f.no. stc/4-07/srpl/o&a/19-20

TRANSCRIPT

F.No. STC/4-07/SRPL/O&A/19-20=<%

0|q[cT7T, uft,\s4t Hf^cl/^^.TF?T.,i-fcFf ^fci^cpPicf)

OFFICE OF THE PRINCIPAL COMMISSIONER OF CENTRAL GST, AHMEDABAD-SOUTH 7th FLOOR, GST BHAVAN, NR. POLYTECHNIC, AMBAVADI,

AHMEDABAD-380015

f^f%TTr^ft^^lTT/ By REGISTERED POST A.D. VX-tlF. No. STC/4-07/SRPL/0&A/19-20 DIN: 20201264WS000000C598 3IT%9r cl 10 <.a/Date of Order: 07-12-2020

^ I (1 cl 10 <d/Date of Issue : 07-12-2020s*lTr MI Rd/Passed by:- jh i < Ri^ ,^rsrpT

SUNIL KUMAR SINGH, PRINCIPAL COMMISSIONER W 3n%^T tmr / Order-In-Original No : AHM-EXCUS-001-COM-016-20-21 Dated 07-12-2020

Rid (4^ ^ ■'dlcRf .^3% odRtdldThis copy is granted free of charge for private use of the person(s) to whom it is sent.

1.

W 3TT?2TR 3T7t^T-FT #^TTf^ A ffpT% ^ftcR;#fTT ,dcqK pTr tfte pr 3TT^?r % 3i41^ Tr^cfi

-dldlRpTTvr ,0-20,

2.

3PftTT ,TTbRT pTi ^cMK p^dOjfldd't ,^5 ^TFffecT,3l^HdidK 016 380-^RTU^fiTcT^Pfl dlf^UIAny person deeming himself aggrieved by this Order may appeal against this Order to the Customs, Excise and Service Tax Appellate Tribunal, Ahmedabad Bench within three months from the date of its communication. The appeal must be addressed to the Assistant Registrar, Customs, Excise and Service Tax Appellate Tribunal, 0-20, Meghani Nagar, Mental Hospital Compound, Ahmedabad-380 016.

TTcT 3rftcT S)l<?M TT. p. ft.-5 dlHdci ejfpft -dlf^^l dcMd 9pF) softer (RdRTdcft 2001 f^lDT 3 %FTR- Rqq (2) ff RRlRg odRbdl ^TTTpcTTSTTf^Ttr rnTTif|

softer qsf fr diRsin f%qr rnrr d-?rr f^rrr softer % softer # ^t ,Fj?r^t ^fttjeoft ft qf^tt ri-errr # fr qor ^ qor p yniRid (ftft ■■dTf|cr(i softn ft

^ qfcUft # s^f^o-rrr^ w^iThe Appeal should be filed in Form No. S.T.-5. It shall be signed by the persons specified in sub-rule (2) of Rule 3 of the Central Excise (Appeals) Rules, 2001. It shall be filed in quadruplicate and shall be accompanied by an equal number of copies of the order appealed against (one of which at least shall be certified copy). All supporting documents of the appeal should be forwarded in quadruplicate.softer f^rrnf qr f=N<ui p- ^offor % sosttt 911PW ^ .■d 1 < qf^ft fr Trf%rr rrnriff o'^tt

nr^r f^rcr so%^r % soflrr ^t Tf ifr ,T?r4it tft Tcoft qfcfTf rronor ^t rnrnft )tjR'^r ft tot 7t tht p y r i Rot q R ’•n (IThe Appeal including the statement of facts and the grounds of appeal shall be filed in quadruplicate and shall be accompanied by an equal number of copies of the order appealed against (one of which at least shall be a certified copy.)spftrr tt wt rnNft apm fr ^rr p ^ rfRi'H' p l^rfr % ftnspffTT % aTUTf % FT? %f\Wt % 3TTiTFf $PTK rTTTT p ^ qrrTff qfr sFHIpIT riuiRid

diFHJ ■dlf^O.IThe form of appeal shall be in English or Hindi and should be set forth concisely and under distinct heads of the grounds of appeals without any argument or narrative and such grounds should be numbered consecutively.

3.

.4

.5

Page 1 of21

-U//SKJ'L/U<5CA/ 1 V-/U

# mr 35 % srA Tffe f^r | ^ %!%# TT^r^cT # ?1WI" ^ <-^l’4 lf^+’!.0l % ^TfFT^ <Rl^K % TPR'WTfTT? % mIRu, 31Tr ^nrrft- cT^TT ^ iTTTr^TTcT 3Ttff^r % Wtt % 3TPT ^TITf%Tr^l^lllThe prescribed fee under the provisions of Section 35 B of the Act shall be paid through a crossed demand draft, in favour of the Assistant Registrar of the Bench of the Tribunal, of a branch of any Nationalized Bank located at the place where the Bench is situated and the demand draft shall be attached to the form of appeal.W STT^r % tflbl ,3cmK % 7.5%

TfW TT QdK f 3f?m^WRT?fh?i^TTfRI%«|RA f^TKf vsh+i 'y+dH sr^ttr^t^TAn appeal against this order shall lie before the Tribunal on payment of 7.5% of the duty demanded where duty or duty and penalty are in dispute, or penalty, where penalty alone is in dispute”.>-•41-4M4 STfirf^BT 1970 ,1-^ 6 % 5ld4d Rib, dvty R)t*Tpr 3tr^?T TT 1.00 ^M4I TT ’-4I-4M-4The copy of this order attached therein should bear a court fee stamp of Rs. 1.00 as prescribed under Schedule 1, Item 6 of the Court Fees Act, 1970.

.6

7.

8.

srfhrTT^ft^A.oo vrhrffdT^if^TiAppeal should also bear a court fee stamp of Rs. 4.00.

9.

Sub : Show Cause Notice bearing F.No. VI/1 (b)/CTA/Tech.-01/SCN/SRPL/2019-20 dated 10.04.2019 to M/s. Safal Reality Private Limited, 11th Floor, Safal Profitaire, Opposite Auda Garden, Prahladnagar, Alimedabad 380015.

Page 2 of21

F.No. STC/4-07/SRPL/O&A/19-20- s

Brief facts of the case

M/s. Safal Reality Private Limited, 11th Floor, Safal Profitaire, Opposite Auda Garden, Prahladnagar, Ahmedabad 380015 (here-in-after referred to as the ‘assessee’) is engaged in providing Construction service other than residential complex, including commercial/industrial building or civil structures, Renting of Immovable service, Construction service of residential complex. The said assessee is holding Service Tax Registration No AABCH6875LSD001 (presently falling under Range-I of Division-VIII (Vejalpur) of Central Goods & Service Tax, Ahmedabad South Commissionerate). The said assessee also avails the facility of Cenvat Credit under CENVAT Credit Rules, 2004.

During the course of audit conducted by the Officers of the Central Tax Audit Commissionerate, Ahmedabad, for the period from April 2016 to 2017-18 (upto June, 2017) and on verification of the Cenvat credit records, it was observed that the assessee is engaged in the activity of construction of commercial complex service and is availing Cenvat Credit of the service tax paid on the services received by them for their construction activity. They are utilizing the credit availed for payment of Service Tax.

2.

3. It was observed that the said assessee has obtained the Building Use (‘BU’) permission in respect of Scheme Sumel-6 on 18.09.2014 and 24.12.2014 for Block Nos “A to J” and in respect of Scheme Mondeal Heights on 29.03.2016 for Blocks “A and B”. After obtaining BU permissions referred above, the said assessee is not paying service tax on the units sold by them.

The assessee had utilized various input services of sub-contractors and other service- providers constituting major part of expenditure in construction of scheme Sumel-6 having total construction area 2138643 sq feet (1347673 sq feet for Sumel-6 and 790970 sq feet for Mondeal Heights) as on the dates of respective Building Use permissions obtained by them from Ahmedabad Municipal Corporation. Out of the total constructed area of 2138643 sq Feet (1347673 sq feet for Sumel-6 and 790970 sq feet for Mondeal Heights), they had sold 993297 sq Feet (723028 sq feet for Sumel-6 and 270269 sq feet for Mondeal Heights) before the BU permission was granted by the competent authority. Thus, 1145346 sq Feet (624645 sq feet for Sumel-6 and 520701 sq feet for Mondeal Heights) area remained as unsold area, as on date of obtaining the BU permission. However, they had already availed and utilized Cenvat credit of the said input services in respect of these constructed area, before the BU permissions were obtained. The said assessee appeared to have not paid service tax in respect of these non-taxable activities as these units have been booked after the dates of B.U. and entire consideration has been received after the date of BU permissions. Hence, there appeared to be a contravention of Rule 3 of Cenvat Credit Rules, 2004. Being provider of output service, they are required to take Cenvat credit of input services which have been used for output services in terms of Rule 3 of Cenvat Credit Rules, 2004.

