finance 590

DESCRIPTION

Finance 590. Enterprise Risk Management Lecture 3 Mark C. Vonnahme Department of Finance University of Illinois at Urbana-Champaign. ERM. What is Enterprise Risk Management A quick review of our prior discussions Industry analysis v individual firm analysis - PowerPoint PPT PresentationTRANSCRIPT

Finance 590

Enterprise Risk Management

Lecture 3

Mark C. Vonnahme

Department of Finance

University of Illinois at Urbana-Champaign

ERM

• What is Enterprise Risk Management– A quick review of our prior discussions– Industry analysis v individual firm analysis

• Organization’s risk profile is unique

• Similarities and differences to others

ERM

• An organization’s risks by their nature– Dynamic– Fluid– Highly interdependent– Cannot be broken into components– Need to be managed in an integrated approach

ERM

• Integrated approach v silos– Personal experiences

• Property casualty

• Surety

ERM

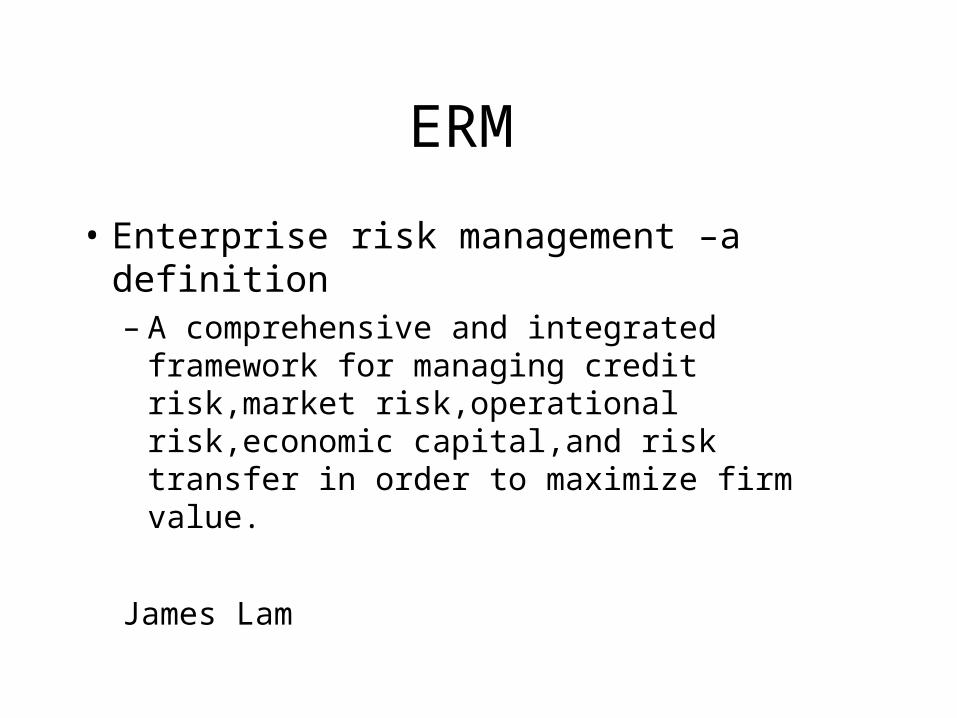

• Enterprise risk management –a definition– A comprehensive and integrated framework for

managing credit risk,market risk,operational risk,economic capital,and risk transfer in order to maximize firm value.

James Lam

ERM

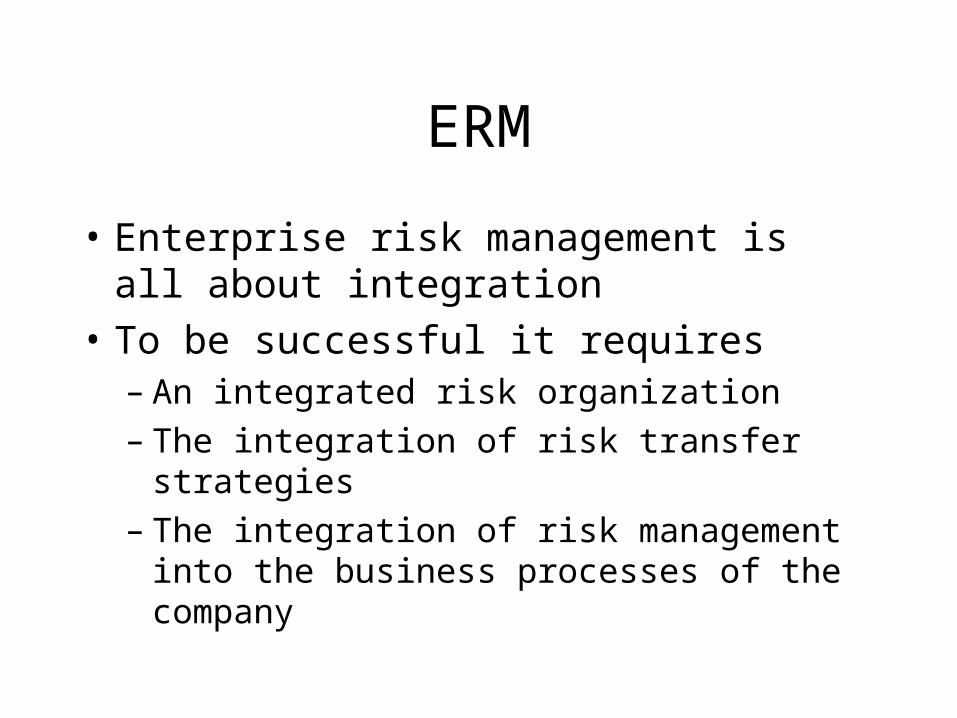

• Enterprise risk management is all about integration

• To be successful it requires– An integrated risk organization– The integration of risk transfer strategies– The integration of risk management into the

business processes of the company

ERM

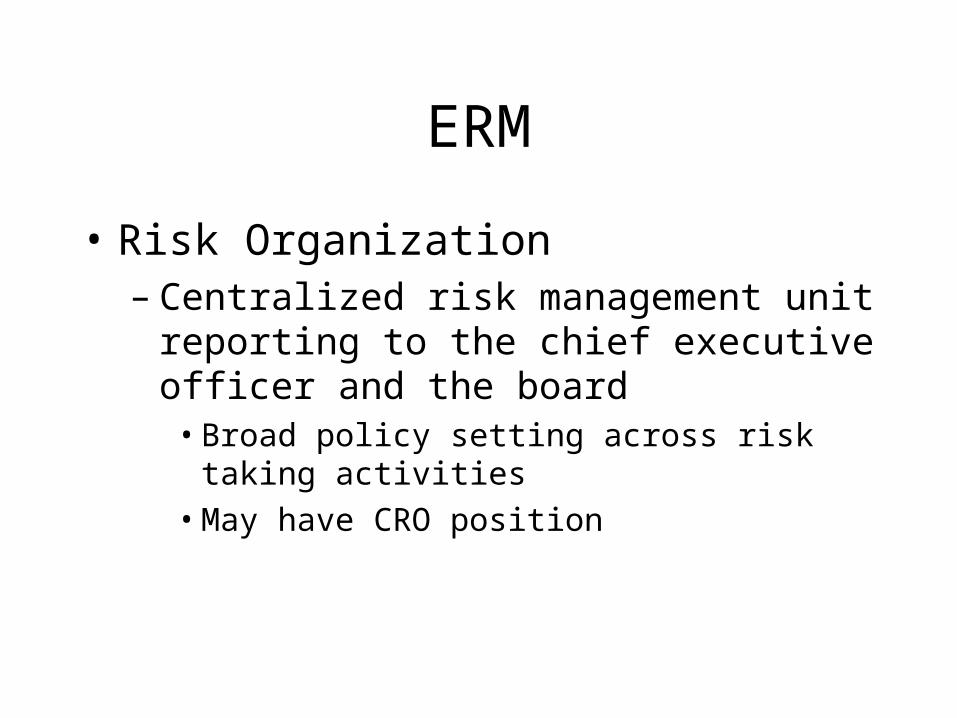

• Risk Organization– Centralized risk management unit reporting to

the chief executive officer and the board• Broad policy setting across risk taking activities

