home sellers guide for listing your home · home sellers guide for listing your home ... we will...

TRANSCRIPT

1

Home Sellers Guide for Listing Your Home

Prepared Exclusively By:

Aldridge & Southerland Realtors Our Family Serving Yours for Over 30 Years!

No One in Pitt County Has Sold More Homes!

Office: 252-756-3500 Toll Free: 1-800-541-5182

Fax: 252-756-4159 Email: [email protected]

Visit Us at: www.aldridgeandsoutherland.com

226 Commerce St. Greenville, NC 27858 04/12

No One in Pitt County Has Sold More Homes!

2

3

Listing Presentation

Outline

Aldridge & Southerland Marketing Plan 1-2

Our Guarantee To You 3

Aldridge & Southerland Results 4

Residential Odds of Selling 5

Total Closings in MLS by Month 6

Absorption Rates 7

ListHub Advertising 8

Realtor.com 9

www.aldridgeandsoutherland.com Total Views 10

Pricing Real ity 11

How Your Agent Will Arrive At A Price Range 12

A Few Words On Condition 13-14

First Impressions Staging, Inc. 15

Notice To Sellers 16

Forty Tips for a Faster Sale 17-19

How to Prepare for a Showing in Ten Minutes or Less... 20

Need Relocation Assistance? 21

Inspectors 22

Repair & Service Contractors 23-27

Home Owners Insurance Companies 28

Closing Attorneys 29

Glossary of Terms 30-33

4

1

Aldridge & Southerland

Marketing Plan

1. Pre –Inspection – We will ask you to have a home structural inspection to reduce your risk of any surprises when negotiations with a buyer and to make your transaction smoother. We

will refund to you the cost of the home structural inspection at closing as part of our service to you.

2. Staging – We will pay for a consultation for you with an accredited Home Stager. Staged homes sell faster and for more money than non-staged properties. A neutral and updated look appears to a larger buyer pool. Photos of staged homes look better in Print and Internet

advertising.

3. Pricing – We will assist you with pricing your home based on a competitive market analysis. This will help you to set the best price on your home so that it will sell within your time frame.

4. Relocation Program – Information will be put in Aldridge & Southerland Relocation pack-ages that go to major employers. This will increase your exposure to relocating buyers.

5. Full Page Ad in Daily Reflector—Your home will be featured as a “Fresh on the Market”.

6. Aldridge & Southerland Sign – We will place the recognizable sign (35 years) in your front

yard.

7. Mobile App Sign Rider—This sign rider will give mobile phone users a direct access to our website and your home while they are in front of your property. They will be able to access all information including interior pictures.

8. Color Flyer – We will have your home photographed and a full color flyer prepared.

9. Flyer Box – We will place a flyer box with the Aldridge & Southerland sign. We will provide you with extra flyers to refill the box.

10. Lock Box – We will place a lock box on your property to increase showings and provide you

with the security of knowing who has shown your home.

11. Multiple Listing Service (MLS) – We will enter your homes information into the MLS, giving your home exposure to 220 Realtors in Pitt County.

2

Aldridge & Southerland

Marketing Plan..Continued

12. Internet – Our website, www.aldridgeandsoutherland.com, averages 90,000 views a

month. We have all of our homes in an enhanced Company Showcase with Realtor.com.

We are averaging 148,500 a month. All of our homes are features on the following web-sites. Google Maps, Zillow.com, homefinder.com, homes.com, realtytrac, freedomsoft,

HomeOnTheTube, , Vast, LakeHomesUSA, PropBot, DataSphere, and eRealInvestor! HomeWinks, Property Shark, USHUD.com, Oodle, CLRSearch, MyRealty.com, Enormo, Overstock, Yahoo Real Estate, Trulia, FrontDoor, hotpads.com, AOL Real Estate,

HomeAwayRealEstate, HomeTourConnect, Property Pursuit, RealtyStore, TweetLister, Cyberhomes

13. Mail Postcards to Neighbors – We will send a color postcard of your house to neighbors closest to your home.

14. Counter Display – We will prepare an informational notebook containing most things a buyer will want to know – survey, school information, utilities, homeowner’s association, pre-inspection information, contract, etc. This information will give buyers the confi-

dence to write a contract.

