qa-2 frm-garp sep-2001 zvi wiener 02-588-3049 mswiener/zvi.html quantitative analysis 2

Post on 20-Dec-2015

216 views

TRANSCRIPT

QA-2 FRM-GARP Sep-2001

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

Quantitative Analysis 2

QA-2 FRM-GARP Sep-2001

Fundamentals of Probability

Following Jorion 2001

Zvi Wiener - QA2 slide 3http://www.tfii.org

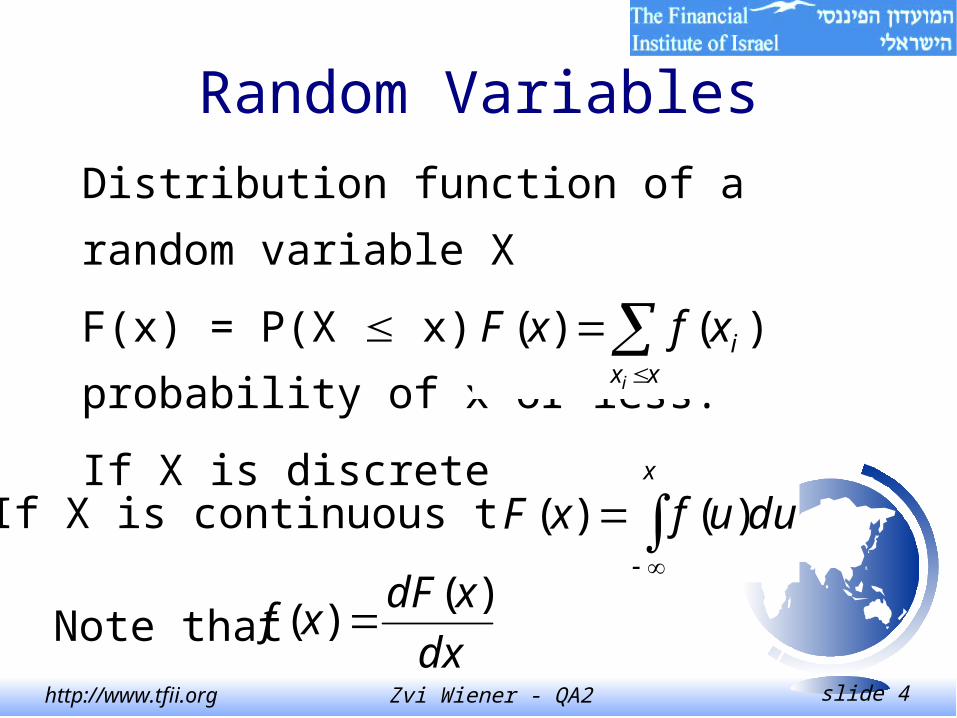

Random Variables

Values, probabilities.

Distribution function, cumulative probability.

Example: a die with 6 faces.

Zvi Wiener - QA2 slide 4http://www.tfii.org

Random Variables

Distribution function of a random variable X

F(x) = P(X x) - the probability of x or less.

If X is discrete then

xx

i

i

xfxF )()(

If X is continuous then

x

duufxF )()(

Note thatdx

xdFxf

)()(

Zvi Wiener - QA2 slide 5http://www.tfii.org

Random Variables

Probability density function of a random

variable X has the following properties

0)( xf

duuf )(1

Zvi Wiener - QA2 slide 6http://www.tfii.org

Multivariate Distribution Functions

Joint distribution function

),(),( 22112112 xXxXPxxF

1 2

2121122112 ),(),(x x

duduuufxxF

Joint density - f12(u1,u2)

Zvi Wiener - QA2 slide 7http://www.tfii.org

Independent variables

)()(),( 22112112 ufufuuf

)()(),( 22112112 uFuFuuF

Credit exposure in a swap depends on two randomvariables: default and exposure.If the two variables are independent one canconstruct the distribution of the credit loss easily.

