cf-1 bank hapoalim jun-2001 zvi wiener 02-588-3049 mswiener/zvi.html computational finance

Post on 20-Dec-2015

214 views

TRANSCRIPT

CF-1 Bank Hapoalim Jun-2001

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

Computational Finance

CF1 slide 2Zvi Wiener

Plan1. Introduction, deterministic methods.2. Stochastic methods.3. Monte Carlo I.4. Monte Carlo II.5. Advanced methods for derivatives.

Other topics:queuing theory, floaters, binomial trees, numeraire, ESPP, convertible bond, DAC, ML-CHKP.

CF1 slide 3Zvi Wiener

Linear Algebra

-2 1

1

Vectors {1, 1}, {-2, 1}

rows or 1 -2columns 1 1

CF1 slide 4Zvi Wiener

Linear Algebra

CF1 slide 5Zvi Wiener

Basic Operations

1 2 3

2 + -1 = 1

-2 1 -1

1 3

3 2 = 6

2 6

CF1 slide 6Zvi Wiener

Linear Algebra

vector

3

2

1

x

x

x

x Vectors form a linear space.

3

2

1

x

x

x

x

33

22

11

yx

yx

yx

yx Zero vector

Scalar multiplication

CF1 slide 7Zvi Wiener

Linear Algebra

matrix

333231

232221

131211

aaa

aaa

aaa

AMatrices alsoform a linearspace.

Zero matrix

000

000

000

Unit matrix

100

010

001

CF1 slide 8Zvi Wiener

Linear Algebra

Matrix can operate on a vector

3

2

1

333231

232221

131211

x

x

x

aaa

aaa

aaa

Ax

333232131

323222121

313212111

xaxaxa

xaxaxa

xaxaxa

How does zero matrix operate?

How does unit matrix operate?

CF1 slide 9Zvi Wiener

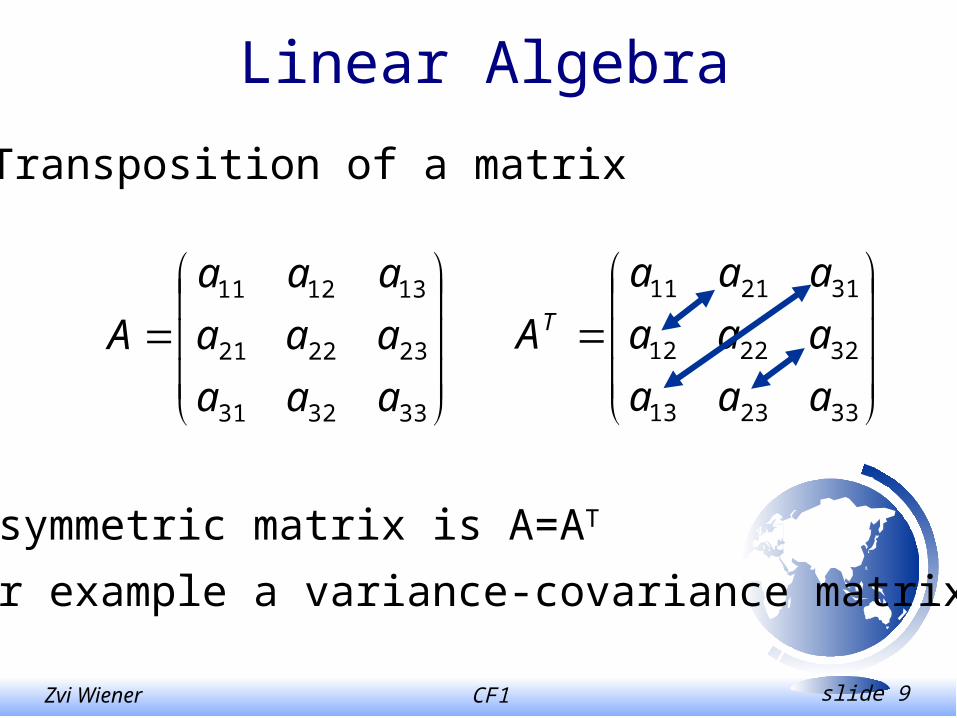

Linear Algebra

Transposition of a matrix

A symmetric matrix is A=AT

for example a variance-covariance matrix.

