guatemala investing for peace: a public investmernt revie · guatemala investing for peace: a...

TRANSCRIPT

Report No. 16392-CU

GuatemalaInvesting for Peace:A Public Investmernt ReviewJuly 15, 1997

Dcumentl A rit of theWr tBan.Litinl A'nicri'ia ind11t ( tirihbel'<,letuifi k t, l

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSCurrency Unit: Quetzal (Q)

US$1.0 =Q.5.91 (July 1, 1997)

GOVERNMENT FISCAL YEARJanuary 1 to December 31

GLOSSARY OF MAIN ACRONYMS AND ABBREVIATIONS

BCIE- Central American Bank for Economic Integration ISR Income TaxBEST Stabilization Bonds KfW German Aid Agency

BOG Central Bank of Guatemala MCTOP Ministry of Communications, Transport andCG Consultative Group Public WorksCIEN National Center for Research and Studies MOE Ministry of EducationCNEE National Commission for Power MOF Ministry of FinanceCONALFA National Literacy Commission MOH/MSPAS Ministry of HealthlMinisterio deCONAMA National Enviromental Commission Salud Publica y Asistencia SocialCOPECAS Permanent Commission for Coordinating NFPS Non Financial Public Sector

Water and Sanitation NGO Non-Governmental OrganizationCOVIAL Roads Commission NSPI National System of Public InvestmentDGC General Directorate of Roads PAYSA Water and Sanitation Program for the AltiplanoDGOP General Directorate of Public Works PHC Primary Health CareDTP Technical Budget Directorate PIP Peace Investment PlanEEGSA Electricity Enterprise of Guatemala PLADES Social Development PlanEMPAGUA Guatemala City Municipal Water POA Annual Operational Plan

Corporation PPA Power Purchase AgreementFIS/SIF Fondo de Inversi6n Social/Social PRONADE National Program for Self-Management in

Investment Fund EducationFODIGUA Guatemalan Fund for Indigenous Development SEGEPLAN Economic Planning SecretariatFOGUAMA Guatemalan Environmental Fund SIAF-SAG Integrated Financial Management System-FOGUAVI Guatemalan Housing Fund Government Auditing SystemFONAGRO National Fund for Agriculture SINISEP National Information System on PublicFONAPAZ National Peace Fund InvestmentFONATIERRA National Land Fund SRH Secretariat of Water ResourcesFOSUVI Housing Subsidy Fund TRS Tax Revenue SuperintendencyFSDC Solidarity and Community Development Fund UDAF Financial Administration UnitGIS Geographic Information System UEP Project Execution UnitGTZ German Technical Cooperation Agency UNEPAR Executing Unit for Rural Water ProjectsGUATEL Guatemalan Telecommunications Enterprise UNICEF United Nations International Children'sIDB Inter-American Development Bank Education FundIGSS Guatemalan Social Security Institute USAID United States Agency for InternationalINDE National Electrification Institute DevelopmentINFOM Municipal Development Institute VAT Value Added TaxIPP Private Owned Generators

Managers and Staff Responsible

Vice President : Mr. Shahid Javed BurkiDirector : Ms. Donna Dowsett-CoiroloLead Economist : Mr. Ian BannonStaff Member : Mr. Josd R. L6pez-Calix

TABLE OF CONTENTS

PrefaceRESUMEN EJECUTIVOEXECUTIVE SUMMARY

INTRODUCTION .................................................................. 1

Chapter I: AN OVERVIEW OF PUBLIC SPENDING ALLOCATION ...........................................3

A. Trends in Public Finance ................................................................. 3B. Spending Pattern .................................................................. 6C. Budget Execution ................................................................. 8

Chapter II: INSTITUTIONAL FRAMEWORK AND THE PUBLIC INVESTMENT CYCLE.... 10

A. The Investmnent Cycle: Main Issues ................................................................. 10B. The Market Approach to the Public Investrnent Cycle ................................................................ 11

Chapter III: PEACE AND THE RECOVERY OF SOCIAL INVESTMENT .. 14

A. Education ................................................................. 14B. Health ................................................................. 17C. Social Safety Net: The Social Funds ................................................................. 20

Chapter IV: BASIC INFRASTRUCTURE PROVISION: WATER, ELECTRICITY,TELECOMMUNICATIONS AND ROADS ................................................................. 24

A. Roads .24B. Power .26C. Telecommunications .28D. Water and Sanitation .30

TECHNICAL ANNEXES

ANNEX 1: The PIP and the Macroeconomnic FramneworkANNEX 2: The Budget: Terminology and ConceptsANNEX 3: Investment Programs in InfrastructureANNEX 4: Recent Legal ChangesANNEX 5: Water and Sanitation: The Institutional Nightmare

BIBLIOGRAPHY

STATISTICAL APPENDIX

TEXT TABLES

1.1 Total Expenditures of Central Government ........................................................... 81.2 Budget and Actual Expenditures of Central Government ......................................................... 811.1 Education Structure of Recurrent Expenditures . .......................................................... 5111.2 Coverage and Regional Distribution of Recurrent Expenditures in Primary Education .................. 15111.3 Regional Variations in Health Conditions .......................................................... 17111.4 Distribution of Health Expenditures by Level of Care ...... .................................................... 18111.5 Regional Distribution of Health Expenditures .......................................................... 19111.6 Health: Existing Investment Projects and Proposed PIP .......................................................... 20111.7 Basic Features FONAPAZ, FIS, FSDC .......................................................... 21

TEXT FIGURES

1.1 Level of Public Expenditures ........................................................... 41.2 Change in the Use of Treasury Bonds ........................................................... 51.3 Trend of Public Floating Debt ........................................................... 51.4 Public Expenditures in Central America ........................................................... 71.5 Allocation of Budget Among Major Expenditure Categories .........................................................71.6 Trends of Official Disbursements .......................................................... 9

TEXT BOXES

0.1 Peace Accords: Quantitative Targets: Socioeconomic and Agrarian Issues ....................................1I. 1 Macroeconomic Scenarios .......................................................... 31.2 Recent Trends in Domestic Debt ................................. 411.1 Expanding the SLAF Information System .............................. 13TI1.1 The Govermment's Education Strategy .............................. ; 16111.2 The Government's Health strategy 1996-2000 .............................. 18111.3 The New Approach to Local Service Delivery .............................. 23IV. 1 The Disincorporation of GUATEL .............................. 29IV.2 The Program Water Source of Peace ....................... 2........ 32

.hi .................. lx~LWG)wAiaragd4(dD N)hvcei ~miu~0f~to Gatemala duing hate 19 eadyi99, ... ..... .. eGve .nt(ScttaiaoPJmi~ Enwtie ~fl*w U omas~oio~ rwpot ndPuli Wrk, ne4v B'. q

Gaatemal~~), (7LIATEL,..N........... . O APZ iE))C...G m n h C r ~ n uwt%Ae Wo ~ ~~r.. .?11 .....~t serpr ee JnB mn av ejo L D~ ejeM ad

Annex l quad malys* Fac.........alat,wte) Cna U r, CnsktUIWOJPMP.ca4iin~~~~~)i Vent~~ara sgoechea (L4SW-wter); Cedar Fe ~~~~~~~~,dez(ConsuIman, infOJ.1~~~~~ar4on syse,n ....

Eduar.do Wieuner (Consrdtwu~~~~~ institutional Luues)~~~~ Peer reviewer.s were~~~~ RCrnA(~~er.(C~~a$.~~9u... . ..w....orI~,.Wee tahr (haper119 8enarJ(gie (Rta ocal,ChaterL.......arg P.....(.I

selecomnuanicationundheulth~~...... .

Guatemala: Investing for Peace:A Public Investment Review

Preface

This report was prepared by the World Bank as a contribution to the policy dialogue withthe Government and donors who are supporting development and the peace process in Guatemala.The World Bank initiated an active policy dialogue with the current Administration in March 1996with a presentation to the members of the new Cabinet of the Bank's report: Building Peace withRapid and Equitable Growth, Country Economic Memorandum (August 22, 1996; Report No.15352-GU). The main message of that report was that ensuring macroeconomic stability will becritical not only to accelerate growth, but also to finance peace and advance in the battle againstpoverty, since the modest growth of the past few years would not be sufficient to make a dent onpoverty. The Report was published in English in August 1996 and widely disseminated inGuatemala. Its preparation provided a valuable input for the negotiations of the Socioeconomicand Agrarian Peace Accord and contributed to the design of new Bank operations in the areas ofpublic sector modernization.

In mid-1996, as the Government was preparing for its first, formal Consultative GroupMeeting, it became clear that a key challenge to be faced after peace signing was improving themanagement of public expenditure and provision of basic infrastructure services. The verycomprehensive and detailed targets agreed in the Peace Accords could not be implemented withouta major restructurng of the Government's overall expenditure program. The Government and theInternational Monetary Fund requested that the World Bank undertake a study to makerecommendations in this area. GTZ, the German Technical Cooperation Agency, also contributedto its realization.

Preparations for the study were fully supported by the Economic Cabinet, and particularlyby the Ministries of Finance, Communications, Transport and Roads, Energy, Education andHealth, by SEGEPLAN, the Bank of Guatemala, GUATEL, FONAPAZ and INFOM, who alsoprovided valuable comments on drafts of this report. A formal discussion of an early draft of thereport was held with the Economic Cabinet in January 1997 and the final draft was cleared by theAuthorities in late May 1997. The conclusions reached during those discussions are reflected inthe final report. Throughout preparation of the report most of the key recommendations have beendiscussed and reviewed with key Government agencies. In many instances, the Government hasalready begun acting on these recommendations. To the extent possible, the report has tried to noteareas where Government efforts or actions are underway to address the constraints identified in theanalysis.

