management accounting acct 481 michael dimond. michael dimond school of business administration...

TRANSCRIPT

Management AccountingACCT 481

Michael Dimond

Michael DimondSchool of Business Administration

Managing & Allocating Costs

• Pricing Decisions• Cost Management & Allocation• Customer-profitability Analysis• Sales-variance Analysis• Support-department Cost Allocation• Common-cost Allocation• Revenue Allocation• Joint-cost Allocation• Byproducts• Spoilage, Rework & Scrap

Michael DimondSchool of Business Administration

Pricing Decisions

• Major influences on pricing decisions: Customers, competitors & costs.

• How companies make long-run pricing decisions.• Target-costing approach for product pricing.• Cost-plus approach for product pricing.• Antitrust laws & pricing.

Michael DimondSchool of Business Administration

Cost Management & Allocation

• A company’s revenues and costs differ across customers.• Customer-profitability analysis examines revenues earned

from customers and the direct costs incurred. • This helps management determine which customers are the

most profitable and strategically beneficial.

Michael DimondSchool of Business Administration

Consideration in customer-cost analysis• Customer output unit-level costs – these are per unit• Customer batch-level costs – cost per customer order, for

example, or per delivery• Customer-sustaining costs – cost to support individual

customers regardless of number of units or batches• Distribution-channel costs – these costs relate to the

distribution channel rather than to each unit or customer. For example, we might have a wholesale distribution manager’s salary and a retail distribution manager’s salary.

• Division-sustaining costs – costs that cannot be traced to a product, customer or even a distribution channel. An example would be the division manager’s salary.

