fy21 unaudited results

TRANSCRIPT

FY21 Unaudited Results

Joe Fitzgerald, Acting Group Chief Financial Officer

7 July 2021

Executive Chairman Introduction

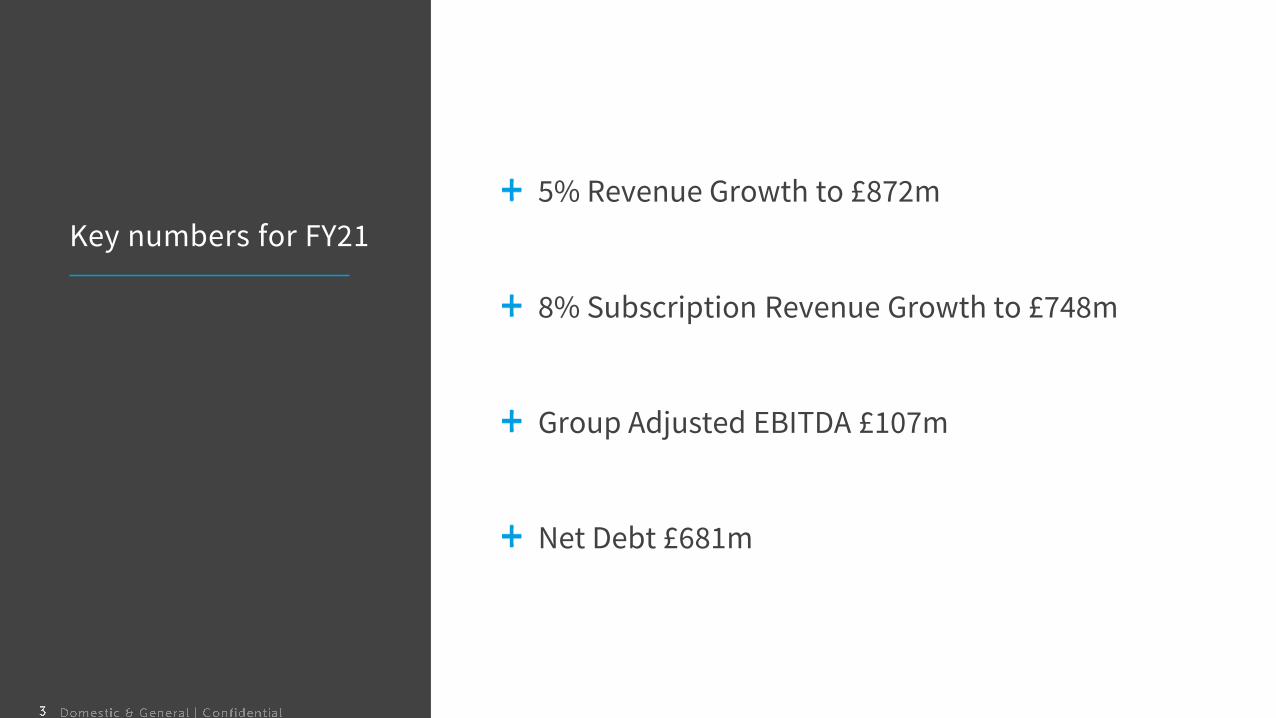

Key numbers for FY21

5% Revenue Growth to £872m

8% Subscription Revenue Growth to £748m

Group Adjusted EBITDA £107m

Net Debt £681m

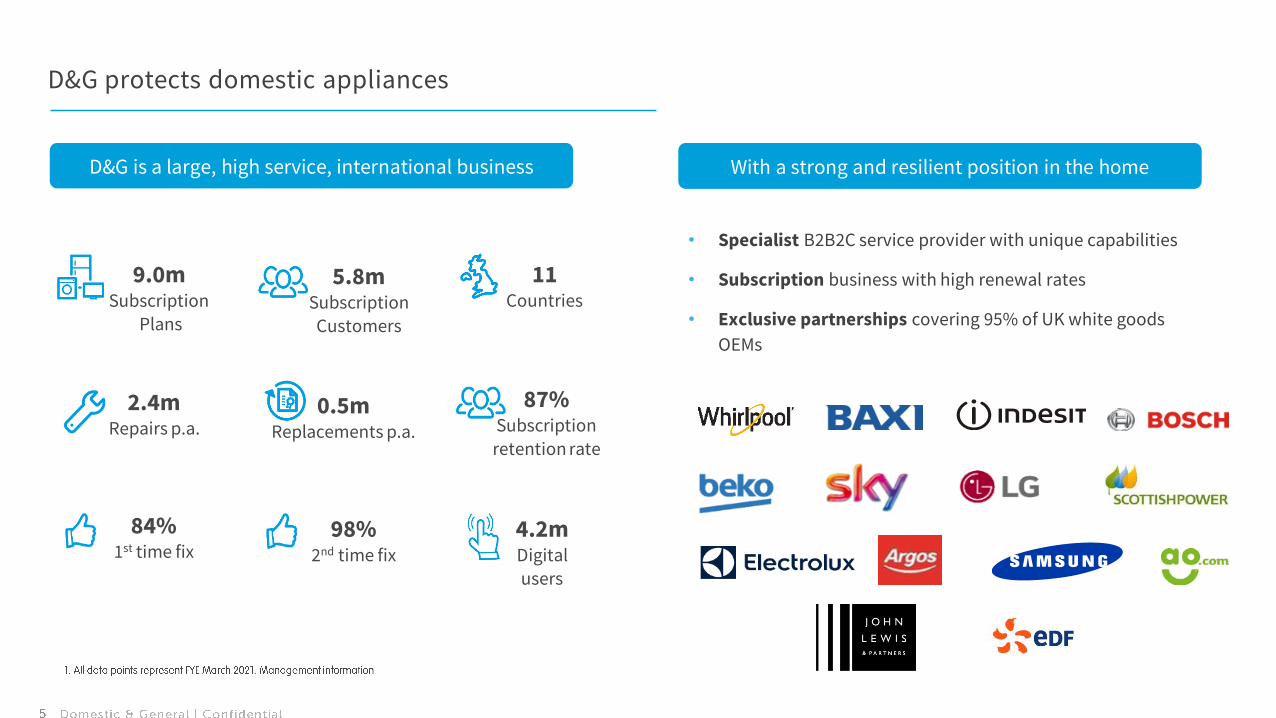

About D&G

• Specialist B2B2C service provider with unique capabilities

• Subscription business with high renewal rates

• Exclusive partnerships covering 95% of UK white goods

OEMs

D&G protects domestic appliances

D&G is a large, high service, international business With a strong and resilient position in the home

9.0mSubscription

Plans

5.8mSubscription

Customers

11Countries

0.5mReplacements p.a.

2.4mRepairs p.a.