• May have CRO position

ERM

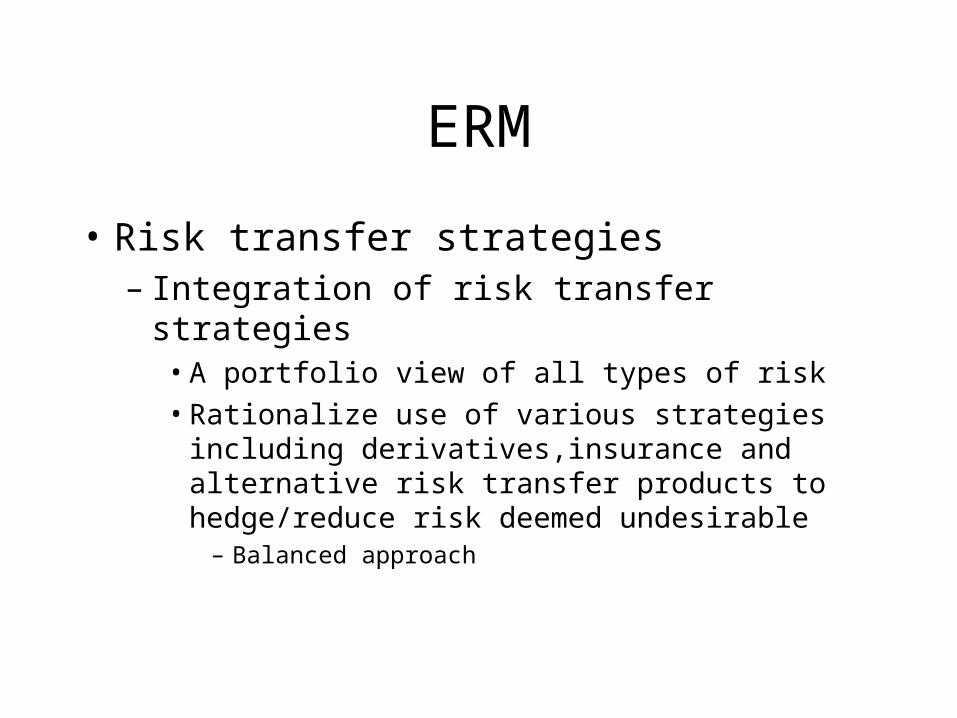

• Risk transfer strategies– Integration of risk transfer strategies

• A portfolio view of all types of risk

• Rationalize use of various strategies including derivatives,insurance and alternative risk transfer products to hedge/reduce risk deemed undesirable

– Balanced approach

ERM

• Risk management into the business processes of the company– Offensive v defensive mechanism

• Proactive v reactive management approach

– Optimize business performance • Influence on pricing , resource allocation and other

business decisions

ERM

• The benefits of ERM– Increased organizational effectiveness– Better risk reporting– Improved business performance

ERM

• Increased organizational efficiency– CRO plus enterprise risk approach provides top

down approach for coordination– Address both individual risks plus the

interdependencies

ERM

• Better risk reporting– Provides timely and relevant info to management

• Info that allows them to manage the risks

– Silo v integrated approach• Which is more effective

– Increase risk transparency

– Provide the appropriate detail to • Management

• CEO

• Board

ERM

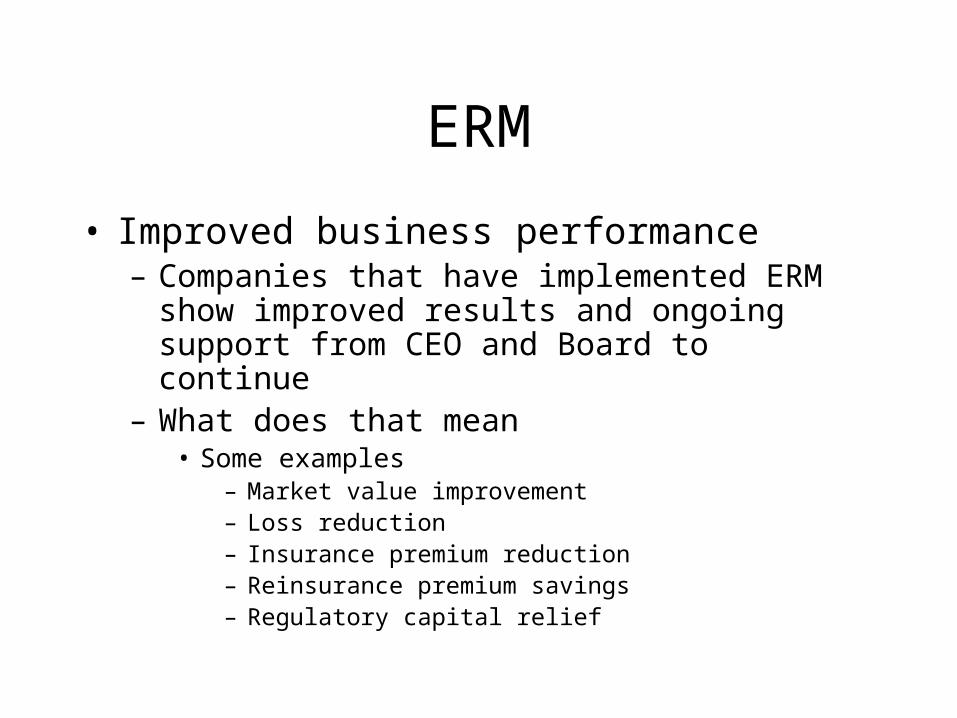

• Improved business performance– Companies that have implemented ERM show

improved results and ongoing support from CEO and Board to continue

– What does that mean• Some examples

– Market value improvement– Loss reduction– Insurance premium reduction– Reinsurance premium savings– Regulatory capital relief

