entrepreneur’s fold fold guide ipo scaleup … · square peg capital ... preparing the business...

TRANSCRIPT

www.smeguide.orgwww.smeguide.org

ENTREPRENEUR’S GUIDE

STARTUP SCALEUP IPO

ENTREPRENEUR’S STA

RTUP | SCA

LEUP | IPO

ww

w.sm

eguide.orgGUIDE

CONTRIBUTORS FROM:

● Addisons

● Alphastation

● Ashurst Australia

● Australian Securities Exchange

● BoardRoom

● CBRE

● Cicada Innovations

● Clyde & Co.

● DLA Piper Australia

● Employsure

● Gilbert + Tobin

● Glasshouse Advisory

● Google Australia

● Jackson McDonald Lawyers

● Kain Lawyers

● KPMG

● Legalvision

● Link Market Services

● Main Sequence Ventures

● muru-D

● National Australia Bank

● Partners for Growth Australia

● Pottinger

● Principals

● Silicon Valley Foundry

● Spruson & Ferguson

● Square Peg Capital

● StartupAUS

● Startup Onramp

● Stone & Chalk

● Sydney Angels

● TDM Asset Management

● Transition Level Investments

● University of South Australia

● Upguard

● Watson Mangioni Lawyers

● Xero

FOLD FOLD

FOLD FOLD

1

32SETTING SAIL ON YOUR IPO JOURNEYKPMG

Cecily Conroy, Head of Equity Capital Markets, Australia

Going public is a huge decision for any company. It is a complex, costly and time-

consuming process that places enormous demands on a company and its management

team. There are many advisors to manage, meetings to attend and tasks to complete,

frequently under significant time pressure. Management will be heavily involved in

preparing the business for the initial public offering (IPO), yet will also need to maintain

focus on the day-to-day operations and continue to deliver on the growth strategy.

REALISE THE IMPORTANCE OF EARLY PLANNINGIn addition to facing the challenges just mentioned, making the transition from a

private company to a publicly listed company is also likely to result in significant

changes to how your business operates.

The effort can be worth it. An IPO can prove transformative, giving you access to a

deep pool of capital to propel your business forward. The company will also have

been placed under a microscope, giving you an opportunity to critically examine

your business.

In this regard, early planning and preparation are key to achieving a successful IPO

and a smooth transition to being a listed company.

KNOW YOUR OBJECTIVES FOR LISTINGA company may pursue an IPO for many reasons. Before commencing formal IPO

preparations, identify your objectives for the IPO and ensure that they are reflected

in your IPO strategy.

Ask yourself the following questions:

• What are your main reasons for listing? For example, if a main reason is to enhance

the profile of the business, how will your IPO strategy help you to achieve this?

• How much money will be raised at IPO? Will the proceeds be used by the company

or be distributed to existing shareholders, or will you use a combination of both?

How will the company deploy the proceeds, and does this tie into your equity story?

• When is the optimal time to become a listed company? Also consider the

prevailing equity market conditions and investor sentiment towards listed

companies in your sector.

• Have any other companies in your sector or with similar businesses floated? How

did they fare? Can you learn anything from their processes?

2

PA

RT

III: IPO

APPLY A CAPITAL MARKET LENSIt is important to look at your company through

an equity capital market lens. In other words,

apply the same level of scrutiny that the

investment community (e.g., public market

investors, research analysts, investment banks

or brokers) will apply to your business while

preparing for an IPO and once your company

becomes a publicly listed company.

It can be helpful to meet with one or two

friendly institutional investors to hear their

thoughts and perspectives on your business.

You should be well prepared before meeting

with any investors. Avoid disclosing any specific

financial information and do not leave behind

any presentation materials on your business.

Ask yourself:

• What is your equity story? Will your business

appeal to public market investors? Are there

any themes that might concern investors and,

if so, how can these be mitigated?

• What are the key drivers of value? How will

the company be positioned relative to other

listed comparable companies, and how can

you positively differentiate it?

• How will you give investors confidence

in your ability to deliver on the growth

strategy? What key performance indicators

(KPIs) will demonstrate positive momentum

in the business in the lead-up to the IPO?

Can these KPIs be made available to the

market on a regular basis once the company

is listed?

• How will the strategic decisions you make

today shape your ability to list in the future?

• How will you engage with the investment

community before commencing formal IPO

preparations? Determine how early, with

whom and what should or should not be said.

START PREPARING THE BUSINESS FOR LIFE AS A LISTED COMPANYYou should evaluate your company’s readiness

to commence formal IPO preparations and its

ability to meet the obligations of being a listed

company. Management and the company

could benefit from operating with a listed

company mind-set well before actually going

public.