Zvi Wiener - QA2 slide 8http://www.tfii.org

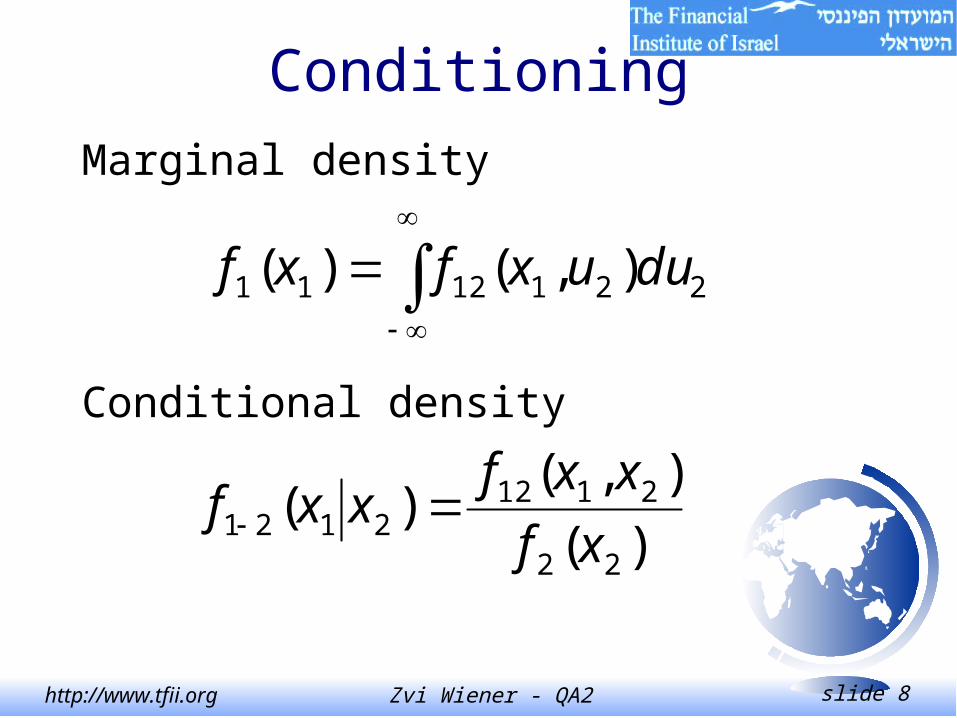

Conditioning

Marginal density

2211211 ),()( duuxfxf

Conditional density

)(

),()(

22

21122121 xf

xxfxxf

Zvi Wiener - QA2 slide 9http://www.tfii.org

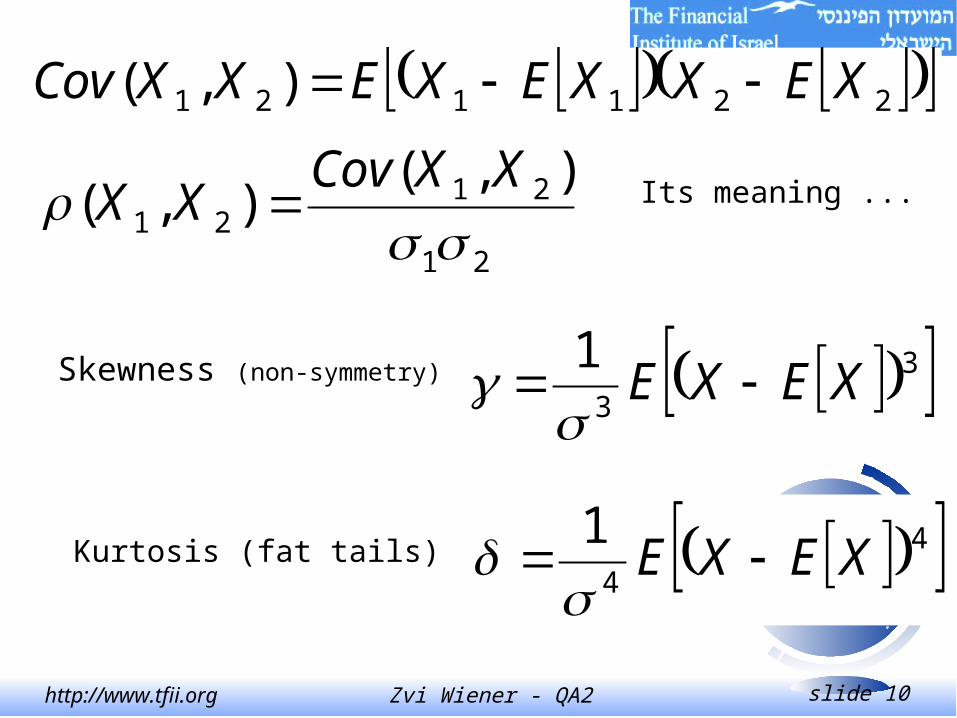

MomentsMean = Average = Expected value

dxxxfXE )()(

Variance

dxxfXExXV )()()( 22

VarianceDeviationdardS tan

Zvi Wiener - QA2 slide 10http://www.tfii.org

221121 ),( XEXXEXEXXCov

Its meaning ...

3

3

1XEXE

21

2121

),(),(

XXCov

XX

Skewness (non-symmetry)

4

4

1XEXE

Kurtosis (fat tails)

