fatca: impact on data management - six · fatca: impact on data management ... for the purpose of...

TRANSCRIPT

FATCA: impact on data management Jacob Gertel, Business Development April 2014

Agenda

2

• Introduction

• IRS Final Regulation and Amendments Highlights

• SIX Financial Information Data Offering

− Issuer Level Classification & Status

− Instrument Level Tax Status

− Pass-through Payment Information

• Implementation Timeline

INTRODUCTION

Foreign Account Tax Compliance Act (FATCA)

3

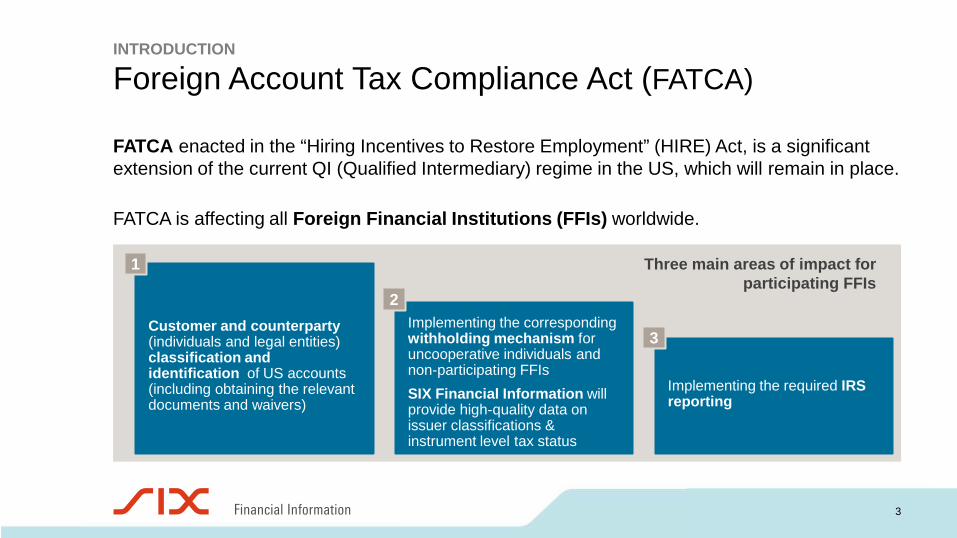

FATCA enacted in the “Hiring Incentives to Restore Employment” (HIRE) Act, is a significant extension of the current QI (Qualified Intermediary) regime in the US, which will remain in place. FATCA is affecting all Foreign Financial Institutions (FFIs) worldwide.

Customer and counterparty (individuals and legal entities) classification and identification of US accounts (including obtaining the relevant documents and waivers)

Implementing the corresponding withholding mechanism for uncooperative individuals and non-participating FFIs SIX Financial Information will provide high-quality data on issuer classifications & instrument level tax status