Michael DimondSchool of Business Administration

Data for analysis

Michael DimondSchool of Business Administration

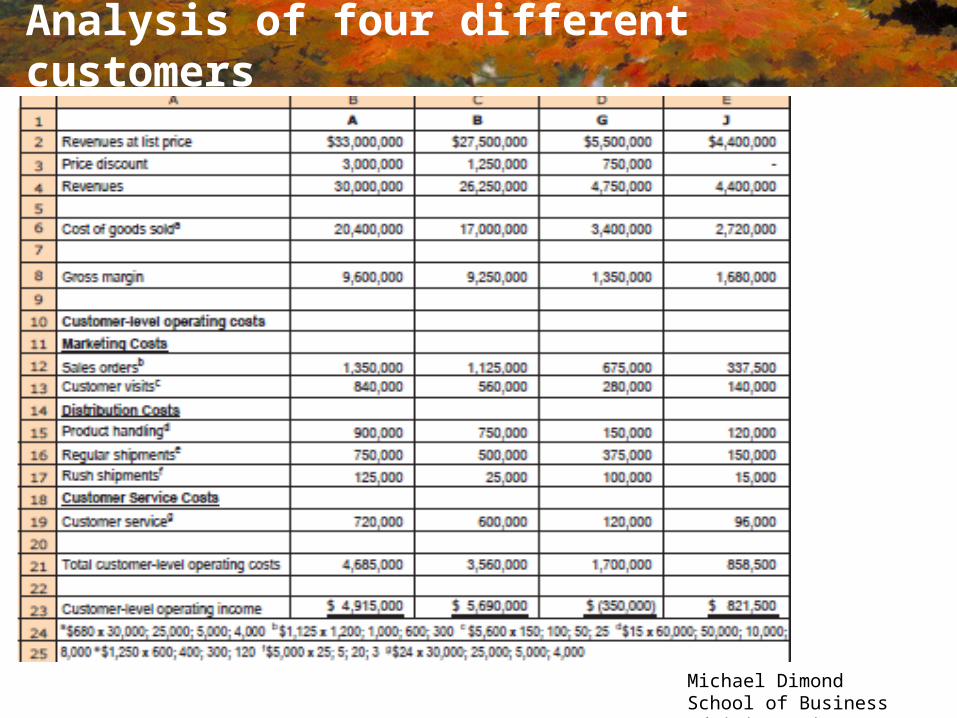

Analysis of four different customers

Michael DimondSchool of Business Administration

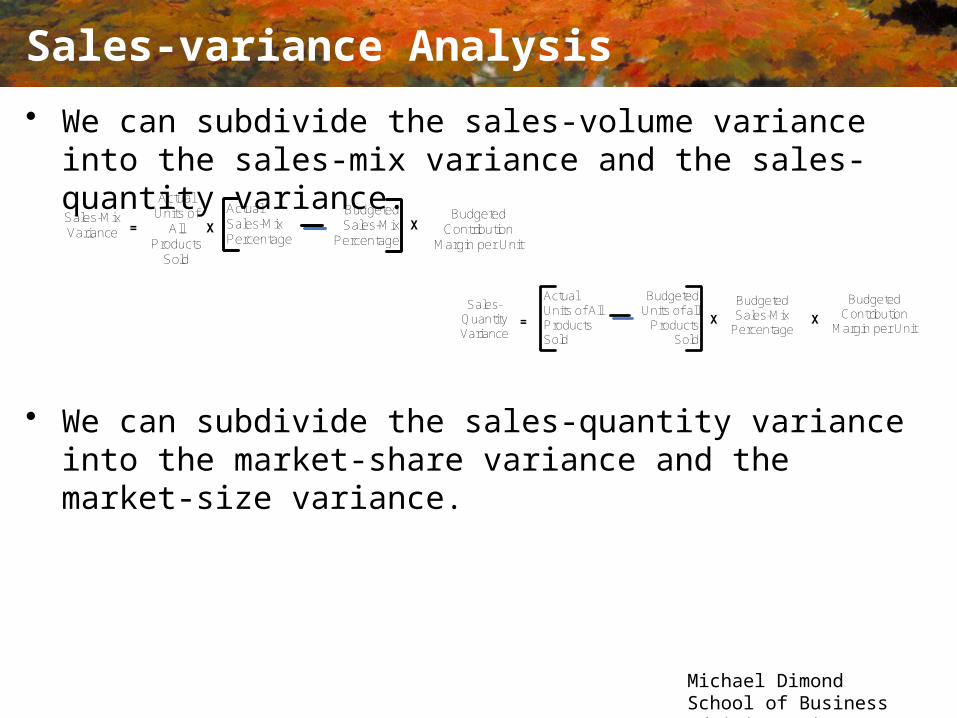

Sales-variance Analysis

• We can subdivide the sales-volume variance into the sales-mix variance and the sales-quantity variance.

• We can subdivide the sales-quantity variance into the market-share variance and the market-size variance.