Ask yourself:

• What changes are required to be ready to list?

Identify the items that may take a longer time

to complete, such as corporate restructuring,

presentation and audit of historical financials,

board and management changes, governance,

systems and controls.

• Does management have the time to prepare

for an IPO and continue to successfully

manage the company? The period in the

lead-up to the IPO is certainly not the time for

management to take its eye off the ball.

• Have you identified the ‘red flag’ items that

could delay your IPO timetable or affect value

or investor demand?

• Are you tracking information (such as KPIs)

that will support your equity story and give

greater confidence to investors?

You may discover early issues that need

addressing before you can even start to think

more deeply about an IPO.

APPOINT THE RIGHT TEAM OF ADVISORSCompanies often underestimate the effort and

resources required to prepare for an IPO. An

IPO requires a huge commitment from both the

internal deal team as well as the external advisory

team—both of whom need to work closely

together. Choose an experienced team of advisors

to help your company prepare for an IPO, and

have a strong start to life as a listed company.

Appointing the right team of advisors (in

particular, selecting the right lead manager) can

have a direct bearing on the success of your IPO.

Ask yourself:

• What advisors do you need to appoint to help

you prepare for an IPO?

• Who is best positioned to advise your

company?

3

CH

AP

TE

R 3

2: S

ET

TIN

G S

AIL

ON

YO

UR

IPO

JOU

RN

EY

• When and how should you appoint your

advisors?

ADDRESS OTHER CONSIDERATIONSTwo fundamental success factors are commonly

highlighted by companies who have been

through the IPO process. These are:

• dedicating time to developing your equity

story early on

• appointing the right lead manager to market

your IPO to investors.

Many challenges and complexities are involved

in each of these areas, so we will dive into each

area in more detail in the next sections.

DEVELOP YOUR EQUITY STORY

Why is it important?An equity story is your rationale for why

investors should buy shares in your company.

Some people call it an ‘investment thesis’, others

a ‘sales pitch’.

You must develop a clear, differentiated and

accurate equity story that makes a compelling

case for why investors should back your

company (Figure 1).

Importantly, to achieve a successful IPO, your

equity story must appeal to public market

investors. If you have previously raised private

capital from angel investors, venture capital firms

or other private investors, you may need to refine

your equity story to draw out the investment

attributes sought by public market investors.

A strong equity story drives investor

engagement and demand and will also influence

an investor’s perception around the positioning

of your company relative to listed peers. It

is critical in maximising value, achieving a

quality shareholder register and ensuring a

healthy aftermarket. It is important to consider

management’s ability to present that equity

story credibly. It may be that management

needs to rehearse or even change some

members of the management team so that they

are suitable for the public market.

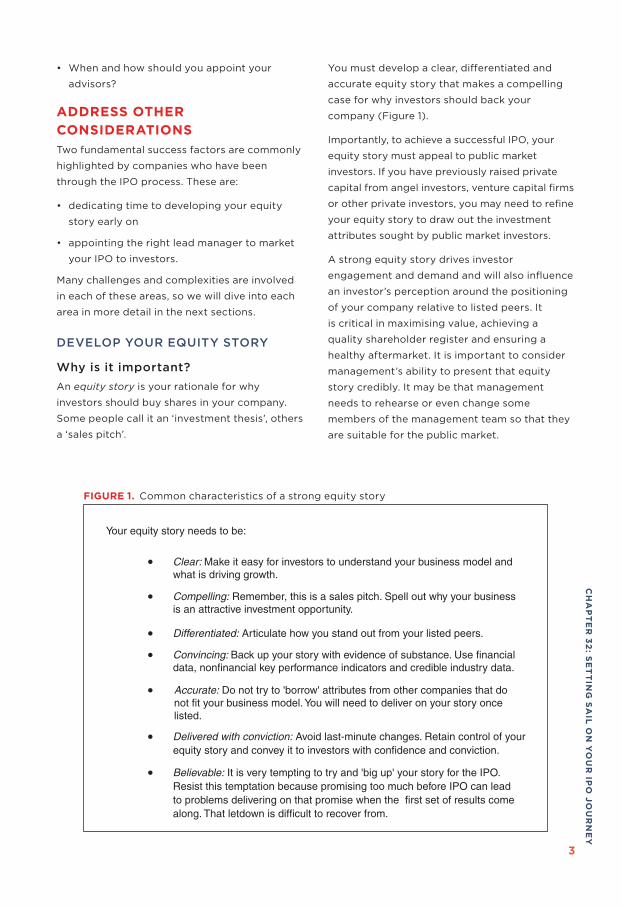

FIGURE 1. Common characteristics of a strong equity story

Your equity story needs to be:

Clear: Make it easy for investors to understand your business model andwhat is driving growth.

