european coffee consumption trends 2016 cr - · pdf filebrazil colombia ethiopia honduras...

TRANSCRIPT

EuropeanSpecialityCoffeeMarketOutlook

EUROPEAN SPECIALITY COFFEE CONSUMPTION TRENDS

Mick Wheeler

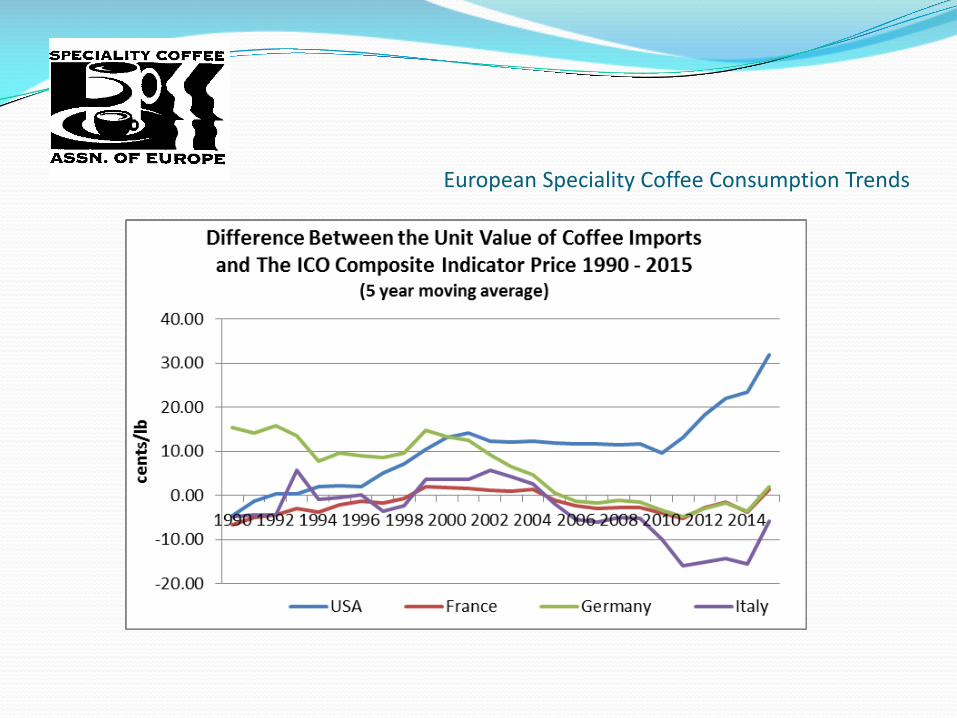

EuropeanSpecialityCoffeeConsumptionTrends

� It would be fair to say that when the specialty coffee movement started off in America, Europe was fairly dismissive of this new American trend, believing that it had always concentrated on quality.

� But the force proved too strong and this new phenomenon rapidly moved across the Atlantic.

� However the two markets have developed in slightly different ways.

EuropeanSpecialityCoffeeConsumptionTrends

Differences between the American and European Specialty

� Europe is more fragmented with a greater number of independent participants than is the case in America;

� The European specialty coffee sector encompasses a much wider range of regional brewing preferences than is evident in America;

� The American specialty movement has been more successful in raising the overall quality profile of coffee consumption in general than the European Speciality coffee movement has been.

EuropeanSpecialityCoffeeConsumptionTrends

EuropeanSpecialityCoffeeMarketOutlook

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Brazil Colombia Guatemala Honduras Indonesia Mexico Nicaragua Vietnam

