cf-5 bank hapoalim jul-2001 zvi wiener 02-588-3049 mswiener/zvi.html computational finance

Post on 20-Dec-2015

220 views

TRANSCRIPT

CF-5 Bank Hapoalim Jul-2001

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

Computational Finance

CF-5 Bank Hapoalim Jul-2001

Following T. Bjork, ch. 15

Arbitrage Theory in Continuous Time

Bonds and Interest Rates

CF5 slide 3Zvi Wiener

Bonds and Interest Rates

Zero coupon bond = pure discount bond

T-bond, denote its price at time t by p(t,T).

principal = face value,

coupon bond - equidistant payments as a % of the face value, fixed or floating coupons.

CF5 slide 4Zvi Wiener

Assumptions

• There exists a frictionless market for T-

bonds for every T > 0

• p(t, t) =1 for every t

• for every t the price p(t, T) is differentiable

with respect to T.

CF5 slide 5Zvi Wiener

Interest Rates

Let t < S < T, what is IR for [S, T]?

• at time t sell one S-bond, get p(t, S)

• buy p(t, S)/p(t,T) units of T-bond

• cashflow at t is 0

• cashflow at S is -$1

• cashflow at T is p(t, S)/p(t,T)

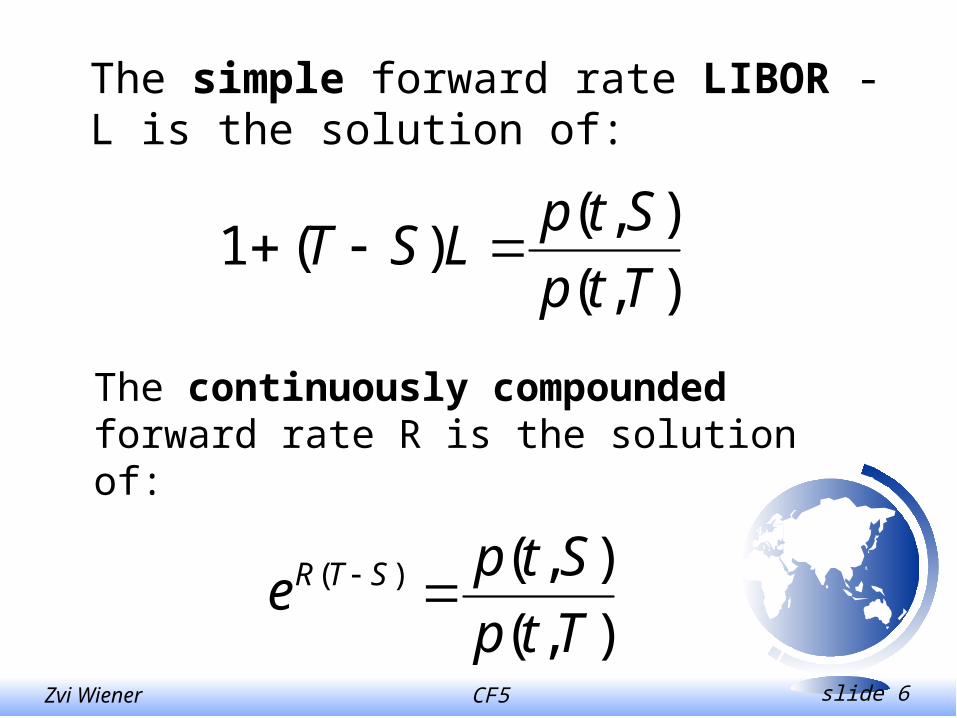

the forward rate can be calculated ...

CF5 slide 6Zvi Wiener

The simple forward rate LIBOR - L is the solution of:

),(

),()(1

Ttp

StpLST

The continuously compounded forward rate R is the solution of:

),(

),()(

Ttp

Stpe STR

CF5 slide 7Zvi Wiener

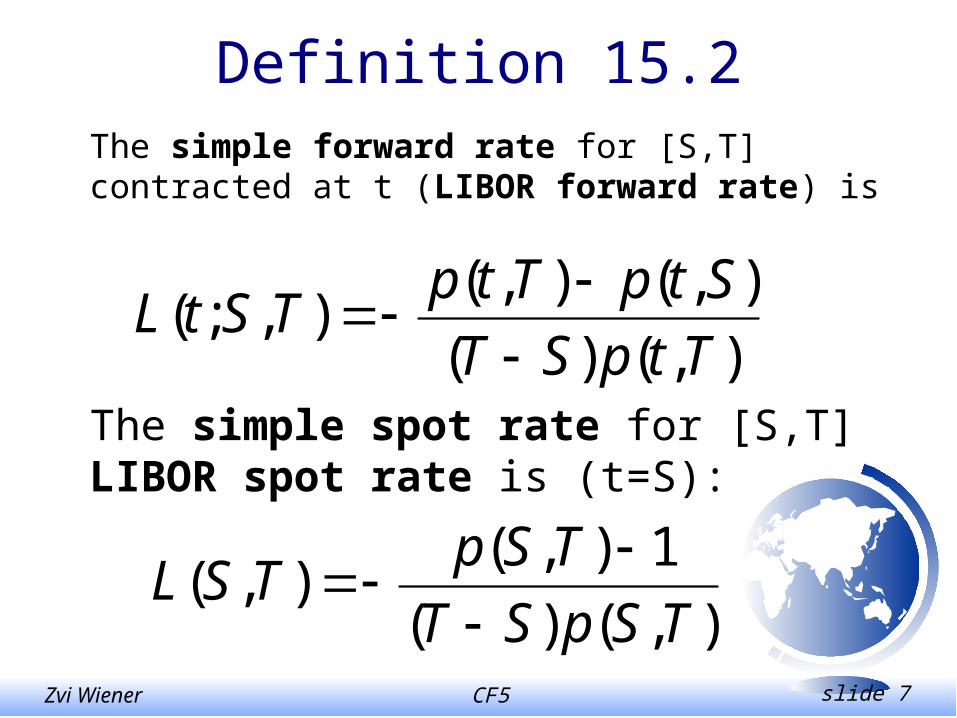

Definition 15.2

The simple forward rate for [S,T] contracted at t (LIBOR forward rate) is

),()(

),(),(),;(

TtpST

StpTtpTStL

The simple spot rate for [S,T] LIBOR spot rate is (t=S):

),()(

1),(),(

TSpST

TSpTSL

CF5 slide 8Zvi Wiener

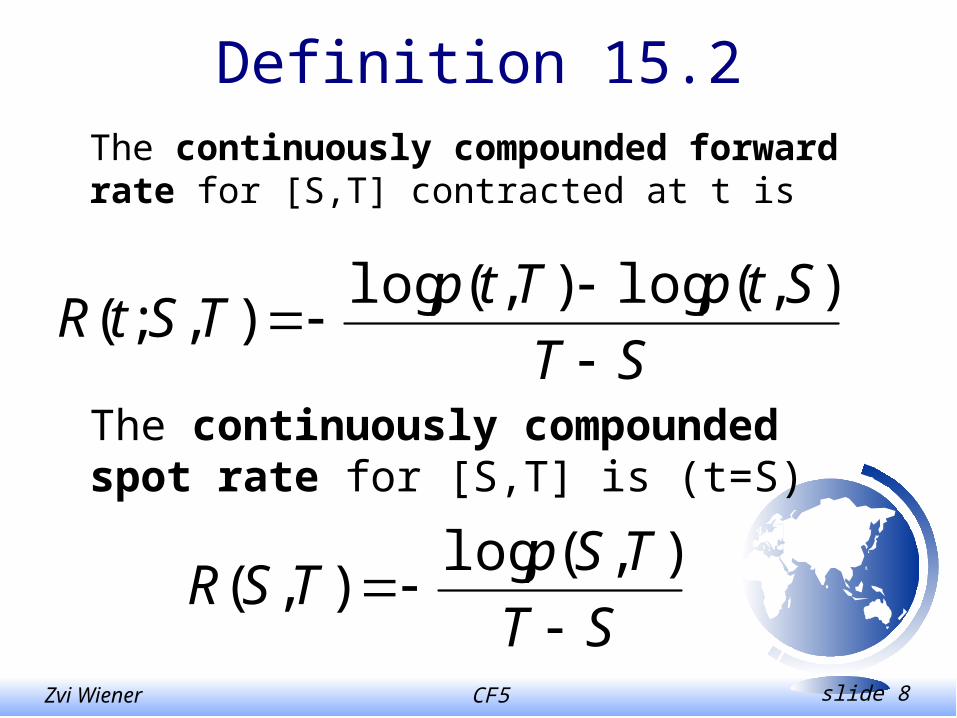

Definition 15.2

The continuously compounded forward rate for [S,T] contracted at t is

ST

StpTtpTStR

),(log),(log

),;(

The continuously compounded spot rate for [S,T] is (t=S)

