global monthly may 2017 - world...

TRANSCRIPT

Global Monthly May 2017

Sources: Bloomberg, World Bank.

Note: MSCI stock market indexes for 23 advanced and 23 emerging market

economies. Weighted by market capitalization. Five-day average. Last observation

is May 22, 2017.

Stock market indexes

Overview

• Global growth was temporarily held back in Q1 by a slowdown in U.S. consumption, which is expected to recover in Q2.

• Growth continues to firm in other major advanced economies and is gradually recovering in commodity-exporting emerging market and developing economies (EMDEs).

• Capital inflows to EMDEs remained strong in May, supported by continued investor risk appetite.

• Oil prices have risen since mid-May on the prospect of an extension of the OPEC/non-OPEC production cuts, which was confirmed at an OPEC meeting on May 25.

Chart of the Month

• Despite heightened policy and political uncertainty, global equity prices reached record highs in May.

• In particular, EMDE stock indexes have registered the largest January-to-May increase in at least a decade, and have significantly out-performed advanced economies.

• The strong performance of EMDE equity markets reflects diminishing growth headwinds for commodity exporters, increased appetite for high-yielding assets, and strengthening corporate earnings in EMDEs.

• Following an uptick mid-May, stock market volatility in both advanced economies and EMDEs returned to low historical levels.

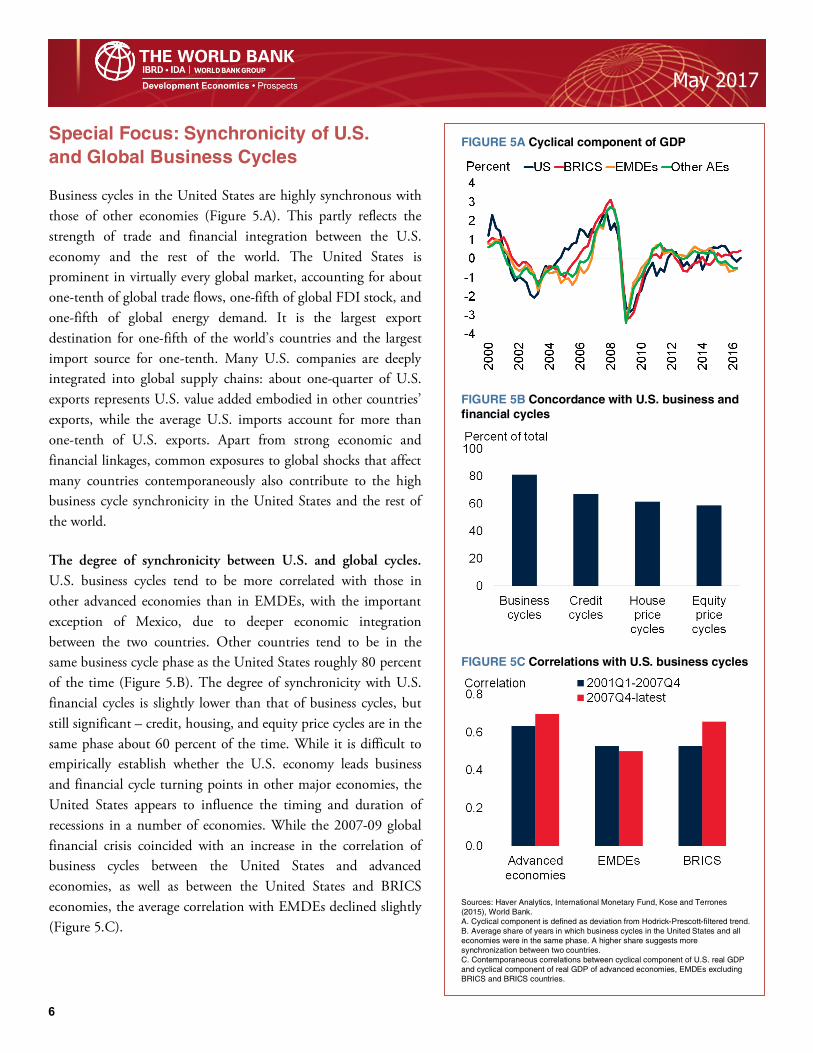

Special Focus: Synchronicity of U.S. and Global Business Cycles

• Business cycles in the United States are highly synchronized with those of other economies.

• This partly reflects the strength of trade and financial linkages between the U.S. economy and the rest of the world, as well as the impact of global shocks that affect many countries simultaneously.

• U.S. business cycles tend to be more correlated with business cycles in other advanced economies than those in EMDEs, with the key exception of Mexico, due to deep economic integration.

4e Global Monthly is a publication of the Global Macroeconomics Team of the Prospects Group in the Development Economics Vice Presidency. 4is edition was prepared by Marc Stocker and Dana Vorisek, based on contributions from John Ba6es, Mai Anh Bui, Sinem Celik, Gerard Kambou, Eung Ju Kim, Csilla Lakatos, Hideaki Matsuoka, Yoki Okawa, Temel Taskin, Ekaterine Vashakmadze, Collette Wheeler, and Lei Sandy Ye. 4is Global Monthly re=ects information available as of May 24. For more information, visit: http://www.worldbank.org/en/research/brief/economic-monitoring

Table of Contents

Monthly Highlights .............................................. 2

Special Focus ....................................................... 6

Recent Publications of Prospects Group .................. 8

Recent World Bank Working Papers....................... 8

Key World Bank Reports ...................................... 8

Table A: Major Data Releases ............................... 8

Table B: Activity and Inflation.............................. 9

Table C: Trade and Finance ................................. 9

Table D: Financial Markets ............................... 10

Table E: Commodity Prices ................................. 10

2

May 2017

Global economy: manufacturing-driven upturn. Global

industrial production was robust in 17Q1, growing by 3.7

percent (q/q saar). This pace is somewhat slower than a six-year

peak of 5.3 percent (q/q saar) reached in 16Q4, but still

significantly higher than the post-crisis average (Figure 1.A).

Based on available national data, global GDP growth likely

moderated in 17Q1, to around 2.5 percent (q/q saar), driven by a

consumption-led slowdown in the United States. However,

growth was solid in other advanced economies and appears to

have accelerated in major commodity-exporting emerging

EMDEs. In April, the global composite PMI was firmly in

expansionary territory, and broadly stable since the start of the

year. Global median inflation stabilized in March and April at

close to 2.5 percent, the highest level since mid-2014.