98% 2nd time fix

4.2m Digital users

87% Subscription retention rate

84%1st time fix

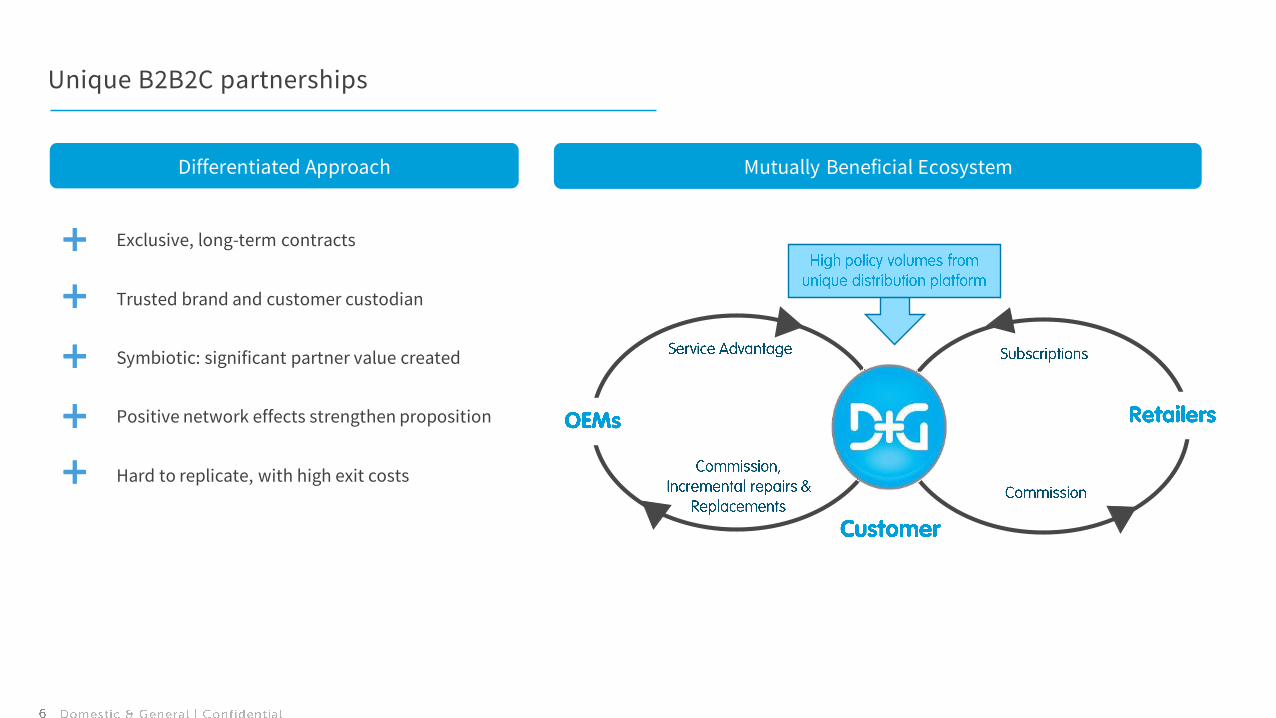

• Exclusive, long-term contracts

• Trusted brand and customer custodian

• Symbiotic: significant partner value created

• Positive network effects strengthen proposition

• Hard to replicate, with high exit costs

Unique B2B2C partnerships

Differentiated Approach Mutually Beneficial Ecosystem

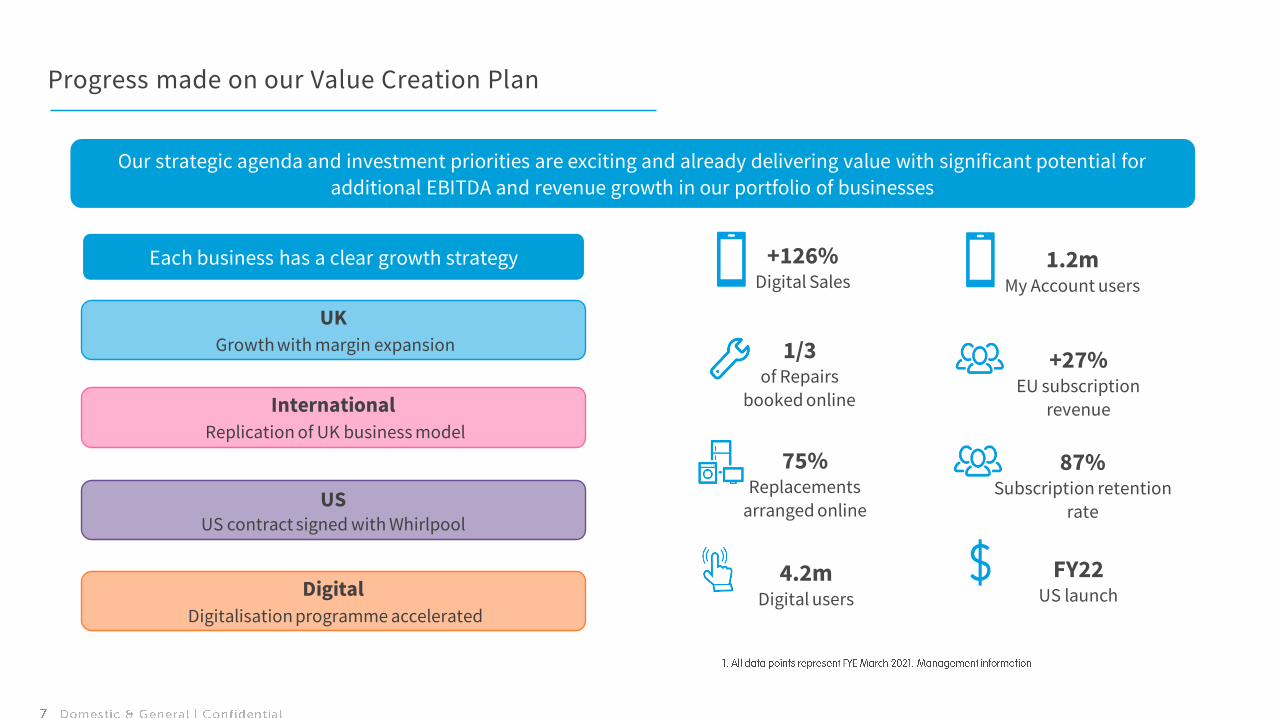

Progress made on our Value Creation Plan

Our strategic agenda and investment priorities are exciting and already delivering value with significant potential for

additional EBITDA and revenue growth in our portfolio of businesses

+126%Digital Sales

FY22US launch

1.2mMy Account users

+27%EU subscription

revenue

1/3of Repairs

booked online

4.2m Digital users

87% Subscription retention

rate

75%Replacements

arranged online

UKGrowth with margin expansion

InternationalReplication of UK business model

USUS contract signed with Whirlpool

DigitalDigitalisation programme accelerated

Each business has a clear growth strategy

FY21

Further growth and resilience

FY21 Key Messages

D&G continues to

demonstrate growth and

resilience

Double digit growth in FY21 new business subscription plan sales drives real medium-

term value

Strong retention rates driving growth in renewals & 8% subscription revenue growth

Group Adjusted EBITDA broadly flat year-on-year, despite the Covid pandemic and

investments made in the platform, with EBITDA up year-on-year after adjusting for one-

off Covid impacts on claim costs.

Digitalisation continues at pace with high advocacy

Homeworking a success for the Group and will form basis of new hybrid working model

US launch preparations remain on track – expected launch in early Autumn

Brexit transition & Part VII process completed

Continue to be well covered from an insurance capital perspective

£100m raised in July 2020 to fund investment in US & Digitalisation program

Brexit

We have safely transitioned the

business and have a platform

for growth

Part VII transfer from DGI to DGIEU successfully completed on 31 December 2020

Group capital coverage ratio and cash (distributable reserves) reduced by Part VII

transfer, reflecting investment to capitalise German regulated entity.

