintheRoundMountainmineonJanuary11,2016.6 Barricksold50%ofitsVeladeromineonJune30,2017;accordingly,the2017productionrepresentsBarrick’sshareofgoldproductionona100%basisfrom

January1toJune30,2017andona50%basisfromJuly1,2017onwards.7 Excludes122thousandouncesand92thousandouncesofgoldproducedbythePierinaminein2017and2016,respectively,incidentaltoclosureactivities.8 OnMarch3,2017,theTanzanianGovernmentannouncedageneralbanontheexportofmetallicmineralconcentrates.Acaciaimmediatelyceasedallexportsof

itsgold/copperconcentrate.Foradditionalinformation,see“LegalMatters–LegalProceedings–AcaciaMiningplc–ConcentrateExportBanandRelatedDisputes”.

ThefollowingtablesummarizesBarrick’sinterestinitsprincipalproducingcopperminesanditsshareofcopperproductionfromtheseminesfortheperiodsindicated:

CopperMines Ownership

1

20172(millionsofpounds)

20162(millionsofpounds)

JabalSayidMine,SaudiArabia3,4 50% 43 30LumwanaMine,Zambia 100% 256 271ZaldívarMine,Chile3 50% 114 114

CompanyTotal 413 415

1 Barrick’sinterestissubjecttoroyaltyobligationsatcertainmines.2 Sumofcoppermineproductionamountsmaynotequaltotalproductionamountsduetorounding.3 Barrick’sproportionalshare.4 CommencedcommercialproductiononJuly1,2016.

See“NarrativeDescriptionoftheBusiness”inthisAnnualInformationForm,Note5“SegmentInformation”totheConsolidatedFinancialStatementsandtheMD&AforfurtherinformationontheCompany’soperatingsegments.See“NarrativeDescriptionoftheBusiness–MineralReservesandMineralResources”forinformationontheCompany’smineralreservesandresources.

-20-

-21-

NARRATIVEDESCRIPTIONOFTHEBUSINESS

Barrickisengagedintheproductionandsaleofgold,aswellasrelatedactivitiessuchasexplorationandminedevelopment.Barrickalsoproducessignificantamountsofcopper,principallyfromitsZaldívarjointventure,JabalSayidjointventureanditsLumwanamineandholdsotherinterests.Unlessotherwisespecified,thedescriptionofBarrick’sbusiness,includingproducts,principalmarkets,distributionmethods,employeesandlaborrelationscontainedinthisAnnualInformationForm,appliestoeachofitsoperatingsegmentsandBarrickasawhole.

Production

FortheyearendedDecember31,2017,Barrickproduced5.3millionouncesofgoldatcostofsalesapplicabletogoldof$794perounce,all-insustainingcostsof$750perounceandcashcostsof$526perounce.Barrick’s2018goldproductionistargetedat4.5to5.0millionounces.Barrickexpectsaveragecostofsalesapplicabletogoldof$810to$850perouncein2018,all-insustainingcostsof$765to$815perounceandcashcostsof$540to$575perounce,assumingamarketgoldpriceof$1,200perounce,amarketoilpriceof$55perbarrelandanAustraliandollarexchangerateof$1:A$0.75.See“Forward-LookingInformation”.TheCompany’s2018goldproductionisexpectedtobelowerthan2017asaresultofproductiondecreasesatBarrickNevada,PuebloViejoandVeladero.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

FortheyearendedDecember31,2017,Barrickproduced413millionpoundsofcopperatcostofsalesapplicabletocopperof$1.77perpound,all-insustainingcostsof$2.34perpoundandC1cashcostsof$1.66perpound.Barrick’s2018copperproductionistargetedatapproximately385to450millionpoundsatexpectedcostofsalesapplicabletocopperof$1.80to$2.10perpound,all-insustainingcostsofapproximately$2.30to$2.60perpoundandC1cashcostsofapproximately$1.55to$1.75perpound,assumingamarketoilpriceof$55perbarrelandaChileanpesoexchangerateof650:$1.See“Forward-LookingInformation”.“All-insustainingcosts”and“C1cashcosts”perpoundarenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandC1cashcostsperpound,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

ReportableOperatingSegments

Barrick’sbusinessisorganizedintoelevenindividualminesites,BarrickNevada,onepubliclytradedcompany(Acacia)andoneproject(Pascua-Lama).Barrick’sChiefOperatingDecisionMaker,thePresident,reviewstheoperatingresults,assessesperformanceandmakescapitalallocationdecisionsattheminesite,grouping,Companyand/orprojectlevel,withtheexceptionofBarrick’s63.9%equityinterestinAcacia,whichisreviewedandassessedasaseparatebusiness.Therefore,eachindividualminesite,withtheexceptionofBarrickNevada,AcaciaandthePascua-Lamaproject,isanoperatingsegmentforfinancialreportingpurposes.

BarrickhasbeenpursuingstepchangesinperformanceinNevadabyfullyintegratingtheCortezandGoldstrikeoperations.Overthepastthreeyears,thesemineshavebenefitedfromincreasedcollaborationandadditionalsynergies,includingjointproductionplanningtooptimizeoreprocessing.Byfullyintegratingthemanagementoftheirassets,infrastructure,andexpertise,Barrickexpectstofurtheraccelerateimprovementsinefficiencyandproductivity.Asaresultofthesechanges,inthefirstquarter

-22-

of2017,BarrickunifiedthemanagementandoperationofitsCortezandGoldstrikeproperties,nowreferredtoasBarrickNevada.

SetoutbelowisabriefdescriptionofBarrick’supdatedreportableoperatingsegments,consistingoffourindividualgoldmines,BarrickNevada,Acaciaandoneproject.EachmineandprojectreceivesdirectionfromBarrick’sheadoffice,buthasresponsibilityforcertainaspectsofitsbusiness,suchassustainabilityofminingoperations,includingexploration,productionandclosure.AcaciahasagreateramountofindependenceincomparisontoBarrick’sotheroperatingsegments,asfurtherdescribedbelow.

Fordetailsregarding2017productionforalloperatingsegments,see“GeneralInformation–GeneralDevelopmentoftheBusiness”.Foradditionaldetailsregardingthereservesandresourcesheldineachoperatingsegment,see“–MineralReservesandMineralResources”.SeealsoNote5“SegmentInformation”totheConsolidatedFinancialStatementsandtheMD&AforfurtherfinancialandotherinformationontheCompany’soperatingsegments.Barrick’sabilitytodeliveronitsvision,strategicobjectivesandoperatingguidancedependsontheCompany’sabilitytounderstandandappropriatelyrespondtouncertaintiesandrisks.Foradescriptionofcertainofthosesourcesofuncertainty,relevantriskmodificationactivitiesandoversightbytheCompany’sBoardofDirectorsandexecutiveofficers,seepages35to38oftheMD&A.Foradiscussionofmaterialrisksrelevanttoinvestors,see“RiskFactors”.