Global trade: continued recovery. Global trade growth remained

strong in 17Q1, at around 6 percent (q/q saar). At the regional

level, export growth showed continued signs of recovery in East

Asia and Pacific, Europe and Central Asia, and Latin America,

but remained subdued in Sub-Saharan Africa. The expansion of

new export orders stabilized at a high level in April, suggesting

continued strong trade growth at the start of 17Q2 (Figure 1.B).

However, indicators such as demand for automotive products,

electronic components, and agricultural raw materials point to

weakening global import demand.

United States: ongoing rebound. Growth slowed to 0.7 percent

(q/q saar) in 17Q1, the weakest pace in two years, as real personal

consumption expenditure was held back by transitory factors. In

contrast, private fixed investment growth reached a five-year high,

and export growth recovered strongly. A pickup in retail sales and

industrial production growth in April point to a strong start in

17Q2, and various forecasts suggest that real GDP growth could

accelerate significantly this quarter (Figure 1.C). The

unemployment rate fell to 4.4 percent in April, the lowest level

since May 2007. Wage growth, though still subdued, has been on

a mild upward trajectory since 2015. Compensation costs rose by

2.3 percent in March (y/y), dampened by a sluggish increase in

benefits, while average hourly earnings growth slowed marginally

in April, to 2.5 percent (y/y). Core CPI inflation slowed to 1.9

percent in April, down 0.4 percentage point since January.

Monthly Highlights

FIGURE 1B Global manufacturing PMI

FIGURE 1C U.S. GDP growth

Sources: Consensus Economics, CPB Netherlands Bureau for Economic Policy

Analysis, Federal Reserve Bank of Atlanta, Federal Reserve Bank of New York,

Haver Analytics, World Bank.

A. Last observation is March 2017 for industrial production and February 2017 for

trade. Estimates for 2017Q1 trade data assume unchanged levels in March.

B. 3-month moving averages. Last observation is April 2017.

C. Diamonds indicate forecast data as of May 23, 2017.

FIGURE 1A Global industrial production and trade

3

May 2017

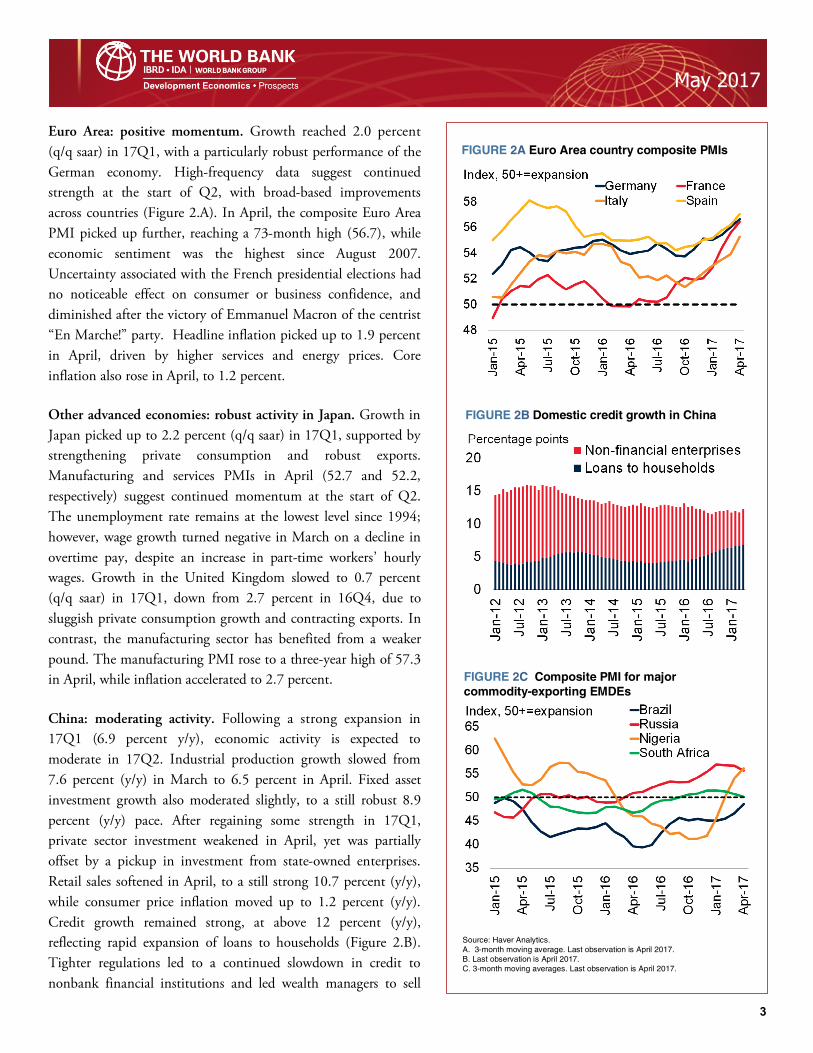

Euro Area: positive momentum. Growth reached 2.0 percent

(q/q saar) in 17Q1, with a particularly robust performance of the

German economy. High-frequency data suggest continued

strength at the start of Q2, with broad-based improvements

across countries (Figure 2.A). In April, the composite Euro Area

PMI picked up further, reaching a 73-month high (56.7), while

economic sentiment was the highest since August 2007.

Uncertainty associated with the French presidential elections had

no noticeable effect on consumer or business confidence, and

diminished after the victory of Emmanuel Macron of the centrist

“En Marche!” party. Headline inflation picked up to 1.9 percent

in April, driven by higher services and energy prices. Core

inflation also rose in April, to 1.2 percent.

Other advanced economies: robust activity in Japan. Growth in

Japan picked up to 2.2 percent (q/q saar) in 17Q1, supported by

strengthening private consumption and robust exports.

Manufacturing and services PMIs in April (52.7 and 52.2,

respectively) suggest continued momentum at the start of Q2.

The unemployment rate remains at the lowest level since 1994;

however, wage growth turned negative in March on a decline in

overtime pay, despite an increase in part-time workers’ hourly

wages. Growth in the United Kingdom slowed to 0.7 percent

(q/q saar) in 17Q1, down from 2.7 percent in 16Q4, due to

sluggish private consumption growth and contracting exports. In

contrast, the manufacturing sector has benefited from a weaker

pound. The manufacturing PMI rose to a three-year high of 57.3

in April, while inflation accelerated to 2.7 percent.

China: moderating activity. Following a strong expansion in

17Q1 (6.9 percent y/y), economic activity is expected to

moderate in 17Q2. Industrial production growth slowed from

7.6 percent (y/y) in March to 6.5 percent in April. Fixed asset

investment growth also moderated slightly, to a still robust 8.9

percent (y/y) pace. After regaining some strength in 17Q1,

private sector investment weakened in April, yet was partially

offset by a pickup in investment from state-owned enterprises.