Zvi Wiener - QA2 slide 11http://www.tfii.org

Main properties

)()( XbEabXaE

)()( XbbXa

)()()( 2121 XEXEXXE

),(2)()()( 2122

12

212 XXCovXXXX

Zvi Wiener - QA2 slide 12http://www.tfii.org

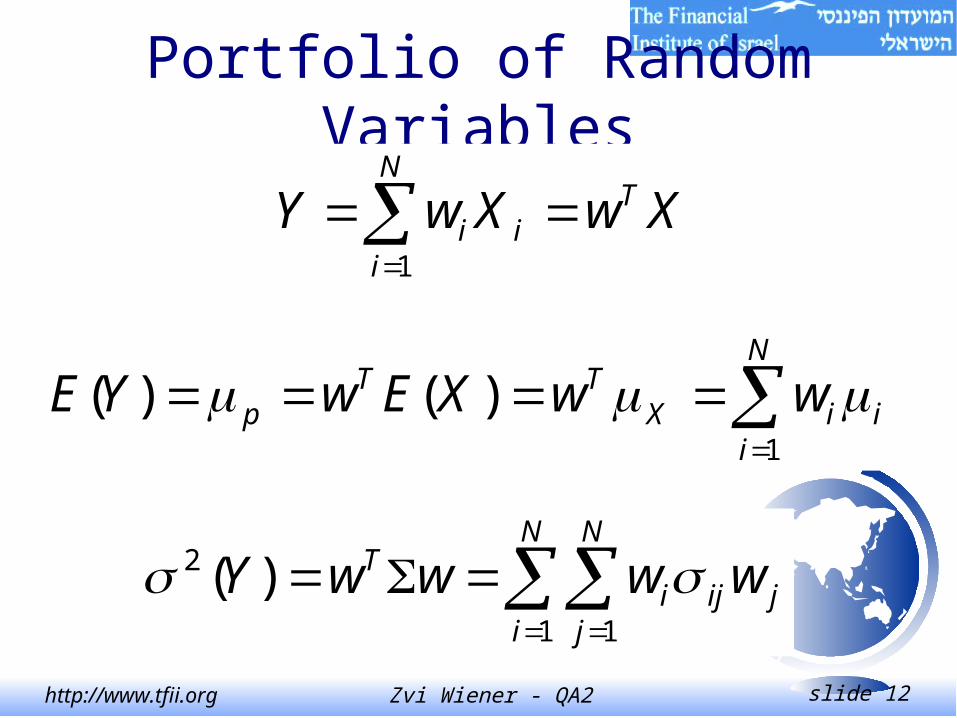

Portfolio of Random Variables

XwXwY TN

iii

1

N

iiiX

TTp wwXEwYE

1

)()(

N

i

N

jjiji

T wwwwY1 1

2 )(

Zvi Wiener - QA2 slide 13http://www.tfii.org

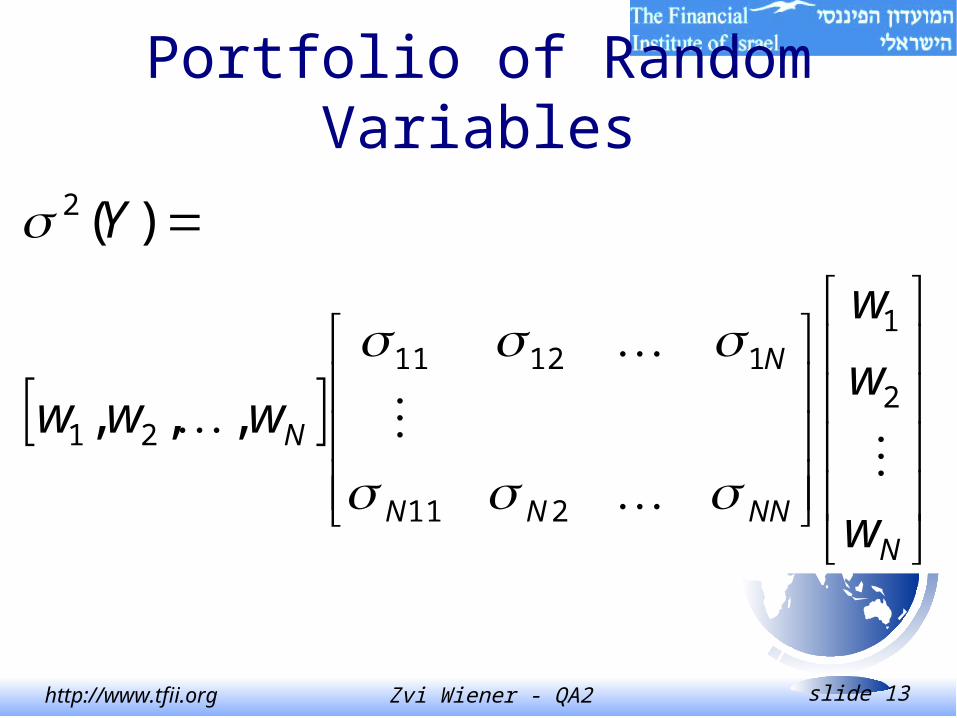

Portfolio of Random Variables

NNNNN

N

N

w

w

w

www

Y

2

1

211

11211

21

2

,,,

)(

Zvi Wiener - QA2 slide 14http://www.tfii.org

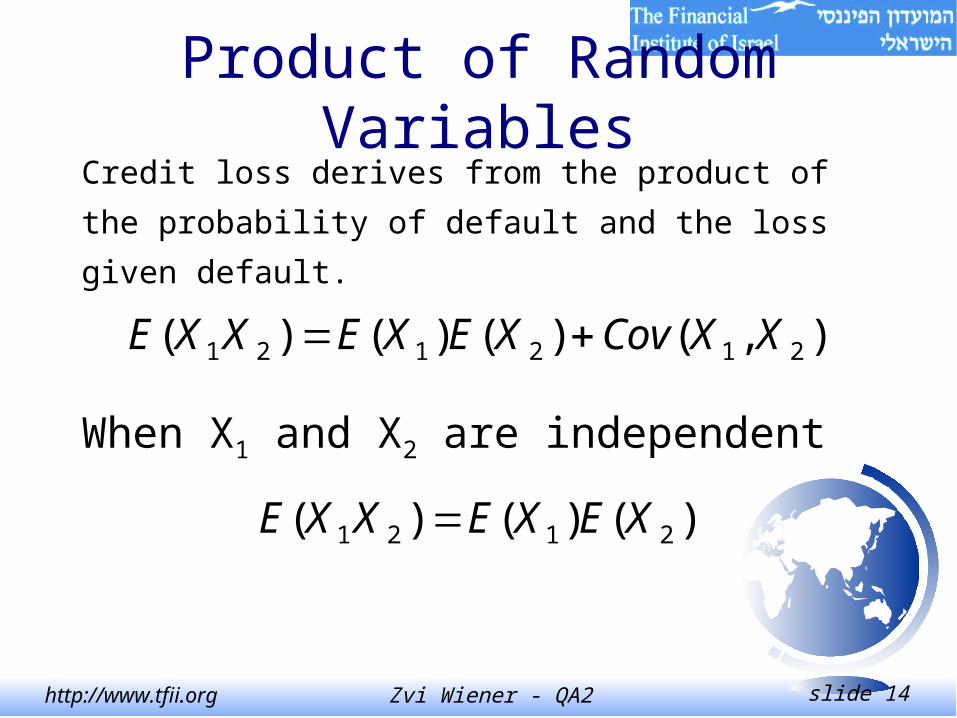

Product of Random Variables

Credit loss derives from the product of the

probability of default and the loss given default.