333231

232221

131211

aaa

aaa

aaa

A

332313

322212

312111

aaa

aaa

aaa

AT

CF1 slide 10Zvi Wiener

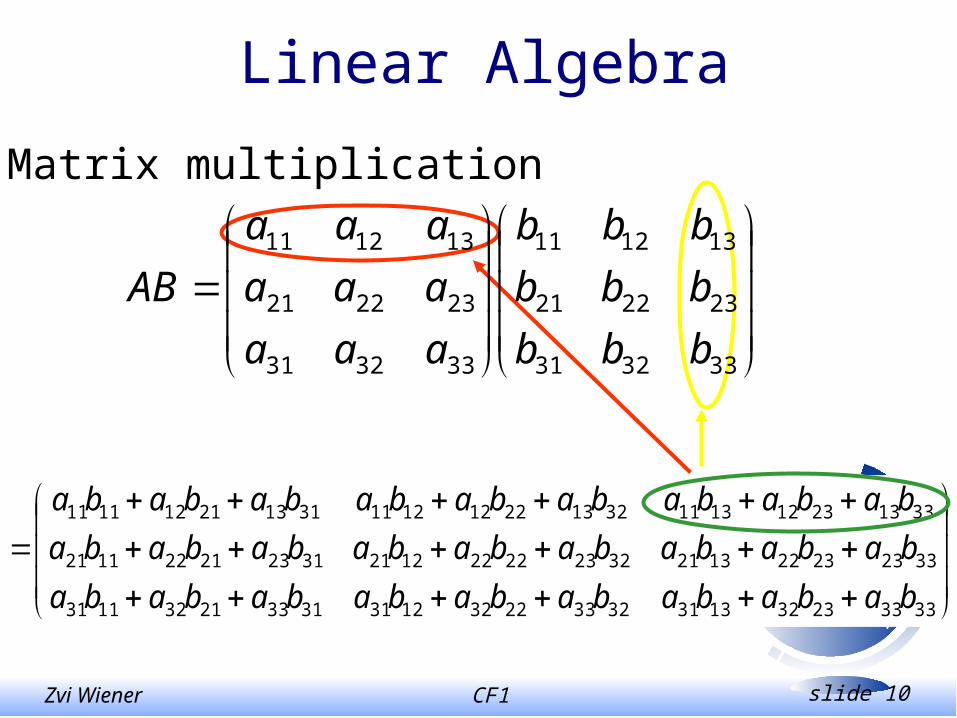

Linear Algebra

Matrix multiplication

333323321331323322321231313321321131

332323221321322322221221312321221121

331323121311321322121211311321121111

bababababababababa

bababababababababa

bababababababababa

333231

232221

131211

333231

232221

131211

bbb

bbb

bbb

aaa

aaa

aaa

AB

CF1 slide 11Zvi Wiener

Scalar Product

i

iibaba

332211

3

2

1

321 ,, bababa

b

b

b

aaa

a is orthogonal to b if ab = 0

CF1 slide 12Zvi Wiener

Linear Algebra

Scalar product of two vectors

332211

3

2

1

321 yxyxyx

y

y

y

xxxyxT

Euclidean norm

23

22

21

2xxxxxx T

CF1 slide 13Zvi Wiener

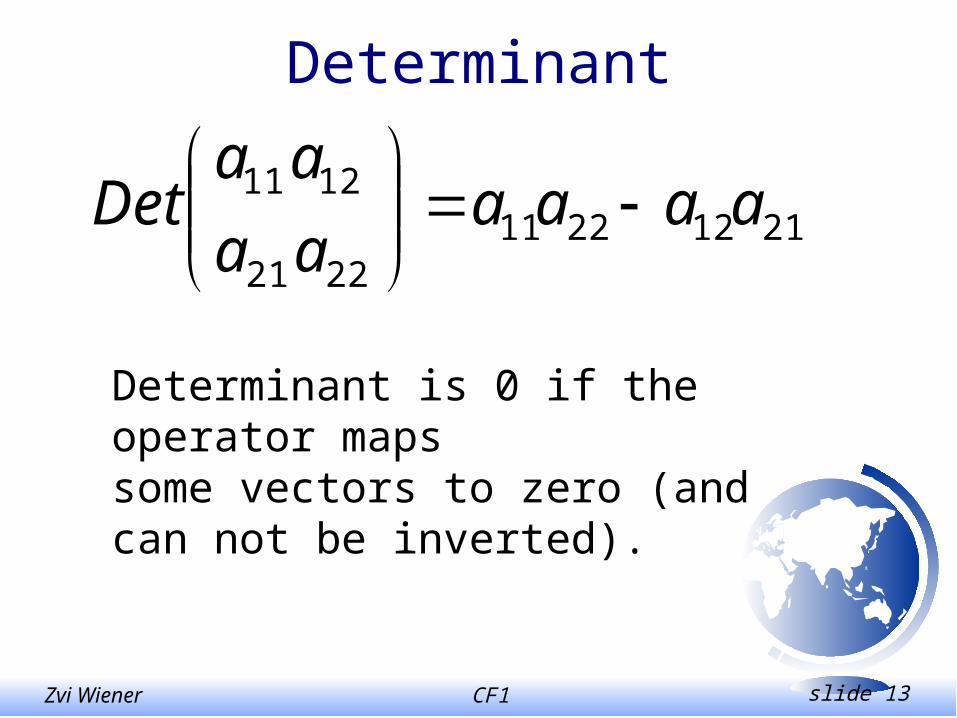

Determinant

211222112221

1211 aaaaaa

aaDet

Determinant is 0 if the operator mapssome vectors to zero (and can not be inverted).

CF1 slide 14Zvi Wiener

Linear Algebra

• Matrix multiplication corresponds to a

consecutive application of each operator.

• Note that it is not commutative! ABBA.

• Unit matrix does not change a vector.

• An inverse matrix is such that AA-1=I.

CF1 slide 15Zvi Wiener

Linear Algebra

• Determinant of a matrix ...

• A matrix can be inverted if det(A)0

• Rank of a matrix

• Matrix as a system of linear equations Ax=b.

• Uniqueness and existence of a solution.

• Trace tr(A) – sum of diagonal elements.

CF1 slide 16Zvi Wiener

Linear Algebra

• Change of coordinates C-1AC.

• Jordan decomposition.

• Matrix power Ak.

• Matrix as a quadratic form (metric) xTAx.

• Markov process.

• Eigenvectors, eigenvalues Ax=x,

optimization.

CF1 slide 17Zvi Wiener

Problems

Check how the following matrices act on vectors:

00

01

10

01

10

01

cossin

sincos

01

10

01

10

CF1 slide 18Zvi Wiener

Simple Exercises

• Show an example of ABBA.

• Construct a matrix that inverts each vector.

• Construct a matrix that rotates a two dimensional vector by an angle .

• Construct a covariance matrix, show that it is symmetric.

• What is mean and variance of a portfolio in matrix terms?

CF1 slide 19Zvi Wiener

Examples

• Credit rating and credit dynamics.

• Variance-covariance model of VaR.

• Can the var-covar matrix be inverted

• VaR isolines (the ovals model).

• Prepayment model based on types of clients.

• Finding a minimum of a function.

CF1 slide 20Zvi Wiener

Calculus

• Function of one and many variables.

• Continuity in one and many directions.

• Derivative and partial derivative.

• Gradient and Hessian.

• Singularities, optimization, ODE, PDE.