ST

TSpTSR

),(log),(

CF5 slide 9Zvi Wiener

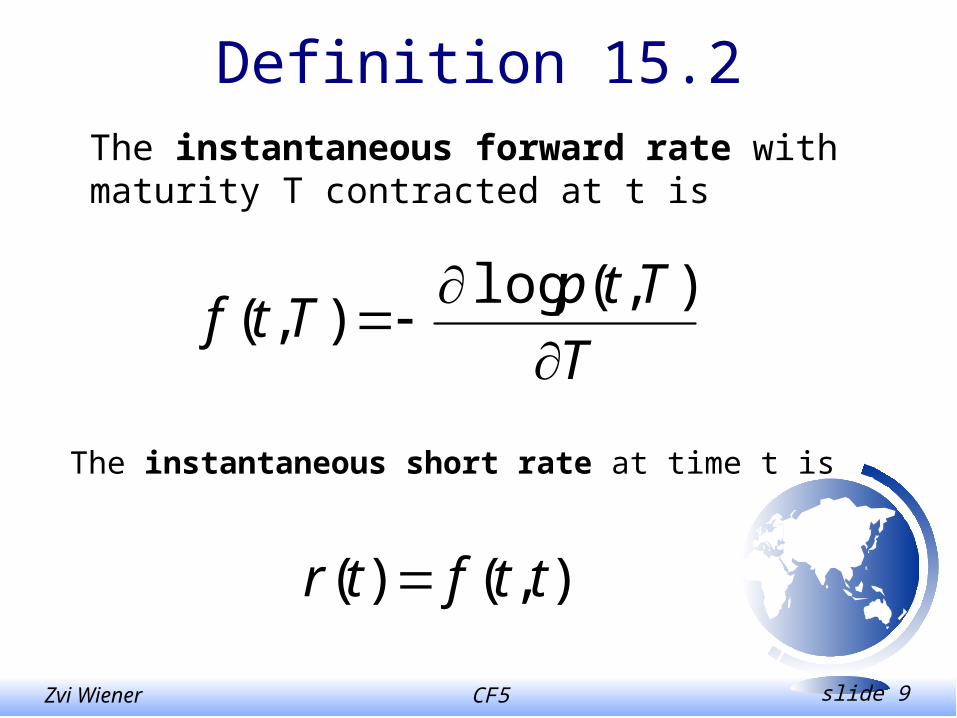

Definition 15.2

The instantaneous forward rate with maturity T contracted at t is

T

TtpTtf

),(log

),(

The instantaneous short rate at time t is

),()( ttftr

CF5 slide 10Zvi Wiener

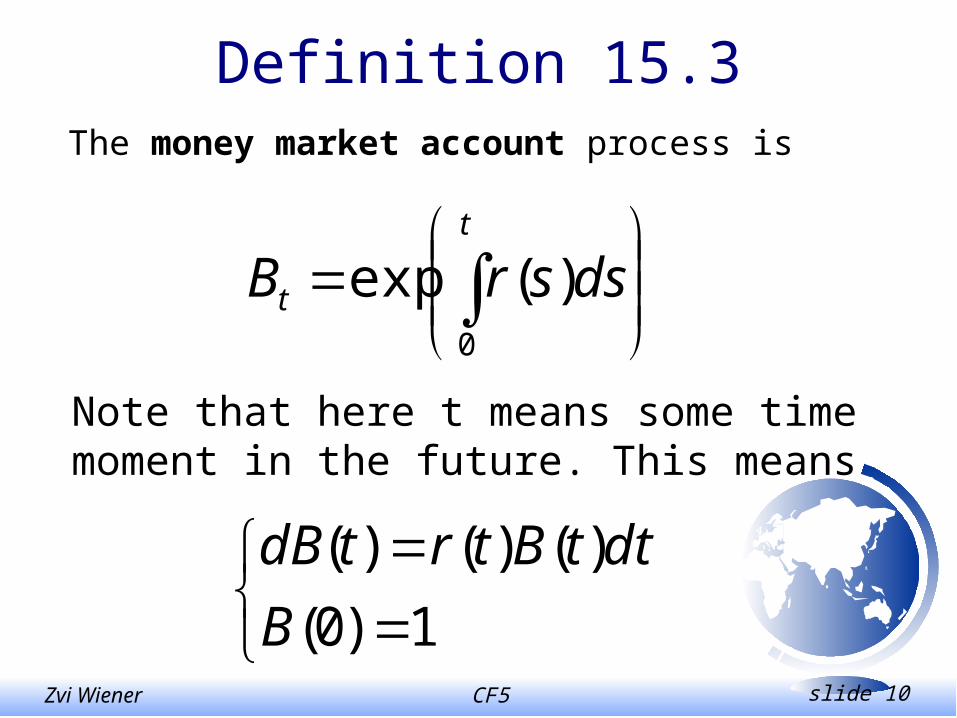

Definition 15.3The money market account process is

t

t dssrB0

)(exp

Note that here t means some time moment in the future. This means

1)0(

)()()(

B

dttBtrtdB

CF5 slide 11Zvi Wiener

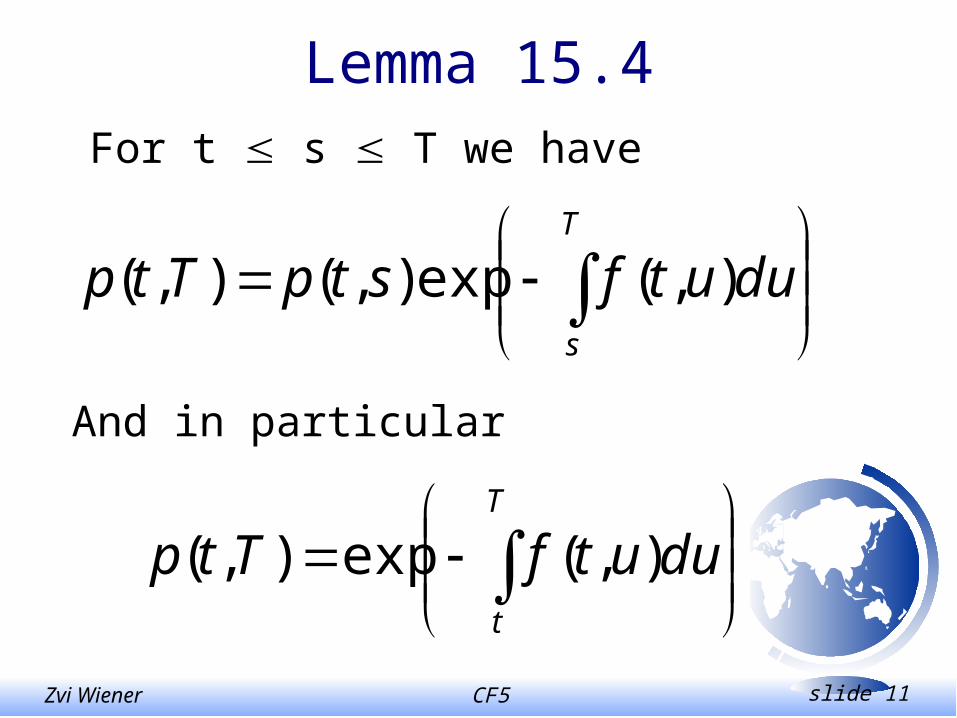

Lemma 15.4For t s T we have

T

s

duutfstpTtp ),(exp),(),(

And in particular

T

t

duutfTtp ),(exp),(

CF5 slide 12Zvi Wiener

Models of Bond Market

• Specify the dynamic of short rate

• Specify the dynamic of bond prices

• Specify the dynamic of forward rates

CF5 slide 13Zvi Wiener

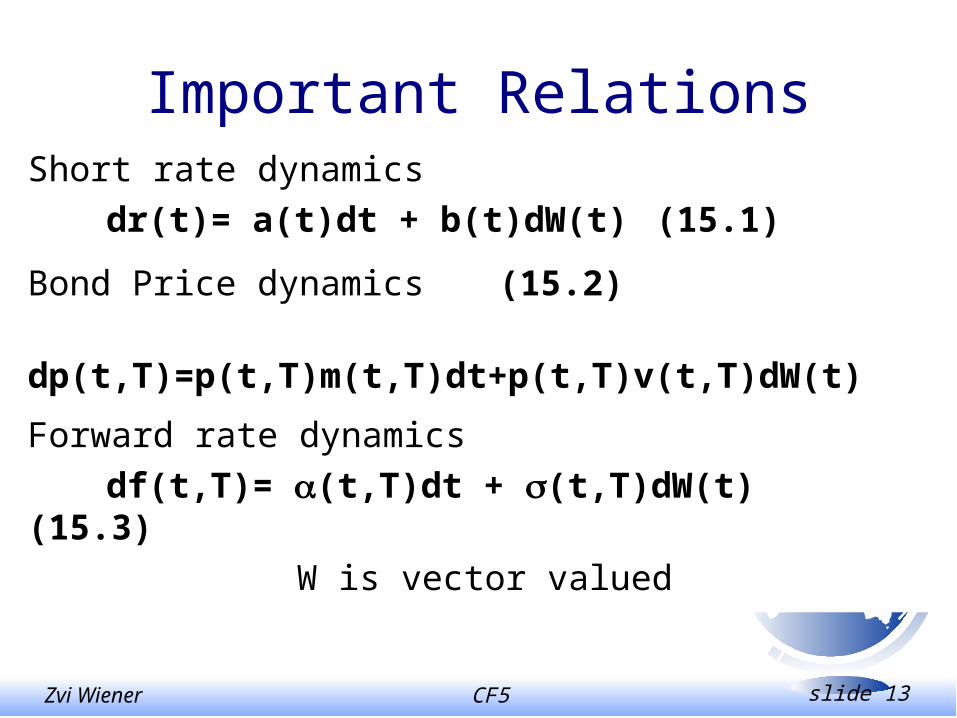

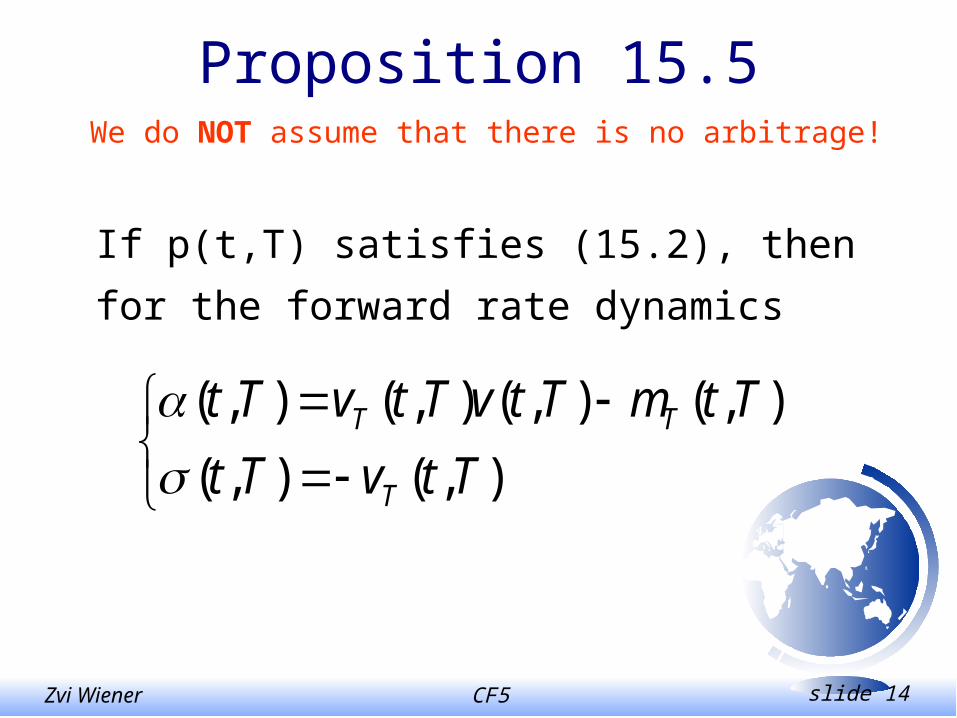

Important RelationsShort rate dynamics

dr(t)= a(t)dt + b(t)dW(t) (15.1)

Bond Price dynamics (15.2)

dp(t,T)=p(t,T)m(t,T)dt+p(t,T)v(t,T)dW(t)

Forward rate dynamics

df(t,T)= (t,T)dt + (t,T)dW(t) (15.3)

W is vector valued

CF5 slide 14Zvi Wiener

Proposition 15.5We do NOT assume that there is no arbitrage!

),(),(

),(),(),(),(

TtvTt

TtmTtvTtvTt

T

TT

If p(t,T) satisfies (15.2), then for the forward

rate dynamics

CF5 slide 15Zvi Wiener

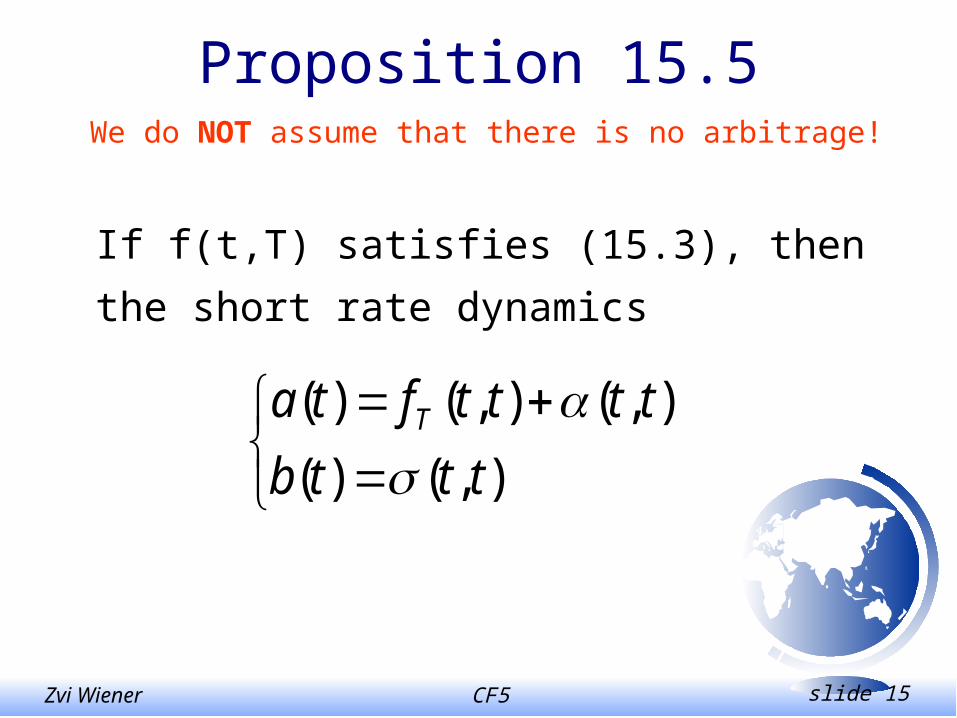

Proposition 15.5We do NOT assume that there is no arbitrage!

),()(

),(),()(

tttb

ttttfta T

If f(t,T) satisfies (15.3), then the short rate

dynamics

CF5 slide 16Zvi Wiener

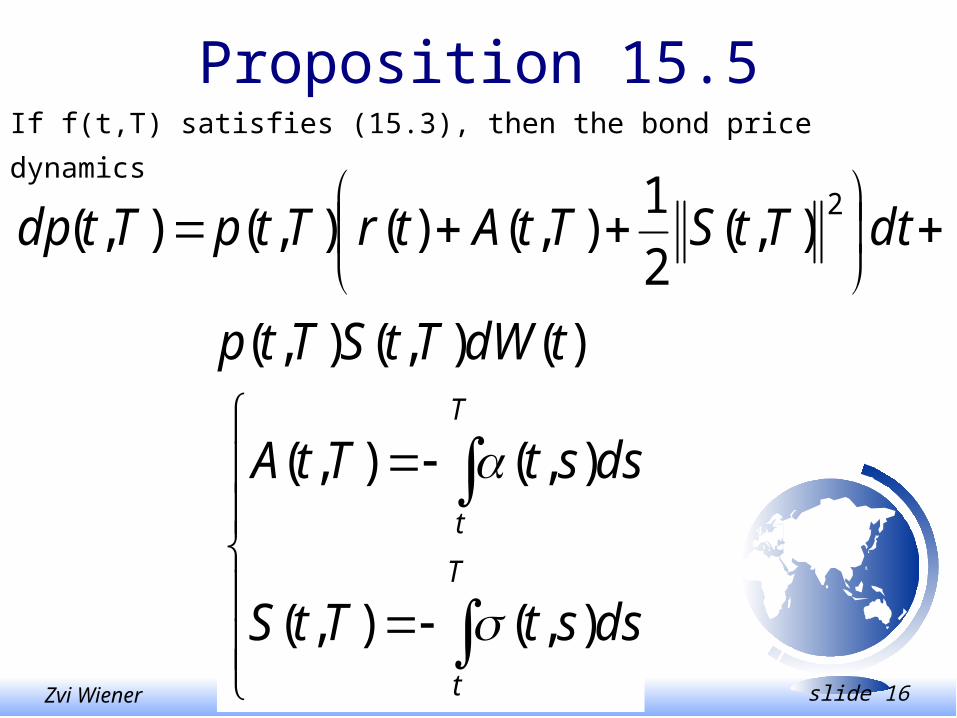

Proposition 15.5

)(),(),(

),(2

1),()(),(),(

2

tdWTtSTtp

dtTtSTtAtrTtpTtdp

If f(t,T) satisfies (15.3), then the bond price dynamics

T

t

T

t

dsstTtS

dsstTtA

),(),(

),(),(

CF5 slide 17Zvi Wiener

Proof of Proposition 15.5Left as an exercise …

CF5 slide 18Zvi Wiener

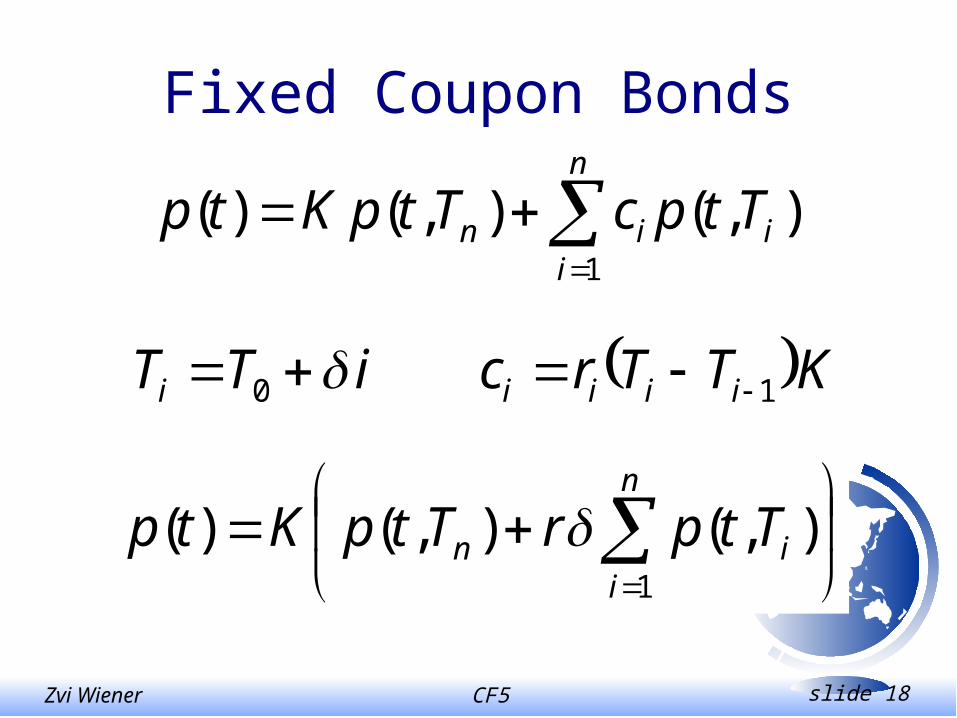

Fixed Coupon Bonds

n

iiin TtpcTtpKtp

1

),(),()(

n

iin TtprTtpKtp

1

),(),()(

KTTrciTT iiiii 10

CF5 slide 19Zvi Wiener

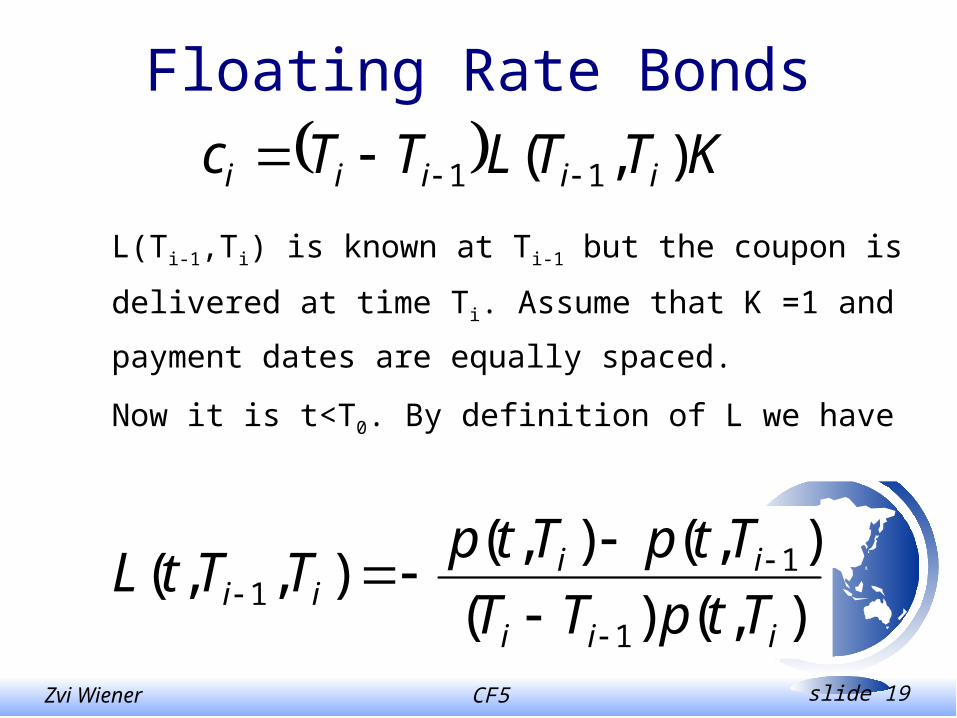

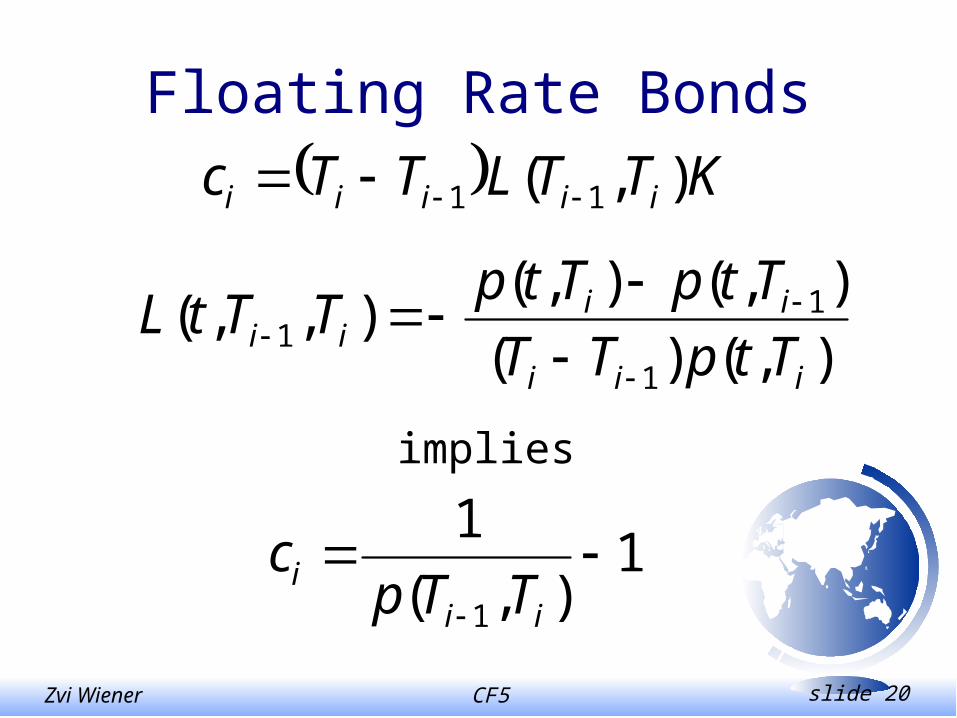

Floating Rate Bonds

KTTLTTc iiiii ),( 11

L(Ti-1,Ti) is known at Ti-1 but the coupon is

delivered at time Ti. Assume that K =1 and

payment dates are equally spaced.

