china economic and market outlook jun ma, ph.d. chief economist for greater china head of china/hk...

TRANSCRIPT

China Economic and Market Outlook

Jun Ma, Ph.D.Chief Economist for Greater ChinaHead of China/HK Macro Strategy

Deutsche Bank AG

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters,

Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies

covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their investment decision. Independent, third-party research (IR) on certain companies

covered by DBSI's research is available to customers of DBSI in the United States at no cost. Customers can access IR at

http://gm.db.com/IndependentResearch or by calling 1-877-208-6300. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1.

Jun Ma (852) 2203 8308, [email protected] September 2009

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 2

Summary

Long-term outlook

2009-10 Economic outlook: a W shaped recovery

FAI growth will slow on fading stimulus

Export growth to recover strongly, and will be frontloaded

Real consumption growth to be sluggish, but nominal growth steady

2010 macro risks: overheating or stagflation?

When will the govt exit from expansionary macro policy?

Equity market outlook and strategy

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 3

We forecast that China’s nominal GDP will overtake the US within 10 years, much faster than we expected 2 years ago

Nominal GDP comparison between China and US (in USD tn)

-

5

10

15

20

25

2007

2008

2009

F

2010

F

2011

F

2012

F

2013

F

2014

F

2015

F

2016

F

2017

F

2018

F

2019

F

2020

F

China US

Source: Deutsche Bank

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 4

RMB to become a global reserve currency – imply that it needs to appreciate steadily over medium term

China announced the plan to build an international financial center in Shanghai by 2020 – implies that RMB needs to become convertible within 11 years

HKMA says the HKD may be pegged to the RMB when the latter becomes convertible

China has obviously signaled its desire to make the RMB a regional and eventually global reserve currency. Recent efforts include

– RMB settlement in trade between China and Hong Kong– Currency swaps arrangements with HK, Korea, Indonesia, Malaysia, Belarus,

and Argentina

An important condition for the RMB to become a reserve currency is that in the run up to that status, the RMB needs to be steadily appreciating.

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 5

However, on a long-term basis, stronger productivity growth should justify 3-5% annual appreciation of RMB vs USD

Total productivity factor growth (annual average), China vs. US

0%

1%

2%

3%

4%

5%

6%

1973-1981 1981-1992 1994-2004

US China

Source: ECB, IJ PEC, UN

Correlation between GDP over USA and Currency Appreciation against US$

Singapore, 87-97

Taiwan, 86-92

Korea, 86-90China, 05-08

India, 03-07

Thailand, 02-07

Singapore, 99-04

Taiwan, 99-04

India, 96-00-8

-6

-4

-2

0

2

4

6

8

0 1 2 3 4 5 6 7 8 9 10

GDP yoy over USA, US$

App

reci

atio

n a

gai

nst

US

$, p

pt

Source: Deutsche Bank, CEIC

China’s total factor productivity growth is 5ppts higher than that in the US, which allows China to steady appreciate its currency without losing competitiveness.

International experience also supports this trend

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 6

China-related investment opportunities over longer-term

Heath care: We estimate that China’s health care spending will grow at 1.3 times GDP growth in next ten years. This implies nearly 20% annual average growth in USD terms. Drug distribution is especially impressive in growth potential.

Equipment sector (power, medical, telco, shipbuilding, auto, auto parts): to gain 20% world market share from the current single digit levels.

Alternative energies

• Nuclear, Wind, Solar, Natural gas, Hybrid car batteries

Subways: China has 100 cities that need to build subways, and each of them is larger than Singapore.

Consumer

Diaper, packaging, funeral services, online travel, animation, etc.

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 7

Medium-term growth outlook

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 8

GD

P g

row

th Q

oQ

sa.

A double-dip scenario (or W shaped recovery) for GDP growth over next 1.5 years --- an illustrative example

Policy Stimulus

Source: Deutsche Bank.

FAI 1995-2002, corporate vs. government

Source: Deutsche Bank, CEIC

Real GDP growth, qoq %, saar.

0%

2%

4%

6%

8%

10%

12%

14%

1997Q4 1998Q1 1998Q2 1998Q3 1998Q4 1999Q1 1999Q2 1999Q3 1999Q4

Source: Deutsche Bank, CEIC

During crises, frontloaded policy stimulus tends to generate an invested V shape impact on economic growth. It occurred in 98-99 and will repeat in this round of economic recovery

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 9

China economic growth forecast for 2009 and 2010 Following the first dip in Q4 08, we expect growth to tentatively recover in

H1 this year but will likely slide again until hitting the 2nd trough in H1 2010.

Need to focus on qoq growth this year, which captures economic turning points 2-3 quarters earlier than yoy data.

Yoy and qoq annualized GDP growth forecast

Annualised sa qoq% yoy%2008Q1 9.4% 10.6%2008Q2 10.6% 10.1%2008Q3 6.5% 9.0%2008Q4 1.4% 6.8%2009Q1 5.9% 6.1%2009Q2 18.3% 7.9%2009Q3F 10.4% 8.8%2009Q4F 8.3% 10.5%2010Q1F 7.6% 11.0%2010Q2F 6.5% 8.3%2010Q3F 6.0% 7.4%2010Q4F 8.3% 7.1%

Source: Deutsche Bank

Deutsche Bank AG

Recent version to our “W”: higher Q2 with a more prolonged second dip

• Q2 GDP growth reached 18% on qoq saar basis. The most recent change in our view is that the second dip of the economy may last a bit longer (5 quarters) than previous forecast (4 quarters). Main reason is that govt spending program has delayed many companies’ capex reduction process.

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 10

China annulized qoq GDP growth forecast, saar %

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Source: Deutsche Bank

Deutsche Bank AG

Sequential qoq deceleration in H2 is becoming consensus

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 11

Consensus forecast of annualized qoq GDP growth by ten economists (%)

(2.0)-

2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0 18.0 20.0

2008 1Q 2008 2Q 2008 3Q 2008 4Q 2009 1Q 2009 2Q 2009 3Q* 2009 4Q*

Median Low High

Source: Wall Street J ournal poll by Andrew Baston. * Forecasts. The ten economists/institutions surveyed include Albert Keidel, Barclays, CICC, Citigroup, Deutsche Bank, Goldman Sachs, J .P. Morgan, Merrill Lynch, UBS and two others who names are withheld.