Implementing the required IRS reporting

3

2

1 Three main areas of impact for participating FFIs

FATCA

IRS Final Regulation and Amendments Highlights

4

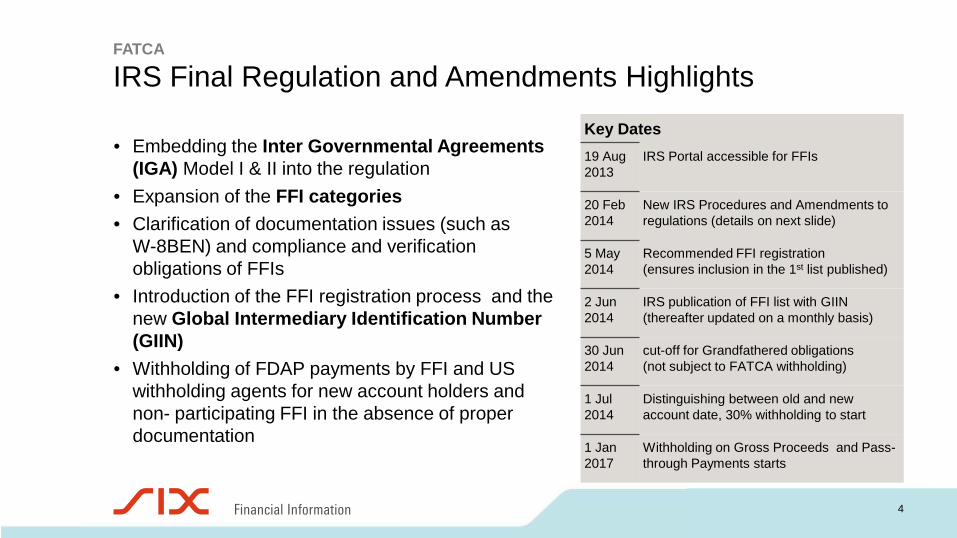

• Embedding the Inter Governmental Agreements (IGA) Model I & II into the regulation

• Expansion of the FFI categories • Clarification of documentation issues (such as

W-8BEN) and compliance and verification obligations of FFIs

• Introduction of the FFI registration process and the new Global Intermediary Identification Number (GIIN)

• Withholding of FDAP payments by FFI and US withholding agents for new account holders and non- participating FFI in the absence of proper documentation

Key Dates 19 Aug 2013

IRS Portal accessible for FFIs

20 Feb 2014

New IRS Procedures and Amendments to regulations (details on next slide)

5 May 2014

Recommended FFI registration (ensures inclusion in the 1st list published)

2 Jun 2014

IRS publication of FFI list with GIIN (thereafter updated on a monthly basis)

30 Jun 2014

cut-off for Grandfathered obligations (not subject to FATCA withholding)

1 Jul 2014

Distinguishing between old and new account date, 30% withholding to start

1 Jan 2017

Withholding on Gross Proceeds and Pass-through Payments starts

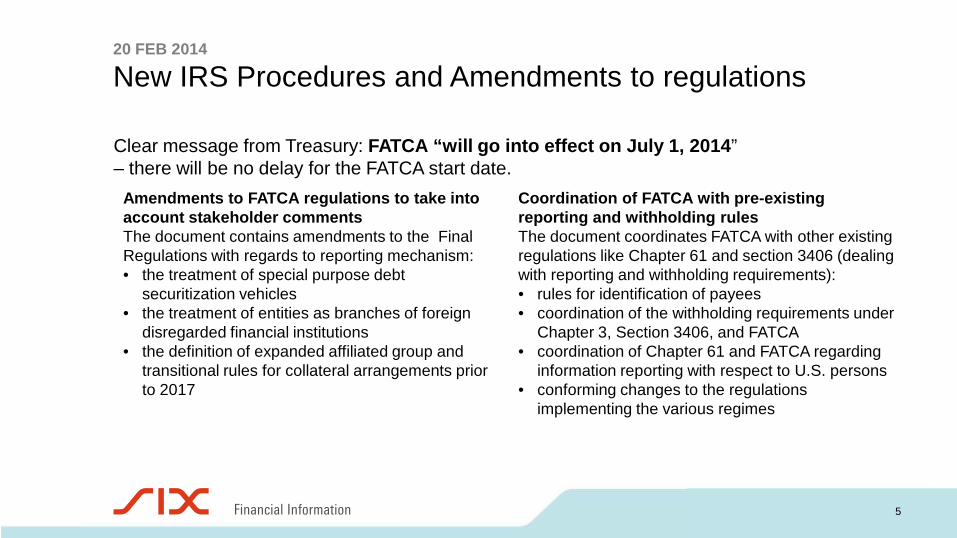

20 FEB 2014

New IRS Procedures and Amendments to regulations

5

Clear message from Treasury: FATCA “will go into effect on July 1, 2014” – there will be no delay for the FATCA start date. Amendments to FATCA regulations to take into

account stakeholder comments The document contains amendments to the Final Regulations with regards to reporting mechanism: • the treatment of special purpose debt

securitization vehicles • the treatment of entities as branches of foreign

disregarded financial institutions • the definition of expanded affiliated group and

transitional rules for collateral arrangements prior to 2017

Coordination of FATCA with pre-existing reporting and withholding rules The document coordinates FATCA with other existing regulations like Chapter 61 and section 3406 (dealing with reporting and withholding requirements): • rules for identification of payees • coordination of the withholding requirements under