Now it is t<T0. By definition of L we have

),()(

),(),(),,(

1

11

iii

iiii TtpTT

TtpTtpTTtL

CF5 slide 20Zvi Wiener

Floating Rate Bonds

1),(

1

1

ii

i TTpc

KTTLTTc iiiii ),( 11

),()(

),(),(),,(

1

11

iii

iiii TtpTT

TtpTtpTTtL

implies

CF5 slide 21Zvi Wiener

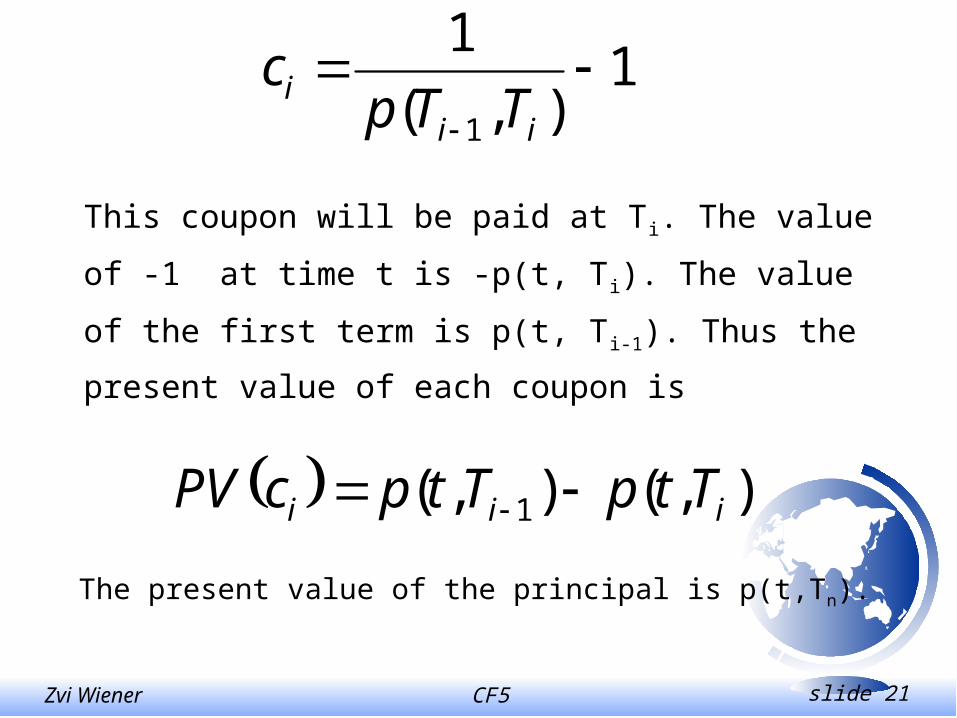

1),(

1

1

ii

i TTpc

This coupon will be paid at Ti. The value of -1 at

time t is -p(t, Ti). The value of the first term is

p(t, Ti-1). Thus the present value of each coupon

is

),(),( 1 iii TtpTtpcPV

The present value of the principal is p(t,Tn).

CF5 slide 22Zvi Wiener

The value of a floater is

n

iiin TtpTtpTtptp

11 ),(),(),()(

),()( 0Ttptp

Or after a simplification

CF5 slide 23Zvi Wiener

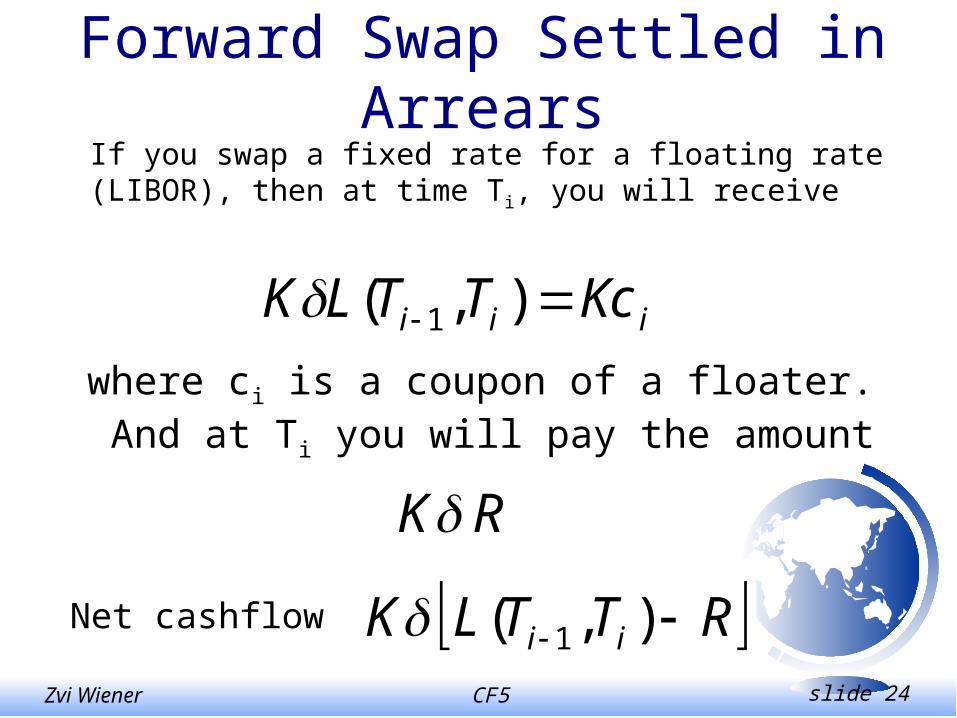

Forward Swap Settled in Arrears

K - principal, R - swap rate,

rates are set at dates T0, T1, … Tn-1 and paid at

dates T1, … Tn.

T0 T1 Tn-1 Tn

CF5 slide 24Zvi Wiener

Forward Swap Settled in Arrears

If you swap a fixed rate for a floating rate (LIBOR), then at time Ti, you will receive

iii KcTTLK ),( 1where ci is a coupon of a floater. And at Ti you will pay the amount

RK

Net cashflow RTTLK ii ),( 1

CF5 slide 25Zvi Wiener

Forward Swap Settled in Arrears

At t < T0 the value of this payment is

),()1(),( 1 ii TtpRKTtKp

The total value of the swap at time t is then

n

iii TtpRTtpKt

11 ),()1(),()(

CF5 slide 26Zvi Wiener

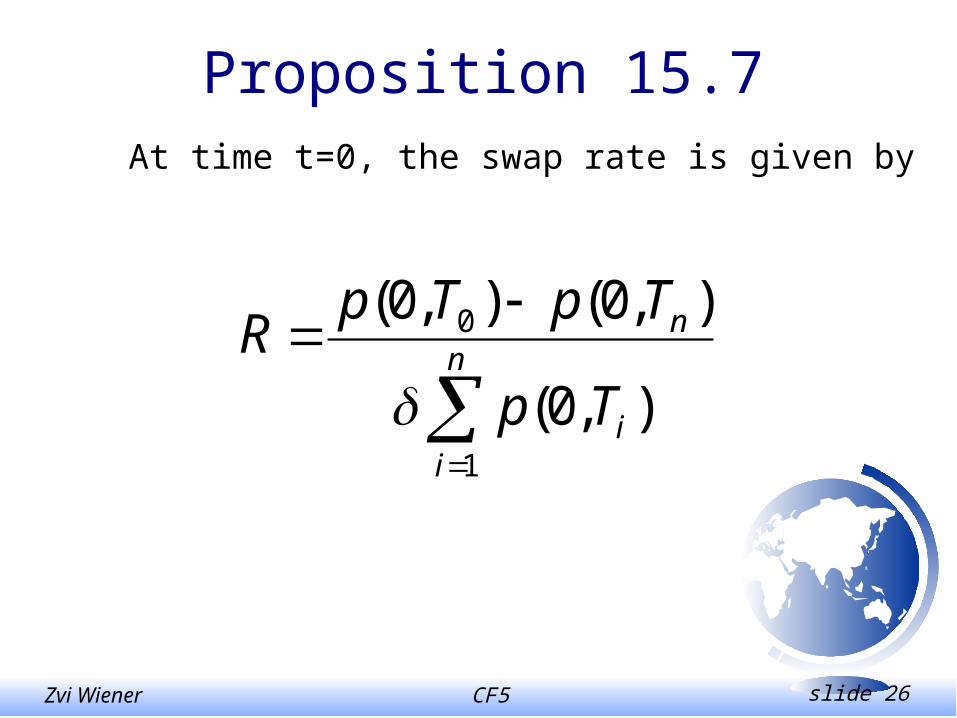

Proposition 15.7

At time t=0, the swap rate is given by

n

ii

n

Tp

TpTpR

1

0

),0(

),0(),0(

CF5 slide 27Zvi Wiener

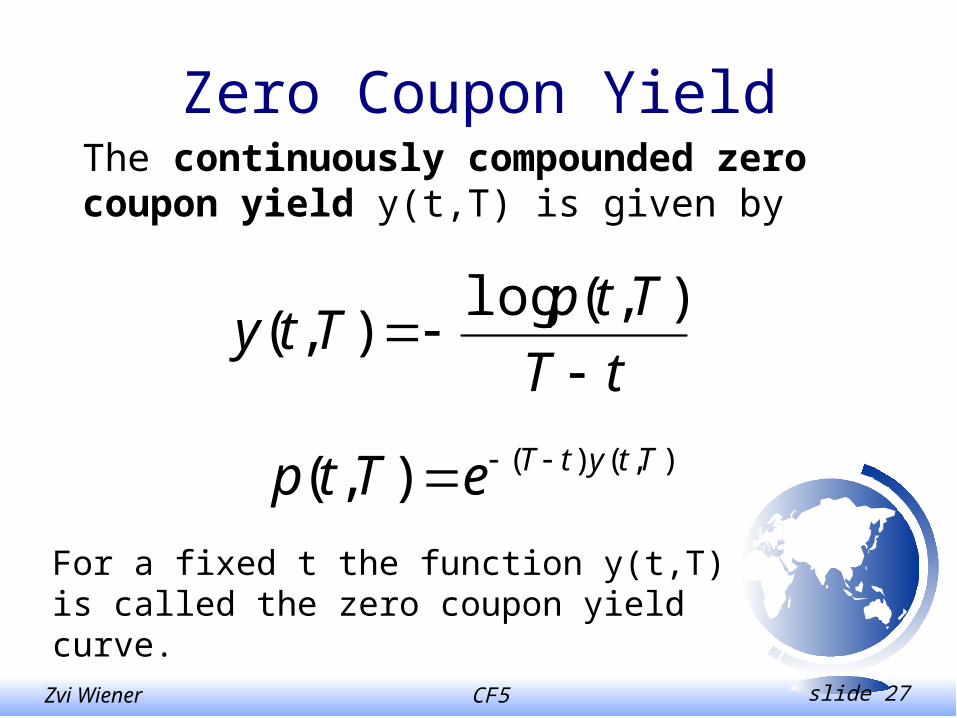

Zero Coupon YieldThe continuously compounded zero coupon yield y(t,T) is given by

tT

TtpTty

),(log),(

),()(),( TtytTeTtp

For a fixed t the function y(t,T) is called the zero coupon yield curve.

CF5 slide 28Zvi Wiener

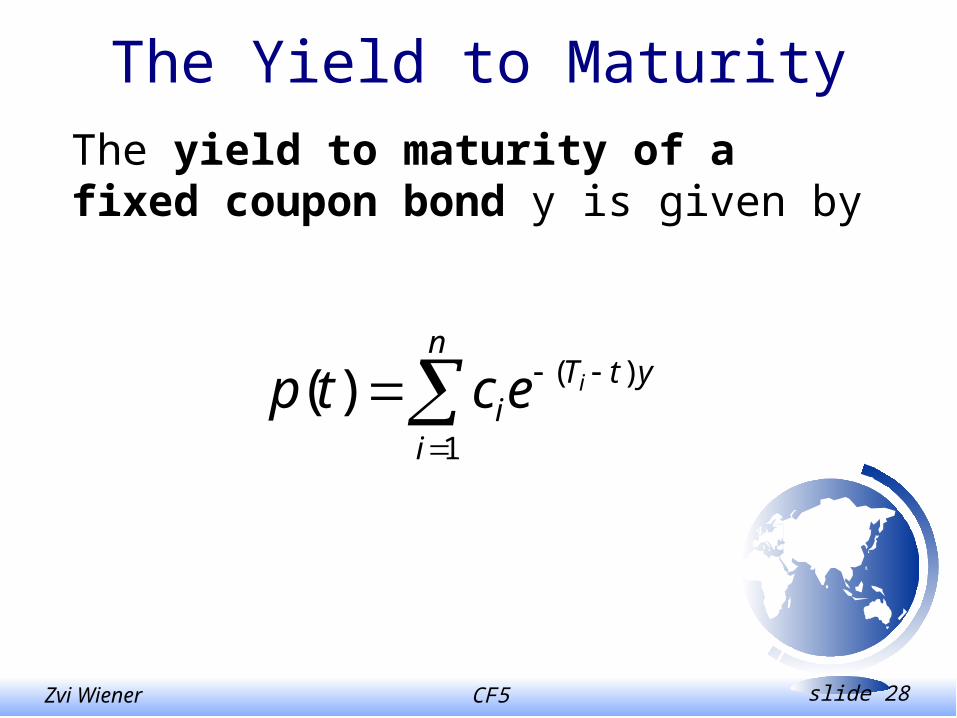

The Yield to Maturity

The yield to maturity of a fixed coupon bond y is given by

n

i

ytTi

iectp1

)()(

CF5 slide 29Zvi Wiener

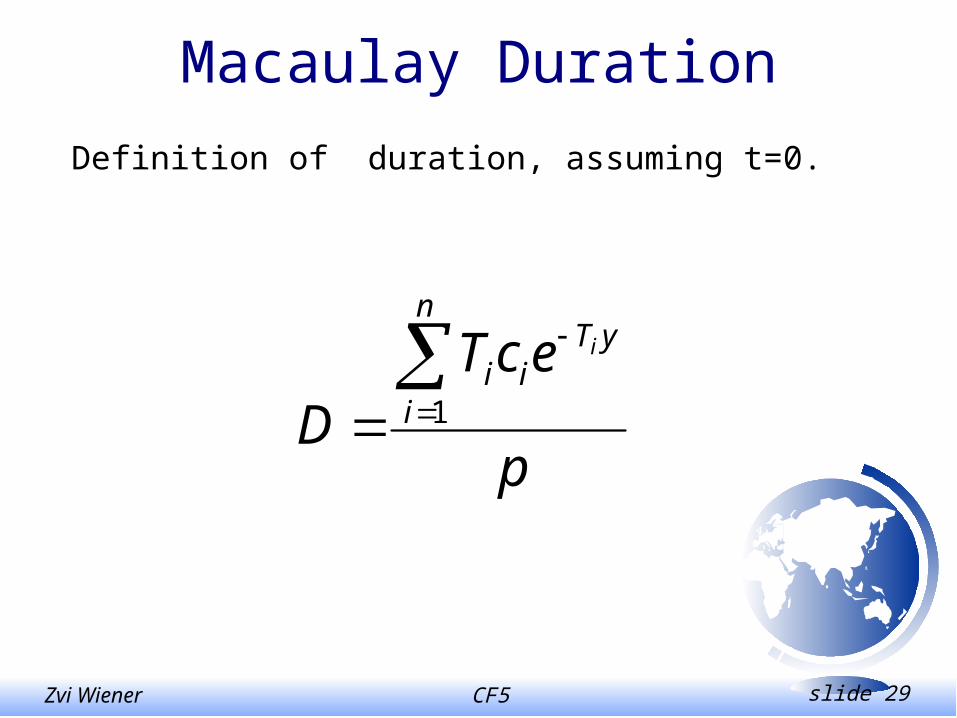

Macaulay Duration

Definition of duration, assuming t=0.

p

ecTD

n

i

yTii

i

1

CF5 slide 30Zvi Wiener

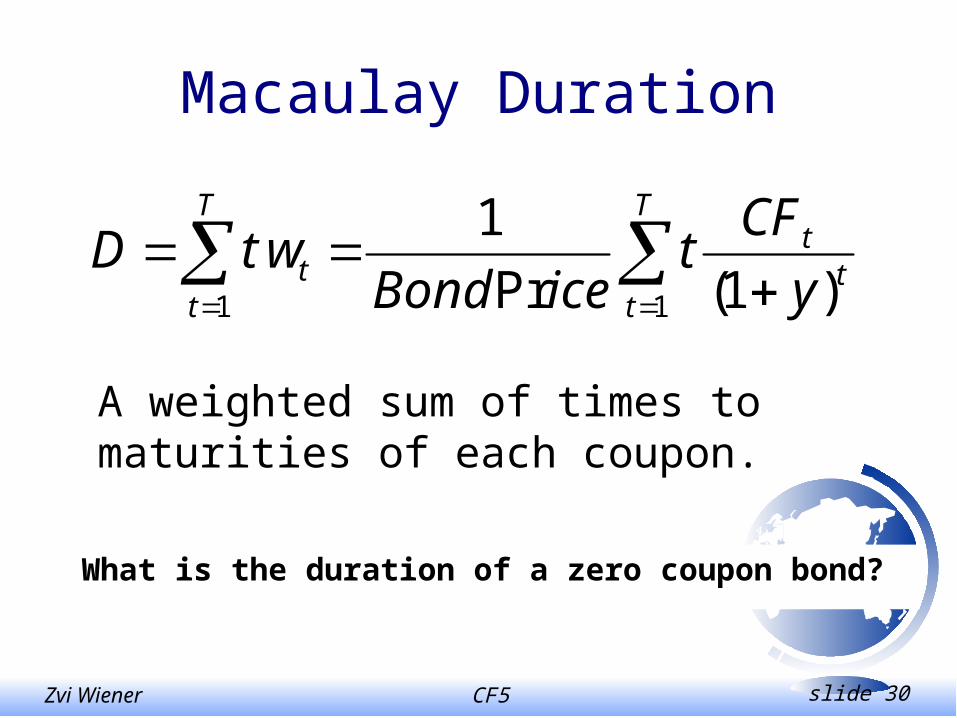

Macaulay Duration

What is the duration of a zero coupon bond?