Compelling: Remember, this is a sales pitch. Spell out why your business is an attractive investment opportunity.

Differentiated: Articulate how you stand out from your listed peers.

Convincing: Back up your story with evidence of substance. Use financial data, nonfinancial key performance indicators and credible industry data.

Accurate: Do not try to 'borrow' attributes from other companies that donot fit your business model. You will need to deliver on your story oncelisted.

Delivered with conviction: Avoid last-minute changes. Retain control of yourequity story and convey it to investors with confidence and conviction.

Believable: It is very tempting to try and 'big up' your story for the IPO. Resist this temptation because promising too much before IPO can lead to problems delivering on that promise when the first set of results comealong. That letdown is difficult to recover from.

4

PA

RT

III: IPO

The equity story itself will evolve throughout

the IPO process and is the blueprint for key IPO

documents. It underpins the lead manager’s

preliminary IPO valuation, the presentation for

research analysts and institutional investors,

and your prospectus. It will form the basis of

certain due diligence enquiries from banks,

lawyers and accountants. Ultimately, your

equity story will determine whether an investor

participates in your IPO. Developing your equity

story is therefore one of the most important

workstreams in your IPO process and requires

an early focus from management.

Where should you start?Start preparing your equity story very early

in your IPO preparations, and certainly well in

advance of appointing a lead manager.

Gather your business plan, corporate strategy,

board papers, marketing materials, KPIs,

research and development program and other

key internal documents relevant to your strategy

and company’s track record. Reflect on where

you have come from as a business, and where

you are going.

Identify the key value drivers of your business

and any potential weaknesses or risks that may

affect valuation or investor appeal for your IPO.

Be sure to do the following:

• Articulate your key achievements and the

positive attributes of your business model. For

example, you may be a disruptive player or be

using proprietary technology.

• Consider your positioning. Investors will

compare your business to other similar

companies listed on both domestic and

potentially international stock markets, so it

is important that you positively differentiate

your business; make a strong case for why

they should invest in it.

• Look carefully at your financials, operations

and growth prospects relative to your listed

peers.

• Consider what financial and nonfinancial

information you can provide investors to

support your equity story and give greater

confidence to investors.

Create a first draft with the key ingredientsCommon areas of focus for an equity story

include the following:

• Company platform and maturity: What is

your business model and strategy? Is it

unique, and is there a demonstrated demand

for your product/service offering? What

has been achieved so far? What are the

attractive attributes of your business model

(e.g., disruptive player, high barriers to entry,

market leader or proprietary technology)?

How mature is your business model (i.e., do

you have clear proof of concept, visibility

of revenue and predictability of earnings

potential)? Is there a reasonable operating

history? Does the business have good

systems and governance in place?

• Addressable market and opportunity: What

is the size of the addressable market? Are

credible industry data available that can

be used to educate investors? What is your

market share and competitive positioning?

Can you maintain your competitive advantage

as you grow? What is the geographic reach?

• Financial and operational profile: What is your

revenue and earnings track record? What are

your margins, and how will they change as

your company grows? Do you have a track

record of delivering growth? Is this growth

sustainable in the medium term? What is

your cash conversion? Are you profitable,

or is there a clear path to profitability and

improving operating leverage? Are your

operating metrics (e.g., cost of customer

acquisition, customer numbers and churn)

improving? Do you have a sticky customer

base?

• Future growth prospects: What are your key

pillars of growth? Is your growth trajectory

sustainable? Will future growth be organic

or acquisition-led? How will you continue

to grow your margins? How do you plan to

5

CH

AP

TE

R 3

2: S

ET

TIN

G S

AIL

ON

YO

UR

IPO

JOU

RN

EY

capitalise on your existing position, cross-

sell to existing customers, enter adjacent

markets/geographies, etc.? How will you use

your IPO proceeds?

• Management capability: What is the

background and experience of your

management team? Do they have a proven

track record in management and leadership?

Articulate your story to investorsThe chief executive officer and chief financial

officer must be able to convey the company’s

story to investors during roadshow meetings

with genuine confidence and conviction because

investors are ultimately backing the management

team to deliver on the company’s growth

strategy. Management’s ability to do so will have

a direct bearing on demand and valuation.

Poor planning can result in an equity story

changing at the eleventh hour before launching

the IPO. This situation could undermine

management’s ability to deliver the story

with conviction and may result in investors

misunderstanding the business model or value

proposition or lead to inconsistency in how

investors value the company.