Strong capital coverage ratios in both DGI and DGIEU

Mitigated effects of “non-equivalence” on our solvency position

Platform to continue growth in our European territories

Covid

Strong and resilient

performance whilst delivering

excellent service

Our service model is industry leading - full service maintained throughout the

pandemic

Incurred costs to maintain service (supply chain issues)

Customer retention levels - strong throughout the year

Homeworking a great success and will form the basis of a hybrid working model in

future

Our business model allowed us to take advantage of the change in customer buying

habits and the move to online

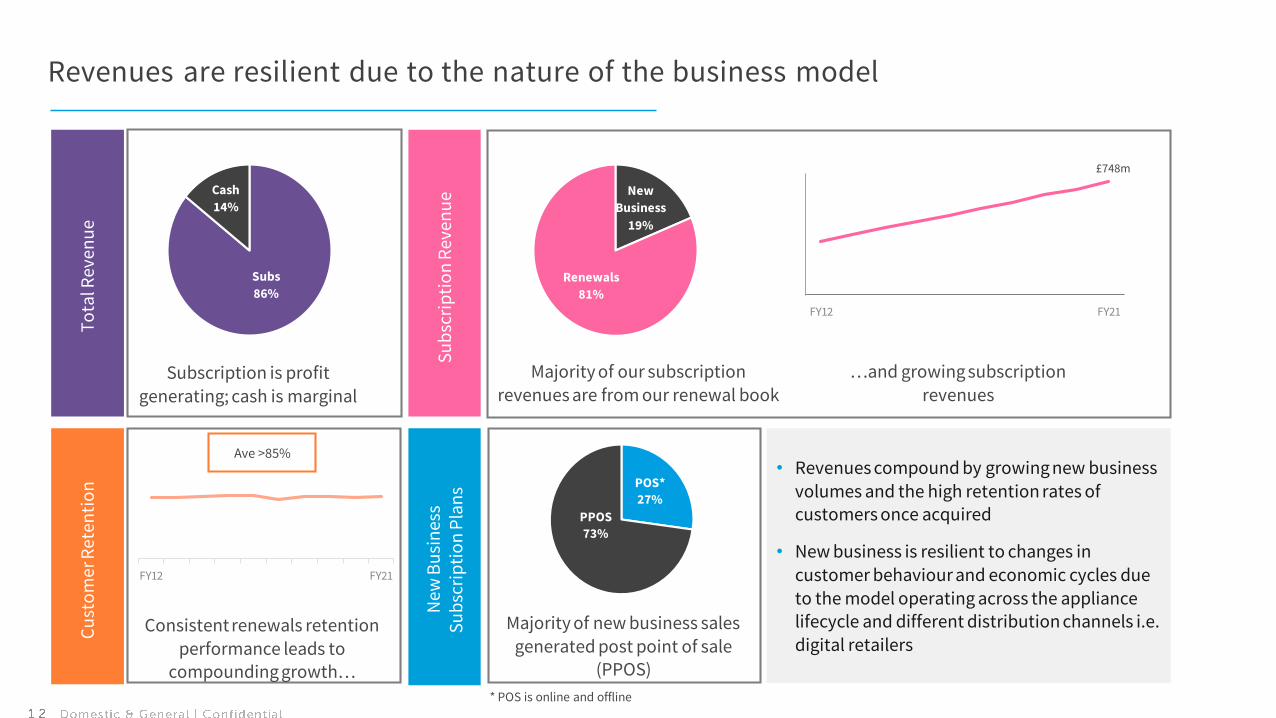

Revenues are resilient due to the nature of the business model

Su

bsc

rip

tio

n R

even

ue

Cu

sto

mer

Ret

enti

on

New

Bu

sin

ess

Su

bsc

rip

tio

n P

lan

s

Subscription is profit generating; cash is marginal

To

tal R

even

ue

New

Business

19%

Renewals

81%

• Revenues compound by growing new business volumes and the high retention rates of customers once acquired

• New business is resilient to changes in customer behaviour and economic cycles due to the model operating across the appliance lifecycle and different distribution channels i.e. digital retailers

Majority of our subscription revenues are from our renewal book

…and growing subscription revenues

Consistent renewals retention performance leads to

compounding growth…

Majority of new business sales

generated post point of sale (PPOS)

