changes, drivers, and challenges in the north american steel industry thomas a. danjczek president...

TRANSCRIPT

Changes, Drivers, and Challenges in the North American Steel Industry

Thomas A. DanjczekPresidentSteel Manufacturers AssociationNovember 8, 2012Scottsdale, Arizona

CHAIN LINK FENCE MANUFACTURERS INSTITUTE ANNUAL MEETING

Update 10-24-2012

Outline

•About the SMA

•Set the Tone - Economy

•Set the Tone - Steel

•Changes Impacting Steel

•Drivers Impacting Steel

•Challenges Impacting Steel

•Final Thoughts

CLFMI – Annual Meeting

3

About the SMA- Composed of 35 North American electric arc furnace (“EAF”) steel producing Member Companies, and 123 Associate Member steel industry suppliers

- SMA Members account for approximately 80% of U.S. domestic steel capacity

- Today, roughly two-thirds of North American steel production comes from the scrap-based EAF process, up from just 10% in the early 1970s

CLFMI – Annual Meeting SMA

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 201120.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

U.S. EAF Share of Total Production

% of EAF Production

Approximately 2/3 of U.S. Steel Production

4

CLFMI – Annual Meeting Set the Tone - Economy

• U.S. & Canada GDP Growth Around 2%

NEAR STAGNATION

• U.S. Manufacturing Production Rebounding

STILL 6% BELOW PEAK & MAY BE DROPPING

• Global Slowdown Weakens Demand, Poor Earnings

ARE WE LOSING MOMENTUM?

• U.S. Auto, Aerospace, Machinery Strong

WILL IT CONTINUE? MAY BE DROPPING…

• “Trimming Profits”

• Second Recession in U.S.???

US GOOds

CLFMI – Annual Meeting Set the Tone - Economy

$620 Billion Annual Deficit projected in 2012 is most significant barrier to U.S. economic recovery

UNSUSTAINABLE

6

Set the Tone - SteelCLFMI – Annual Meeting

• Primary metal 4% growth YTD 2012 over 2011 in US

• U.S. capacity utilization approx. 76.5% through October 2012

Up 6.4% over 2011, but…Recent weeks around 70%, now 69%

• Scrap price volatility (75% of minimill costs)

$100/150 drop in 45 days – half back; maybe $20 down in September, maybe $50 in October???

• U.S. may hit 97ms tons in 2012

• Inventories remains LOW

• Changes in mill orders lead time from 6 weeks to 2.5weeks, back to 5 weeks…all in 2 months – VOLATILE