),()()()( 212121 XXCovXEXEXXE

When X1 and X2 are independent

)()()( 2121 XEXEXXE

Zvi Wiener - QA2 slide 15http://www.tfii.org

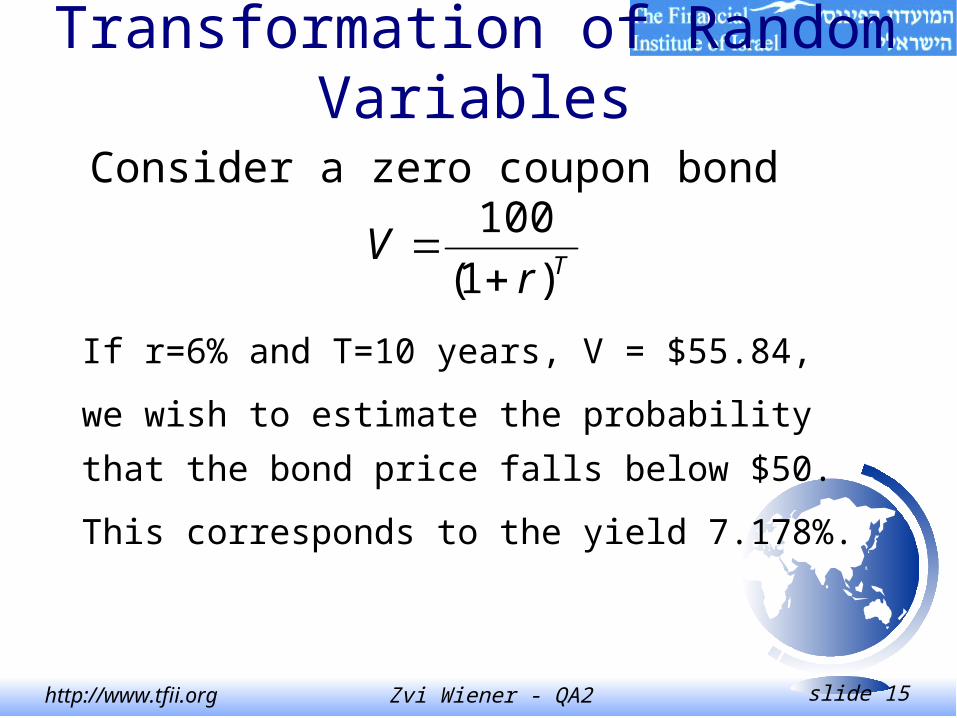

Transformation of Random Variables

Consider a zero coupon bond

TrV

)1(

100

If r=6% and T=10 years, V = $55.84,

we wish to estimate the probability that the

bond price falls below $50.

This corresponds to the yield 7.178%.

Zvi Wiener - QA2 slide 16http://www.tfii.org

The probability of this event can be derived

from the distribution of yields.

Assume that yields change are normally

distributed with mean zero and volatility 0.8%.

Then the probability of this change is 7.06%

Example

Zvi Wiener - QA2 slide 17http://www.tfii.org

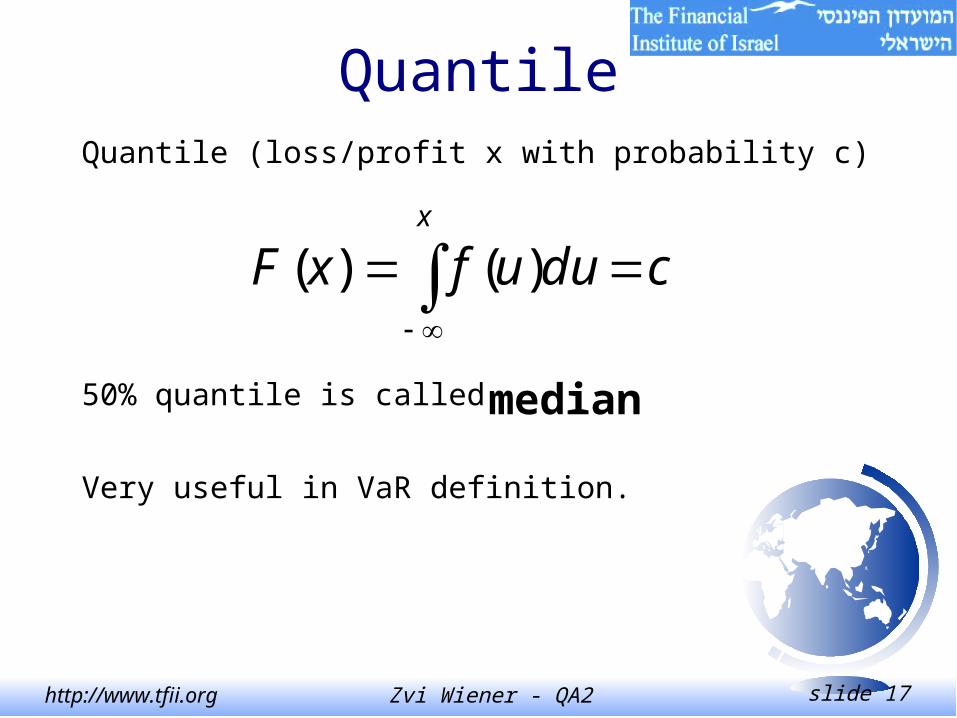

Quantile

Quantile (loss/profit x with probability c)

cduufxFx

)()(

50% quantile is called median

Very useful in VaR definition.