Update your website and other marketing materialsOne of the first things a potential investor will do

is look at your website. As you craft your equity

story, also consider updating your website and

other marketing materials to reflect it, to ensure

you are putting out a consistent message. Be

sure to do this well before commencing formal

IPO preparations.

APPOINT YOUR LEAD MANAGERAppointing the right lead manager is key to

achieving a successful listing and your start

to life as a publicly listed company (Figure 2).

The lead manager role is performed by

an investment bank or broker who will be

responsible for managing the offering and

marketing your IPO to investors. The number

of banks appointed will vary depending on the

amount of equity to be raised at IPO.

Understand the appointment processIt is common in Australia for a company to

select a lead manager following a competitive

appointment process, also known as a ‘beauty

parade’. This task would usually involve a

company identifying a shortlist of suitable

banks and inviting them to submit a written

proposal that outlines their credentials, views

on the IPO and fees. Each bank is subsequently

invited to ‘pitch’ or present their views to the

company’s executive team and shareholders.

A competitive process can provide a company

with the opportunity to hear from a range of

different banks and consider the personal fit

with their internal deal team. It also gives the

company the ability to compare the capability

of each bank on a consistent and transparent

basis.

In certain circumstances, it may be

advantageous to avoid a broad process (which

could leak into the media) and instead run a

hybrid appointment process. For instance, the

company may have previously met with several

banks and understands the capabilities of each

bank, one or two banks may be standouts or

confidentiality is critical to the company. An

independent financial advisor can also assist

with bank negotiations to deliver competitive

tension outside of a formal competitive

process.

Make first impressions countThe appointment of a lead manager is usually a

‘two-way’ process. That is, while the company is

considering which bank to appoint, each bank

is also determining whether to accept the lead

manager role. First impressions therefore count!

The company’s executive management and

shareholders should consider how to succinctly

communicate the company’s equity story as well

as the rationale for listing well before meeting

with the banks.

As part of the appointment process, the

company will also need to provide the banks

with an overview of the business, explain

the strategy and growth prospects, provide

6

PA

RT

III: IPO

certain financial information and demonstrate

the strength of the management team. This

information will form the basis of their indicative

valuation and preliminary recommendations

in relation to the IPO. As with any third party,

you should carefully consider what confidential

company information you share and with whom

you share it.

Maximise your negotiating leverageA company’s leverage to negotiate favourable

terms with the banks is highest ahead of

formal appointment. It is often beneficial to

agree as much as possible with the banks

before you confirm their appointment, either

verbally or in writing.

FIGURE 2. What to consider when selecting a lead manager

The criteria for selecting a lead manager will vary for each company. However, someof the common considerations include the following:

quality and experience of the individual team members and senior-levelcommitment; rapport with the company and strength of existing relationships

track record, relevant credentials and distribution capability (both institutional andretail)

sector expertise, understanding of the business and how best to present the equitystory to investors, approach to valuation and positioning

depth of existing research coverage universe in your sector as well as knowledgeand credibility of research analysts (e.g., rankings)

proposed fees and engagement terms

ability to support the company and, if relevant, facilitate an exit for the majorshareholders once listed.

If the company is appointing more than one bank, it is important to ensure that eachbank brings complementary strengths to your IPO process. For instance, one bank mayhave excellent sector expertise whereas another may have a stronger distribution platform.

www.smeguide.org

7

CH

AP

TE

R 3

2: S

ET

TIN

G S

AIL

ON

YO

UR

IPO

JOU

RN

EY

KPMG

Tower Three, International Towers Sydney,

300 Barangaroo Avenue,

Sydney NSW 2000

Tel: +61 2 9335 7000

Web: www.kpmg.com.au

CECILY CONROYHead of Equity Capital Markets, Australia

Email: [email protected]

Ms. Conroy is the National Head of Equity

Capital Markets (ECM) Advisory at KPMG. She

provides strategic and tactical advice to clients

on raising equity in the global capital markets,

such as helping private companies prepare

for and execute an IPO, listed companies to

raise new equity or strategic shareholders

to monetise a stake in a listed entity. She

has advised on a broad spectrum of ECM

transactions raising c.A$50 billion across

Australian, New Zealand, Asian, European

and U.S. equity markets. Her deal experience

spans a diverse range of sectors, deal types

and deal sizes, including a number of landmark

transactions. She has specialised in ECM and

corporate finance for the past 15 years. She

brings a unique perspective to a client’s internal

deal team gained from her deep experience

as both an independent equity advisor and

an investment banker in the ECM division of a

global investment bank.