Chapter 3, Section 3406, and FATCA • coordination of Chapter 61 and FATCA regarding

information reporting with respect to U.S. persons • conforming changes to the regulations

implementing the various regimes

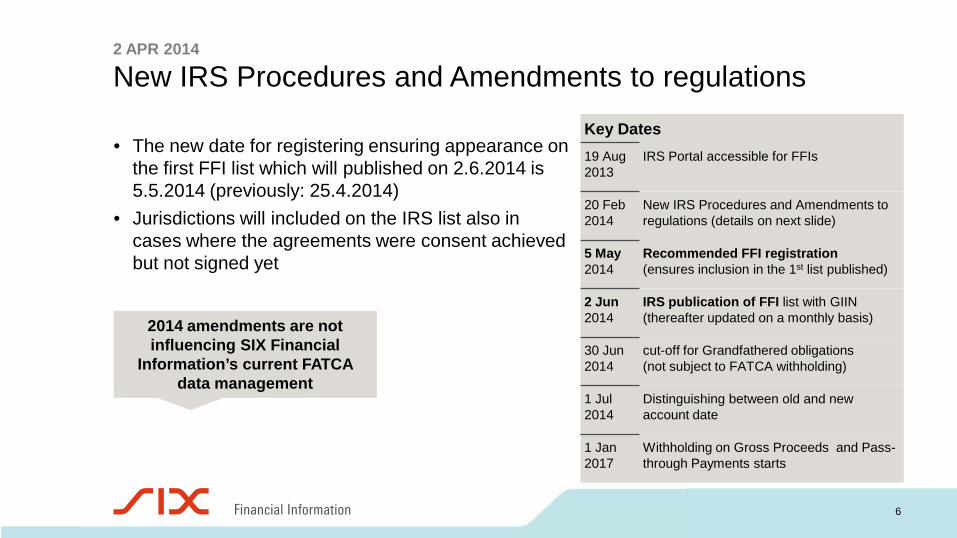

2 APR 2014

New IRS Procedures and Amendments to regulations

6

• The new date for registering ensuring appearance on the first FFI list which will published on 2.6.2014 is 5.5.2014 (previously: 25.4.2014)

• Jurisdictions will included on the IRS list also in cases where the agreements were consent achieved but not signed yet

2014 amendments are not influencing SIX Financial

Information’s current FATCA data management

Key Dates 19 Aug 2013

IRS Portal accessible for FFIs

20 Feb 2014

New IRS Procedures and Amendments to regulations (details on next slide)

5 May 2014

Recommended FFI registration (ensures inclusion in the 1st list published)

2 Jun 2014

IRS publication of FFI list with GIIN (thereafter updated on a monthly basis)

30 Jun 2014

cut-off for Grandfathered obligations (not subject to FATCA withholding)