Zvi Wiener - QA2 slide 18http://www.tfii.org

FRM-99, Question 11

X and Y are random variables each of which follows a standard normal distribution with cov(X,Y)=0.4.

What is the variance of (5X+2Y)?

A. 11.0

B. 29.0

C. 29.4

D. 37.0

Zvi Wiener - QA2 slide 19http://www.tfii.org

FRM-99, Question 11

37254.0225 22

BABA 222

Zvi Wiener - QA2 slide 20http://www.tfii.org

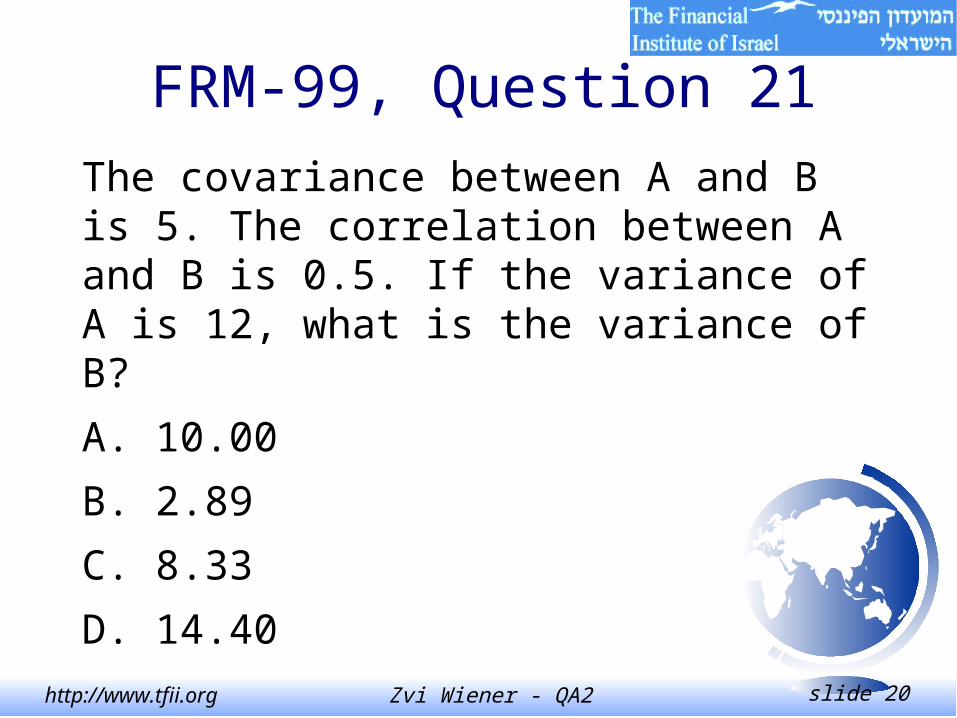

FRM-99, Question 21

The covariance between A and B is 5. The correlation between A and B is 0.5. If the variance of A is 12, what is the variance of B?