Retail sales softened in April, to a still strong 10.7 percent (y/y),

while consumer price inflation moved up to 1.2 percent (y/y).

Credit growth remained strong, at above 12 percent (y/y),

reflecting rapid expansion of loans to households (Figure 2.B).

Tighter regulations led to a continued slowdown in credit to

nonbank financial institutions and led wealth managers to sell

FIGURE 2B Domestic credit growth in China

FIGURE 2A Euro Area country composite PMIs

FIGURE 2C Composite PMI for major

commodity-exporting EMDEs

Source: Haver Analytics.

A. 3-month moving average. Last observation is April 2017.

B. Last observation is April 2017.

C. 3-month moving averages. Last observation is April 2017.

4

May 2017

bonds, pushing 5-year government bond yields above the 10-year

yield for the first time on record. The new U.S.-China guidelines

for bilateral trade released in early May reduced the risk of

retaliatory trade restrictions between the two countries.

EMDE commodity exporters: continued recovery. The

composite PMI for Nigeria surged to 58.2 in April, from an

average of 41.8 in 17Q1, pointing to a likely recovery in the

manufacturing sector. Growth in Russia accelerated to 0.5

percent (y/y) in 17Q1, from 0.3 percent in 16Q4. The composite

PMI remained elevated in April, but suggests that the pace of the

recovery might have peaked. In Brazil, the central bank’s

economic activity index advanced further into positive territory in

March, to 0.7 percent (y/y). The manufacturing and services

PMIs were both above the threshold of 50 in April. Disinflation

has allowed policy interest rate cuts in Brazil and Russia (Figure

3A). At 4.1 percent (y/y) in April in both countries, inflation is

close to or below target levels in Russia (4.0 percent) and Brazil

(4.5 percent central target). Growth in 17Q1 remained strong (5

percent y/y) in Indonesia and accelerated to 5.6 percent (y/y) in

Malaysia, supported by recovering exports and still robust

domestic demand. In South Africa, mining production expanded

by 3.5 percent (q/q, sa) in 17Q1, after contracting in 16Q4.

Manufacturing output grew 0.3 percent (y/y) in March—the first

annual expansion since November.

EMDE commodity importers: generally solid performance. In

India, industrial production growth increased to 2.7 percent (y/

y) in March, from an upwardly revised 1.9 percent in February.

The manufacturing PMI was stable in April, at 52.5, while

inflation eased to 3 percent (y/y), a 12-year low. Mexico’s 17Q1

GDP growth was 2.6 percent (y/y, sa), led by a solid services

sector performance, which offset a contraction in the industrial

sector. Amid steadily rising inflation, the policy interest rate was

further raised on May 18 (Figure 3B). In Turkey, industrial

production and retail sales data suggest a softening of growth in

17Q1. Inflation accelerated to a 10-year high of 11.8 percent in

April. According to a flash estimate, GDP in Poland expanded

4.1 percent (y/y, sa) in 17Q1, amid signs of a recovery in

investment and private consumption. Thailand’s GDP growth

picked up to 5.2 percent (q/q saar) in 17Q1, driven by a rebound

of private consumption and exports, which offset a deceleration

in private investment.

FIGURE 3B Policy interest rates in major

commodity-importing EMDEs

FIGURE 3A Policy interest rates in major

commodity-exporting EMDEs

FIGURE 3C Global stock market index and implied

volatility

Sources: Bloomberg, Haver Analytics, World Bank.

A. Last observation is May 23, 2017.

B. Last observation is May 23, 2017.

C. Last observation is May 23, 2017.

5

May 2017

Global financing conditions: limited impact of policy

uncertainty. Financial market volatility generally remained low,

although it increased somewhat mid-May amid heightened

political uncertainties (Figure 3.C). Global equity prices remain

close to record highs as the ongoing global recovery appears to be

supporting investor risk appetite. U.S. 10-year Treasury yields fell

back as prospects of U.S. fiscal stimulus waned. However, at 2.3

percent, yields are still 40 basis points above levels prevailing

before the U.S. elections. The probability of a June interest rate

hike by the U.S. Federal Reserve is currently above 80 percent

(Figure 4.A), as U.S. labor market conditions continue to tighten

and inflation nears the target level.

EMDE financial markets: ongoing gains. EMDE stocks,

sovereign and corporate bonds, and currencies all posted gains

from January to April. In May, EMDE financial markets

remained buoyant. Capital inflows to EMDEs continued to be

robust, while bond spreads remain near their lowest levels since

September 2014, despite an uptick in second half of the month.

Bond issuance has also continued at a fast clip in May, with

Brazil’s state-owned oil company Petrobras selling $4 billion of 5-

and 10-year notes. Corporate issuances continue to dominate

bond market activity, as EMDE companies take advantage of

favorable borrowing cost to refinance existing debt (Figure 4.B).

Among sovereign borrowers, Panama, Senegal, Sri Lanka, and

Turkey came to the market with new public debt issuance.

Oil prices: controlling supply. Oil traded below the $50/bbl

mark during the first half of May on persistently high

stocks and quicker-than-expected rebound of U.S. shale oil

production. The rebound of U.S. production, along with

higher-than-expected Libyan and Nigerian output, pushed

oil stocks in OECD countries to near record levels. Stocks

are expected to gradually diminish as demand is projected to

outpace production in the second half of 2017 (Figure 4.C).

Oil prices have gained ground since mid-May on the prospect of

an extension of the OPEC/non -OPEC production cuts.

Indeed, Saudi Arabia and Russia announced on May 15th

that they support extending cuts for nine months, which lifted

prices above $52/bbl. The extension was confirmed at an

OPEC meeting on May 25.

FIGURE 4B EMDE international bond issuance

FIGURE 4A Probability of U.S. interest rate hike in

June 2017

FIGURE 4C Global oil markets

Sources: Bloomberg, Dealogic, International Energy Agency, World Bank.

A. Data begin March 16, 2017—one day after Federal Reserve Open Market

Committee. Last observation is May 23, 2017.

B. Last observation is May 23, 2017.

C. Balance is defined as the difference between world oil demand and supply.

OPEC crude oil production for 2017 is assumed at 32.0 mb/d. Shaded area

(2017Q2-2017Q4) represents IEA projections.