1 Jul 2014

Distinguishing between old and new account date

1 Jan 2017

Withholding on Gross Proceeds and Pass-through Payments starts

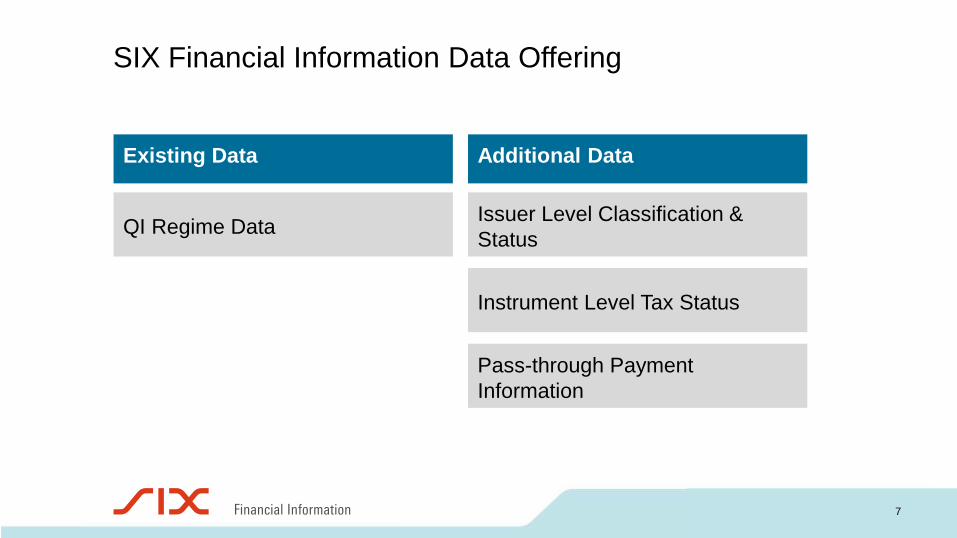

Existing Data Additional Data

QI Regime Data

Pass-through Payment Information

Instrument Level Tax Status

Issuer Level Classification & Status

SIX Financial Information Data Offering

7

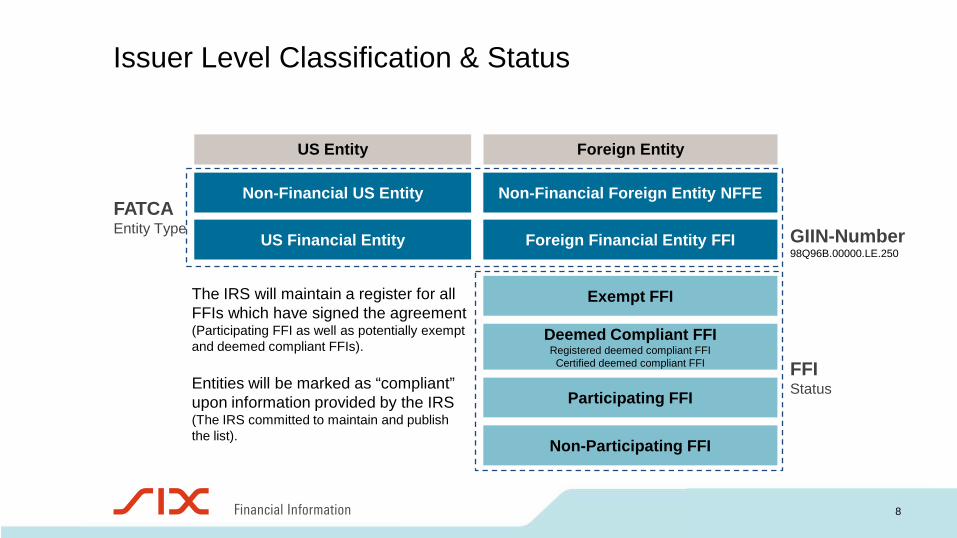

The IRS will maintain a register for all FFIs which have signed the agreement (Participating FFI as well as potentially exempt and deemed compliant FFIs). Entities will be marked as “compliant” upon information provided by the IRS (The IRS committed to maintain and publish the list).