% o

f tot

al im

port

s

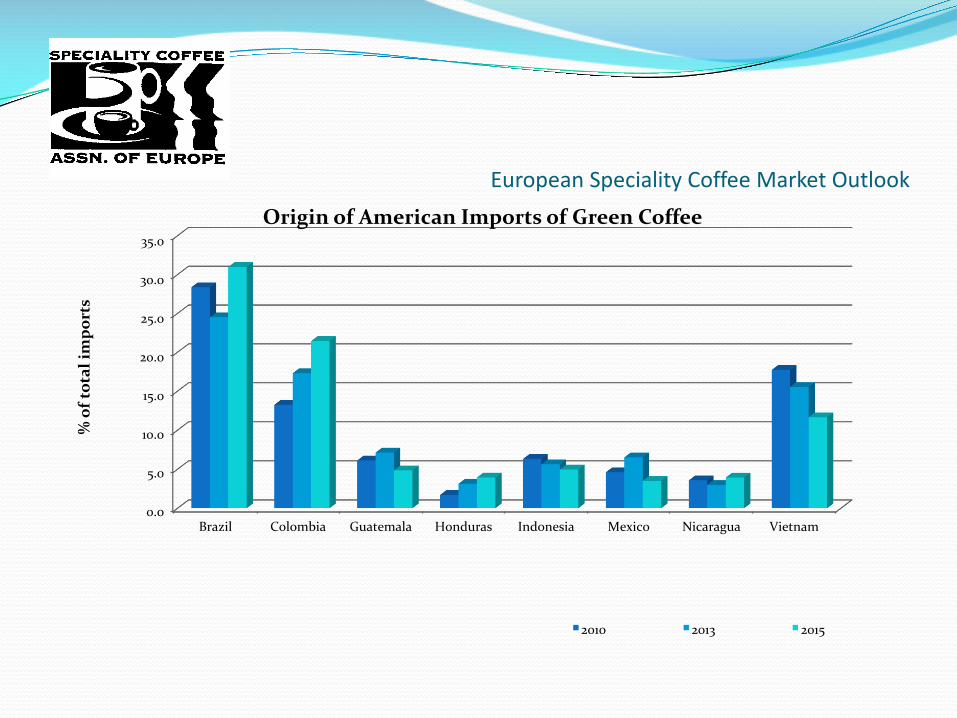

Origin of American Imports of Green Coffee

2010 2013 2015

EuropeanSpecialityCoffeeConsumptionTrends

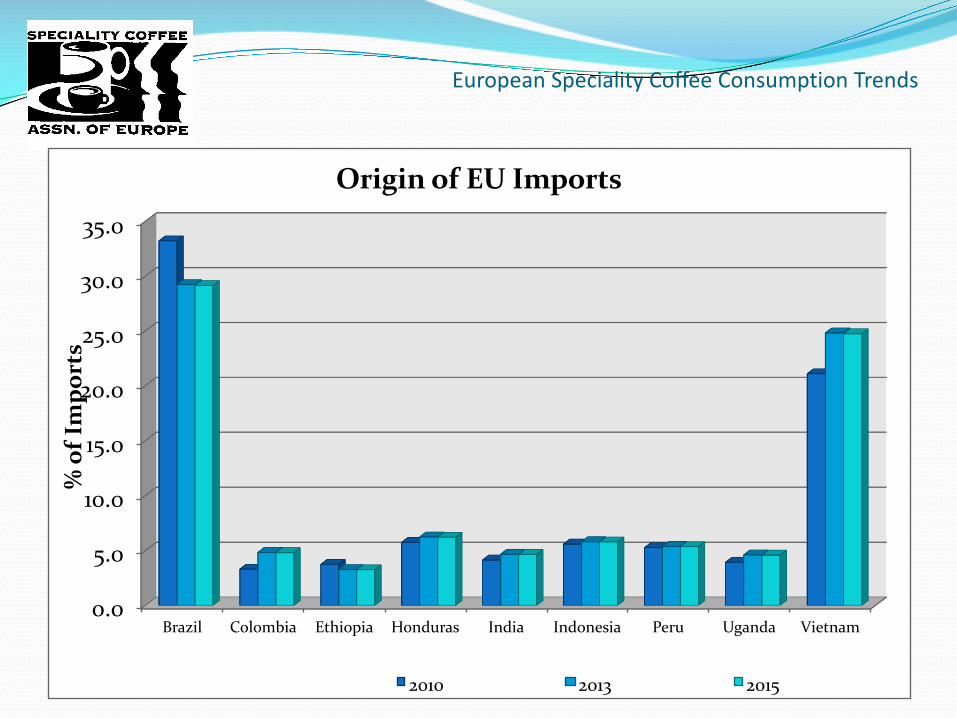

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Brazil Colombia Ethiopia Honduras India Indonesia Peru Uganda Vietnam

% o

f Im

port

s

Origin of EU Imports

2010 2013 2015

EuropeanSpecialityCoffeeConsumptionTrends

But let’s take a closer look at what is happening in Europe:

Overall - The Future is Relatively Bright, But there are Clouds on the Horizon

� Various sources all show the same trend, coffee consumption in Europe is growing, but that growth is extremely slow;

� The speciality coffee sector, however, appears to be growing a little faster;

� Although, the data sources remain fragmented and are somewhat limited.

EuropeanSpecialityCoffeeConsumptionTrends

� To explore this in a little more depth, I will examine the following:

� Exports of Organic and Differentiated Coffee into Europe,

� Overall coffee consumption in Europe, and the

� Development of the Coffee Sectors in the UK and Germany, with a greater focus on the coffee shop sectors in these countries.

