chapter 10--costs of the firm chapter outline costs in the short run allocating production between...

TRANSCRIPT

Chapter 10--Costs of the Firm

Chapter OutlineCosts In The Short RunAllocating Production Between Two ProcessesThe Relationship Among MP, AP, MC, And AVCCosts In The Long RunLong-run Costs And The Structure Of IndustryThe Relationship Between Long-run And Short-run Cost Curves

10-1

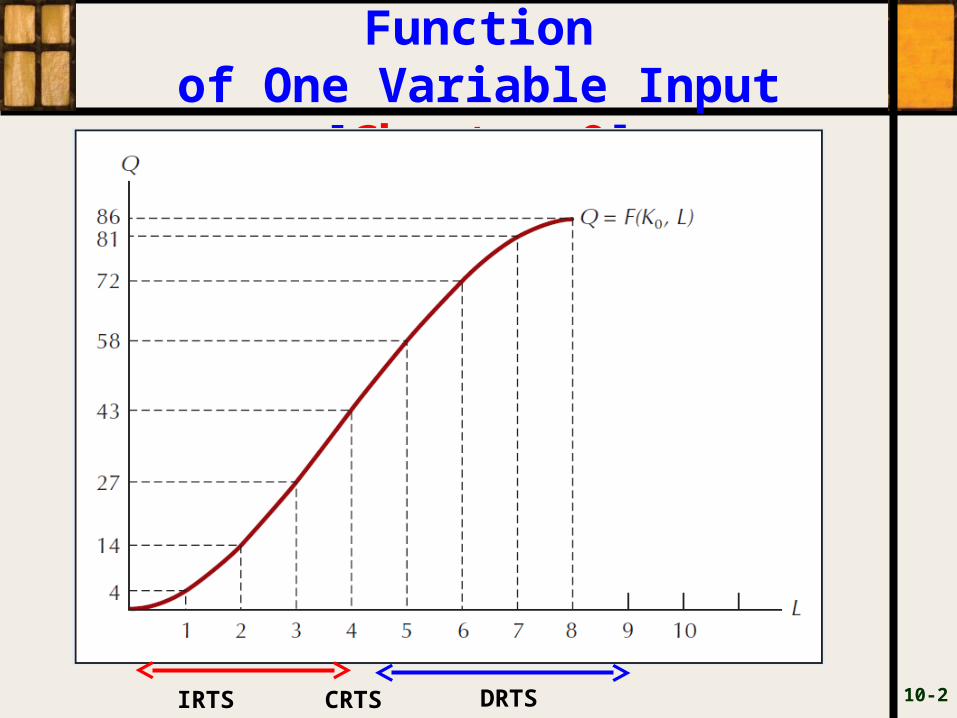

Figure 10.1: Output as a Function

of One Variable Input [Chapter 9]

10-2IRTS DRTSCRTS

Figure 10.2: The Total, Variable,

and Fixed Cost Curves

10-3

TCQ = FC + VCQ = rK0 + wL where TCQ, VCQ indicate that costs depend on output unlike FC which is independent of Q.Fixed cost (FC): cost that does not vary with the level of output in the short run (the cost of all fixed factors of production).Variable cost (VC): cost that varies with the level of output in the short run (the cost of all variable factors of production).Total cost (TC): all costs of production= the sum of variable cost and fixed cost.

Note:similar curvature of TC and VC: VC=0 if Q=0Before Q=43 -> IRTS, thus VC increases at a decreasing rateAfter Q=43, DRTS, VC increases at an increasing rate

Figure 10.3: The Production Function

Q = 3KL, with K = 4 (CRTS)

10-4

Slope =∆Q/∆L =12

Average Costs In The Short Run

Average fixed cost (AFC): fixed cost divided by the quantity of output, AFCQ = rKo/Q =FC/Q

Average variable cost (AVC): variable cost divided by the quantity of output, AVCQ = wL/Q=VCQ/Q

Average total cost (ATC): total cost divided by the quantity of output, ATC = AVC + AFC= (wL+rKo)/Q = TCQ/Q

Marginal cost (MC): change in total cost that results from a 1-unit change in output,

MC = ∆TCQ/Q = ∆VCQ/Q since ∆FC/Q = 0 Graphing The Short-run Average and Marginal Cost

Curves Geometrically, average variable cost at any level of

output Q may be interpreted as the slope of a ray to the variable cost curve at Q .