FATCA Entity Type GIIN-Number

98Q96B.00000.LE.250

Issuer Level Classification & Status

8

FFI Status

Non-Financial US Entity

US Financial Entity

US Entity Foreign Entity

Foreign Financial Entity FFI

Non-Financial Foreign Entity NFFE

Exempt FFI

Deemed Compliant FFI Registered deemed compliant FFI

Certified deemed compliant FFI

Participating FFI

Non-Participating FFI

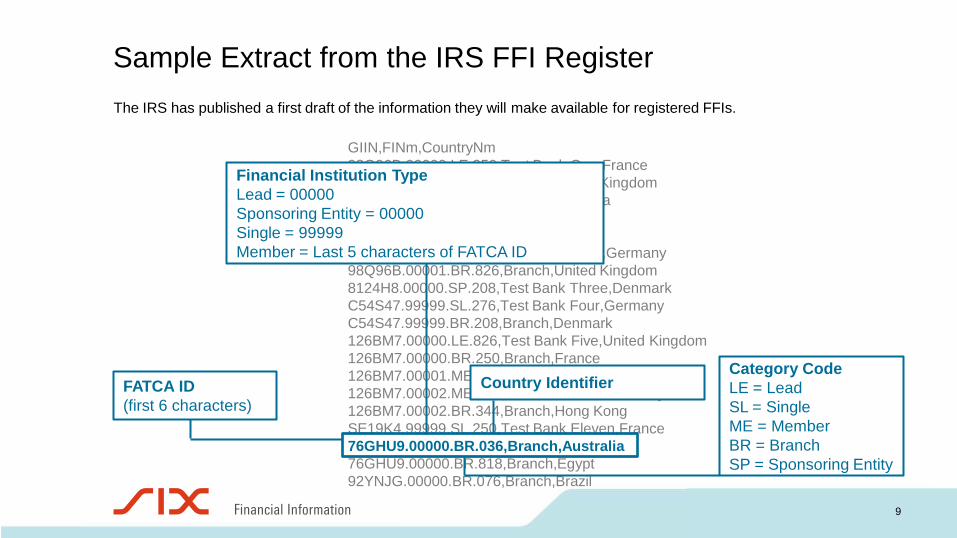

Sample Extract from the IRS FFI Register

9

The IRS has published a first draft of the information they will make available for registered FFIs.

GIIN,FINm,CountryNm 98Q96B.00000.LE.250,Test Bank One,France 98Q96B.00000.BR.826,Branch,United Kingdom 98Q96B.00000.BR.036,Branch,Australia 98Q96B.00000.BR.076,Branch,Brazil 98Q96B.00000.BR.818,Branch,Egypt 98Q96B.00001.ME.276,Test Bank Two,Germany 98Q96B.00001.BR.826,Branch,United Kingdom 8124H8.00000.SP.208,Test Bank Three,Denmark C54S47.99999.SL.276,Test Bank Four,Germany C54S47.99999.BR.208,Branch,Denmark 126BM7.00000.LE.826,Test Bank Five,United Kingdom 126BM7.00000.BR.250,Branch,France 126BM7.00001.ME.208,Test Bank Nine,Denmark 126BM7.00002.ME.276,Test Bank Ten,Germany 126BM7.00002.BR.344,Branch,Hong Kong SE19K4.99999.SL.250,Test Bank Eleven,France 76GHU9.00000.BR.036,Branch,Australia 76GHU9.00000.BR.818,Branch,Egypt 92YNJG.00000.BR.076,Branch,Brazil

FATCA ID (first 6 characters)

Financial Institution Type Lead = 00000 Sponsoring Entity = 00000 Single = 99999 Member = Last 5 characters of FATCA ID

Category Code LE = Lead SL = Single ME = Member BR = Branch SP = Sponsoring Entity

Country Identifier

Instrument Level Tax Status

10

30% withholding tax deducted for recalcitrant account holders and non-participating FFIs

Obligations with a fixed maturity date outstanding on 1 July 2014 exempt from 30% withholding tax

Subject to the pass-through payment percentage rules for the purpose of the 30% withholding tax

Not subject to the 30% withholding tax

FATCA Instrument Tax Status

In Scope US Security

Exempt Grandfathered US Security

Partly In Scope Security Issued by FFI

Out of Scope Security Issued by NFFE

In Scope Materially Modified Security

Exempt Short-Term Obligation

Obligations which are payable 183 days or less from the date of original issue

Previously Grandfathered Security which has undergone a Material Modification and is now subject to withholding