Ave >85%

Subs

86%

Cash

14%

FY12 FY21

FY12 FY21

PPOS

73%

POS*

27%

* POS is online and offline

£748m

Q1 Q2 Q3 Q4 FY

FY20 FY21

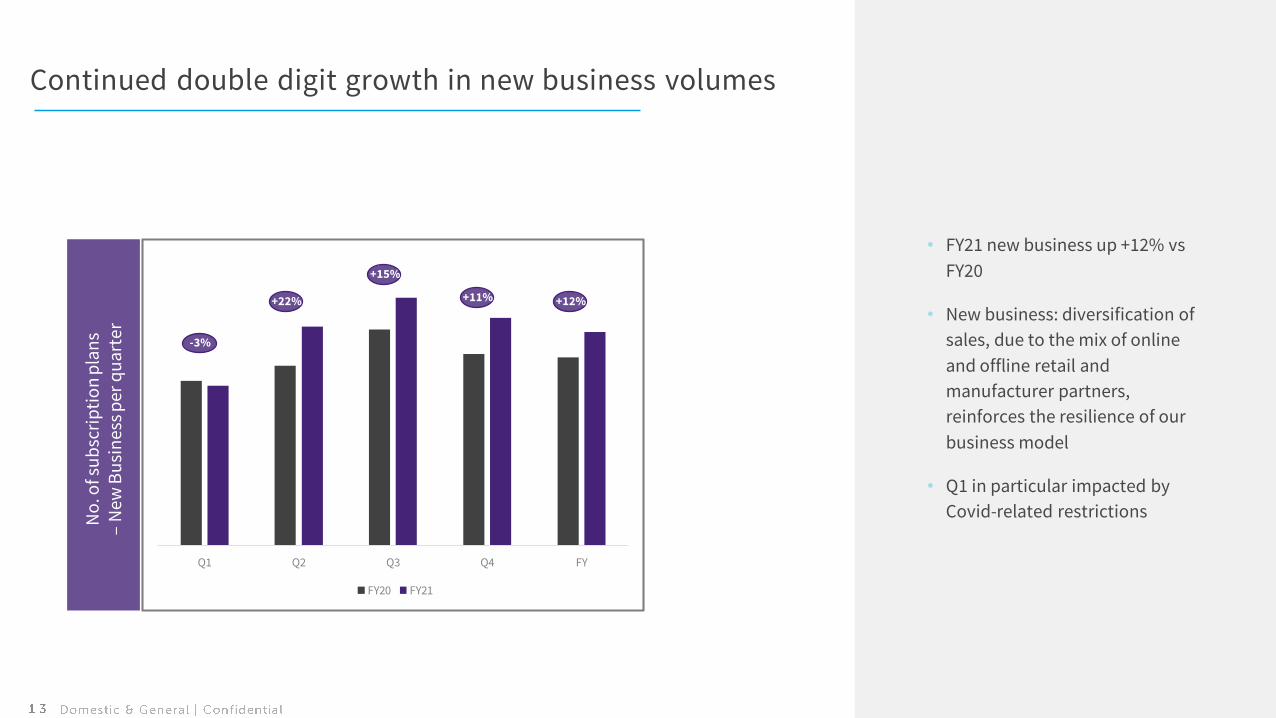

Continued double digit growth in new business volumes

• FY21 new business up +12% vs

FY20

• New business: diversification of

sales, due to the mix of online

and offline retail and

manufacturer partners,

reinforces the resilience of our

business model

• Q1 in particular impacted by

Covid-related restrictionsNo

. of s

ub

scri

pti

on

pla

ns

–N

ew B

usi

nes

s p

er q

uar

ter

-3%

+22%

+15%

+11% +12%

Q1 Q2 Q3 Q4 FY

FY20 FY21

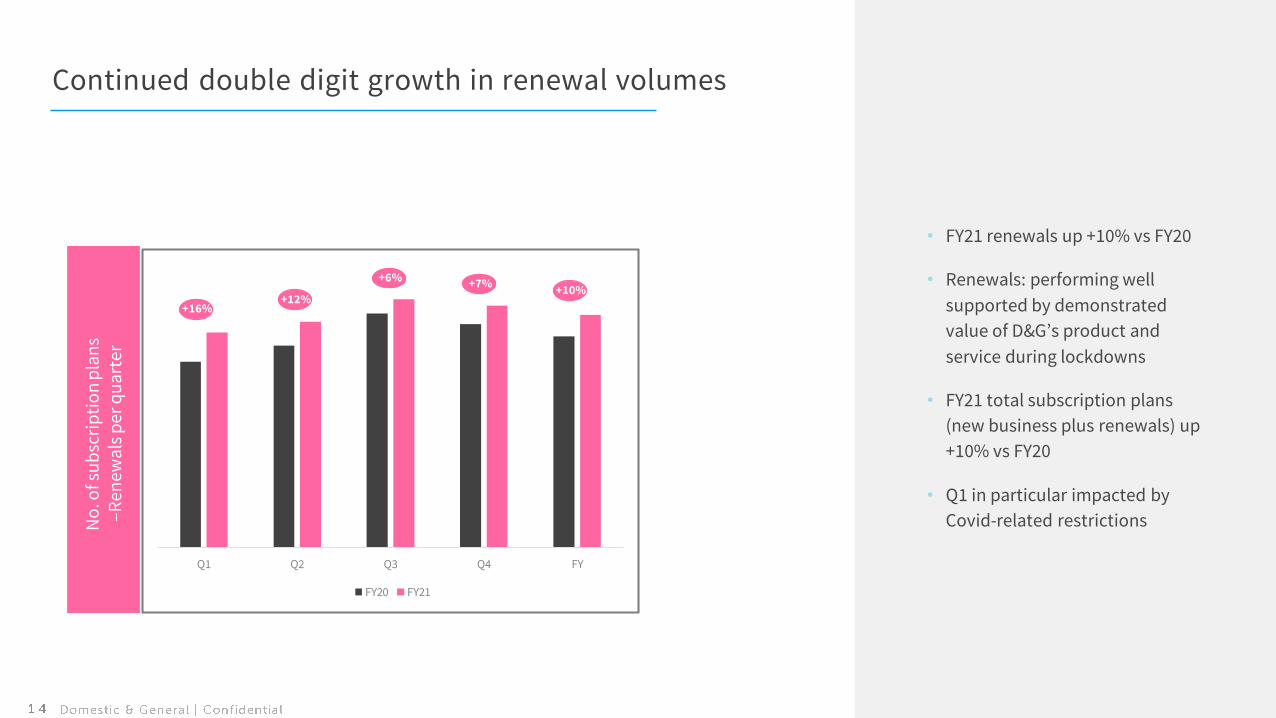

Continued double digit growth in renewal volumes

• FY21 renewals up +10% vs FY20

• Renewals: performing well

supported by demonstrated

value of D&G’s product and

service during lockdowns

• FY21 total subscription plans

(new business plus renewals) up

+10% vs FY20

• Q1 in particular impacted by

Covid-related restrictionsNo

. of s

ub

scri

pti

on

pla

ns

–Ren

ewa

ls p

er q

ua

rter

+16%+12%

+6% +7%+10%

Q1 Q2 Q3 Q4 FY

FY20 FY21

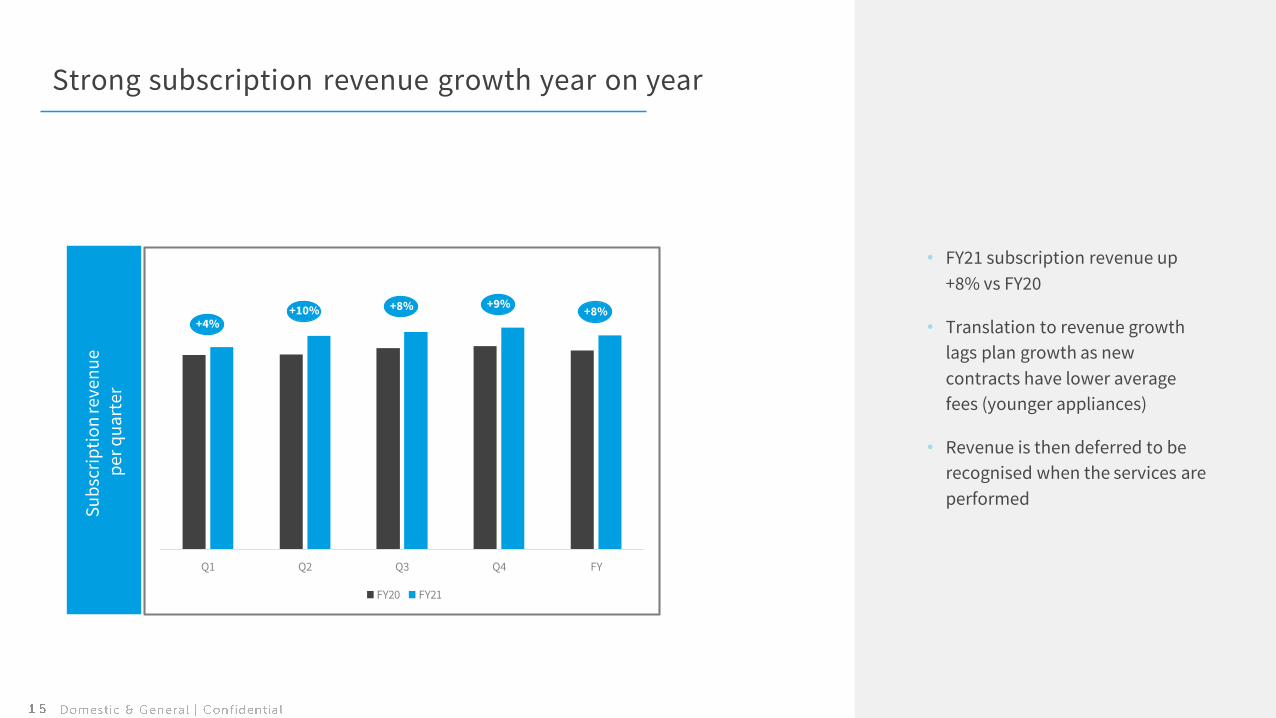

Strong subscription revenue growth year on year

• FY21 subscription revenue up

+8% vs FY20

• Translation to revenue growth

lags plan growth as new

contracts have lower average

fees (younger appliances)

• Revenue is then deferred to be

recognised when the services are

performed

Su

bsc

rip

tio

n re

ven

ue

per

qu

art

er

+4%+10% +8% +9%

+8%

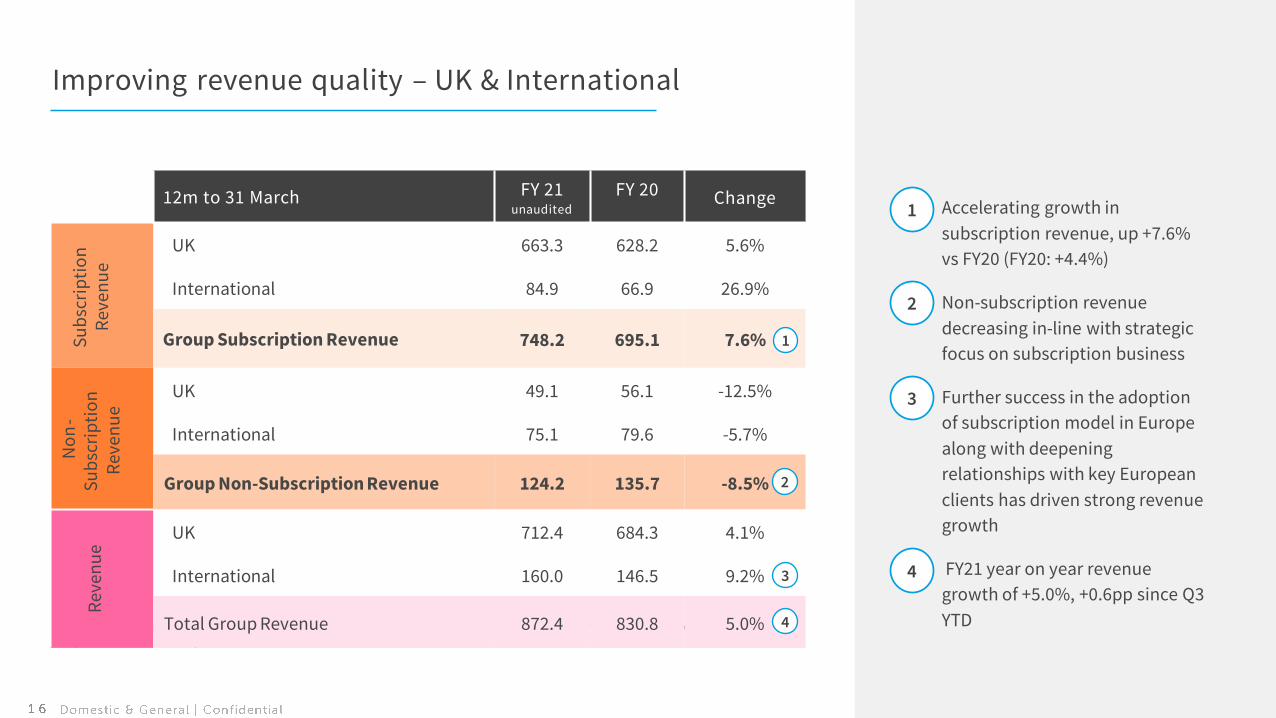

Improving revenue quality – UK & International

*Distributable reserves comprise net income of Regulated Business before significant items and as adjusted for changes in capital requirements and Solvency II valuation differences