CF1 slide 21Zvi Wiener

x

$

Linear and quadratic terms

CF1 slide 22Zvi Wiener

Taylor series

22

2)(")(')()( xo

xxfxxfxfxxf

2222

22

),(),(

yxoy

gyxgx

g

ygxgyxgyyxxg

yyxyxx

yx

2)("

2

1)(')()( xoxxFxxxFxFxxF T

CF1 slide 23Zvi Wiener

Variance-Covariance

),...,,()( 21 nxxxVxV

nnn

n

n

1

2221

112111

,

CF1 slide 24Zvi Wiener

Variance-Covariance

nx

V

x

V

xV 1

)('Gradient vector:

CF1 slide 25Zvi Wiener

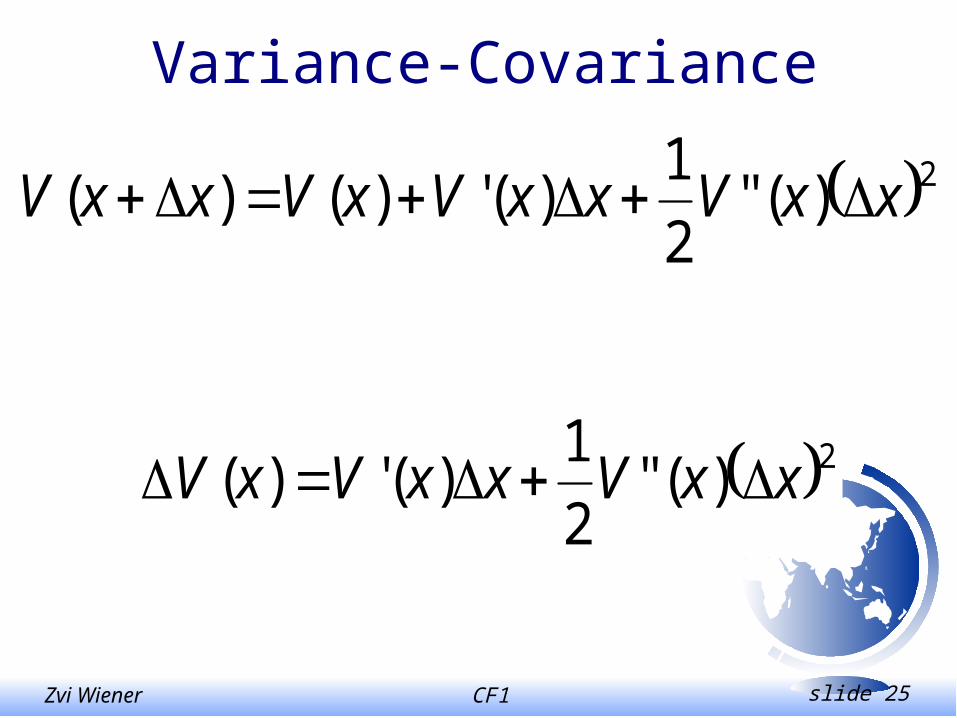

Variance-Covariance

2)("2

1)(')()( xxVxxVxVxxV

2)("2

1)(')( xxVxxVxV

CF1 slide 26Zvi Wiener

Variance-Covariance

22

)(")(' xE

xVxVxEVE

"2

1' VtrVVE T

'' VVV T

CF1 slide 27Zvi Wiener

Variance-Covariance

For a short time period , the changes in the value are distributed approximately normal with the following mean and variance:

''

"2

1'

2 VVV

VtrVVE

T

T

CF1 slide 28Zvi Wiener

Variance-Covariance

Then VaR can be found as:

)(33.2)(%,1 VVVVaR

''33.2"2

1' VVVtrV TT

CF1 slide 29Zvi Wiener

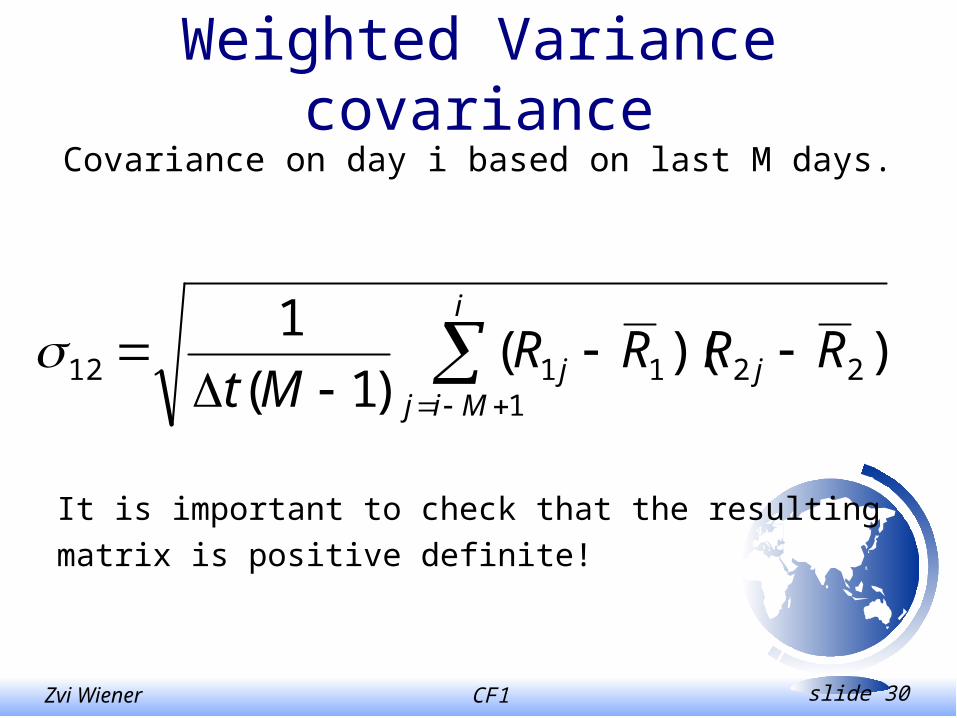

Weighted Variance covariance

Volatility estimate on day i based on last M days.

i

Mijj RR

Mt 1

2)()1(

1

i

jj

ji RRt

2)(1

CF1 slide 30Zvi Wiener

Weighted Variance covariance

Covariance on day i based on last M days.

i

Mijjj RRRR

Mt 1221112 ))((

)1(

1

It is important to check that the resulting

matrix is positive definite!

CF1 slide 31Zvi Wiener

Positive Quadratic Form

For every vector x a we have x.A.x > 0

Only such a matrix can be used to define a

norm.

