brent stockwellsylvia dlott strategic initiatives director sr. budget analyst scottsdale city...

TRANSCRIPT

Brent Stockwell Sylvia DlottStrategic Initiatives Director Sr. Budget AnalystScottsdale City Manager’s Office Scottsdale Finance & Accounting

Division(480) 312-7288 (480) [email protected] [email protected]

www.ScottsdaleAZ.gov/finance

Elected ExpectationsAdministrative Realities

Different perspectives;Different goals

Consider the role of the translator

“A translator is a person who helps people who speak different languages to communicate or who takes something (such as a speech or a book) in one language and who puts it into a different language for people to understand.”

http://www.yourdictionary.com/translator

Presentation Framework The budget is a policy document Use the budget to communicate

effectively Encourage public involvement and

transparent decision-making Pay careful attention to revenues Monitor the budget. Require timely

updates and adjustments. Establish a fund balance policy. Maintain

and deploy fund balances wisely Encourage performance targets and

measures as management tools

Source: Elected Officials Guide to Government Finance, Second Edition, 2008, Girard Miller

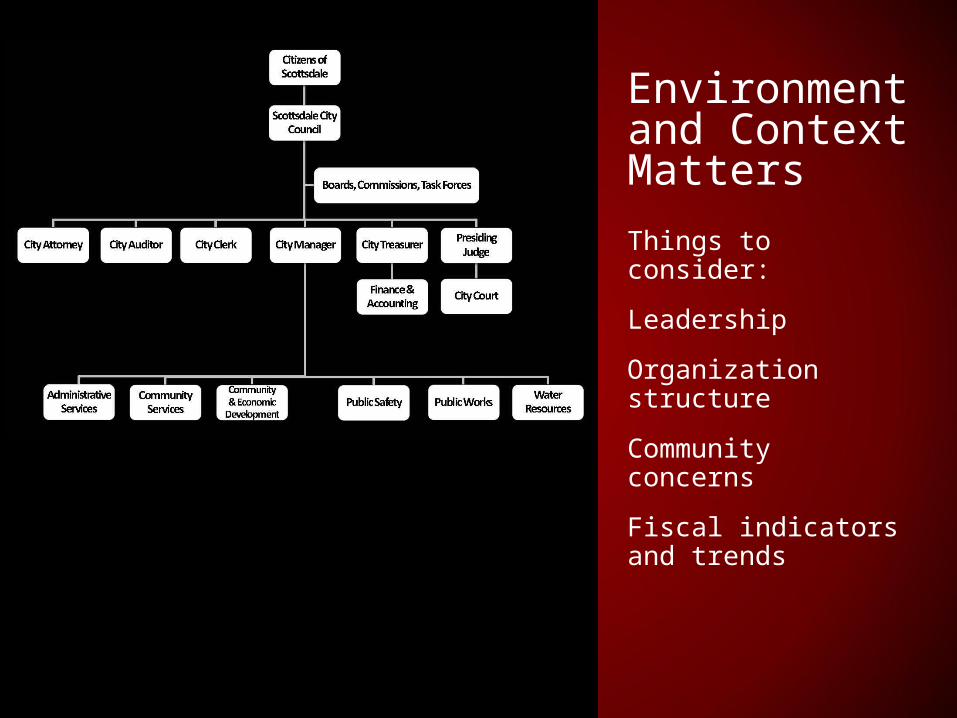

Environment and Context Matters

Things to consider:

Leadership

Organization structure

Community concerns

Fiscal indicators and trends

Structuring the review process

Several variations

Advantages and disadvantages to each

Full CouncilBudget CommissionCouncil Subcommittee

Difference between Proposed and Adopted Budget (General Fund)

The budget is a policy document

“Elected officials should focus on policies…”

“Excessive review of details, however may preclude thoughtful study of broader policy issues that rightfully should dominate the public policy dialogue. Many budget deliberation sessions have suffered from debates over relatively inconsequential operational details and special interests of individual elected officials, while long-term fiscal problems loomed ahead.” (p.12)

Make everything available, but focus on key issues

Examples?

Use the budget to communicate effectively

“with a deliberate focus on decision-relevant information, government can improve the communications quality of their budget documents.” (p. 13)

Refer back to the provided documents, build trust and confidence

Keep in mind that crisis can impact decisions for a long time…

Use the budget process to help them understand what’s important to understand from a management perspective.

What information do use to make decisions?

What are you trying to accomplish?

How will you know when you’ve done it?

How do you know what you need? $$$, staff, etc.

“It’s got to be math, got to be simple math” ~ David N. Smith

Tips for Council communicationsWhat’s the goal? clear, unbiased and politically sensitive

Get to the point. Include information necessary to adequately understand the issue and make a decision

Place it in context. Don’t forget to remind Council of past discussions, actions and direction

Explain the effect on the citizen. What we do impacts others, and we need to clearly explain the impacts, and what input we have received

Remember that the City Council “is the boss.” Your writing and interactions should acknowledge their role in the policy process

Tips for Council communications (cont’d)Don’t “waffle” on difficult subjects. Limit the times you “frame” or soften an issue. Be up front, clear and honest.