It is a bit of mish-mash of data, but helps to paint a picture of a sector of the industry, where some areas are growing vibrantly but others not so well,

EuropeanSpecialityCoffeeConsumptionTrends

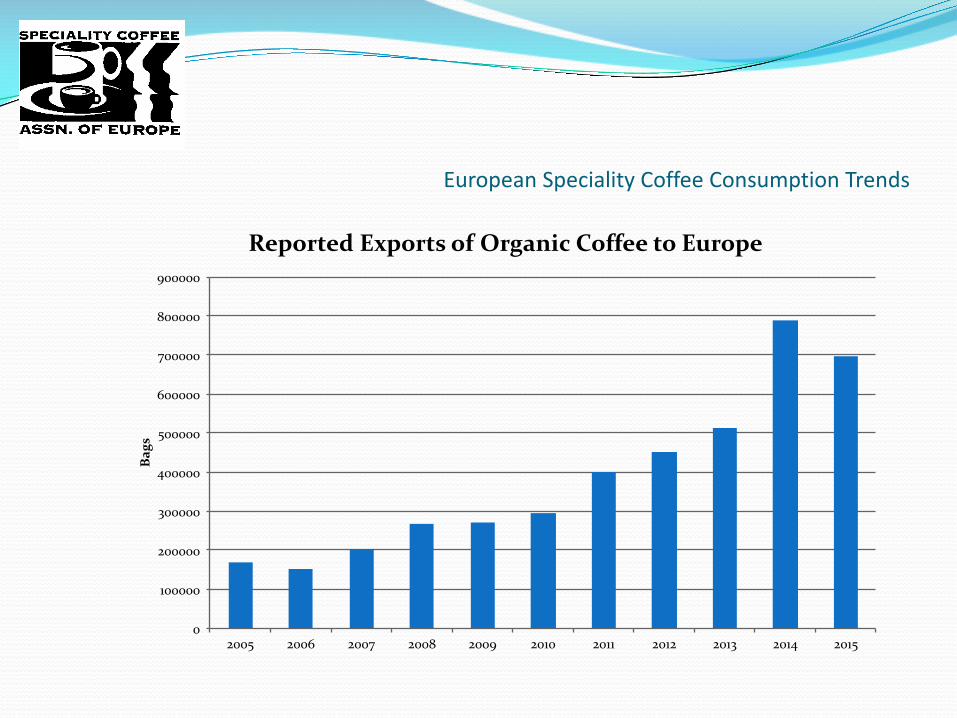

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bag

s

Reported Exports of Organic Coffee to Europe

EuropeanSpecialityCoffeeConsumptionTrends

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

2200000

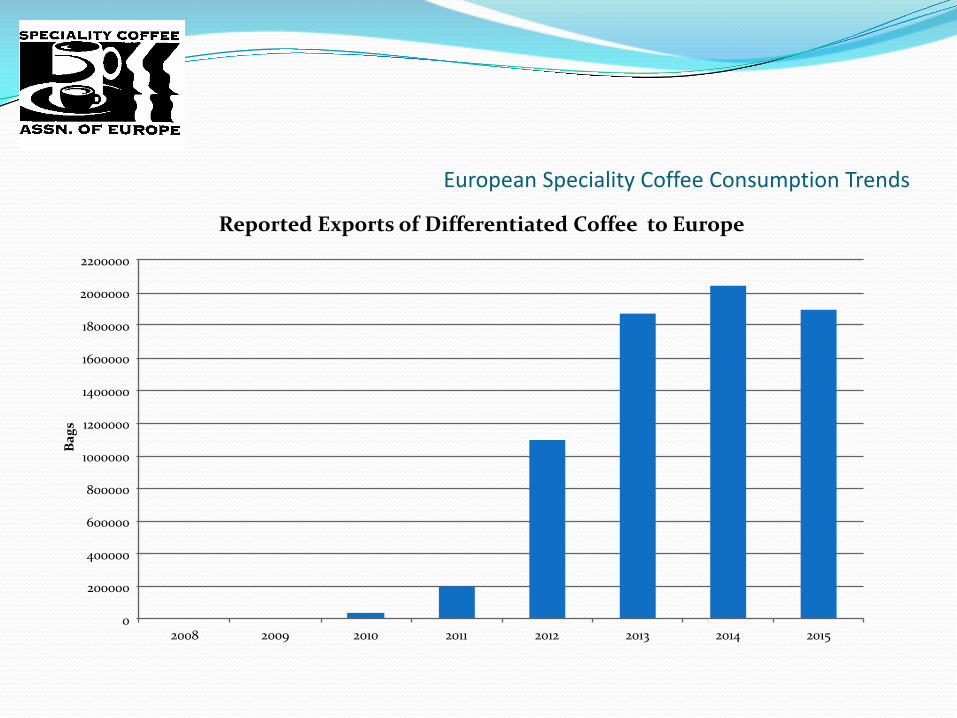

2008 2009 2010 2011 2012 2013 2014 2015

Bag

s

Reported Exports of Differentiated Coffee to Europe

EuropeanSpecialityCoffeeConsumptionTrends

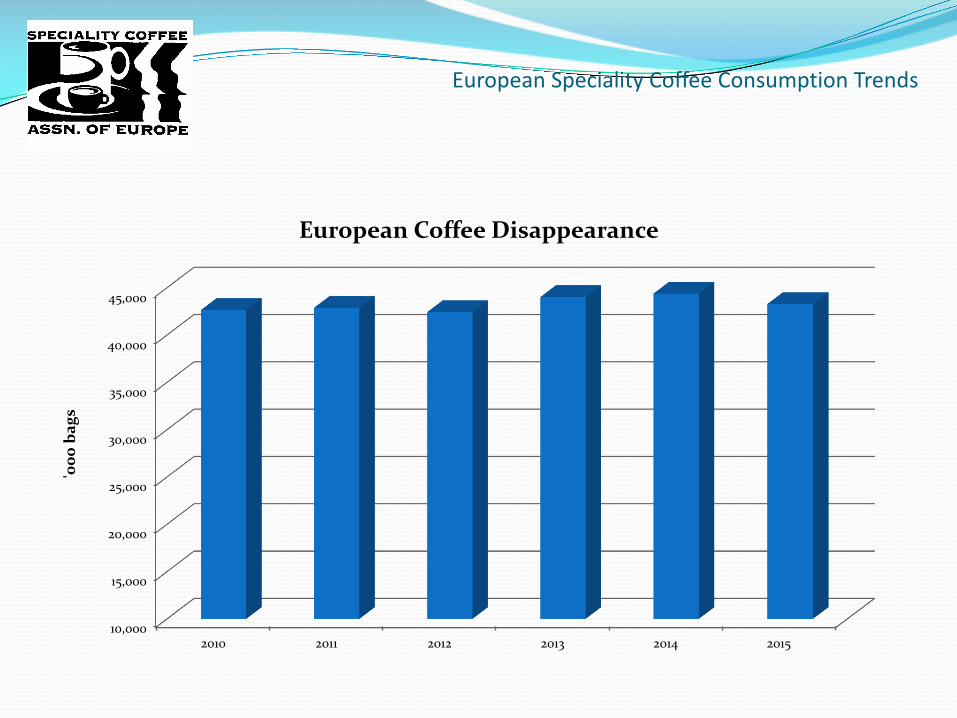

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2010 2011 2012 2013 2014 2015