“LIVE” DATA available now

Material Modification

EXAMPLE

“In scope” Instrument: IBM Share, ISIN US4592001014

11

12

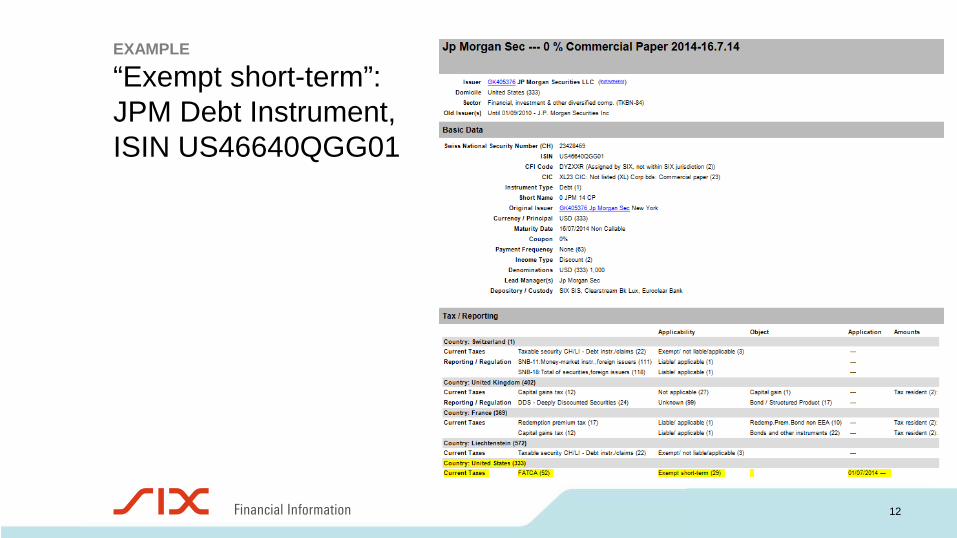

EXAMPLE

“Exempt short-term”: JPM Debt Instrument, ISIN US46640QGG01

13

EXAMPLE

“Exempt grandfathered”: IBM Bond, ISIN US459200HK05

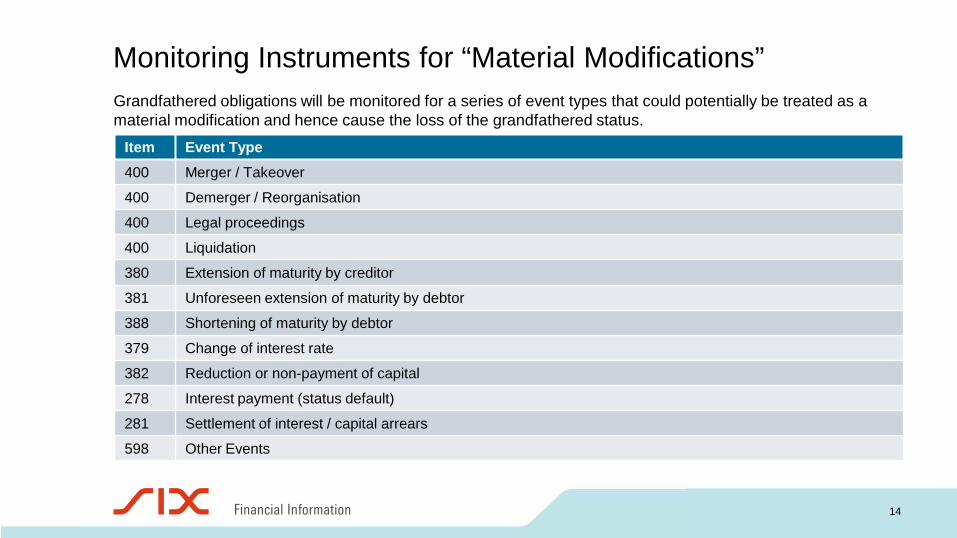

Monitoring Instruments for “Material Modifications”

14

Item Event Type 400 Merger / Takeover

400 Demerger / Reorganisation

400 Legal proceedings

400 Liquidation

380 Extension of maturity by creditor

381 Unforeseen extension of maturity by debtor

388 Shortening of maturity by debtor

379 Change of interest rate

382 Reduction or non-payment of capital

278 Interest payment (status default)

281 Settlement of interest / capital arrears

598 Other Events

Grandfathered obligations will be monitored for a series of event types that could potentially be treated as a material modification and hence cause the loss of the grandfathered status.