15. Weekly Contact – We will contact you weekly to give you an update on the marketing of your home and answer any questions you may have.

16. Monthly report – We will give you the monthly number of views on your property from Realtor.com and aldridgeandsoutherland.com.

17. Aldridge & Southerland Office Tour – Our sales staff will preview all single family homes in Pitt County. For multi-family properties, we will have a slide presentation for the office in an office sales meeting.

18. Aldridge & Southerland Grab Bag – We will provide you a large duffle bag, yours to

keep, to pick up toys, clothes etc in the event of a showing without much notice.

19. Brand Strength of the largest real estate advertiser for the past 30 years!

3

Announcing! …

Aldridge & Southerland Realtors

Unconditional Guarantee!

If for any reason we at Aldridge & Southerland do not provide

100% satisfactory service, please just let us know, and we will take

care of the situation immediately. After that, if you still are not

100% satisfied, we will release you from the listing agreement

with an “Unconditional Release” with no cost or obligation to

you whatsoever.

We are absolutely positive that you will be 100% satisfied with

us, and that’s our “Aldridge & Southerland Guarantee!”

Thank you for trusting in us!

Aldridge & Southerland Home Sellers

____________________ ___________________

___________________

4

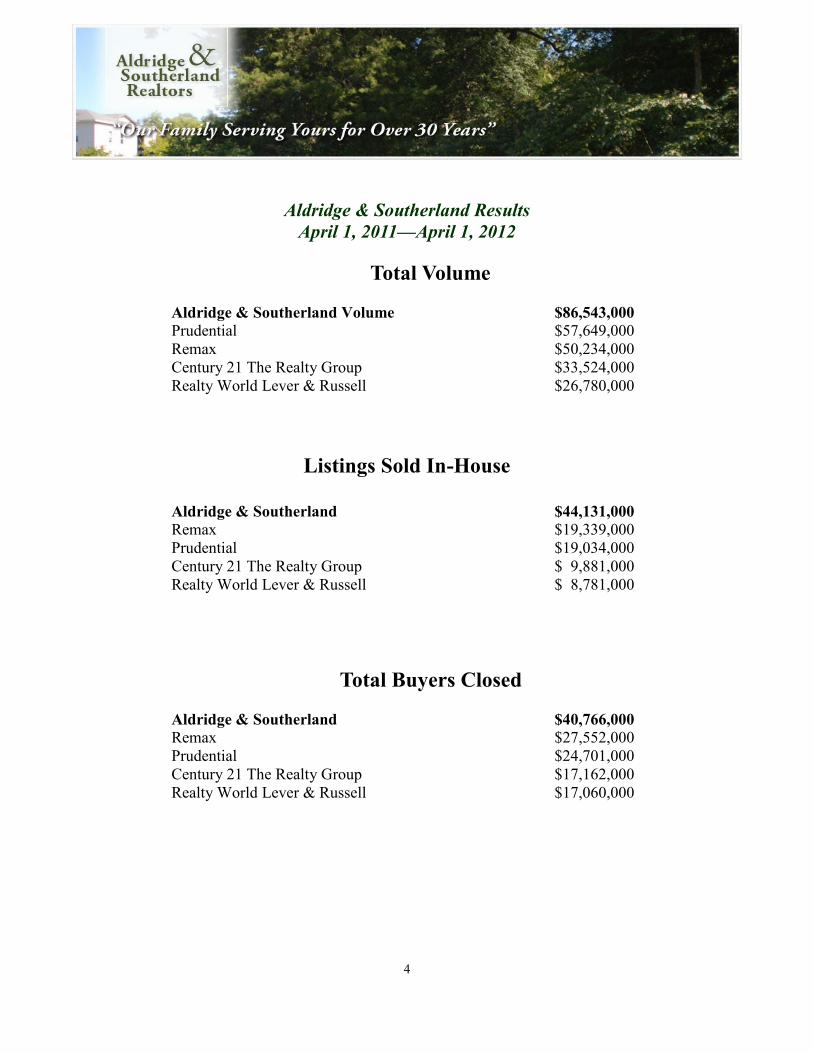

Aldridge & Southerland Results

April 1, 2011—April 1, 2012

Total Volume

Aldridge & Southerland Volume $86,543,000

Prudential $57,649,000

Remax $50,234,000

Century 21 The Realty Group $33,524,000

Realty World Lever & Russell $26,780,000

Listings Sold In-House

Aldridge & Southerland $44,131,000 Remax $19,339,000

Prudential $19,034,000

Century 21 The Realty Group $ 9,881,000

Realty World Lever & Russell $ 8,781,000

Total Buyers Closed

Aldridge & Southerland $40,766,000 Remax $27,552,000

Prudential $24,701,000

Century 21 The Realty Group $17,162,000

Realty World Lever & Russell $17,060,000

5

Residential

Odds of Selling

APRIL 1, 2011—APRIL 1, 2012

PRICE RANGE TOTAL PAST 12 MONTHS

RESIDENTIAL LISTINGS

TOTAL PAST 12 MONTHS

CLOSED ODDS OF SELLING

0-100 1085 600 55%

100-120 239 127 53%

120-140 393 219 56%

140-160 262 137 52%

160-180 238 107 45%

180-200 198 101 51%

200-220 90 50 56%

220-240 130 58 45%

240-260 90 38 42%

260-280 58 33 57%

280-300 53 28 53%

300-320 27 8 30%

320-340 41 17 41%

340-360 45 18 40%

360-380 24 6 25%

380-400 30 14 47%

400-420 7 3 43%

420-440 14 7 50%

440-460 11 3 27%

460-480 9 2 22%

480-500 15 8 53%

500-550 11 6 55%

550-600 8 3 38%

600 & UP 32 2 6%

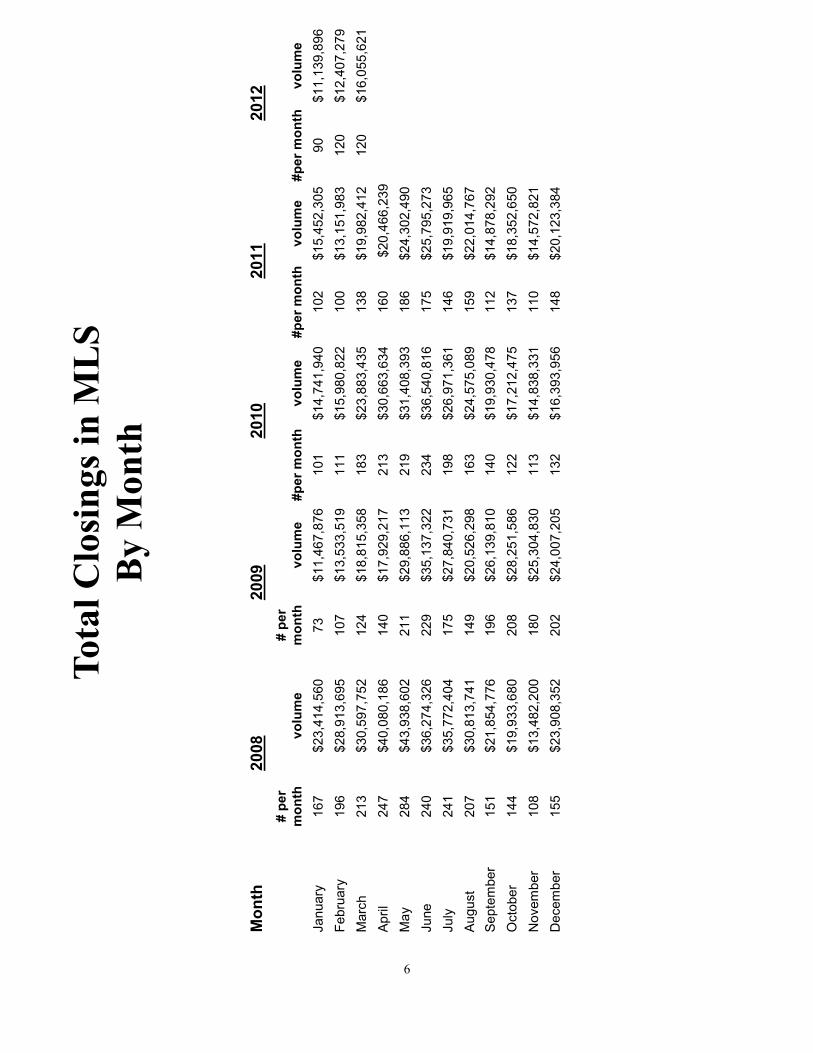

6

To

tal

Clo

sin

gs

in M

LS

By

Mo

nth

Mo

nth

20