3.1

Considering the above, the said service provider is required to reverse/pay the wrongly availed proportionate Cenvat credit of Rs 5,49,25,527/- for the period October 2013 to March- 2016, in respect of 1145346 Square Feet (624645 for Sumel-6 and 520701 for Mondeal Heights) which remain as unsold area as on date of B.U. Permission, along with applicable interest under Rule 14 of Cenvat Credit Rules, 2004 for contravention of Rule 3 of Cenvat Credit Rules, 2004. At the time of audit, on the basis of information provided by the said assessee, they had been asked to reverse Cenvat credit of Rs 5,49,25,527/- in respect of 1145346 sq feet area (624645 sq feet for Sumel-6 and 520701 sq feet for Mondeal Heights), on which service tax was not paid. The assessee under their letter dated 23.2.2019 showed their disagreement to the objection.

Taking into account Rule 3 of Cenvat Credit Rules, 2004, it appears that the said provider is required to avail Cenvat credit of input services which have been used in taxable output services only. Since taxable output service does not happen to be there in the course of transfer of title of immovable property by way of units/area sold after BU, the said service provider is required to pay/reverse wrongly availed Cenvat credit along with applicable interest under Rule 14 of the Cenvat Credit Rules, 2004. Accordingly, Revenue Para No 5 was raised and Final Service Tax Audit Report No. ST: 1353/2018-19(ST) dated 2.4.2019 was issued by the Assistant Commissioner, Circle-IV, Central Goods and Service Tax, Audit, Ahmedabad to the said assessee.

3.2

service3.3

Page 3 of21

■ , • F.No. STC/4-07/SRPL/O&A/19-20

Under the negative-list regime of Service Tax, with effect from 01.07.2012, certain activities have been made chargeable to Service Tax, as ‘declared services’ by virtul^of Section 66E of the Finance Act, 1994. One of such declared services is Construction Services and the relevant text of the statute reads as under:

4.

'3 S

" Section 66E: The following shall constitute declared services, namely :—a)b) construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration is received after issuance of completion-certificate by the competent authority.Explanation—For the purposes of this clause,—(I)(II)

When the construction is completed and the ‘Completion Certificate” is obtained, what turns out is an immovable property. When such property is sold/transferred after ‘Completion Certificate’ is received, it is deemed to be sale of immovable property which is specifically excluded from the definition of service, in terms of Section 65 (B) (44) of the Finance Act 1994, of which the relevant text reads as under:

4.1.

(44) “service” means any activity carried out by a person for another for consideration, and includes a declared service, but shall not include—

(a) an activity which constitutes merely,-—

(i) a transfer of title in goods or immovable property, by way of sale, gift or in any other manner; or

From the above definition, it is clear that sale/transfer of title of immovable property, by way of sale, gift or in any other manner is excluded from the definition of service. Therefore, such a sale does not constitute ‘Service’.

A conjoint reading of the above provisions of law makes it explicit that, the activity of construction attracts Service Tax, if a part or whole of the consideration towards such construction is received prior to Completion Certificate/ Building Use permission is received. The activity of construction in which the entire consideration is received after Building Use permission, has been kept out of the scope of‘declared services’.

4.2

Accordingly, the said assessee is liable to pay Service Tax only for those units which have been booked /sold before the issue of Building Use (BU) permissions for Scheme Sumel-6 on 18.09.2014 and 24.12.2014 for Block Nos “A to J” and in respect of Scheme Mondeal Heights on 29.03.2016 for Blocks “A and B”, under Section 66 of the Finance Act, 1994 read with Service Tax Rules, 1994 .and consequentially no Service Tax would be paid for those units which have been sold after the issue of B. U. Permissions.

4.3

The builders undertake the construction of the building having different units. All the material, labour and other expenses are incurred in lump sum. However, the agreement for sale (booking) in respect of different units can be at different stage, right from Bhoomi-poojan to various phases of construction or even after completion of construction and obtaining Completion Certificate/ B. U. Permission. However, during the course of construction of complex, the builder/ developer utilizes the services of various labour contractors, such as electrical contractors, furniture contractors (for doors/ windows), tiles fitting contractors, colour contractors, etc., constituting major part of expenditure incurred by the builder/ developer. In addition, they also utilize certain services such as security service, telephone service, housekeeping service, etc. The builder/ developer receives Service Tax paid invoices from such contractors/service providers and avail the Cenvat Credit of Service Tax paid by the contractors/service providers.

5.

6. The eligibility and admissibility of Cenvat credit flows from the authority of Rule 3 of the Cenvat Credit Rules, 2004 which reads as under:

Page 4 of21

V'lrfW■ f ■

F.No. STC/4-07/SRPL/O&A/19-20

RULE 3. CENVAT credit. (J) A manufacturer or producer of final products or a provider of output service shall be allowed to take credit (hereinafter referred to as the CENVAT credit) of the duties, taxes, cess specified in the said rule paid

any input or capital goods received in the factory of manufacture of final product or [by] the provider of output service on or after the 10th day of September, 2004; and

any input service received by the manufacturer of final product or by the providerof output services on or after the 10th day of September. 2004

on -(i)

(ii)

The above definition clearly specifies the class of persons, who are entitled to Cenvat credit, as (i) Manufacturer or Producer of Final Products and (ii) Output service provider.

Though construction of a complex, building, civil structure or a part thereof, including a complex or.building intended for sale to a buyer, wholly or partly, is considered to be a declared service under Section 66E (b) of the Finance Act, 1994, the developer/builder cannot be said to have provided or agreed to provide such service in respect of each individual unit, till such unit is booked/sold on full or part payment, before the requisite permission is obtained from the competent authority. This situation exists because the sale of unit after receipt of “completion certificate” does not constitute service.

6.1

In the typical case of Construction service, service is said to be provided to each individual who books/purchases a unit, on payment of part/full consideration and not in respect of the entire building constructed. In other words, the builder is agreeing to provide or provide services to multiple service recipients in respect of individual unit of the same project. Till the time, an individual unit is booked/ sold, there is no element of service involved in as much as there is no service recipient and the natural corollary that follows is that no service is provided or agreed to be provided. In such a situation, it is service to self and therefore the developer/builder cannot be said to be the provider of output service (emphasis supplied) for the unit not booked/sold, at the time the requisite permission from the competent authority was issued. This will be the case for each individual unit constructed. This is the crux of the matter especially in light of the interpretation of the term ‘declared service’ at Sec. 65B (22) which read as under:

6.2

“declared service ” means any activity carried out by a verson for another person for consideration and declared as such under section 66E".

In other words the developer/builder is deemed to be the provider of output service only in those cases where the units are booked/ sold prior to obtaining the ‘Completion Certificate’ from the competent authority. Consequentially, no Cenvat credit can be availed in terms of Rule 3(1) supra, till the time a unit is booked on part/full payment of consideration, as till such time the person indulged in construction cannot be said to be the “Service provider” and is providing service to self, in so far as the units not booked/sold. The fact remains that the builder is very well aware of the booking status of the individual units and this leads to his knowledge of the fact whether he is an Output Service Provider for that particular shop/unit or otherwise. This position is very clear in light of the provisions of Sec. 65B (22) supra to which the builder cannot claim ignorance. Thus, the assessee cannot be held to be an Output Service Provider for the individual unit till such time every single unit is booked, prior to obtaining Completion Certificate. This is especially so in light of the fact that in the event that the unit is booked after receipt of Completion Certification, the builder is engaged in the activity of sale of immovable property and if the unit is booked before receipt of Completion Certification, the builder is engaged in providing Construction services to the proposed owner of the unit.

In a nutshell, till the time a unit is booked on payment of part/full consideration, service is provided or agreed to be provided. Thus, the assessee cannot be said to be an Output Service Provider in respect of such units in as much as there is no service recipient for such units and resultantly no service is provided or agreed to be provided.

In view of the above, it appears that the assessee is not entitled to take Cenvat credit proportionate to the services utilized for construction of units which have not been booked/sold prior to receiving Completion/B.U. certificate i.e. for which the assessee is not an Output Seivice Provider. Rule 3(1) of Cenvat Credit Rules clearly stipulates that only an output service provider is entitled to take Cenvat Credit.

no6.3

6.4

Page 5 of21

.No. STC/4-07/SRPL/O&A/19-20!;>r -V

It further appears that it may be generally claimed by the builders that at the time of incurring expenses or availing services, it is not known if it is being used for providing ‘output service’ or is being used for construction of units sold after receipt of completion certificate, not liable to payment of Service Tax. So far so good, but the builders availing credit of the entire expenses incurred on goods and services, even for those flats sold after receipt of completion certificate and where no service is provided and where no tax is paid, is not in consonance with law. This in itself should have been the cause for the builders to not avail the Cenvat credit, till each individual unit is booked on receipt of consideration, prior to obtaining completion/Building use certificate or in other words to say that they could have availed the Cenvat Credit only as and when the individual unit was booked and that too prior to obtaining Completion/Building Use Certificate. The said assessee has therefore wrongly taken the Cenvat Credit, in respect of those area which do not constitute service, in violation of the Rule 3(1) of the Cenvat Credit Rules, 2004.