15

Grandfathered Securities Corporate Events

Create Monitoring List

Issuer / Agent

Request Qualification

Monitoring List Process Monitoring List

Update Instrument Tax Status

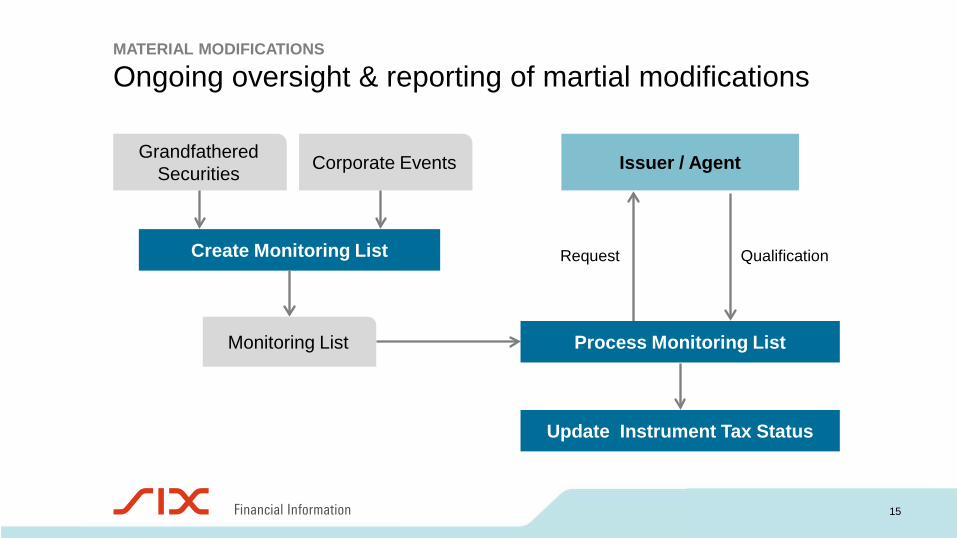

MATERIAL MODIFICATIONS

Ongoing oversight & reporting of martial modifications

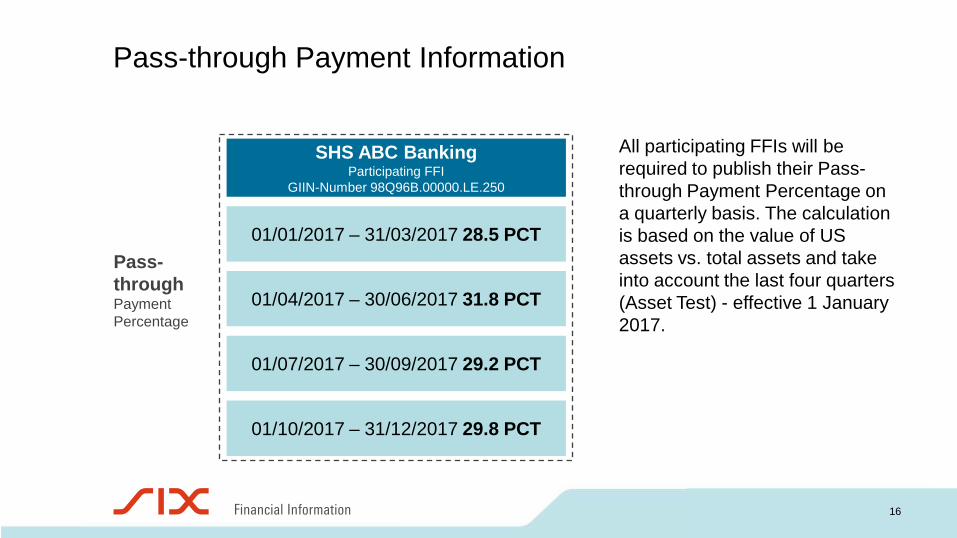

All participating FFIs will be required to publish their Pass-through Payment Percentage on a quarterly basis. The calculation is based on the value of US assets vs. total assets and take into account the last four quarters (Asset Test) - effective 1 January 2017.