6

May 2017

FIGURE 5B Concordance with U.S. business and

financial cycles

FIGURE 5A Cyclical component of GDP

FIGURE 5C Correlations with U.S. business cycles

Sources: Haver Analytics, International Monetary Fund, Kose and Terrones

(2015), World Bank.

A. Cyclical component is defined as deviation from Hodrick-Prescott-filtered trend.

B. Average share of years in which business cycles in the United States and all

economies were in the same phase. A higher share suggests more

synchronization between two countries.

C. Contemporaneous correlations between cyclical component of U.S. real GDP

and cyclical component of real GDP of advanced economies, EMDEs excluding

BRICS and BRICS countries.

Special Focus: Synchronicity of U.S.

and Global Business Cycles

Business cycles in the United States are highly synchronous with

those of other economies (Figure 5.A). This partly reflects the

strength of trade and financial integration between the U.S.

economy and the rest of the world. The United States is

prominent in virtually every global market, accounting for about

one-tenth of global trade flows, one-fifth of global FDI stock, and

one-fifth of global energy demand. It is the largest export

destination for one-fifth of the world’s countries and the largest

import source for one-tenth. Many U.S. companies are deeply

integrated into global supply chains: about one-quarter of U.S.

exports represents U.S. value added embodied in other countries’

exports, while the average U.S. imports account for more than

one-tenth of U.S. exports. Apart from strong economic and

financial linkages, common exposures to global shocks that affect

many countries contemporaneously also contribute to the high

business cycle synchronicity in the United States and the rest of

the world.

The degree of synchronicity between U.S. and global cycles.

U.S. business cycles tend to be more correlated with those in

other advanced economies than in EMDEs, with the important

exception of Mexico, due to deeper economic integration

between the two countries. Other countries tend to be in the

same business cycle phase as the United States roughly 80 percent

of the time (Figure 5.B). The degree of synchronicity with U.S.

financial cycles is slightly lower than that of business cycles, but

still significant – credit, housing, and equity price cycles are in the

same phase about 60 percent of the time. While it is difficult to

empirically establish whether the U.S. economy leads business

and financial cycle turning points in other major economies, the

United States appears to influence the timing and duration of

recessions in a number of economies. While the 2007-09 global

financial crisis coincided with an increase in the correlation of

business cycles between the United States and advanced

economies, as well as between the United States and BRICS

economies, the average correlation with EMDEs declined slightly

(Figure 5.C).

7

May 2017

Concordance of cyclical turning points. Global GDP growth is

substantially correlated with different phases of the U.S. business

cycle, but international business cycle concordance has been

particularly strong during U.S. recessions. Growth in other

advanced economies and EMDEs was, on average, higher during

periods of U.S. expansions relative to U.S. recessions (Figure

6.A). While the four global economic recessions since 1960

(1975, 1982, 1991, and 2009) were driven by a host of problems

in various corners of the world, they also all overlapped with

recessions in the United States.

The global recession of 1975 coincided with the beginning of a

prolonged period of stagflation, low output growth, and high

inflation in the United States. During the 1982 recession, the

United States, along with several other advanced economies,

experienced a sharp decline in activity and steep increase in

unemployment in the wake of anti-inflationary monetary

policies. Following the peak in July 1990, the United States again

went into recession, this time due to depressed activity in the

housing market and a credit crunch. The U.S. recession of 2007-

09 also had its origins in the U.S. housing market, which turned

into a global crisis after the collapse of Lehman Brothers in

September 2008. While these four U.S. recessions coincided with

global recessions, four other U.S. recessions post-1960 did not.

Activity around U.S. recessions. An event study of the last two

U.S. recessions, in 2001 and 2007-09, illustrates the concordance

of the turning points of the U.S. business cycle with those of

other advanced economies and EMDEs (Figure 6.B and 6.C).

The U.S. economy experienced only a mild recession in 2001

following the burst of the “dot com” bubble of the late 1990s,

whereas the 2007-09 recession was particularly severe. In the four

quarters preceding these last two U.S. business cycle troughs,

other advanced economies also experienced a decline in the

cyclical component of their GDP, while their subsequent

recoveries have remained sluggish. Among EMDEs, slower

activity was also observed around U.S. cyclical troughs, although

to a lesser extent in commodity importers. The cyclical slowdown

in commodity exporters was amplified during the last two U.S.

recessions by declining commodity prices.

FIGURE 6B Activity around the U.S. recession of

2001

FIGURE 6A Growth during U.S. business cycles,

1960-2015

FIGURE 6C Activity around the U.S. recession of 2009

Sources: Haver Analytics, International Monetary Fund, Kose and Terrones

(2015), World Bank.

A. Cyclical component is defined as deviation from Hodrick-Prescott-filtered

trend.

B.C: The graphs show the cyclical component of GDP measured as the deviation

from trend GDP computed using a Hodrick-Prescott filter on seasonally adjusted

quarterly GDP around a trough in U.S. business cycle (t = 0) indicated by the

solid gray bar. Troughs are 2001Q4 and 2009Q2, as defined by the National

Bureau of Economic Research. The lines refer to the medians of 35 advanced

economies (excluding the United States) and 51 EMDEs.

8

May 2017

Recent Prospects Group Publications Global Economic Prospects - June 2017 (forthcoming)

Commodity Markets Outlook - April 2017

Global Economic Prospects - January 2017: Weak Investment in Uncertain Times

Commodity Markets Outlook - January 2017: Investment Weakness in Commodity Exporters

Commodity Markets Outlook - October 2016: OPEC in Historical Context

Recent World Bank Working Papers The Rise of the Middle Class and Economic Growth in ASEAN

Do Countries Learn from Experience in Infrastructure PPP? PPP Practice and Contract Cancellation

Does Oil Revenue Crowd out Other Tax Revenues? Policy Lessons for Uganda

What to Do When Foreign Direct Investment Is Not Direct or Foreign: FDI Round Tripping

Structural Change, Fundamentals, and Growth: A Framework and Case Studies

Migration and Cross-Border Financial Flows

The Economics of Forced Displacement: An Introduction

How Much Labor Do South African Exports Contain?