6.5

In the case of construction service every project is a differently identifiable business and the provision of service element would begin on the booking of each individual unit & would cease on completion of the project and obtaining of completion/B.U. certificate, and therefore as exemplified above, no output service is said to be provided till the individual unit is booked on payment of part/full consideration, prior to obtaining completion/B.U. certificate. Moreover as soon as the completion/B.U. certificate is obtained, no service element exists in respect of the units sold/booked thereafter. However, majority of input services are used for the entire project and the Cenvat credit of the tax paid thereon is availed much prior to the completion of the project and obtaining completion/B.U. certificate & is also utilized for payment of Service Tax on the units booked/sold prior to obtaining such certificate. Hardly any credit availed, is in balance which would lapse on completion of the project/obtairiing of completion certificate. In such a scenario the exchequer would be defrauded of its legitimate dues in so far as the Cenvat credit of the tax paid on the services used in the construction of units sold after completion/B.U. certificate is obtained, is availed, and in which case there is neither any element of service nor any Service Tax is paid. To exemplify, a builder starts construction of project having 100 units. All the services of landscaping, works contractor (for construction), electrical fittings, architect service, furniture contractors (for doors/ windows), tiles fitting contractors, color contractors, etc. are availed and utilized prior to completion of the project subsequent to which a completion/B.U. certificate is issued. Assuming that Rs.10 lacs of Cenvat credit is involved/availed in the construction of these hundred , which works out to say Rs. 10,000 per unit, assuming all they are of equal dimensions. Now, if out of 100 units constructed, 60 units are sold/ booked prior to obtaining the completion certificate, output service will be said to be provided on these 60 units only in terms of provisions of Service Tax Act/Rules and Service Tax will be paid on the value of these 60 units only. In fact, no service is provided in respect of the remaining 40 units & no Service Tax is payable/ paid on these units. Consequentially, the builder should be entitled to Cenvat credit proportionate to the units in case where output service is provided, i.e. Rs.6 lacs (60 x 10000) and should have availed the same only as and when they provided output service to those persons who booked the units prior to obtaining completion certificate/B.U. permission. Therefore, availing & utilizing entire credit of Rs.10 lacs was neither intended by law nor is in consonance with the provisions of Cenvat Credit Rules. The availment of Cenvat credit in respect of all 100 units while paying Service Tax only in respect of 60 units , goes not only against the will of the statute but also enriches the assessee by permitting him to pay almost all his dues utilizing Cenvat credit, which in fact was never due to him. Permitting the Cenvat credit of all the services used for the entire project would result in double benefit & unjust enrichment of the builders at the cost of exchequer. This cannot be countenanced by law. Therefore, Cenvat credit wrongly availed in excess of the entitlement is required to be recovered under the provisions of Rule 14 of the Cenvat Credit Rules.

6.6

Further, in terms of Rule 2(1) of Cenvat Credit Rules, 2004, "input service ” means any service used by a provider of output service for providing an output service (emphasis supplied). Rule 2(1) reads thus:

7.

[(l) "input service ” means any service, -used by a provider of output service for providins an output service; or(0

Page 6 of21

: :

F.No. STC/4-07/SRPL/0&A/19-20.■ ■*

wi'eflf 6y a manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products up to the place of removal,]

(ii)

As amply discussed hereinabove, the said assessee is not an Output Service Provider in respect of the units which have not been booked/ sold, on the date the completion certificate/B.U. permission is received. Resultantly, the portion of services utilized for construction of such units would not qualify as ‘input service’ in as much as such portions of services have not been utilized for providing an output service. Therefore, the said assessee is not eligible to take Cenvat credit of such portion of input services, utilized in an activity which does not constitute ‘service’.

7.1

Further, as per Rule 2(p) of Cenvat Credit Rules, 2004, “output service” means any service provided by a provider of service located in the taxable territory but shall not include a service,-

12

specified in section 66D of the Finance Act; orwhere the whole of service tax is liable to be paid by the recipient of service;

0)(2)

In view of the above definition, it appears that activity of transfer of title of immovable property i.e. unsold flats by way of sale, after the date of B.U. in respect of which the entire consideration has been received by the said service provider, cannot be termed as ‘output service’. However, the said service provider has availed Cenvat credit of input services in respect of these 1145346 square feet area (as on the dates of B.U./issuance of completion certificates) also.

The Cenvat credit scheme has been introduced with a view to avoid the cascading effect of taxes. The question of cascading effect would not arise in respect of the activity on which no Service Tax is payable. Consequently, the Cenvat credit would not be admissible in respect of such activities which are not chargeable to Service Tax. This analogy is amply specified in the legal statuette by virtue of Rule 6(1) of the Cenvat Credit Rules, 2004 which read as under at the material time:

8.

“The CENVAT credit shall not be alloM’ed on such quantity of input used in or in relation to the manufacture of exempted goods or for provision of exempted services, or input service used in or in relation to the manufacture of exempted goods and their clearance up to the place of removal or for provision of exempted services except in the circumstances mentioned in subrule (2)"

The above rule also clarifies the intention of the law-makers to the effect that the assessee is not to be benefitted by Cenvat credit of inputs/input services used in the activity exempted from tax. It is pertinent to note that the provisions of Rule 6 of the Cenvat Credit Rules, 2004 are not applicable to the facts of the instant case since the said Rule deals only with the limited circumstances wherein an assessee is provider of both taxable and exempted output services. However, in the instant case, the said assessee is provider of taxable services in respect of only those booked on full or partial payment which is received prior to obtaining Completion Certificate. The sale of units with full/partial consideration after ‘Completion Certificate’ is received does not constitute ‘service’ at all. Such an activity is entirely out of the scope of ‘service’ in terms of the definition provided at Section 66B (44). Therefore, the Cenvat Credit in respect of such non-taxable activity not constituting ‘service’ is not admissible in terms of Rule 3(1) itself. The text of Rule 6 has been discussed only for the purpose of arriving at the intention of the legislature to the effect that the Cenvat credit would not be admissible in respect of such activities which are not chargeable to Service Tax.

9.

Further Section 66B of the Finance Act provides as under:

“SECTION [66B.Charge of service tax on and after Finance Act, 2012.—There shall be levied a tax (hereinafter referred to as the service tax) at the rate of [fourteen per cent.] on the value of all services, other than those services specified in the negative list, provided or agreed to be provided in the taxable territory by one person to another and collected in such manner as may be prescribed. 1

From the foregoing, it is explicit that Service Tax is levied only on the value of the services provided or agreed to be provided by one person to another and conversely no Service

9.1

9.2

Page 7 of 21

F_NOi STC/4-07/SRPL/O&A719-20

Tax is levied when no service is provided (emphasis supplied'), as in the case where fhe units are sold after obtaining requisite permission from the competent authority.

However, in the instant case, builder/developer has taken Cenvat Credit ift respect of services received for the construction of the entire building/complex and the unit-wise segregation of such input services is not possible. Therefore, it is not possible to segregate the Cenvat Credit for each unit since the services of construction, security, etc. are utilized for the entire project. In such circumstances, the best recourse to determine such ineligible Cenvat Credit on a composite project would be to ascertain it on proportionate basis, either based on the number of units, if all the units are of equal, dimension or on the basis of constructed area if the units are having different dimensions or on the basis of value of sold before/after B.U. is received, as applicable.

10.