'000

bag

s

European Coffee Disappearance

EuropeanSpecialityCoffeeConsumptionTrends

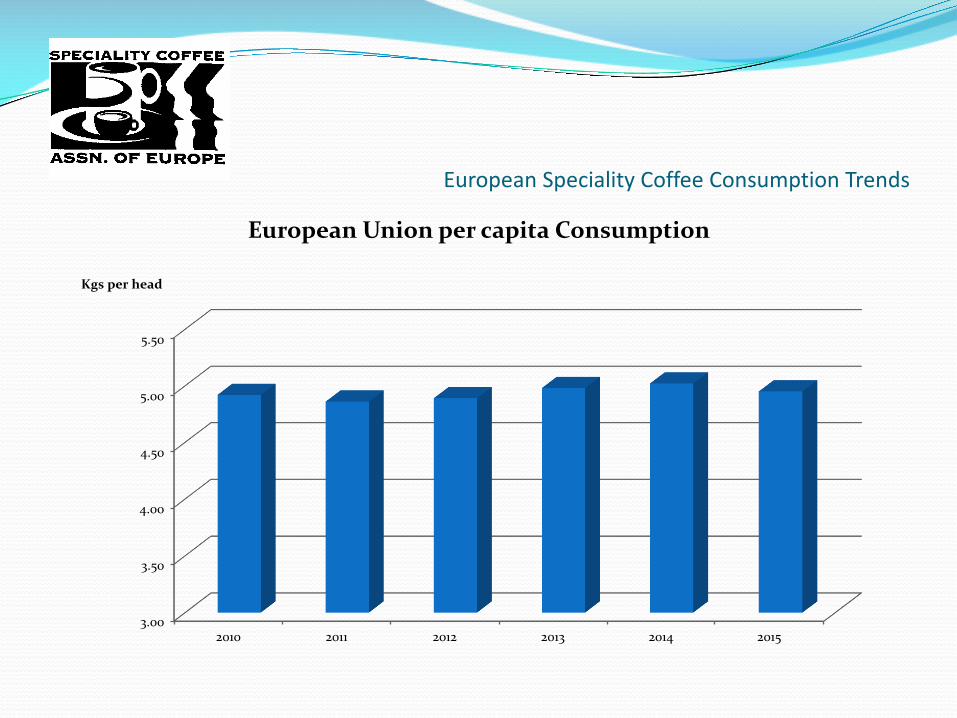

3.00

3.50

4.00

4.50

5.00

5.50

2010 2011 2012 2013 2014 2015

Kgs per head

European Union per capita Consumption

EuropeanSpecialityCoffeeConsumptionTrends

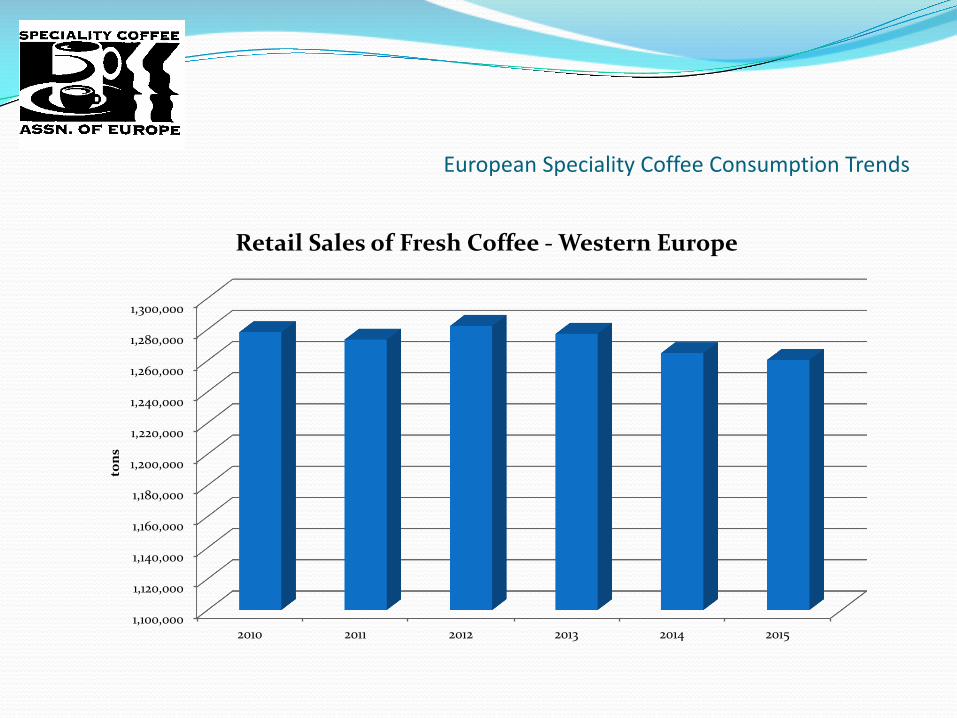

1,100,000

1,120,000

1,140,000

1,160,000

1,180,000

1,200,000

1,220,000

1,240,000

1,260,000

1,280,000