T

tt

tT

tt y

CFt

iceBondwtD

11 )1(Pr

1

A weighted sum of times to maturities of each coupon.

CF5 slide 31Zvi Wiener

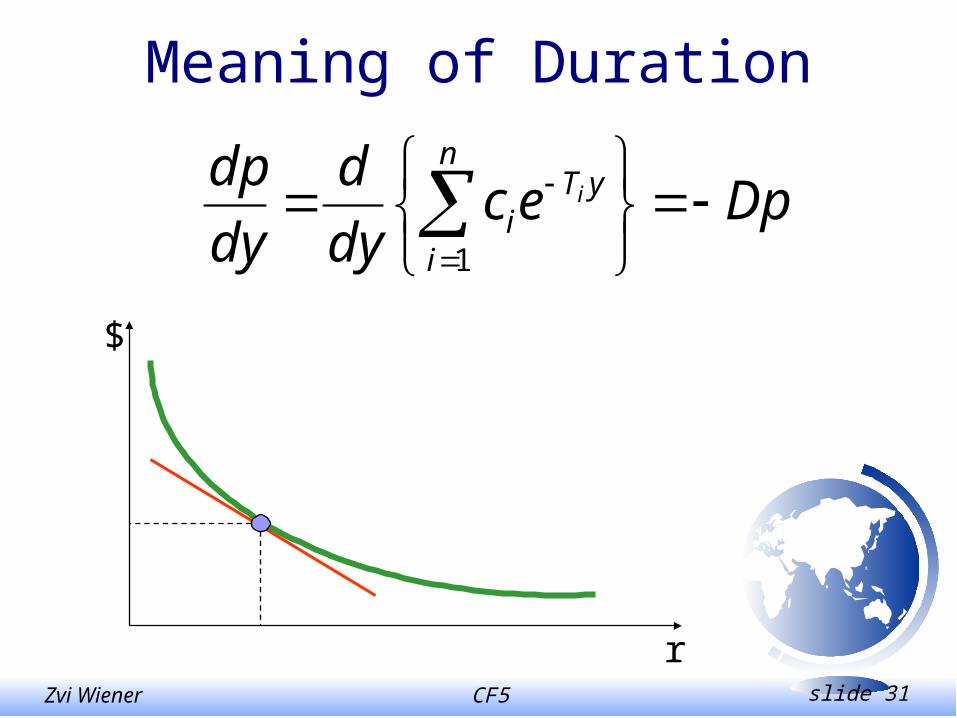

Meaning of Duration

Dpecdy

d

dy

dp n

i

yTi

i

1

r

$

CF5 slide 32Zvi Wiener

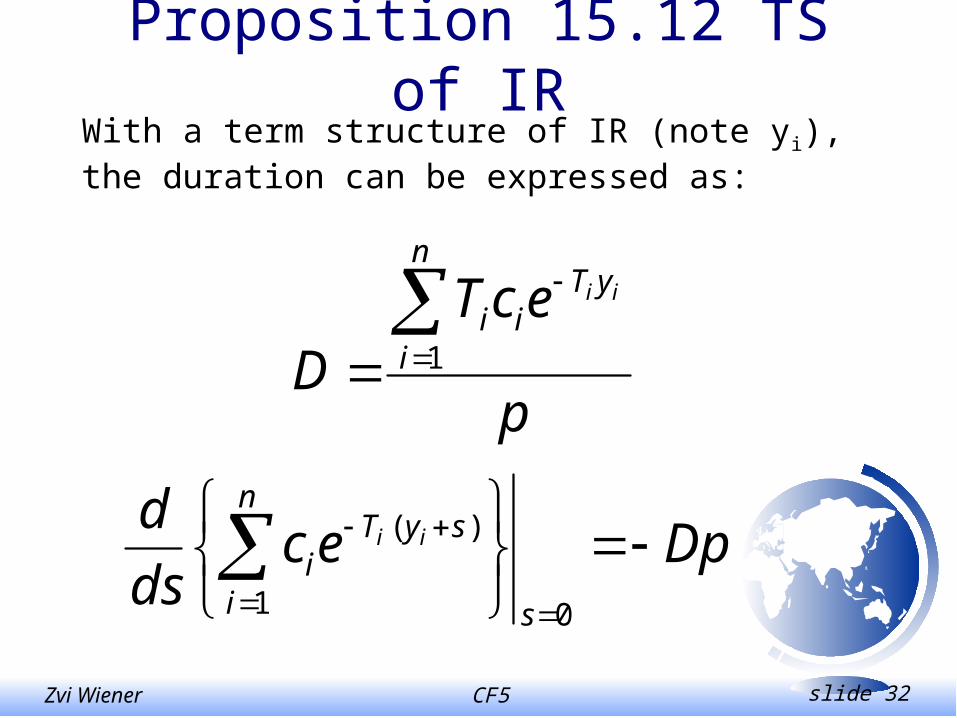

Proposition 15.12 TS of IRWith a term structure of IR (note yi), the duration can be expressed as:

Dpecds

d

s

n

i

syTi

ii

01

)(

p

ecTD

n

i

yTii

ii

1

CF5 slide 33Zvi Wiener

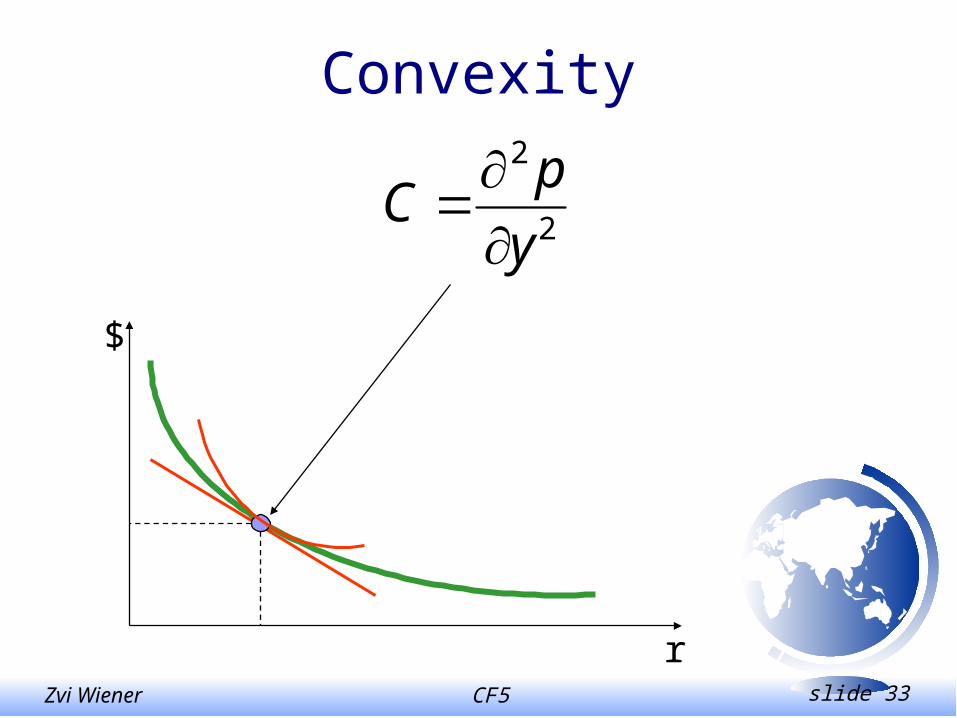

Convexity

r

$

2

2

y

pC

CF5 slide 34Zvi Wiener

FRA Forward Rate Agreement

A contract entered at t=0, where the parties (a lender and a borrower) agree to let a certain interest rate R*, act on a prespecified principal, K, over some future time period [S,T].

Assuming continuous compounding we have

at time S: -K

at time T: KeR*(T-S)

Calculate the FRA rate R* which makes PV=0hint: it is equal to forward rate

CF5 slide 35Zvi Wiener

Exercise 15.7Consider a consol bond, i.e. a bond which will forever pay one unit of cash at t=1,2,…

Suppose that the market yield is y - flat. Calculate the price of consol.

Find its duration.

Find an analytical formula for duration.

Compute the convexity of the consol.

CF-5 Bank Hapoalim Jul-2001

Following T. Bjork, ch. 19

Arbitrage Theory in Continuous Time

Change of Numeraire

CF5 slide 37Zvi Wiener

Change of Numeraire

P - the objective probability measure,

Q - the risk-neutral martingale measure,

We will introduce a new class of measures such that Q is a member of this class.

CF5 slide 38Zvi Wiener

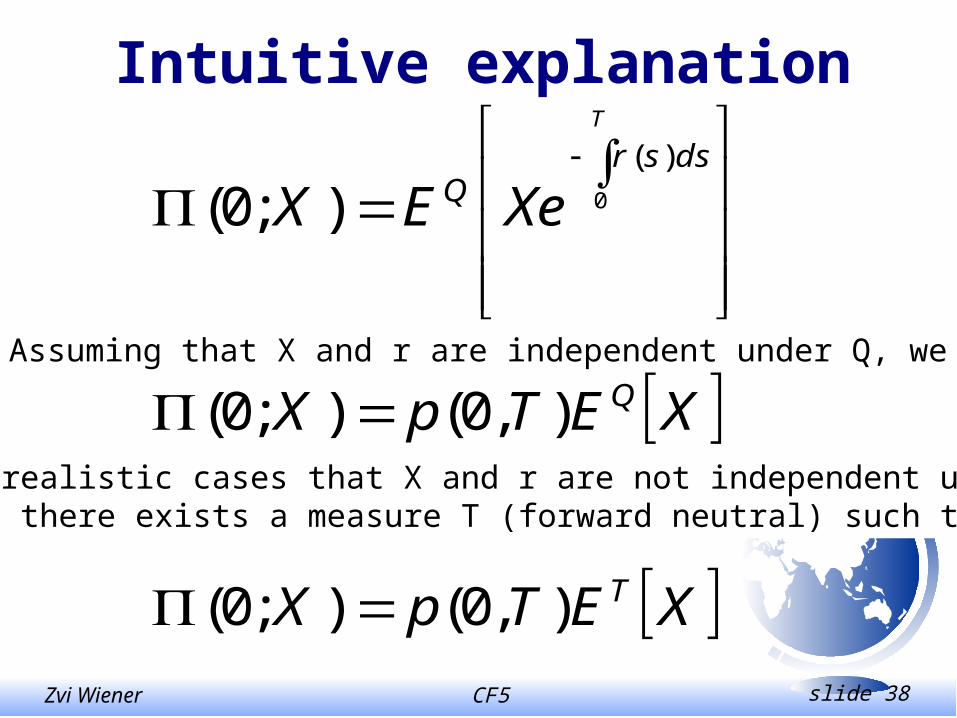

Intuitive explanation

T

dssrQ XeEX 0

)(

);0(

XETpX Q),0();0( Assuming that X and r are independent under Q, we get

In all realistic cases that X and r are not independent under Q.However there exists a measure T (forward neutral) such that

XETpX T),0();0(

CF5 slide 39Zvi Wiener

Risk Neutral Measure

Is such a measure Q that for every choice of price process (t) of a traded asset the following quotient is a Q-martingale.

)(

)(

tB

t

Note that we have divided the asset

price (t) by a numeraire B(t).

CF5 slide 40Zvi Wiener

Conjecture 19.1.1For a given financial market and any asset price process S0(t) there exists a probability measure Q0 such that for any other asset (t)/S0(t) is a Q0-martingale.

For example one can take p(t,T) (fixed T) as S0(t) then there exists a probability measure QT such that for any other asset (t)/p(t,T) is a QT-martingale.

CF5 slide 41Zvi Wiener

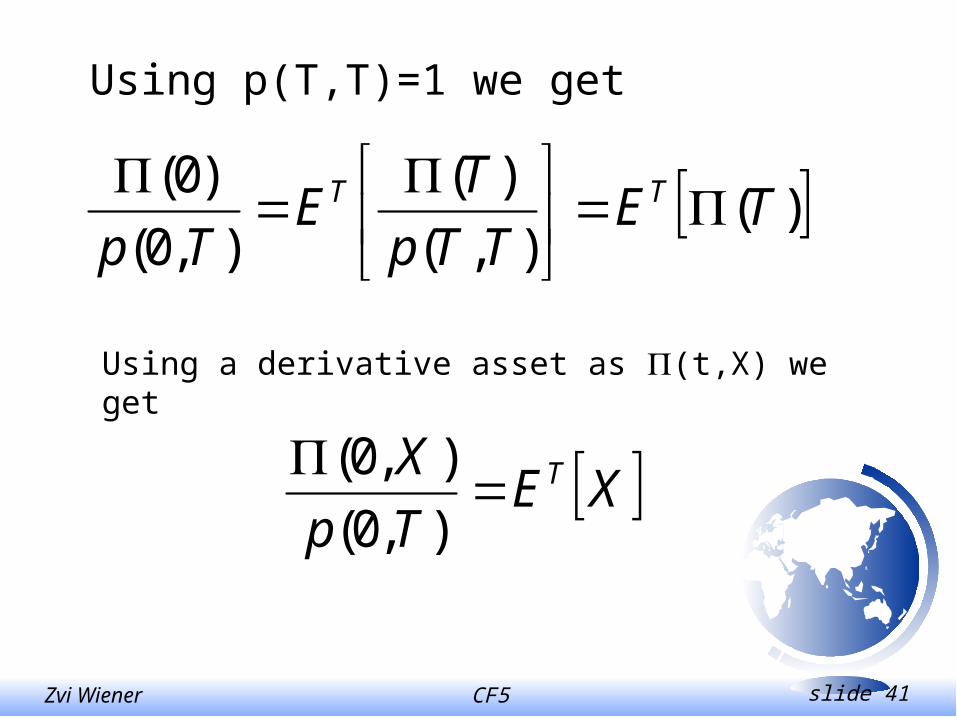

Using p(T,T)=1 we get

)(),(

)(

),0(

)0(TE

TTp

TE

TpTT

Using a derivative asset as (t,X) we get

XETp

X T

),0(

),0(

CF5 slide 42Zvi Wiener

Assumption 19.2.1

Denote an observable k+1 dimensional process X=(X1, …, Xk, Xk+1) where

Xk+1(t)=r(t) (short term IR)

Denote by Q a fixed martingale measure under which the dynamics is:

dXi(t)=i(t,X(t))dt + i(t,X(t))dW(t), i=1,…,k+1

A risk free asset (money market account):

dB(t)=r(t)B(t)dt

CF5 slide 43Zvi Wiener

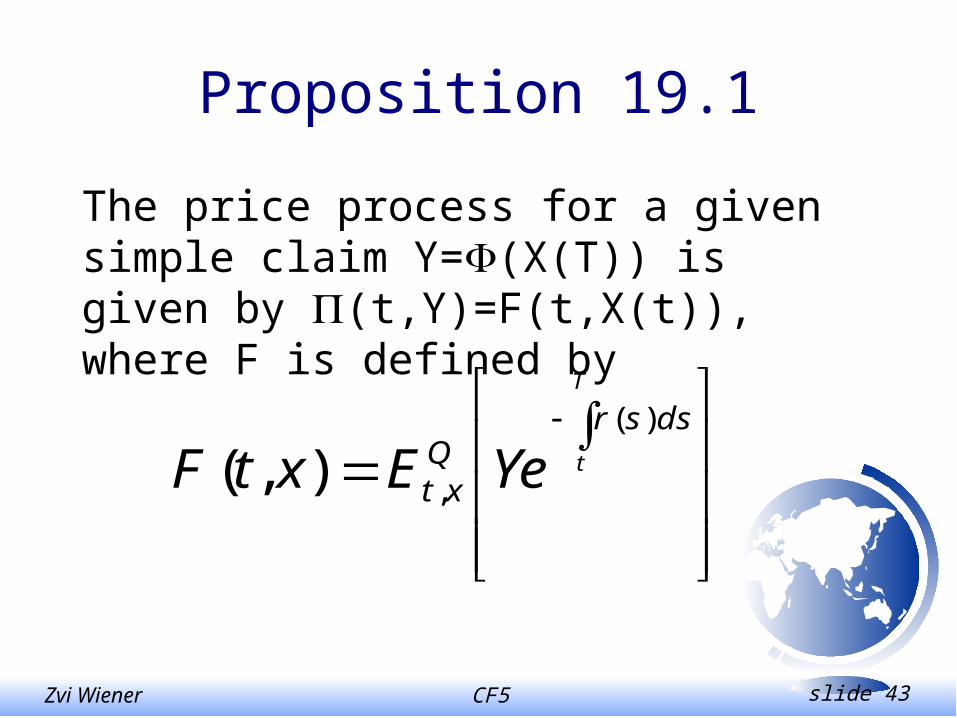

Proposition 19.1

The price process for a given simple claim Y=(X(T)) is given by (t,Y)=F(t,X(t)), where F is defined by

T

t

dssrQ

xt YeExtF)(

,),(

CF-5 Bank Hapoalim Jul-2001

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

Practical Numeraire Approach

CF5 slide 45Zvi Wiener

Options with uncertain strikeStock option with strike fixed in foreign currency.How it can be priced?

