container industry outlook - container owners association · container industry outlook the ‘new...

TRANSCRIPT

Container Industry Outlook

The ‘New Normal’ for

Container Owners

Rotterdam - November 14th 2016

Mark Bennett

Not much good news• Shipping line record losses

• The largest bankruptcy in shipping history - Hanjin

• Leasing companies – losses despite high utilization

• Container production contracting

• Global political uncertainty

• Weak global growth

• Weak container cargo growth

Overcapacity• Vessel capacity – much higher than cargo volumes

• Vessel capacity increase in 2016 slower but still exceeds cargo growth

• Freight rates have fallen to uneconomic levels

• Hanjin: 3% of global capacity disappeared – but only temporary

• Freight rates improve due to Hanjin failure in some trades

• Vessel scrapping with modest cargo growth may absorb current surplus capacity in 3 to 4 years - if no further major vessel orders

• Shipyards desperate for orders - low prices & government finance

Hanjin

• Over 100 ships – most will remain in the market & at lower rates

• A few older vessels may be scrapped

• c.850,000 TEU of containers, 550,000 TEU from leasing companies

• Owned boxes may be sold or taken over by other lines

• Leased boxes – c.80% will be recovered, some sold, most re-leased

• Recovery of containers – a tough and expensive task

• Big costs for vessel charterers, lessors, ports, shippers, insurers, partner lines, lenders

Shanghai – Los Angeles Freight Rates

500

1000

1500

2000

2500

3000

2012 2013 2014 2015 2016

Profitablility range

Source: World Container Index

Atlantic Trade – freight rates

0

500

1000

1500

2000

2500

3000

RTM-NYC NYC-RTM

Source: World Container Index

Global Freight Rates

500

700

900

1,100

1,300

1,500

1,700

1,900

2,100

2,300

2,500

Source Bloomberg

Profitablility range

Freight Rates

• Supply side: Surplus vessel capacity

• Demand side: Low cargo growth

• Increased scrapping

• Restraint on ordering new vessels

• Profitability will improve with supply/demand imbalance correction

• Mergers & consolidation may improve efficiency but not freight rates

• Bankruptcies don’t get rid of surplus vessel capacity

Exports from China

• China’s exports peaked in 2014

• Exports declined 7.7% in the first 10 months of 2016

• Migration of manufacturing to China - finished several years ago

• ‘Near-sourcing’ & protectionism may further impact cargo growth

• Strong export growth from China was the norm for more than 20 years

• The New Normal: low growth & contraction of China export cargo

China Exports per month US$ Bn

50

100

150

200

250

Source: Tradingeconomics.com

Drivers of Demand for Containers

• Cargo growth

• Retirements

• Trade imbalances

• Seasonal factors

• Container price

• Factory Space

• Shipping Line & Leasing company utilisation

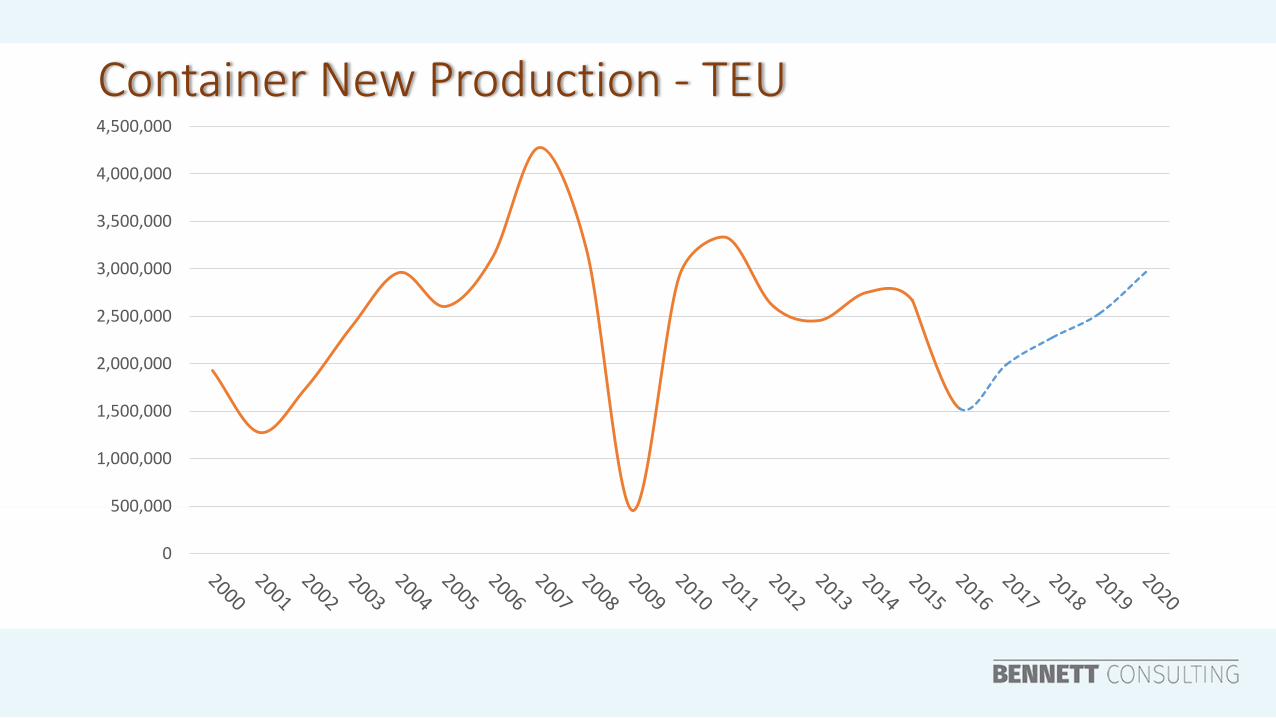

Container New Production - TEU

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

Container Production Outlook

• Very low trade growth or even contraction

• New production demand will come more from replacing retirements

• Increase in retirement volumes from 2018

• More retirements = downward pressure on re-sale prices

• Factories: nominal production capacity of c.5+ million TEU

• Productivity impacted by weak labor retention & waterborne paint

• 2016: less than 1.5M TEU of dry vans manufactured

Price Drivers for New Containers

• Cost of iron ore, metallic coal and steel

• Demand for containers and factory space availability

• Transition to waterborne paint with productivity impact and investment hurdle

• Iron ore and steel prices rising from a cyclical low in good part due to futures market speculation

Iron Ore and Steel Price $/ton

0

20

40

60

80

100

120

140

160

180

200

200

300

400

500

600

700

800

900

steel iron ore

20’ price

$2400

20’ price

$2650

20’ price

$2300

20’ price

$2100

20’ price

$1950

20’ price

$1250

Conclusions

• Low cargo growth is the ‘New Normal’

• Profitability of lines, lessors & container factories will remain under pressure

• Credit risk remains for some shipping lines

• Container prices: unlikely to return to the high levels of 5 years ago

• Container production volumes: tempered by lack of growth

• Consolidation in the industry likely to continue - but will not improve low freight rates, rental rates or container prices