RESUMEN EJECUTIVO

La firma de la paz proporciona una oportunidad uinica para acelerar el crecimiento y reducir lapobreza.

i. El Programa Econ6mico y Social del Gobiemo 1996-2000 expone una estrategia para acelerar elcrecimiento y reducir la pobreza. Alcanzar la paz marc6 un hito clave para dicha estrategia, perosostenerla requiere de mas que el cese de violencia. La paz duradera requerira de un marcomacroecon6mico firme, asegurando el financiamiento apropiado de las necesidades relacionadas con la pazy redefiniendo la relaci6n entre los sectores puiblico y privado, para permitirle al sector privado encabezarel crecimiento econ6mico y fortalecer las funciones reguladoras y de subsidio del sector piublico mientras sealeja de las actividades directamente productivas. Este Reporte identifica las areas prioritarias del gastopuiblico para respaldar la paz. Enfoca las reformas actuales de modernizaci6n al sector puiblico y analiza elPrograma de Inversiones de la Paz (PIP), sometido por el Gobierno en la reuni6n de enero de 1997 alGrupo Consultivo (GC), y otras inversiones sectoriales prioritarias. El Reporte expone las inquietudes dela comunidad intemacional acerca de la importancia de orientar los recursos hacia las prioridadessectoriales claves, mientras asegura la absorci6n apropiada de los recursos extemos y una ejecuci6nefectiva y eficiente de la inversi6n piiblica.

Una pre-condici6n para la paz duradera es asegurar la estabilidad macroecondmica

ii. La baja y fluctuante recaudaci6n tributaria ha significado que las metas de estabilizaci6n han sidologradas en su mayoria a traves de un severo control del gasto piiblico. Aunque esto ha asegurado politicasfiscales relativamente adecuadas, la cobertura de la infraestructura social y basica sigue siendo la mas bajade la regi6n. Ademas, la calidad de los servicios puiblicos es extremadamente pobre y, debido a los gastosde la paz, existe un margen limitado para una mayor reducci6n del gasto piiblico.

iii. La d6bil recaudaci6n tributaria tambien se ha convertido en una carga inapropiada para la politicamonetaria en su objetivo de preservar la estabilizaci6n macroecon6mica. Una estricta politica monetaria,tendiente a contrarrestar los desequilibrios fiscales de 6pocas anteriores - basada en requerimientos deencaje con altas tasas y en operaciones de mercado abierto-aunada a las necesidades de financiamientodel gobierno satisfechas principalnente en el mercado domestico de corto plazo, han elevado las tasas deinteres domdsticas e incrementado la carga del servicio a la deuda interma. Como resultado, mAs de uno decada cuatro d6lares recaudados como impuesto-y mas de una quinta parte del total de gastos delGobiemo Central - es utilizado para pagar intereses de la deuda intema. En cuanto avance laimplementaci6n de la paz, reducir y reestructurar la deuda intema es esencial para crear un espacio fiscaladicional que permita financiar los gastos relacionados con la paz. Esto requiere de: (i) la aprobaci6n delas reformas a la Ley Organica del Banco de Guatemala (BG), la cual es necesaria para reducir loscoeficientes de encaje y, por lo tanto, las tasas de interes domesticas; (ii) la mejora de la administraci6nfinanciera por el Ministerio de Finanzas, respaldado por el Sistema Integrado de Administraci6n Financiera(SIAF), para evitar la tradicional emisi6n de bonos a corto plazo que cubren dificultades temporales decaja; (iii) seguir ampliando el plazo de vencimiento de los Bonos del Gobiemo; y (iv) mantener un enfoqueconservador en la politica de emisi6n de bonos en d6lares.

iv. El Gobiemo estA consciente de que para mantener la estabilidad macroecon6mica durante laimplementaci6n de la paz, se requiere de un ahorro interno considerablemente mayor. Esto es esencial nosolamente para financiar mayores gastos, sino tambien para crear suficiente soporte fiscal en caso de que elrespaldo externo se materializase mas lentamente de lo esperado. AdemAs, la carga tributaria podria bajar

ii Resumen Ejecufivo

en un escenario pasivo en 1997. Para incrementarla de 7.9 por ciento del PIB (8.5 por ciento del PIB conel impuesto temporal) en 1996 a las metas 1997-1999 establecidas en los Acuerdos de Paz, las medidasrequeridas incluyen: (i) cambios de politica tributaria urgentes (incluyendo alzas de los impuestos y laeliminaci6n de exenciones de impuestos) y cambios en la administraci6n tributaria (la creaci6n de laSuperintendencia de Administraci6n Tributaria-SAT); (ii) modificaciones adicionales al c6digo tributariopara fortalecer la SAT; (iii) la emisi6n de nuevas normas judiciales para respaldar el cumplimientotributario y la sanci6n efectiva por evasi6n fiscal. La disciplina fiscal tambien requiere de: (i) mantener lapolitica de gastos bajo control, mientras cambia el orden de prioridades hacia las metas de gastos sociales yde paz establecidas en los Acuerdos de Paz; (ii) ajustar las tarifas de servicios publicos para incrementar elahorro piiblico; (iii) proceder a desincorporar las empresas publicas y utilizar los recursos de su ventamayoritariamente para reducir la deuda intema (incluyendo las perdidas del BG); y (iv) en cuanto se hayareducido significativamente la deuda intema, considerar nueva legislacion apropiada para poner un limitemiximno, en forma permanente, al deficit del sector puiblico.

v. Guatemala tiene una carga de deuda externa baja, la cual debera manejar cuidadosamente. Luegoque el Gobierno anterior concluyera acuerdos bilaterales con cinco de los seis participantes de lareprogramaci6n del Club de Paris de 1994, Guatemala disfruta una posici6n firme en cuanto a su deudaexterna. Los indicadores de deuda han mejorado en los ultimos afios como resultado no solo de lareprogramaci6n de la deuda, sino de las politicas conservadoras y tradicionales de endeudamiento y lasdecrecientes tasas de interes mternacionales. Los donantes comprometieron aproximadamente $1.9 milmillones durante la reuni6n del GC para financiar el PIP y otras inversiones puiblicas. La absorci6n deestos fondos deberia estar acompafiada por una estrategia de endeudamiento externo prudente.

Es esencial incrementar el nivel y mejorar la calidad y eficiencia de la inversidn relacionada con lapaz

vi. Asegurar el uso eficiente de los recursos es tan esencial como elevar los ingresos tributarios, parapoder cumplir con los compromisos de paz. La paz requerira solucionar los problemas de pobreza y dedesigualdad social en Guatemala, especialmente en las areas rurales y con fuerte concentraci6n en laspoblaciones indigena y femenina. Esto requerira mAs que el simple incremento de los recursos. Aim conuna base tributaria domestica mas fuerte y el apoyo significativo de los donantes, sera necesario que elGobiemo equipare las prioridades de la agenda de la paz con los recursos disponibles. Balancearcuidadosamente estas prioridades es el primer reto del Gobiemro; puesto que el financiamiento puede nofluir de manera uniforme, lo que conllevaria tomar decisiones dificiles de asignaci6n de recursos.

vii. Un mayor nivel de inversiones requiere de: (i) la reducci6n de los costos recurrentes de su altaparticipaci6n actual del 79 por ciento del total de los gastos; (ii) el mantenimiento consistente de laasignaci6n efectiva de los fondos con el monto presupuestario original; (iii) el incremento de la capacidadde absorcion limitada del sector puiblico para desembolsar financiamiento externo; (iv) el asegurar lacompleta ejecuci6n de las inversiones presupuestadas, principalmente en los Ministerios de Salud y deEducaci6n; y (v) la descentralizaci6n operativa de la ejecuci6n hacia los fondos sociales, en primerainstancia, y las mumcipalidades en segunda instancia. Las demandas adicionales a corto plazo de lasnecesidades urgentes de la paz, generalmente no deberian ser cumplidas a costa de las necesidadesprioritarias de infraestructura social y bAsica a largo plazo-esenciales para el crecimiento sostenido y lareducci6n de la pobreza.

viii. Aunque las asignaciones de gastos a traves de los sectores han sido paralelas con los objetivosenunciados en la estrategia establecida por el Programa de Gobiemo-recibiendo las comunicaciones(carreteras), trabajo municipal (agua), salud y educaci6n, la porci6n mas grande-sus asignaciones dentro

Resumen Ejecutivo Hi-

de los sectores no han sido siempre consistentes con las prioridades econ6micas y sociales enunciadas porel Gobierno. Por ejemplo, el gasto en educaci6n pre-prirnaria y primaria es parcial a favor de la regi6nmetropolitana en relacion a las areas rurales mas pobres. Ocurre una situaci6n similar en salud, en cuantoa que los hospitales siguen recibiendo mas de la mitad del presupuesto de salud en detrimento del cuidadoprimario y preventivo, el cual tiende a beneficiar al pobre rural. La acumulaci6n de necesidades derehabilitaci6n de caminos primarios y secundarios justifica el esfuerzo actual del Ministerio deComunicaciones, Transportes y Obras Publicas (MCTOP) para rehabilitar esta red.