Financial Inclusion and Inclusive Growth: A Review of Recent Empirical Evidence

Consumption Smoothing and Shock Persistence: Optimal Fiscal Rules for Commodity Exporters

Recent World Bank Reports World Development Report 2017: Governance and the Law

Doing Business 2017: Equal Opportunity for All

TABLE A: Major Data Releases (Percent change y-o-y) (Percent change y-o-y)

Recent releases: April 23, 2017 - May 23, 2017 Upcoming releases: May 24, 2017 - June 22, 2017

Country Date Indicator Period Actual Forecast Previous Country Date Indicator Period Previous

France 4/28/17 GDP Q1 0.7 % 0.8 % 1.1 % Austria 5/24/17 IP MAR 3.1 %

Austria 4/28/17 GDP Q1 2.0 % 1.7 % 1.8 % Switzerland 5/24/17 IP Q1 -1.2 %

Spain 4/28/17 GDP Q1 3.0 % 3.0 % 3.0 % South Africa 5/24/17 CPI APR 6.1 %

UK 4/28/17 GDP Q1 2.1 % 2.2 % 1.9 % Japan 5/25/17 CPI APR 0.2 %

United States 4/28/17 GDP Q1 1.9 % 2.0 % Singapore 5/26/17 IP APR 10.2 %

Mexico 4/28/17 GDP Q1 2.7 % 1.8% 2.4% United States 5/26/17 GDP Q1 2.0 %

Indonesia 5/5/17 GDP Q1 5.0% 4.9% France 5/30/17 GDP Q1 1.1 %

Hong Kong 5/12/17 GDP Q1 4.3% 3.2% Sweden 5/30/17 GDP Q1 2.3 %

Thailand 5/15/17 GDP Q1 3.3 % 3.2 % Denmark 5/31/17 GDP Q1 2.3 %

Greece 5/15/17 GDP Q1 -0.5 % 0.2 % -1.1 % Poland 5/31/17 GDP Q1 4.0 %

Portugal 5/15/17 GDP Q1 2.8 % 2.1 % 2.0 % India 5/31/17 GDP Q4 7.0 %

Italy 5/16/17 GDP Q1 0.8 % 1.0 % 1.0 % Belgium 5/31/17 GDP Q1 1.2 %

Romania 5/16/17 GDP Q1 5.7 % 4.9 % Switzerland 6/1/17 GDP Q1 0.6 %

Czech Republic 5/16/17 GDP Q1 2.9 % 1.9 % Finland 6/1/17 GDP Q1 1.3 %

Netherland 5/16/17 GDP Q1 3.4 % 2.8 % 2.8 % Brazil 6/1/17 GDP Q1 -2.5 %

Poland 5/16/17 GDP Q1 4.0 % 3.1 % Greece 6/2/17 GDP Q1 -1.1 %

Euro Area 5/16/17 GDP Q1 1.7 % 1.7 % 1.7 % Australia 6/5/17 GDP Q1 2.4 %

Japan 5/17/17 GDP Q1 1.6 % 1.8 % 1.2 % South Africa 6/6/17 GDP Q1 0.7 %

Philippines 5/17/17 GDP Q1 6.4 % 6.6 % Hungary 6/7/17 GDP Q1 1.5 %

Malaysia 5/18/17 GDP Q1 5.6 % 4.5 % Turkey 6/12/17 GDP Q1 3.5 %

Germany 5/23/17 GDP Q1 1.7 % 1.7 % 1.7 % New Zealand 6/14/17 GDP Q1 2.7 %

9

May 2017

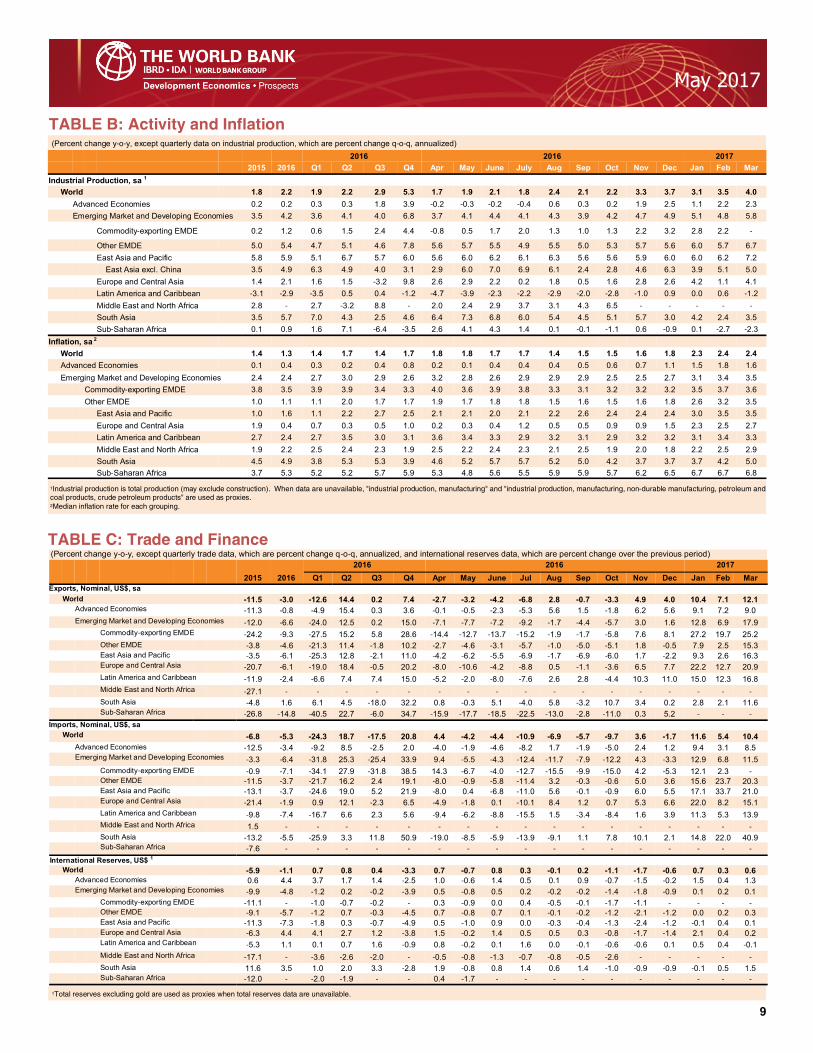

TABLE B: Activity and Inflation (Percent change y-o-y, except quarterly data on industrial production, which are percent change q-o-q, annualized)

1Industrial production is total production (may exclude construction). When data are unavailable, "industrial production, manufacturing" and "industrial production, manufacturing, non-durable manufacturing, petroleum and coal products, crude petroleum products" are used as proxies. 2Median inflation rate for each grouping.

TABLE C: Trade and Finance (Percent change y-o-y, except quarterly trade data, which are percent change q-o-q, annualized, and international reserves data, which are percent change over the previous period)

1Total reserves excluding gold are used as proxies when total reserves data are unavailable.