ERM

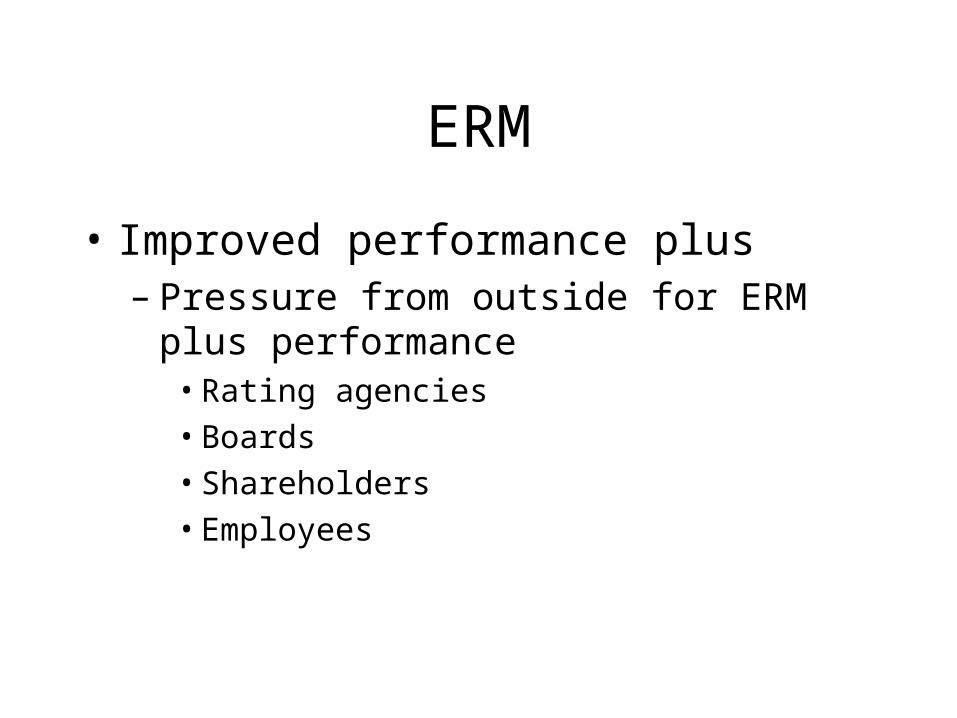

• Improved performance plus– Pressure from outside for ERM plus

performance• Rating agencies

• Boards

• Shareholders

• Employees

ERM

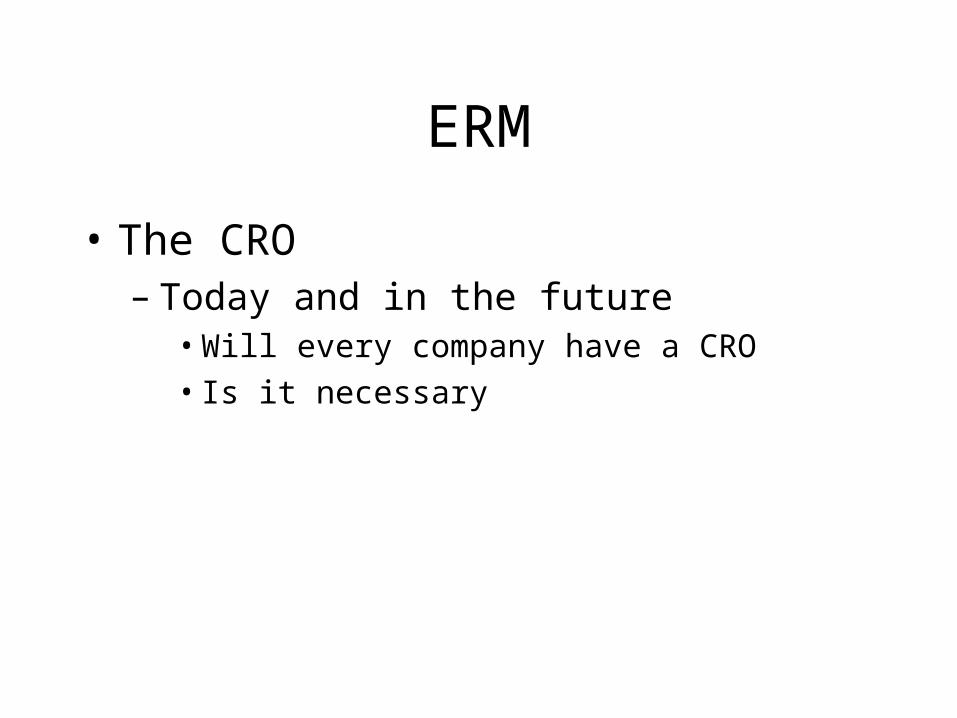

• The CRO– Today and in the future

• Will every company have a CRO

• Is it necessary

ERM

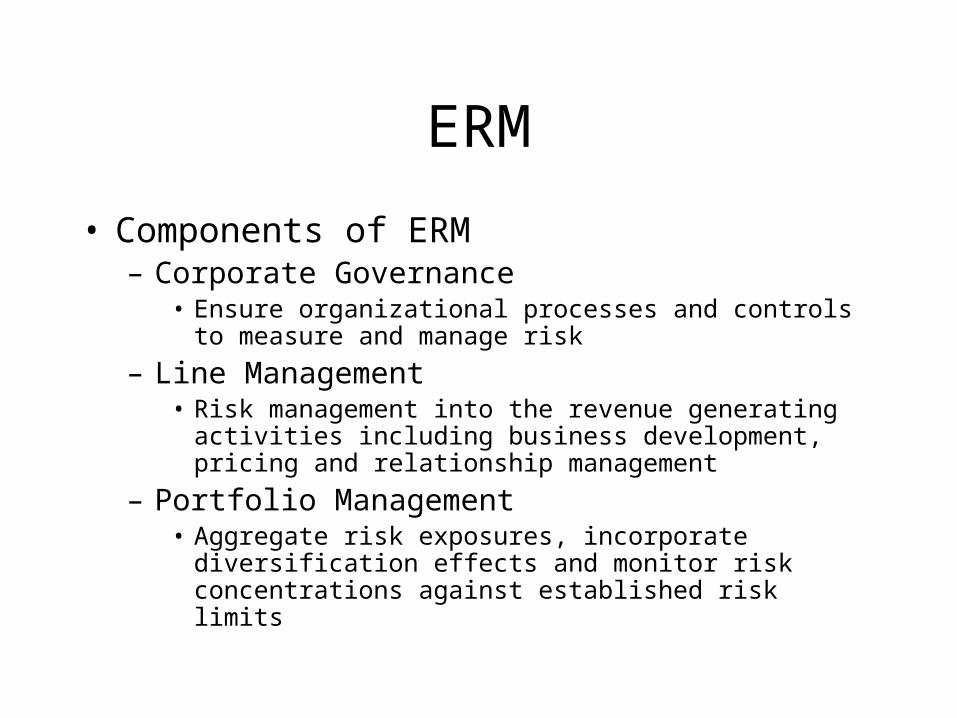

• Components of ERM– Corporate Governance

• Ensure organizational processes and controls to measure and manage risk

– Line Management• Risk management into the revenue generating activities

including business development, pricing and relationship management

– Portfolio Management• Aggregate risk exposures, incorporate diversification effects

and monitor risk concentrations against established risk limits

ERM

• Components of ERM continued– Risk Transfer

• Mitigate risk exposures that are too high or more cost effective to transfer v hold

– Risk Analytics• Risk measurement, analysis,and tools to quantify

and track risk exposures

ERM

• Components of ERM continued– Data and Technology Resources

• Support analytics and reporting processes

– Stakeholder Management• Communicate and report the company’s risk

information to key stakeholders

ERM

• Risk Analytics– Started to discuss last class– Will continue as we move forward

• Corporate Governance – Will begin discussion today– Will continue throughout class

• Line Management – Will start to share thoughts on it today– Share some experiences with you

ERM

• Questions

Finance 590

Enterprise Risk Management

Mark C. Vonnahme

Department of Finance

UIUC

ERM

• Corporate Governance– Ensures board of directors and senior

management have established “appropriate” organizational processes and corporate controls to measure and manage risk