Support your statements. Avoid terms that make value judgments about the topic, i.e. good/bad, right/wrong, etc.

Anticipate questions. Don’t assume that anything is simple or minor. Be prepared for anything; or better yet – anticipate the questions and include responses

Use graphics appropriately. Some readers prefer visual information, others prefer written or oral explanations. Provide both.

Ask others to review. Clarify and simplify any information that may be difficult to understand.

“Unfortunately, public attendance at preliminary hearings tends to reflect special interest and general apathy regarding broader fiscal issues…” (p. 14)

Want to increase attendance at budget meetings?

1.Raise taxes

2.Cut services

Encourage public involvement and transparent decision-making

Discussion

What have you learned in your community about:

focusing discussions at the policy level?

using the budget to communicate effectively?

Involving citizens and transparent decision-making?

Pay careful attention to revenues“Overly optimistic revenue projections often precede a financial crisis. Inflating revenue estimates to avoid cutting expenditures only defers and aggravates any fiscal imbalance.” (p. 15)

Monitor the budget. Require timely updates and adjustments. “…interim reports should highlight variances from the original budget and provide sufficient narrative explanations for elected officials to make informed judgments.” (p. 16)

Establish a fund balance policy. Maintain and deploy fund balances wisely

When is the budget, truly “balanced?”

Discussion

What have you learned in your community about:

paying careful attention to revenues?

timely budget monitoring?

maintaining and deploying fund balances wisely?

Encourage performance targets and measures as management tools

“… legislators have two roles: 1) to allocate resources among various agencies (and their only available guidance is their own political or personal values), and 2) to provide an incentive scheme that appropriately rewards and punishes managers for behaviors consistent with the goals of the government.”

“Performance measures are not useful for the legislative problem of allocating resources among disparate goals, but they are useful for improving the quality and reducing the cost of providing services.”

“when the legislature is hesitant or unwilling to state its desires, the value of performance measures is limited.”

“Evidence suggests that improved performance occurs at a much greater rate when performance measures are compared.”

Smith, Ken A. and Cheng, Rita Hartung, Assessing Reforms of Government Accounting and Budgeting (November 5, 2004). , . Available at SSRN: http://ssrn.com/abstract=616921

“…elected officials should encourage public managers to develop realistic performance targets and reliable, relevant measures for assessing and reporting performance…” (p. 20)

Some things to think about, from some practical academics

The existing process is costly and time consuming.“…no government in the world devotes as much time, energy and talent to budget decision making as ours does.” ~ Alice Rivlin (1984)

“…there is always one army formulating budgets, another adopting them, and a third executing them. Where flexibility is needed to adapt to changed circumstances… transferring spending authority from one place to another is often almost as time consuming as enacting it in the first place.”

It doesn’t work (do what it was/is supposed to do).Budget reform (1921) was intended to “moderate spending growth, produce better estimates of revenues and expenditures, and reduce government waste and fraud.”

It doesn’t actually do much of anything useful.“what and how government spends, taxes, and borrows matters a great deal. However, there is very little evidence that all the time and effort devoted to budgeting has much, if any, influence on the actual pattern of spending, taxing and borrowing.”

Budgets focus attention on the wrong things.“Under current norms, once budgets have been adopted, they must be executed as enacted, spending is supposed to follow the numbers in the budget. This has the effect of constraining responsiveness and retarding experimentation and learning.”

Source: Smith, Ken A. and Thompson, Fred, Budgets? We Don’t Need No Stinkin Budgets: Ten Things We Think We Think We Know about Budgets and Performance (August 24, 2010). Available at SSRN: http://ssrn.com/abstract=1664771

Some things to think about, from some practical academics

Transparency is good…“When government processes are transparent, officials have greater incentives to put public benefit ahead of narrower interests, and citizens’ confidence in government expands…”

What to do? “In Beyond Budgeting, Hope and Fraser describe the experiences of many of the businesses around the world that have discarded annual performance targets/contracts because their leaders believed they tended to produced dysfunctional behaviors, promoted centralized command and control instead of localized learning, performance or growth, and got in the way of achieving the purposes of enterprises. To replace them they designed a slew of alternative financial planning systems: rolling forecasts, scenario planning and relative performance evaluation.”

“The time and resources previously wasted on traditional annual budgeting could be productively reallocated to figuring out how to reasonably evaluate relative performance and to difficult but useful discussions about how to prepare for events (scenario planning).

Source: Smith, Ken A. and Thompson, Fred, Budgets? We Don’t Need No Stinkin Budgets: Ten Things We Think We Think We Know about Budgets and Performance (August 24, 2010). Available at SSRN: http://ssrn.com/abstract=1664771

Discussion

What, if anything, stands out to you about the academic critiques of the budget process?

Describe budget “fantasyland” – if you could do anything, what might you do?

From the perspective of an elected official… what improvements to the budget process would you recommend?