Margarbe 78 or Numeraire approach

1. Price it using this currency as a numeraire.foreign interest rateforeign current priceforeign volatility!

2. Translate the resulting price into SHEKELS using the current exchange rate.

CF5 slide 46Zvi Wiener

Options with uncertain strike

Endowment warrants

strike is increasing with short term IR.

strike is decreasing when a dividend is paid

What is an appropriate numeraire?

A closed Money Market account.

Result – price by standard BS but with 0 dividends and 0 IR.

CF5 slide 47Zvi Wiener

Options with uncertain strike

An option to choose by some date between dollar

and CPI indexing (may be with some interest).

Margrabe can be used or one can price a simple

CPI option in terms of an American investor and

then translate it to SHEKELS.

CF5 slide 48Zvi Wiener

Convertible Bonds

A convertible bond typically includes an option to convert it into some amount of ordinary shares.

This can be seen as a package of a regular bond and an option to exchange this regular bond to shares of the company.

If the company does not have traded debt there is a problem of pricing this option.

CF5 slide 49Zvi Wiener

Convertible BondsThis is an option to exchange one asset to another and can be priced with Margrabe approach.

However in order to use this approach one need to know the correlation between the two assets (stock and regular bond).

When there is no market for regular bonds this might be a problem.

CF5 slide 50Zvi Wiener

Convertible BondsAn alternative approach is with a numeraire.

Denote by

St stock price at time t,

Bt price at time t of a regular bond (may be not observable).

CBt price of a convertible bond.

C - value of the conversion option, so that

CB = C(B) + B at any time

CF5 slide 51Zvi Wiener

Convertible BondsNote that C is a decreasing function of B (the higher the strike price, the lower is the option’s value).

This means that as soon as

CBt < St = C(B=0) the right hand side of the following equation (B - an unknown)

CBt = C(Bt) + Bt

has a unique solution.

CF5 slide 52Zvi Wiener

Convertible BondsThe left hand side is a known constant, the right hand side is a sum of two variables.

The first one is decreasing in B, but its derivative is strictly less than one and approaches zero for large B.

The second one is linear with slope one.

This means that as soon as CB>C(B=0)+0=S there exists a unique solution.

CF5 slide 53Zvi Wiener

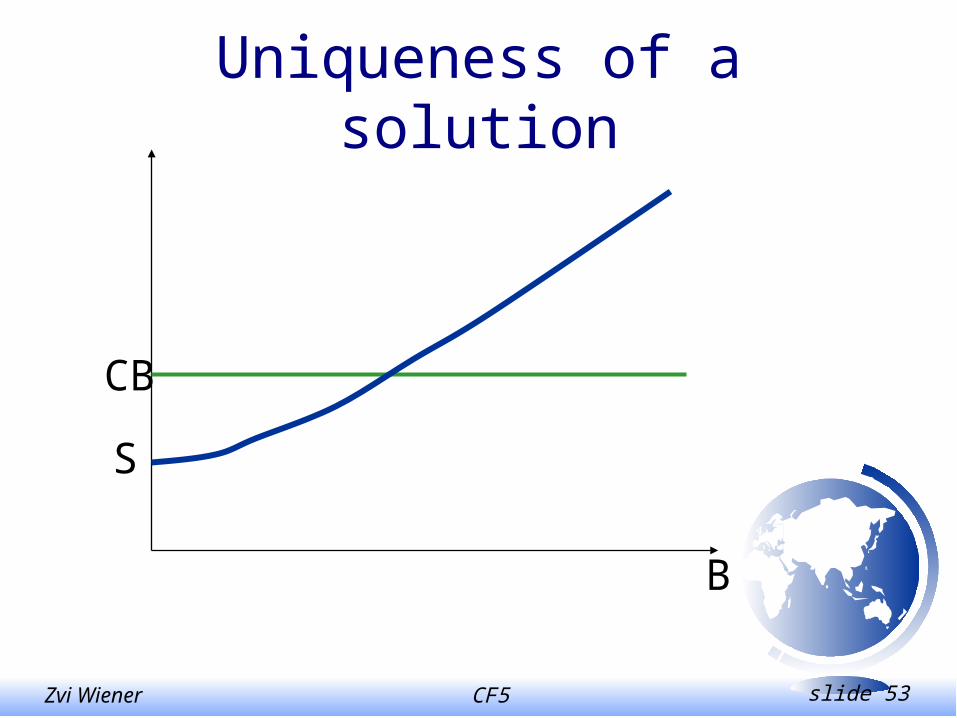

Uniqueness of a solution

B

CB

S

CF5 slide 54Zvi Wiener

Pricing with known volatility

Let’s use Bt as a numeraire, then the stochastic variable is St/Bt.

Assume that St/Bt has a constant volatility .

Then this option has a fixed strike (in terms of B) and is equivalent to a standard option, which can be priced with BS equation.

Call(St/Bt, T, 1, , r) (in terms of Bt),

the dollar value is then BtCall(St/Bt, T, 1, , r).

CF5 slide 55Zvi Wiener

Pricing with known volatility

This means that when is known the option can be priced easily and consequently the straight bond.

However that we need can not be observed. The solution is in the following procedure.

CF5 slide 56Zvi Wiener

Pricing with known volatility

Assume that is stable but unknown. For any value of we can easily price the option at any date, and hence we can also derive the value of Bt.

Take a sequence of historical data (meaning St and CBt). For any value of we can construct the implied Bt().

Then using these sequence of observations we can check whether the volatility of St/Bt is indeed .

If our guess of was correct this is true.

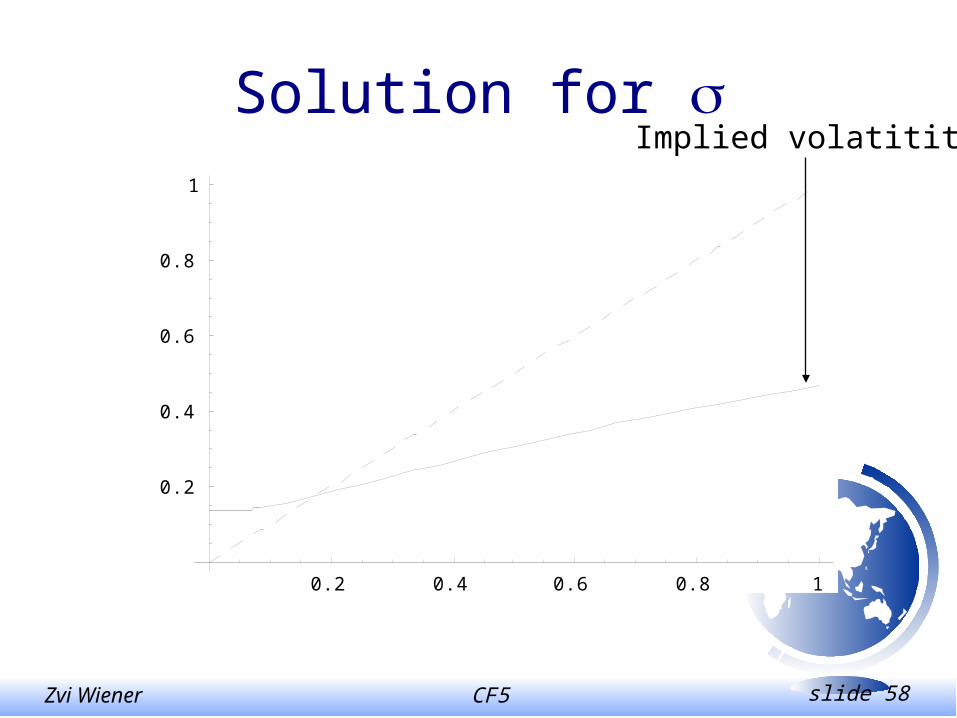

CF5 slide 57Zvi Wiener

Pricing with known volatility

However there is no reason why some value of will give the same implied historical volatility. This means that we have to solve for such that the implied volatility is equal .

Numerically this can be done easily.

Why there exists a unique solution???

Check monotonicity!!

CF5 slide 58Zvi Wiener

Solution for

0.2 0.4 0.6 0.8 1

0.2

0.4

0.6

0.8

1

Implied volatitity

CF5 slide 59Zvi Wiener

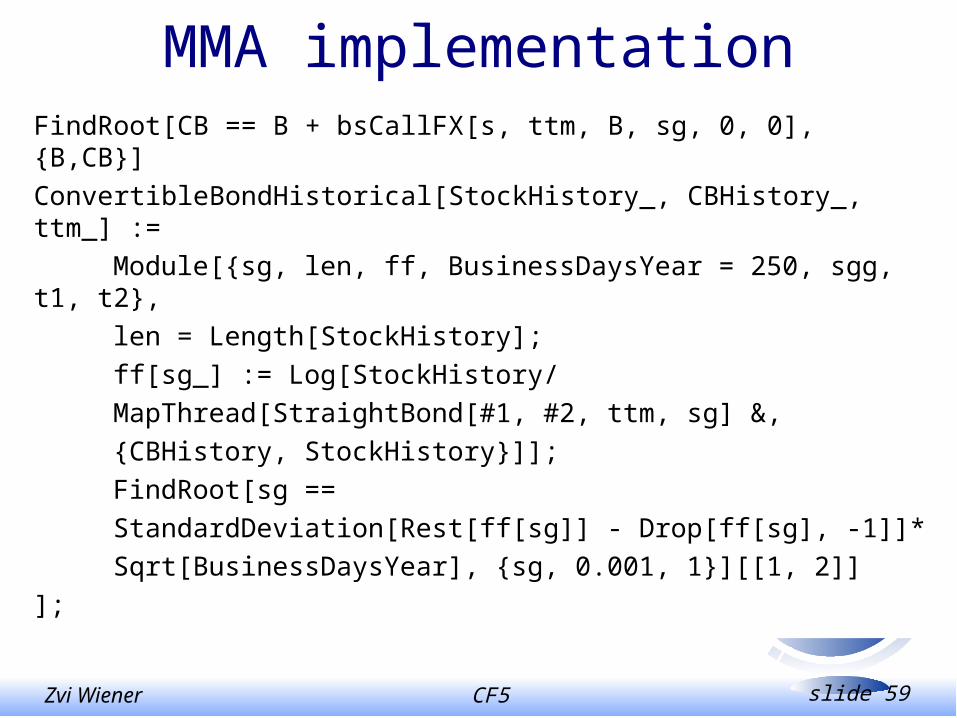

MMA implementationFindRoot[CB == B + bsCallFX[s, ttm, B, sg, 0, 0], {B,CB}]

ConvertibleBondHistorical[StockHistory_, CBHistory_, ttm_] :=

Module[{sg, len, ff, BusinessDaysYear = 250, sgg, t1, t2},

len = Length[StockHistory];

ff[sg_] := Log[StockHistory/

MapThread[StraightBond[#1, #2, ttm, sg] &,

{CBHistory, StockHistory}]];

FindRoot[sg ==

StandardDeviation[Rest[ff[sg]] - Drop[ff[sg], -1]]*

Sqrt[BusinessDaysYear], {sg, 0.001, 1}][[1, 2]]

];