– Mandate is worldwide in business• Regulatory agencies and legislative bodies are

calling for stronger controls

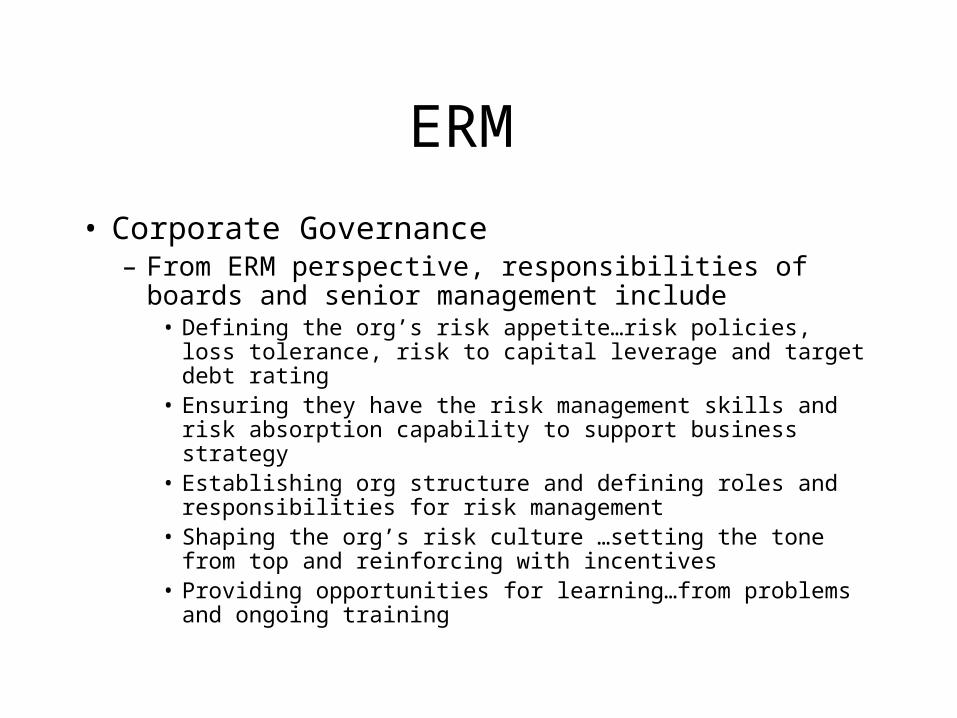

ERM

• Corporate Governance – From ERM perspective, responsibilities of boards and

senior management include• Defining the org’s risk appetite…risk policies, loss tolerance,

risk to capital leverage and target debt rating• Ensuring they have the risk management skills and risk

absorption capability to support business strategy• Establishing org structure and defining roles and

responsibilities for risk management• Shaping the org’s risk culture …setting the tone from top and

reinforcing with incentives• Providing opportunities for learning…from problems and

ongoing training

ERM

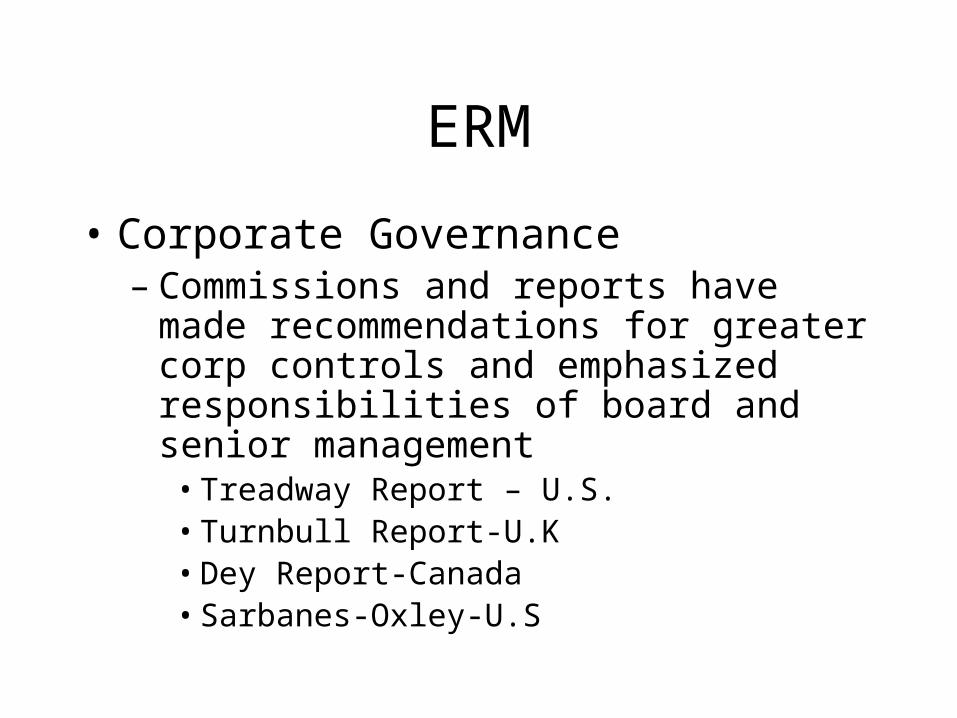

• Corporate Governance– Commissions and reports have made

recommendations for greater corp controls and emphasized responsibilities of board and senior management

• Treadway Report – U.S.• Turnbull Report-U.K• Dey Report-Canada• Sarbanes-Oxley-U.S