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 12

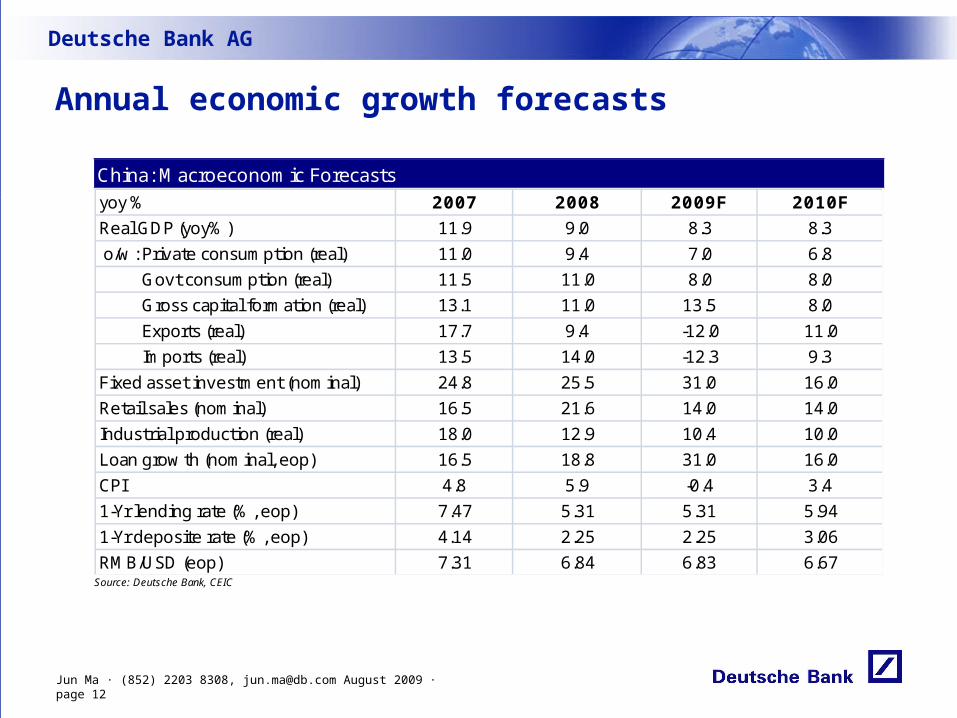

Annual economic growth forecasts

China: Macroeconomic Forecasts yoy % 2007 2008 2009F 2010F

Real GDP (yoy%) 11.9 9.0 8.3 8.3

o/w: Private consumption (real) 11.0 9.4 7.0 6.8

Govt consumption (real) 11.5 11.0 8.0 8.0

Gross capital formation (real) 13.1 11.0 13.5 8.0

Exports (real) 17.7 9.4 -12.0 11.0

Imports (real) 13.5 14.0 -12.3 9.3

Fixed asset investment (nominal) 24.8 25.5 31.0 16.0

Retail sales (nominal) 16.5 21.6 14.0 14.0

Industrial production (real) 18.0 12.9 10.4 10.0

Loan growth (nominal, eop) 16.5 18.8 31.0 16.0

CPI 4.8 5.9 -0.4 3.4

1-Yr lending rate (%, eop) 7.47 5.31 5.31 5.94

1-Yr deposite rate (%, eop) 4.14 2.25 2.25 3.06

RMB/USD (eop) 7.31 6.84 6.83 6.67 Source: Deutsche Bank, CEIC

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 13

Project approvals, lending and project starts have peaked sequentially By design, most centrally-

sponsored stimulus projects should have started this year. New lending peaked in Q1 this year. We think project new starts have peaked in Q2 this year

New lending peaked in 1Q09

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

3Q08 4Q08 1Q09 2Q09 3Q09F 4Q09F

RMB bn

Source: CEIC, Deutsche Bank

Project starts peaked in 2Q09

-

1.0

2.0

3.0

4.0

5.0

6.0

1Q09A 2Q09F 3Q09F 4Q09F 1Q10F

RMB tn

Source: CEIC, Deutsche Bank

Govt capex growth

0

100

200

300

400

500

600

700

0%10%20%30%40%50%60%70%80%90%

2008 2009F 2010F

Govt capital spending growth (yoy %, lhs)

Disbursement for stimulus (RMB bn, rhs)

Source: Deutsche Bank

Deutsche Bank AG

Govt-led FAI will likely fall from 60% yoy now to 10% in H2 2010

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 14

Government-led investment this cycle vs. 1998-99

-10%0%10%20%30%40%50%60%70%80%

-10%0%

10%20%30%40%50%60%70%80%

Mar

-97

Dec

-07

Jun-

97 M

ar-0

8

Sep-

97 J

un-0

8

Dec-

97 S

ep-0

8

Mar

-98

Dec

-08

Jun-

98 M

ar-0

9

Sep-

98 J

un-0

9F

Dec-

98 S

ep-0

9F

Mar

-99

Dec

-09F

Jun-

99 M

ar-1

0F

Sep-

99 J

un-1

0F

Dec-

99 S

ep-1

0F

Mar

-00

Dec

-10F

Jun-

00 M

ar-1

1F

Sep-

00 J

un-1

1F

Dec-

00 S

ep-1

1F

Govt FAI (1997-2000)

Govt FAI (2007-2011F)

Source: Deutsche Bank, CEIC Note: Government FAI(1997-2000) comprise agriculture and transport sectors; Government FAI(2007-2011F) comprise agriculture, transport, scientific research, water conversancy & environment, healthcare, education and culture

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 15

Corporate and real estate FAI

outlook

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 16

FAI breakdown by sector

Breakdown of FAI, 2009 ytd

Govt-led, 25.1%

Property, 22.6%

Manufacturing/Mining, 43.1%

Other services, 9%

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 17

Manufacturing FAI should follow industrial revenue growth

Manufacturing / mining revenue vs. FAI growth

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

F2

01

0F

FAI manufacturing & mining, yoy%Industrial revenue, yoy%

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Overcapacity requires capex deceleration

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 18

A large part of overcapacity is structural in nature

Global overcapacity also requires Chinese capex cuts in tradable sectors

Stimulus induced more capex addition, which will worsen overcapacity later

FAI of selected stimulus beneficiaries, yoy%, 3mma

30%

35%

40%

45%

50%

Source: Deutsche Bank, CEIC Note: the sectors included in this FAI series are non-metal mining, cement product, plastics, and non-ferrous. For non-ferrous, in addition to the stimulus of govt-led FAI, another important factor was govt restocking of inventory which partly induced a major spike in prices.