For example, this matrix can not have

negative diagonal elements. Any variance-

covariance matrix must be positive.

CF1 slide 32Zvi Wiener

Positive Quadratic Form

Needs["LinearAlgebra`MatrixManipulation`"];

ClearAll[ positiveForm ];

positiveForm[ a_?MatrixQ ] := Module[{aa, i},

aa = Table[

Det[ TakeMatrix[ a, {1, 1}, {i, i}] ],

{i, Length[a]}];

{ aa, If[ Count[ aa, t_ /; t < 0] > 0, False, True]}

];

CF1 slide 33Zvi Wiener

Stochastic (transition) Matrix

Used to define a Markov chain (only the last state matters).

A matrix P is stochastic if it is non-negative and sum of elements in each line is 1.

One can easily see that 1 is an eigenvalue of any stochastic matrix.

What is the eigenvector?

CF1 slide 34Zvi Wiener

Markov chain

• credit migration

• prepayment and freezing of a program

CF1 slide 35Zvi Wiener

Stochastic (transition) Matrix

Theorem: P0 is stochastic iff (1,1,…1) is an eigenvector with an eigenvalue 1 and this is the maximal eigenvalue.

If both P and PT are stochastic, then P is called double stochastic.

CF1 slide 36Zvi Wiener

Cholesky decomposition

The Cholesky decomposition writes a symmetric positive definite matrix as the product of an upper triangular matrix and its transpose.

In MMA CholeskyDecomposition[m]

CF1 slide 37Zvi Wiener

Generating Random Samples

We need to sample two normally distributed variables with correlation .

If we can sample two independent Gaussian variables x1 and x2 then the required variables can be expressed as

2212

11

1

xxy

xy

CF1 slide 38Zvi Wiener

Generating Random Samples

We need to sample n normally distributed variables with correlation matrix ij, ( >0).

Sample n independent Gaussian variables x1…xn.

n

kkiki xay

1

xAy .

AAAanda Tn

kik ,,1

1

2

CF1 slide 39Zvi Wiener

Function of a matrix

!3!2

32 AAAEeA

TJTA

TJTJTJTTTA

JTTA

nn 1

21112

1

CF1 slide 40Zvi Wiener

ODE

Axdt

dx 00 )( xtx

0)( 0)( xetx ttA

CF1 slide 41Zvi Wiener

ODE

)(tfAxdt

dx 00 )( xtx

t

t

tAttA dtfexetx0

0 )()( )(0

)(

CF1 slide 42Zvi Wiener

Bisection method

If the function is monotonic, e.g. implied vol.

x

f

CF1 slide 43Zvi Wiener

Newton’s method

x

f

x1x2x3

CF1 slide 44Zvi Wiener

Solve and FindRoot

Solve[ 0 = = x2- 0.8x3- 0.3, {x}]

{{x -> -0.467297}, {x ->0.858648 -0.255363*I}, {x -> 0.858648 + 0.255363*I}}

FindRoot[ x2 + Sin[x] - 0.8x3 - 0.3, {x, 0,1}]

{x -> 0.251968}

CF1 slide 45Zvi Wiener

Max, min of a multidimensional function

• Gradient method

• Solve a system of equations (both derivatives)

-1

-0.5

0

0.5

1-1

-0.5

0

0.5

1

0

0.5

1

-1

-0.5

0

0.5

1

CF1 slide 46Zvi Wiener

-1 -0.5 0 0.5 1-1

-0.5

0

0.5

1

Gradient method

CF1 slide 47Zvi Wiener

Level curve of a multivariate function

ContourPlot[ x^2+y^3, {x,-2,2}, {y,- 2,2}]

ContourPlot[ x^2+y^3, {x,-2,2}, {y,- 2,2}], Contours->{1 ,-0.5}, ContourShading->False];

CF1 slide 48Zvi Wiener

ContourPlot[ x^2+y^3, {x,-2,2}, {y,- 2,2}]

-2 -1 0 1 2

-2

-1

0

1

2

CF1 slide 49Zvi Wiener

ContourPlot[ x^2+y^3, {x,-2,2}, {y,- 2,2}], Contours->{1 ,-0.5}, ContourShading->False];

-2 -1 0 1 2

-2

-1

0

1

2

CF1 slide 50Zvi Wiener

Example

Consider a portfolio with two risk factors and benchmark duration of 6M.

The VaR limit is 3 bp. and you have to make two decisions:

a – % of assets kept in spread products

q – duration mismatch

we assume that all instruments (both treasuries and spread) have the same duration T+q months.

CF1 slide 51Zvi Wiener

q - durationmismatch

Contour Levels of VaR (static)

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

a (% of spread)

CF1 slide 52Zvi Wiener

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

q - durationmismatch

a (% of spread)

position

VaR=2 bp

VaR=3 bp

CF1 slide 53Zvi Wiener

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

q - durationmismatch

a (% of spread)

In order to reducerisk one can increase duration(in this case).

CF1 slide 54Zvi Wiener

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

What we can do using limits

VaR = 6 bp

CF1 slide 55Zvi Wiener

0 0.2 0.4 0.6 0.8 1

-0.2

-0.1

0

0.1

0.2

spread %

duration mismatch (yr)

Position 2M, and10% spread5% weekly VaR=2.2 bp

weekly VaR limit 3 bp

CF1 slide 56Zvi Wiener

Splines

x1 x2 x3 … xn

CF1 slide 57Zvi Wiener

Splines<<Graphics`Spline`

pts = {{0, 0}, {1, 2}, {2, 3}, {3, 1}, {4, 0}}

Show[

Graphics[

Spline[pts, Cubic, SplineDots -> Automatic]]]

CF1 slide 58Zvi Wiener

Splinespts = Table[{i, i + i^2 + (Random[] - 0.5)}, {i, 0, 1, .05}];

Show[Graphics[Spline[pts,Cubic,SplineDots ->Automatic]]]