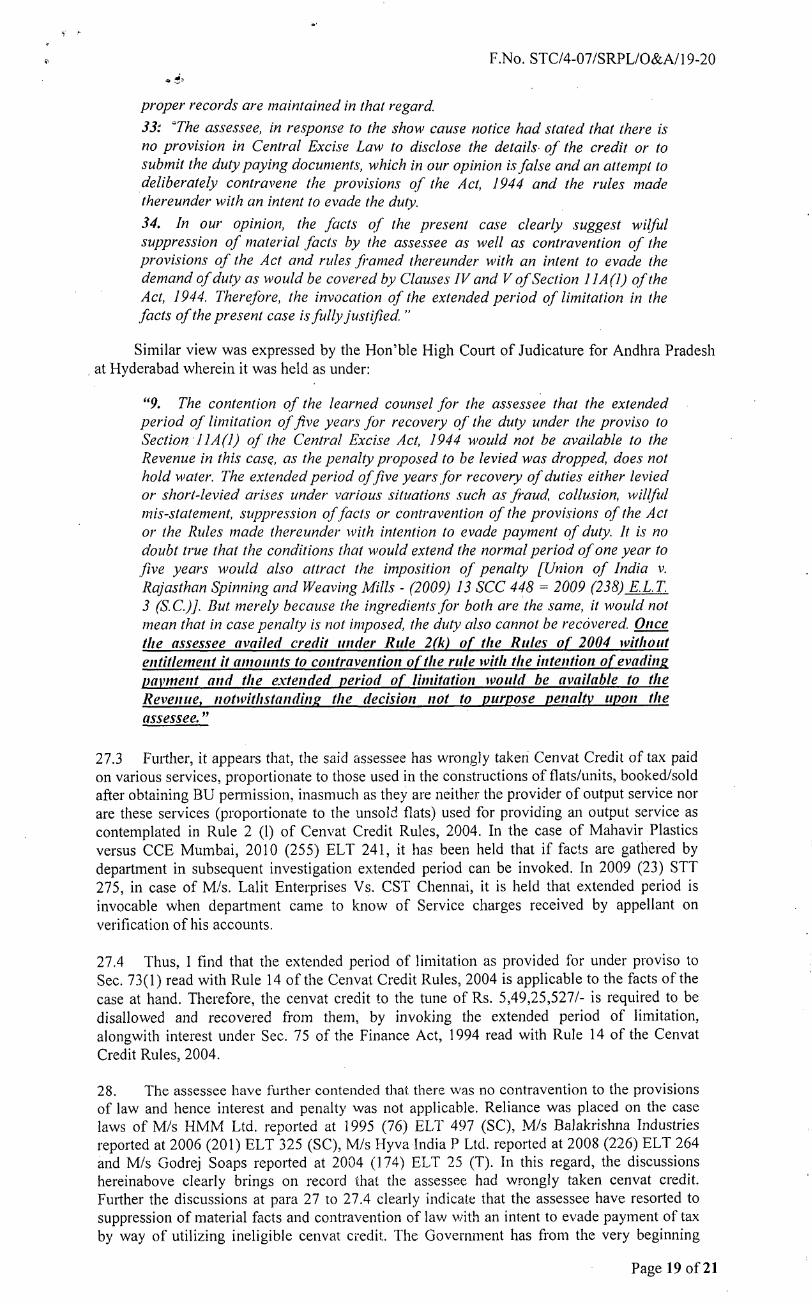

In view of the above discussion, it appears that the builder/developer including the assessee in this case, was eligible to take proportionate credit only for the units booked on payment of consideration, either based on the total area of construction or number of units (if all the units are of equal dimensions) or based on value of units sold before/after B.U. In such a scenario, neither undue credit would be availed nor there would be any requirement of recovery of excess credit availed. This will also not entail any financial burden on the builders as they will avail the proportionate credit at the time of booking the units and the Service Tax will also be paid thereafter on receipt of payment/ advance including Service Tax from the service recipient. On an illustration basis, taking into consideration basis of the total area of construction or number of units, let us assume that a builder proposes to construct 1000 sq. mts. of residential complex and commences construction by utilizing various services. Assuming that 200 sq. mts. are booked/sold on part/full payment during the first month of the commencement, the builder can avail 20% of the Service Tax paid on the various services utilized and also can utilize the said credit for payment of Service Tax on the amount so received for booking/sale. This is so because the builder is an Output Service Provider only in respect of 20% of the construction which has been booked/sold. As and when further booking/sale is made the builder can take the subsequent credit proportionately, including the units previously booked. This is coherently explained hereunder:

10.1

Credit entitled (for the area booked proportionate to total area proposed to

Total area to beconstructed (sq. mts.)

Total % of areabooked to the total areaproposed to beconstructed

Total Credit availed at the end of

Month of Commen- cenment of Construction

Service Taxpaid onservicesutilizedduringconstruction

Areabooked(sq.mts.)

themonth(Rs.)

beconstructed)

(f)(b) (d)(a) (c) (e) M1000 100 20Apr-15 200 10 20

0May-15 400 10 40 60200Jun-15 500 30 270 330

Jul-15 0 210700 30 540Aug-15 800 100 40 500 1040Sep-15 100 10101500 50 2050

20504100

10.2 From the above table, it is seen that in the first month of commencement of construction only 10% of the proposed area to be constructed (1000 sq. mts.) is booked on full/partial payment and therefore service is said to be provided in respect of only 10% of the proposed construction. Though Service Tax paid on the services utilized for construction during the month is Rs.200/- the builder would be entitled to take credit only to the extent of 10% of the Service Tax paid on the input services, i.e. Rs.20/-. In the subsequent month though there is no further booking, Service Tax paid on the services utilized in the month is Rs.400/-. As the services used in the second month are also used for the construction of the 10% of the area booked in the previous month, the builder would be entitled to take credit of 10% of the Service Tax of Rs.400/- paid in the second month, i.e. Rs.40/-. Thus at the end of second month the builder will

Page 8 of21

y 1 f M 4* J*

F.No. STC/4-07/SRPL/O&A/19-20it

have availed Cenvat credit to the tune of Rs.60/-, i.e. 10% of the total Service Tax paid (Rs.600/- ) till the^end of the month, as service is said to be provided only in respect of 10% of the proposed construction. Further in the third month of construction, assuming another 200 sq. mts. are booked, service is now said to be provided in respect of 30% of the proposed construction area. Assuming the builder has paid Service Tax of Rs.500/- on the-input services used in the third month, the builder will be entitled to take Cenvat credit of Rs.270/- i.e. @ 30% of the Service Tax paid in all the three months (Rs.500/- + Rs.400/- + Rs.200/-), i.e. Rs.330/- less Rs.60/- Cenvat credit already availed till the end of the second month and therefore by the end of the third month he will have availed Cenvat credit equivalent to Rs.330/- i.e. 30% of the Service Tax paid (Rs.l 100/-) on the services utilized so far. Accordingly, by the end of the sixth month the builder will be entitled to avail 50% of the Cenvat credit (Rs.2050/-) of the Service Tax paid (Rs.4100/-) on the input services utilized, as by the time 50% of the total proposed construction area is booked on payment of full/partial amount and in which case the service is said to be provided. This should be the scheme of the things, till the time the completion/B.U. certificate is obtained, instead of the builder availing the entire credit of the Service Tax paid on the services utilized, as once the completion/B.U. certificate is received there is no element of service on the flats/ booked/sold post receipt of the said certificate. The same analogy will be applicable if eligibility of Cenvat credit is decided on the basis of value of output services provided by the said assessee.

10.3 Details of units/area sold before B.U. permission of schemes namely Sumel-6 and Mondeal Height along with statement showing availment of Cenvat for the scheme were made available by the said assessee during the course of audit. On the basis of financial records and details regarding number and area of units constructed, sold before B.U. permission and remained unsold as on the date of respective B.U. permissions made available by the said assessee during the course of audit, Annexure-II has been prepared showing calculation of ineligible Cenvat credit of Rs.5,49,25,527/- which is attached along with this SCN. As evident from Annexure-II attached with this SCN, BU permissions were given for their scheme ‘Sumel- 6’ on 18.09.2014 and 24.12.2014 for Block No. “A to J” and in respect of Scheme ‘Mondeal Heights’ on 29.03.2016 for Block “A and B” by the competent authority. There has been total built-up area of 2138643 Square feet out of which area of 1145346 Square foot was unsold at the time respective BU permissions were received. Out of total Cenvat credit taken amount to Rs.9,32,95,682/- by the assesse during the period October-2013 to March-2016, proportionate Cenvat Credit to the extent of Rs.5,49,25,527/-, as worked out in Annexure-II referred above, availed and utilized for the part of the construction in which no element of service was involved, is not admissible as discussed supra.

Without prejudice to the above, even if the said assessee had taken Cenvat Credit in respect of all the services utilized for construction of project/building, the said assessee should have paid back the ineligible Cenvat Credit with interest at the time, the ‘Completion Certificate’ is obtained. At least at the time of obtaining “Completion Certificate”, the assessee was aware that they had taken ineligible Cenvat Credit in respect of units, the sale of which would not constitute a service. Therefore, at least at the time the “Completion Certificate” was obtained, the assessee ought to have paid the excess amount of Cenvat Credit availed on the units, the sale of which did not constitute service. Even the said fact of obtaining ‘Completion Certificate’, by virtue of which the need to pay back ineligible Cenvat credit arose, was never disclosed to the Department. The assessee had suppressed these facts from the Department to illegally avail the Cenvat Credit which was ineligible by the virtue of Rule 3 (1) of the Cenvat Credit Rules, 2004.