12m to 31 March FY 21unaudited

FY 20 Change

Su

bsc

rip

tio

n

Rev

enu

e

UK 663.3 628.2 5.6%

International 84.9 66.9 26.9%

Group Subscription Revenue 748.2 695.1 7.6%

No

n-

Su

bsc

rip

tio

n

Rev

enu

e

UK 49.1 56.1 -12.5%

International 75.1 79.6 -5.7%

Group Non-Subscription Revenue 124.2 135.7 -8.5%

Rev

enu

e

UK 712.4 684.3 4.1%

International 160.0 146.5 9.2%

Total Group Revenue 872.4 830.8 5.0%

• Accelerating growth in

subscription revenue, up +7.6%

vs FY20 (FY20: +4.4%)

• Non-subscription revenue

decreasing in-line with strategic

focus on subscription business

• Further success in the adoption

of subscription model in Europe

along with deepening

relationships with key European

clients has driven strong revenue

growth

• FY21 year on year revenue

growth of +5.0%, +0.6pp since Q3

YTD

1

2

3

4

1

2

3

4

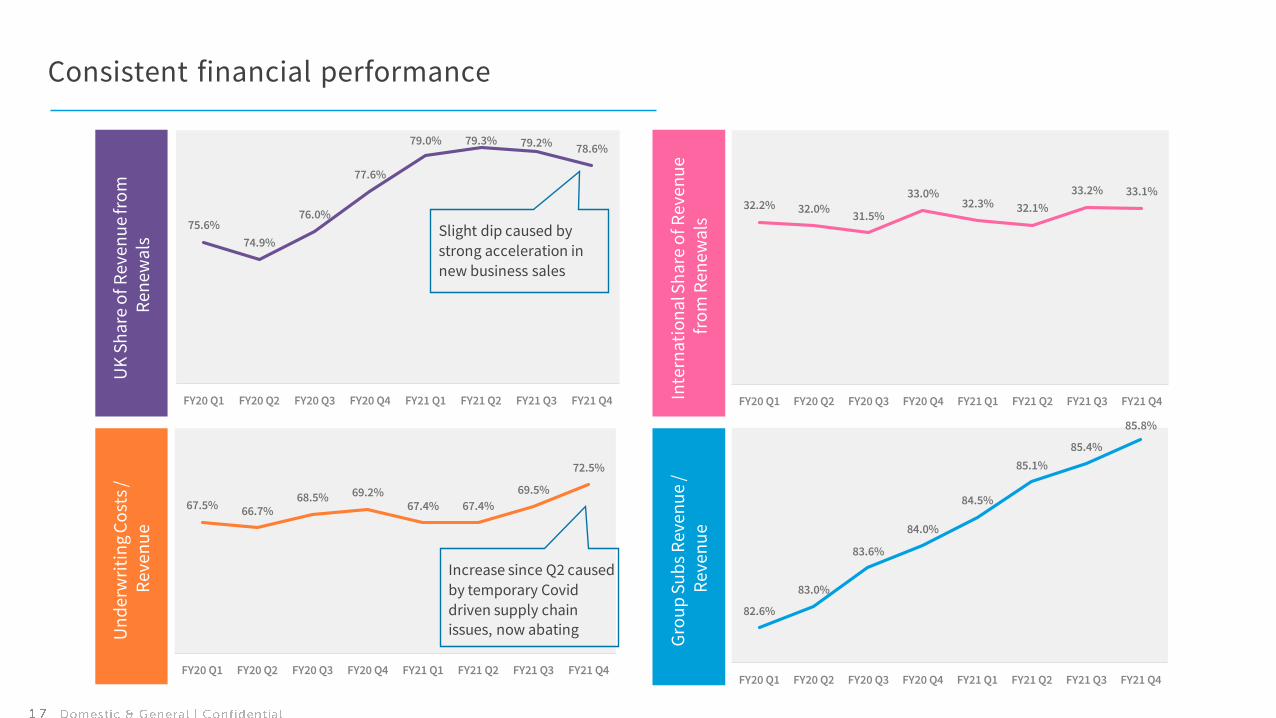

Consistent financial performance

UK

Sh

are

of R

even

ue

fro

m

Ren

ewal

s

Inte

rna

tio

na

l Sh

are

of R

even

ue

fro

m R

enew

als

Un

der

wri

tin

g C

ost

s /

Rev

enu

e

Gro

up

Su

bs

Rev

enu

e /

Rev

enu

e

75.6%

74.9%

76.0%

77.6%

79.0% 79.3% 79.2% 78.6%

FY20 Q1 FY20 Q2 FY20 Q3 FY20 Q4 FY21 Q1 FY21 Q2 FY21 Q3 FY21 Q4

32.2% 32.0%31.5%

33.0%32.3% 32.1%

33.2% 33.1%

FY20 Q1 FY20 Q2 FY20 Q3 FY20 Q4 FY21 Q1 FY21 Q2 FY21 Q3 FY21 Q4

67.5% 66.7%68.5% 69.2%

67.4% 67.4%

69.5%

72.5%

FY20 Q1 FY20 Q2 FY20 Q3 FY20 Q4 FY21 Q1 FY21 Q2 FY21 Q3 FY21 Q4

82.6%

83.0%

83.6%

84.0%

84.5%

85.1%

85.4%

85.8%

FY20 Q1 FY20 Q2 FY20 Q3 FY20 Q4 FY21 Q1 FY21 Q2 FY21 Q3 FY21 Q4

Slight dip caused by

strong acceleration in

new business sales

Increase since Q2 caused

by temporary Covid

driven supply chain issues, now abating

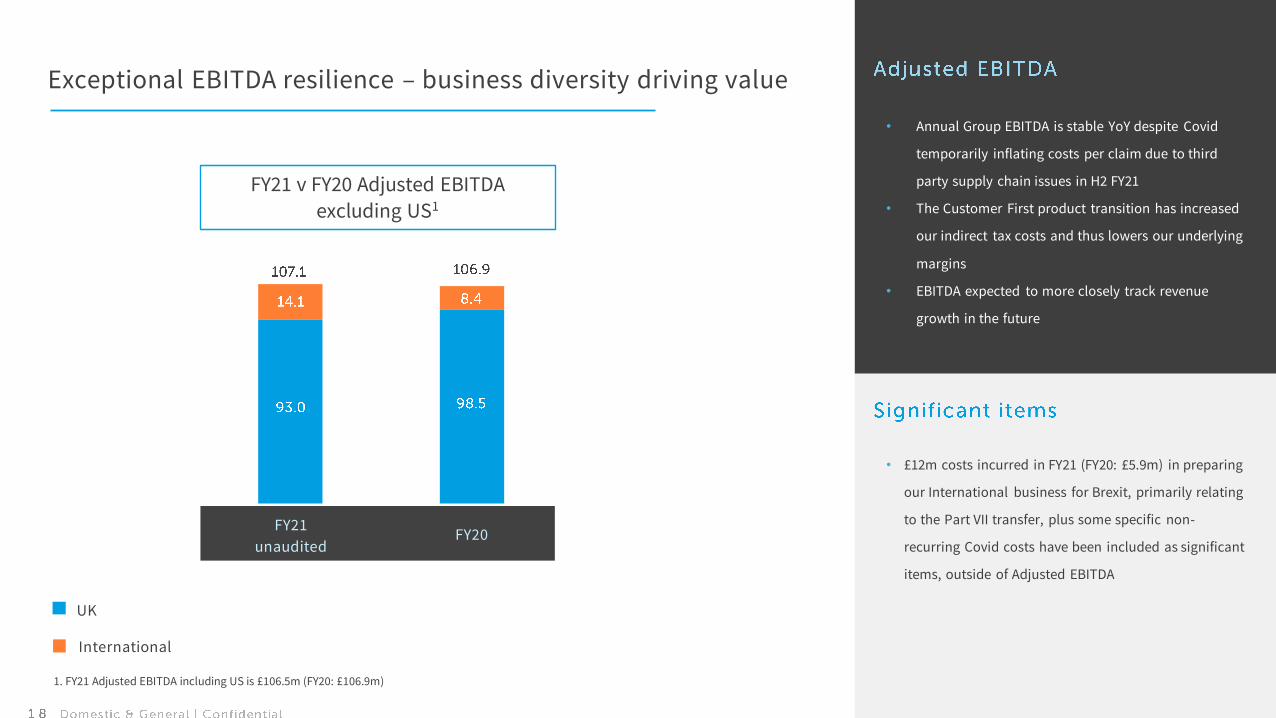

Exceptional EBITDA resilience – business diversity driving value

• Annual Group EBITDA is stable YoY despite Covid

temporarily inflating costs per claim due to third

party supply chain issues in H2 FY21

• The Customer First product transition has increased

our indirect tax costs and thus lowers our underlying

margins

• EBITDA expected to more closely track revenue

