chip technology - cuna councils · •consumer education is key to success •fraud migration...

TRANSCRIPT

Chip TechnologyJune 14, 2012

Leanne Phelps, SVP Card Services, State ECU, Raleigh, NC

Danny Clark, Credit Card Fraud Strategy & Analytics | Group Security , Lloyd’s Banking Group (LBG), London

UK Chip and PIN Deployment

14th June 2012

Danny Clark - BiographyDanny Clark has worked in the Financial Services industry for 23 years starting his career

at NatWest Bank. Danny Spent 11 years at NatWest undertaking a number of roles including Senior Fraud investigator within debit cards, ATM and cheque fraud. Danny also undertook a number of Credit Risk roles whilst at NatWest in credit card issuing.

Following his departure from NatWest, Danny moved on to work at Morgan Stanley UK (Discover Financial Services) credit cards and was responsible for fraud strategy. Danny was one of the key stakeholders at Morgan Stanley for the Chip & PIN roll out project and sat on the APACS Plastic Fraud Prevention Forum steering group for Chip and PIN. Whilst at Morgan Stanley he was involved with several data migrations and Falcon installations.

He has spent the past 3 years at Lloyds Banking Group (LBG) managing the credit card fraud strategy team responsible for approx 13m cards. The LBG portfolio is made up of two portfolios, LTSB and HBOS. Both of these brands are currently 1st and 2nd

respectively in the industry when measured against its core peers from a loss per card perspective.

Lessons Learned•Consumer education is key to success

•Fraud Migration

•Customer authentication across channels

•Pace of the migration needs to be balanced

•Protect your PIN

•Risk Management

•Scripting

•Pilot undertaken in a small geographical area

•Consideration given to PIN fall back (damaged chips)

•Policy for chip and signature cards

•Policy decisions for cross boarder transactions (non chip terminals)

•Self Select PIN

•DDA vulnerabilities

•Host system set up

SECU Approach to EMV

• Non-profit financial cooperative serving state employees, teachers and family members in North Carolina

• 1.7 million members

• 245 branch offices

• 1100 ATMs

About State Employees’ Credit Union

• Debit Portfolio– 1.1 million Visa Check Cards– 28,000 Cash Points Global Cards– $4.8 billion annual purchase volume – 154 million transactions

• Credit Portfolio– 230,000 Visa credit cards– $520 M Open credit lines– 11 million transactions

SECU Debit Card Program

• Problem free acceptance for our member– International operability

• Begin migration to dynamic data transaction processing in a real time environment

• Counterfeit is our biggest challenge• US is a prime target and will only worsen as

Canada and Mexico implement• Fraudster’s technology continues to be refined

SECU Migration to Chip – why now?

• Learn the lingo! – On-line versus off-line is not what it used to be– Talk to vendors and industry experts– Talk to vendors and industry experts some more!

• Phased Approach – Phase 1 – Reissue all SECU debit cards as Chip and Signature

• This will eliminate acceptance issues for our members internationally

• Our BINs will be recognized as “chip enabled”• Cash Points Global reissued April 2011• Visa Check Debit reissue completed in October 2011• Credit to be re-issued as chip

SECU’s Approach

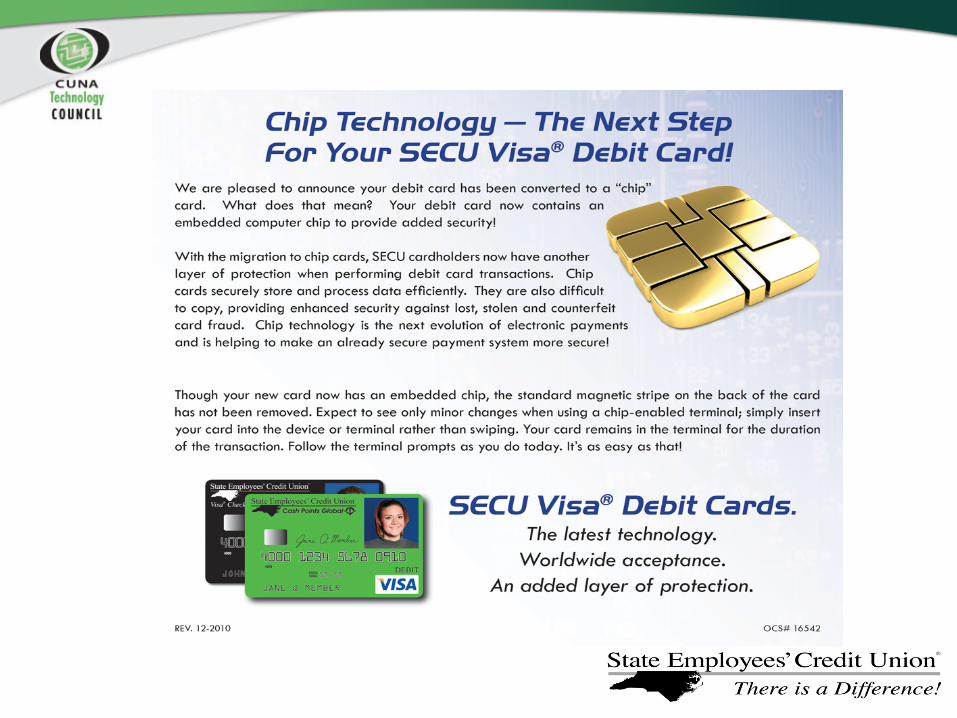

• SECU implemented EMV using the “Visa Early Option” which takes advantage of Visa’s chip authentication service. Visa will authenticate the cryptogram from the chip and pass the results to SECU.

• Our initial deployment supports chip and on-line PIN or chip and signature”– When SECU card is presented at a chip enabled terminal,

the card will be authenticated through the chip– The cardholder can be authenticated with a signature or PIN

depending upon merchant capability– Will not work at unattended terminals outside US due to no

off-line PIN support• Cards continue to have mag stripe for use at non-chip

terminals

SECU’s Chip and PIN rollout

Chip transaction activity begins in North Carolina July 2011!

Merchant Acceptance Issues

Don’t assume anything!

Let the real challenges begin!

• Phase 2– ATM upgrades – install/enable chip readers– Upgrade ATM application software – Host changes for EMV support from our ATM

network– Visa DPS upgrades to support acquiring

transaction activity – Visa DPS support for M-Chip EMV to enable

Visa and MasterCard chip profiles on same card??

What’s Next at SECU?

• MasterCard liability shift for ATM Acquirers– April 2013

• Visa liability shift for Acquirers – October 1, 2015 – October 1, 2017 for AFD merchants

Network Mandates

– Visa • Provided International expertise and project resources• VisaNet changes • Certification Testing • Chip profile tool

– Visa DPS• Provides SECU transaction switch services • Project management for overall project• ISO changes for additional data elements

Project Team

– Oberthur Technologies• SECU debit card personalization services • Experience in chip technology in international markets• Provided plastics and chip production

– CV Systems• Host vendor for transaction processing software

– SECU Project Team• Business Users• Host programmers• Marketing

Project Team

• Word of mouth– Advisory Boards

– Employee education

– Newsletter Articles

– Insert with card mailings

– Updates to card carriers

Member Education

Contact me:

Leanne PhelpsSVP Card Services State Employees’ Credit Union1-800-662-7508 or 919-839-5349