2016 2017

2015 2016 Q1 Q2 Q3 Q4 Apr May June July Aug Sep Oct Nov Dec Jan Feb Mar

Industrial Production, sa 1

World 1.8 2.2 1.9 2.2 2.9 5.3 1.7 1.9 2.1 1.8 2.4 2.1 2.2 3.3 3.7 3.1 3.5 4.0

Advanced Economies 0.2 0.2 0.3 0.3 1.8 3.9 -0.2 -0.3 -0.2 -0.4 0.6 0.3 0.2 1.9 2.5 1.1 2.2 2.3

Emerging Market and Developing Economies 3.5 4.2 3.6 4.1 4.0 6.8 3.7 4.1 4.4 4.1 4.3 3.9 4.2 4.7 4.9 5.1 4.8 5.8

Commodity-exporting EMDE 0.2 1.2 0.6 1.5 2.4 4.4 -0.8 0.5 1.7 2.0 1.3 1.0 1.3 2.2 3.2 2.8 2.2 -

Other EMDE 5.0 5.4 4.7 5.1 4.6 7.8 5.6 5.7 5.5 4.9 5.5 5.0 5.3 5.7 5.6 6.0 5.7 6.7

East Asia and Pacific 5.8 5.9 5.1 6.7 5.7 6.0 5.6 6.0 6.2 6.1 6.3 5.6 5.6 5.9 6.0 6.0 6.2 7.2

East Asia excl. China 3.5 4.9 6.3 4.9 4.0 3.1 2.9 6.0 7.0 6.9 6.1 2.4 2.8 4.6 6.3 3.9 5.1 5.0

Europe and Central Asia 1.4 2.1 1.6 1.5 -3.2 9.8 2.6 2.9 2.2 0.2 1.8 0.5 1.6 2.8 2.6 4.2 1.1 4.1

Latin America and Caribbean -3.1 -2.9 -3.5 0.5 0.4 -1.2 -4.7 -3.9 -2.3 -2.2 -2.9 -2.0 -2.8 -1.0 0.9 0.0 0.6 -1.2

Middle East and North Africa 2.8 - 2.7 -3.2 8.8 - 2.0 2.4 2.9 3.7 3.1 4.3 6.5 - - - - -

South Asia 3.5 5.7 7.0 4.3 2.5 4.6 6.4 7.3 6.8 6.0 5.4 4.5 5.1 5.7 3.0 4.2 2.4 3.5

Sub-Saharan Africa 0.1 0.9 1.6 7.1 -6.4 -3.5 2.6 4.1 4.3 1.4 0.1 -0.1 -1.1 0.6 -0.9 0.1 -2.7 -2.3

Inflation, sa 2

World 1.4 1.3 1.4 1.7 1.4 1.7 1.8 1.8 1.7 1.7 1.4 1.5 1.5 1.6 1.8 2.3 2.4 2.4

Advanced Economies 0.1 0.4 0.3 0.2 0.4 0.8 0.2 0.1 0.4 0.4 0.4 0.5 0.6 0.7 1.1 1.5 1.8 1.6

Emerging Market and Developing Economies 2.4 2.4 2.7 3.0 2.9 2.6 3.2 2.8 2.6 2.9 2.9 2.9 2.5 2.5 2.7 3.1 3.4 3.5

Commodity-exporting EMDE 3.8 3.5 3.9 3.9 3.4 3.3 4.0 3.6 3.9 3.8 3.3 3.1 3.2 3.2 3.2 3.5 3.7 3.6

Other EMDE 1.0 1.1 1.1 2.0 1.7 1.7 1.9 1.7 1.8 1.8 1.5 1.6 1.5 1.6 1.8 2.6 3.2 3.5

East Asia and Pacific 1.0 1.6 1.1 2.2 2.7 2.5 2.1 2.1 2.0 2.1 2.2 2.6 2.4 2.4 2.4 3.0 3.5 3.5

Europe and Central Asia 1.9 0.4 0.7 0.3 0.5 1.0 0.2 0.3 0.4 1.2 0.5 0.5 0.9 0.9 1.5 2.3 2.5 2.7

Latin America and Caribbean 2.7 2.4 2.7 3.5 3.0 3.1 3.6 3.4 3.3 2.9 3.2 3.1 2.9 3.2 3.2 3.1 3.4 3.3

Middle East and North Africa 1.9 2.2 2.5 2.4 2.3 1.9 2.5 2.2 2.4 2.3 2.1 2.5 1.9 2.0 1.8 2.2 2.5 2.9

South Asia 4.5 4.9 3.8 5.3 5.3 3.9 4.6 5.2 5.7 5.7 5.2 5.0 4.2 3.7 3.7 3.7 4.2 5.0

Sub-Saharan Africa 3.7 5.3 5.2 5.2 5.7 5.9 5.3 4.8 5.6 5.5 5.9 5.9 5.7 6.2 6.5 6.7 6.7 6.8

2016

2016 2016

2015 2016 Q1 Q2 Q3 Q4 Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar

Exports, Nominal, US$, sa

World -11.5 -3.0 -12.6 14.4 0.2 7.4 -2.7 -3.2 -4.2 -6.8 2.8 -0.7 -3.3 4.9 4.0 10.4 7.1 12.1

Advanced Economies -11.3 -0.8 -4.9 15.4 0.3 3.6 -0.1 -0.5 -2.3 -5.3 5.6 1.5 -1.8 6.2 5.6 9.1 7.2 9.0

Emerging Market and Developing Economies -12.0 -6.6 -24.0 12.5 0.2 15.0 -7.1 -7.7 -7.2 -9.2 -1.7 -4.4 -5.7 3.0 1.6 12.8 6.9 17.9

Commodity-exporting EMDE -24.2 -9.3 -27.5 15.2 5.8 28.6 -14.4 -12.7 -13.7 -15.2 -1.9 -1.7 -5.8 7.6 8.1 27.2 19.7 25.2

Other EMDE -3.8 -4.6 -21.3 11.4 -1.8 10.2 -2.7 -4.6 -3.1 -5.7 -1.0 -5.0 -5.1 1.8 -0.5 7.9 2.5 15.3

East Asia and Pacific -3.5 -6.1 -25.3 12.8 -2.1 11.0 -4.2 -6.2 -5.5 -6.9 -1.7 -6.9 -6.0 1.7 -2.2 9.3 2.6 16.3

Europe and Central Asia -20.7 -6.1 -19.0 18.4 -0.5 20.2 -8.0 -10.6 -4.2 -8.8 0.5 -1.1 -3.6 6.5 7.7 22.2 12.7 20.9