Whereas, it appears that in the instant case, the said assessee has taken and utilized the CENVAT Credit of the services used for the construction of entire project i.e. for the units booked/sold prior to obtaining the B.U. permission on which Service Tax was paid, as well as on the booked/sold after obtaining the B.U. permission and on which, no Service Tax was paid and in fact, in which case no services were provided by the assessee. However, no Cenvat credit is admissible for the sales made after obtaining the B.U. permission /completion certificates as no output service is provided in such cases and the services utilized for the construction of the unsold at the time B.U. permission is obtained, proportionate to the total area constructed or total sale value arrived, if possible, cannot be termed as input service and hence such portion of Cenvat credit availed and utilized for construction of units sold after obtaining B.U. permission is not admissible under Rule 3(1) read with Rule 2(1) of the Cenvat Credit Rules, 2004. Therefore, the service provider is required to reverse the excess Cenvat credit taken in respect of units lying unsold on dates of B.U. Permissions.

11.

12.

Page 9 of21

F.No. STC/4-07/SRPL/O&A/19-20

■' -Therefore, such Cenvat credit amounting to Rs.5,49,25,527/- availed by the assessee is

found to be availed in contraventions of Rule 3(1) read with Rule 2(1) of the Cenvat Credit Rules, 2004 with intent to evade the payment of Service Tax, as the said wrong and inadmissible Cenvat credit has been used for payment of Service Tax.

13.

Further, Rule 9(6) of the Cenvat Credit Rules, 2004 stipulates that the burden of proof regarding the admissibility of Cenvat credit on input services shall lie upon the manufacturer or provider of output services, taking such credit. In this era of self-assessment, the onus of taking legitimate Cenvat credit has been passed on the assessee in terms of the said Rule. In other words, it is the responsibility of the assessee to take Cenvat credit only if the same is legally admissible. Therefore, it appears that there is intention to evade payment of Service Tax and they contravened the provisions of Rule 3(1) read with 2(1) of the Cenvat Credit Rules, 2004 and therefore, the wrongly availed and utilized input Service Tax credit of Rs.5,49,25,527/- is liable to be recovered by invoking extended period of five years under proviso to Section 73(1) of the Finance Act, 1994, read with Rule 14(l)(ii) of the Cenvat Credit Rules, 2004. Applicable interest is also to be demanded and recovered from them in terms of Section 75 of the Act ibid read with Rule 14(l)(ii) of the Cenvat Credit Rules, 2004.

14.

The Government has from the very beginning placed full trust on the manufacturers/ service providers and accordingly measures like Self-assessments etc., based on mutual trust and confidence are in place. Further, a manufacturer/service provider is not required to maintain any statutory or separate records under the provisions of the Finance Act and Rules made there under, as considerable amount of trust is placed on them and private records maintained by them, for normal business purposes are accepted, practically for all the purposes. All these operate on the basis of honesty of the assessee; therefore, the governing statutory provisions create an absolute liability when any provision is contravened or there is a breach of trust placed on them. From the evidences, it appears that the said assessee has knowingly availed ineligible Cenvat Credit with intent to evade payment of Service Tax. The deliberate non-payment of duty/ tax and/or availing of ineligible Cenvat Credit and suppression of value of taxable services provided/received is in utter disregard to the requirements of law and breach of trust deposed on them and is certainly not in tune with government’s efforts in the direction to create a voluntary tax compliance regime.

15.

Further, it appears that, the assessee has wrongly taken Cenvat credit of tax paid on various services, proportionate to those used in the constructions of units, booked/sold after obtaining BU permission, in as much as they are neither the provider of output service nor are these services (proportionate to the unsold units) used for providing an output service as contemplated in Rule 2 (I) of Cenvat Credit Rules, 2004. The provisions of the Cenvat Credit Rules, 2004 are explicit in as much as they clearly lay down the provisions for eligibility/ineligibility for availing credit of duty paid on goods & capital goods as well as Service Tax paid on services. What construes “Capital Goods”, “Inputs” & “Input Services” is well defined under the Rules. Therefore, there cannot be any ambiguity regarding the eligibility for availing Cenvat Credit and the assessee could not have bred any doubt as regards the same. However, the assessee in sheer disregard to the provisions of law availed and utilized ineligible Cenvat credit and thereby, they contravened the provisions of Rule 3(1) of the Cenvat Credit Rules, 2004, read with Rule 2(1) of the Cenvat credit Rules, 2004. Further, it appears that, the event of obtaining of B.U. was never disclosed to the Department and consequent reflecting of the non-taxable value in the ST-3 returns was never brought to the notice of the Department by the assessee. Thus, it appears that the assessee has suppressed the said facts with intent to evade payment of tax by utilizing such inadmissible Cenvat credit. Moreover, in the present regime of liberalization, self-assessment and filing of ST-3 returns online, no documents whatsoever are submitted by the assessee to the department and therefore the department would come to know about such wrong availing of Cenvat credit only during audit or preventive/other checks. Therefore, the Government in its wisdom has incorporated the provisions of Sub Rule 5 & 6 of Rule 9 of the Cenvat Credit Rules, 2004 to cast upon the burden of proof of admissibility of Cenvat credit on the manufacturer or output service provider taking such credit. As the wrong and inadmissible credit taken is in contravention of the provisions of the Cenvat Credit Rules, 2004 by resorting to suppression & misrepresentation, the same is required to be recovered under the proviso to Section 73(1) of the Finance Act, 1944 read with Rule 14(l)(ii) of Cenvat Credit Rules, 2004, by invoking extended period. In the case of Mahavir Plastics versus CCE Mumbai, 2010 (255) ELT 241, it has been held that if facts are gathered by department in subsequent

16.

Page 10 of 21

- • •

F.No. STC/4-07/SRPL/O&A/19-20.i •

investigation, extended period can be invoked. In 2009 (23) STT 275, in case of Lalit Enterprises Vs. CST Chbnnai, it is held that extended period is evocable when department came to know of Service charges received by appellant on verification of his accounts. Interest at the appropriate rate is also required to be recovered from them tinder the provisions of Section 75 of the Finance Act, 1994 read with Rule 14(l)(ii) of the' rules ibid.. All the -above-mentioned acts of contravention of the provisions of the Finance Act and Rules framed there under on the part of the assessee have been committed with intent to evade payment of duty and thereby they have rendered themselves liable for penalty under Section 78(1) of the Finance Act, 1944 read with Rule 15(3) of the Cenvat Credit Rules, 1994.

Pre-Show Cause Notice consultation for Litigation Management and Dispute Resolution, in terms of instructions issued from File No.l080/09/DLA/Misc/2015 dated 21-12-2015 was granted to the said assessee on 9.4.2019 before the Commissioner, Central Tax Audit, Ahmedabad. The assessee under their E-mail communication have informed that they do not want pre-show cause consultation.

17

The said assessee was earlier registered under the Jurisdiction of the Commissioner of Service Tax, Ahmedabad. Consequent to the issue of the Notification No. 12/2017-Central Excise (NT) to 14/2017-Central Excise (NT) all dated 09.06.2017, appointing the officers of various ranks as Central Excise officers & reallocating the jurisdiction of the Central Excise Officers and Trade Notice No. 001/2017 dated 16.06.2017 issued by the Chief Commissioner, Central Excise & Service Tax, Ahmedabad Zone, the said assessee is now registered under the Jurisdiction of the Commissioner, Central Goods and Service Tax, Ahmedabad South.

18.

The provisions of the repealed Central Excise Act, 1944, the Central Excise Tariff Act, 1985 and amendment of the Finance Act, 1994 have been saved vide Section 174(2) of the COST Act, 2017 and therefore the provisions of the said repealed/amended Acts and Rules made there under are enforced for the purpose of demand of duty, interest, etc. and imposition of penalty under this notice.

19.

In view of the above facts, the assessee were called upon to show cause as to why:-20.

(i) Wrongly taken and utilized Cenvat credit of Rs.5,49,25,527/- (Rupees Five Crore Forty- nine Lakh Twenty-five Thousand Five Hundred and Twenty-seven only) as detailed in Annexure-II to the Show Cause Notice should not be disallowed and recovered from the said assessee, under the proviso to Section 73(1) of the Finance Act, 1994 read with Rule 14(l)(ii) of the Cenvat Credit Rules,2004;

(ii) Interest should not be charged and recovered on the demand at (i) above under Section 75 of the Finance Act, 1994 read with Rule 14(l)(ii) of the Cenvat Credit Rules, 2004; and

(iii) Penalty should not be imposed upon them on demand mentioned at (i) above under the provisions of Section 78(1) of the Finance Act, 1994 read with Rule 15(3) of the Cenvat Credit Rules, 2004.

Assessee’s written submission

The assessee filed their written submissions under their letter dated 3.3.2020 wherein they submitted that:21.