08

20

09

20

10

20

11

20

12

# p

er

mo

nth

v

olu

me

# p

er

mo

nth

v

olu

me

#p

er

mo

nth

v

olu

me

#p

er

mo

nth

v

olu

me

#p

er

mo

nth

v

olu

me

January

167

$23,4

14,5

60

73

$11,4

67,8

76

101

$14,7

41,9

40

102

$15,4

52,3

05

90

$11,1

39,8

96

Febru

ary

196

$28,9

13,6

95

107

$13,5

33,5

19

111

$15,9

80,8

22

100

$13,1

51,9

83

120

$12,4

07,2

79

Marc

h

213

$30,5

97,7

52

124

$18,8

15,3

58

183

$23,8

83,4

35

138

$19,9

82,4

12

120

$16,0

55,6

21

Apri

l

247

$40,0

80,1

86

140

$17,9

29,2

17

213

$30,6

63,6

34

160

$20,4

66,2

39

Ma

y

284

$43,9

38,6

02

211

$29,8

86,1

13

219

$31,4

08,3

93

186

$24,3

02,4

90

June

240

$36,2

74,3

26

229

$35,1

37,3

22

234

$36,5

40,8

16

175

$25,7

95,2

73

July

241

$35,7

72,4

04

175

$27,8

40,7

31

198

$26,9

71,3

61

146

$19,9

19,9

65

Aug

ust

207

$30,8

13,7

41

149

$20,5

26,2

98

163

$24,5

75,0

89

159

$22,0

14,7

67

Septe

mber

151

$21,8

54,7

76

196

$26,1

39,8

10

140

$19,9

30,4

78

112

$14,8

78,2

92

Octo

ber

144

$19,9

33,6

80

208

$28,2

51,5

86

122

$17,2

12,4

75

137

$18,3

52,6

50

Novem

ber

108

$13,4

82,2

00

180

$25,3

04,8

30

113

$14,8

38,3

31

110

$14,5

72,8

21

Decem

ber

155

$23,9

08,3

52

202

$24,0

07,2

05

132

$16,3

93,9

56

148