Latin America and Caribbean -11.9 -2.4 -6.6 7.4 7.4 15.0 -5.2 -2.0 -8.0 -7.6 2.6 2.8 -4.4 10.3 11.0 15.0 12.3 16.8

Middle East and North Africa -27.1 - - - - - - - - - - - - - - - - -

South Asia -4.8 1.6 6.1 4.5 -18.0 32.2 0.8 -0.3 5.1 -4.0 5.8 -3.2 10.7 3.4 0.2 2.8 2.1 11.6

Sub-Saharan Africa -26.8 -14.8 -40.5 22.7 -6.0 34.7 -15.9 -17.7 -18.5 -22.5 -13.0 -2.8 -11.0 0.3 5.2 - - -

Imports, Nominal, US$, sa

World -6.8 -5.3 -24.3 18.7 -17.5 20.8 4.4 -4.2 -4.4 -10.9 -6.9 -5.7 -9.7 3.6 -1.7 11.6 5.4 10.4

Advanced Economies -12.5 -3.4 -9.2 8.5 -2.5 2.0 -4.0 -1.9 -4.6 -8.2 1.7 -1.9 -5.0 2.4 1.2 9.4 3.1 8.5

Emerging Market and Developing Economies -3.3 -6.4 -31.8 25.3 -25.4 33.9 9.4 -5.5 -4.3 -12.4 -11.7 -7.9 -12.2 4.3 -3.3 12.9 6.8 11.5

Commodity-exporting EMDE -0.9 -7.1 -34.1 27.9 -31.8 38.5 14.3 -6.7 -4.0 -12.7 -15.5 -9.9 -15.0 4.2 -5.3 12.1 2.3 -

Other EMDE -11.5 -3.7 -21.7 16.2 2.4 19.1 -8.0 -0.9 -5.8 -11.4 3.2 -0.3 -0.6 5.0 3.6 15.6 23.7 20.3

East Asia and Pacific -13.1 -3.7 -24.6 19.0 5.2 21.9 -8.0 0.4 -6.8 -11.0 5.6 -0.1 -0.9 6.0 5.5 17.1 33.7 21.0

Europe and Central Asia -21.4 -1.9 0.9 12.1 -2.3 6.5 -4.9 -1.8 0.1 -10.1 8.4 1.2 0.7 5.3 6.6 22.0 8.2 15.1

Latin America and Caribbean -9.8 -7.4 -16.7 6.6 2.3 5.6 -9.4 -6.2 -8.8 -15.5 1.5 -3.4 -8.4 1.6 3.9 11.3 5.3 13.9

Middle East and North Africa 1.5 - - - - - - - - - - - - - - - - -

South Asia -13.2 -5.5 -25.9 3.3 11.8 50.9 -19.0 -8.5 -5.9 -13.9 -9.1 1.1 7.8 10.1 2.1 14.8 22.0 40.9

Sub-Saharan Africa -7.6 - - - - - - - - - - - - - - - - -

International Reserves, US$ 1

World -5.9 -1.1 0.7 0.8 0.4 -3.3 0.7 -0.7 0.8 0.3 -0.1 0.2 -1.1 -1.7 -0.6 0.7 0.3 0.6

Advanced Economies 0.6 4.4 3.7 1.7 1.4 -2.5 1.0 -0.6 1.4 0.5 0.1 0.9 -0.7 -1.5 -0.2 1.5 0.4 1.3

Emerging Market and Developing Economies -9.9 -4.8 -1.2 0.2 -0.2 -3.9 0.5 -0.8 0.5 0.2 -0.2 -0.2 -1.4 -1.8 -0.9 0.1 0.2 0.1

Commodity-exporting EMDE -11.1 - -1.0 -0.7 -0.2 - 0.3 -0.9 0.0 0.4 -0.5 -0.1 -1.7 -1.1 - - - -

Other EMDE -9.1 -5.7 -1.2 0.7 -0.3 -4.5 0.7 -0.8 0.7 0.1 -0.1 -0.2 -1.2 -2.1 -1.2 0.0 0.2 0.3

East Asia and Pacific -11.3 -7.3 -1.8 0.3 -0.7 -4.9 0.5 -1.0 0.9 0.0 -0.3 -0.4 -1.3 -2.4 -1.2 -0.1 0.4 0.1

Europe and Central Asia -6.3 4.4 4.1 2.7 1.2 -3.8 1.5 -0.2 1.4 0.5 0.5 0.3 -0.8 -1.7 -1.4 2.1 0.4 0.2

Latin America and Caribbean -5.3 1.1 0.1 0.7 1.6 -0.9 0.8 -0.2 0.1 1.6 0.0 -0.1 -0.6 -0.6 0.1 0.5 0.4 -0.1

Middle East and North Africa -17.1 - -3.6 -2.6 -2.0 - -0.5 -0.8 -1.3 -0.7 -0.8 -0.5 -2.6 - - - - -

South Asia 11.6 3.5 1.0 2.0 3.3 -2.8 1.9 -0.8 0.8 1.4 0.6 1.4 -1.0 -0.9 -0.9 -0.1 0.5 1.5

Sub-Saharan Africa -12.0 - -2.0 -1.9 - - 0.4 -1.7 - - - - - - - - - -

2017

10

May 2017

© 2017 International Bank for Reconstruction and Development / 4e World Bank

1818 H Street NW, Washington, DC 20433

Telephone: 202-473-1000; Internet: www.worldbank.org

Some rights reserved

4is work is a product of the sta6 of 4e World Bank with external contributions. 4e Qndings, interpretations, and conclusions expressed in this work do not necessarily re=ect the views of 4e World Bank, its

Board of Executive Directors, or the governments they represent. 4e maps were produced by the Map Design Unit of 4e World Bank. 4e World Bank does not guarantee the accuracy of the data included in this

work. 4e boundaries, colors, denominations, and other information shown on these maps do not imply, on the part of 4e World Bank Group, any judgment on the legal status of any territory, or any endorse-

ment or acceptance of such boundaries. Nothing herein shall constitute or be considered to be a limitation upon or waiver of the privileges and immunities of 4e World Bank, all of which are speciQcally reserved.