ERM

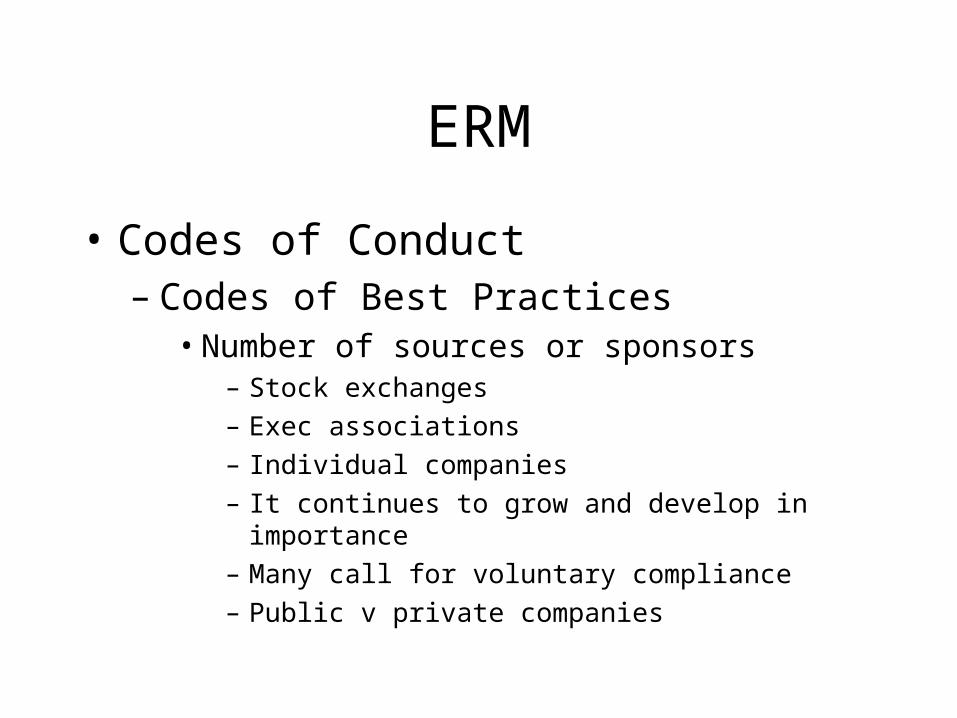

• Codes of Conduct– Codes of Best Practices

• Number of sources or sponsors– Stock exchanges

– Exec associations

– Individual companies

– It continues to grow and develop in importance

– Many call for voluntary compliance

– Public v private companies

ERM

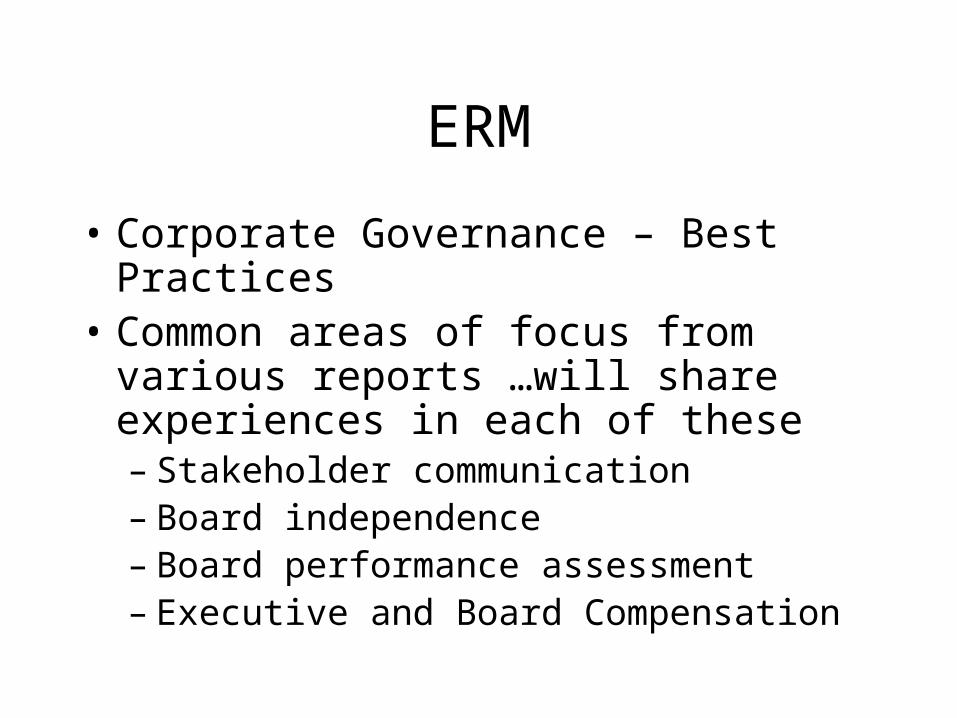

• Corporate Governance – Best Practices• Common areas of focus from various

reports …will share experiences in each of these– Stakeholder communication– Board independence– Board performance assessment– Executive and Board Compensation

ERM

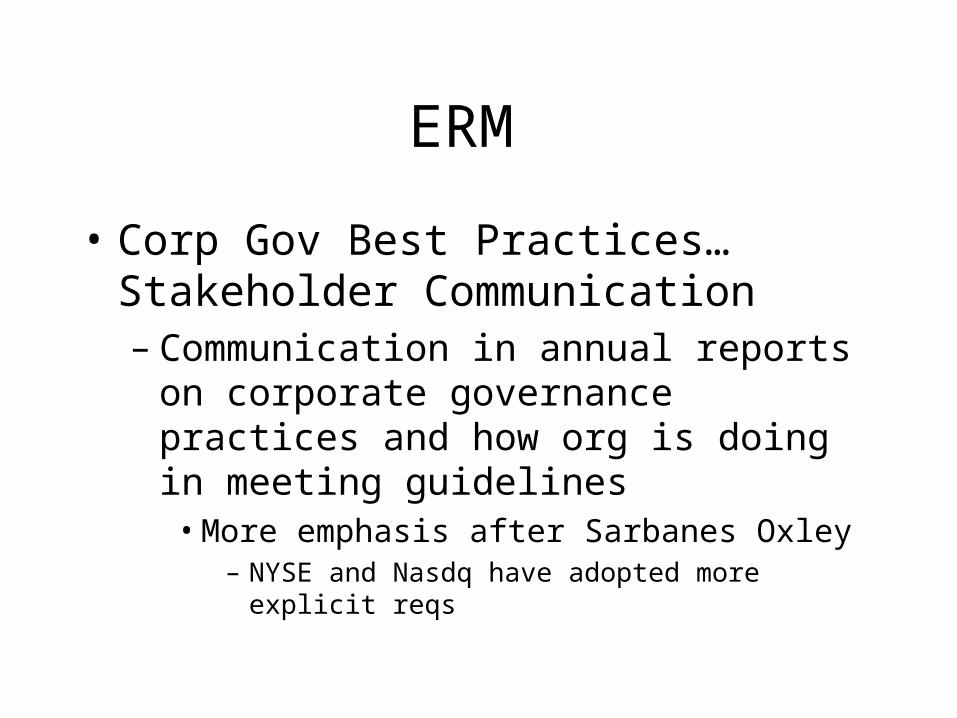

• Corp Gov Best Practices…Stakeholder Communication– Communication in annual reports on corporate

governance practices and how org is doing in meeting guidelines

• More emphasis after Sarbanes Oxley – NYSE and Nasdq have adopted more explicit reqs

ERM

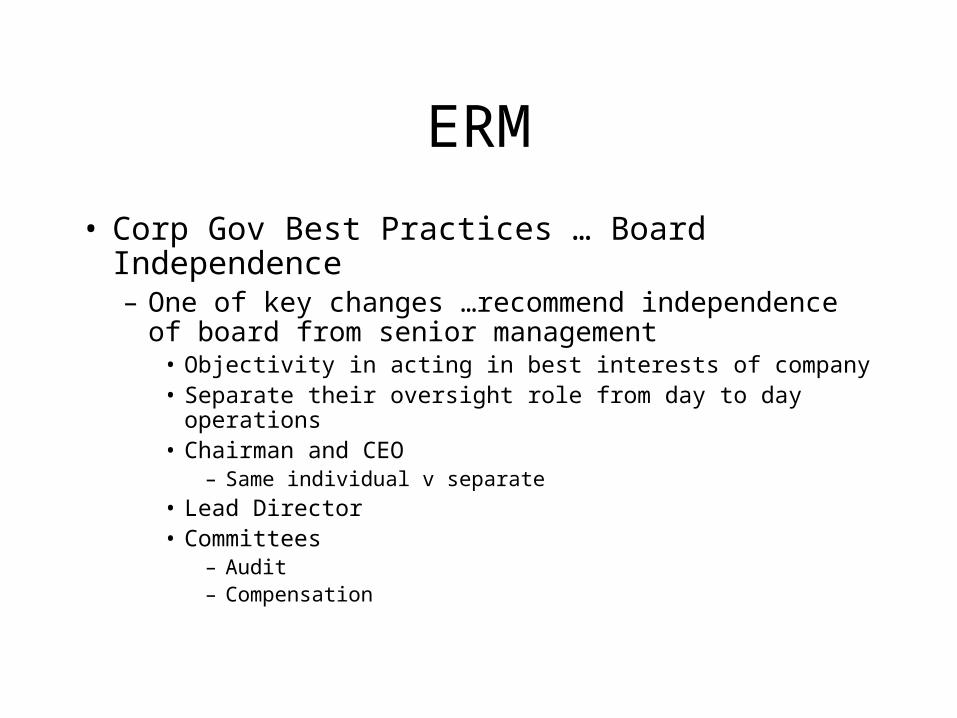

• Corp Gov Best Practices … Board Independence– One of key changes …recommend independence of

board from senior management• Objectivity in acting in best interests of company• Separate their oversight role from day to day operations• Chairman and CEO

– Same individual v separate

• Lead Director• Committees

– Audit– Compensation

ERM

• Corp Gov Best Practices…Board Performance Assessment– Recommendation to assess individual and

overall board performance• Will develop over time

– Not universally in place today

• Board positions are “hard work”– Difficult to find board members for public companies

ERM

• Corp Gov Best Practices …Executive and Board Comp– Performance evaluation of CEO

• Set goals and objectives

• Comp structure ... salary, bonus, LT incentives

– Director Compensation• “Avoid overpayment”

– Theory v reality

• Should comp include stock in company– Most would say yes

ERM

• Linking Corporate Governance and ERM– Why is it important– What is the linkage

ERM

• Corp Gov and ERM– Impetus for change in corp governance has

changed corp risk management practices– Similar focus on strategic direction, corporate

integration, and motivation– Good board practices and corp governance are

crucial for effective ERM

ERM

• Corp Governance and ERM– Areas of ERM allied to boards

• Risk appetite and policy

• Organizational structure

• Risk culture and corporate values

ERM

• Questions

• Discussion

Finance 590

Enterprise Risk Management Line Management

Mark C. Vonnahme

Department of Finance

UIUC

ERM

• Line Management – Key revenue producing activities– Structure generally involves SBUs