$20,1

23,3

84

7

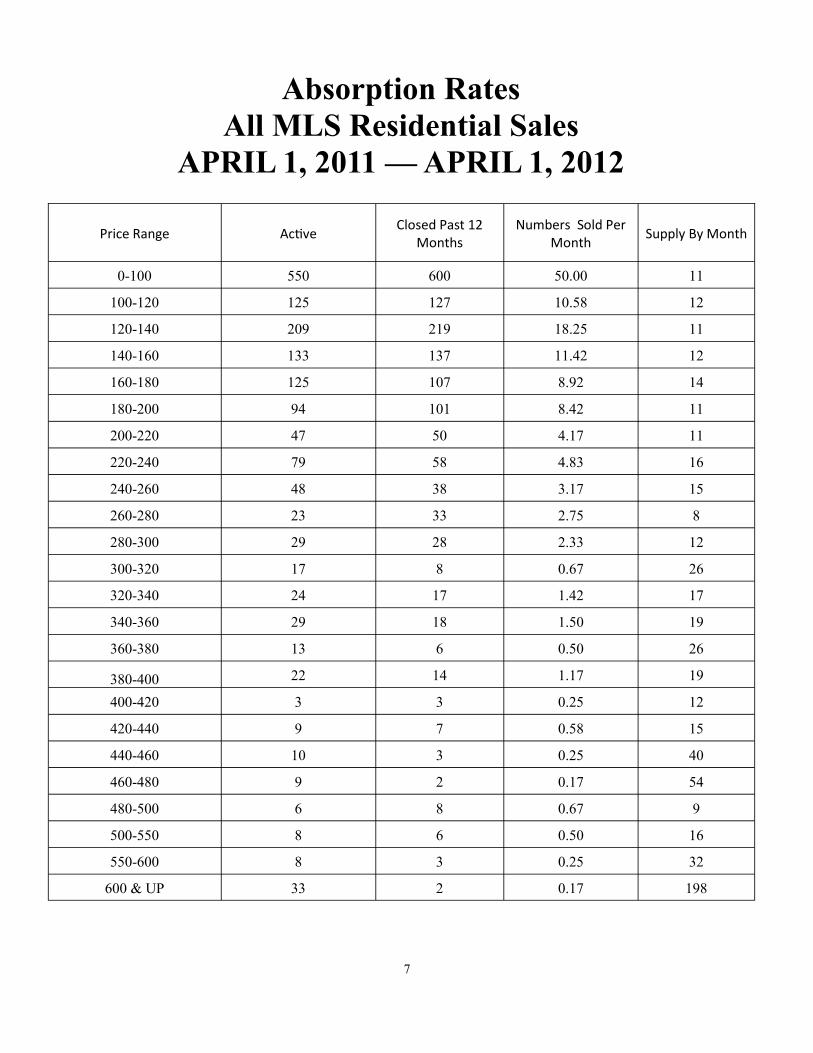

Absorption Rates

All MLS Residential Sales

APRIL 1, 2011 — APRIL 1, 2012

Price Range Active Closed Past 12

Months Numbers Sold Per

Month Supply By Month

0-100 550 600 50.00 11

100-120 125 127 10.58 12

120-140 209 219 18.25 11

140-160 133 137 11.42 12

160-180 125 107 8.92 14

180-200 94 101 8.42 11

200-220 47 50 4.17 11

220-240 79 58 4.83 16

240-260 48 38 3.17 15

260-280 23 33 2.75 8

280-300 29 28 2.33 12

300-320 17 8 0.67 26

320-340 24 17 1.42 17

340-360 29 18 1.50 19

360-380 13 6 0.50 26

380-400 22 14 1.17 19

400-420 3 3 0.25 12

420-440 9 7 0.58 15

440-460 10 3 0.25 40

460-480 9 2 0.17 54

480-500 6 8 0.67 9

500-550 8 6 0.50 16

550-600 8 3 0.25 32

600 & UP 33 2 0.17 198

8

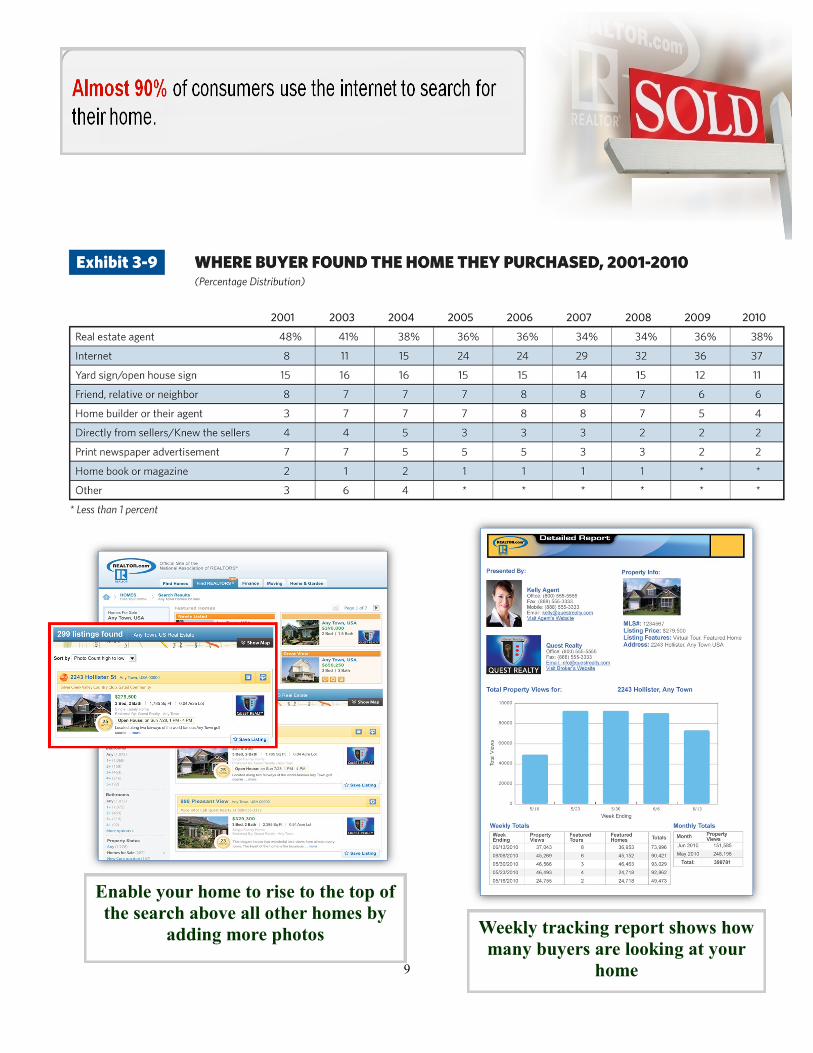

9

Weekly tracking report shows how

many buyers are looking at your

home

Enable your home to rise to the top of

the search above all other homes by

adding more photos

10

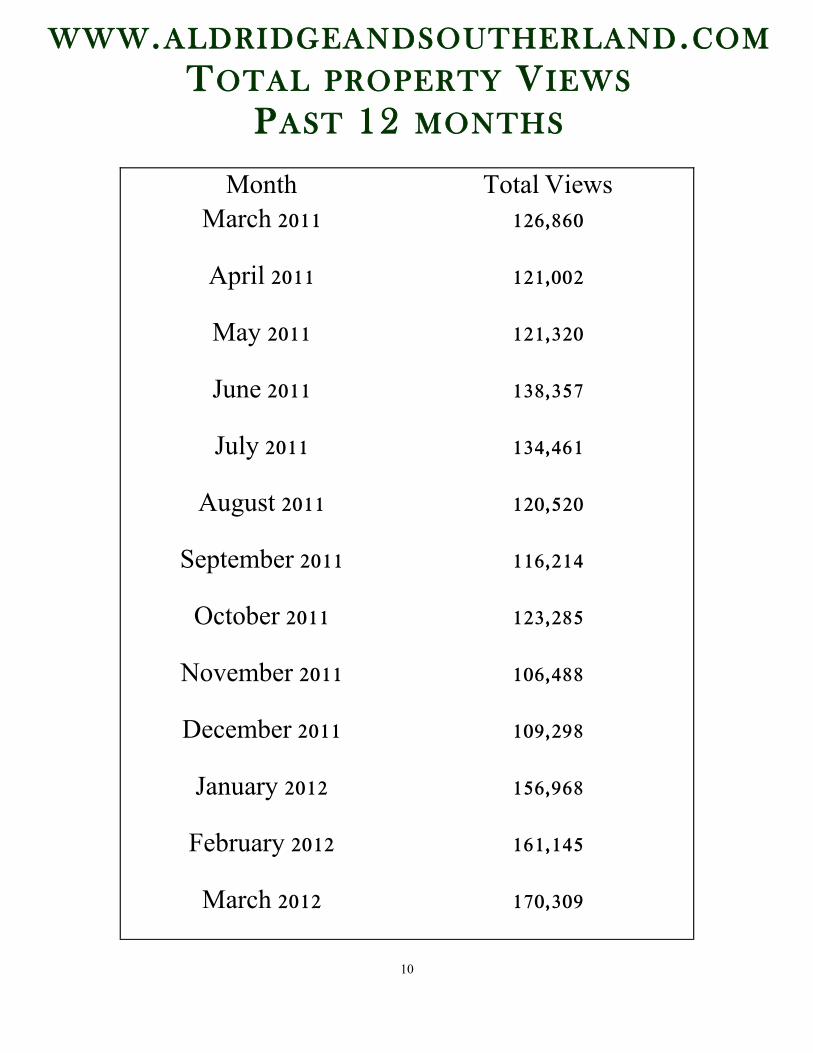

WWW .ALDRIDGEANDSOUTHERLAND .COM

TOTAL PROPERTY V IEWS

PAST 12 MONTHS

Month Total Views

March 2011 126,860

April 2011 121,002

May 2011 121,320

June 2011 138,357

July 2011 134,461

August 2011 120,520

September 2011 116,214

October 2011 123,285

November 2011 106,488

December 2011 109,298

January 2012 156,968

February 2012 161,145

March 2012 170,309