Barrick Nevada

Inthefirstquarterof2017,BarrickunifiedthemanagementandtheoperationofitsCortezandGoldstrikeproperties,which,togetherwiththeGoldrushpropertyandtheCompany’s60%interestintheSouthArturoproperty,arenowreferredtoasBarrickNevada.However,eachofCortezandGoldstrikecontinuetobematerialpropertiesforthepurposesofthisAnnualInformationForm.

BarrickNevadaproducedapproximately2.3millionouncesofgoldatcostofsalesattributabletogoldof$792perounce,all-insustainingcostsof$624perounceandcashcostsof$455perouncein2017,comparedtoapproximately2.2millionouncesofgoldatcostofsalesattributabletogoldof$876perounce,all-insustainingcostsof$618perounceandcashcostsof$502perouncein2016.In2017,productionwaspositivelyimpactedbyhighergradesminedandprocessedfromCortezHillsopenpit(“CHOP”),coupledwithhigherthroughputattheoxidemillasaresultofBest-in-Classprocessimprovementsandanincreasedpermitlimit.Theseimprovementsresultedinthehighestannualthroughputleveleverachievedattheoxidemill.ThiswaspartiallyoffsetbylowerGoldstrikeopenpitstockpilegradesavailableforprocessingattheroastercomparedtohigherstockpilegradesintheprioryear,fewerGoldstrikeundergroundouncesprocessedduetoadecreaseinlong-holestopingandavailablestopestomine,andfewerleachtonnesminedandplacedinthecurrentyearatCortez.LowergradesatCortezHillsunderground(“CHUG”)asitadvancesdeeperintotheminewerepartiallyoffsetbyhigherminingratesasaresultofdigitizationinitiativessuchasshortintervalcontrolandautomation.AtBarrickNevada,theCompanyexpects2018goldproductiontobeintherangeof2.0to2.255millionounces.LowerproductionisexpectedatCHOPandCHUG.AtCHOP,miningwilltransitionfrompurelyoxideoretoamixofoxide,refractoryandtransitionalores.GrademinedfromCHUGisexpectedtobelowerasprogressionismadedeeperintothemine.Thisispartiallyoffsetbyincreasedthroughputattheoxidemill,increasedgradesatGoldstrikeopenpitfromprocessingthethirdnorthwestlaybackcomparedtostockpileprocessingintheprioryearandhighergradesatGoldstrikeunderground.Throughputinitiativesattheautoclaveareexpectedtomorethanoffsetlowerautoclaverecoveryasthetransitionprimarilyfromanallacidblendtoanalkaline/acidblendoccurs.In2018,theCompanyexpectscostofsalesattributabletogoldtobeintherangeof$760to$810perounce,whichisconsistentwith2017.All-insustainingcostsareexpectedtobeintherangeof$610to$660perounce,consistentwith2017,aslowerproductionisoffsetbylowersustainingcapitalexpendituresfortailingsexpansions,processimprovementsand

-23-

Goldstrikeundergroundprojectstoenableminingdeeperinthemine.Cashcostsareexpectedtobeintherangeof$470to$530perounce,anincreasefrom2017.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

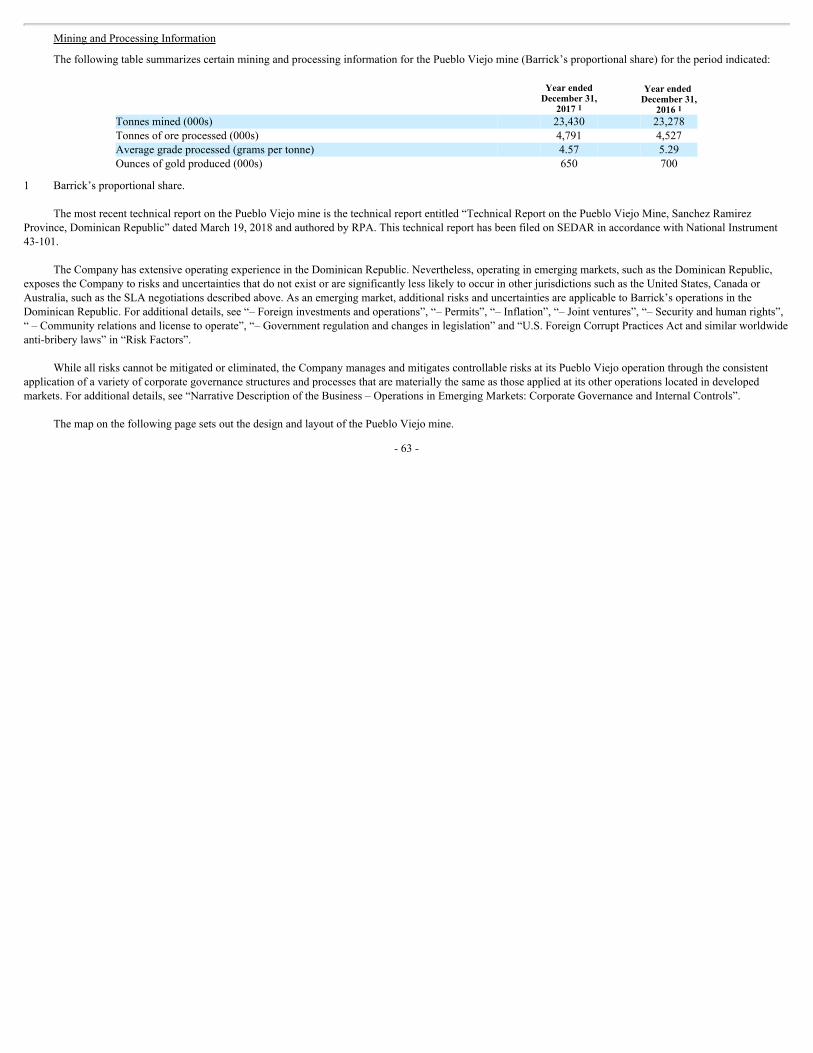

Pueblo Viejo (60% basis)