Pass-through Payment Percentage

SHS ABC Banking Participating FFI

GIIN-Number 98Q96B.00000.LE.250

01/01/2017 – 31/03/2017 28.5 PCT

01/04/2017 – 30/06/2017 31.8 PCT

01/07/2017 – 30/09/2017 29.2 PCT

01/10/2017 – 31/12/2017 29.8 PCT

16

Pass-through Payment Information

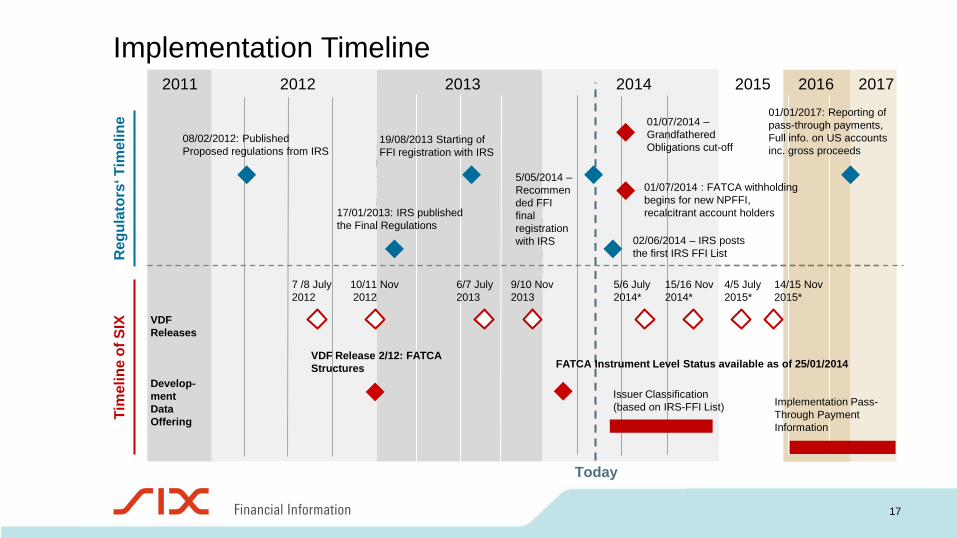

Implementation Timeline

17

2012 2013 2014 2015

2011

Starting of FFI registration with IRS

Summer 2012: Final regulations from IRS anticipated

1 January 2014 /2015: Start of withholding and reporting of US clients personal information and acc. balance 7 /8 July

2012 10/11 Nov 2012

16/17 Nov 2013*

15/16 Nov 2014*

6/7 July 2013*

5/6 July 2014*

8 February 2012: Published Proposed regulations from IRS

Reg

ulat

ors‘

Tim

elin

e

2012 2013 2014 2011

19/08/2013 Starting of FFI registration with IRS

01/01/2017: Reporting of pass-through payments, Full info. on US accounts inc. gross proceeds

17/01/2013: IRS published the Final Regulations

01/07/2014 : FATCA withholding begins for new NPFFI, recalcitrant account holders

7 /8 July 2012

10/11 Nov 2012

9/10 Nov 2013

15/16 Nov 2014*

14/15 Nov 2015*

VDF Releases

6/7 July 2013

5/6 July 2014*

4/5 July 2015*

Develop- ment Data Offering

08/02/2012: Published Proposed regulations from IRS

Tim

elin

e of

SIX

Issuer Classification (based on IRS-FFI List) Implementation Pass-

Through Payment Information

2016

5/05/2014 – Recommended FFI final registration with IRS

2017

02/06/2014 – IRS posts the first IRS FFI List

VDF Release 2/12: FATCA Structures

01/07/2014 – Grandfathered Obligations cut-off

FATCA Instrument Level Status available as of 25/01/2014

Today

Thank you for your attantion Jacob Gertel

Business Development, SIX Financial Information