A. 10.00

B. 2.89

C. 8.33

D. 14.40

Zvi Wiener - QA2 slide 21http://www.tfii.org

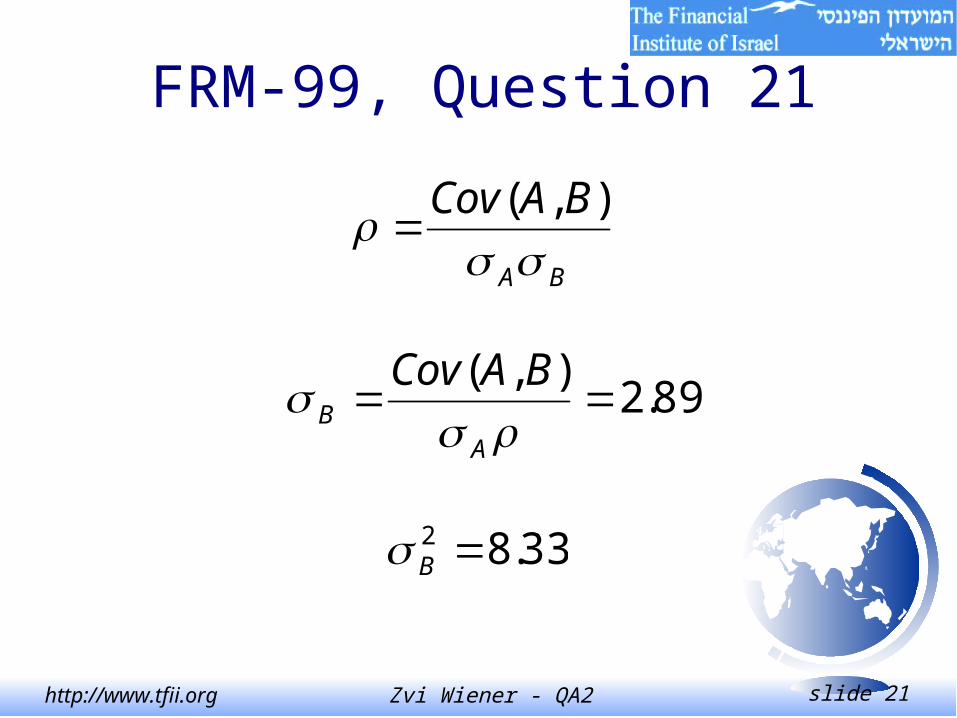

FRM-99, Question 21

BA

BACov

),(

89.2),(

AB

BACov

33.82 B

Zvi Wiener - QA2 slide 22http://www.tfii.org

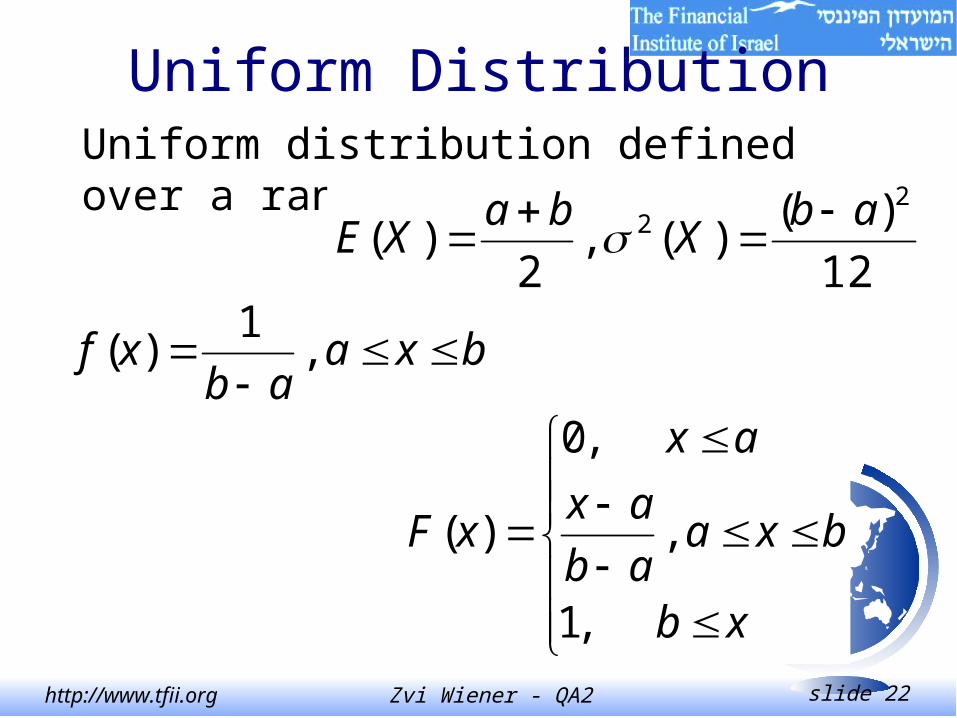

Uniform DistributionUniform distribution defined over a range of values axb.

bxaab

xf

,1

)(

12

)()(,

2)(

22 ab

Xba

XE

xb

bxaab

ax

ax

xF

,1

,

,0

)(

Zvi Wiener - QA2 slide 23http://www.tfii.org

Uniform Distribution

a b

ab 1

1

Zvi Wiener - QA2 slide 24http://www.tfii.org

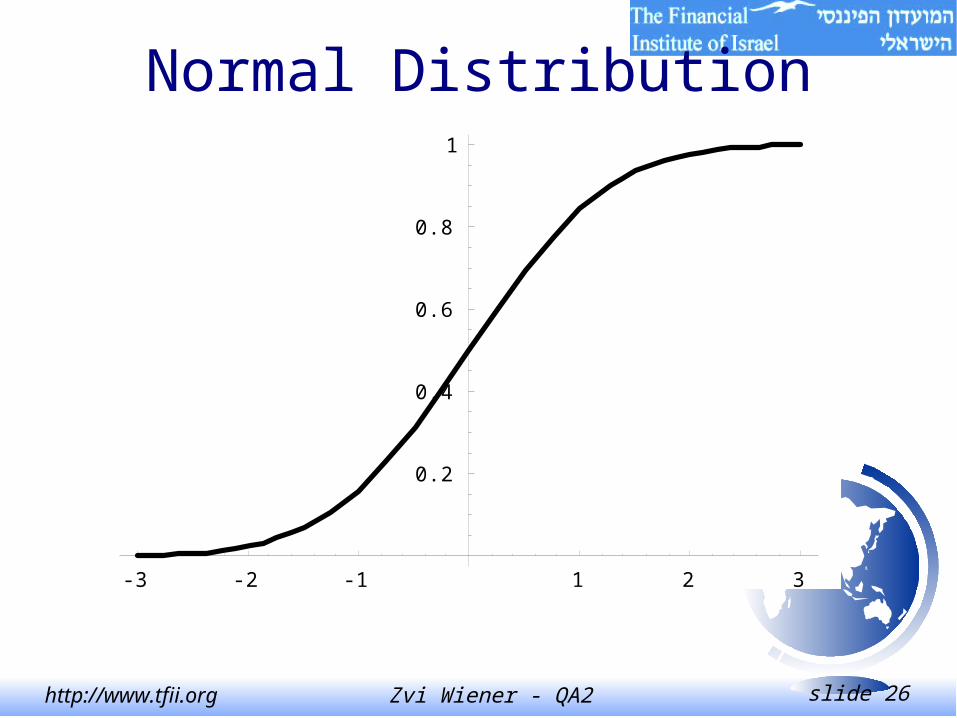

Normal DistributionIs defined by its mean and variance.