Barrick’s60%interestinthePuebloViejomine(amaterialpropertyforthepurposesofthisAnnualInformationForm,see“MaterialProperties–PuebloViejoMine”)producedapproximately650thousandouncesofgoldatcostofsalesattributabletogoldof$699perounce,all-insustainingcostsof$525perounceandcashcostsof$405perouncein2017,comparedtoapproximately700thousandouncesofgoldatcostofsalesattributabletogoldof$564perounce,all-insustainingcostsof$490perounceandcashcostsof$395perouncein2016.Barrickistheoperatorofthejointventure.In2017,costofsalesattributabletogoldwasnegativelyimpactedbytheeffectoflowersalesvolumeonunitproductioncosts,combinedwithhigherdepreciationexpenserelatingtoatailingsstoragefacilitydepreciationadjustmentandhigherfuelprices.AtPuebloViejo,theCompanyexpectsitsequityshareof2018goldproductiontobeintherangeof585to615thousandounces,below2017productionlevels,drivenbyreducedgoldheadgrade,partiallyoffsetbyincreasedautoclavethroughputresultingfromimprovedmaintenancestrategiesandsmall-scalepre-oxidationandflotationconcentratepre-processingexpansions.In2018,Barrickexpectscostofsalesattributabletogoldtobeintherangeof$720to$750perounce.All-insustainingcostsareexpectedtobe$590to$620perounceandcashcostsareexpectedtobeintherangeof$425to$450perounce.Costofsalesattributabletogold,all-insustainingcostsandcashcostsareexpectedtobehigherthanin2017primarilyduetoareductionintotalouncesproducedandsold,higherfuelpricesandhighersustainingcapitalexpendituresrelatedmainlytoincreasedcapitalizedwastestripping,tailingsdamconstruction,QuisqueyapowerstationgasconversionandBonaosub-stationconstructioncapitalprojects.Byproductcreditsareexpectedtobehigherthanin2017,reflectingincreasedmetalprices,oregradesandrecoveriesforbothsilverandcopper.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

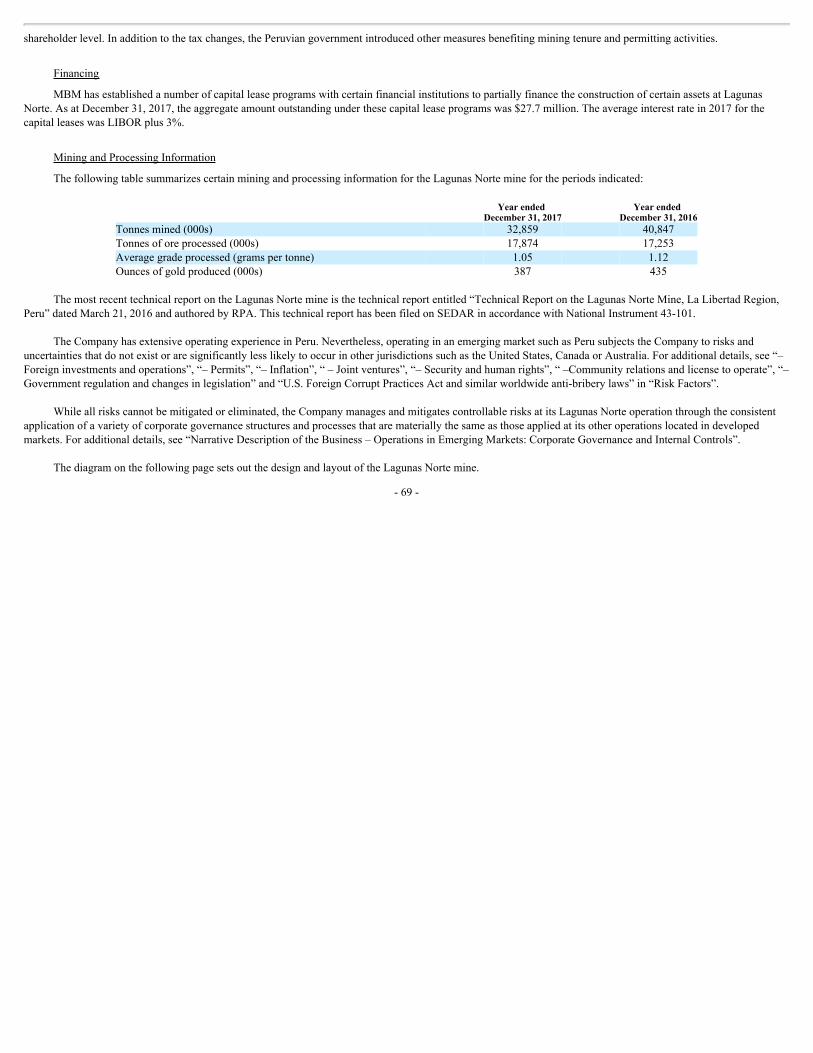

Lagunas Norte

Barrick’sLagunasNortemine(amaterialpropertyforpurposesofthisAnnualInformationForm,see“MaterialProperties–LagunasNorteMine”)producedapproximately387thousandouncesofgoldatcostofsalesattributabletogoldof$617perounce,all-insustainingcostsof$483perounceandcashcostsof$405perouncein2017,comparedtoapproximately435thousandouncesofgoldatcostofsalesattributabletogoldof$651perounce,all-insustainingcostsof$529perounceandcashcostsof$383perouncein2016.Thelowercostofsalesattributabletogoldin2017wasmainlyduetolowerdepreciationexpenseandrealizedcostsavingsfromtheBest-in-Classprogram,suchasinitiativestoimproveefficienciesinthecarbon-in-columncircuit,implementationofshortintervalcontrolandimprovementsinplannedmaintenance.Thesewerepartiallyoffsetbytheimpactoflowersalesvolumeandhigherdirectminingcosts,resultingfromlowercapitalizedwastestrippingandhigherprocessingcostsdrivenbyhighertonnageprocessedandincreasedsuppliesconsumptiongiventhetreatmentofdifferentoretypesinthemineplan.AtLagunasNorte,theCompanyexpects2018productiontobeintherangeof230to270thousandounces,lowerthan2017productionlevels,asaresultoftheprogressivedepletionofoxideores,whicharebeingreplacedwithharderorematerialwithlowerkineticsandrecoveries.In2018,theCompanyexpectscostofsalesattributabletogoldtobeintherangeof$780to

-24-

$910perounce,mainlydrivenbytheimpactoflowergoldsalescombinedwithanincreaseindepreciationexpenseandhighercorporatesocialresponsibilityexpenses.All-insustainingcostsareexpectedtobe$670to$780perounceandcashcostsareexpectedtobeintherangeof$420to$490perounce.Theincreaseinall-insustainingcostsisdrivenmainlybythedecreaseinproductionandincreaseinsustainingcapitalexpendituresin2018.Operationalcostsareexpectedtodecrease,alignedtothereducedmineproductionplan,comparedto2017.Best-in-Classoperationalinitiativesfor2018willbefocusedongettinggoldouncesfrominjectionwellsandslagprocessing.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