> At the time of taking the disputed input services, they were rendering taxable output services and they had correctly taken cenvat credit on the disputed input services

> They had complied with the provisions of Rule 4(7) of the Cenvat Credit Rules, 2004 and the said rule does not contain any provision for reversal of cenvat credit on account of units remaining unsold at the time of BU permission

> By virtue of insertion of Explanation 3 to Rule 6(1) vide Notn. No. 13/2016-CE(NT), the restriction on availment of cenvat credit is only in respect of the service tax paid during the tax period in which the said exempted service is provided.

Page II of 21

- F.No. STC/4-07/SRPL/O&A/19-20

They had not claimed any cenvat credit after the BU permission and had complied with all the conditions enumerated under Rule 4 & 6 of the Cenvat Credit Rules, 2004

>

■3 *

Rule 6(3) read with Rule 6(3A) deals with a requirement of reversal of cenvat credit in a situation where the output service provider provides exempted and non-exempted During the construction period of the relevant projects, they were providing only taxable services and therefore reversal under Rule 6(3) was not applicable

>services.

> The provision of Rule 11 of the Cenvat Credit Rules, 2004 is applicable only to inputs and not input services

> Tax cannot be levied merely by inferences or presumptions. Reliance was placed on the case of M/s Mathuram Agrawal reported at (1999) 8 SCC 667

> Credit availed during the period when the finished goods manufactured are dutiable is not liable to be reversed in future when such goods become non-dutiable. Reliance was placed on the case laws of M/s HMT reported at 2008 (232) ELT 217 (T), M/s HMT (TD) Ltd. reported at 2015 (322) ELT 342 (P&H), M/s TAPE Ltd reported at 2011 (268) ELT 49 (Kar), M/s TAPE Ltd. reported at 2015 (320) ELT A 185 (SC), M/s TAPE Ltd. reported at 2015 (322) ELT 864 (Kar), M/s PSL Corrosion Control Services Ltd. reported at 2016 (339) ELT 406 (Guj) & 2016 (339) ELT A208 (SC), M/s Ashok Iron & Steel Fabricators reported at 2002 (140) ELT 277 (T) and M/s Dai Ichi Karkaria Ltd. reported at 1999 (112) ELT 353 (SC)

They were eligible to the cenvat credit as held by the Tribunal in the case of M/s Alembic Ltd. reported at 2019 (28) GSTL 71 (T) which was upheld by the High Court of Gujarat as reported at 2019 (29) GSTL 625 (Guj)

>

The input services in the respective projects were availed for a period prior to the date of BU permission

>

The eligibility of credit has to be examined only at the time of receipt of input service.>

That the department had conducted an audit for the period from April 13 to March 15 for which FAR No. 696/15-16 dated 16.6.2016 had been issued wherein no objection in this regard was raised and thus extended period was not applicable. Reliance was placed on the case law of M/s Sunil Forging & Steel Ind. reported at 2016 (332) ELT 341 (T)

>

The extended period of limitation was not applicable in light of the case laws of M/s Mafatlal Industries Ltd. reported at 2009 (245) ELT 265 (T), M/s Pahwa Chemicals P Ltd. reported at 2005 (189) ELT 257 (SC), M/s Meghmani Dyes & Intermediate Ltd. reported at 2013 (288) ELT 514 (Guj) and M/s Anand NishiKawa Co. Ltd. reported at 2005 (188) ELT 149 (SC)

>

There was no contravention to the provisions of law and hence interest and penalty was not applicable. Reliance was placed on the case laws of M/s HMM Ltd. reported at 1995 (76) ELT 497 (SC), M/s Balakrishna Industries reported at 2006 (201) ELT 325 (SC), M/s Hyva India P Ltd. reported at 2008 (226) ELT 264 and M/s Godrej Soaps reported at 2004 (174) ELT 25 (T)

>

Record of personal hearing

Virtual hearing in the matter was held on 5.10.2020 wherein Shri Arjun Akruwala, C.A. appeared on behalf of the assessee and he reiterated the contentions in their written submissions dated 3.3.2020. He further stated that if at all any credit was to be reversed the same would apply to the period only after receipt of BU permission and the credit taken before BU permission would be admissible. He placed reliance on the case of M/s Alembic Ltd. reported at 2019 (28) GSTL 21 (T).

22.

Discussion and finding

I have carefully gone through the SCN, relevant case records and the assessee’s submissions both, in written and in person.23.

Page 12 of 21

•«**F.No. STC/4-07/SRPL/O&A/19-20

The short point of examination is whether the assessee is eligible to cenvat credit of input services used in construction of units in the complex which were not booked till the time of obtaining BU permission and were sold after receipt of the BU permission. The answer to the same would lie in the analysis of the conditions of eligibility of the cenvat credit.

24.

24.1 The initial step in the chronological manner while examining the eligibility criteria of the cenvat credit is to ascertain whether the person claiming such credit qualifies for taking cenvat credit or otherwise. The persons who are eligible to claim cenvat credit have been spelt out under Rule 3(1) of the Cenvat Credit Rules, 2004 and the relevant text of the same is reproduced under:

RULE 3. CENVAT credit.—(1) A manufacturer or producer offinal products or a provider of output service shall be allowed to take credit (hereinafter referred to as the CENVAT credit) of the duties, taxes, cess specified in the said rule paid on -

any input or capital goods received in the factory of manufacture of final product or [by] the provider of output service on or after the 10th day of September, 2004; and

any input service received by. the manufacturer of final product or by theprovider of output services on or after the 10th day of September, 2004

0)

(U)

The above statute clearly specifies that two classes of persons are entitled to Cenvat credit and those persons have been specified as (i) Manufacturer or Producer of Final Products and (ii) Output service provider. In the instant case, it is not the case of the assessee that they are manufacturers or producers of final products and as such they are ruled out of the first class of qualifying persons. Thus, it remains to be examined whether the as.sessee qualifies under the second class i.e. Provider of Output Service of persons.

The term ‘Provider of Output services’ has not been defined in either the Cenvat Credit24.2Rules, 2004 or Chapter V of the Finance Act, 1994 and the rules made thereunder. Thus, the meaning of the said term has to be construed as per the general laws of linguistic construction: This can be done by vivisecting the said term in two parts viz. ‘Provider of and ‘Output services’. The term ‘output services’ has been defined at Rule 2(p) of the Cenvat Credit Rules, 2004 as under:

“output service ” means any service provided by a provider of service located in the taxable territory but shall not include a service, -

specified in section 66D of the Finance Act; orwhere the whole of service tax is liable to be paid by the recipient of

(1)(2)service

The term ‘service’ has been defined at Sec. 65B(44) of the Finance Act, 1994 as under:

“service” means any activity carried out by a person for another for consideration, and includes a declared service

The term ‘provider of is to be read in terms of the linguistic construction. The word ‘provider’ is a noun for which the corresponding verb is ‘provide’. The dictionary meaning of the word ‘provide’ is to give someone something that they need. Thus the term ‘provider’ would mean a person who gives something to someone.

Conjoint reading of the above legal and linguistic terminology indicates that ‘Provider of24.3Output service’ would mean a person who carries out an activity for someone at his behest. The .inference that can be drawn from the same is that there must essentially be a recipient for the existence of a provider. In other words there can be no ‘provider’ in absence of a ‘recipient’. This inference is drawn from the principles of linguistic construction. The same meaning and essence is also present in the legal term ‘service’ which has been defined as ‘an activity carried out by a person for another’. The term ‘service’ and ‘declared service’ has been defined at Sec. 65B(44) & 65B(22) of the Finance Act, 1994 respectively as under:

“service” means any activity carried out by a person for another for consideration, and includes a declared service

Page 13 of 21

t ■ F.No. STC/4-07/SRPL/Oc&A/19-20

“declared service ” means any activity carried out by a person for another verson for consideration and declared as such under section 66E Ss

The above legal definitions also indicate that for the fulfillment of the term ‘service’, the existence of two persons viz. one who is carrying out the activity and other for whom the activity is being carried out is essential. In other words the legal terminology also emphasizes on the existence of two entities i.e. 1) the provider and 2) the recipient. Therefore, for a person to be a provider of Output Service, the existence of a recipient of service is of utmost necessity and in absence of a recipient of service there can be no ‘provider of output service’. Accordingly, if the assessee is to be construed as ‘Provider of output service’, there ought to inevitably be a ‘recipient of service’. Thus, it needs to be examined whether there existed a ‘recipient of service’ in respect of the units sold after obtaining BU permission or otherwise.