La implementacion del PIP requiere de un nuevo marco institucional e instrumentos de gesti6n

ix. Desde una perspectiva institucional, aunque el sector piiblico es pequen'o, es excepcionalmenteineficiente en el suministro de los servicios que ofrece, su administraci6n y sus funciones reguladoras. Lainversi6n puiblica ocurre dentro de cuatro bloques principales, con considerable autonomia y pocacoordinaci6n en todas las fases del ciclo de inversi6n: la infraestructura y la inversi6n social de losministerios sectoriales, la inversi6n en infraestructura de empresas puiblicas, y la inversi6n por los fondossociales y por las municipalidades. La sub-ejecuci6n de grandes presupuestos de la inversi6n puiblica y lapoca capacidad de desembolso de fondos extemos, son justamente el reflejo de problemas institucionalesacumulados durante muchos afnos, incluyendo: (i) con la excepci6n del MCTOP y el Ministerio deEducaci6n (ME), la ausencia de mecanismos institucionales para conectar el disenjo del proyecto con lasprioridades sectoriales, lo cual hace que las decisiones de inversi6n se tomen frecuentemente en funci6n dela disponibilidad de financiamiento externo, en vez de las prioridades sectoriales; (ii) la debil capacidad delos ministerios de linea (con la excepci6n del MCTOP y del ME) y SEGEPLAN de evaluar las inversionespropuestas; (iii) la ausencia de un ente regulador efectivo para la planificaci6n de inversiones, en partedebido a la dispersi6n de SEGEPLAN en demasiadas funciones; (iv) la falta de recursos tecnicos yfinancieros adecuados en SEGEPLAN y en el Ministerio de Finanzas (MF) para dedicarse a laplanificaci6n, monitoreo y evaluaci6n de inversiones, asi como para negociar y desembolsar fondosextemos efectivamente; (v) la centralizaci6n de la ejecuci6n presupuestaria en el MF, que conlleva a lainhabilidad de los ministerios de linea de operacionalizar las estrategias sectoriales; (vi) fondos decontraparte no siempre disponibles para respaldar la implementaci6n de los proyectos financiadosexternamente, lo cual define que las prioridades del gasto efectivamente sean determinadas por ladisponibilidad de efectivo del MF; (vii) deficiencias organizacionales y gerenciales dentro de los ministeriosde linea; (viii) incipiente coordinaci6n y control de la inversi6n por los fondos sociales y empresas estatales,lo cual conHleva a traslapes efectivos, ineficiencia de escala y asignaciones de inversi6n no-coordinadasentre sectores; y (ix) con la excepci6n del mantenimiento de caminos, escasa o ninguna participaci6n delsector privado en la ejecuci6n de proyectos.

x. La implementaci6n del Sistema Integrado de Administraci6n Financiera (SIAF) por el MF yalgunos ministerios de linea (MF, MCTOP, Educaci6n y Salud) ya esta dando respuesta a varios de estosproblemas mediante: (i) la centralizaci6n de las 6rdenes de compra y pago por cada ministerio en una solaunidad (UDAF), reduciendo los tranites de 130 a 19 pasos y eliminando un promedio de 600 chequesdiarios que previamente eniitia el tesorero de la naci6n; (ii) el control por cada ministerio, a trav6s de laUDAF y las Unidades de Control Interno (UDAI), de la formulaci6n, ejecuci6n y control de su propiopresupuesto mediante un programa mensual de caja acordado con el MF; y (iii) la formulaci6n delpresupuesto 1998 en base a una nueva metodologia que ha reducido la estructura programitica de 1,007actividades a 50 unidades. El SIAF es consistente con el programna de modernizaci6n del estado quetambi6n incluye: reformas a la administraci6n tributaria y el servicio civil, la desincorporaci6n de lasempresas del Estado, y la reforma de la estructura y el funcionamiento del Gobierno Central por medio dela Ley del Ejecutivo propuesta, la cual considera agrupar al Ministerio de Finanzas y SEGEPLAN en unsolo Ministerio de Economia

iv Resumen Ejecutivo

xi. El principio de centralizaci6n normativa con descentralizaci6n operativa requiere de un nuevoenfoque de mercado-basado no s6lo en nuevos arreglos institucionales sino en nuevos instrumentos degesti6n-dirigido hacia una asignaci6n 6ptima y eficaz de la inversi6n puiblica. Dicho enfoque deberiamejorar la calidad tecnica de los proyectos, y unificar y fortalecer los mecanismos recientes decoordinaci6n ad hoc-Gabinete ministerial social, Fondos Sociales-acordados para su preparaci6n yevaluaci6n entre ministerios, empresas puiblicas, fondos sociales y municipalidades en 1997. Este incluiria:(i) la creaci6n de un Sistema Nacional de Inversi6n Publica (SNIP) integrado por un Consejo de Ministros;(ii) la simplificaci6n de las funciones rectoras de SEGEPLAN en el SNIP en dos principales: lacoordinaci6n de la planificaci6n y politicas de pre-inversi6n, y la evaluaci6n de proyectos; (iii) elfortalecimiento t6cnico de SEGEPLAN para Ilevar a cabo PIP-anuales y plurianuales-consistentes conlas proyecciones macroecon6micas, el sistema (banco) de proyectos, el sistema de preinversi6n y el sistemade informaci6n geografica; (iv) el fortalecimiento de las unidades descentralizadas localizadas en losministerios sectoriales, consejos de desarrollo urbano y rural, fondos sociales, municipalidades y ONGs enel disenlo de inversi6n, ejecuci6n presupuestaria y monitoreo; (v) el aumento de la participaci6n del sectorprivado en la pre-inversi6n (en parte financiado por SINAFIP), ejecuci6n y evaluaci6n del proyecto,contratados extemamnente por el Gobiemo; (vi) la creaci6n de un nuevo subsistema de credito-externo einterno-publico en el MF que simplifique/mejore el marco mstitucional que rodea la contratacion deprestamos extemos y apoye la ventanilla uinica recientemente creada mediante la Comisi6nInterinstitucional para la Agilizaci6n de la Cooperaci6n Internacional (CIACI) y el tratamiento de "fasttrack" recientemente aprobado por el Congreso para las donaciones externas; y (vii) la creaci6n de unnuevo subsistema de informaci6n de mversi6n puiblica en el MF para pernitir el control de la ejecucionfinanciera y fisica de los proyectos por la futura Secretaria de Finanzas, SEGEPLAN y el SNIP. Los dosItimos subsistemas formarian parte de la ampliaci6n del SIAF.

Los Acuerdos de Paz estdn orientados a incrementar significativamente la eficiencia del gasto social

xii. El reto de mejorar las condiciones sociales requiere enfocar las deficiencias claves, tales como:mejorar la asignaci6n de fondos en linea con prioridades declaradas; mantener la consistencia del PIP conlos balances macroecon6micos y las prioridades de paz, y asegurar que las reformas institucionales (y suimplementaci6n) requeridas para alcanzar las metas de inversi6n social est6n bien enfocadas, alentandomayor participaci6n comunitaria y su sostenibilidad. Debe especificarse que criterios seran utilizados paraque la inversion sea consistente con las necesidades prioritarias del sector; lo cual se vuelve mias importanteque simplemente estimar cuanta inversi6n deberia hacerse a corto y mediano plazo.

xiii. El PIP propuesto para el sector de educaci6n es factible y consistente con las prioridadessectoriales, pero el de salud es excesivamente alto para la capacidad de absorci6n del Ministerio. En amboscasos, es esencial duplicar la capacidad de absorci6n de los fondos sociales para satisfacer loscompromisos de paz.

xiv. El PIP del sector educaci6n se propone: (i) ampliar la cobertura de los servicios educativos en lasareas rurales a traves de PRONADE, un modelo de escuelas primarias manejadas por la comunidad;programas de educaci6n pre-primaria acelerados; alternativas de modelos para el suministro modular de losservicios de educaci6n primaria y de becas para satisfacer las necesidades de grupos especiales; losprogramas de alfabetizaci6n y de post-alfabetizaci6n de CONALFA en espafiol y en lenguas indigenas; yprogramas especiales para grupos directamente afectados por el conflicto armado; (ii) fortalecer y ampliarla educaci6n bilingue, el adiestramniento de maestros, el adiestramiento en la administraci6n de escuelas delas juntas escolares, e iniciativas de educaci6n civil; y (iii) aumentar la inversi6n piiblica en la construcci6ny provisi6n de equipo de escuelas, pero ejecutados por los fondos sociales. La cartera de este sector esrealizable, pero se deben seguir varios pasos:

Resumen Ejecutivo v

* asegurar el puntual aporte financiero del MF de la contraparte de los fondos extemos;* Ilevar a cabo un esfuerzo de reestructuraci6n intema del Ministerio coherente y global orientado hacia

la redefinicion de sus funciones y nuevas responsabilidades en diversos niveles; y la focalizaci6n, comoprimer paso, en los programas prioritarios orientados hacia mejorar el suministro de los serviciosclaves;

* la descentralizaci6n efectiva de la ejecuci6n presupuestaria a traves de la pronta creaci6n de la unidadde administraci6n financiera (UDAF) en el ME para iniciar la implementaci6n del SIAF;

* la contrataci6n externa de servicios de consultoria para la ejecuci6n de proyectos, hasta que seaaprobada y puesta en vigor una legislaci6n nueva sobre el servicio civil;

* el fortalecimiento efectivo de la estructura administrativa y de ejecuci6n de PRONADE; y* la inversi6n en contrataci6n externa para infraestructura escolar de los fondos sociales y el sector

privado.

xv. El PIP propuesto para el sector salud tiene cinco objetivos clave, que son consistentes con la saludpreventiva y los cuidados primarios de la salud, prioridades de la estrategia sectorial y de los Acuerdos dePaz: (i) ampliar la cobertura a traves del sumninistro de un paquete basico de servicios; (ii) construir,rehabilitar y ampliar los puestos y centros de salud; (iii) proyectos de agua y saneamiento; (iv)rehabilitaci6n de la infraestructura y del equipo, asi como el desarrollo institucional de los hospitalesregionales; y (v) apoyo a la medicina Maya. Sin embargo, la cartera es demasiado ambiciosa, ya querepresenta cuatro veces mas su presente nivel de capacidad de ejecuci6n. Su reducci6n a un tamaflo masrealista deberia ser detenninada por:

* la probable contribuci6n de cada proyecto para con las metas estrategicas y las prioridades sectoriales;* la selecci6n de proyectos de hospitales que sean absolutamente esenciales para lograr las estrategias de

salud preventiva y cuidados prinmarios de la salud, asi como la puesta de atenci6n para evitar laduplicaci6n y mejorar la coordinaci6n entre las actividades del Ministerio de Salud (MS) y del IGSS;

* las implicaciones del costo recurrente incrementado de cada proyecto propuesto;* la efectiva contribuci6n de fondos extemos y de contraparte;* el progreso del reciente Programna de Mejoras de Servicios de Salud que incluye: (i) la reestructuraci6n

del MS, (ii) la introducci6n de un modelo recien desarrollado de suministro de servicios, y (iii) unnuevo programa administrativo para hospitales piublicos; y

* la efectiva descentralizaci6n de la ejecuci6n presupuestaria a traves de la creaci6n de la unidad deadrninistraci6n financiera (UDAF) en el MS y la contratacion extema de ONGs, el sector privado,cooperativas, municipalidades, y grupos comunitarios para la ejecuci6n de programas prioritarios.

xvi. Los fondos sociales tienen la capacidad potencial de duplicar el nivel de sus operaciones durantelos siguientes cuatro afnos al mismo tiempo que lograr una mas eficiente utilizaci6n de sus recursos. Sinembargo, ello solo es posible dentro de un nuevo marco institucional que redefina sus funciones yresponsabilidades, elimine la duplicaci6n y la fragmentaci6n, integre su sistema de informaci6n sobreinversiones al sistema SLAF y considere la conveniencia de transferir la responsabilidad de las inversionespublicas a los ministerios. Esto requerira que se tomen medidas para:

* evitar que siga la dispersi6n y la fragmentaci6n institucional a trav6s de la creaci6n de mas fondos;* desarrollar un modelo de suministro de servicio local que involucre directamente no s6lo a las

municipalidades y ONGs, sino tambien las poblaciones indigenas y pobres que seran las principalesbeneficiarias de los programas rurales;

* llevar a cabo una completa reestructuraci6n de sus tranites y procedimientos internos con el prop6sitode unificar las normas tecnicas entre los ministerios de linea y simplificar sus procedimientos;

vi Resumen Ejecutivo

* fortalecer y facilitar la participaci6n del sector privado en la preparaci6n de proyectos tanto a nivellocal (comunidad, municipalidad) como a nivel de ministerio de linea;

* ampliar los mecanismos de coordinacion existentes por medio de mas especializaci6n de cada fondo enciertas actividades, de un sistema de informaci6n geogrifica (SIG), de la unificaci6n de la informaci6nbAsica de demanda, y del establecimiento de un sistema periodico nacional de encuestas a hogares queayudaria a monitorear y evaluar las necesidades de las comunidades y el impacto de los proyectos.

La infraestructura bdsica actual existente es perjudicialpara la consolidacidn de la paz

xvii. La existencia actual de infraestructura bAsica en Guatemala es debil y claramente perjudicial parala aceleraci6n del crecimiento, la reducci6n de la pobreza imperante y, como consecuencia, la consolidacionde la paz. Mucho de este desempeflo pobre se le puede atribuir al papel dominante del Estado en elsuministro de servicios de infraestructura, la ausencia de mecanismos de mercado, y un marco institucionalque no es adecuado. Esto resulta en la sub-ejecuci6n, el mal disenio, el pobre monitoreo y evaluaci6n de losproyectos de inversi6n; deficiencias comunes que se comparten con el resto de la inversi6n piiblica.

xviii. Debido a su papel critico en facilitar el acceso a servicios y mercados, las carreteras son laprincipal necesidad de infraestructura del pais, seguida por agua y saneamiento (debido a su papel clave enlas condiciones de salud), energia y telecomunicaciones (debido a su impacto sobre el crecimiento). Elprograma de inversiones de carreteras estA bien enfocado y, dada la capacidad de ejecuci6n actual delMinisterio, de contarse con el financiamiento apropiado podria ejecutarse en un alto porcentaje; elprograma de energia continuara siendo poco apegado a la realidad, a menos que se encuentre una soluci6nlegal a los impedimentos para efectuar los ajustes tarifarios; el programa de telecomunicaciones se limita enla inversi6n hasta 1997, debido a la esperada desincorporaci6n de GUATEL durante 1997; y no existe unPIP realista para el sector de agua y saneanuiento, lo que muestra la falta de un marco institucionalapropiado y la ausencia de una estrategia sectorial global.

xix. El programa de inversiones para carreteras 1997-00, que no se limita al PIP, pone un enfasisadecuado en la rehabilitaci6n. Superar la rehabilitaci6n acumulada durante los ultimos 5 aAosrepresentaria un monto de $864 millones, de los cuales aproximadamnente una quinta parte ($170 millones)seria para los caminos de ZONAPAZ. A pesar de la significativa mejora en los niveles de ejecuci6n delMCTOP en 1996 (arriba del 90 por ciento), la inversi6n anual en carreteras es aun dos tercios de lo querequiere el programa propuesto, las agencias de gobiemo y las empresas nacionales de construcci6n notienen aun la capacidad financiera e institucional para ejecutar un programa tan ambicioso, los fondos delexterior son limitados y la participaci6n privada es auin baja. Inplementar dicho programa requiere no s6Lode financiamiento suficiente, sino de acciones (algunas ya bajo implementaci6n):

* La Direcci6n General de Caniinos (DGC) debe fortalecer su capacidad institucional en cuanto a lapreparaci6n de la planificaci6n de inversi6n sectorial y a la ampliacion de su esquema innovador decontrataci6n extema de empresas del sector privado pam darle mantenimiento a las carreterasprincipales (prirarias) y caminos secundarios. La inversi6n en caminos terciarios y ruralesprioritarios puede ser Ilevada a cabo por la DGC, pero pernitiendo la sub-contrataci6n a los fondossociales y gobiernos locales para Ilevar a cabo su ejecucion.

* Se requiere de mas coordinaci6n bajo el futuro SNIP, entre el MCTOP con el futuro Ministerio deEconomia, y entre el MCTOP y los fondos sociales, principalmente en lo que se refiere a laconstrucci6n, la rehabilitaci6n y el mantenimiento de caninos terciarios.

* Para poder darle apoyo a la implementaci6n de futuros tratados de libre comercio con America delNorte y Central, es prioritario que se continue con el financianmiento para la rehabilitaci6n de carreteras

Resumen Ejecutivo vii

(primarias) entre las fronteras. La construcci6n de by-pass (tramos ampliados) ya ha sido consideradapara facilitar el trafico.

* Para reducir los costos de rehabilitaci6n, tres estrategias complementarias estan siendo implementadasy debiesen fortalecerse: (i) permitir la participaci6n de empresas de construcci6n no-guatemaltecas enel proceso de licitaci6n; (ii) lograr una mayor descentralizaci6n que conlleve a proyectos de gastoscompartidos con los gobiernos locales; y (iii) mejorar (asfaltar) los caminos terciarios en base a unanalisis de caso por caso.

* El fortalecimiento tecnico del fondo para caminos (COVIAL) creado recientemente y el posible uso depeajes (e.g.,. Palin-Escuintla) son mecanismos apropiados para obtener recursos adicionales.

xx. A falta de un ambiente propicio para el ajuste tarifario, las compafiias electricas van canmino a labancarrota, luchando contra su actual ineficiencia, insolvencia y constantes crisis de racionamiento. Lacalidad del servicio continuarA en deterioro en vista de que no habra fondos para invertir. Debido a sudificil situaci6n financiera, las empresas puiblicas de energia no estan en la posici6n de contribuir con unprograma de inversi6n. Para poder mejorar el ambiente regulador, la reciente Ley de Electricidad requiere:

* normas reguladoras complementarias para apoyar la nueva Ley y promover la competencia en lageneraci6n, permitiendo el desarrollo de un mercado mayorista.

* poner atenci6n a la desesperada situaci6n financiera de la EEGSA y el INDE para lo cual seranecesario que la cuasi-aut6noma Conmisi6n de la Electricidad-parte del Ministerio de Energia-proceda a fijar y sostener las nuevas tarifas (incluyendo aquellas que aplican a EEGSA) y prepare unmecanismo transparente de actualizaci6n de tarifas, como estA provisto en la Ley, el que deberia sercapaz de afrontar retos legales futuros. Adicionalmente, ambas empresas deberian de: (i) reducir suscostos de personal; (ii) promover la participaci6n privada en la distribuci6n, ademas de la generacion;(iii) concluir con las negociaciones de deuda cruzada entre las empresas estatales y el Gobiemo; (iv)desincorporar sus activos; y (v) introducir terminos comerciales en la relaci6n con las municipalidadesque compran al por mayor, solicitandoles que le compren a empresas de distribuci6n privadas en vez deal INDE.

xxi. GUATEL no tiene proyectos de inversi6n previstos para 1997, ya que se asume que habrA unanueva administracion representando los intereses de los nuevos accionistas. Apoyado por un nuevo marcolegal, el sector de telecomunicaciones se prepara para una mayor competencia, lo que resultara en unamejor cobertura y calidad de servicio. El futuro precio de GUATEL sera determinado en parte por losrecientes ajustes tarifarios, los costos de reducci6n de personal y la cantidad que se pague enindenunizaciones.