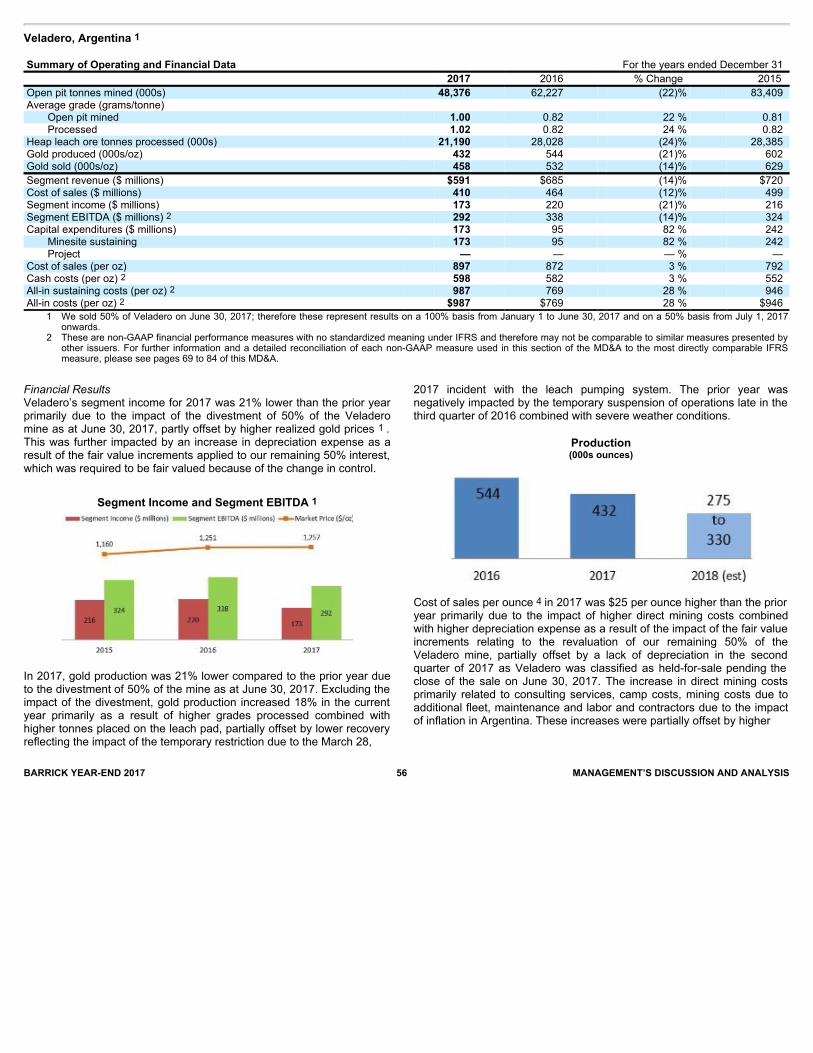

Veladero

Barrick’s100%interestintheVeladeromine(amaterialpropertyforpurposesofthisAnnualInformationForm,see“MaterialProperties–VeladeroMine”)fromJanuary1toJune30,2017and50%interestintheVeladerominefromJuly1,2017onwards(reflectingBarrick’sdivestmentof50%ofitsinterestintheVeladeromineonJune30,2017)producedapproximately432thousandouncesofgoldatcostofsalesattributabletogoldof$897perounce,all-insustainingcostsof$987perounceandcashcostsof$598perouncein2017,comparedtoapproximately544thousandouncesofgoldatcostofsalesattributabletogoldof$872perounce,all-insustainingcostsof$769perounceandcashcostsof$582perouncein2016whenBarrickhelda100%interestintheminethroughouttheyear.See“GeneralInformation–GeneralDevelopmentoftheBusiness”.Thehighercostofsalesattributabletogoldin2017wasprimarilyduetotheimpactofhigherdirectminingcostscombinedwithhigherdepreciationexpenseasaresultoftheimpactofthefairvalueincrementsrelatingtotherevaluationofBarrick’sremaining50%interestintheVeladeromine,partiallyoffsetbyalackofdepreciationinthesecondquarterof2017asVeladerowasclassifiedasheld-for-salependingthecloseofthesaleonJune30,2017.Theincreaseindirectminingcostsprimarilyrelatedtoconsultingservices,campcosts,miningcostsduetoadditionalfleet,maintenance,laborandcontractorsandduetotheimpactofinflationinArgentina.Theseincreaseswerepartiallyoffsetbyhighercapitalizedwastestrippingcostsinthecurrentyearastherewasnocapitalizedwastestrippinginthethirdquarterof2016asaresultofsevereweatherconditions.

OnSeptember13,2015,avalveonaleachpadpipelineattheVeladerominefailed,resultinginareleaseofcyanide-bearingprocesssolutionintoanearbywaterwaythroughadiversionchannelgatethatwasopenatthetimeoftheincident.InMarch2016,theProvincialminingauthorityimposedanadministrativefineagainstMineraArgentinaGoldSRL(“MAG”),theArgentinesubsidiarythatoperatestheVeladeromine,inconnectionwiththeincident.OnApril14,2016,inaccordancewithlocalrequirements,MAGpaidtheadministrativefineofapproximately$10million.Formoreinformationaboutthismatter,see“MaterialProperties–VeladeroMine”.

OnSeptember8,2016,icerollingdowntheslopeoftheleachpadattheVeladerominedamagedapipecarryingprocesssolution,causingsomematerialtoleavetheleachpad.Thismaterial,primarilycrushedoresaturatedwithprocesssolution,wascontainedontheminesiteandreturnedtotheleachpad.Formoreinformationaboutthismatter,see“MaterialProperties–VeladeroMine”.

OnMarch28,2017,themonitoringsystematVeladerodetectedaruptureofapipecarryinggold-bearingsolutionontheleachpad.Allsolutionwascontainedwithintheoperatingsiteandnosolutionreachedanydiversionchannelsorwatercourses.Asaresultofthisrupture,theGovernmentofSanJuantemporarilyrestrictedtheadditionofcyanidetotheVeladeromine’sheapleachfacilitypendingcompletionofcertainremedialworks.ThesuspensionwasliftedonJune15,2017.

-25-

OnDecember27,2017,theSanJuanminingauthorityassessedacombinedfineforthe2016and2017incidentsatVeladeroofapproximately$5.6million(calculatedattheprevailingexchangerateonDecember31,2017).OnJanuary23,2018,inaccordancewithlocalrequirements,MAGpaidtheadministrativefineandfiledarequestforreconsiderationwiththeSanJuanProvincialminingauthority,whichremainspending.