• My experiences as head of SBU

– Account for majority of assets and employees– Risks are/ or can be significant

• Property casualty insurance

• Surety

ERM

• Interaction of Line with Risk Management• Alignment of Line with RM strategies is crucial

– Impact on new business development• Relationship between line and RM can impact customer

relationships

– Line managers need to understand pricing implications• Losses

• Cost of capital

• Other

ERM

• Key risk issues involving Line and RM– Relationship between line units and RM– Key challenges for line risk management– Best practices for line risk management

ERM

• Relationship between Line and RM– Adversarial relationship v a working

partnership– Structural issues

• Offense v defense

• Policy and policing

• Partnership

ERM

• Line management and RM– Structure

• Offense v defense– Objectives may not be aligned

– HO v Field

– We v they

» Some personal experiences in credit extension

ERM

• Line management and RM– Structure

• Policy and policing– The government v citizenry model

– Policy set

– Line can operate unless exceptions

– But RM is not involved on day to day

– Policies become outmoded

– No real incentives to report outsiders to policy

ERM

• Line Management and RM– Partnership

• RM fully integrated into business

ERM

• Line management and risk management alignment – Key challenges

• Conflict resolution

• Role of line risk management

• Incentive alignment

• Non-financial risk management

ERM

• Line Management-Best Practices• ERM program should integrate risk

management processes into business management processes– Business strategy and planning– New product and business development– Product pricing– Business performance measurement

ERM

• Summary

• Questions

Finance 590Enterprise Risk Management

Steve D’ArcyDepartment of Finance

Lecture 3

Hazard Risk Analytics

April 5, 2005

Reference Material• Chapter 8 – Enterprise Risk Management by

Lam

• Risk and Insurance by Anderson and Brown

http://www.soa.org/ccm/cms-service/stream/asset/?asset_id=8027034

Overview

• Characteristics of Hazard Risk

• Insurance Terminology

• Examples

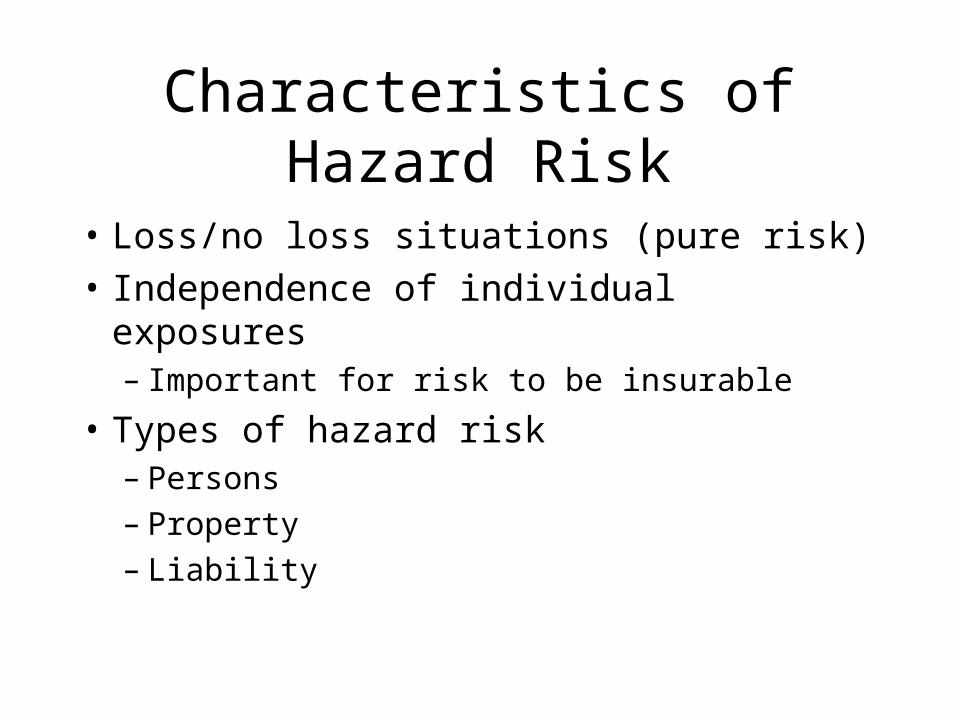

Characteristics of Hazard Risk

• Loss/no loss situations (pure risk)

• Independence of individual exposures– Important for risk to be insurable

• Types of hazard risk– Persons– Property– Liability

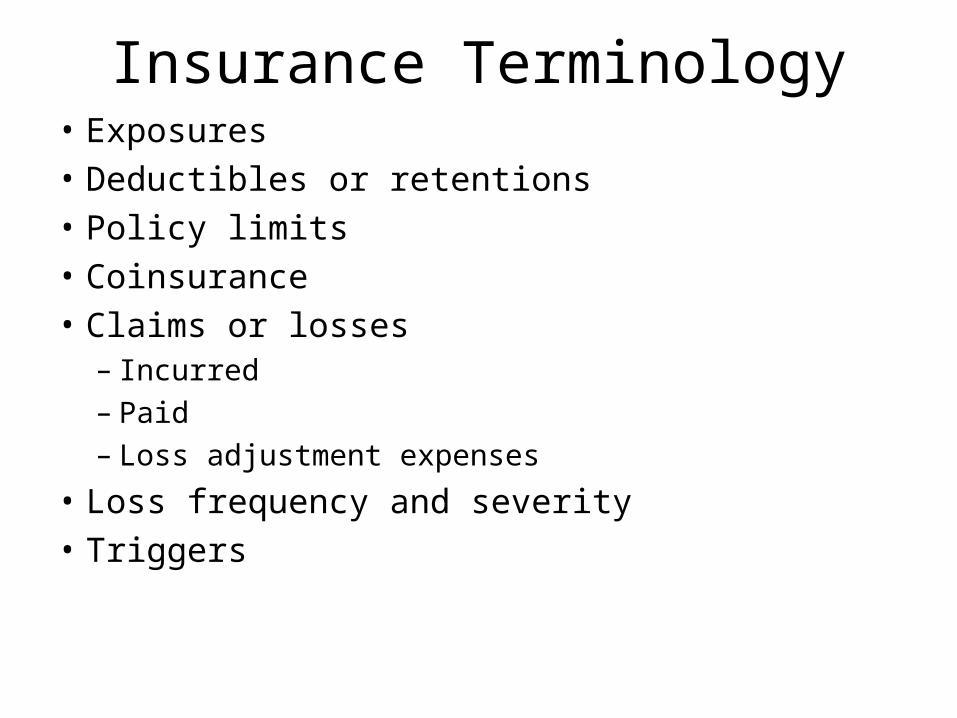

Insurance Terminology• Exposures• Deductibles or retentions• Policy limits• Coinsurance• Claims or losses