TABLE D: Financial Markets (Percent change y-o-y, except quarterly trade data, which are percent change q-o-q, annualized, and international reserves data, which are percent change over the previous period )

2016 2016 2017 MRV 1

2015 2016 Q2 Q3 Q4 Q1 May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

Interest rates and LIBOR (percent)

U.S. Fed Funds Effective 0.13 0.40 0.37 0.39 0.45 0.70 0.36 0.38 0.39 0.40 0.40 0.41 0.41 0.55 0.66 0.66 0.79 0.91 0.91

ECB repo 0.05 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

US$ LIBOR 3-months 0.32 0.74 0.64 0.79 0.92 1.07 0.65 0.65 0.70 0.81 0.85 0.88 0.91 0.98 1.03 1.04 1.13 1.16 1.19

EURIBOR 3-months -0.02 -0.26 -0.26 -0.30 -0.31 -0.33 -0.26 -0.27 -0.29 -0.30 -0.30 -0.31 -0.31 -0.32 -0.33 -0.33 -0.33 -0.33 -0.33

US 10-yr Treasury yield 2.12 1.84 1.75 1.56 2.12 2.44 1.80 1.64 1.48 1.56 1.63 1.74 2.12 2.50 2.44 2.42 2.47 2.29 2.24

German Bund, 10 yr 0.54 0.14 0.12 -0.07 0.18 0.35 0.16 0.01 -0.09 -0.07 -0.05 0.03 0.22 0.30 0.34 0.32 0.39 0.25 0.40

Spreads (basis points)

JP Morgan Emerging Markets 415 410 419 372 369 340 418 418 387 367 361 357 380 370 354 338 329 331 320

Asia 224 221 227 197 197 175 223 233 210 190 191 192 201 198 185 173 166 173 164

Europe 348 302 305 282 283 261 305 303 290 282 273 274 294 282 272 258 253 250 237

Latin America & Caribbean 540 537 551 477 475 445 552 541 496 473 463 453 491 481 463 442 431 431 422

456 517 538 508 467 396 530 545 540 492 493 487 475 438 416 396 377 350 359

Africa 415 518 548 461 436 389 552 546 494 448 440 441 444 422 401 387 380 400 373

Stock Indices (end of period)

Global (MSCI) 399 424 399 418 424 449 403 399 414 417 418 413 413 424 433 445 449 455 463

Advanced Economies ($ Index) 1663 1761 1653 1726 1761 1854 1675 1653 1713 1720 1726 1697 1712 1761 1792 1839 1854 1878 1907

United States (S&P 500) 2044 2258 2099 2168 2258 2363 2097 2099 2170 2171 2168 2139 2199 2258 2279 2364 2363 2384 2398

Europe (S&P Euro 350) 1474 1475 1339 1388 1475 1547 1399 1339 1376 1390 1388 1377 1388 1475 1463 1501 1547 1564 1587

Japan (Nikkei 225) 18817 19302 15576 16450 19302 18909 17235 15576 16556 16887 16450 17050 18604 19302 19035 19342 18909 19197 19755

Emerging Market and Developing Economies (MSCI)

794 861 834 903 861 958 807 834 879 894 903 908 863 861 909 936 958 978 1004

EM Asia 404 419 407 448 419 474 400 407 431 442 448 444 426 419 443 459 474 484 502

EM Europe 244 295 265 273 295 301 268 265 264 269 273 274 273 295 302 296 301 313 316

EM Europe & Middle East 211 248 225 233 248 252 225 225 227 232 233 232 230 248 253 249 252 259 262

EM Latin America & Caribbean 1830 2341 2269 2381 2341 2611 2038 2269 2359 2402 2381 2608 2330 2341 2516 2600 2611 2601 2537

Exchange Rates (LCU / USD)

Advanced Economies

Euro Area 0.90 0.90 0.89 0.90 0.93 0.94 0.89 0.89 0.90 0.89 0.89 0.91 0.93 0.95 0.94 0.94 0.94 0.93 0.89

Japan 121.00 108.80 107.96 102.36 109.63 113.63 108.97 105.34 104.09 101.31 101.69 103.72 108.90 116.28 115.03 112.96 112.91 110.02 110.99

Emerging and Developing Economies

Brazil 3.33 3.49 3.51 3.25 3.28 3.14 3.54 3.42 3.28 3.21 3.25 3.18 3.33 3.35 3.20 3.10 3.13 3.14 3.27

China 6.29 6.65 6.53 6.67 6.84 6.89 6.53 6.59 6.68 6.65 6.67 6.74 6.85 6.92 6.89 6.87 6.90 6.89 6.89

Egypt 7.70 10.12 8.87 8.87 14.71 17.82 8.86 8.87 8.87 8.87 8.88 9.25 16.34 18.56 18.68 17.01 17.76 18.09 18.11

India 64.14 67.19 66.91 66.94 67.39 66.97 66.93 67.29 67.18 66.91 66.74 66.73 67.60 67.86 68.06 67.01 65.83 64.52 64.55

Russia 61.34 67.06 65.84 64.61 62.95 58.67 65.96 65.01 64.43 64.93 64.48 62.57 64.25 62.03 59.76 58.42 57.83 56.53 56.50

South Africa 12.77 14.71 15.01 14.07 13.92 13.24 15.36 15.05 14.40 13.79 14.01 13.92 13.96 13.88 13.60 13.17 12.95 13.46 13.26

Memo: U.S. nominal effective rate (index)

114.7 119.7 117.5 118.4 122.5 123.4 117.8 118.2 118.9 117.8 118.6 119.7 122.9 124.9 124.8 123.0 122.5 121.6 120.5

1 MRV = Most Recent Value.

Middle East

TABLE E: Commodity Prices

2016 2016 2017 MRV 1

2015 2016 Q2 Q3 Q4 Q1 May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

Energy 2

65 55 56 57 64 68 57 59 57 58 58 64 59 68 69 69 65 67 67

Non-energy 2

82 80 81 82 83 86 81 83 82 82 81 81 83 84 85 87 85 83 83

89 89 91 91 90 91 91 94 92 91 90 90 90 89 91 91 89 88 88

Metals and minerals 2

68 64 62 64 71 78 61 61 64 65 64 65 73 75 76 79 79 75 73

Memo items:

Crude oil, average ($/bbl) 51 43 45 45 49 53 46 48 44 45 45 49 45 53 54 54 51 52 52

Gold ($/toz) 1161 1249 1260 1334 1221 1219 1261 1276 1337 1340 1327 1267 1238 1157 1192 1234 1231 1267 1267

Baltic Dry Index 711 676 613 736 994 938 623 608 707 675 826 870 1080 1031 913 760 1142 1229 954

Source: World Bank, World Bank Commodities Price Data (The Pink Sheet), Bloomberg

1 MRV = Most Recent Value.

2 Indexes, 2010 = 100.

Agriculture 2