24.4 The term ‘service’ as defined under Sec. 65B(44) of the Finance Act, 1994 includes declared services. The ‘declared services’ have been specified at Sec. 66E of the Finance Act, 1994 and the relevant text of the same is reproduced under:

The following shall constitute declared services, namely :—(a)(b) construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration is received after issuance of completion- certificate by the competent authority.Explanation. — For the purposes of this clause,—(J) the expression “competent authority ” means the Government or any authority authorised to issue completion certificate under any law for the time being in force and in case of non-requirement of such certificate from such authority, from any of the following, namely :—(A) architect registered with the Council of Architecture constituted under the Architects Act, 1972 (20 of 1972); or(B) chartered engineer registered with the Institution of Engineers (India); or(C) licensed surveyor of the respective local body of the city or town or village or development or planning authority;

In the instant case, it is an undisputed fact that the assessee is engaged in the activity of construction of a complex and is covered under the declared services as specified at Sec. 66E(b) of the Finance Act, 1994. The above indicates that the activity of construction of complex is not a service if the entire consideration is received after issuance of completion-certificate by the competent authority. Thus, in cases where the entire consideration for the unit has been received after BU permission, no service is rendered and as such there is no existence of ‘recipient of service’. The existence of ‘recipient of service’ comes into play only in the event that a part or whole of the consideration for a unit has been received before the issue of BU permission. This discussion clearly indicates that the following two classes of persons at the receiving end come into play in respect of acquiring a constructed unit in a complex:

Recipient of Service - In cases where a part or whole of the payment of the unit is made before issuance of BU permissionBuyer of Constructed Unit - In cases where the entire payment for the unit is made after issuance of BU permission.

0

ii)

24.5 The natural corollary to the above analysis when applied to the assessee infers that the assessee assumes a dual identity in respect of different units in a complex as under:

i. Provider of Output Service - In cases where a part or whole of the payment of the unit is made before issuance of BU permission

ii. Seller of Constructed Unit - In cases where the entire payment for the unit is made after issuance of BU permission.

Thus, the assessee does not qualify as a ‘Provider of Output Services’ in respect of units situated within a complex for which the entire consideration has been received after issuance of BU permission. Resultantly, the assessee does not qualify under the class of persons who are eligible for taking cenvat credit in respect of such units for which the entire consideration has been

Page 14 of 21

F.No. STC/4-07/SRPL/O&A/19-20«•

received after issuance of BU permission in terms of the provisions of Rule 3(1) of the Cenvat Credit Rules, 2004.

24.6 Further, the term ‘input service’ has been defined at Rule 2(1) of the Cenvat Credit Rules, 2004 as under:

(l) "input service ” means any service, -used by a provider of output service for providing an output service; or0)

used by a manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products up to the place of removal

(ii)

The above definition makes it clear that a service should be used by a ‘provider of output service’ to be covered under the ambit of ‘input service’. In light of the above discussion the assessee is not an Provider of Output services in cases where the entire consideration for the unit has been received after BU permission and resultantly, the services used for construction of only such units do not qualify as ‘input services’.

In view of the above position of law, I proceed to examine the contentions put forth by the assessee in this regard. It has been argued that at the time of taking the cenvat credit on input services they were rendering only taxable services. As amply discussed above, the assessee was not an Output service provider in respect of the units for which no consideration had been received prior to obtaining of BU permission (hereinafter referred to as ‘such units’). Thus, the assessee were not eligible for taking cenvat credit in respect of such units which were not booked since they did not qualify as a person eligible to take cenvat credit in terms of the provisions of Rule 3(1) of the Cenvat Credit Rules, 2004. Accordingly, the fact that the assessee were an Output service provider for a few of the units in the complex would not make them eligible to take the entire cenvat credit in respect of all the units.

25.

The assessee have submitted that Rule 4(7) of the Cenvat Credit Rules, 2004 does not25.1contain any provision for reversal of cenvat credit on account of units remaining unsold at the time of BU permission. The matter under consideration is not reversal of cenvat credit but is pertaining to admissibility of taking cenvat credit at material time. It is seen in light of the provisions of law that the assessee was not eligible for cenvat credit in respect of the services used for such units since they did not qualify as an Output Service Provider for such units. Thus, the cenvat credit proportionate to such units was not admissible and had been wrongly taken. The show cause notice does not seek for reversal of cenvat credit but rather seeks to recover thewrongly taken cenvat credit. Further it is to mention that Rule 4 deals with the conditions of taking cenvat credit and before travelling to the conditions, the assessee should first meet the tests under Rule 2(1) and Rule 3(1) of the Cenvat Credit Rules, 2004 to the effect that the activity should qualify as an ‘input service’ and the assessee should be either a ‘manufacturer’ or an ‘output service provider’ as amply discussed above. The instant case deals with a situation where the assessee is not an Provider of Output services in cases where the entire consideration for the unit has been received after BU permission and as a consequence the services used for construction of such units where do not qualify as ‘input services’. Thus, in the instant case the assessee does not fulfil the test under Rule 2(1) and Rule 3(1) of the Cenvat Credit Rules, 2004 since the services do not qualify as ‘input services’ and the assessee does not meet the criteria of being a Provider of Output Services. Accordingly, the question of proceeding to the further conditions laid down under Rule 4 of the Cenvat Credit Rules, 2004 does not arise. The cenvat credit in the instant case has been wrongly taken for the reasons elaborated above and as such I find that the arguments put forth by the assessee are out of context and are not sustainable.

The assessee has stated that restriction of taking cenvat credit is only in respect of the tax25.2period during which exempted service is provided as per Explanation 3 to Rule 6(1) inserted vide Notn. No. 13/2016-CE(NT). The argument is not acceptable in as much as the provisions of Rule 6(1) ibid do not come into play in a situation where the cenvat credit is debarred owing to the fact that the assessee is not an Output Service Provider in respect of such units. It has been further stated that they had not claimed any cenvat credit after the BU permission and had complied with all the conditions enumerated under Rule 4 & 6 of the Cenvat Credit Rules, 2004. It is reiterated that the conditions pertaining to eligibility of cenvat credit come into play only

Page 15 of 21

WWn*« F-No_ STC/4-07/SRPL/O&A/19-20

when the assessee is found to be covered under the class of persons eligible for cenvat credit. In the instant case, the assessee is not covered under the class of persons eligible for cenvat credit in respect of such units and as such traveling to the conditions of eligibility is ruled out. Further, it has been contended that during the construction period of the relevant projects,5they were providing only taxable services and therefore reversal under Rule 6(3) was not applicable. The argument of the assessee is totally misplaced in as much as the show cause notice does not charge violation of the provisions of Rule 6(3) of the Cenvat Credit Rules, 2004.

The assessee have stated that the provision of Rule 11 of the Cenvat Credit Rules, 2004 is applicable only to inputs and not input services. Here again it is to mention that the cenvat credit is not sought to be recovered by invoking the provisions of Rule 11 ibid but is sought to be recovered for the sole reason that the assessee was not covered under the ambit of Rule 3(1) of the Cenvat Credit Rules, 2004 in respect of such units. It has been argued that tax cannot be levied merely by inferences or presumptions by placing reliance on the case of M/s Mathuram Agrawal reported at (1999) 8 SCC 667. The instant case deals with a situation wherein the admissibility of cenvat credit is under examination and does not deal with levy of tax and as such the argument of the assessee is not maintainable as also the case law cited by them is not applicable to the facts of the case.

25.3

The assessee have contended that cenvat credit availed during the period when the25.4finished goods manufactured are dutiable is not liable to be reversed in future when such goods become non-dutiable by placing reliance the various case laws as mentioned at para 21 above. The case laws cover a situation where the cenvat credit was admissible to the manufacturer at thematerial time and subsequently the finished goods became non-dutiable. The present case does not deal with a situation where a service was subsequently made exempted but is a case where the cenvat credit is not admissible at the time of taking the credit on the ground that the assessee does not fall under the ambit of Rule 3(1) of the Cenvat Credit Rules, 2004 in respect of such units. In other words, the issue involved in the present case is that the cenvat credit was not admissible even at the time of taking such credit by the assessee whereas the case laws cited by the assessee cover an issue where the cenvat credit was admissible at the time of taking such credit. Thus, the facts of the case laws cited by the assessee are on a different footing and would not be applicable to the facts of the present case.

25.5 The assessee have the submitted that Hon’ble High court of Gujarat has recently passed a judgment in the case of The Principal Commissioner VERSUS M/s Alembic Limited 2019 (7) TMI 908-Gujarat High Court wherein the facts of which are identical to the notice case. In this regard I find that the factual matrix of the said case and the case at hand is entirely different. In the case of M/s Alembic, department was seeking payment of an amount in terms of the provisions of Rule 6(3) of the Cenvat Credit Rules, 2004 as is evident from the narration at para1.5 of Final Order No. A / 12229-12232 /2018 dated 23.10.2018 of the CESTAT of which the relevant text is reproduced under for ease of understanding:

the revenue authorities issued separate SCNs, demanding 6%/8%/10% amount of sale of immovable property after obtaining Completion certificate where no Service Tax was paid by the Appellant, on the ground that they had availed Cenvat Credit and provided taxable as well as exempt services (sale of immovableproperty), and they had not maintained separate accounts._________________Such demand were confirmed against the Appellants under Rule 6 of CCR, 04, vide the impugned orders passed by the Ld. Commissioner.