2

2

2

)(

2

1)(

x

exf

22 )(,)( XXE

Cumulative is denoted by N(x).

Zvi Wiener - QA2 slide 25http://www.tfii.org

-3 -2 -1 1 2 3

0.1

0.2

0.3

0.4

Normal Distribution66% of events liebetween -1 and 1

95% of events liebetween -2 and 2

Zvi Wiener - QA2 slide 26http://www.tfii.org

Normal Distribution

-3 -2 -1 1 2 3

0.2

0.4

0.6

0.8

1

Zvi Wiener - QA2 slide 27http://www.tfii.org

Normal Distribution• symmetric around the mean

• mean = median

• skewness = 0

• kurtosis = 3

• linear combination of normal is normal

99.99 99.90 99 97.72 97.5 95 90 84.13 50

3.715 3.09 2.326 2.000 1.96 1.645 1.282 1 0

Zvi Wiener - QA2 slide 28http://www.tfii.org

Central Limit Theorem

The mean of n independent and identically distributed variables converges to a normal distribution as n increases.

n

iiX

nX

1

1

nNX

2

,

Zvi Wiener - QA2 slide 29http://www.tfii.org

Lognormal DistributionThe normal distribution is often used for rate of return.

Y is lognormally distributed if X=lnY is normally distributed. No negative values!

2

2

2

))(ln(

2

1)(

x

ex

xf

22

2

22222 )(,)(

eeXeXE

222 )(ln)(,)(ln)( XYXEYE

Zvi Wiener - QA2 slide 30http://www.tfii.org

Lognormal DistributionIf r is the expected value of the lognormal variable X, the mean of the associated normal variable is r-0.52.

0.5 1 1.5 2 2.5 3

0.1

0.2

0.3

0.4

0.5

0.6

Zvi Wiener - QA2 slide 31http://www.tfii.org

Student t DistributionArises in hypothesis testing, as it describes the distribution of the ratio of the estimated coefficient to its standard error. k - degrees of freedom.

2

12

1

11

2

2

1

)(

k

k

xkk

k

xf

0

1)( dxexk xk

Zvi Wiener - QA2 slide 32http://www.tfii.org

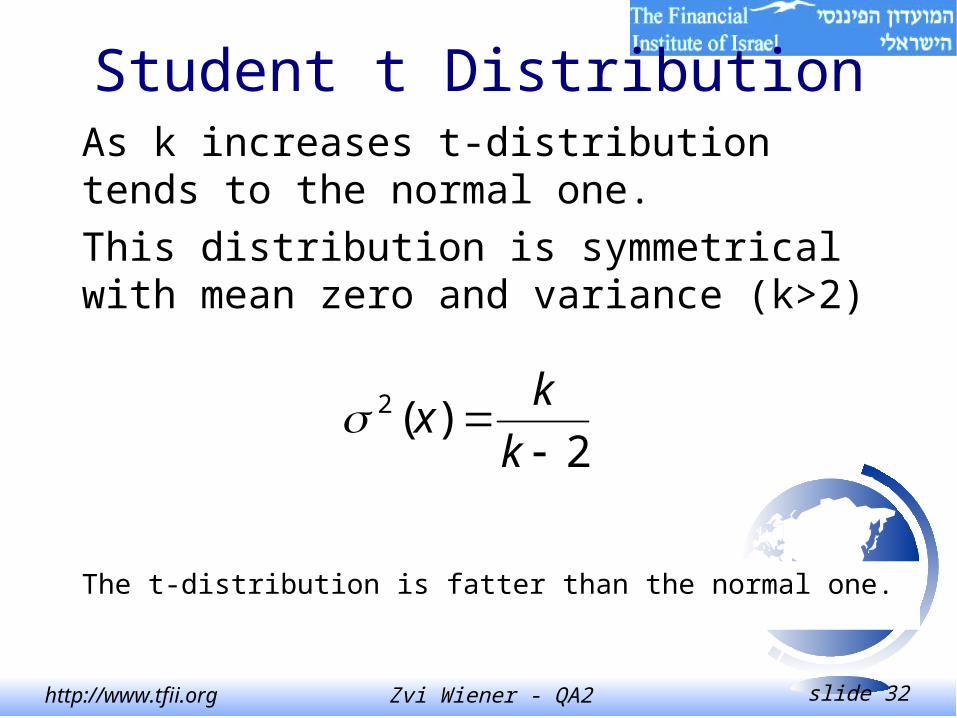

Student t DistributionAs k increases t-distribution tends to the normal one.

This distribution is symmetrical with mean zero and variance (k>2)

2)(2

k

kx

The t-distribution is fatter than the normal one.

Zvi Wiener - QA2 slide 33http://www.tfii.org

Binomial DistributionDiscrete random variable with density function:

nxppx

nxf xnx ,,.1,0,)1()(

nppXpnXE )1()(,)( 2

For large n it can be approximated by a normal.