G3 capacity utilization rate

60%

65%

70%

75%

80%

85%

90%

95%

100%

105%

110%

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

US

EU

JP

Source: Deutsche Bank, CEIIC, Bloomberg Note: US figures are manufacturing capacity utilization rate (season adjusted) reported on SIC-basis (Standard Industrial Classification); EU figures are capacity utilization rate (sa) of EU 27 countries; J apan figures are manufacturing capacity utilization (2005 average =100) reported by J apanese Ministry of Economy, Trade and Industry.

China manufacturing capacity utilization diffusion index

-25

-20

-15

-10

-5

0

Ma

r-05

Jun-

05

Sep-

05

Dec

-05

Ma

r-06

Jun-

06

Sep-

06

Dec

-06

Ma

r-07

Jun-

07

Sep-

07

Dec

-07

Ma

r-08

Jun-

08

Sep-

08

Dec

-08

Ma

r-09

Jun-

09

Source: CEIC

Deutsche Bank AG

Real estate investment: an upside risk but can only offset 1/2 of govt-led capex slowdown

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 19

Real estate FAI vs. Govt-led FAI, 3mma, yoy%

-20%

0%

20%

40%

60%

80%Ju

l-07

Sep-

07

No

v-07

Jan-

08

Ma

r-08

Ma

y-08

Jul-0

8Se

p-0

8N

ov-0

8Ja

n-0

9M

ar-0

9M

ay-0

9Ju

l-09

Sep-

09

FN

ov-0

9F

Jan-

10

FM

ar-1

0F

Ma

y-10

FJu

l-10

FSe

p-1

0F

No

v-10

F

GovtPptyGovt+Ppty

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Export growth likely rise by 35ppts in next 12 months

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 21

China export vs. G3 GDP

-6%

-4%

-2%

0%

2%

4%

6%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

No

v-99

Jul-0

0

Ma

r-01

No

v-01

Jul-0

2

Ma

r-03

No

v-03

Jul-0

4

Ma

r-05

No

v-05

Jul-0

6

Ma

r-07

No

v-07

Jul-0

8

Ma

r-09

No

v-09

Jul-1

0

China export growth, yoy % (lhs) China export forecast

G3 real GDP, yoy % (rhs) G3 GDP forecast

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Stronger and front-loaded export growth recovery

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 22

Changes to China’s export forecast

-30%

-20%

-10%

0%

10%

20%

30%

Jul-0

8

Sep-

08

No

v-08

Jan-

09

Ma

r-09

Ma

y-09

Jul-0

9

Sep-

09

No

v-09

Jan-

10

Ma

r-10

Ma

y-10

Jul-1

0

Sep-

10

No

v-10

Export, yoy%, 3mma Previous forecast New forecast

Source: Deutsche Bank

Deutsche Bank AG

Why will export growth surprise to the upside?

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 23

For each 1ppt rise in G3 GDP, Chinese export growth recovers by 7ppts. We expect US GDP growth to recovery 6ppts within next 12 months. For next 3-4 quarters, US economy will likely experience a V shape recovery, due to:

normalization of inventory -- if every company increases inventory from 2 weeks back to 2 months, it would lead to 12% GDP growth!

normalization of auto sales -- as long as auto sales recover to replacement demand level (replacing broken cars only), auto sales will rise 25%;

if housing starts return to household formation level (# of new households per yr), it requires 20% increase in housing starts per yr in next 4 yrs.

We think China's export recovery will be much more front-loaded than market expectations. If China's monthly export recovery (mom increase) maintains at half of the pace seen over past two months (5% rise each in June and July), we should see 26ppt recovery from now to Dec. If the mom recovery maintains the pace in past two months, we should see 35ppt recovery in next 5 months.

Deutsche Bank AG

US new orders index now substantially higher than that in China

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 24

US ISM index

20

30

40

50

60

70

80

Au

g-00

Dec

-00

Ap

r-01

Au

g-01

Dec

-01

Ap

r-02

Au

g-02

Dec

-02

Ap

r-03

Au

g-03

Dec

-03

Ap

r-04

Au

g-04

Dec

-04

Ap

r-05

Au

g-05

Dec

-05

Ap

r-06

Au

g-06

Dec

-06

Ap

r-07

Au

g-07

Dec

-07

Ap

r-08

Au

g-08

Dec

-08

Ap

r-09

Au

g-09

Manufacturing PMI

New Orders Index

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 25

Exports > consumer > FAI

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 26

Exports to significantly outperform FAI over next 12 months

We expect export growth to rally by 35ppts in next 12 months, while FAI growth to slow by about 20ppts. This suggests a pair trade between export-related sectors against construction materials.

This divergence is almost identical to 1999, when exports rallied together with a plunge in FAI growth, following the perk of stimulus.