11

Pricing Reality

1. A buyer will not pay more for a home if they can purchase a similar home for less money.

2. Most Sellers feel their home is unique. Their emotional feelings about the uniqueness

of their home lead them to overprice it.

3. Sellers can become the victims of misinformation which can lead to overpricing .

Sources vary but often include friends, relatives, neighbors, agents, the internet and ap-

praisers.

4. Sellers usually overestimate the impact of additions or improvements to their home.

Pricing a home based upon recouping such costs will almost always result in overpricing.

Appreciation is another factor that is relative to a given market segment.

5. Exterior painting, replacing a roof, replacing appliances is usually considered mainte-

nance and not an improvement. Any value added for these reasons will be negligible.

6. A seller’s financial needs often lead to overpricing.

7. Overpricing a home will often discourage an interested buyer at the initial showing.

8. A Financial Institution will not lend more than the appraised value of a home.

9. Overpricing can result in extended marketing times. Since the Seller is usually paying

mortgage payments, and incurring other living expenses, the net sells price may be more

than if the home had been priced right in the first place.

10. Shown to sell, not just to compare.

11. Competitively priced homes sell faster!

12. A home that sells in the first 30 days will bring the highest possible price.

13. Seller is able to move on to next chapter without the headache of marketing a home and

maintaining it in “Show” condition.

14. The “market” should set the price. The Buyer (with agreement from the seller) will

ultimately determine the value.

15. If Buyer and Seller can’t reach agreement, there is no sale.

12

Questions Your Agent Will Answer To Help You Arrive At Market Value

1. How many homes are for sale currently in your range?

(supply) 2. How many in your price range are selling each month? (demand)

3. How does your particular area compete in the overall

price range? A. How many homes are for sale in your area? (supply) B. How many in your area are selling each month? (demand)

After evaluating the present market condition, (1) Competing homes

(2) Supply vs. demand in this price range (3) Supply vs. demand in your subdivision or area

Your agent will be able to give you an accurate range of current market value.

13

A Few Words on Condition

We live in our homes in one way, we market them in another. Just as

builders recognize that a finished, clean, decorated model enables them to

enhance the appeal of the homes they are building, “staging” your home to

enhance its appeal will give you a competitive edge against all the other homes

on the market.