AtVeladero,theCompanyexpectsattributable2018productiontobeintherangeof275to330thousandounces,lowerthan2017productionlevels.Thedecreaseismainlytheresultofthedivestmentof50%oftheVeladeromineasatJune30,2017,combinedwithslightlyloweroregradetotheleachpadin2018,offsetbyongoingsolubleinventorydrawdownwithimprovedsolutionmanagement(see“MaterialProperties–VeladeroMine”).Barrickexpectscostofsalesattributabletogoldtobeintherangeof$970to$1,110perounce,mainlyduetohigherdepreciationexpensereflectingtheeffectofthefairvalueincrementsappliedtoBarrick’sremaining50%interestintheVeladeromine.All-insustainingcostsareexpectedtobe$960to$1,100perounce,alignedwith2017aslowercashcostsareoffsetbyhighercapitalizedwastestripping.Cashcostsin2018areexpectedtobeintherangeof$560to$620perounce,lowerthan2017levelsmainlyduetolowerdirectoperatingcosts,partlyoffsetbytheimpactofhigherchargesfromtheproductioninventorymovements.OperatingcostsatVeladeroarealsohighlysensitivetolocalinflationandfluctuationsinforeignexchangerates.TheCompanyhasassumedanaverageARSexchangerateofARS18.3:$1andalocalinflationrateof15%forpurposesofpreparingitscashcostandall-insustainingcostguidancefor2018.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

Thegovernance,ownershipandjointoperationoftheVeladerojointventureisgovernedbythetermsofashareholders’agreementbetweenBarrickandShandong(the“VeladeroShareholders’Agreement”).Forfurtherdetails,referto“MaterialProperties–VeladeroMine–GeneralInformation–History”.

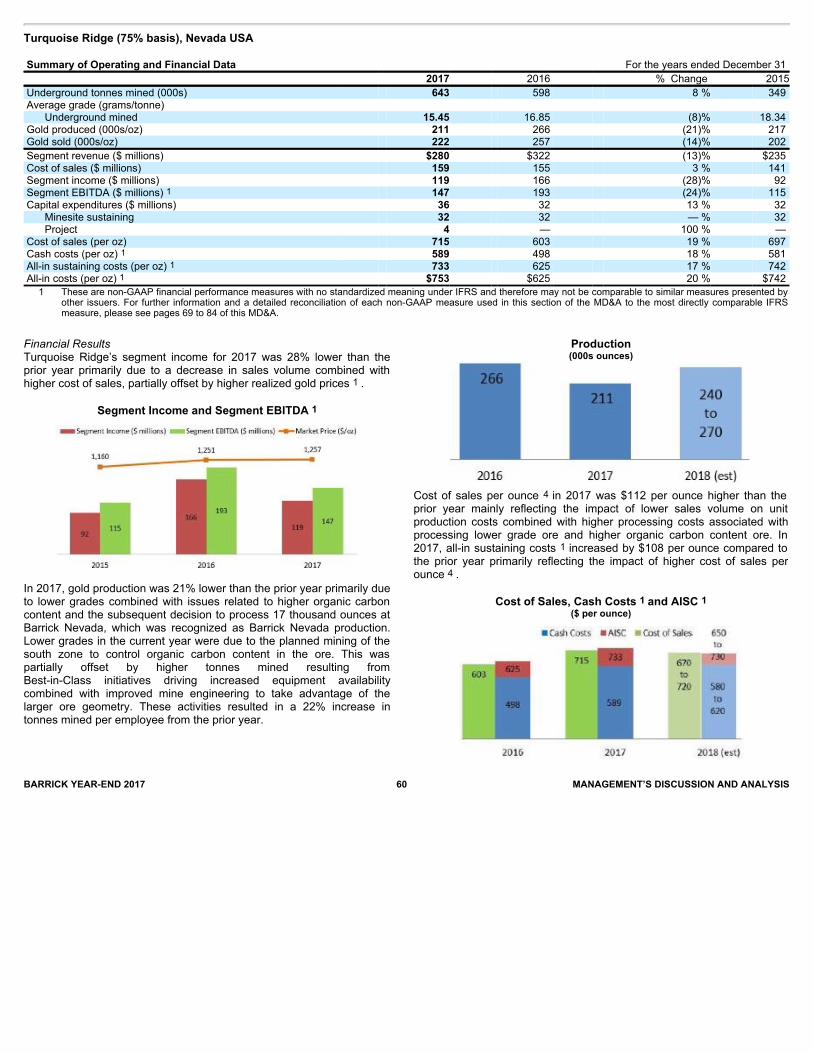

Turquoise Ridge (75% basis)

TurquoiseRidge(amaterialpropertyforpurposesofthisAnnualInformationForm,see“MaterialProperties–TurquoiseRidgeMine”)isanundergroundminethatusesunderhanddrift-and-fillminingmethods.Barrickistheoperatorofthejointventure.Barrick’s75%interestintheTurquoiseRidgemineproducedapproximately211thousandouncesofgoldatcostofsalesattributabletogoldof$715perounce,all-insustainingcostsof$733perounceandcashcostsof$589perouncein2017,comparedtoapproximately266thousandouncesofgoldatcostofsalesattributabletogoldof$603perounce,all-insustainingcostsof$625perounceandcashcostsof$498perouncein2016.Thehighercostofsalesattributabletogoldin2017mainlyreflectedtheimpactoflowersalesvolumeonunitproductioncostscombinedwithhigherprocessingcostsassociatedwithprocessinglowergradeoreandhigherorganiccarboncontentore.AtTurquoiseRidge,theCompanyexpectsattributable2018productiontobeintherangeof240to270thousandounces,whichishigherthan2017productionlevels.TurquoiseRidgehascompletelytransitionedtostandardizedequipmentallowingforgreaterminingflexibilitywithhigherreliabilityandlessequipment.Capitalandwastedevelopmentrequirementsareinlinewith2017miningrates.Costofsalesattributabletogoldareexpectedtobeintherangeof$670to$720perouncewhichisin-linewith2017.All-insustainingcostsin2018areexpectedtobeintherangeof$650to$730perounce.All-insustainingcostsin2018areexpectedtobelowerthan2017duetoareductioninsustainingcapitalastheconstructionofthethirdshaftisincludedinprojectcapital.Cashcostsin2018areexpectedtobeintherangeof$580to$620perounce,consistentwith2017.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsper

-26-

ounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

BarrickcontinuestoadvanceaphasedapproachtoexpansionatTurquoiseRidgethatmaximizesfreecashflowfromtheoperation,whileoptimizingthetimingofcapitalspendingforexpansion.

InJanuary2018,BarrickandNewmontMiningCorporation(“Newmont”)reachedanagreementonanew,seven-yeartollmillingagreement(the“TMA”)fortheprocessingofTurquoiseRidgeoreatNewmont’sTwinCreeksfacility.TheTMAsupportsplanstoexpandproductionatTurquoiseRidgebyincreasingcontractualprocessingcapacity.Itprovidesforthroughputof850,000tonsperyearin2018and2019,risingto1.2milliontonsperyearbetween2020and2024.