1997-99 FAI vs. exports

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0%

5%

10%

15%

20%

25%

Sep-

96

Dec

-96

Ma

r-97

Jun-

97

Sep-

97

Dec

-97

Ma

r-98

Jun-

98

Sep-

98

Dec

-98

Ma

r-99

Jun-

99

Sep-

99

Dec

-99

Ma

r-00

Jun-

00

FAI, yoy%, 3mma (lhs) Export, yoy%, 3mma (rhs)

Source: Deutsche Bank, CEIC

Export growth vs. FAI growth, yoy %

-30%

-20%

-10%

0%

10%

20%

30%

40%

0%5%

10%15%20%25%30%35%40%

Ma

r-06

Jul-0

6

No

v-06

Ma

r-07

Jul-0

7

No

v-07

Ma

r-08

Jul-0

8

No

v-08

Ma

r-09

Jul-0

9

No

v-09

Ma

r-10

Jul-1

0

No

v-10

FAI, yoy%, 3mma (lhs) FAI forecast

Export, yoy%, 3mma (rhs) Export forecast

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Export-related companies vs investment goods producers

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 27

Updated list of export-related companies

Ticker Company Market cap (US$ bn) Sector DB rating

3988 HK BANK OF CHINA 140,735 Bank Buy

763 HK ZTE 8,842 Telco equipment Buy

144 HK CHINA MERCHANT 8,302 Port operator Hold

316 HK ORIENT OVERSEAS 3,358 Container shipping Buy

2038 HK FOXCONN INTL 4,646 Electronic Hold

551 HK YUE YUEN INDUS 4,488 Footwear NR

669 HK TECHTRONIC INDS 1,384 Electronic NR

285 HK BYD ELECTRONIC 1,154 Electronic Hold

321 HK TEXWINCA HLDG 1,031 Textile Buy Source: Deutsche Bank; Note: NR (none-rate) stocks are not covered by Deutsche Banks’ fundamental research and consequently we make no representations relation to the quality of the business, assets or management

Updated list of investment-related companies

Ticker Company Market cap (US$ bn) Sector DB rating

347 HK ANGANG STEEL 14,331 Steel Hold

358 HK J IANGXI COPPER 11,831 Copper Sell

1171 HK YANZHOU COAL 10,568 Coke NR

1138 HK CHINA SHIP DVLP 6,020 Dry bulk Sell

323 HK MAANSHAN IRON 5,501 Steel Sell

3993 HK CHINA MOLYBDENUM 4,038 Non-ferrous Sell

3808 HK SINOTRUCK 2,474 Truck Hold Source: Deutsche Bank; Note: NR (none-rate) stocks are not covered by Deutsche Banks’ fundamental research and consequently we make no representations relation to the quality of the business, assets or management

Deutsche Bank AG

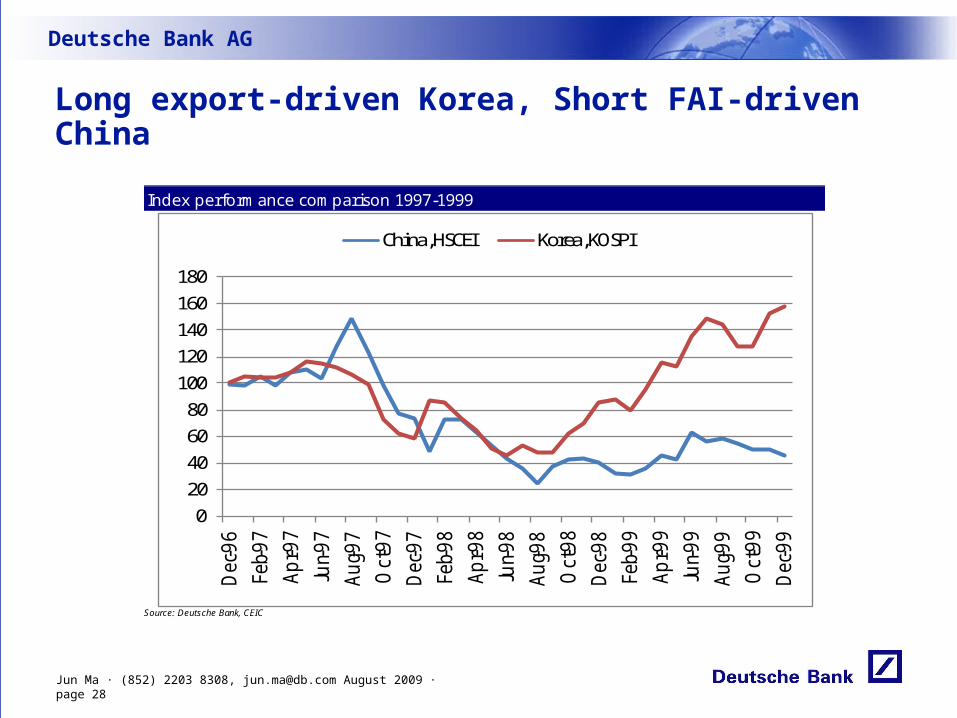

Long export-driven Korea, Short FAI-driven China

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 28

Index performance comparison 1997-1999

020406080

100120140160180

Dec

-96

Feb-

97

Ap

r-97

Jun-

97

Au

g-97

Oct

-97

Dec

-97

Feb-

98

Ap

r-98

Jun-

98

Au

g-98

Oct

-98

Dec

-98

Feb-

99

Ap

r-99

Jun-

99

Au

g-99

Oct

-99

Dec

-99

China, HSCEI Korea, KOSPI

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Potential beneficiaries of new stimulus for consumer and technology

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 29

Potential beneficiaries from a second round of stimulus 28-Jun PB

Company Ticker Sector Rating Price local M. cap (US$m)

2008 2009 2009

CHSTE 0658.HK Capital Goods Buy 16.2 2,590 19.9 17.4 3.8 24%

China Dongxiang 3818.HK Consumer Durables & Apparel Buy 5.3 3,699 13.7 18.3 3.5 9%

China Foods 0506.HK Food, Beverage & Tobacco Buy 4.7 1,671 21.2 17.7 2.4 20%

Mengniu Dairy 2319.HK Food, Beverage & Tobacco Buy 18.1 3,474 NM 25.8 4.6 -207%

Golden Eagle Retail 3308.HK Retailing Buy 8.4 1,885 19.1 19.4 6.4 12%

Ports Design Limited 0589.HK Consumer Durables & Apparel Buy 18.7 1,249 23.0 20.3 6.1 8%

Gome 0493.HK Retailing Buy 1.9 3,144 24.1 18.3 2.3 -4%

Beijing Cap Int'L Airport 0694.HK Transportation Buy 5.4 3,001 302.2 67.1 1.6 99%

Yingli Green Energy YGE.N Capital Goods Hold 13.2 1,696 20.2 20.6 2.2 -15%

Ctrip CTRP.OQ Consumer Services Hold 44.8 2,966 47.9 39.3 8.7 16%

PEEPS CAGR

08-10

Source: Deutsche Bank

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 30

Structural trends support sustainable growth in several consumer spending categories

Diaper

Packaging

Funeral services

Drug distribution

Online travel

Animation, etc.