CF5 slide 60Zvi Wiener

20 40 60 80 100

0.9

0.95

1.05

1.1

1.15

Example 1CB

S

B

CF5 slide 61Zvi Wiener

20 40 60 80 100

0.75

0.85

0.9

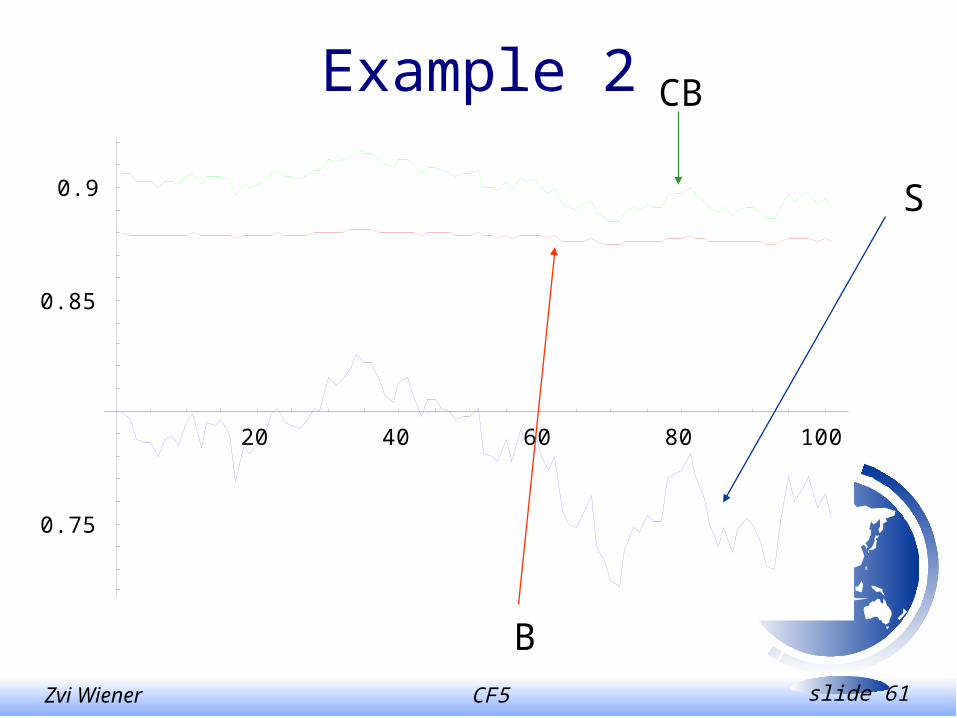

Example 2 CB

S

B

CF-5 Bank Hapoalim Jul-2001

Zvi Wiener

The Hebrew University of Jerusalem

Value of Value-at-Risk

CF5 slide 63Zvi Wiener

P&L

VaR

1 day

1% probability 1d

1 week

1% probability 1w

CF5 slide 64Zvi Wiener

Model

• Bank’s choice of an optimal system

• Depends on the available capital

• Current and potential capital needs

• Queuing model as a base

CF5 slide 65Zvi Wiener

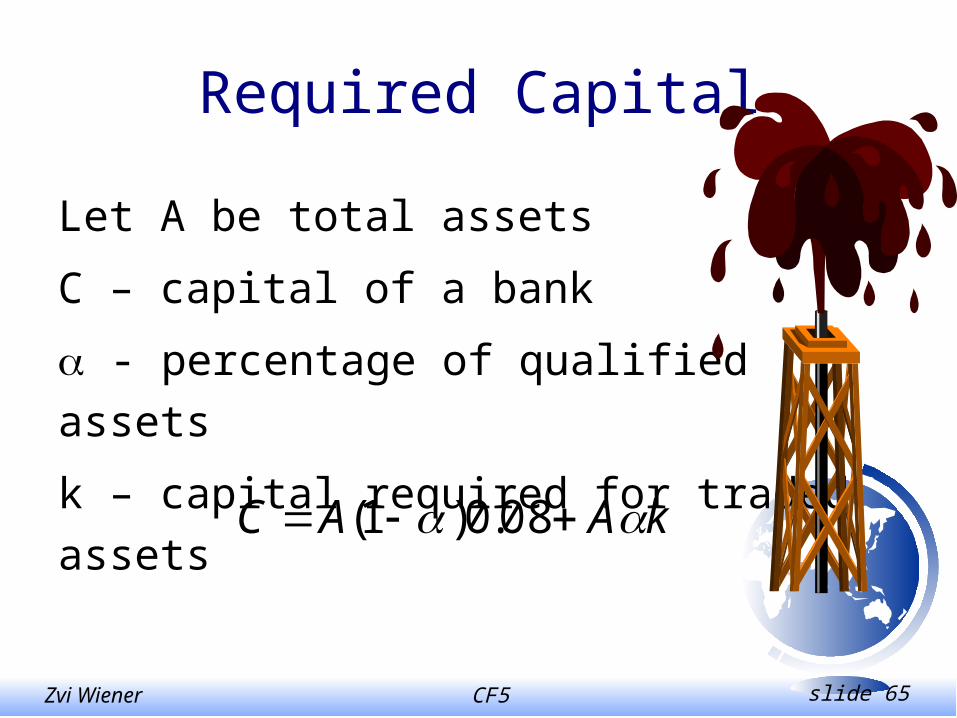

Required Capital

Let A be total assets

C – capital of a bank

- percentage of qualified assets

k – capital required for traded assets

kAAC 08.0)1(

CF5 slide 66Zvi Wiener

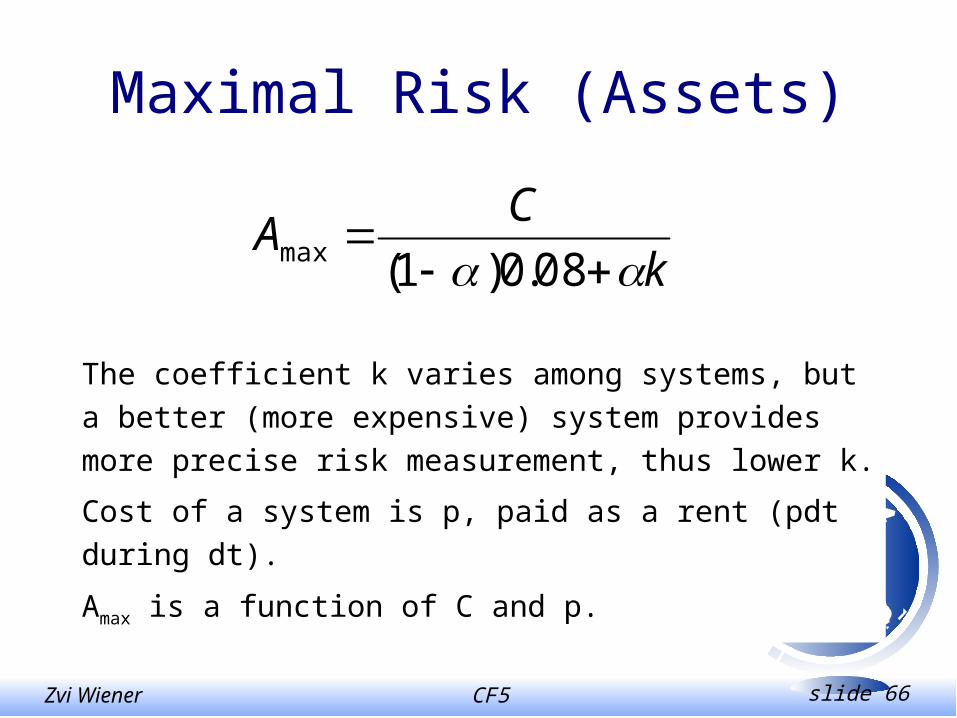

Maximal Risk (Assets)

The coefficient k varies among systems, but a better

(more expensive) system provides more precise risk

measurement, thus lower k.

Cost of a system is p, paid as a rent (pdt during dt).

Amax is a function of C and p.

k

CA

08.0)1(max

CF5 slide 67Zvi Wiener

Risky Projects

Deposits arrive and are withdrawn randomly.

All deposits are of the same size.

Invested according to bank’s policy.

Can not be used if capital requirements are

not satisfied.

CF5 slide 68Zvi Wiener

Arrival of Risky ProjectsWe assume that risky projects arrive randomly (as a Poisson process with density ).

This means that there is a probability dt that during dt one new project arrives.

CF5 slide 69Zvi Wiener

Arrival of Risky ProjectsA new project is undertaken if the bank has enough capital (according to the existing risk measuring system).

We assume that one can NOT raise capital or change systems quickly.

CF5 slide 70Zvi Wiener

Termination of Risky Projects

We assume that each risky project disappears randomly (as a Poisson process with density ).

CF5 slide 71Zvi Wiener

Termination of Risky Projects

We assume that each risky project disappears randomly (as a Poisson process with density ).

This means that there is a probability ndt that during dt one out of n existing projects terminates.

With probability (1-ndt) all existing projects will be active after dt.

CF5 slide 72Zvi Wiener

ProfitWe assume that each existing risky project gives a profit of dt during dt.

Thus when there are n active projects the bank has instantaneous profit (n-p)dt.

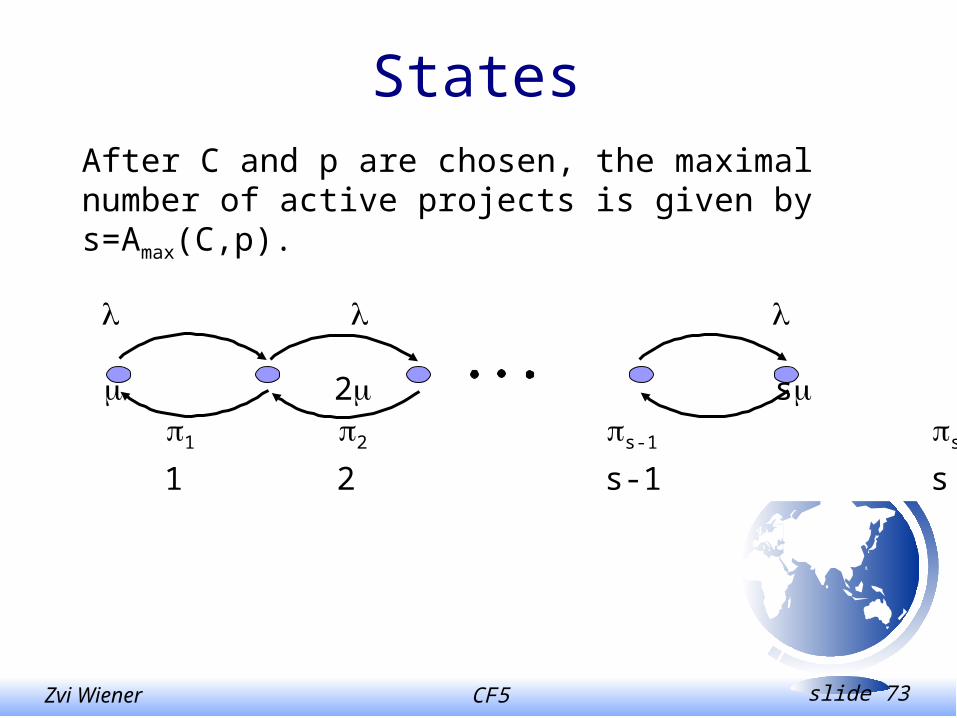

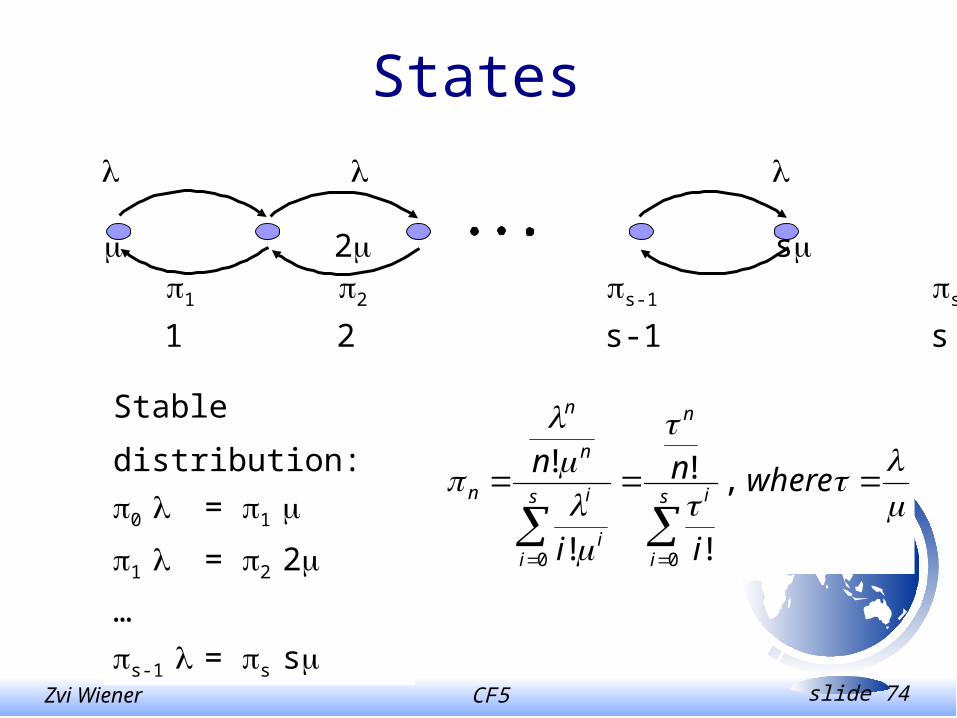

CF5 slide 73Zvi Wiener

States

After C and p are chosen, the maximal number of active projects is given by s=Amax(C,p).

0 1 2 s-1 s

0 1 2 s-1 s

2 s

CF5 slide 74Zvi Wiener

States

0 1 2 s-1 s

0 1 2 s-1 s

2 s

Stable distribution:

0 = 1

1 = 2 2

…

s-1 = s s

where

i

n

i

ns

i

i

n

s

ii

i

n

n

n ,

!

!

!

!

00

CF5 slide 75Zvi Wiener

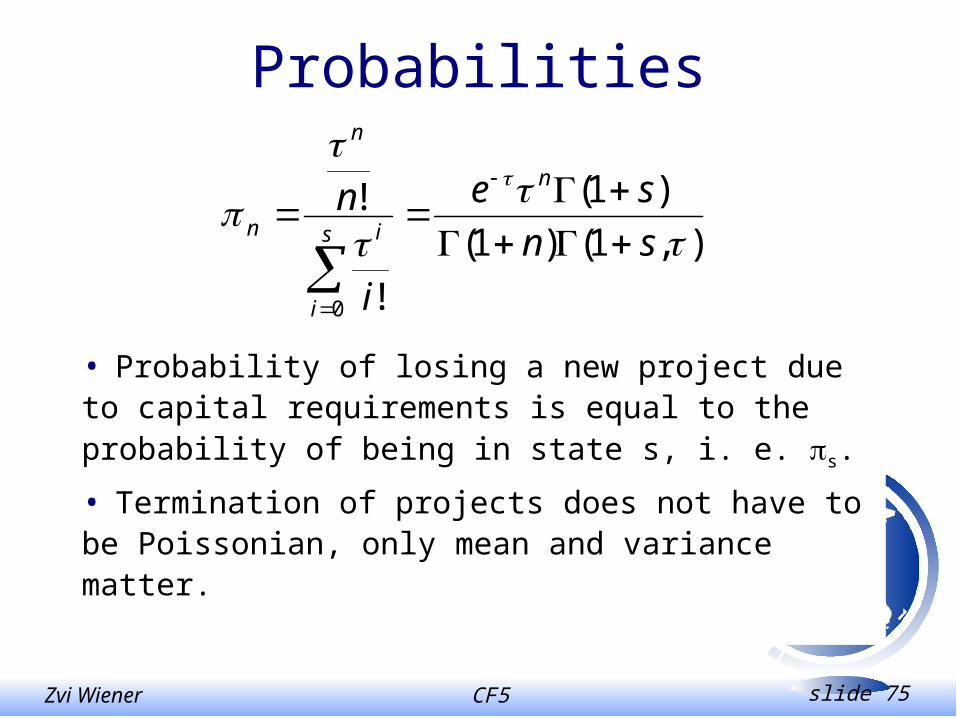

Probabilities

• Probability of losing a new project due to capital requirements is equal to the probability of being in state s, i. e. s.

• Termination of projects does not have to be Poissonian, only mean and variance matter.

),1()1(

)1(

!

!

0

sn

se

i

nn

s

i

i

n

n

CF5 slide 76Zvi Wiener

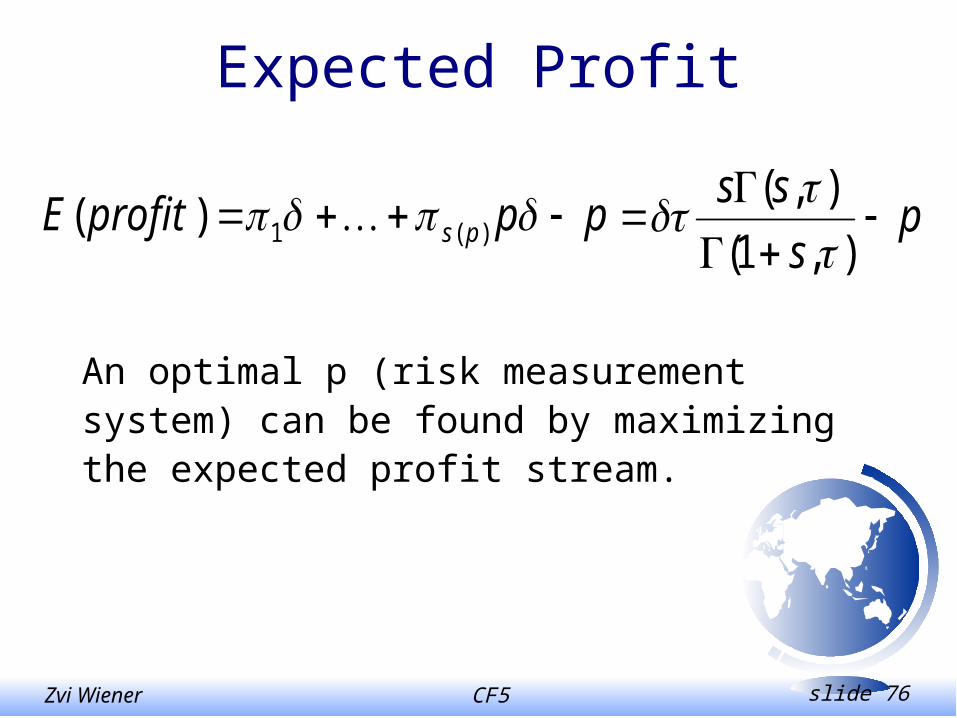

Expected Profit

An optimal p (risk measurement system) can be found by maximizing the expected profit stream.

ppprofitE ps )(1)( ps

ss

),1(

),(

CF5 slide 77Zvi Wiener

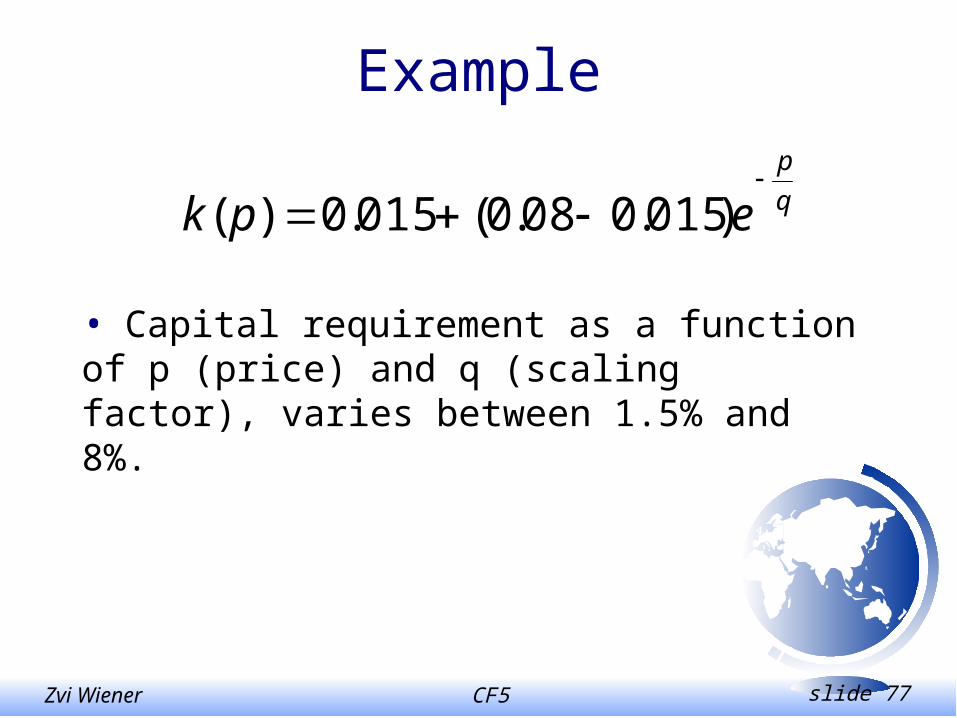

Example

• Capital requirement as a function of p (price) and q (scaling factor), varies between 1.5% and 8%.