)1,0(~)1(

Nnpp

pnxz

Zvi Wiener - QA2 slide 34http://www.tfii.org

FRM-99, Question 12

For a standard normal distribution, what is the approximate area under the cumulative distribution function between the values -1 and 1?

A. 50%

B. 66%

C. 75%

D. 95%

Error!

Zvi Wiener - QA2 slide 35http://www.tfii.org

FRM-99, Question 13

What is the kurtosis of a normal distribution?

A. 0

B. can not be determined, since it depends on the variance of the particular normal distribution.

C. 2

D. 3

Zvi Wiener - QA2 slide 36http://www.tfii.org

FRM-99, Question 16

If a distribution with the same variance as a normal distribution has kurtosis greater than 3, which of the following is TRUE?

A. It has fatter tails than normal distribution

B. It has thinner tails than normal distribution

C. It has the same tail fatness as normal

D. can not be determined from the information provided

Zvi Wiener - QA2 slide 37http://www.tfii.org

FRM-99, Question 5

Which of the following statements best characterizes the relationship between normal and lognormal distributions?A. The lognormal distribution is logarithm of the normal distribution.B. If ln(X) is lognormally distributed, then X is normally distributed.C. If X is lognormally distributed, then ln(X) is normally distributed.D. The two distributions have nothing in common

Zvi Wiener - QA2 slide 38http://www.tfii.org

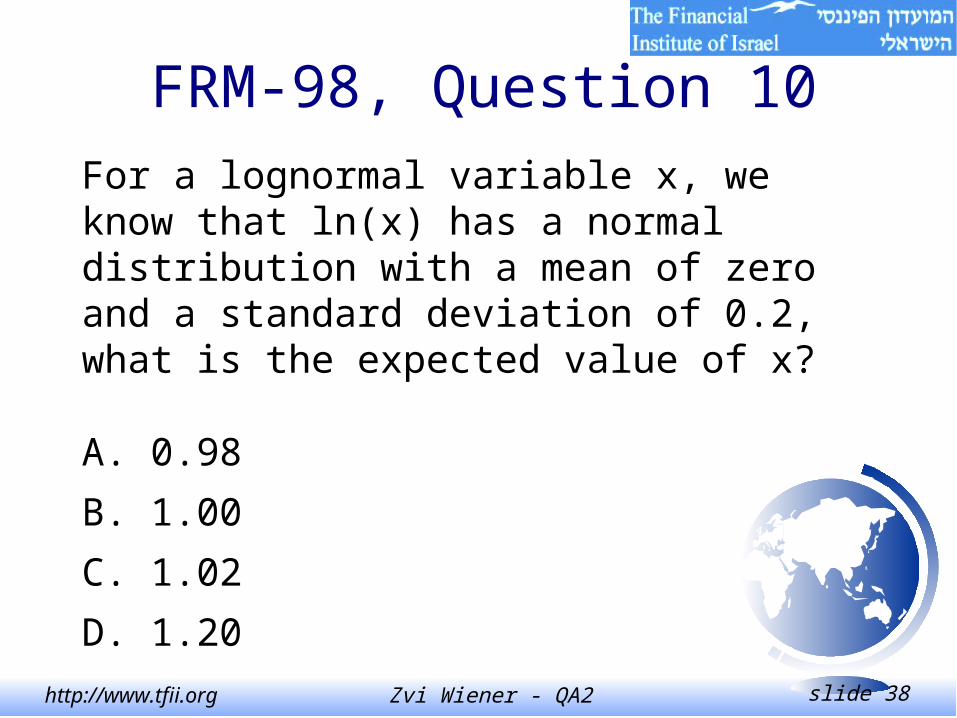

FRM-98, Question 10

For a lognormal variable x, we know that ln(x) has a normal distribution with a mean of zero and a standard deviation of 0.2, what is the expected value of x?

A. 0.98

B. 1.00

C. 1.02

D. 1.20

Zvi Wiener - QA2 slide 39http://www.tfii.org

FRM-98, Question 10

02.1][ 2

2.00

2

22

eeXE

Zvi Wiener - QA2 slide 40http://www.tfii.org

FRM-98, Question 16

Which of the following statements are true?

I. The sum of normal variables is also normal

II. The product of normal variables is normal

III. The sum of lognormal variables is lognormal

IV. The product of lognormal variables is lognormalA. I and IIB. II and IIIC. III and IVD. I and IV

Zvi Wiener - QA2 slide 41http://www.tfii.org

FRM-99, Question 22

Which of the following exhibits positively skewed distribution?

I. Normal distribution

II. Lognormal distribution

III. The returns of being short a put option

IV. The returns of being long a call optionA. II onlyB. III onlyC. II and IV onlyD. I, III and IV only

Zvi Wiener - QA2 slide 42http://www.tfii.org

FRM-99, Question 22

C. The lognormal distribution has a long right

tail, since the left tail is cut off at zero. Long

positions in options have limited downsize,

but large potential upside, hence a positive

skewness.

Zvi Wiener - QA2 slide 43http://www.tfii.org

FRM-99, Question 3

It is often said that distributions of returns from financial instruments are leptokurtotic. For such distributions, which of the following comparisons with a normal distribution of the same mean and variance MUST hold?A. The skew of the leptokurtotic distribution is greaterB. The kurtosis of the leptokurtotic distribution is greaterC. The skew of the leptokurtotic distribution is smallerD. The kurtosis of the leptokurtotic distribution is smaller