1,300,000

2010 2011 2012 2013 2014 2015

tons

Retail Sales of Fresh Coffee - Western Europe

EuropeanSpecialityCoffeeConsumptionTrends

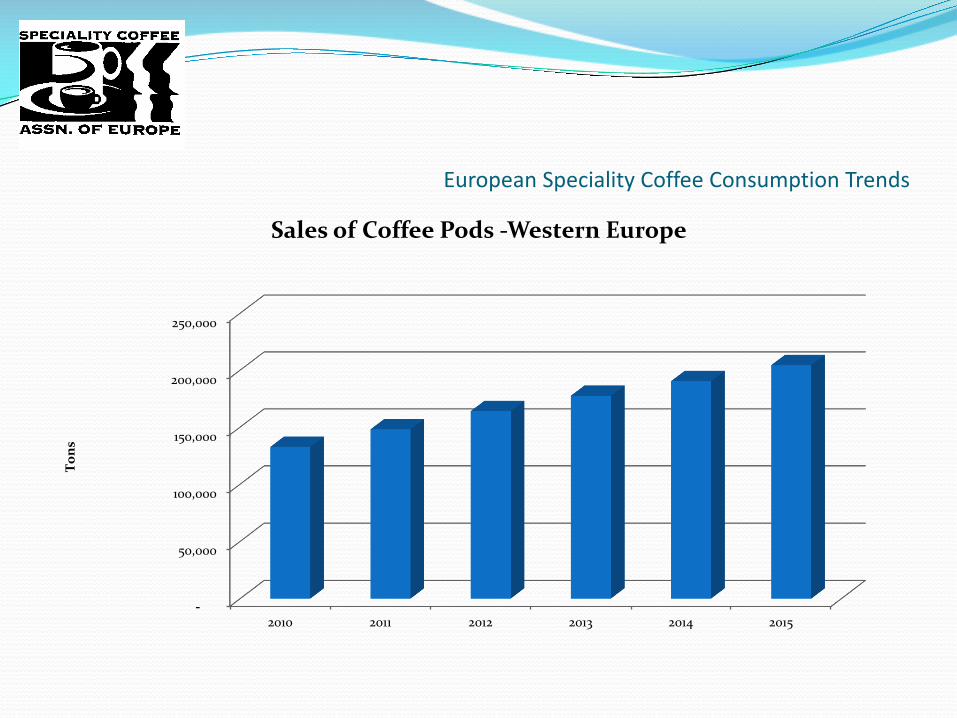

-

50,000

100,000

150,000

200,000

250,000

2010 2011 2012 2013 2014 2015

Tons

Sales of Coffee Pods -Western Europe

EuropeanSpecialityCoffeeConsumptionTrends

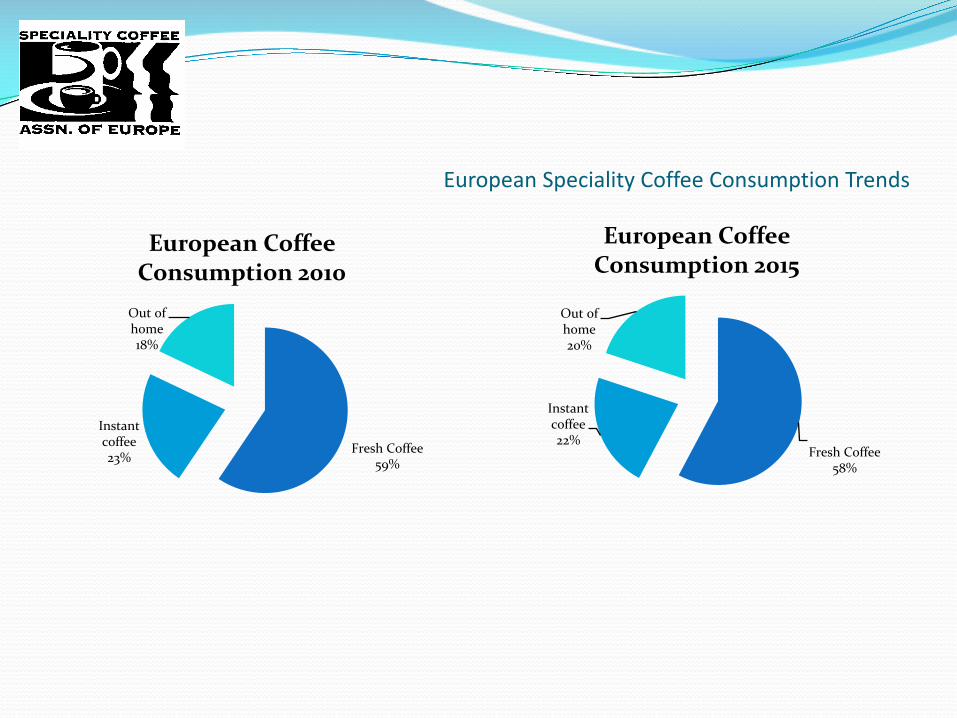

Fresh Coffee59%

Instant coffee23%

Out of home18%

