fy/q4 2014 investor conference call presentation charts

TRANSCRIPT

Investor Conference CallFY/Q4 2014 Results

February 26, 2015 / Marijn Dekkers, CEO

DisclaimerThis presentation may contain forward-looking statements based on currentassumptions and forecasts made by Bayer Group or subgroup management.

Various known and unknown risks, uncertainties and other factors could lead tomaterial differences between the actual future results, financial situation,development or performance of the company and the estimates given here.These factors include those discussed in Bayer’s public reports which areavailable on the Bayer website at www.bayer.com.

The company assumes no liability whatsoever to update these forward-lookingstatements or to conform them to future events or developments.

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers Page 2

Page 3

2014 – Strong Business Development and Focus on Life Sciences

Delivered strong organic growth with record earnings; all subgroups contributed

Q4 – product innovations and emerging markets continued to drive performance

Portfolio transformation into a pure Life Science Company underway

Integration of acquired businesses on track

Dividend proposal of €2.25, up 7% yoy, 37% payout of Core EPS

Financial outlook 2015 projects further growth and higher earnings

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

Page 4

EBITin € million

-14%

561655

Salesin € million% currency & portfolio adj.

+7%

11,0399,888

EBITDABefore special itemsin € million

+4%

1,8461,769

Core EPSin €

+8%

1.191.10

Q4’14Q4’13 Q4’14Q4’13 Q4’14Q4’13 Q4’14Q4’13

Q4 2014 – Solid Finish to a Successful Year

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

Q4 2014 – Divisional Break-Down

Page 5

Group €11,039m; +7%

1,609

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

2013 2014

3,490

3691,844

487

+16%

-13%

1,846

+14%

EBITDA

217

939

-5%

+4%

MaterialScience+5%

CropScience+8%

Pharma+10%

ConsumerHealth+4%

2,195 2,327

3,2712,948 822

515

319

248

1,769

EBITDABefore special itemsin € million

Salesin € million% currency & portfolio adj.

FY 2014 – All Targets Achieved

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers Page 6

Sales ∆ Fx & portf. adjusted, EBITDA before special items

2014 Guidance 2014Actual

∆ 2014 Actual

vs. 2013

Sales ~5% to~€41-42bn €42.2bn +7%

adj. EBITDA mid-single-digit % increase €8.8bn +5%

core EPS mid-to-high-single-digit % increase €6.02 +7%

✓

✓

✓

FY 2014 – Recently Launched Products Continued to Drive Performance at Pharma

Page 7

Stivarga

Recentlylaunched

+95%

Establishedproducts-2%

Pharma €12,052m; +11%

759

+133%1,679

+82%

89

nm224

+17%

2,9089,144

EyleaXarelto

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

+287%

157

Sales in € million% currency & portfolio adj.

Product Salesin € million% currency adj.

Consumer Care – Brands and Emerging Market Focus Countries Drive Growth

• FY/Q4 2014 Investor Conference Call • Marijn DekkersPage 8

+10%+5%** +18%

2013 2014pro-forma*

China Brazil Russia

+28% +26% +26%∆% Fx adj. yoy

€3.9bn

€5.6bn

* including acquired businesses** including Aspirin Cardio recognized at Pharma

FY 2014 – Commercial Execution, New Products, and Seeds Drive Growth At CropScience

Page 9

CropScience €9,494m; +11%

In € million, ∆% yoy currency & portfolio adj.

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

Crop Protection+11%

EnvironmentalScience

+7%

Seeds+20%

7,712678

1,104

820974

2012 2013 2014

1,104

Seed Sales

* Launched since 2006; nominal growth

+20%

1.11.5

2012 2013 2014

1.9

New CP Product Sales*

+23%in €bn

FY 2015 Group Guidance –Further Sales and Earnings Growth

Page 10

2014 2015e*

Sales €42.2bnLow-single digit %

increase~€46bn

(positive FX effect approx. +3%)

adj. EBITDA €8.8bnLow-to-mid-teens %

increase(positive FX effect approx. +2%)

core EPS €6.02Low-teens %

increase(positive FX effect approx. +3%)

Sales ∆ Fx and portfolio adjusted, EBITDA before special items

*Assuming Fx rates of 12/31/2014 (USD 1.21)Outlook depends on specific planning assumptions as detailed in the Annual Report• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