The above text clearly indicates that the department had sought to recover an amount of 6%/8%/10% of the value of unit sold after obtaining Completion certificate as provided for under Rule 6(3) of the Cenvat Credit Rules, 2004. Secondly, ground of raising the demand has been narrated that the appellants were engaged in providing taxable as well as exempt services and had not maintained separate records in respect of the cenvat credit taken. Thirdly, it is observed that the demand was confirmed by the department under Rule 6 of the Cenvat Credit Rules, 2004. A brief comparison of the facts under the case at hand reveals that the show cause notice does not dwell on the premises that the assessee was engaged in engaged in providing taxable as well as exempt services and had not maintained separate records in respect of the cenvat credit taken. The entire show cause notice nowhere states that the assessee had taken cenvat credit on common input services used for providing taxable as well as exempted services. The present show cause does not seek to demand an amount equivalent to 7% of the value of exempted

Page 16 of 21

F.No. STC/4-07/SRPL/O&A/19-20« A

services in terms of the provisions of Rule 6(3) of the Cenvat Credit Rules, 2004. There is no charge in the show cause notice to the effect that the assessee had violated the provisions of Rule 6 of the Cenvat Credit Rules, 2004. Contrary to the above, the present show cause notice deals with a situation where the assessee if found to be not qualifying as a person who is eligible to take cenvat credit in terms of the provisions of Rule 3(1) of the Cenvat Credit Rules, 2004 in respect of such units for which the entire consideration has been received after issuance of BU permission. It is in the backdrop of this finding that the show cause notice alleges that the assessee has wrongly taken cenvat credit in respect of the input services used for construction of those units for which the entire consideration has been received after issuance of BU permission. In other words, the present show cause notice alleges that the assessee does not qualify as a person who is eligible to take cenvat credit in terms of the provisions of Rule 3(1) of the Cenvat Credit Rules, 2004. In a nutshell, the present show cause notice alleges wrong taking of cenvat credit and seeks to disallow such wrongly taken cenvat credit for violation of Rule 3(1) of the Cenvat Credit Rules, 2004 whereas, the case of M/s Alembic Ltd. sought to recover an amount equivalent to percentage of value of the exempted services for violation of the provisions of Rule 6 of the Cenvat Credit Rules, 2004. The present show cause notice does not enter into the realm of Rule 6 of the Cenvat Credit Rules, 2004. Thus, I find that the matter under consideration in the case of M/s Alembic Ltd. is totally on a different ground than the facts of the case at hand and as such the ratio of the said case law is not applicable to the instant case. So the contention of the assessee is not tenable in this regard.

In the instant case, I find that the assessee is neither a manufacturer nor a Provider of Output Services in respect of the units for which the entire payment for the said unit has been received after issuance of BU permission. It may be appreciated that in the typical case of Construction service, service is said to be provided to each individual who books/purchases flats/units, on payment of part/full consideration and not in respect of the entire building constructed. In other words, the builder is agreeing to provide or provide services to multiple service recipients in respect of individual flat/unit of the same project. Till the time, an individual flat/unit is booked/sold, there is no element of service involved inasmuch as there is no service recipient and the natural corollary that follows is that no service is provided or agreed to be provided. This will be the case for each individual unit constructed. In other words, the developer/builder is deemed to be the provider of output service only in respect of those units which are booked/sold and for which part or whole payment is received prior to obtaining the ‘Completion Certificate’ from the competent authority. Consequentially, the developer/ builder would not be a Provider of Output services in respect of those units where the entire amount has been received after issuance of BU permission. In nutshell, till the time a flat/unit is booked on payment of part/full consideration, no service is provided or agreed to be provided. Thus, the said assessee cannot be said to be an Output Service Provider in respect of such units in as much as there is no service recipient for such units and resultantly no service is provided or agreed to be provided. Accordingly, the assessee does not qualify as a person who is entitled to take cenvat credit in respect of such units for which the entire consideration has been received after issuance of BU permission and as such they are not entitled to take cenvat credit of the input services used for construction of such units for which the entire consideration has been received after issuance of BU permission. Therefore, I find that the assessee have wrongly taken the cenvat credit on input services used for construction of units for which the entire consideration has been received after issuance of BU permission.

26.

It has been contended by the assessee that the department had conducted an audit for the period from April 13 to March 15 for which FAR No. 696/15-16 dated 16.6.2016 had been issued wherein no objection in this regard was raised and thus extended period was not applicable. The argument does not merit consideration since audit is conducted in select areas based on risk analysis. The theory of knowledge of the department does not hold true in case where the short-payment or non-payment of tax is owing to reasons of fraud, collusion or any wilful mis-statement or suppression of facts, or contravention of any of the provisions of the Act or of the rules made under it with intent to evade payment of tax. The said principle has been laid down by the Hon’ble Apex Court in the case of M/s Rajasthan Spinning & Weaving Mills as reported at 2009 (238) ELT 3 (SC) and the relevant text of the same is reproduced under:

From sub-section 1 read with its proviso it is clear that in case the short payment, non payment, erroneous refund of duty is unintended and not attributable to fraud, collusion or any wilful mis-statement or suppression of facts, or contravention of any of the provisions of the Act or of the rules made under it with

27.

Page 17 of 21

'* M ■ * ; F.No. STC/4-07/SRPL/O&A/19-20

intent to evade payment of duly then the Revenue can give notice for recovery of the duly to the person in default within one year from the relevant date (defined in sub-section 3). In other words, in the absence of any element of deception or malpractice the recovery of duty can only be for a period not exceeding one yiear. But in case the non-payment etc. of duty is intentional and by adopting any means as indicated in the proviso then the period of notice and a priory the period for which duty can be demanded gets extended to five years.

The above ratio has also been followed by the Hon’ble High Court of Gujarat in the case of M/s Neminath Fabrics P. Ltd. as reported at 2010 (256) ELT 369 (Guj). The case law of M/s Sunil Forging & Steel hid. reported at 2016 (332) ELT 341 (T), cited by the assessee, pertained to the issue of classification of goods. Under such circumstances it was observed that the aspect of classification and discharge of proper duty liability was covered under the scope of audit and as such the matter was held as time barred. In the instant case, the issue involved is the act of taking ineligible Cenvat credit by the assessee which has arisen out of the fact that the assessee had obtained BU Permission and resultantly the units sold after such BU Permission was sale of immovable property and not a service. Thus, the assessee was not entitled to Cenvat credit on such units which had been wrongly taken. So far as the verification of Cenvat credit is concerned, the scope of the audit is only on selective basis and 100% of the Cenvat credit verification is not covered under the scope of audit. Thus, the facts of the case law of M/s Sunil Forging & Steel Ind. supra are on a different footing and the ratio of the same would not be applicable to the facts of the present case.

The assessee have advanced pleas on limitation in light of the case laws of M/s Mafatlal Industries Ltd. reported at 2009 (245) ELT 265 (T), M/s Pahwa Chemicals P Ltd. reported at 2005 (189) ELT 257 (SC), M/s Meghmani Dyes & Intermediate Ltd. reported at 2013 (288) ELT 514 (Guj) and M/s Anand NishiKawa Co. Ltd. reported at 2005 (188) ELT 149 (SC). In this regard I find that Rule 9(6) of Cenvat Credit Rules, 2004 stipulates that the burden of proof regarding the admissibility of Cenvat Credit on input services shall lie upon the manufacturer or provider of output services, taking such credit. In this era of self-assessment, the onus of taking legitimate Cenvat Credit has been passed on the said assessee in terms of the said Rule. In other words, it is the responsibility of the said assessee to take Cenvat Credit only if the same is legally admissible. The provisions of the Cenvat Credit Rules, 2004 are explicit inasmuch as they clearly lay down the provisions for eligibility/ineligibility for availing credit of duty paid on goods and capital goods as well as Service Tax paid on services. What construes “Capital Goods”, “Inputs” and “Input Services” is well defined under the Rules. Therefore, there cannot be any ambiguity regarding the eligibility for availing Cenvat Credit and the said assessee could not have bred any doubt as regards the same. However, the said assessee in sheer disregard to the provisions of law availed and utilized ineligible Cenvat Credit and thereby they contravened the provisions of Rule 3(1) of the Cenvat Credit Rules, 2004 read with Rule 2(1) of the Cenvat Credit Rules, 2004 as discussed above. Further, it appears that the event of obtaining of B.U. was never disclosed to the Department and consequent reflecting of the non-taxable value in the ST-3 returns was never brought to the notice of the Department by the said assessee. Thus, I find that the said assessee has suppressed the said facts with intent to evade payment of tax by utilizing such inadmissible Cenvat Credit. The various case laws relied upon by the assessee do not come to their rescue, having different factual matrix.

27.1