European Coffee Consumption 2010

Fresh Coffee58%

Instant coffee22%

Out of home20%

European Coffee Consumption 2015

EuropeanSpecialityCoffeeConsumptionTrends

So let’s look at two markets in Europe, where reasonable (accessible) data exists:

THE UK &

GERMANY

EuropeanSpecialityCoffeeConsumptionTrends

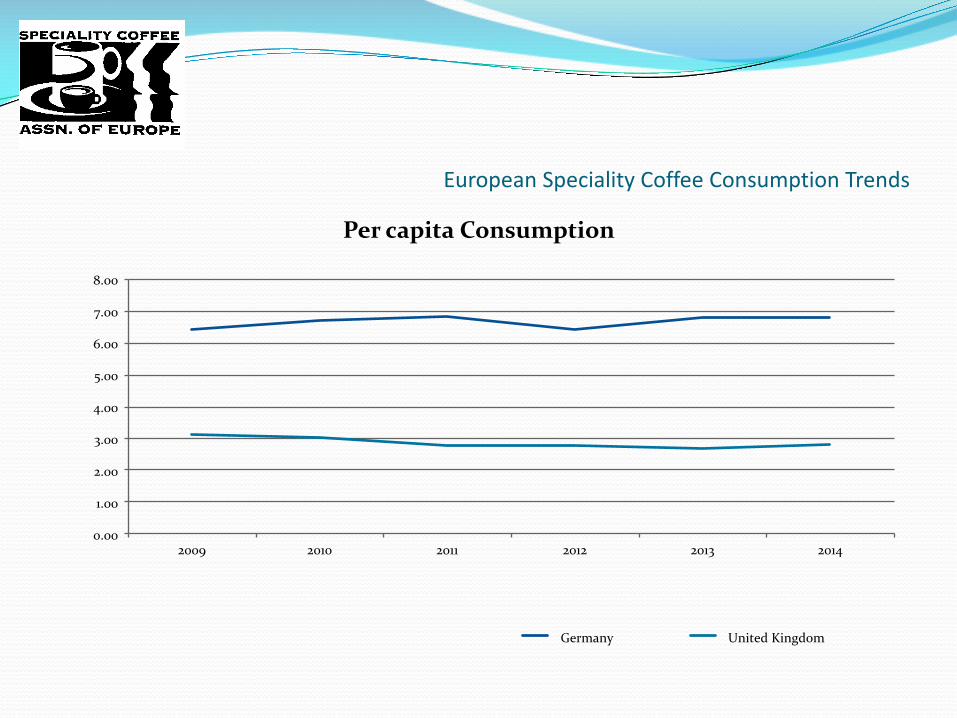

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2009 2010 2011 2012 2013 2014