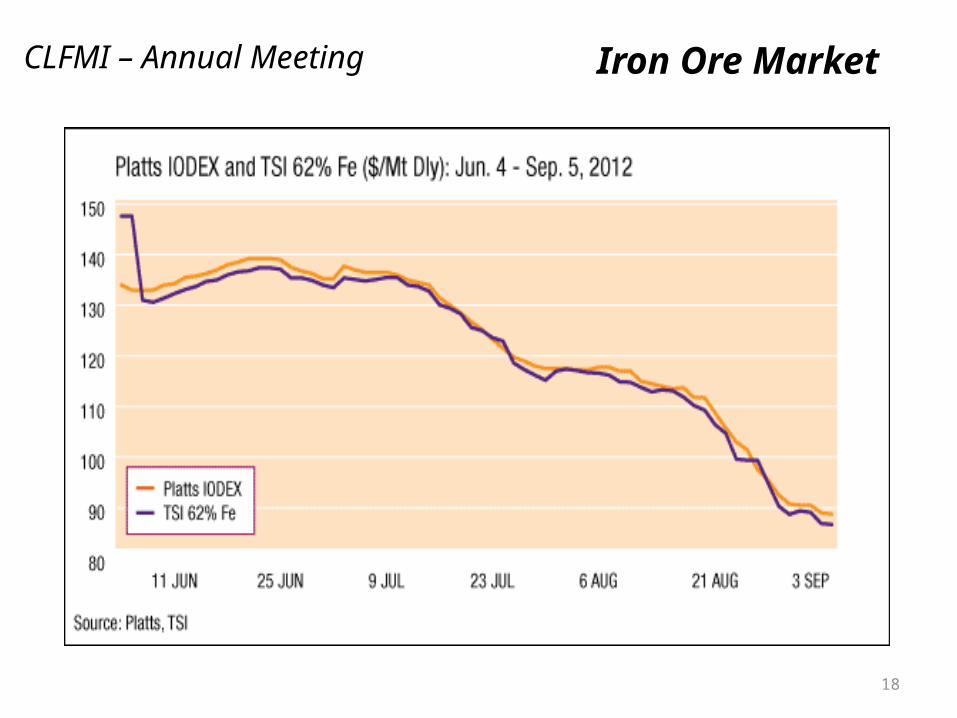

• Iron ore prices down 36% YTD

7

CLFMI – Annual Meeting

Source: Gerdau NA, US Census Bureau & AISI

NAFTA Auto Production

Source: Wards Automotive

0

2

4

6

8

10

12

14

16

18

Units (m

illions)

CLFMI – Annual Meeting

Construction Activity*Non-building structures (e.g., infrastructure) not included

Source: McGraw-Hill (Dodge)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Squa

re F

oota

ge (0

00)

Residential (1 & 2 family dwellings) Non-Residential

CLFMI – Annual Meeting

10

CLFMI – Annual Meeting

Energy Production

Source: Baker Hughes, U.S. Dept. of Energy

0

500

1,000

1,500

2,000

2,500

JAN

APR

JUL

OCT

JAN

APR

JUL

OCT

JAN

APR

JUL

OCT

JAN

APR

JUL

OCT

Jan

Apr

Jul

2008 2009 2010 2011 2012

RIG

CO

UN

T

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$ M

cf

Total RIGS

Verticle RIGS

Horizontal RIGS

Natural Gas Price at Wellhead

CLFMI – Annual Meeting

World Steel Association Global Overview NAFTAApparent Steel Use, finished steel (SRO October 2012)

2011 Actual

1380.9 million tonnes 6.2% growth 121.3 9.0% growth

2012 forecast

1409.4 million tonnes 2.1% growth 130.4 7.5% growth

2013 forecast

1454.9 million tonnes 3.2% growth 135.1 3.6% growth

2013 As PCT 2007 119.5% growth 95.3% growth

CLFMI – Annual Meeting

Source: AISI

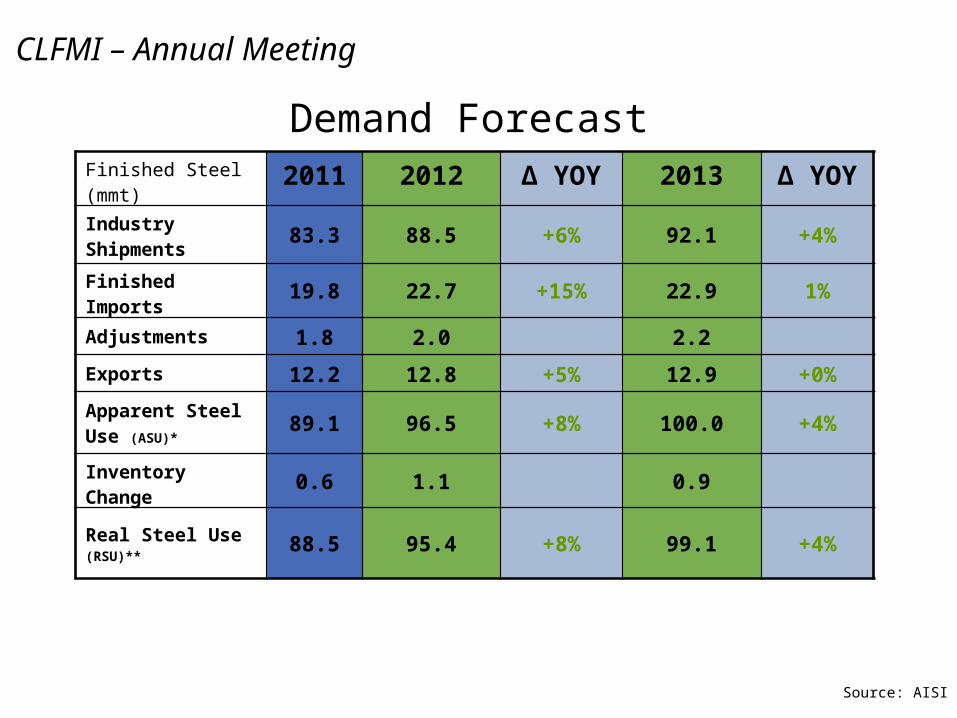

Demand ForecastFinished Steel (mmt)