q

p

epk

)015.008.0(015.0)(

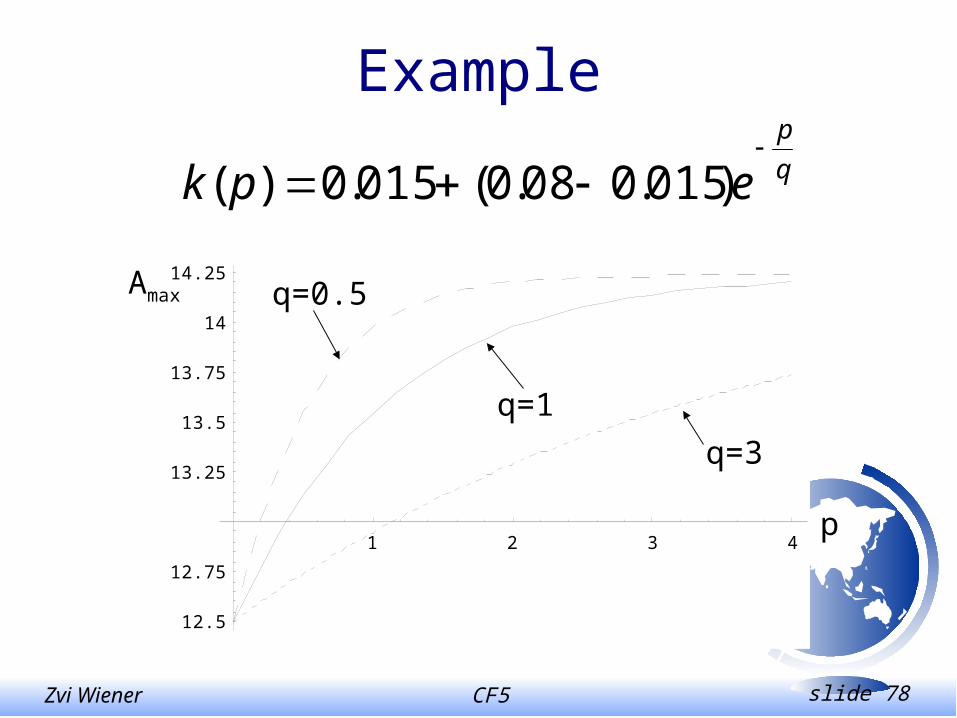

CF5 slide 78Zvi Wiener

Example

q

p

epk

)015.008.0(015.0)(

1 2 3 4

12.5

12.75

13.25

13.5

13.75

14

14.25q=0.5

q=1

q=3

p

Amax

CF5 slide 79Zvi Wiener

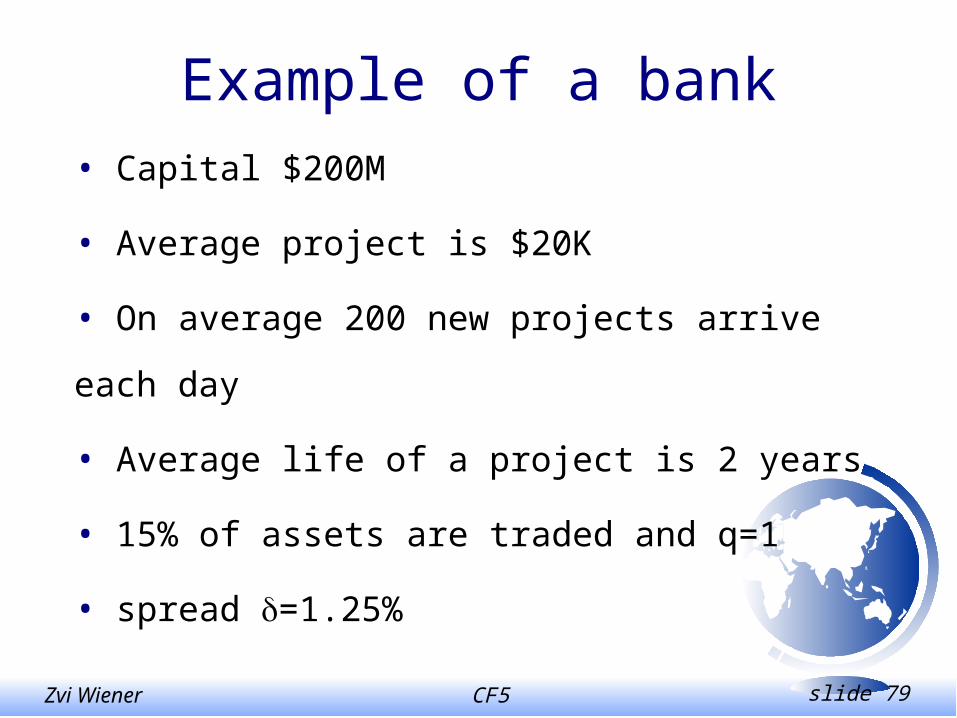

Example of a bank

• Capital $200M

• Average project is $20K

• On average 200 new projects arrive each day

• Average life of a project is 2 years

• 15% of assets are traded and q=1

• spread =1.25%

CF5 slide 80Zvi Wiener

Bank’s profit as a function of cost p. C=$200M, arrival rate 200/d,size $20K, average life 2 yr.,

spread 1.25%, q=1, 15% of assets are traded.

1 2 3 4 5 629.5

30.5

31

31.5

32

32.5

33

rent p

Expected profit

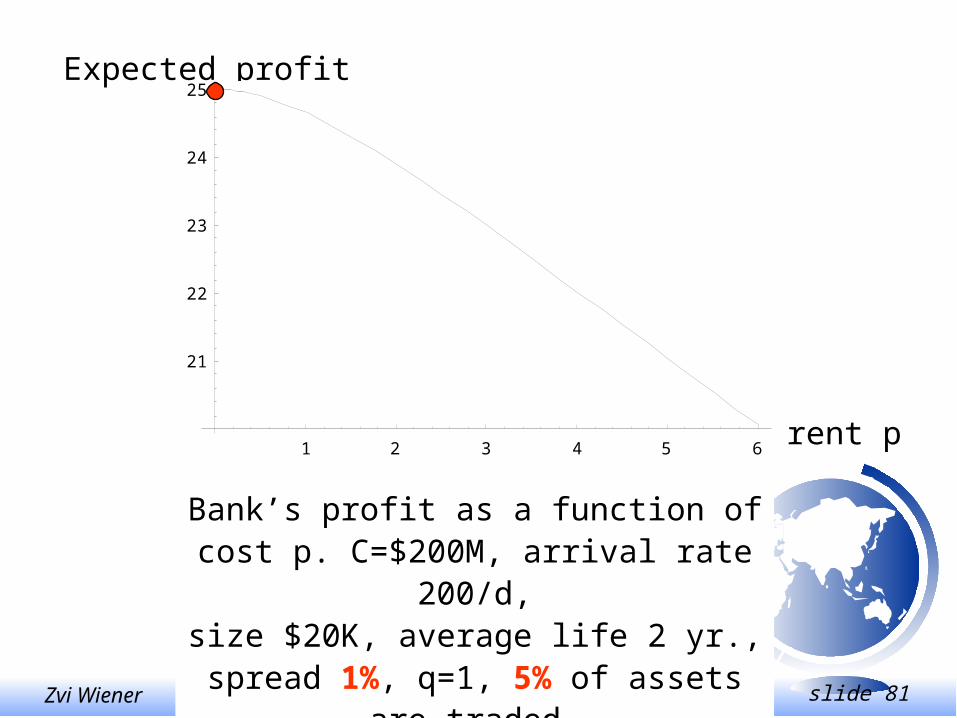

CF5 slide 81Zvi Wiener

rent p

Expected profit

1 2 3 4 5 6

21

22

23

24

25

Bank’s profit as a function of cost p. C=$200M, arrival rate 200/d,size $20K, average life 2 yr.,

spread 1%, q=1, 5% of assets are traded.

CF5 slide 82Zvi Wiener

Conclusion• Expensive systems are appropriate for banks with

• low capitalization

• operating in an unstable environment

• Cheaper methods (like the standard approach) should be appropriate for banks with

• high capitalization

• small trading book

• operating in a stable environment• many small uncorrelated, long living projects

CF5 slide 83Zvi Wiener

A simple intuitive and flexible model of

optimal choice of risk measuring method.

CF-5 Bank Hapoalim Jul-2001

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

DAC

CF5 slide 85Zvi Wiener

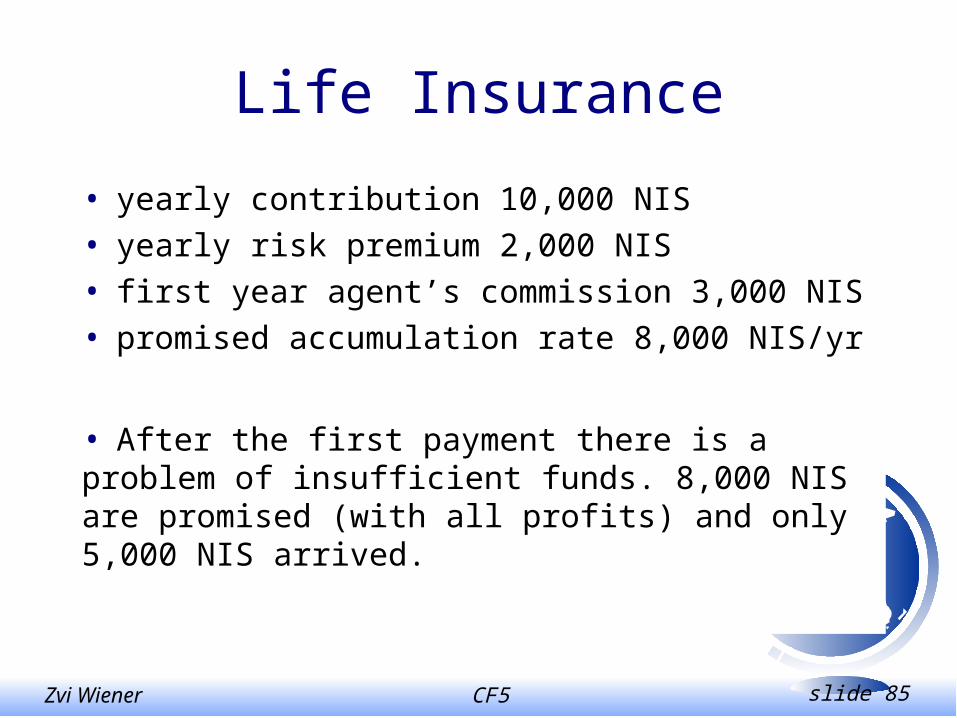

Life Insurance

• yearly contribution 10,000 NIS

• yearly risk premium 2,000 NIS

• first year agent’s commission 3,000 NIS

• promised accumulation rate 8,000 NIS/yr

• After the first payment there is a problem of insufficient funds. 8,000 NIS are promised (with all profits) and only 5,000 NIS arrived.

CF5 slide 86Zvi Wiener

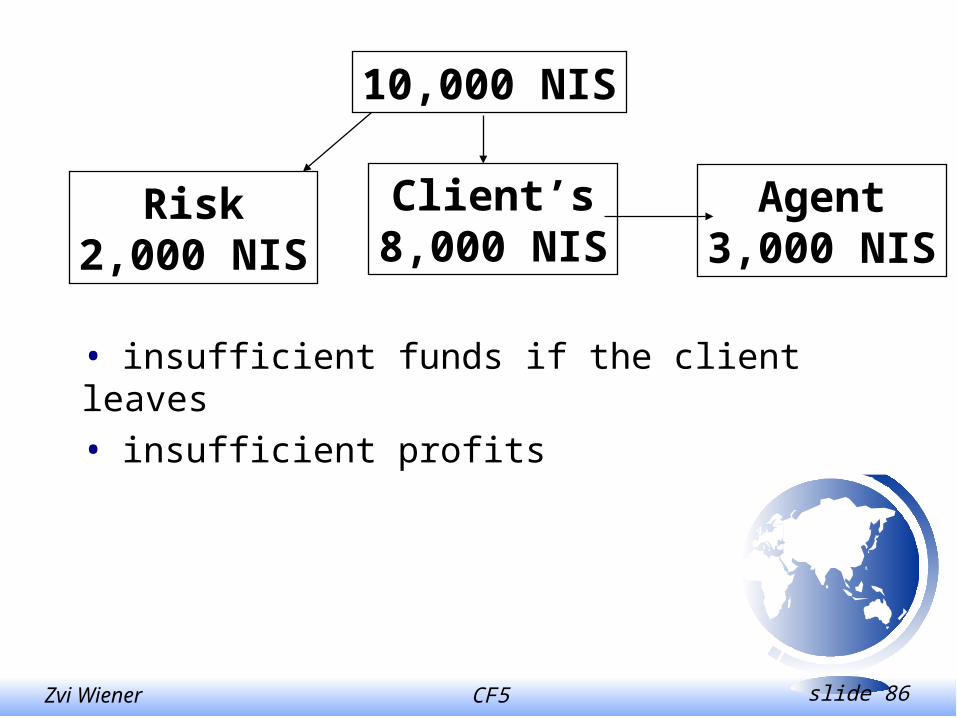

10,000 NIS

Risk2,000 NIS

Client’s8,000 NIS

Agent3,000 NIS

• insufficient funds if the client leaves

• insufficient profits

CF5 slide 87Zvi Wiener

Risk measurement

• The reason to enter this transaction is because of the expected future profits.

• Assume that the program is for 15 years and the probability of leaving such a program is .

• Fees are • 0.6% of the portfolio value each year

• 15% real profit participation

CF5 slide 88Zvi Wiener

Obligations

• The most important question is what are the

obligations?

• The Ministry of Finance should decide

• Transparent to a client

• Accounted as a loan

CF5 slide 89Zvi Wiener

One year example

Assume that the program is for one year only

and there is no possibility to stop payments

before the end.

Initial payment P0, fees lost L0, fixed fee a%

of the final value P1, participation fee b% of

real profits (we ignore real).

Investment policy TA-25 (MAOF).

CF5 slide 90Zvi Wiener

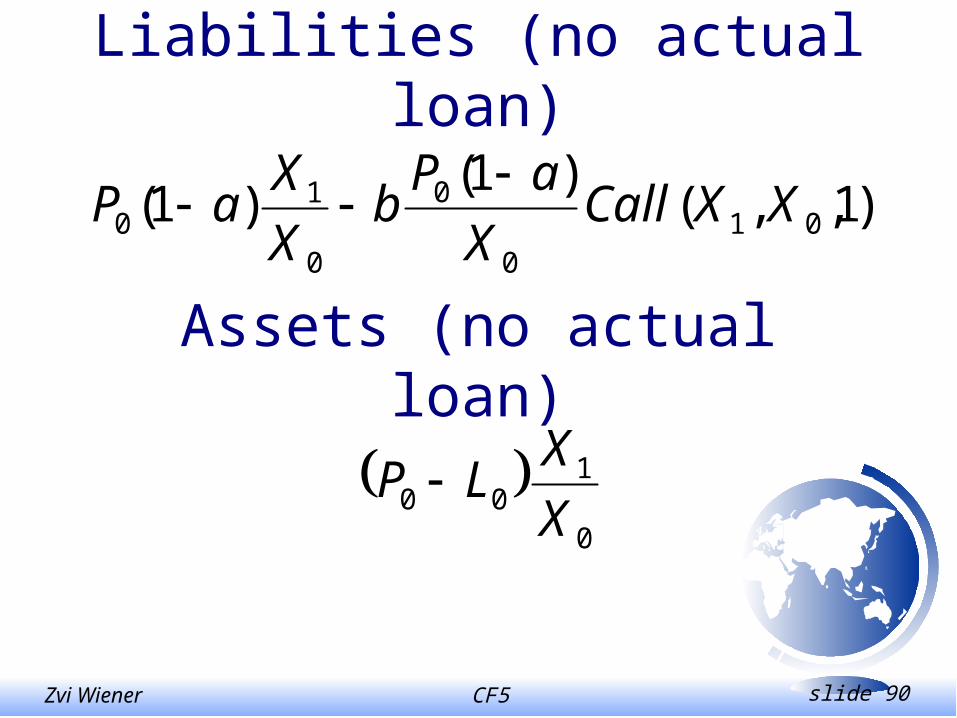

Liabilities (no actual loan)

)1,,()1(

)1( 010

0

0

10 XXCall

X

aPb

X

XaP

Assets (no actual loan)