10-5

Figure 10.5: The Marginal, Average Total, Average Variable, and Average

Fixed Cost Curves

10-6

The MC intersects both the ATC and the AVC at their minimums

Figure 10.6: Quantity vs. Average Costs

10-7

Marginal Costs

Is the same as the cost of expanding output (or the savings from contracting).

By far the most important of the seven cost curves. Reason: a typical firm makes a marginal decision whether to expand or contract production. This involves cost-benefit analysis (CBA).

Geometrically, at any level of output may be interpreted as the slope of the total cost curve at that level of output.– And since the total cost and variable cost curves are

parallel, it is also equal to the slope of the variable cost curve.

Marginal and Average Costs-When MC is less than average cost (either ATC or AVC), the average

cost curve must be decreasing with output; and when MC is greater than average cost, average cost must be increasing with output.

10-8

Figure 10.7: Cost Curves for a Specific Production Process : Q= 3KL ,K=4

10-9

Given that Q= 3KL ,K=4, so Q =3*4L = 12L and L = Q/12, w=$24, r=$2, thus TCQ = wL +rK0 =2*4 + 24(Q/12) = 8 + 2QThus,TCQ= 8 + 2Q so that ATCQ = (8+2Q)/Q = 8/Q + 2FC = $8 so that AFCQ = 8/QVC =2Q so that AVC = 2Q/Q =2 and MC =∆TCQ/∆Q = 2 – slope of the TCQ

ATC = TCQ=/Q = AVC +AFC = 2 + 8/Q

Figure 10.9: The Relationship Between MP, AP, MC, and AVC

10-10

Chap.9: MPL cuts the APL at the maximum value of the APL.Chap. 10: MCQ cuts the AVC at the minimum value of the AVC.These relationships serve a vital link for day-to-day management of a profit-maximizing firm: productivity (Chap. 9) is inversely linked to cost-control – a crucial understanding in all Accounting courses!MCQ = ∆VCQ/∆Q and if Q= f(L), then ∆VCQ = ∆wL so that ∆VCQ/∆Q = ∆wL/∆Q. Given a fixed wage (w), then w∆L/∆Q = w/MPL = MCQ

The same reasoning applies to AVC = w/APL

Figure 10.10: The Isocost Line

10-11

Costs In The Long RunIsocost line: a set of input bundles each of which costs the same amount.

To find the minimum cost point we begin with a specific isoquant then superimpose a map of isocost lines, each corresponding to a different cost level.

--The least-cost input bundle corresponds to the point of tangency between an isocost line and the specified isoquant.

Given: w=$4, r =$2 and C= $100Thus, wL + rK =CK= C/r - (w/r)*L –Isocost for the firm ≈ Budget Constraint for the Consumer4L +2K= 100w∆L + r∆K = ∆C =0-w∆L= r∆K-w/r = ∆K/∆L =-4/2=-2

Figure 10.11: The Maximum Output

for a Given Expenditure

10-12

Firm should set MRTSL,K = -MPL/MPK = -w/r

B

C

A

1. At B, MPL/MPK < PL/PK. In order to fix this, less labor and more capital is advised until the MPL/MPK = PL/PK at A.2. At C, MPL/MPK >PL/PK. In order to fix this, more labor and less capital is advised until the MPL/MPK = PL/PK at A.3. At A, MPL/MPK = PL/PK. Thus, the firm is optimizing its employment of K at K* and L at L* to minimize its costs in producing Q0.

Figure 10.12: The Minimum Costfor a Given Level of Output

10-13

Firm should set MRTSL,K = -MPL/MPK = -w/r OR MPL/w = MPK/r

Figure 10.13: Different Ways of Producing 1 Ton of Gravel (Nepal) versus the US

10-14

Gravel is made by hand in Nepal (isocost line), but by machine in the U.S.(isocost line) because the relative prices of labor and capital differ so dramatically in the two countries.