Per capita Consumption

Germany United Kingdom

EuropeanSpecialityCoffeeConsumptionTrends

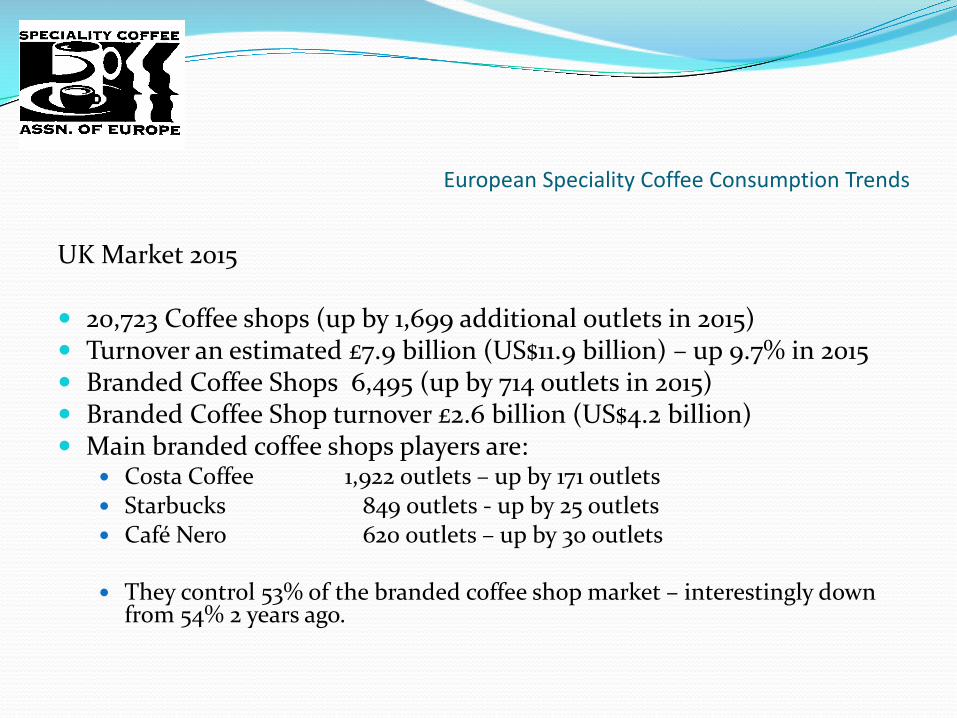

UK Market 2015

� 20,723 Coffee shops (up by 1,699 additional outlets in 2015)� Turnover an estimated £7.9 billion (US$11.9 billion) – up 9.7% in 2015� Branded Coffee Shops 6,495 (up by 714 outlets in 2015)� Branded Coffee Shop turnover £2.6 billion (US$4.2 billion)� Main branded coffee shops players are:

� Costa Coffee 1,922 outlets – up by 171 outlets� Starbucks 849 outlets - up by 25 outlets� Café Nero 620 outlets – up by 30 outlets

� They control 53% of the branded coffee shop market – interestingly down from 54% 2 years ago.