FY 2015 –R&D and CapEx Budgets

Page 11

2%

MaterialScience~€0.2bn

HealthCare~€2.6nthereof Pharma ~€2.2bn

MaterialScience~€0.5bn

HealthCare~€0.8bn

Reconciliation~€0.1bn

66%27%

5%

Reconciliation~€0.3bn

CropScience~€1.1bn

CropScience~€0.7bn

23%

31%

35%

11%

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

R&D 2015e: >€4.0bn (+10%) CapEx (PPE) 2015e: ~€2.3bn

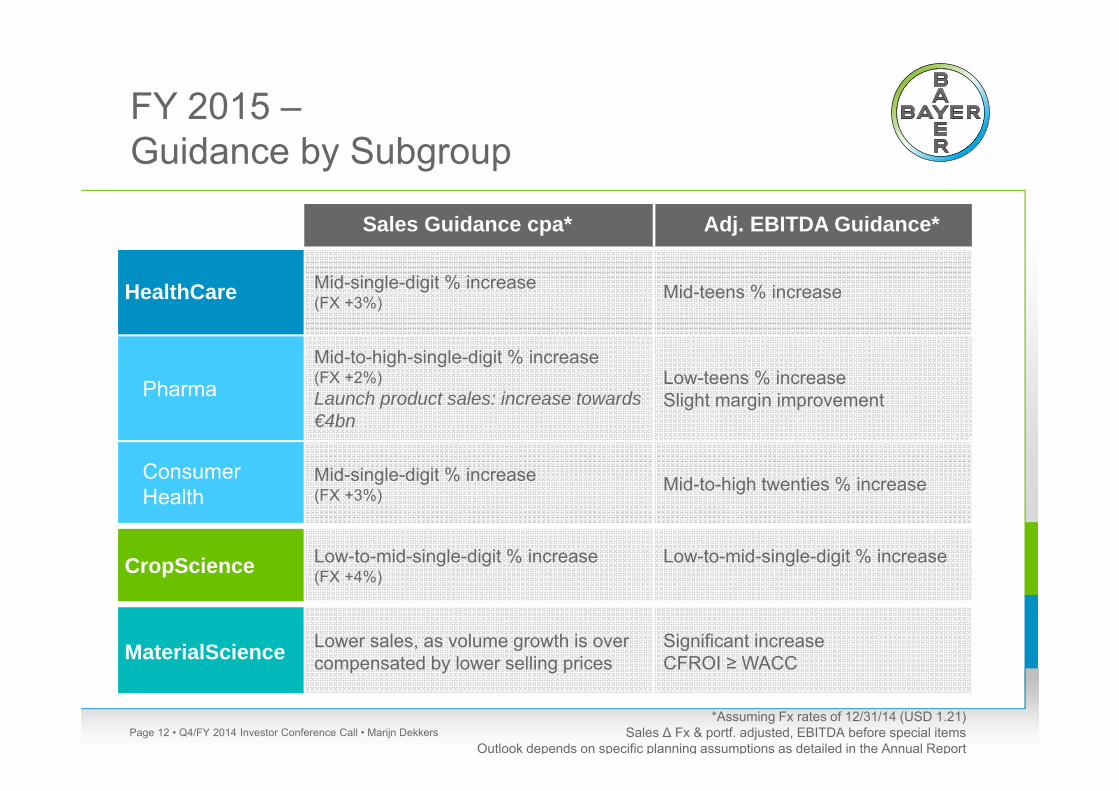

HealthCare Mid-single-digit % increase(FX +3%) Mid-teens % increase

PharmaMid-to-high-single-digit % increase (FX +2%)Launch product sales: increase towards €4bn

Low-teens % increaseSlight margin improvement

ConsumerHealth

Mid-single-digit % increase (FX +3%) Mid-to-high twenties % increase

CropScience Low-to-mid-single-digit % increase (FX +4%)

Low-to-mid-single-digit % increase

MaterialScience Lower sales, as volume growth is over compensated by lower selling prices

Significant increase CFROI ≥ WACC

FY 2015 –Guidance by Subgroup

Page 12*Assuming Fx rates of 12/31/14 (USD 1.21)

Sales ∆ Fx & portf. adjusted, EBITDA before special itemsOutlook depends on specific planning assumptions as detailed in the Annual Report

• Q4/FY 2014 Investor Conference Call • Marijn Dekkers

Sales Guidance cpa* Adj. EBITDA Guidance*