That is, | | | |NepalUS

US Nepal

WW

r r

Figure 10.15: The Long-Run Expansion Path

10-15

The Relationship Between Optimal Input Choice And Long-run CostsOutput expansion path (OEP)- the locus of tangencies (minimum cost input combinations) traced out by an isocost line of given slope as it shifts outward into the isoquant map for a production process.

Recall the (1) Price Expansion Path (PEP) and (2) Income Consumption (ICP) in case of the Consumer

Figure 10.16: The Long-Run Total, Average, and Marginal

Cost Curves

10-16

Plot (Q1, TCQ1), (Q2, TCQ2) and so forth from Figure 10.15 onto top Panel of Figure 10.16.Since in the LR, there are no FCs this means that all costs are variable.The long-run total cost (LTC) always passes through the origin since the firm can always liquidate all its inputs.

The Long-run MC =LMCQ = ∆LTCQ/∆QThe long-run average cost, LACQ = LTCQ/QThere are no fixed costs (FC) in the LR!

Figure 10.17: The LTC, LMC and LAC Curves for a PF exhibiting Constant

Returns to Scale (CRTS)

10-17

Constant returns to scale - long-run total costs are thus exactly proportional to output.

Figure 10.18: The LTC, LAC and LMC Curves for a Production Process with Decreasing

Returns to Scale

10-18

Decreasing returns to scale - a given proportional increase in output requires a greater proportional increase in all inputs and hence a greater proportional increase in costs.

Figure 10.19: The LTC, LAC and LMC Curves for a Production Process with

Increasing Returns to Scale

10-19

Increasing returns to scale - long-run total cost rises less than in proportion to increases in outputNext: Examine the importance of long-run costs for the structure of an industry.

Figure 10.20: LAC Curves Characteristic of Highly Concentrated

Industrial Structures

10-20

Long-run Costs And The Structure Of IndustryNatural monopoly: an industry whose market output is produced at the lowest cost when production is concentrated in the hands of a single firm[Panel A].Minimum efficient scale: the level of production required for LAC to reach its minimum level, Q0 [Panel B].

Industry dominated by a few firms if Q0 forms a substantial share for an industry.

Ever declining LAC is a cost advantage that allows an existing firm defensive barriers against possible competitors (barriers to entry)

Figure 10.21: LAC Curves Characteristic of Unconcentrated

Industry Structures

10-21

Survival in an industry requires a low-cost structure (U-shaped LAC) and if Q0 is small share for the industry, then many firms are in the industry (Panel A).Similarly, if the LAC is flat (Panel B) or rising (Panel C), it is possible to have many firms, each producing a small portion of the industry output.Industry – collection of firms that produce identically or similar products.

Figure 10.22: The Family of Cost Curves Associated with a U-

Shaped LAC

10-22

The LAC is the “envelope” of all ATC curvesLMC = SMC at the value of output (Q2 in this case) where ATC is tangent to the LAC.At the minimum point of the LAC, LMC = SMC = ATC = LACFor Plant sizes 1 (ATC1) and 2 (ATC2), the SMC1 and SMC3 do not hit LAC or ATC at its minimum.Only and only with Plant Size 2 (ATC2) does the LMC hit the ATC and LAC from below at its minimum. Plant Size 2 minimizes both SR and LR costs.

Figure A10.1: The Short-run and Long-Run Expansion

Paths

10-23

OE is the LR expansion pathWith K fixed at K = K2*, the SR expansion path is a horizontal line through point (0, K2*).Given that K2* is the optimal K for producing Q = 2, the LR and SR expansion paths intersect at point T.The SR TCQ of producing a given level of output is the cost given by the relevant isocost line. For example, for Q3, the SR TCQ is given by STC3

Figure A10.2: The LTC and STC Curves Associated with the Isoquant Map in Figure

A.10.1

10-24

As Q approaches Q=2 (the level of output for which the fixed factor is at optimal level), STCQ approaches LTCQ.The STCQ and LTCQ curves are tangent at Q=2Beyond Q=2, STCQ increases faster than LTCQ due to diminishing returns that partly governs the behavior of STCQ in the SR.