growth in the future

• £12m costs incurred in FY21 (FY20: £5.9m) in preparing

our International business for Brexit, primarily relating

to the Part VII transfer, plus some specific non-

recurring Covid costs have been included as significant

items, outside of Adjusted EBITDA

FY21 v FY20 Adjusted EBITDA

excluding US1

FY21

unauditedFY20

UK

International

1. FY21 Adjusted EBITDA including US is £106.5m (FY20: £106.9m)

Cashflow

& capitalisation

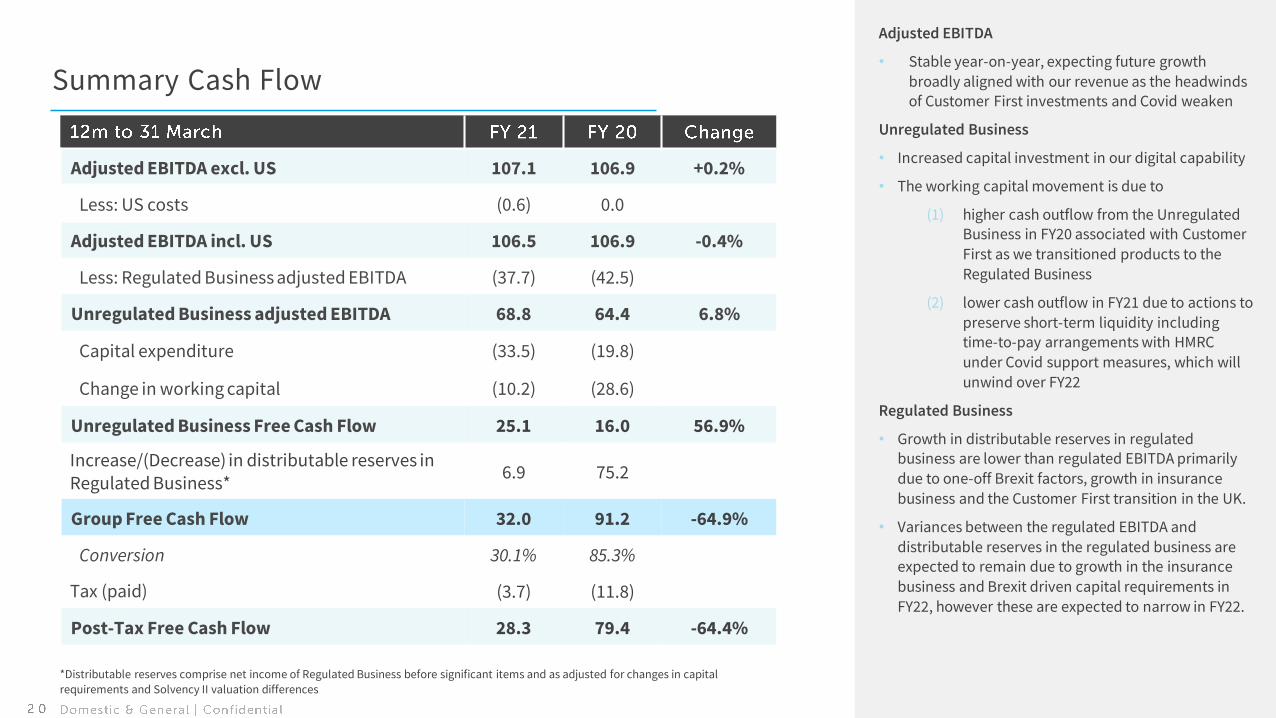

Summary Cash Flow

Adjusted EBITDA excl. US 107.1 106.9 +0.2%

Less: US costs (0.6) 0.0

Adjusted EBITDA incl. US 106.5 106.9 -0.4%

Less: Regulated Business adjusted EBITDA (37.7) (42.5)

Unregulated Business adjusted EBITDA 68.8 64.4 6.8%

Capital expenditure (33.5) (19.8)

Change in working capital (10.2) (28.6)

Unregulated Business Free Cash Flow 25.1 16.0 56.9%

Increase/(Decrease) in distributable reserves inRegulated Business*

6.9 75.2

Group Free Cash Flow 32.0 91.2 -64.9%

Conversion 30.1% 85.3%

Tax (paid) (3.7) (11.8)

Post-Tax Free Cash Flow 28.3 79.4 -64.4%

Adjusted EBITDA

• Stable year-on-year, expecting future growth

broadly aligned with our revenue as the headwinds of Customer First investments and Covid weaken

Unregulated Business

• Increased capital investment in our digital capability

• The working capital movement is due to

(1) higher cash outflow from the Unregulated Business in FY20 associated with Customer

First as we transitioned products to the

Regulated Business

(2) lower cash outflow in FY21 due to actions to

preserve short-term liquidity including time-to-pay arrangements with HMRC

under Covid support measures, which will

unwind over FY22

Regulated Business

• Growth in distributable reserves in regulated business are lower than regulated EBITDA primarily

due to one-off Brexit factors, growth in insurance

business and the Customer First transition in the UK.

• Variances between the regulated EBITDA and

distributable reserves in the regulated business are expected to remain due to growth in the insurance

business and Brexit driven capital requirements in

FY22, however these are expected to narrow in FY22.