CF1 slide 59Zvi Wiener

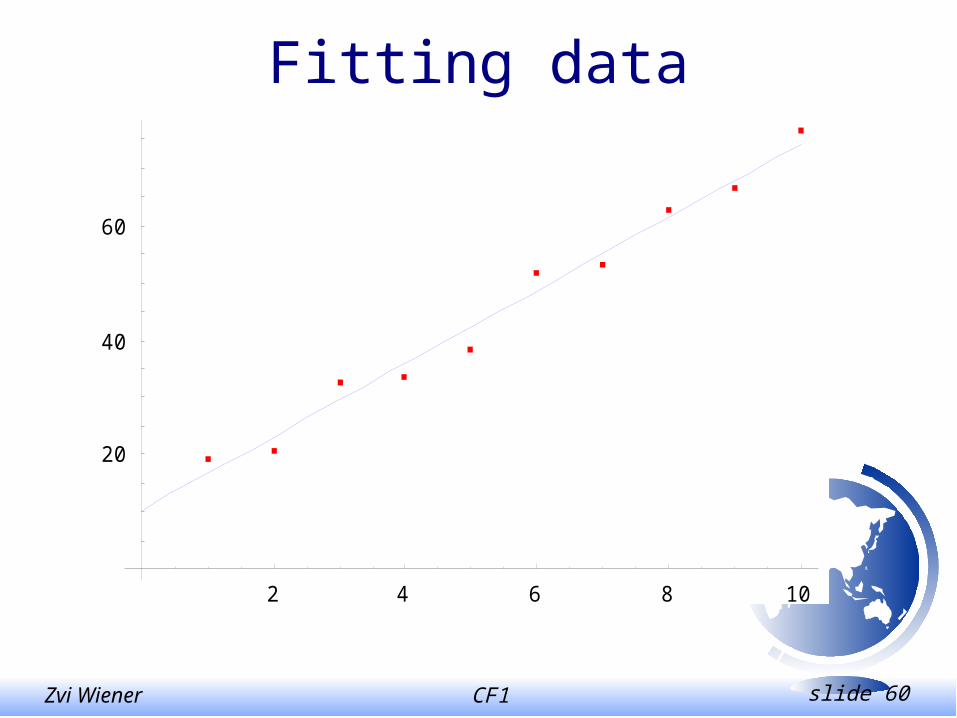

Fitting datadata = Table[7*x + 3 + 10*Random[], {x, 10}];

f[x_] := Evaluate[Fit[data, {1, x}, x]]

Needs["Graphics`Graphics`"]

DisplayTogether[

ListPlot[data, PlotStyle -> {AbsolutePointSize[3],

RGBColor[1, 0, 0]}],

Plot[f[x], {x, 0, 10}, PlotStyle -> RGBColor[0, 0, 1]]

];

CF1 slide 60Zvi Wiener

Fitting data

2 4 6 8 10

20

40

60

CF1 slide 61Zvi Wiener

Fitting data

data = {{1.0, 1.0, .126}, {2.0, 1.0, .219},

{1.0, 2.0, .076}, {2.0, 2.0, .126}, {.1, .0, .186}};

ff[x_, y_] = NonlinearFit[data,

a*c*x/(1 + a*x + b*y), {x, y}, {a, b, c}];

ff[x, y]

nonlinear, multidimensional

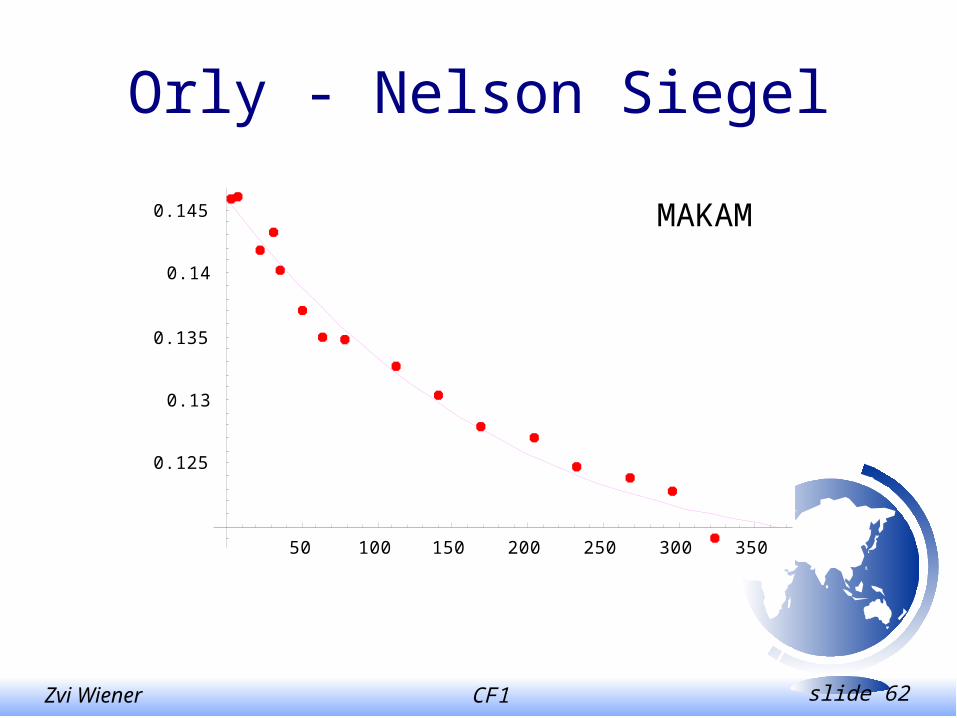

CF1 slide 62Zvi Wiener

Orly - Nelson Siegel

50 100 150 200 250 300 350

0.125

0.13

0.135

0.14

0.145 MAKAM

CF1 slide 63Zvi Wiener

Numerical Differentiation

22

2)(")(')()( xo

xxfxxfxfxxf

22

2)(")(')()( xo

xxfxxfxfxxf

2)('2)()( xoxxfxxfxxf

xoxfx

xxfxxf

)('2

)()(

CF1 slide 64Zvi Wiener

Numerical Differentiation

22

2)(")(')()( xo

xxfxxfxfxxf

22

2)(")(')()( xo

xxfxxfxfxxf

22)(")()(2)( xoxxfxxfxfxxf

22

)(")()(2)(

xOxfx

xxfxfxxf

CF1 slide 65Zvi Wiener

Finite Differences

Typically equal time and S (or logS) steps.

time

S Following P. Wilmott, “Derivatives”

CF1 slide 66Zvi Wiener

Finite Differences

Time step tasset step S(i,k) node of the grid is t = T - kt, iS0 i I, 0 k K

assets value at each node is

note the direction of time!