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 31

Inflation to surprise on upside

-- overheating or stagflation?

Deutsche Bank AG

We expect CPI inflation to rise from current -1.8% yoy to 4% by mid next year

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 32

CPI projection, yoy%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%Ja

n-08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Forecast

Source: Deutsche Bank, CEIC

Deutsche Bank AG

M2 growth, currently running at 29% yoy, will transmit to CPI with a 12-month lag

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 33

Differential between yoy M2 growth and nominal GDP growth, ppts

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Ma

r-93

Jan-

94

No

v-94

Sep-

95

Jul-9

6

Ma

y-97

Ma

r-98

Jan-

99

No

v-99

Sep-

00

Jul-0

1

Ma

y-02

Ma

r-03

Jan-

04

No

v-04

Sep-

05

Jul-0

6

Ma

y-07

Ma

r-08

Jan-

09

Source: Deutsche Bank, CEIC

Yoy M2 growth comparison – China vs. other countries, J une/J uly 2009

0%

5%

10%

15%

20%

25%

30%

35%

China India Korea Thailand UK USA Taiwan EU

Source: Deutsche Bank, CEIC

China’s M2 growth is 3 times that in the US and other major countries

M2 growth is now 24ppts higher than nominal GDP growth in China

CPI driven by M2 with 12-month lag

10%

15%

20%

25%

30%

35%

40%

45%

50%

-5%

0%

5%

10%

15%

20%

25%

30%

Jun-

91

Ma

r-92

Dec

-92

Sep-

93

Jun-

94

Ma

r-95

Dec

-95

Sep-

96

Jun-

97

Ma

r-98

Dec

-98

Sep-

99

Jun-

00

Ma

r-01

Dec

-01

Sep-

02

Jun-

03

Ma

r-04

Dec

-04

Sep-

05

Jun-

06

Ma

r-07

Dec

-07

Sep-

08

Jun-

09

CPI (lhs) M2 (rhs)

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Why can inflation rise despite overcapacity?

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 34

China CPI component weights

Residence, 13%

Services, 26%

Manufactured goods, 29%

Food, 33%

Source: Deutsche Bank, CEIC

Overcapacity may restrain inflation of manufactured goods, but the majority of China’s CPI basket (71%) are non-manufacturing and are more subject to cost push inflation. The latter can be driven by speculative demand due to excess liquidity (e.g., oil, soft commodities, copper, property, etc)

Cost push inflation is perfectly possible even when capacity utilization is falling

The CPI can surge when capacity utilization falls: the US during 1973-74

70%72%74%76%78%80%82%84%86%88%90%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Jan-

72

Ma

y-72

Sep-

72

Jan-

73

Ma

y-73

Sep-

73

Jan-

74

Ma

y-74

Sep-

74

Jan-

75

Ma

y-75

Sep-

75

Jan-

76

Ma

y-76

Sep-

76

Jan-

77

Ma

y-77

CPI, yoy % (lhs) Capacity utilization rate, % (rhs)

Source: Deutsche Bank, CEIC

Deutsche Bank AG

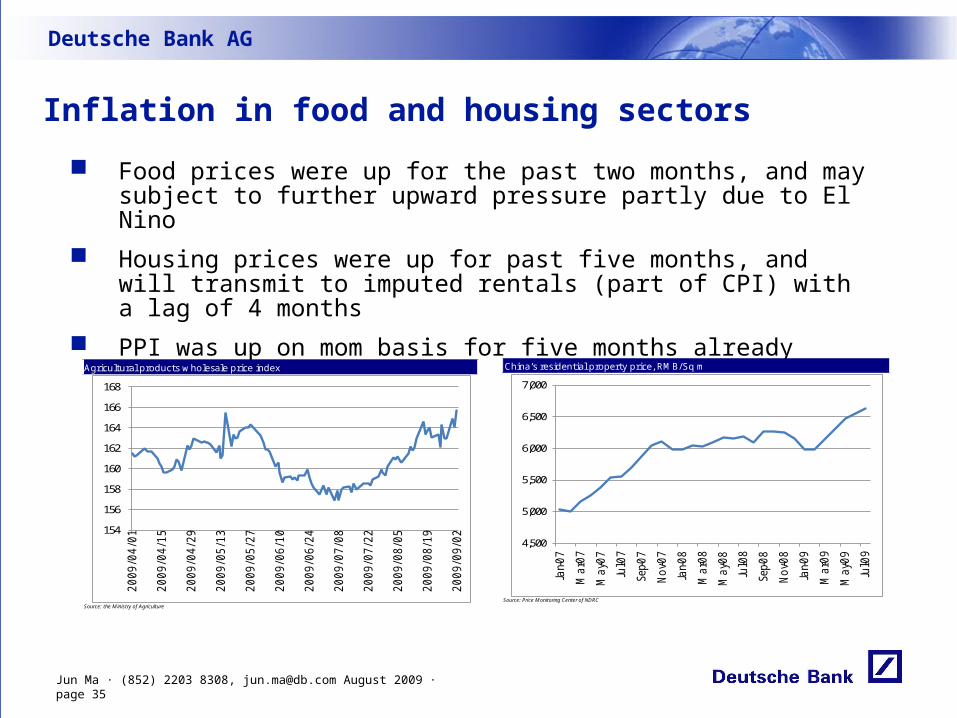

Inflation in food and housing sectors

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 35

Food prices were up for the past two months, and may subject to further upward pressure partly due to El Nino

Housing prices were up for past five months, and will transmit to imputed rentals (part of CPI) with a lag of 4 months

PPI was up on mom basis for five months already

Agricultural products wholesale price index

154

156

158

160

162

164

166

168

20

09

/04

/01

20

09

/04

/15

20

09

/04

/29

20

09

/05

/13

20

09

/05

/27

20

09

/06

/10

20

09

/06

/24

20

09

/07

/08

20

09

/07

/22

20

09

/08

/05

20

09

/08

/19

20

09

/09

/02

Source: the Ministry of Agriculture

China’s residential property price, RMB/Sq m

4,500

5,000

5,500

6,000

6,500

7,000

Jan-

07

Ma

r-07

Ma

y-07

Jul-0

7

Sep-

07

No

v-07

Jan-

08

Ma

r-08

Ma

y-08

Jul-0

8

Sep-

08

No

v-08

Jan-

09

Ma

r-09

Ma

y-09

Jul-0

9

Source: Price Monitoring Center of NDRC

Deutsche Bank AG

Medium-term (2Q10-2Q11) macro risk: overheating or stagflation?