xxii. Desde una perspectiva estrategica o de politica, s6lo recientemente se han iniciado esfiuerzos pordefinir un sector de agua y saneamiento de por si. Como resultado no existe aun un PIP efectivo y bienarticulado para dicho "sector". El Programa de Gobiemo contempla un incremento en la cobertura deservicios de agua en comunidades rurales con una inversi6n anual promedio de $300 millones. Sinembargo, esto seria 25 veces los niveles de inversi6n actual. En mayo de 1997, como un primer paso paraenfrentar este reto, el Gobiemno aprobo el documento "Politicas y Estrategias del Sector Agua Potable ySaneamiento" y decidi6 delegar a INFOM la gesti6n de su implementaci6n, incluyendo la ejecuci6n de losprogramas y proyectos de agua potable y saneamiento, y la coordinaci6n de la asistencia t6cnica yfinanciera con los ministerios, fondos sociales, entidades descentralizadas e intemacionales. Las medidasadicionales a considerarse incluyen:

viii Resunen Ejecutivo

* Como primer paso, completar la elaboraci6n de la estrategia de agua y saneamiento, cuyaadministraci6n estaria bajo la responsabilidad de una sola agencia (el nuevo Ministerio de RecursosNaturales o el INFOM). Tal estrategia deberia incluir: (i) una nuova ley de agua, cuyo anteproyectoesta bajo preparaci6n; (ii) la definici6n de una politica de tarifas nacionales, quizas basada en un"reglamento municipal" consensuado con las autoridades locales que INFOM propone como pre-requisito; (iii) una adecuada supervisi6n de su implementaci6n; (iv) el establecimiento de criterios deinversi6n y en la supervisi6n de la calidad de servicios de agua y de saneamiento a nivel nacional; y (v)en el seno del SNIP, y bajo coordinaci6n del INFOM, la formulaci6n de un programa de inversi6n delsector que asigne claras responsabilidades a cada entidad participante.

* El INFOM deberia ser reacondicionado para convertirse en el principal ente regulador, proveedor deasistencia tecnica y financiera del sector, a fin de apoyar a las municipalidades en la administraci6n yoperaci6n exitosa de los sistemas rurales de suministro de agua. El modelo Agua, fuente de paz, unasoluci6n de provisi6n de agua rural participativa y a bajo costo, con auditoria social compartida conlos fondos sociales y las comunidades locales podria ser el enfoque apropiado y iunico adoptado por elGobiemo. El INFOM y las municipalidades deberian solucionar la mayoria de los cuellos de botellaasociados a su implementaci6n (preinversi6n, el disen'o de acueductos y la ejecuci6n de proyectos) atraves de la subcontrataci6n al sector privado y el monitoreo descentralizado.

Medidas adicionales para desarrollar un PIP sostenible

xxiii. El Gobiemo ha tomado decisiones s6lidas para desarrollar un PIP sostenible, pero retosimportantes persisten. La mayoria de esos esfuerzos es descrita previamente, pero es valiosos anladiralgunos comentarios sobre iniciativas mas recientes: (i) una coordinaci6n muy estrecha se requiere entrevarios esfuerzos interinstitucionales dirigidos a elaborar un PIP Global en consistencia con el PIP del GC,un eventual PIP para Desarrollo Rural y los trabajos de la Comisi6n Interinstitucional de ProyeccionesMacroecon6micas, o severas inconsistencias inter e intra-sectoriales podrian surgir; (ii) la revisi6n porparte del SIAF del ciclo del proyecto por donante (identificaci6n-preparaci6n-negociaci6n-implementaci6n-evaluaci6n), no detallada aqui, debiese conducir hacia un mayor enfoque de demanda de proyectospreparados; (iii) una vez aprobada la nueva Ley del Ejecutivo, la creaci6n del SNIP requerira del apoyo deun entorno legal y reglamentario que establezca sus principios, objetivos, estructura, instrumentos,metodologias y normas; tal entorno, sin embargo, tambien deberia estar estrechamente vinculado a una(aum faltante) estrategia de descentralizaci6n del Estado; y (iv) el estado precario de los indicadoresecon6micos y sociales no permite un efectivo monitoreo del desarrollo de los proyectos y la evaluaci6n desu impacto, requiriendo la formulaci6n (en gestaci6n con el Instituto Nacional de Estadisticas) del"Programa de Indicadores Econ6micos y Sociales".

0

EXECUTIVE SUMMARY

The signing ofpeace provides a unique opportunity to accelerate growth and reduce poverty

i. The Government's Economic and Social Program 1996-2000 articulates a strategy to accelerategrowth and reduce poverty. Achieving peace was a key milestone for such a strategy, but sustaining itrequires more than the cessation of violence. Lasting peace will require a sound macroeconomicframework, ensuring appropriate financing of peace-related needs, and redefining the relationship betweenthe private and public sectors, to allow the private sector to lead economic growth and to strengthen thepublic sector's regulatory and subsidiary functions, while moving away from directly productive activities.This report identifies priority areas of public spending to support peace. It focuses on the on-going reformsaimed to modernize the public sector and, in particular, the Peace Investment Program (PIP) submitted bythe Government to the Consultative Group (CG) meeting in January 1997 and other investment sectorpriority needs. The report addresses the need to shift resources in line with sectoral priorities, whileensuring appropriate absorption of external resources, and an effective and efficient execution of publicinvestment.

Ensuring macroeconomic stability is a pre-condition for lasting peace

ii. inadequate and irregular tax revenues has meant that stabilization goals have been met largelythrough tight expenditure controls. Although this has ensured relatively adequate fiscal policies, social andbasic infrastructure coverage remains the lowest in the region. In addition, service quality is extremely lowand there is only limited scope for further reduction of public outlays.

iii. The public sector's weak revenue base has placed an undue burden on monetary policy to meet theGovernment's stabilization objectives. However, tight monetary policy to offset fiscal imbalances and theissuance of short-term government bonds to meet the financing needs of the Central Government, havepushed up domestic interest rates and increased the burden of servicing domestic debt. As a result, morethan one of every four dollars collected in tax revenues-and more than one fifth of total CentalGovernment spending-goes to service interest payments on domestic debt. As peace implementationprogresses, reducing and restructuring domestic debt is essential to create additional fiscal space to financepeace-related expenditures. This will require: (i) approving reformns to the Bank of Guatemala (BOG)Organic Law, which are necessary to reduce reserve requirements and, hence, domestic interest rates; (ii)improving financial management by the Ministry of Finance, supported by the Integrated FinancialManagement System (SIAF) to prevent issuing short-term bonds to cover temporary cash flow difficulties;(iii) continuing to lengthen the maturity of Treasury Bonds; and (iv) maintain a cautious approachregarding the further issuance of dollar bonds.

iv. The Government is aware that to maintain macroeconomic stability throughout peaceimplementation, a considerably greater domestic revenue effort is required. This is essential not only tofinance higher spending, but also to build a sufficient fiscal cushion in the event that external supportmaterializes more slowly than expected. Moreover, tax revenues could decrease under a passive scenarioin 1997. To raise the tax ratio from 7.9 percent of GDP (8.5 percent of GDP with the temporary tax) in1996 to tax targets set in the Peace Accords for 1997-99, required measures would include: (i) reforrns intax policy (including raising rates and eliminating exemptions) and tax administration (creation of theSuperintendency of Tax Administration-SAT); (ii) additional modifications to the tax code to strengthen theSAT; and (iii) issuance of new judicial norns to support tax enforcement and effective penalties for tax

ii Executive Summory

evasion. Fiscal discipline also requires: (i) keeping expenditure policy under control, while assigningpriority to social and peace expenditure targets set in the peace accords; (ii) adjusting tariffs of publicservices to raise public savings; (iii) disincorporating public enterprises and using the proceeds mainly toreduce domestic debt; and (iv) once domestic debt (including BOG losses) is reduced significantly,considering legislation to limit the size of the combined public sector deficit permanently.

v. Guatemala has a low external debt burden which it should manage carefully. After the previousGovernment concluded bilateral agreements with five of six participants in the 1994 Paris Clubrescheduling, Guatemala enjoys a sound external debt position. Debt indicators have improved in the lastfew years as a result not only of debt rescheduling, but of traditionally conservative indebtedness policiesand decreasing international interest rates. Donors pledged about $1.9 billion at the CG meeting to financethe PIP and other public investments. Absorbing such funds should be accompanied by a prudent extemalborrowing strategy.

Increasing the level and improving the targeting of peace-related investment is essential

vi. Ensuring an efficient use of increased resources is as essental as raising tax revenues in order tofulfill peace commitments. Peace will require addressing Guatemala's poverty and social inequality,especially prevalent in rural areas and strongly associated with ethnicity and gender. This will require morethan just increased resources. Even with a stronger domestic revenue base and significant donor support, itwill be necessary for the Government to match the priorities of the peace agenda with available resources.A careftl balancing of priorities is a first challenge for the Government; but funding may not flow evenlyand trade-offs will have to be made over time.

vii. An increased level of investment requires: (i) reducing recurrent costs from their current high shareof 79 percent of total spending; (ii) keeping the effective allocation of funds consistent with the originalbudget amount; (iii) increasing the public sector's limited absorptive capacity to disburse foreign financing;(iv) ensuring full execution of budgeted investments, mainly at the Ministries of Health and Education; and(v) effective decentralization of execution capacity toward the social funds and the municipalities.Additional short-term demands of urgent peace needs should not generally be met at the expense of longer-term priority social and basic infrastructure needs-the latter will be essential for sustained growth andpoverty reduction.

viii. Although expenditure allocations across sectors have been in line with the objectives spelled out inthe strategy set by the Government's Program-with communications (roads), municipal works (water),health and education receiving the largest shares-allocations within sectors are not always consistent withthe Government's stated social and economic priorities. Spending on pre-primary and primary education isbiased in favor of the metropolitan region relative to poorer rural areas. A similar situation occurs inhealth, with hospitals continuing to receive more than half of the health budget to the detriment ofpreventive and primary care which tends to benefit the rural poor. The rehabilitation backlog in primaryand secondary roads justifies the efforts currently being made by the Ministry of Communications,Transport and Public Works (MCTOP) to improve (rehabilitate) this network.