EuropeanSpecialityCoffeeConsumptionTrends

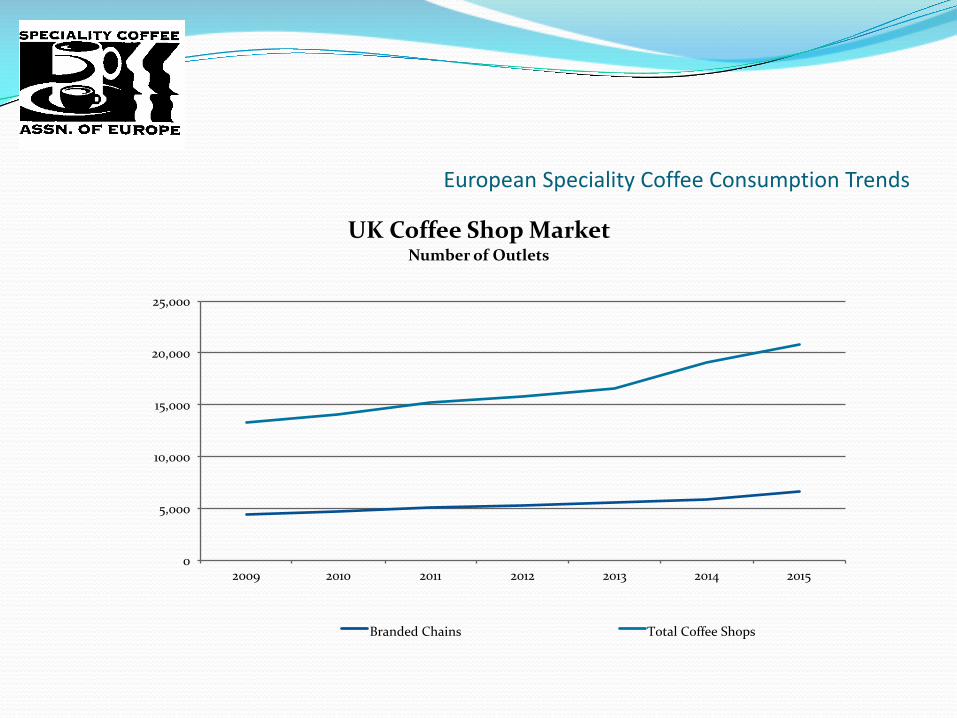

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 2012 2013 2014 2015

UK Coffee Shop Market Number of Outlets

Branded Chains Total Coffee Shops

EuropeanSpecialityCoffeeConsumptionTrends

-

5,000

10,000

15,000

20,000

25,000

30,000

2010 2011 2012 2013 2014 2015

Tons

Retail Coffee Sales in the UK

Pods Fresh coffee

EuropeanSpecialityCoffeeConsumptionTrends

THE EUROPEAN MARKET:

So what’s happening in Germany

Errr………… Not much!!!!!

BUT

EuropeanSpecialityCoffeeConsumptionTrends

German Market 2015

� The number of coffee shops in Germany, which includes dedicated coffee shops, bakery stores, fast food outlets, petrol stations and other outlets in 2015 was just over 25,000 (up just 0.1%)

� Turnover an estimated €3.5 billion (US$3.9 billion) – up 2.2% in 2015� Branded Coffee Shops 1,882 (up by just 30 outlets or 1.6% in 2015)� Branded Coffee Shop turnover estimated at €974 million (US$1.1

billion)� Main branded coffee shops players are:

� McCafe 867 outlets – up by 7 outlets� Starbucks 163 outlets - up by 6 outlets� Segafredo 87 outlets – up by 4 outlets

EuropeanSpecialityCoffeeConsumptionTrends

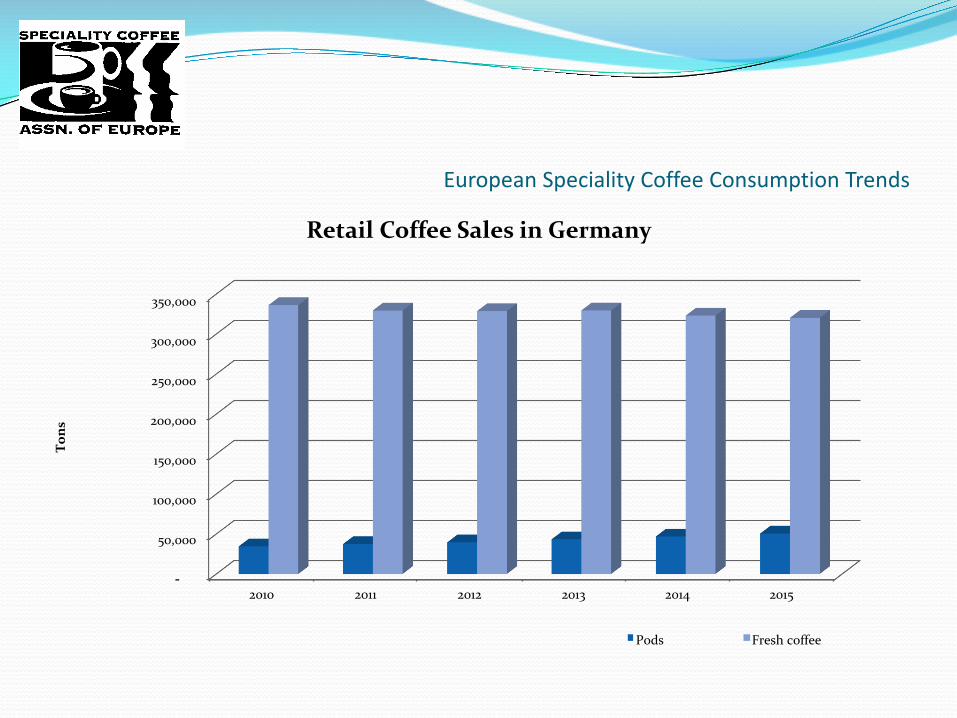

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2010 2011 2012 2013 2014 2015

Tons

Retail Coffee Sales in Germany

Pods Fresh coffee

EuropeanSpecialityCoffeeConsumptionTrend

The Future for Consumption of Speciality Coffee in Europe

� European Consumption of Speciality coffee should continue to grow;

� Furthermore the shifts in that consumption, witnessed over the last 5 years looks, set to continue, i.e.:

� Out of home consumption will continue to grow;

� Consumption of pods will continue to expand; but

� Overall consumption of green coffee looks set to continue to stagnate.

EuropeanSpecialityCoffeeConsumptionTrends

Thank You