),( tkTSiVV ki

CF1 slide 67Zvi Wiener

The Black-Scholes equation

Linear parabolic PDE

0)(2

12

222

rVS

VSrr

S

VS

t

Vf

Final conditions )(),( SPayoffTSV

Boundary conditions ...

CF1 slide 68Zvi Wiener

Transformation of BS

U

x

U2

2

.2

,

,12

4

1

,12

2

1

),(),(

2

2

2

2

rTt

eS

r

r

xUetSV

x

x

CF1 slide 69Zvi Wiener

Approximating

h

tSVhtSV

t

Vh

),(),(lim

0

tOt

VVtS

t

V ki

ki

1

),(

CF1 slide 70Zvi Wiener

Approximating

211

2),( SO

S

VVtS

S

V ki

ki

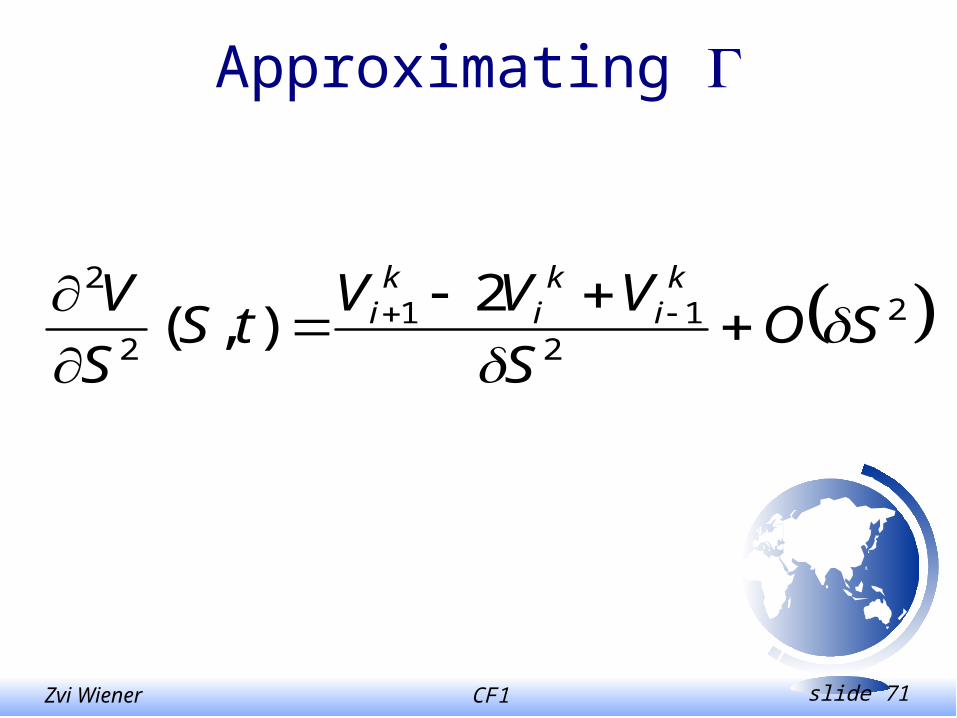

CF1 slide 71Zvi Wiener

Approximating

22

112

2 2),( SO

S

VVVtS

S

V ki

ki

ki

CF1 slide 72Zvi Wiener

Bilinear Interpolation

A3A4

A2A1

V3V4

V2V1

4

1

4

1

jj

jjj

A

VA

V

Area of the rectangle

CF1 slide 73Zvi Wiener

Final conditions and payoffs

)(),( SPayoffTSV

)(0 SiPayoffVi

For example a European Call option

)0,(0 ESiMaxVi

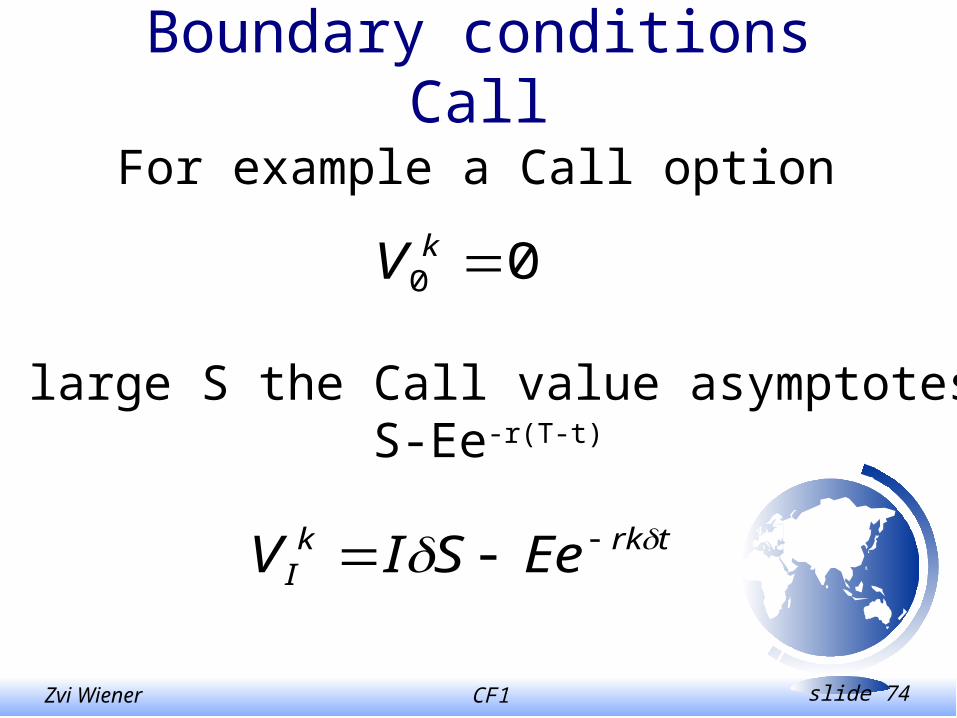

CF1 slide 74Zvi Wiener

Boundary conditions Call

00 kV

For example a Call option

trkkI EeSIV

For large S the Call value asymptotes toS-Ee-r(T-t)