*Distributable reserves comprise net income of Regulated Business before significant items and as adjusted for changes in capital requirements and Solvency II valuation differences

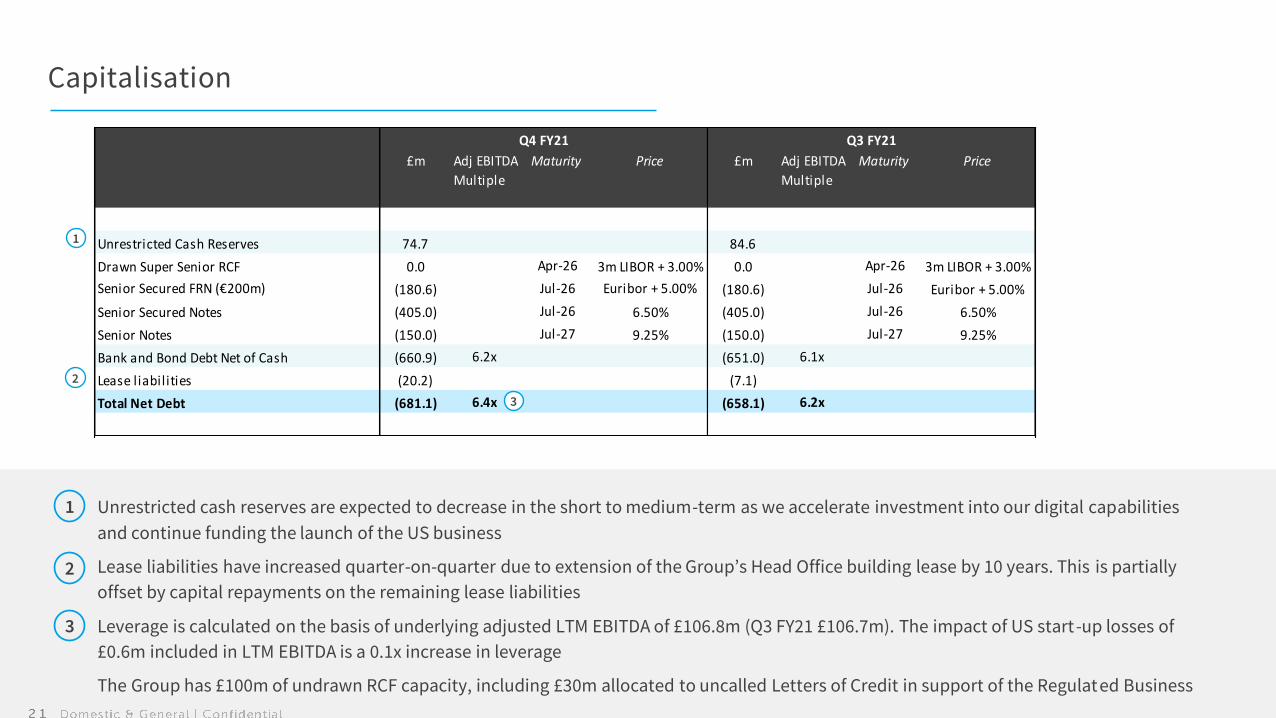

Adj EBITDA

Multiple

Adj EBITDA

Multiple

Unrestricted Cash Reserves 74.7 84.6

Drawn Super Senior RCF 0.0 Apr-26 3m LIBOR + 3.00% 0.0 Apr-26 3m LIBOR + 3.00%

Senior Secured FRN (€200m) (180.6) Jul-26 Euribor + 5.00% (180.6) Jul-26 Euribor + 5.00%

Senior Secured Notes (405.0) Jul-26 6.50% (405.0) Jul-26 6.50%

Senior Notes (150.0) Jul-27 9.25% (150.0) Jul-27 9.25%

Bank and Bond Debt Net of Cash (660.9) 6.2x (651.0) 6.1x

Lease liabilities (20.2) (7.1)

Total Net Debt (681.1) 6.4x (658.1) 6.2x

Maturity

Q4 FY21 Q3 FY21

£m £m Price Maturity Price

Capitalisation

Unrestricted cash reserves are expected to decrease in the short to medium-term as we accelerate investment into our digital capabilities

and continue funding the launch of the US business

Lease liabilities have increased quarter-on-quarter due to extension of the Group’s Head Office building lease by 10 years. This is partially

offset by capital repayments on the remaining lease liabilities

Leverage is calculated on the basis of underlying adjusted LTM EBITDA of £106.8m (Q3 FY21 £106.7m). The impact of US start-up losses of

£0.6m included in LTM EBITDA is a 0.1x increase in leverage

The Group has £100m of undrawn RCF capacity, including £30m allocated to uncalled Letters of Credit in support of the Regulat ed Business

1

2

1

2

3

3

FY21 Summary

A positive year where the

resilience and strength of our

business model allowed us to

grow our revenues and we

made significant progress on

our strategic agenda

Strong new business and retention rates enabled +10% subscription plan

sales growth

International growth particularly encouraging

Stable EBITDA in the face of headwinds

Significant progress on our digital programme

Expected US launch in FY22

Well capitalised with significant headroom

Appendix

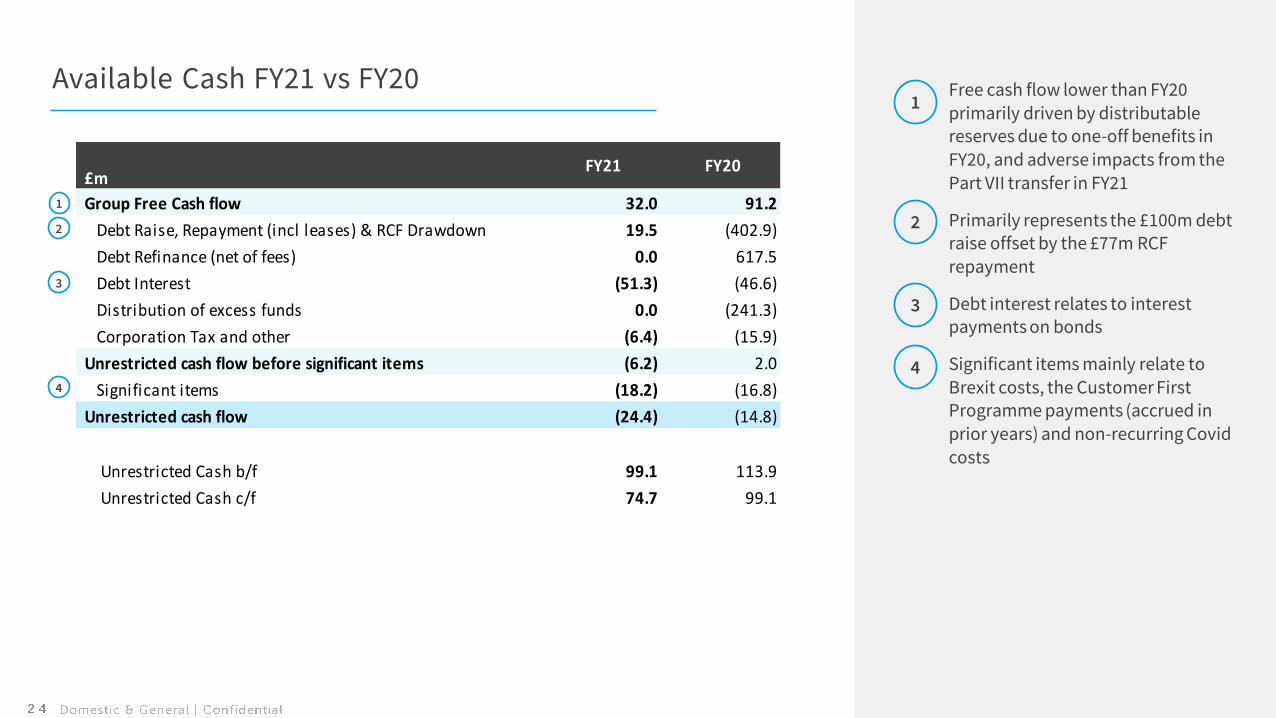

Available Cash FY21 vs FY20 • Free cash flow lower than FY20 primarily driven by distributable reserves due to one-off benefits in FY20, and adverse impacts from the Part VII transfer in FY21

• Primarily represents the £100m debt raise offset by the £77m RCF repayment

• Debt interest relates to interest payments on bonds

• Significant items mainly relate to Brexit costs, the Customer First Programme payments (accrued in prior years) and non-recurring Covid costs

1

2

3

4

1

2

3

4

£m

Group Free Cash flow 32.0 91.2

Debt Raise, Repayment (incl leases) & RCF Drawdown 19.5 (402.9)

Debt Refinance (net of fees) 0.0 617.5

Debt Interest (51.3) (46.6)