1. Scenario I (base case: 40% probability): yoy GDP growth at around 8%, inflation at around 3%

loan and FAI growth has slowed significantly as new project starts decline and old projects are getting finished. Food and commodity prices are steady.

2. Scenario II (stagflation: 25% probability): GDP growth falling to 7%, inflation rising to 4% and uptrend continuing

inflation rising due to food price increases, speculative buying of commodities leading to PPI and then CPI increase. Very negative for equity market.

3. Scenario III (overheating: 25% probability) : GDP at 11-12%, inflation above 4% and rising

inflation due to continued strong FAI and lending growth. But eventually lead to massive policy tightening. Abrupt market reactions: from bubbles to bursting.

4. Scenario IV (high growth, no inflation, 10% probability). 10% GDP growth, CPI below 2%

monetary expansion does not transmit to inflation (historical transmission breaks down). Weather and commodities prices behave well. Best for equity.

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 36

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 37

How and when to exit from stimulus?

Deutsche Bank AG

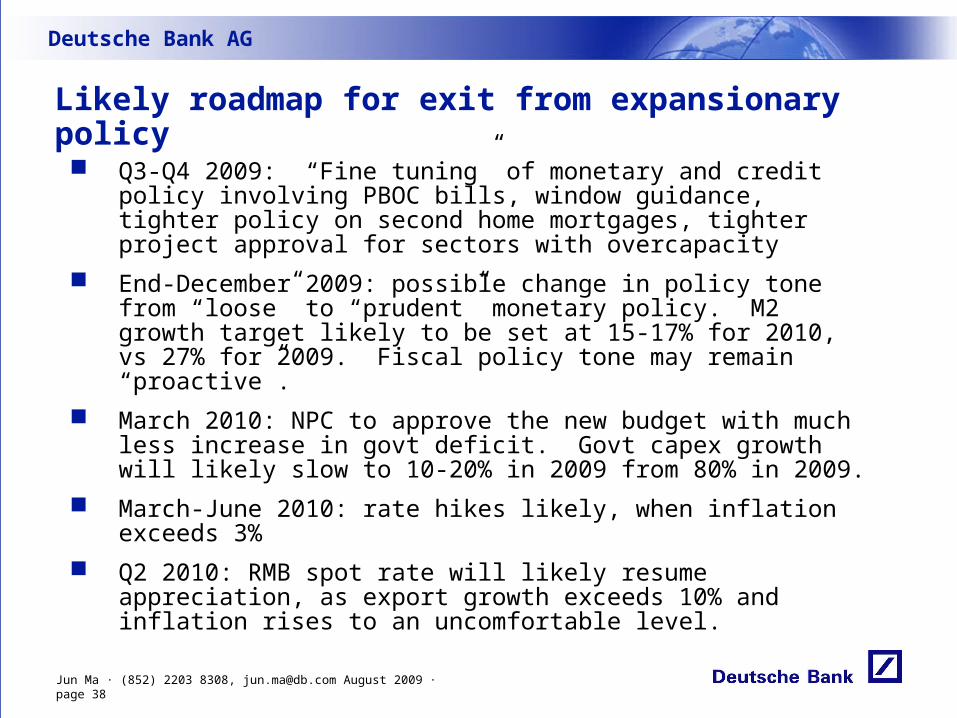

Likely roadmap for exit from expansionary policy

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 38

Q3-Q4 2009: “Fine tuning” of monetary and credit policy involving PBOC bills, window guidance, tighter policy on second home mortgages, tighter project approval for sectors with overcapacity

End-December 2009: possible change in policy tone from “loose” to “prudent” monetary policy. M2 growth target likely to be set at 15-17% for 2010, vs 27% for 2009. Fiscal policy tone may remain “proactive”.

March 2010: NPC to approve the new budget with much less increase in govt deficit. Govt capex growth will likely slow to 10-20% in 2009 from 80% in 2009.

March-June 2010: rate hikes likely, when inflation exceeds 3%

Q2 2010: RMB spot rate will likely resume appreciation, as export growth exceeds 10% and inflation rises to an uncomfortable level.

Deutsche Bank AG

Net lending deceleration is certain with or without monetary policy tightening; we forecast net lending to slow to RMB400bn per month in H2 from RMB1.2tn/m in H1Reasons for loan growth slowdown include:

• Project starts will decline in H2 by policy design.

• Two major banks have announced that they intend to slow net lending to RMB200bn in H2 from RMB800-900bn in H1.

• Many companies have over-borrowed and loan demand will slow in H2.

• PBOC and ICBC are adopting “fine-tuning” measures to slow loan growth, for fear that excess loan growth would lead to inflation, bad loans, and asset bubbles.

• Specific measures that regulators are taking right now include open market operations, window guidance, and targeted bill issuance. Next options will include an increase in the reserve requirement. CBRC will likely further tighten mortgage policies on second homes.