CF1 slide 75Zvi Wiener

Boundary conditions Put

trkk EeV 0

For example a Put option

0kIV

For large S

CF1 slide 76Zvi Wiener

Boundary conditions S=0

0),0(),0(

trVtt

V

100 )1( kk VtrV

10

01

0

k

kk

rVt

VV

CF1 slide 77Zvi Wiener

Explicit scheme

0),(),(),(2

2

VtScS

VtSb

S

VtSa

t

V

),(2

2

211

211

1

StOVcS

VVb

S

VVVa

t

VV

ki

ki

ki

kik

i

ki

ki

kik

i

ki

ki

CF1 slide 78Zvi Wiener

Explicit scheme

),(2

2

211

211

1

StOVcS

VVb

S

VVVa

t

VV

ki

ki

ki

kik

i

ki

ki

kik

i

ki

ki

ki

ki

ki

ki

ki

ki

ki VCVBVAV 11

1 )1(

Local truncation error 22 , SttO

CF1 slide 79Zvi Wiener

Explicit scheme

ki

ki

ki

ki

ki

ki

ki VCVBVAV 11

1 )1(

time

S

Value here is calculated

These values arealready known

CF1 slide 80Zvi Wiener

Explicit scheme

ki

ki

ki

ki

ki

ki

ki VCVBVAV 11

1 )1(

This equation is defined for 1i I-1,

for i=1 and i=I we use boundary conditions.

CF1 slide 81Zvi Wiener

Explicit scheme

ki

ki

ki

ki

ki

ki

ki VCVBVAV 11

1 )1(

For the BS equation (with dividends)

,2/))((

,)(

,2/))((

22

22

22

tiDriC

triB

tiDriA

ki

ki

ki

CF1 slide 82Zvi Wiener

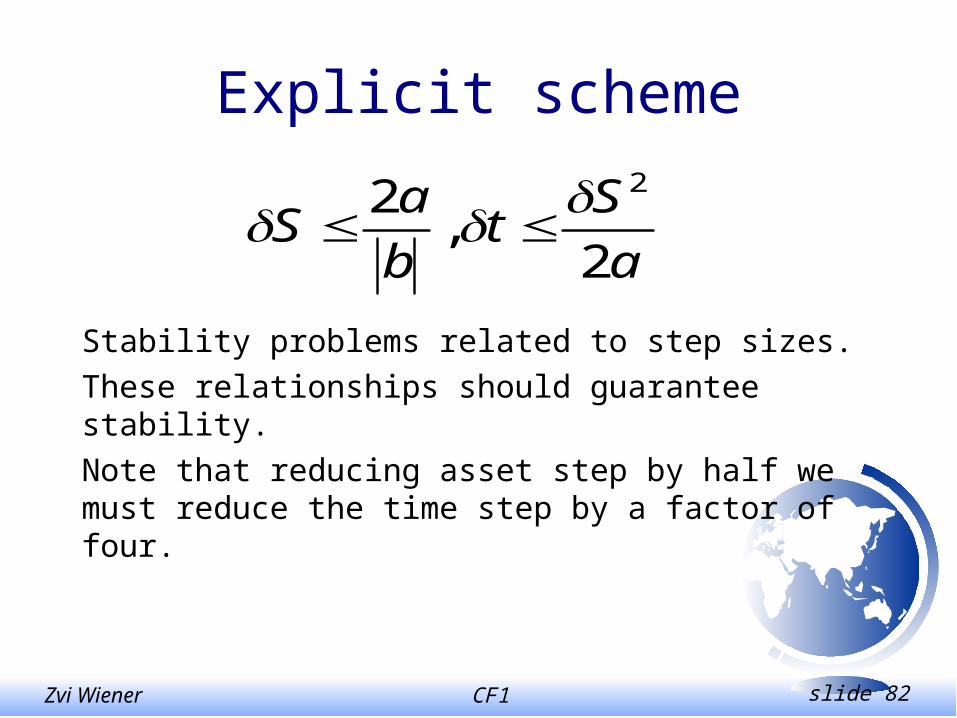

Explicit scheme

Stability problems related to step sizes.

These relationships should guarantee stability.

Note that reducing asset step by half we must reduce the time step by a factor of four.

a

St

b

aS

2,

2 2

CF1 slide 83Zvi Wiener

Explicit scheme

Advantages

easy to program, hard to make a mistake

when unstable it is obvious

coefficients can be S and t dependent

Disadvantages

there are restrictions on time step, which may cause slowness.