– Incurred– Paid– Loss adjustment expenses

• Loss frequency and severity • Triggers

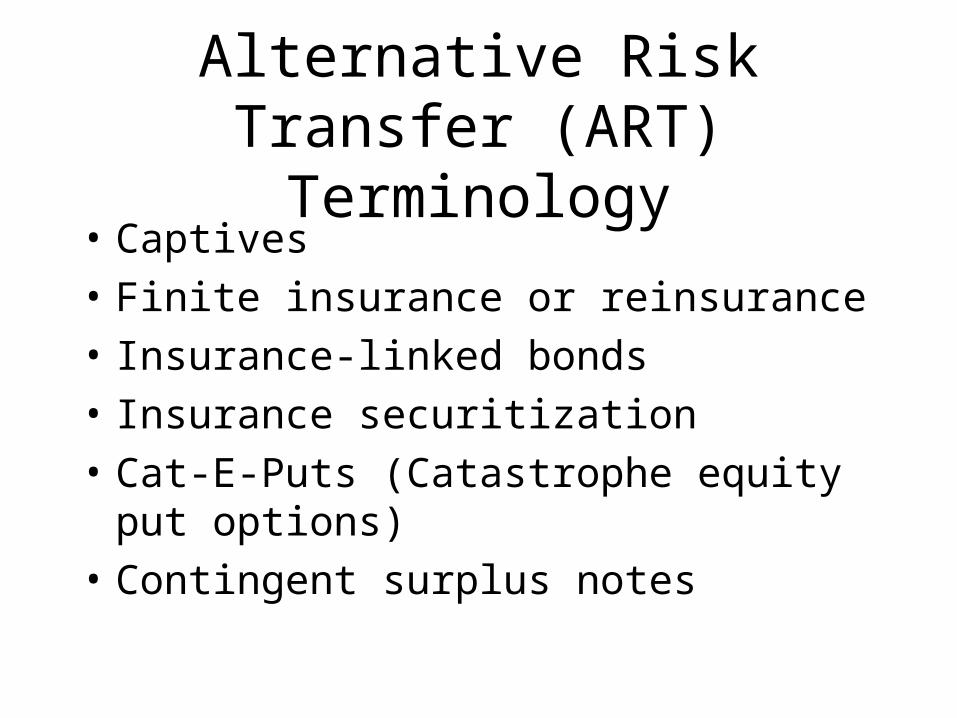

Alternative Risk Transfer (ART) Terminology

• Captives

• Finite insurance or reinsurance

• Insurance-linked bonds

• Insurance securitization

• Cat-E-Puts (Catastrophe equity put options)

• Contingent surplus notes

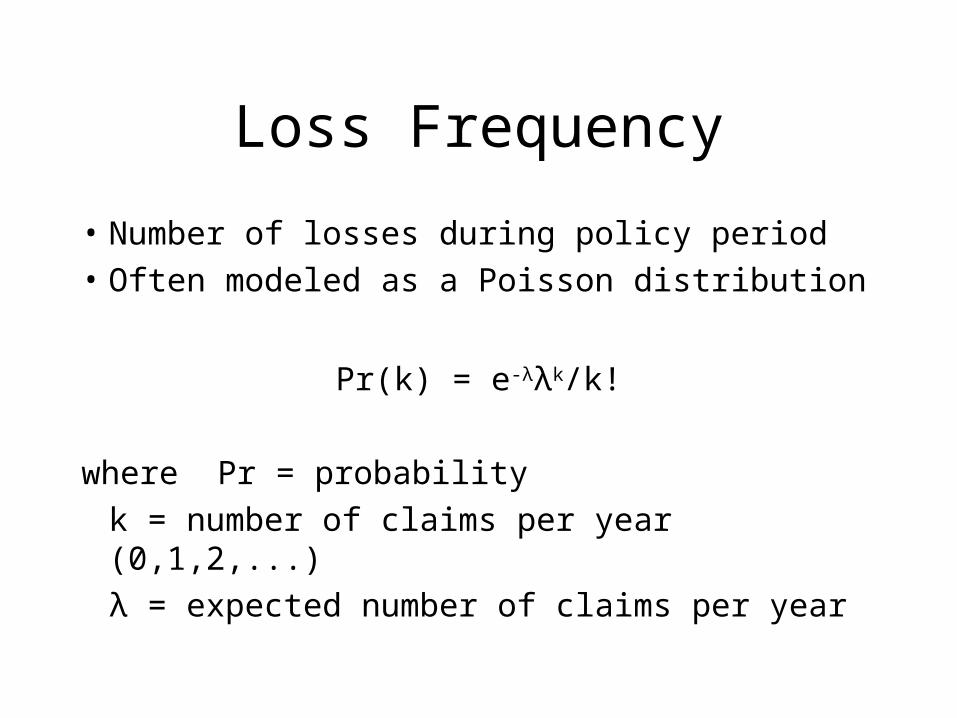

Loss Frequency

• Number of losses during policy period

• Often modeled as a Poisson distribution

Pr(k) = e-λλk/k!

where Pr = probability

k = number of claims per year (0,1,2,...)

λ = expected number of claims per year

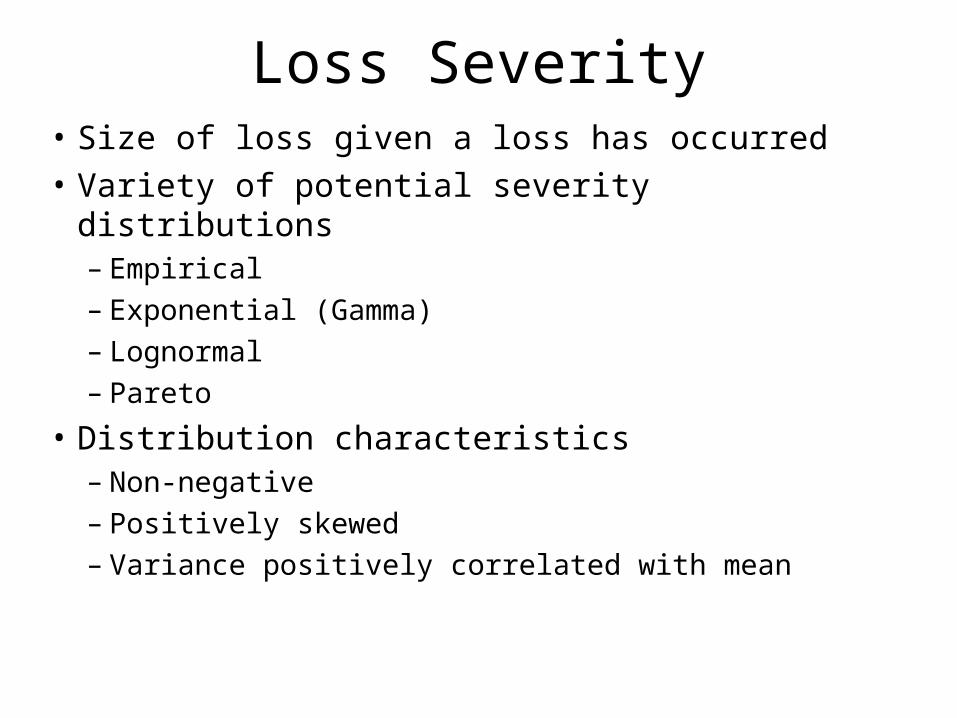

Loss Severity• Size of loss given a loss has occurred• Variety of potential severity distributions

– Empirical– Exponential (Gamma)– Lognormal– Pareto

• Distribution characteristics– Non-negative– Positively skewed– Variance positively correlated with mean