Implementing the PIP requires an improved institutional setting and new management tools

ix. From an institutional perspective, the public sector is small but it is exceptionally inefficient in its servicedelivery, management and regulatory functions. Public investment takes place witin four major blocks, withconsiderable autonomy and litde coordination among all stages of the investment cycle: infiastructure and socialinvestment by sector ministries, infiastructure investment by public enterprises, and investment by social funds

Executive Summary iii

and by the municipalities. Large budget underexecution of public investment and low capacity to disburseexternal funds reflect long-standing institutional problems, including: (i) absence of institutional mechanisms(except for MCTOP and the Ministry of Education) to link project design to sectoral priorities, whichmakes investment decisions frequently tied to the availability of external financing rather than sectoralpriorities; (ii) weak capacity by line ministries (except for MCTOP and the MOE) and SEGEPLAN to evaluateproposed investnents; (iii) absence of an effective regulatory body for investment planning, partly due toSEGEPLAN's dispersion over too many functions; (iv) lack of adequate technical and financial resources atSEGEPLAN and the Ministry of Finance (MOF) to devote to investment planning, monitoring and evaluation, aswell as to negotiate and disburse external funds effectively; (v) cenralization of budget execution at the MOF,leading to the inability of line ministries to operationalize their sector strategies; (vi) unreliable counterpartfunds to support implementation of externally-financed projects, which makes spending priorities effectivelydetermined by MOF cash availability; (vii) organizational and managerial deficiencies within line ministries;(viii) little control of investment by social funds and state enterprises, which leads to effective overlaps,inefficiencies of scale and uncoordinated investment allocations among sectors; and (ix) little or no participationof the private sector in project execution, except for road maintenance.

x. The on-going Integrated Financial Management System (SIAF) being implemented by MOF and otherline ministries (MCTOP, Education and Health) is addressing some of these problems by: (i) cetalzgpurchase orders in a single unit (UDAF), thus reducing the number of processing steps from 130 to 19 andeliminting the need for an average of 600 daily checks previously issued by the Treasury; (ii) UDAF and thebiternal Management Units (UDAI) in line ministries are taking control of the preparation, monitoring andexecution of their budgets, agreed with MOF; and (iii) preparing the 1998 budget with a new methodology thatreclassified 1,007 activities into 50 program units. SIAF is an important component of the state modernizationprogram that also includes: civil service and tax administration reforms, disincorporation of state enterprises andthe reform of the structure and functioning of the Central Government based on a new Law of the Executive; thelatter includes grouping MOF and SEGEPLAN in a single ministry.

xi. The principle of normative centralization with operative decentalization requires a new market approachto public investment based not only on new institutional arrangements, but also on new management tools, aimingtoward a more efficient allocation of public investment. Such approach should improve the quality of projects,while unifying and steghemng recently created ad hoc coordmation mechanisms-the Social Cabinet, socialfunds-agreed between line ministries, public enterprises, social funds and municipalities. The new approachwould include: (i) creation of a National System of Public Investment (NSPI) headed by a council of ministries;(ii) simplification of SEGEPLAN's normative functions under the NSPI to a minimum, focusing on coordinationof investment planning and policy, and project evaluation; (iii) technical strengthening of SEGEPLAN to preparePIPs-annual and multiannual-consistent with macroeconomic projections, the bank of projects, thepreinvestment system, the project evaluation system and the geographic information system; (iv) effectivedecentralization of investment design, budget execution and monitoring to the sector ministries, the social funds,NGOs and local organizations; (v) increased competition of the private sector for project pre-investment,execution and evaluation conracted-out by the Government; (vi) creation of a new subsystem of public-extenaland internal-credit at MOF to improve the institutional framework for the contracting of borrowed resources,including support for the "single window" recently created through the Comisi6n Interinstitucional para laAgilizacion de la Cooperaci6n Internacional (CIACI) and the "fust track" treatment recendy approved byCongress for the processing of grants; and (vii) creation of a public investment information subsystem to monitorthe financial and physical execution of projects by the future Secretariat of Finance, SEGEPLAN and NSPI. Thelatter two subsystems should be part of the on-going expansion of the SIAF.

iv Executive Summary

Peace accords aim to increase the efficiency of social spending significantly

xii. The challenge of improving social conditions requires addressing key shortcomings, such as:improving the allocation of funds in line with stated priorities, maintaining consistency of the PIP submittedto the CG meeting with macroeconomic balances and peace priorities, and ensuring that institutionalreforms (and their pace) required to meet social investment targets are well-focused, encourage increasedcommunity participation and are sustainable. Focusing on what criteria should be used to make investmentconsistent with sector priority needs, then becomes more important than just assessing how muchinvestment should be done in the short- and medium-tenn.

xiii. The proposed PIP for education is feasible and consistent with sectoral priorities, but the healthPIP is exceedingly high relative to the Ministry's absorptive capacity. In both cases, doubhng the socialfunds' absorptive capacity will be essential to fulfill peace commitments.

xiv. The education PIP aims to: (i) expand education coverage in rural areas through PRONADE(community-managed primary schools), accelerated pre-primary education programs, alternative modelsfor modular provision of primary education, targeted scholarships, CONALFA's literacy and post-literacyprograms in Spanish and indigenous languages, and special programs for groups directly affected by thearmed conflict; (ii) strengthen and expand bilingual education, teacher training, school administrationtraining for school boards (juntas escolares), and civil education initiatives; and (iii) increase publicinvestment in school construction and equipment, but executed by the social funds. This portfolio isfeasible, but several actions should be taken:

* ensure timely counterpart financing from MOF in line with availability of external funds;* comprehensive internal restructuring effort to define the functions and new responsibilities of the

various sector levels, concentrating initially on priority programs to improve key services;* effective decentralization of budget execution with the creation of the financial management unit

(UDAF) at MOE to start implementing the SIAF;* contracting-out consulting services for project execution, until a new civil service legislation is

approved and operational;* effective strengthening of PRONADE's management structure and execution; and* contracting-out investment in school infrastructure to the social funds and the private sector.

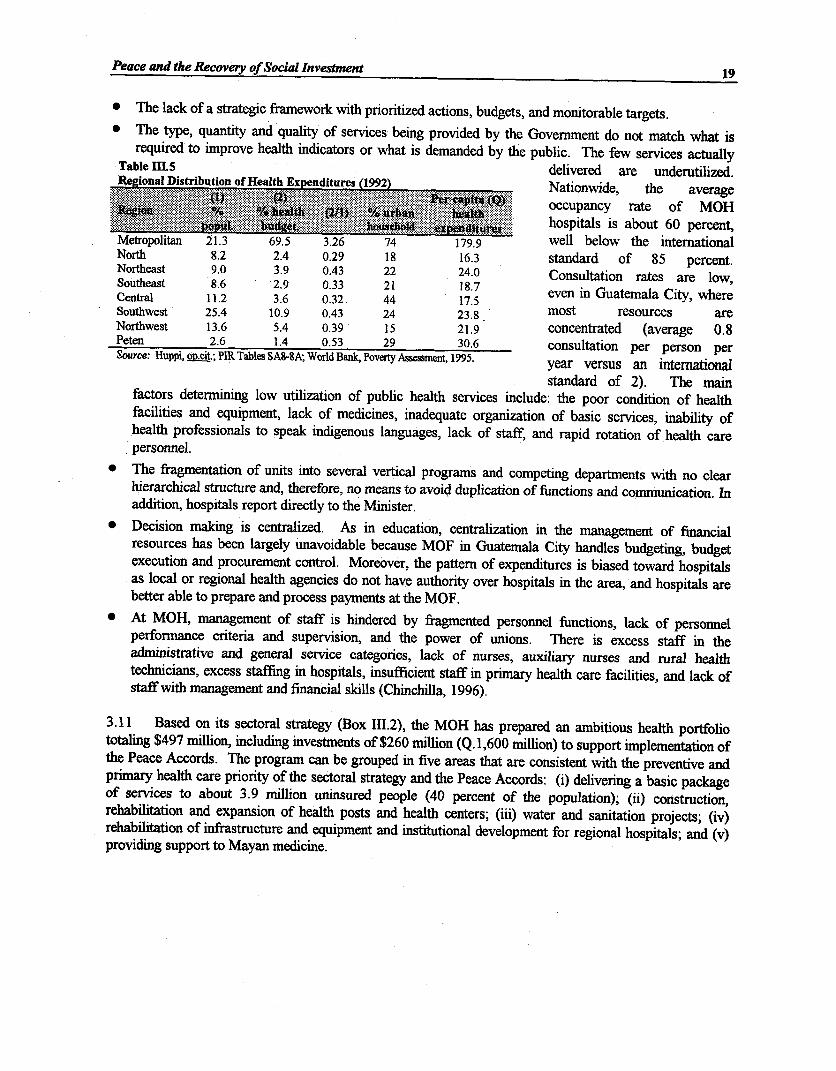

xv. The proposed PIP for health has five key objectives, which are consistent with the preventive andprimary health care priority of the sector strategy and the Peace Agreements: (i) expand coverage throughdelivery of a basic package of services; (ii) construction, rehabilitation and expansion of health posts andhealth centers; (iii) water and sanitation projects; (iv) rehabilitation of infrastructure and equipment andinstitutional development for regional hospitals; and (v) support to Mayan medicine. Its size, however, istoo large, at over four times current execution capacity. Reducing it to a more realistic size should bedetermined by:

* the likely contribution of each project to strategic goals and sectoral priorities;* selecting those hospital projects that are essential to the achievement of the preventive and primary

health care strategy, also avoiding duplication and improving coordination between MOH and IGSS;* the incremental recurrent cost implications of each proposed project;* the likely availability of counterpart and external funds;

Executive Summary v

* progress in the recent Health Services Improvement Program, including: (i) MOH restructuring, (ii)introduction of the newly-developed service delivery model, and (iii) a new management program forpublic hospitals; and

* effective decentralization of budget execution with the creation of the financial management unit(UDAF) at MOH and the contracting out to NGOs, private sector, cooperatives, municipalities, andcommunity groups the execution of priority programs.

xvi. Social funds have the potential to double the level of their operations in the next four years, whileachieving a more efficient utilization of resources. A new institutional framework, however, shouldredefine their functions and responsibilities, eliminating duplication and fragmentation, integrating theirinvestment information systems to the SIAF and considering the convenience of transferring theirinvestment portfolio to line ministries. This requires steps to:

* prevent further dispersion and institutional fragmentation by creating more funds;* develop a model of local service delivery that involves directly not only municipalities and NGOs, but

also indigenous populations who will be the main beneficiaries of rural programs;* re-engineer their internal procedures and processes to standardize technical standards with line

ministries and simplify their procedures;* strengthen and facilitate private sector participation in project preparation both at the local level

(community, municipality) and the line ministry;* strengthen coordination mechanisms through increased specialization of each fund, a geographic

information system (GIS), unification of basic demand information and establishment of a system ofperiodic national household surveys to monitor and evaluate community needs and project impacts.

T7he current provision of basic infrastructure is detrimentalfor peace consolidation

xvii. The provision of basic infrastructure in Guatemala is weak and clearly detrimental to flister growth,reduction of widespread poverty and, hence, peace consolidation. Much of this poor performance can beattributed to the dominant role of the state in the provision of infstructure services, the absence of marketmechanisms, and an inadequate institutional framework. As a result, underexecution, poor design, weakmonitoring and evaluation of investment projects are common deficiencies shared with the rest of publicinvestment.

xviii. Because of its critical role in facilitating access to services and markets, roads is the main infastructureneed of the country, followed by water (due to its impact on health), energy and telecommunications (due to theirimpact on growth). The investment program for roads is well focused and realistic, given the Ministry'scurrent execution capacity and likely financing availability; the program for energy will remain unrealistic,unless a solution can be found to the legal constraints on adjusting tariffs; the telecommunication programis limited to investment up to 1997, due to the expected disincorporation of GUATEL in 1997; and there isno PIP for water, due to the lack of an appropriate institutional framework and the absence of acomprehensive sector strategy.

xix. The 1997-00 investment program for roads, including the PIP, appropriately emphasizes rehabilitation.Overcoming the rehabilitation backlog in five years would represent a program of $864 million, of which aboutone fiffh ($170 million) would be in ZONAPAZ roads. Despite the significant improvetnent in the MCTOP'sexecution capacity in 1996 (above 90 percent), the present annual investnent in roads still is two-third of whatwould be required under the proposed program, Government agencies and the domestic construction sector do nothave the financial and institutional capacity to execute such an ambitious program, external funds are limited and

vi Executive Summary

private participation still is low. Investing in roads requires not just financing, but the following actions (some oftheim already under imnplmentation):

* DGC should stengthen its institutional capacity in preparing sector investnent planning and in expanding itsinnovative scheme of contracting-out private sector participation in the maitenance of the main highways(primary) and secondary roads. Investment in key tertary and rural roads could be undertaken by DGC, butallowing subcontracts to social funds and local governments to carry out their execution.

* improved coordination under the NSPI, between MCTOP and the future Ministry of Economy, and betweenMCTOP and the social funds is required, maily for tertary roads (construction, rehabilitation andmaintenance);

* to support the implementation of future free trade agrements with North and Central America, continuerehabilitation of highways (primary) connecting national borders, which could include construction ofbypasses (enlarged roads) to facilitate border traffic;

* to reduce rehabilitation costs three complementary strategies are being implemented and should bestrengthened: (i) non-Guatmmlan construction firms should be allowed greater participation in biddingprocesses; (ii) increased decentzlhzaton should provide opportunities for joint-financing of projects withlocal goverunments; and (iii) selected upgrading (paving) of tertiary roads; and

* technical strengthening of the recently created road fund (COVIAL) and the possible use of tolls (e.g., Palin-Escuintla) could help to raise additional resources.

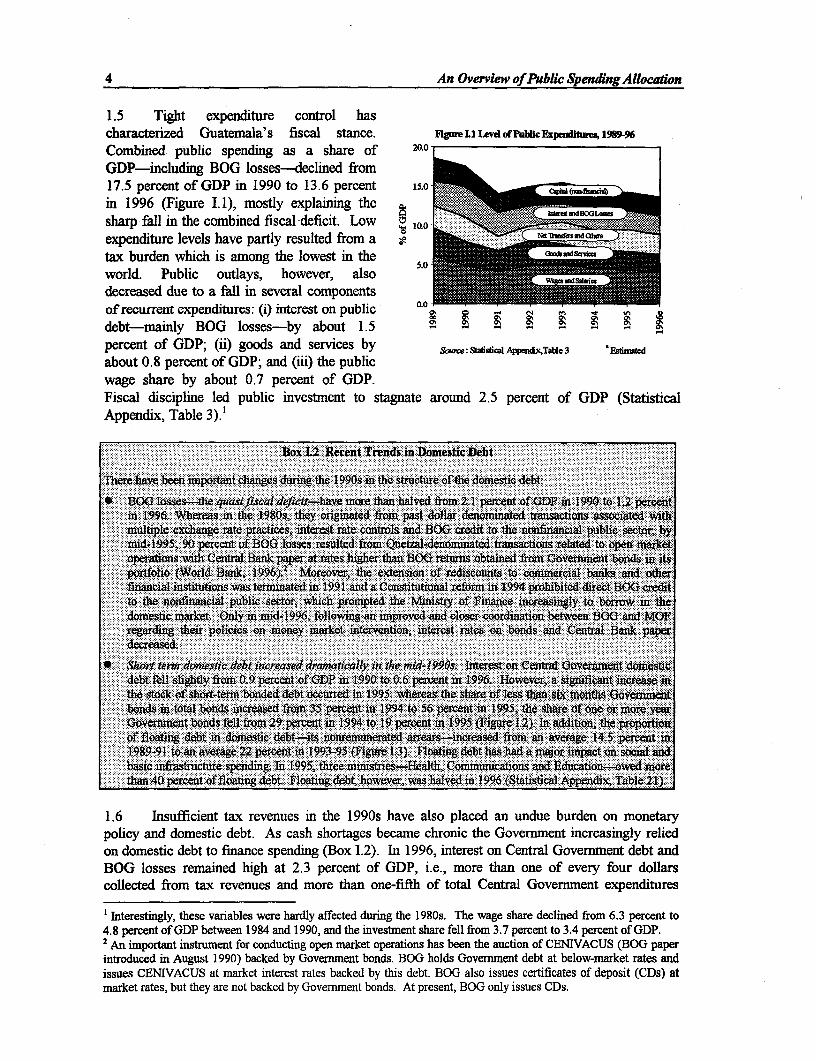

xx. Due to problems in implementing appropriate tariff adjustments, the electricity companies are headingtoward bankruptcy, struggling with their current inefficiency, insolvency and recurrent bouts of rationing.Service quality will continue to deteriorate as there will be no funds to invest. Given their difficult financialsituation, the public power companies are in no position to contribute to an investment program. To improve theregulatory environment, the recently-approved Electricity Law requires:

* complementary regulatory norns to support operation of the new Law, to promote competition in generationand allow the development of a wholesale market;

* addressing the difficult financial situation of EEGSA and INDE, which will require that the quasi-autonomous Commission of Electricity-it is part of the Ministry of Energy-set new tariffs (including thoseapplied to EEGSA) and prepare a transparent tariff setting mechanism that would be able to sustain futurelegal challenges. In addition, the two companies should: (i) reduce personnel costs; (ia) promote privateparticipation in distribution, in addition to generation; (iii) conclude cross-debt negotiations between bothstate firms and the Government; (iv) disincorporate their assets; and (v) introduce commercial terms in therelationship with municipalities that buy in bulk, requesting them to buy from private distribution companies,rather than from INDE.

xi. GUATEL has no investment projects contemplated after 1997, because it is assumed that it will beoperating under new management representing the interests of new shareholders and workig in a competitiveenvironment. Supported by a new legal franmework, GUATEL is preparing for its disincorporation and privatesector participation. The future price of GUATEL will partly be determined by recent tariff adjustments,reduction of personnel costs, and the amount of severance payments.

xxn. From a strategic or policy perspective, efforts have started only recently to define a water and sanitationsector as such. As a result, there is as yet no effective and well-articulated PIP program. The Government'sProgram aims to increase coverage of water sevices in rural communities with an estmated average annualinvestment of $300 million. However, this would be 25 times current investnent levels. As a first step, on May1997 the Government approved the document "Politicas y Estrategias del Sector Agua Potable y Saneamiento"

Executive Summary vii

and delegated to INFOM (the Municipal Body) the managemnent of its imnplementation, including the execution ofwater and sanitation programs and projects, and the coordination of fiancial and technical assistance with lineministries, social funds, decentalized institutions and international orgamzations. Additional neasures to beconsidered include:

* the first step is the conpletion of a water and sanitation strategy, whose management would be responsibiltyof just one agency (the new Ministry of Natural Resources or INFOM). Such a strategy should include: (i)passage of a new water law, whose draft is being prepared; (ii) definition of a national tariff policy, perhapsbased on a reglamento municipal (as proposed by INFOM) previously agreed in consensus with localauthorities; (iii) adequate supervision of its implementation; (iv) establishing criteria for investing in andsupervising the quality of water and sanitation services nationwide; and (v) under the NSPI, and coordinatedby INFOM, the formulation of a sector's investment program that assigns clear responsibilities to each entityinvolved; and

* INFOM should be reengineered to become the main financial and technical body to support municipalities inthe administation and operation of rural water supply systems. Agua, fuente de paz, a low-cost rural watermodel, with shared responsibility with the social funds and local communities, seems an appropriate andunique approach. INFOM should provide continuous training to the municipalities, while most of its currentbottlenecks (preinvestment, the design of aqueducts and project execution) could be solved throughsubcontratg to the private sector and decenthalized monitoring.