2011 2012 ∆ YOY 2013 ∆ YOY

Industry Shipments 83.3 88.5 +6% 92.1 +4%

Finished Imports 19.8 22.7 +15% 22.9 1%

Adjustments 1.8 2.0 2.2

Exports 12.2 12.8 +5% 12.9 +0%

Apparent Steel Use (ASU)*

89.1 96.5 +8% 100.0 +4%

Inventory Change 0.6 1.1 0.9

Real Steel Use (RSU)**

88.5 95.4 +8% 99.1 +4%

CLFMI – Annual Meeting

Imports – 2012

Russia Taiwan Germany Turkey China Japan South Korea

0

500,000

1,000,000

1,500,000

2,000,000

2,500,0002011 YTD vs. 2012 YTD Finished Steel Imports

from Key Offshore Countries

2011 YTD (NT) - 7 months 2012 YTD (NT) - 7 months

+28.04%+26.97%

+94.18% +29.12%

+33.63%

+23.35%

+52.51%

CLFMI – Annual Meeting

Source: DOC

15

CLFMI – Annual Meeting

U.S. Steel Imports

Year M-Metric Tons

2010 21.7

2011 25.9

2012(e) 32.0

U.S. steel imports are a growing problem.

CLFMI – Annual Meeting Changes Impacting Steel

Deeper Recession

Variable Cost Control

Engineers

Scrap Availability

High Unemployment

Labor Intensity

Inventory Levels

CHINA

Safety

ConsolidationsCustomer

Requirements

Environmental Regulations

Foreign Ownership

Transportation Costs

Ore Availability

Energy Costs

Currency

State-Owned Enterprises

Other Factors…

Skilled Jobs Shortages

Semi-finished Imports

Union Contracts

Scrap Exports

• Underlying Weak Economy, with less than 3% GDP growth and estimates downward.

• Recovery underway, but very slow – “Fragile”

• North American steel market under pressure with unused capacity

• Increased import percentages YOY, Impact of currency changes

• Not normal cycle of recession, overcapacity; new supply coming on

• Relative strong demand in auto; construction lagging

• Raw material costs, energy, and variable cost controls are major drivers

• Ore price evolution and recent developments-Platts graph

• Scrap price impact, growth of EAFs, developing world slowing down

• Economic growth turning point is always two quarters away

• Company market cap values at historic lows

Drivers Impacting SteelCLFMI – Annual Meeting

18

CLFMI – Annual Meeting Iron Ore Market

CLFMI – Annual Meeting Challenges Impacting Steel

Scrap Exports

Restrictions

Import Penetration

SOEs

Capital

Scrap Price Volatility

China, China, China Gov’t Subsidies

Trained Workforce

Abundant Natural Gas is a

“Game Changer”

WTO Disputes

Health Care Costs

Tax Manipulation

& Reforms

Trade Restrictions

Another Recession

Indirect Steel %

Environmental Regulations

Global Steel Capacity Growth

Role of Developing World

Anti-Competitive

Behavior

Labor Regulations

Infrastructure Investment

Currency Undervaluation

Final Thoughts

• Volatile times continue, May be between recessions• U.S. is in a traffic jam, moving slightly forward, but don’t know other

consequences. Don’t look to Washington, DC for help. Gridlock continues

• Uncertainty will continue especially in U.S. industry until economic fundamentals are in equilibrium. Limited visibility…

• Other countries increasing steel capacity without regard to market forces or comparative advantage.

• Current status of scrap restrictions is unsustainable• Reasons for optimism in steel in North America:

– Favorable gains with reemerging manufacturing base– Scrap-based, 75% of cost – local supply– Low cost on global basis (energy is positive, labor less than 10%, others have

higher transportation costs)– Relatively strong market and resiliency– Better & stronger company balance sheets

CLFMI – Annual Meeting