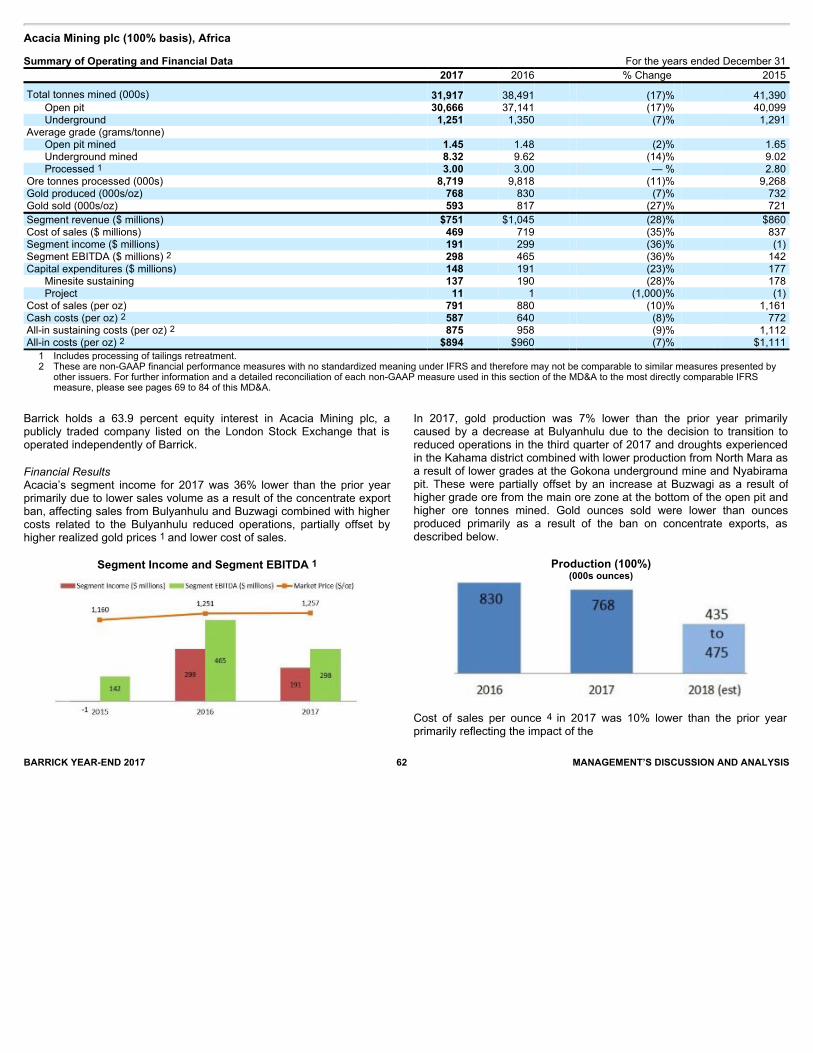

Acacia Mining plc (63.9% basis)

Acacia’soperationsconsistofitsBulyanhuluundergroundmine,itsNorthMaraopenpitandundergroundmineanditsBuzwagiopenpitmine,alllocatedinTanzania.Barrick’sequityinterestinAcaciais63.9%.Theassets,liabilities,operatingresultsandcashflowsofAcaciaareconsolidatedbyBarrick.Acacia’ssharesarelistedfortradingontheLondonStockExchange(“LSE”).In2017,Barrick’sequityinterestinAcacia’sgoldproductionwasapproximately491thousandouncesofgoldatcostofsalesattributabletogoldof$791perounce,all-insustainingcostsof$875perounceandcashcostsof$587perounce,comparedtoapproximately530thousandouncesofgoldatcostofsalesattributabletogoldof$880perounce,all-insustainingcostsof$958perounceandcashcostsof$640perouncein2016.Thisyear-over-yeardeclineinproductionwasdueinlargeparttotheconcentrateexportbanimplementedbytheTanzaniangovernmentonMarch3,2017,affectingsalesfromBulyanhuluandBuzwagiandleadingtoadecisiontotransitiontoreducedoperationsinthethirdquarterof2017,aswellasduetodroughtsexperiencedintheKahamadistrict,combinedwithlowerproductionfromNorthMaraasaresultoflowergradesattheGokonaundergroundmineandNyabiramapit.ThesewerepartiallyoffsetbyaproductionincreaseatBuzwagiasaresultofhighergradeorefromthemainorezoneatthebottomoftheopenpitandhigheroretonnesmined.TheCompanyexpectsAcacia’s2018goldproductiontobeintherangeof275to305thousandounces(Barrick’sshare),whichislowerthan2017productionlevels.Acacia’sproductionisexpectedtobelowerthan2017mainlyduetoBulyanhulu’stransitiontoreducedoperationsandtheplannedtransitionofBuzwagitoastockpileprocessingoperationin2018.In2018,Barrickexpectscostofsalesattributabletogoldtobeintherangeof$970to$1,020perounce.All-insustainingcostsareexpectedtobeintherangeof$935to$985perounceandcashcostsareexpectedtobeintherangeof$690to$720perounce.Theincreaseinallthreemeasuresfrom2017ismainlyduetothenegativeimpactofapproximately$50perounceduetoincreasedinventorycostsatBuzwagiasAcaciaprocessesorestockpilespreviouslyclassifiedasoreinventory.Formoreinformationaboutthismatter,see“LegalMatters–LegalProceedings–AcaciaMiningplc–ConcentrateExportBanandRelatedDisputes”.“All-insustainingcosts”and“cashcosts”perouncearenon-GAAPfinancialperformancemeasures.Foranexplanationofall-insustainingcostsandcashcostsperounce,referto“Non-GAAPFinancialMeasures–All-insustainingcostsperounce,All-incostsperounce,Cashcostsperounce,All-insustainingcostsperpoundandC1cashcostsperpound”atpages150to164ofthisAnnualInformationForm.

OnMarch3,2017,theTanzanianGovernmentannouncedageneralbanontheexportofmetallicmineralconcentrates(the“Ban”).FollowingitsimpositionoftheBan,Acaciaimmediatelyceasedallexportsofitsgold/copperconcentrate.WhileAcaciahasbeenlookingtoaddressallissuesinrespectoftheBanalongwithotherongoingdisputesthroughdialoguewiththeTanzanianGovernment,ithascommencedinternationalarbitrationinaccordancewithitsMineralDevelopmentAgreementswiththeGovernmentofTanzaniatoresolvethesematters.OnOctober19,2017,BarrickannouncedthatithadagreedwiththeGovernmentofTanzaniaonaproposedframeworkforanewpartnershipbetweenAcacia

-27-

andtheGovernmentofTanzania.SuchtermswouldbesubjecttoreviewandapprovalbyAcacia.Discussionsconcerningtheimplementationoftheproposedframework,resolutionofoutstandingtaxmattersrelatingtoAcacia,andtheliftingoftheBanremainongoing.Barrickistargetingthefirsthalfof2018forthecompletionofadetailedproposalforreviewbyAcacia.Foradditionalinformation,see“LegalMatters–LegalProceedings–AcaciaMiningplc–ConcentrateExportBanandRelatedDisputes”.