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 39

Deutsche Bank AG

Loan and FAI forecast, yoy %

0%5%

10%15%20%25%30%35%40%45%

Jan-

08

Ma

r-08

Ma

y-08

Jul-0

8

Sep-

08

No

v-08

Jan-

09

Ma

r-09

Ma

y-09

Jul-0

9

Sep-

09

No

v-09

Jan-

10

Ma

r-10

Ma

y-10

Jul-1

0

Sep-

10

No

v-10

Loan growth FAI single month growth

Source: Deutsche Bank, CEIC

Based on project starts profile, our projection is that yoy loan growth will peak in Q3 at 34% yoy, and decelerate towards 17% yoy at end-2010

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 40

Forecast

Deutsche Bank AG

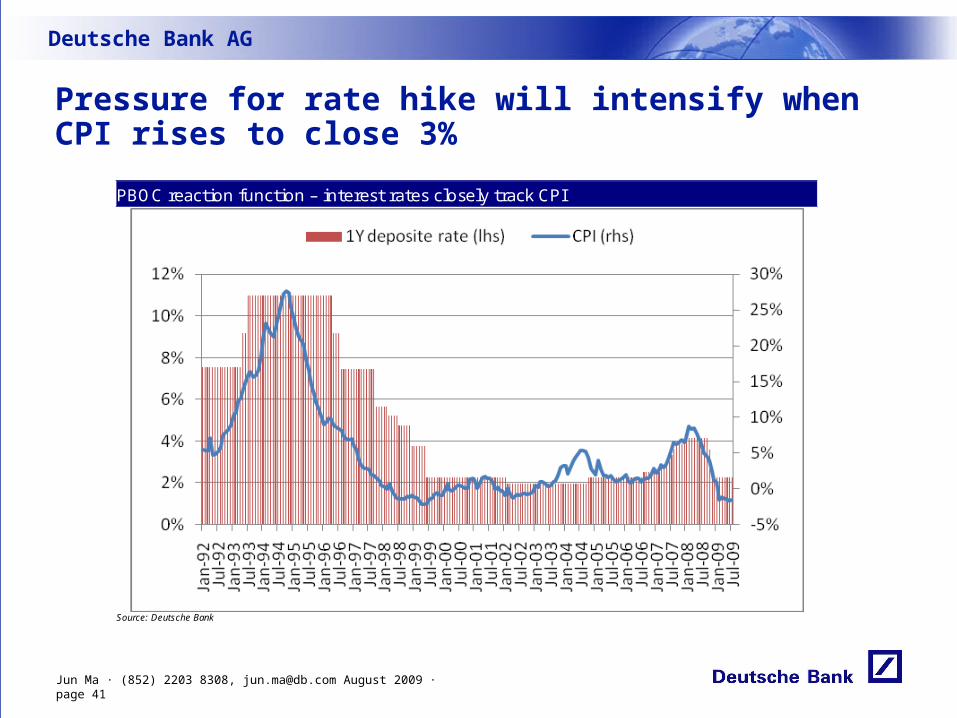

Pressure for rate hike will intensify when CPI rises to close 3%

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 41

PBOC reaction function – interest rates closely track CPI

Source: Deutsche Bank

Deutsche Bank AG

Mar-Jun 10 is good timing of rate hikes – justified by overheating concern but constrained by stagflation concern

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 42

Overheating and Stagflation? Look at what GDP and CPI say

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

6%

7%

8%

9%

10%

11%

12%

GDP, yoy % CPI, yoy %

Source: Deutsche Bank

Stagflation concern

Overheating concern

Deutsche Bank AG

How to play inflation

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 43

Potential Victim #1: Property Mortgage demand is most sensitive to rate hikesProperty companies are highly leveraged

Potential Victim # 2: Oil reining, IPPs, and F&B processing

When CPI inflation rises to 4%, the government tends to exercise price intervention, which will depress margin

Banking? Impact on NIM depends on how asymmetric the rate

hikes will beMacro sentiment tends to suffer as there will be growing

fear of overheating or stagflationBeneficiaries

Insurance, soft commodities, retailers, and airlines

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 44

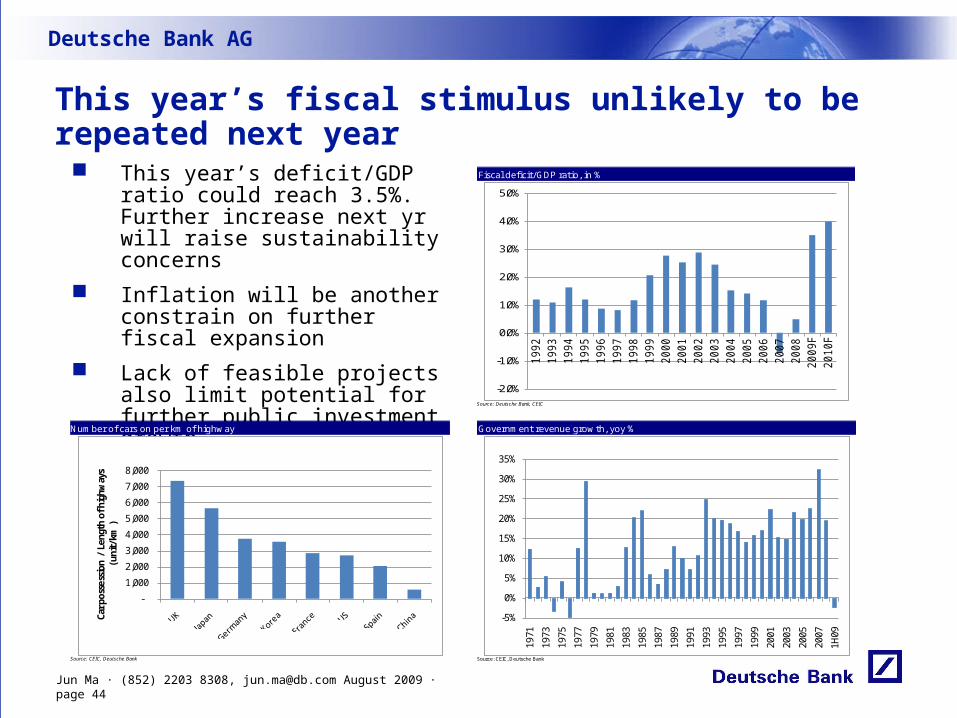

This year’s fiscal stimulus unlikely to be repeated next year

This year’s deficit/GDP ratio could reach 3.5%. Further increase next yr will raise sustainability concerns