Budgeted Sales-Mix

Percentage

Actual Sales-Mix Percentage

XBudgeted

Contribution Margin per Unit

Sales-Mix Variance =

Actual Units of

All Products

Sold

X

Budgeted Units of all

Products Sold

Actual Units of All Products Sold

Budgeted Contribution

Margin per Unit

Sales-Quantity Variance

=

Budgeted Sales-Mix

PercentageX X

Michael DimondSchool of Business Administration

Flexible-Budget and Sales-Volume Variances

Michael DimondSchool of Business Administration

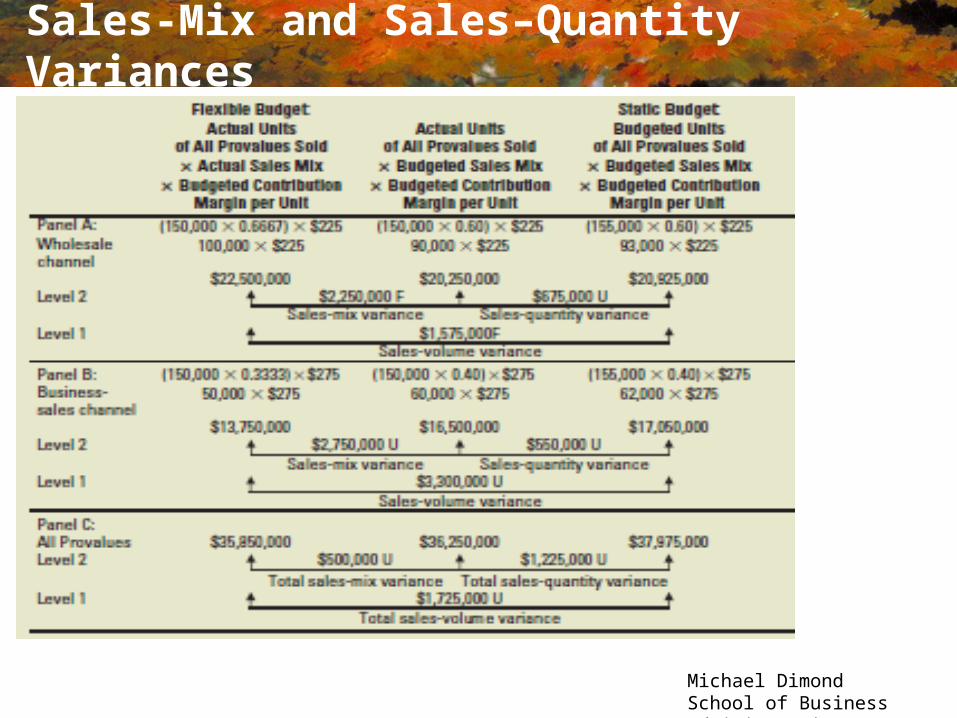

Sales-Mix and Sales–Quantity Variances

Michael DimondSchool of Business Administration

Support-department Cost Allocation

• Two methods: single-rate method vs the dual-rate method.• The single-rate method makes no distinction between fixed and variable

costs. It allocates costs in each cost pool to cost objects using the same rate per unit of a single allocation base.

• The dual-rate method divides the costs of each support department into two pools—a variable-cost pool and a fixed-cost pool.

• Divisional incentives are affected by the choice between allocation based on budgeted and actual rates and budgeted and actual usage.

• Costs of multiple support-departments can be allocated using the direct method, the step-down method, and the reciprocal method.

Michael DimondSchool of Business Administration

Direct vs Step-down Allocation

Michael DimondSchool of Business Administration

Common-cost Allocation

• Common-costs (costs shared by two or more users) are allocated using the stand-alone method and the incremental method.• The stand-alone cost-allocation method determines the weights for cost

allocation by considering each user of the cost as a separate entity. The cost is allocated among the users based upon the total cost for each separately.

• The incremental cost-allocation method ranks the individual users of the cost object in the order of users most responsible for the common cost and uses this ranking to allocate cost among those users. The first ranked user is the primary user and is assigned allocated costs up to the cost as a stand-alone user. The second ranked user is the first incremental user and is assigned cost equal to the additional cost that arises from having two users. This continues until costs have been assigned to all users.

Michael DimondSchool of Business Administration

Joint-cost Allocation

• Joint costs are costs of a production process that yields multiple products simultaneously. Joint costs are incurred prior to the splitoff point.• The splitoff point is defined as the point in the production process at which two

or more products become separately identifiable.• Separable costs are costs incurred beyond the splitoff point and include

manufacturing, marketing, distribution, and other costs.

• Joint costs can be allocated using two approaches: market-based data (sales revenue) or by using physical measures (weight, quantity, or volume).

• There are three methods that use the market-based data approach: Sales-value at splitoff method, net-realizable value (NRV) method, and constant gross-margin percentage NRV method

Michael DimondSchool of Business Administration

Byproducts

• a byproduct is a product emerging from a joint process that has relatively little sales value.

• Due to its inconsequential value, it is not beneficial to expend a large amount of resources accounting for byproducts. Two methods are utilized to account for byproducts.• The production method recognizes byproducts at the time production is

completed. The NRV of the byproduct is offset against the costs of the main product.

• The sales method recognizes the byproduct at the time of sale. No entries are made until the byproduct is sold. Revenues from the sale are reported as a revenue item in the period sold. These revenues can be grouped with sales, treated as other income, or deducted from cost of goods sold.

Michael DimondSchool of Business Administration

Spoilage, Rework & Scrap

• Three distinct categories of costs that result from defects in the manufacturing process are spoilage, rework, and scrap.

• Spoilage, rework, and scrap have different definitions in cost accounting than in common usage. Each receives a different accounting treatment.• Scrap is residual material that results from manufacturing a product. It has low

or zero sales value.• Spoilage is units of production that do not meet the specifications required by

customers for good units and are discarded or sold at reduced prices. Spoilage is further divided into two types: normal spoilage inherent in the production process and abnormal spoilage that is not considered a part of the production process.

• Rework is units of production that do not meet the specifications required by customers but are repaired and sold as good finished units.