BarrickanditsaffiliatesprovidecertainservicestoAcaciaanditssubsidiariesfortheongoingoperationofAcacia’sbusinesspursuanttoaservicesagreemententeredintobytheparties.Inaddition,BarrickandAcaciaarealsopartiestoarelationshipagreementthatregulatesvariousaspectsoftheongoingrelationshipbetweenthetwocompanies.TheprincipalpurposeoftherelationshipagreementistoensurethatAcaciaiscapableofcarryingonitsbusinessindependentlyofBarrickandthatanytransactionsandrelationshipswithBarrickoccuratarm’slengthandundernormalcommercialterms.Underthatagreement,solongasBarrickmaintainsa40%equityinterestinAcacia,Barrickisentitledtoappointthegreaterof(i)threenon-executivedirectorstoAcacia’sboardofdirectors;and(ii)themaximumnumberofnon-executivedirectorsthatmaybeappointedtoAcacia’sboardofdirectors,whileensuringAcaciaiscompliantwiththeUKCombinedCodeofCorporateGovernance.IfBarrick’sshareholdinginAcaciafallsbelow40%,thereisaslidingscaleastothenumberofdirectorsitmayappoint.AsofMarch19,2018,Acaciahadsevendirectors,twoofwhichwereappointedbyBarrick.TherelationshipagreementwillremaininforceaslongasAcacia’ssharesarelistedontheLSEandBarrickmaintainsatleasta15%equityinterest.Therelationshipagreementcontainsanumberofothercommitmentsandrestrictions,includinganon-competitionclausepursuanttowhich(i)BarrickagreesitwillnotpursueanygoldorsilverminingprojectinAfrica,assuchtermsaredefinedintherelationshipagreement,and(ii)AcaciaagreesitwillnotpursueanygoldorsilverminingprojectoutsideofAfrica,assuchtermsaredefinedintherelationshipagreement.Thenon-competitionclauseissubjecttovariousexceptionsandonlyappliesforsolongasBarrickholdsatleasta30%equityinterestinAcacia.IfeitherBarrickorAcaciawantstopursueaprojectwhichissubjecttothenon-competitionrestriction(the“NotifyingParty”),theyarerequiredtonotifytheotherpartyand,iftheotherpartywaivestheopportunityorfailstorespondinatimelyfashion,theNotifyingPartywillbeentitledtopursuetheprojectdescribedinthenotice.

Barrick’sKabanganickelprojectandLumwanacopperminearenotincludedintheassetsheldbyAcacia.Barrickcontinuestodirectlyholdits50%interestintheKabangaproject,whichislocatedinTanzania.Barrickalsodirectlyholdsits100%interestintheLumwanamine,whichislocatedinZambia.

Pascua-Lama Project

ThePascua-Lamaproject,locatedontheborderbetweenChileandArgentina,contains21.3millionouncesofmeasuredandindicatedgoldresources(formoreinformationaboutthePascua-Lamaproject,see“ExplorationandEvaluations–Pascua-Lama”and“LegalMatters–LegalProceedings–Pascua-Lama–ConstitutionalProtectionAction”).

OnJanuary17,2018,Chile’sSuperintendenciadelMedioAmbiente(“SMA”)orderedtheclosureofexistinginfrastructureontheChileansideofthePascua-Lamaproject.Thesanctionispartofare-evaluationprocessorderbythecountry’sEnvironmentalCourtin2014andrelatestohistoricalcompliancematters.Barrickisappealingtheresolutiononanumberofgrounds,includingonthebasisthatthesanctionisdisproportionatetoactualenvironmentalimpacts.See“LegalMatters–LegalProceedings–Pascua-Lama–SMARegulatorySanctions”formoredetailregardingtheSMAregulatorysanctions.

-28-

TheSMAorderdoesnotaffecttheCompany’songoingevaluationofanundergroundmineatPascua-Lama,whichwouldrequireadditionalpermittingandregulatoryapprovalsinbothArgentinaandChile,irrespectiveoftherecentSMAdecision.Inanyundergroundscenario,BarrickwouldalsoclosesitefacilitiesandsurfacedisturbancesinChilenotnecessaryforanundergroundmine.Ashifttoanundergroundoperationwouldaddressanumberofcommunityconcernsbysignificantlyreducingtheoverallenvironmentalimpactsoftheproject,ascomparedtoanopenpitoperation.Inaddition,anundergroundoperationwouldbelesssusceptibletoweather-relatedproductionimpactsduringthewinterseason.

InlightoftheSMAordertoclosesurfacefacilitiesinChile,andcurrentplanstoevaluateanundergroundmine,BarrickreclassifiedPascua-Lama’sprovenandprobablegoldreservesofapproximately14millionouncesasmeasuredandindicatedresourcesasofyear-end2017.

ForadditionalinformationregardingBarrick’sprojects,see“ExplorationandEvaluations”.