Inflation will be another constrain on further fiscal expansion

Lack of feasible projects also limit potential for further public investment growth

Number of cars on per km of highway

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Car p

osse

ssio

n /

Leng

th o

f hig

hway

s

( u

nit/

km )

Source: CEIC, Deutsche Bank

Government revenue growth, yoy %

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

1H09

Source: CEIC, Deutsche Bank

Fiscal deficit/GDP ratio, in %

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

F

20

10

F

Source: Deutsche Bank, CEIC

Deutsche Bank AG

Shift of fiscal focus to supporting consumption and tech

• Size of 2010 stimulus will be smaller

• New stimulus will be much less investment focused • State Council said recently that [we] “should stimulate domestic demand especially

consumer demand, and keep investment growth steady”

• New stimulus will have to be more focused on social welfare and consumption, and technology• Proposals made include using tax policy, consumer coupons, and govt investments to

stimulate• Milk consumption• Wine consumption• Travel consumption• Sports and cultural activities• Credit card• Alternative energy• Incentives for R&D and upgrading

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 45

Deutsche Bank AG

RMB will likely resume appreciation from Q2

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 46

By Q2 2001, we expect export growth will be close to 10% yoy, and should eliminate the most important reason that led to the early decision to stop RMB appreciation

Inflation of 3-4% will provide another argument for using RMB appreciation to contain imported inflation

So we expect RMB spot rate to resume appreciation from Q2 next year

RMB NDR should start reflect the appreciation trend from end of this year or beginning of next year

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 47

Market Outlook and Strategy

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 48

DB EPS forecasts and market valuations

Valuation and EPS forecast

EPS growth (%) 2008A 2009F 2010F

HSI -11.6 1.2 11.0

HSCEI -13.8 18.3 18.5

MSCI HK -6.9 -11.2 14.4

MSCI CN -13.0 15.8 17.5

SHCOMP -16.4 27.1 22.4

P/E 2008A 2009F 2010F

HSI 11.4 16.4 14.7

HSCEI 12.0 15.6 13.2

MSCI HK 12.4 20.7 18.1

MSCI CN 12.6 16.1 13.7

SHCOMP 27.6 21.1 17.2 Note: Data as of September 9 2009 Source: Deutsche Bank

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 49

We think China’s equity market will under perform markets in other

Asia economies (e.g. Korea) which are mainly driven by the US recovery. This is because China is beginning to experience qoq economic deceleration due to fading stimulus, while the US is just beginning its exceptionally strong sequential recovery.

On China market indices, we see upside in the remainder of this year, as in the initial stage of inflation corporates tend to be net beneficiaries. In H1 next year, the macro environment -- further inflation and mounting pressure for rate hikes/price control as well as stagflation fear– will become negative to the market.

Within H1 next year, market sentiment will likely be volatile, switching from the initial fear of overheating to mid year’s stagflation. Banks’ NIM and many corporates’ margin will swing.

On sectors, we are overweight on export-related sectors (til end of this year) followed by consumer, technology and insurance. We dislike investment-related sectors (in short term), property (from next year), oil refining and power (from next year).

Market outlook and strategy

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 50

Our top Buys

Top 10 picks 9-Sep PB

Company Ticker Sector Rating Price

local

M. cap

(US$m)2009 2010 2009

China Life Insurance 2628.HK Insurance Buy 35.0 127,640 27.8 22.4 4.0 35%

Bank Of China 3988.HK Banks Buy 4.2 135,919 12.4 10.5 1.9 17%

OOIL 0316.HK Transportation Buy 44.3 3,573 NM 40.2 0.9 -43%

CHSTE 0658.HK Capital Goods Buy 18.0 2,885 21.6 16.4 4.4 37%

Golden Eagle Retail 3308.HK Retailing Buy 11.0 2,511 23.5 20.7 8.9 21%

Tencent 0700.HK Software & Services Buy 128.5 29,664 41.3 30.3 18.0 57%

China Comservice 0552.HK Telecommunication ServicesBuy 4.6 3,433 14.2 12.9 1.7 17%

Hengan Intl. 1044.HK Household & Personal ProductsBuy 44.7 7,012 26.8 22.0 6.7 36%

China Merchants 0144.HK Transportation Buy 27.4 8,568 23.7 20.4 2.1 3%

Foxconn Int'L Holdings 2038.HK Technology Hardware & EquipmentHold 4.9 4,400 43.2 15.7 1.3 53%

HSCEI 15.4 13.9 2.1 19%

PE EPS

CAGR 08-

10

Source: Deutsche Bank

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 51

Appendix 1

Important DisclosuresAdditional Information Available upon Request

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com.

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst(s). In addition, the undersigned lead analyst(s) has not and will not receive any compensation for providing a specific recommendation or view in this report. Jun Ma

Deutsche Bank AG

Jun Ma · (852) 2203 8308, [email protected] August 2009 · page 52

Regulatory Disclosures

1. Important Additional Conflict Disclosures

Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the “Disclosures Lookup” and “Legal” tabs. Investors are strongly encouraged to review this information before investing.

2. Short-Term Trade Ideas

Deutsche Bank equity research analysts sometimes have shorter-term trade ideas (known as SOLAR ideas) that are consistent or inconsistent with Deutsche Bank’s existing longer term ratings. These trade ideas can be found at the SOLAR link at http://gm.db.com.

3. Country-Specific Disclosures

Australia: This research, and any access to it, is intended only for “wholesale clients” within the meaning of the Australian Corporations Act.

EU countries: Disclosures relating to our obligations under MiFiD can be found at http://globalmarkets.db.com/riskdisclosures.

Japan: Disclosures under the Financial Instruments and Exchange Law: Company name – Deutsche Securities Inc. Registration number – Registered as a financial instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, The Financial Futures Association of Japan. Commissions and risks involved in stock transactions – for stock transactions, we charge stock commissions and consumption tax by multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional losses stemming from foreign exchange fluctuations.

New Zealand: This research is not intended for, and should not be given to, “members of the public” within the meaning of the New Zealand Securities Market Act 1988.

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute, any appraisal or evaluation activity requiring a license in the Russian Federation.