Further steps to inmpement a sustainable PIP

xxiii. The Govenmment has taken solid steps to develop a sustainable PIP, but important challenges remain.This report has analyzed the key ones, but some additional points on recent initiatives should be noted: (i) closecoordination is required among several interinstitutional efforts working on a Global PIP consistent with the CG-PIP, an eventual PIP for Rural Development and the Commission worldng on macroeconomic projections; (ii) adetailed review under the SIAF framework of the project cycle by donor (identification-preparation-negotiation-implementation-evaluation), which is not detailed here, should lead to a more demand-driven approach for publicinvestment; (iii) once the new Law of the Executive is approved, the creation of NSPI will require a supportinglegal and regulatory framework that sets its principles, objectives, structure, instruments, methodologies andnorms; such a framework, however, should also be closely related to a much-needed decentralization strategy;and (iv) the lack of a good economic and social data base prevents any effective monitoring of projectimplementation or evaluation of and requires the formulation (under preparation by the National Data Istitute)of the Programa de Indicadores Econ6micos y Sociales.

m

INTRODUCTION

1.1 The signing of a Peace Agreement presents Guatemala with a unique opportunity toachieve rapid and equitable growth, while pursuing an ambitious agenda of structural reforms-focused on the modernization of the state, fulfilling its commitments to the peace process andsolving long-standing macroeconomic and social imbalances. Having the largest economy ofCentral America and abundant natural resources, the lack of a stable political, social and economicenvironment had prevented Guatemala from reaching the necessary pre-conditions for sustaineddevelopment. An almost uninterrupted military rule until the nid-eighties, three decades of warfarebetween successive Governments and the guerrilla, and a sharply segmented society were majorobstacles to faster growth and sustained development. Peace should help not only to strengthendemocracy and consolidate economnic reform, but to address long-standing challenges, such as lowhuman capital accumulation, poor social indicators, a highly skewed income distribution, a weakand inefficient state and an outdated economic infrastructure.

1.2 Takig advantage of such a XA 1vhistorical opportunity needs more thanthe cessation of violence. The athcomprehensive set of peace accords - w 9 au 1:99.signed is only a first step in addressing Pb - d ( prGuatemala's development needs, but its bM tie anf i a n 20 wiimplementation is another story. This - 9 _ s 0 e xe* ited.lX _ threport addresses public sector issues ..> ... i.. rthat are critical to its success, such as: e t o flow domestic savings-partly due to - bi .netmet... p 2

poor tax collection-insufficient and - .974 99.misallocated spending, slow absorption Corg.Edcin:i)aclteteacssotheof external fnds and weak project - teexecution capacity. Solving these - Xo r in 2000.problems is urgent, since the number of X (i 199 i commitments made in the peace accords - b - t ber t y 2 ais impressive (more than 600), includinga series of key quantitative targets (Box - l -uli0. 1). ~fddLeoa i 0pretices nteeeuo

1.3 Peace consolidation also . 00.i..t..requires social and basic nfrastructureinvestment. A fundamnental tool that the i ots.(i) raete l Government has designed to support d9peace accord commitments is an . - (j) t aambitious Peace Investment Program -- i xeud y(PIP).' The PIP was submitted to the b : iidonor community in the Consultative A ( e mbpGroup meeting held in Brussels inmP 5sgt i)rdueam nnbr y3January, 1997. Most PIP investments pare located in ZONAPAZ, the regioncontaining the nine departments mainly affected by the conflict and where 57 percent of the

1 Since early-1997, the Govemrnment has also been prepaing a Global-PIP and a PIP for Rural Development in agreementwith the CG-PIP.

2 Introducion

population-overwhelmingly rural, poor and indigenous-lives. The PIP comprises a set ofprojects under preparation, negotiation or execution and is organized in four areas:* Reinserfion and Demobilization, which includes three sub-programs: (i) displaced

populations, (ii) demobilization of ex-combatants, and (iii) community development.* Integral Human Development, which includes eight sub-programs: (i) emergency needs for the

poor, (ii) indigenous people, (iii) education, (iv) health, (v) social security, (vi) housing, (vii)basic inrastructure, and (viii) women participation.

* Sustained Productive Development, which includes four programs: (i) labor reform andtraining, (ii) rural development, (iii) a Land Fund, and (iv) support for investment, employmentand exports.

* Modernization of the State, which includes eleven programs: (i) legal and constitutionalreforms, (ii) human rights, (iii) modernization of the executive, (iv) modernization of theLegislative, (v) modernization of the Judiciary, (vi) civil security, (vii) tax administration, (viii)development councils, (ix) municipal strengthening, (x) property registry and cadaster, and (xi)support to the Secretariat of Peace.

1.4 Comparing projections of two alternative PIP scenarios for 1997-2000 (Box 0.1 andAnnex 1) leads to the following conclusions:* Moving from a low case to a high case scenario will critically depend on the Government's

ability to improve its savings performance-mainly through raising tax revenues and publicutility rates-and to disincorporate public enterprises (while paying-off domestic debt).

* Rapid growth with stability is achievable under a high case scenario only. In case domesticsavings remain low and minimum compulsory peace outlays have to be financed, peacecommiitments would not be fully met, and the economy would continue to face a weak fiscalbase and external position, somewhat vulnerable to adverse external developments.

* Progress on structural reforms-especially to modermize the institutional and legalframework and improve the delivery of public services-will be critical to consolidate peaceand effectively use the increasing volume of external support promised to assist theGovernment meet its peace comnitments. In the short-term, however, quick-disbursingexternal financing would support Government efforts while longer-term structural andinstitutional reforms take hold.

1.5 The donor community pledged a significant amount (about $1.9 billion for 1997-2000) ofexternal aid to finance the PIP, but also expressed several concerns. This report addresses some ofthem, mainly the importance of: (i) a sound macroeconomic framework for a sustainable PIP(Chapter I); (ii) an adequate institutional framework to ensure an efficient absorption ofinternational cooperation and an efficient and effective execution of public investment (Chapter II);and (iii) ensuring that social (Chapter III) and basic infrastructure (Chapter IV) investment areincreased and more efficiently allocated to key inter-and intra-sectoral priorities, in such a way thatthe peace dividend is widely shared within Guatemalan society. The donor community alsoemphasized the need to enhance donor coordination and develop appropriate mechanisms to ensurea regular monitoring and verification of peace accords implementation.

CIAPTER I

AN OVERVIEW OF PUBLIC SPENDING ALLOCATION

1.1 Macroeconomic stability is a precondition for sustained peace and faster growth. Themacroeconomic environment needs to be strengthened in three key areas: enhanced public revenuemobilization to finance peace commitments, better control over domestic liquidity, and a sounderexternal position to reduce dependence on volatile capital flows (World Bank 1996). Meetingpeace commitments and implementation of the PIP will exert considerable macroeconomicpressures, especially if domestic financing Seia .is =iadequate, expectations on the peacedividend arising from a reduction of ..:..T o m 'ed .e s s aedmilitary expenditures prove to be .. :leffert e : tof .eoptimistic, and exteral support prse a soum1. a. Iroe.nomic .......framew.rk.(A"'ex">.materializes more slowly than expected. .OhighIIase e threiemnt necess.y.t..meet mos.Under these conditions, it will be important i tlaepeace accords under'aveiy active stance. Then.. .to ensure strict control of public spending -ethe i,'p'.,atio's',f p.r,.,,t,s i,o.e,.,'s,ii

while continuing efforts to improve the poicy sn where y

public sector's capacity to efficiently .........e-.s pa rt... -allocate and execute the public investment tA ih .. rd.. c'oec o X s-whie IW1y iipeHntn h I n ec omtetprogram. id :

1.2 This chapter depicts overall blic developments in public finance, with a R ofover $ mi perfocus on public expenditure issues that will * :-eedn th. isin 'i j-son p - - - ises............. t......be critical for consohdating peace. It : . eti.det, asw as aoassesses public expenditure patterns- q...tyofsproisio;mainly in the social and basic * givng. pj'" '' ''' n ' ., ':. winfrastructure sectors-stressing the need n: vesimei o.er es, ni e jhe. i wto: (i) ensure a prudent overall fiscal liS0, Wp n .r-wth..

* epnigad tngmr deiairno envelope for imnplementation of the peace at'epcayovrulgteistutnlfamwkaccords, so as to prevent the emergence of rt to the pblemacro imbalances; (ii) reduce andrestructure domestic debt; (iii) shift outlays toward social and basic infrastructure investment, (iv)increase the level of public investment execution; and (v) improve capacity to absorb externalfinancing, while maintaining a prudent external debt management strategy.

A. Trends in Public Finance