Distribution of excess funds 0.0 (241.3)

Corporation Tax and other (6.4) (15.9)

Unrestricted cash flow before significant items (6.2) 2.0

Significant items (18.2) (16.8)

Unrestricted cash flow (24.4) (14.8)

Unrestricted Cash b/f 99.1 113.9

Unrestricted Cash c/f 74.7 99.1

FY21 FY20

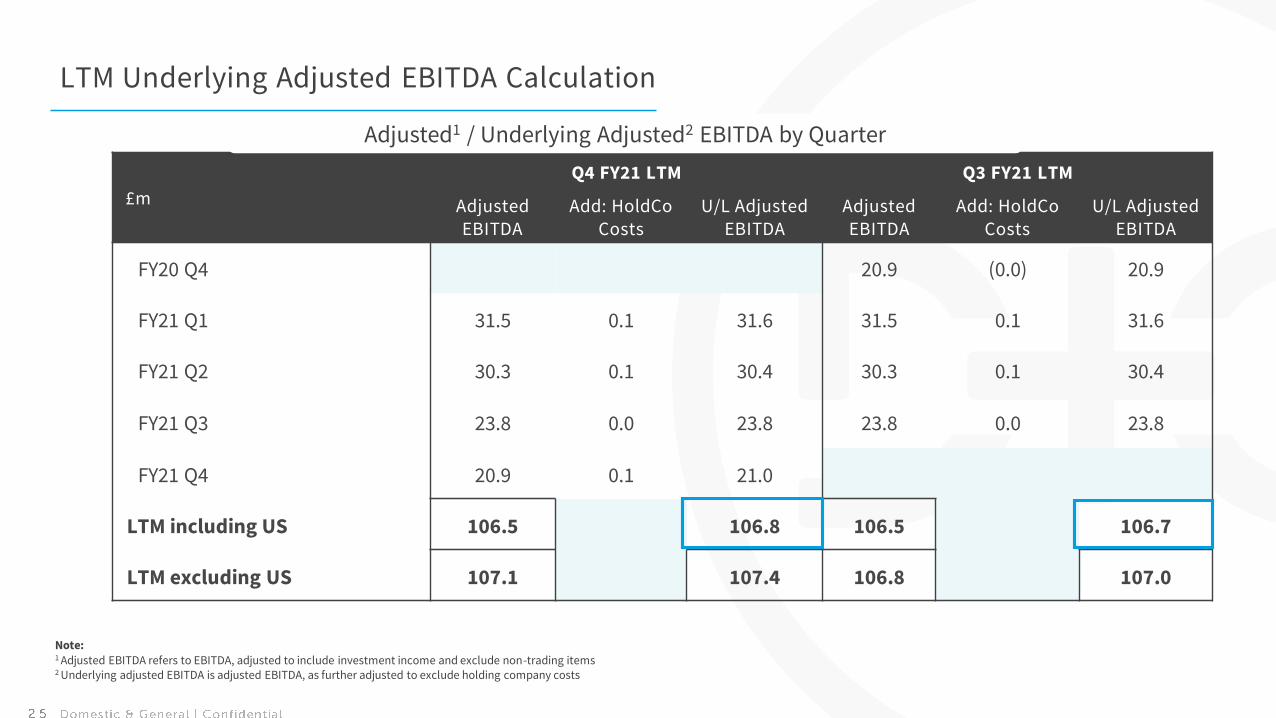

LTM Underlying Adjusted EBITDA Calculation

£m

Q4 FY21 LTM Q3 FY21 LTM

Adjusted EBITDA

Add: HoldCo Costs

U/L Adjusted EBITDA

Adjusted EBITDA

Add: HoldCo Costs

U/L Adjusted EBITDA

FY20 Q4 20.9 (0.0) 20.9

FY21 Q1 31.5 0.1 31.6 31.5 0.1 31.6

FY21 Q2 30.3 0.1 30.4 30.3 0.1 30.4

FY21 Q3 23.8 0.0 23.8 23.8 0.0 23.8

FY21 Q4 20.9 0.1 21.0

LTM including US 106.5 106.8 106.5 106.7

LTM excluding US 107.1 107.4 106.8 107.0

Adjusted1 / Underlying Adjusted2 EBITDA by Quarter

Note:1 Adjusted EBITDA refers to EBITDA, adjusted to include investment income and exclude non-trading items2 Underlying adjusted EBITDA is adjusted EBITDA, as further adjusted to exclude holding company costs

Q + A

Company Confidential, Copyright © Domestic &

General Group Limited. All rights reserved

Disclaimer

This presentation and any materials distributed in connection herewith (together, the “Presentation”) do not constitute or form a part of, and should not be construed as, an offer for sale or subscription of or solicitation of

any offer to purchase or subscribe for any securities in any jurisdiction, and neither this Presentation nor anything contained herein shall form the basis of, or be relied upon in connection with, or act as an inducement to

enter into, any contract or commitment whatsoever.

These materials are being provided to you on a confidential basis, may not be distributed to the press or to any other persons, may not be redistributed or passed on, directly or indirectly, to any person, or published, in

whole or in part, by any medium or for any purpose.

The information contained in this Presentation has not been independently verified and no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy,

completeness, reasonableness or correctness of the information or opinions contained herein. None of Galaxy Finco Limited, its subsidiaries or any of their respective employees, advisers, representatives or affiliates shall

have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this Presentation. The information contained

in this Presentation is provided as at the date of this Presentation and is subject to change without notice.

The information in this Presentation does not constitute investment, legal, accounting, regulatory, taxation or other advice, and the Presentation does not take into account your investment objectives or legal, accounting,

regulatory, taxation or financial situation or other needs. You are solely responsible for forming your own opinions and conclusions on such matters and for making your own independent assessment of the Presentation.

Statements made in this Presentation include forward-looking statements, including in the slide captioned “Summary and Outlook”. These statements may be identified by the fact that they use words such as

“anticipate”, “estimate”, “should”, “expect”, “guidance”, “project”, “intend”, “plan”, “believe”, and/or other words and terms of similar meaning in connection with, among other things, any discussion of results of

operations, financial condition, liquidity, prospects, growth, strategies or developments in the industry in which we operate. Such statements are based on management’s current intentions, expectations or beliefs and

involve inherent risks, assumptions and uncertainties, including factors that could delay, divert or change any of them. Forward-looking statements contained in this Presentation regarding trends or current activities

should not be taken as a representation that such trends or activities will continue in the future. Actual outcomes, results and other future events may differ materially from those expressed or implied by the statements

contained herein. Such differences may adversely affect the outcome and financial effects of the plans and events described herein and may result from, among other things, changes in economic, business, competitive,

technological, strategic or regulatory factors and other factors affecting the business and operations of the company. Neither Galaxy Finco Limited nor any of its affiliates is under any obligation, and each such entity

expressly disclaims any such obligation, to update, revise or amend any forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on any such

forward-looking statements, which speak only as of the date of this Presentation. It should be noted that past performance is not a guide to future performance. Particular uncertainties that could cause our actual results

to be materially different than those expressed in these forward-looking statements include risk factors described in the offering memorandum of Galaxy Bidco Limited and Galaxy Finco Limited dated October 24, 2013, as

updated from time to time by our annual and quarterly financial statements and financial reports, including the section captioned “Principal Risks and Uncertainties” of our Annual Report and Accounts 2020. Nothing in

this Presentation should be construed as a profit forecast.

This Presentation may also contain non-GAAP financial information. Management uses this information in its internal analysis of results and liquidity and believes that this information may be informative to investors in

gauging the quality of our financial performance , assessing our liquidity, identifying trends in our results and providing meaningful period-to-period comparisons. In this financial release we report preliminary unaudited

operating and financial information as of 31 March 2021. This financial information is preliminary, has not been audited by our independent auditors and is subject to change prior to Galaxy Finco Limited issuing its 31

March 2021 audited consolidated financial statements.