CF1 slide 84Zvi Wiener

Implicit scheme

0),(),(),(2

2

VtScS

VtSb

S

VtSa

t

V

),(2

2

2111

11

11

2

11

1111

1

StOVcS

VVb

S

VVVa

t

VV

ki

ki

ki

kik

i

ki

ki

kik

i

ki

ki

CF1 slide 85Zvi Wiener

Implicit scheme

),(2

2

2111

11

11

2

11

1111

1

StOVcS

VVb

S

VVVa

t

VV

ki

ki

ki

kik

i

ki

ki

kik

i

ki

ki

11

11111

1 )1(

ki

ki

ki

ki

ki

ki

ki VCVBVAV

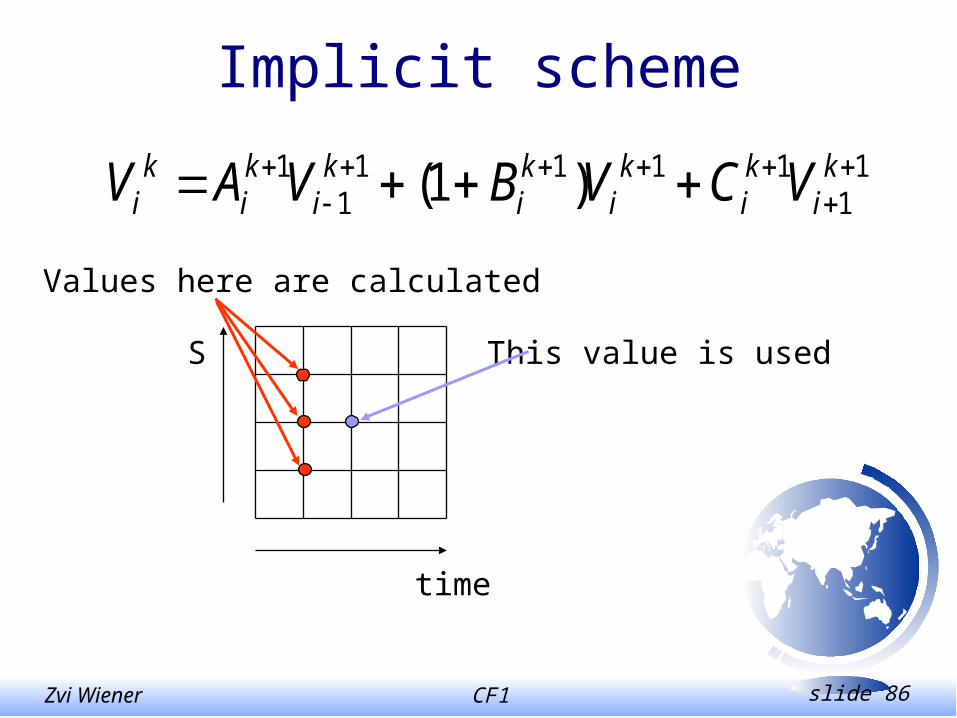

CF1 slide 86Zvi Wiener

Implicit scheme

time

S

Values here are calculated

This value is used

11

11111

1 )1(

ki

ki

ki

ki

ki

ki

ki VCVBVAV

CF1 slide 87Zvi Wiener

Crank-Nicolson scheme

),(2222

22

2

2

2

2

211

11

11

11

1

211

2

11

111

11

StOVc

Vc

S

VVb

S

VVb

S

VVVa

S

VVVa

t

VV

ki

kik

i

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

CF1 slide 88Zvi Wiener

Crank-Nicolson scheme

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

ki

VCVBVA

VCVBVA

11

11

11111

1

)1(

)1(

CF1 slide 89Zvi Wiener

Crank-Nicolson scheme

time

S

Values here are calculated

These values are used

CF1 slide 90Zvi Wiener

Crank-Nicolson scheme

0

0

0

10

10

000

1

01 10

11

11

12

12

11

11

11

12

12

12

12

11

11

kk

kI

kI

k

k

kI

kI

kI

kI

kk

kk VA

V

V

V

V

BA

CB

BA

CB

kkkR

kkL rvMvM 11

A general form of the linear equation is:

Note that M are tridiagonal!

CF1 slide 91Zvi Wiener

Crank-Nicolson scheme

kkkR

kL

k rvMMv 111

Theoretically this equation can be solved as

In practice this is inefficient!

CF1 slide 92Zvi Wiener

LU decomposition

M is tridiagonal, thus M=LU, where L is

lower triangular, and U is upper triangular.

In fact L has 1 on the diagonal and one

subdiagonal only, U has a diagonal and one

superdiagonal.

CF1 slide 93Zvi Wiener

LU decomposition

Then in order to solve Mv=q

orLUv=q

We will solve

Lw=q

first, and then

Uv=w.

CF1 slide 94Zvi Wiener

LU decomposition

Very fast, especially when M is time

independent.

Disadvantages:

Needs a big modification for American options

CF1 slide 95Zvi Wiener

Other methods

• SOR successive over relaxation

• Douglas scheme

• Three time-level scheme

• Alternating direction method

• Richardson Extrapolation

• Hopscotch method

• Multigrid methods

CF1 slide 96Zvi Wiener

Multidimensional case

r

S

Fixed t layer

These values are usedto calculate space derivatives

Note additional boundary conditions.

CF1 slide 97Zvi Wiener

Geometrical Brownian Motion

SdBrSdtdS

)()( SpayoffEeoption neutralrisktTr

CF1 slide 98Zvi Wiener

Lognormal process

SdBrSdtdS

dBdtrSd

2)(log

2

tZtr N

eStS)1,0(

2

2)0()(

CF1 slide 99Zvi Wiener

Euler Scheme

SdBrSdtdS

)()1,0( tOtSZtrSS N

CF1 slide 100Zvi Wiener

Milstein Scheme

SdBrSdtdS

)()1(2

1 22)1,0(

22

)1,0(

tOtZS

tSZtrSS

N

N

CF1 slide 101Zvi Wiener

Stochastic Calculus

Standard Normal

Diffusion process

x z

dzexN 2

2

2

1)(

tdBtXdttXdX ),(),(

ABM tdBdtdX

GBM tXdBXdtdX

CF1 slide 102Zvi Wiener

Ito’s Lemma

tdBtXdttXdX ),(),(

22

2

),( dXX

FdX

X

Fdt

t

FtXdF

dt dXdt 0 0dX 0 dt

CF1 slide 103Zvi Wiener

)1,0(

2

2)0()(

Ztt

eXtX

)ln(XY

22

)(11

0 dXX

dXX

dtdY

tdBdtdY

2

2

)1,0(

2

2)0()( ZttYtY

tXdBXdtdX

CF1 slide 104Zvi Wiener

Siegel’s paradoxConsider two currencies X and Y. Define S an exchange rate (the number of units of currency Y for a unit of X).

The risk-neutral process for S is

tSXY SdBSdtrrdS )(

By Ito’s lemma the process for 1/S is

tSSXY dBS

dtS

rrS

d111 2

CF1 slide 105Zvi Wiener

Siegel’s paradoxThe paradox is that the expected growth rate of 1/S is not ry - rX, but has a correction term.