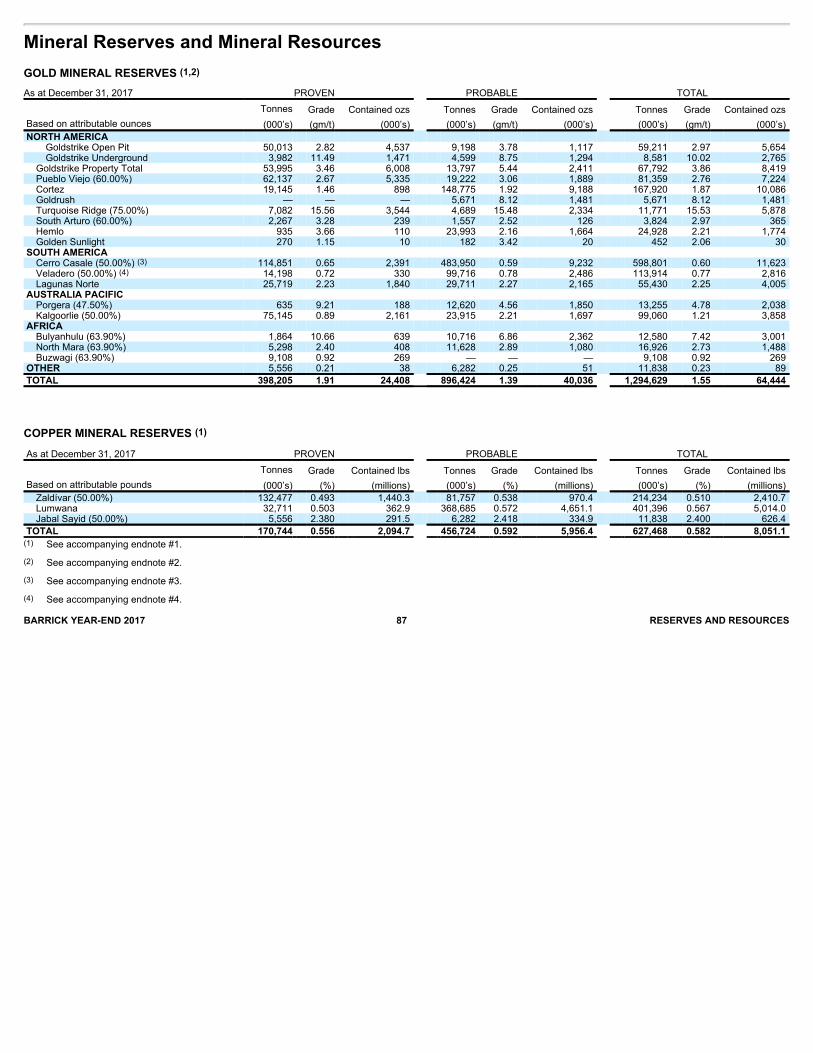

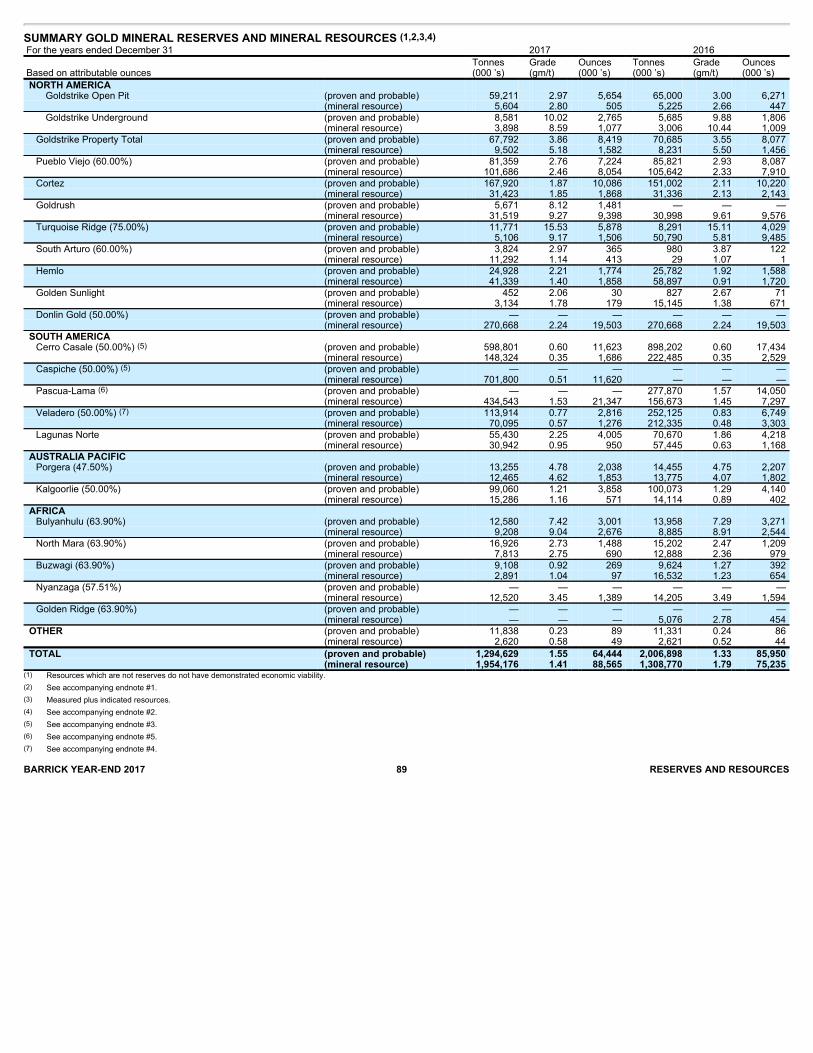

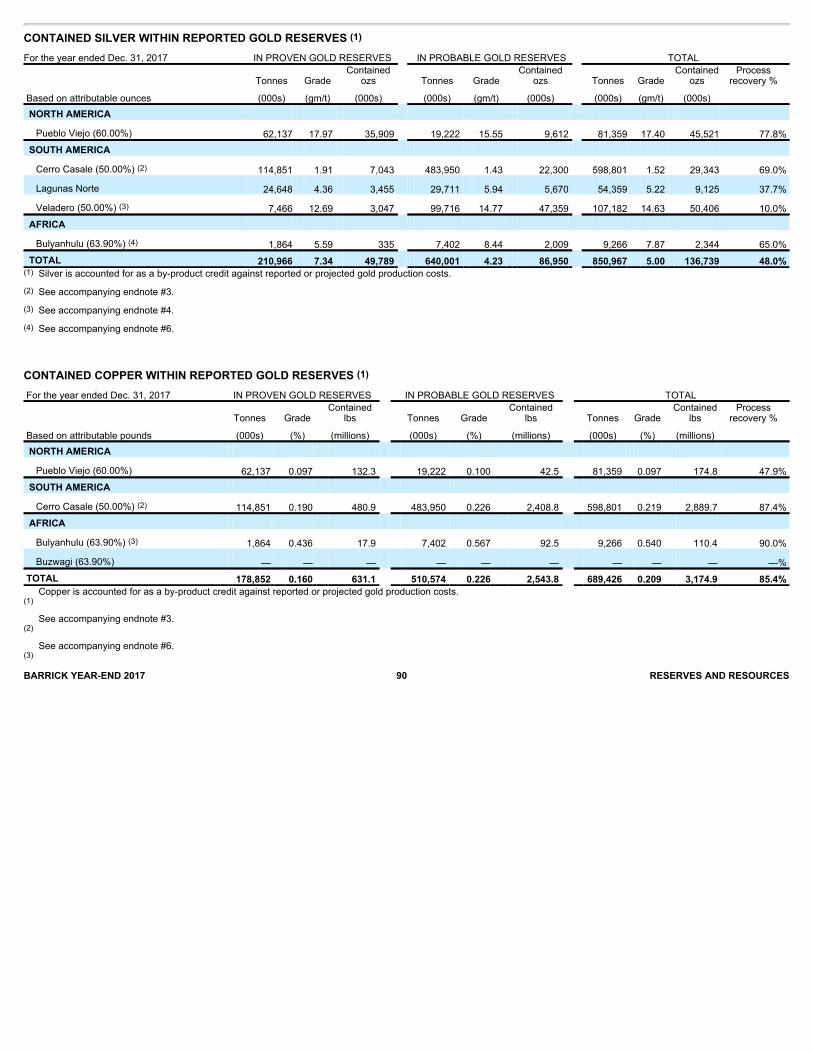

MineralReservesandMineralResources