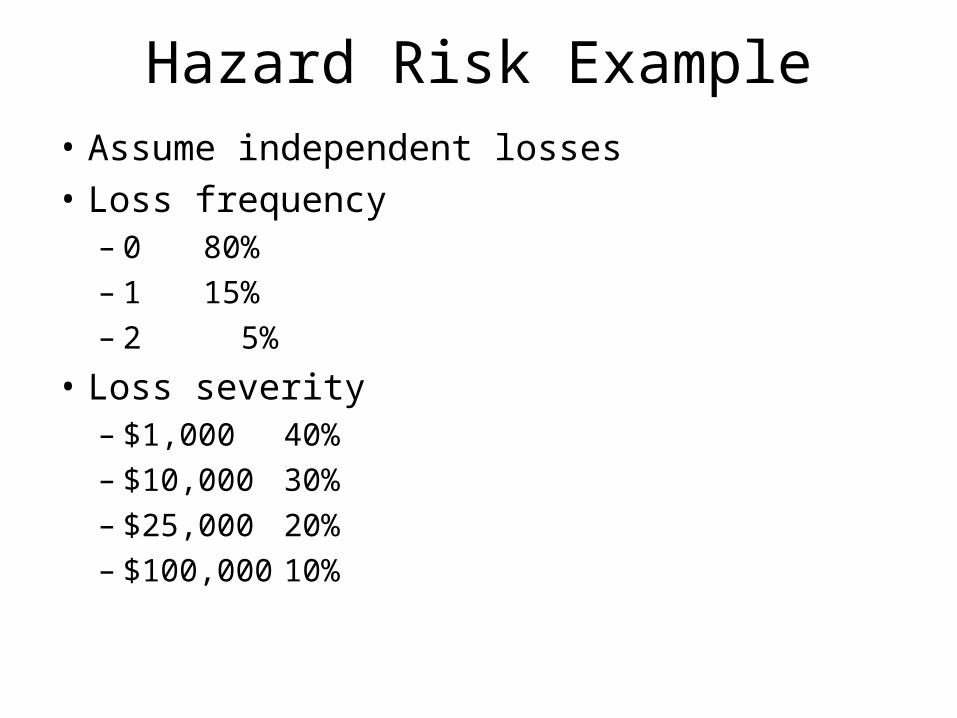

Hazard Risk Example• Assume independent losses• Loss frequency

– 0 80%– 1 15%– 2 5%

• Loss severity– $1,000 40%– $10,000 30%– $25,000 20%– $100,000 10%

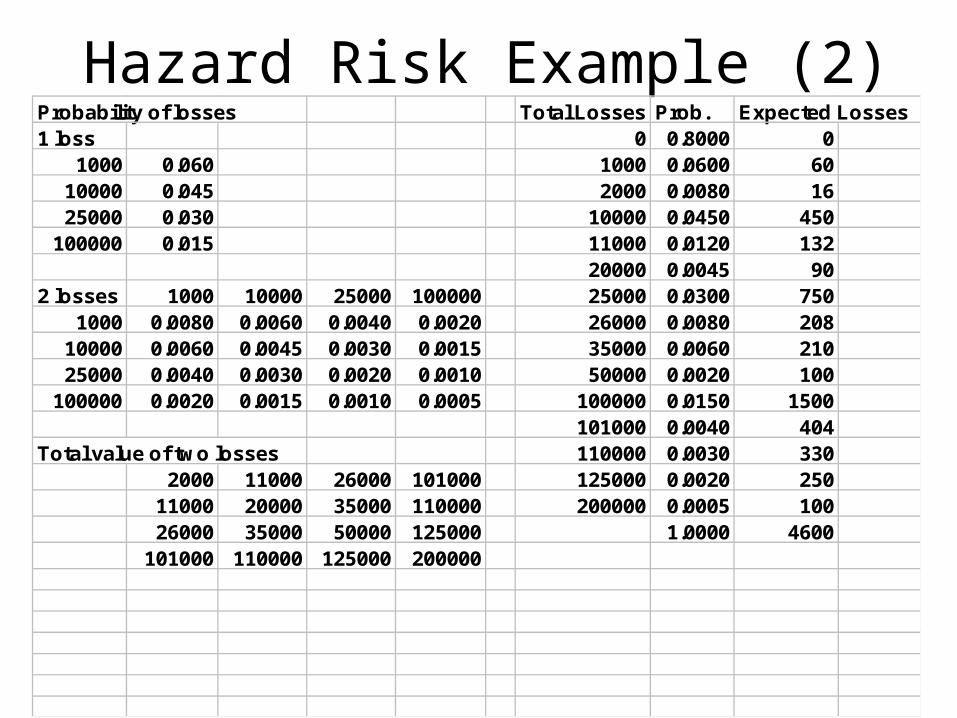

Hazard Risk Example (2)Probability of losses Total Losses Prob. Expected Losses1 loss 0 0.8000 0

1000 0.060 1000 0.0600 6010000 0.045 2000 0.0080 1625000 0.030 10000 0.0450 450

100000 0.015 11000 0.0120 13220000 0.0045 90

2 losses 1000 10000 25000 100000 25000 0.0300 7501000 0.0080 0.0060 0.0040 0.0020 26000 0.0080 208

10000 0.0060 0.0045 0.0030 0.0015 35000 0.0060 21025000 0.0040 0.0030 0.0020 0.0010 50000 0.0020 100

100000 0.0020 0.0015 0.0010 0.0005 100000 0.0150 1500101000 0.0040 404

Total value of two losses 110000 0.0030 3302000 11000 26000 101000 125000 0.0020 250

11000 20000 35000 110000 200000 0.0005 10026000 35000 50000 125000 1.0000 4600

101000 110000 125000 200000

Analysis of Potential Losses

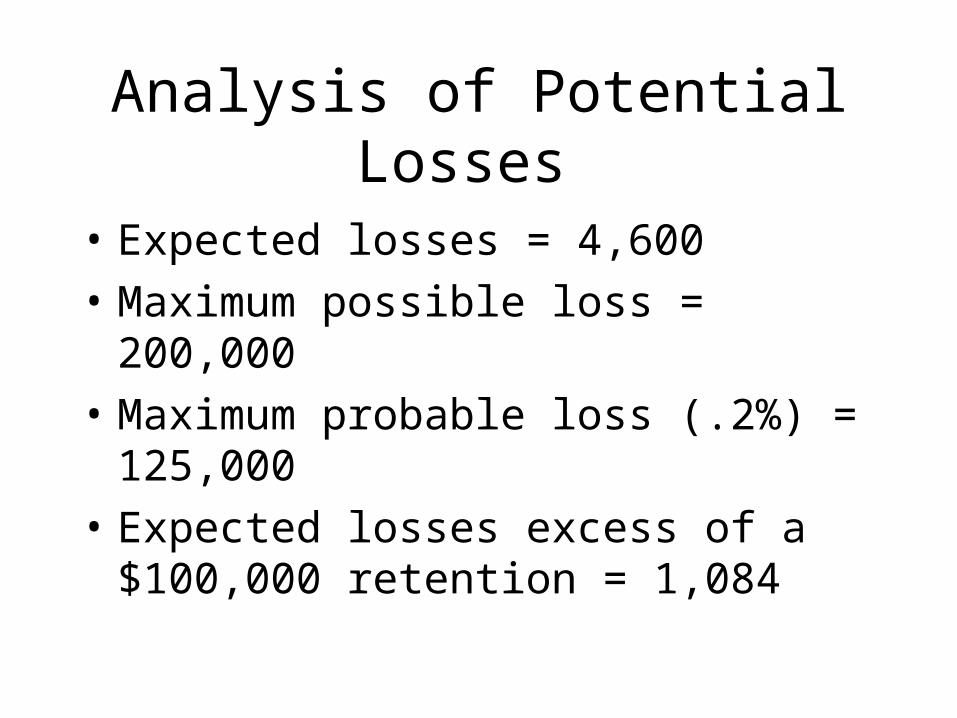

• Expected losses = 4,600

• Maximum possible loss = 200,000

• Maximum probable loss (.2%) = 125,000

• Expected losses excess of a $100,000 retention = 1,084

Conclusion• Insurance industry has developed a high level of

mathematical sophistication for valuing hazard risks

• Alternative market has also developed for dealing with hazard risks

• Key questions for organizations involve amount of risk to retain (deductible) and how much coverage to purchase (policy limits)

• These questions begin to tie hazard risk into enterprise risk management