0

100 X

XLP

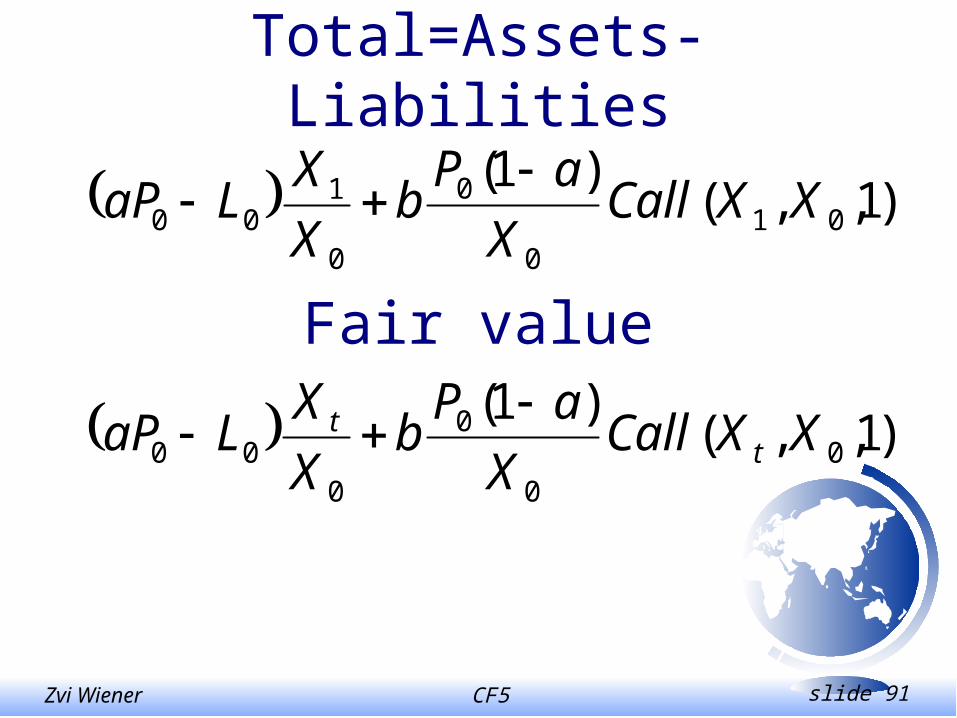

CF5 slide 91Zvi Wiener

Total=Assets-Liabilities

)1,,()1(

010

0

0

100 XXCall

X

aPb

X

XLaP

Fair value

)1,,()1(

00

0

000 XXCall

X

aPb

X

XLaP t

t

CF5 slide 92Zvi Wiener

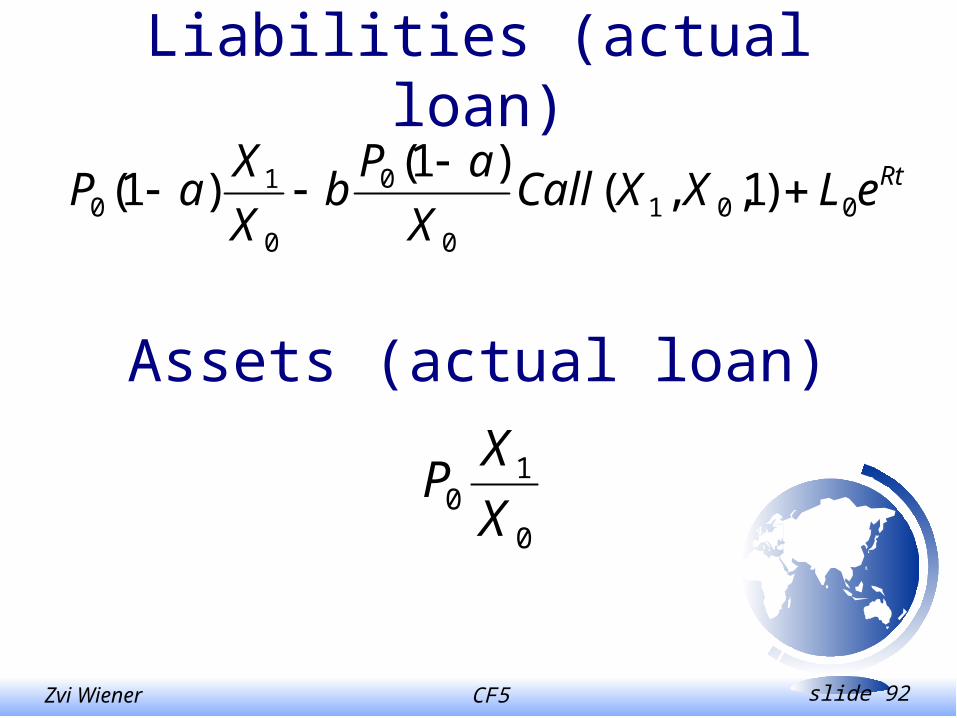

Liabilities (actual loan)

RteLXXCallX

aPb

X

XaP 001

0

0

0

10 )1,,(

)1()1(

Assets (actual loan)

0

10 X

XP

CF5 slide 93Zvi Wiener

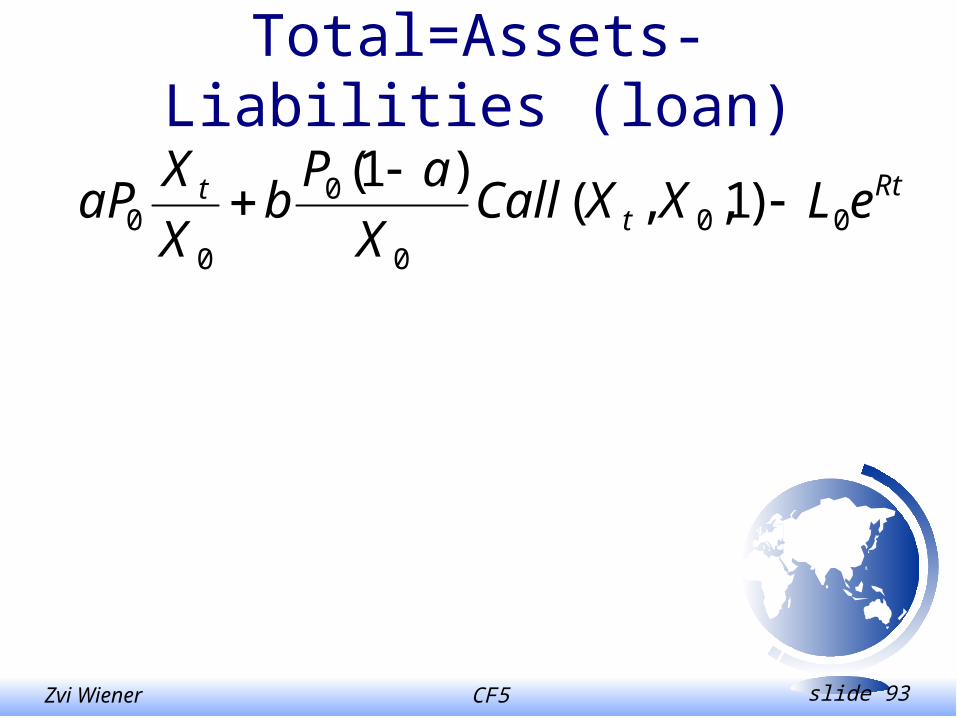

Total=Assets-Liabilities (loan)

Rtt

t eLXXCallX

aPb

X

XaP 00

0

0

00 )1,,(

)1(

CF5 slide 94Zvi Wiener

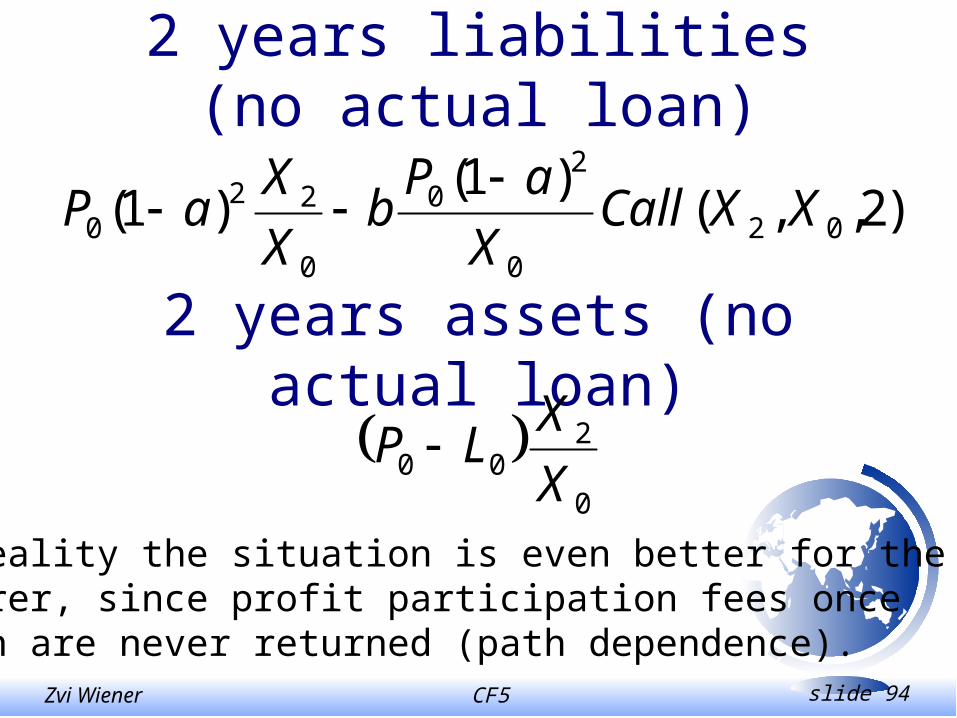

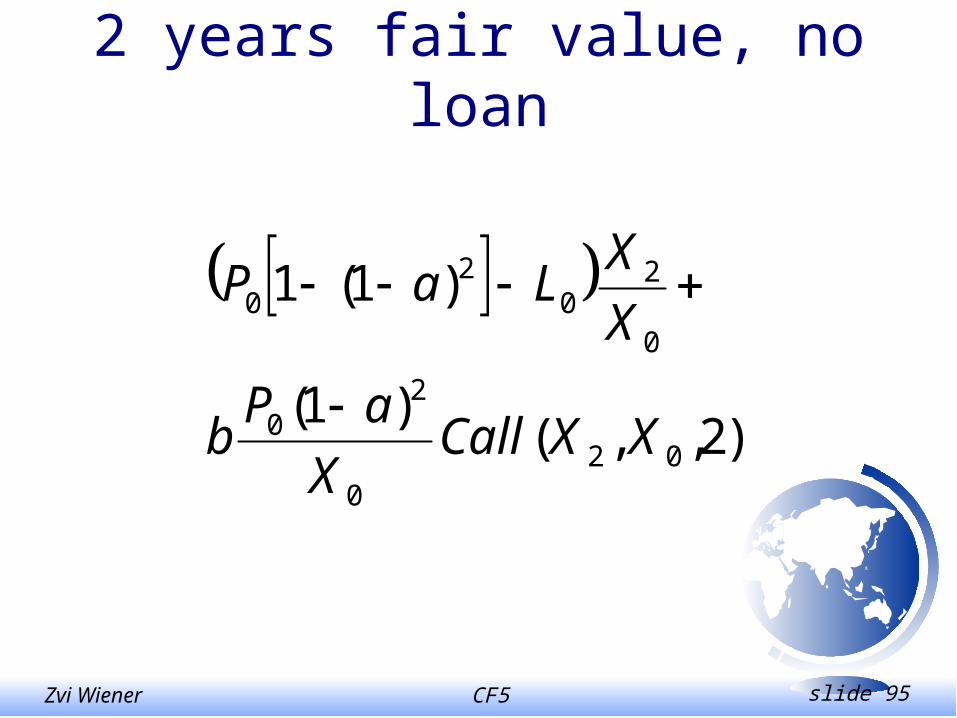

2 years liabilities (no actual loan)

)2,,()1(

)1( 020

20

0

220 XXCall

X

aPb

X

XaP

2 years assets (no actual loan)

0

200 X

XLP

In reality the situation is even better for theinsurer, since profit participation fees oncetaken are never returned (path dependence).

CF5 slide 95Zvi Wiener

2 years fair value, no loan

)2,,()1(

)1(1

020

20

0

20

20

XXCallX

aPb

X

XLaP

CF5 slide 96Zvi Wiener

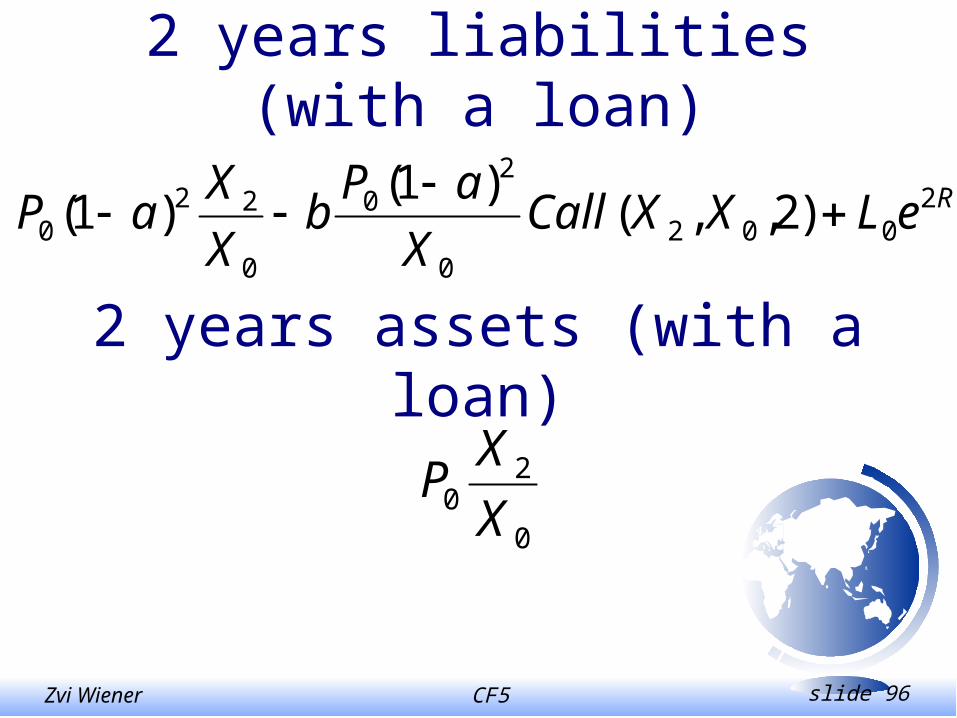

2 years liabilities (with a loan)

ReLXXCallX

aPb

X

XaP 2

0020

20

0

220 )2,,(

)1()1(

2 years assets (with a loan)

0

20 X

XP

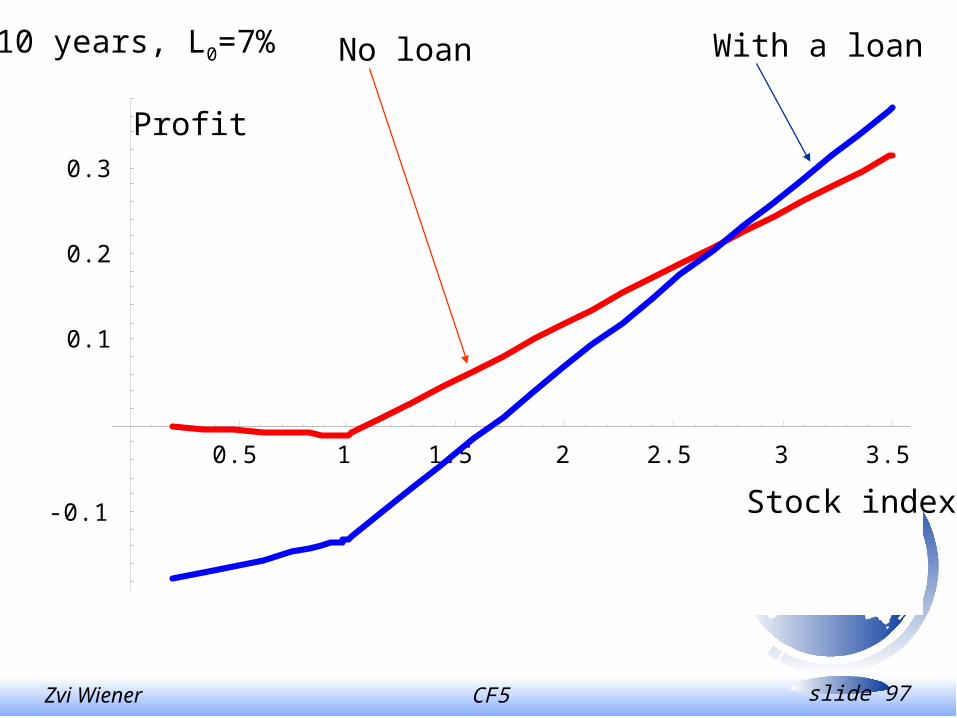

CF5 slide 97Zvi Wiener

0.5 1 1.5 2 2.5 3 3.5

-0.1

0.1

0.2

0.3

Stock index

Profit

No loan With a loan10 years, L0=7%

CF5 slide 98Zvi Wiener

Partial loan - portion q

nRn

n

nn

qLenXXCallX

aPb

X

XLqaP

),,()1(

)1()1(1

00

0

000

Theoretically q can be negative.

CF5 slide 99Zvi Wiener

Mixed portfolio

When the investment portfolio is a mix one should analyze it in a similar manner. Important: an option on a portfolio is less valuable than a portfolio of options.

Another risk factor - leaving rate should be accounted for by taking actuarial tables as leaving rate.

CF5 slide 100Zvi Wiener

Conclusions

It is a reasonable risk management policy not to take a loan against DAC.

Up to some optimal point it creates a useful hedge to other assets (call options and shares) of the firm.

Intuitively DAC is good when the stock market performs badly and profit participation is valueless. DAC performs bad when the market performs well.