Our agents understand which items are cost effective and will pay you

back many times over in buyer interest. After you agree to list your home with

us, your agent will provide a one hour consultation with a certified home stager

to help you enhance your homes appeal.

Aldridge & Southerland is responsible for Marketing your home.

You are in control of its Marketability, through the price you set, and the ef-

forts you take to stage your home.

The moment you decide to sell your home, you must start thinking like a

buyer! After all, you have chosen Aldridge & Southerland Realtors to

market your home. You will be a buyer before you know it!

14

A Few Words on Condition

Remember, buyers will be looking at many potential homes. If you want

yours to sell First , it Must be priced correctly and look the Best! Buyers

these days do not want to have to clean, paint & make necessary repairs.

Most prefer “move-in condition”.

May we suggest making a list of things You would want done if you were

a buyer interested in your home. And… Start Working! Be sure to finish pri-

or to your 1st showing. Remember, your best showings and most

activity typically come during the first 30 days of marketing. So… Be Ready!

Please ask your agent for a copy of our video, “Dress Your House For

Success”. You’ll find it very helpful in preparing your home for sale.

15

Why does Aldridge and Southerland believe it pays to Stage®? Staged homes sell faster and for more money than non-staged properties. Staged homes create interest among prospective buyers. Staging is fast and affordable. Property looks more attractive to potential buyers than competing homes in local market. Buyer spends more time viewing house without being distracted by personal items. Neutral and updated look appeals to larger buyer pool. Appraisers are more likely to appraise Staged homes at full value. Photos of Staged homes look better in print and Internet advertising.

Staging is cheaper than your first price reduction!

Call today to make your Staging consultation!

First Impressions Staging, Inc. Becky Blizzard (252)916-6499

www.firstimpressionsstaging.net

© 2006 StagedHomes.com. All rights reserved. Stage® is a Federally Registered

Trademark of StagedHomes.com (800) 392-7161

Jordan Robertson (252) 412-2827

Sue Aldridge (252) 531-7020

Home Staging Services

16

NOTICE TO SELLERS

Keep in mind that buyers want to obtain the lowest price and

best terms for themselves. We recommend that you do not

discuss the following types of information with any buyers or

real estate agents, regardless of whom they represent, other

than your own listing agent:

Reason for selling.

Motivation or urgency to sell.

Willingness to consider an offer less than the listing price.

Terms under which you would sell.

Relocation, timing, benefits of policies (if applicable).

Items of personal property which you “might” be willing to

include in a sale.

Any confidential information that would serve to disclose

your negotiation strategy.

17

Forty Tips For A Faster Sale

There are a number of things you can do to Improve the Overall Impression made by your home. But first, you must learn to look at your home through the eyes of the Buyer.

1. Reduce clutter. Sort through closets, drawers, and storage areas. Toss away what you

can; organize the rest. If you have too much furniture in your home, put some pieces in storage to make a better first impression.

2. Clean. Not only should your home be spotless, it must sell clean. Apply elbow grease and strong cleaners to surfaces inside and outside your home. Clean window sills. Consider painting if cleaning doesn’t do the job.

3. Sparkling windows are a signal to buyers that you care about your home. Clean your interior and exterior windows. Repair cracked panes, torn screens, broken sashes, and ropes or cords. Whenever your home is being shown, open curtains and blinds to let the light in - especially if the view is nice.

4. Make minor repairs. Tighten loose knobs, fix leaky faucets and discolored sinks, lubricate squeaky hinges, clean out clogged drains, replace filters, secure loose shingles, fix holes in screens, tighten loose banisters, repair doors and door knobs.

5. Clean all curtains and draperies; shampoo carpets and rugs and wax floors.

6. Arrange furniture to make each room appear larger.

7. Make sure all lighting fixtures work. Add new bulbs with the highest wattage allowed for each fixture to make your room seem brighter.

8. Appeal to the senses. Create an aroma during the open house. Burn candles or potpourri, boil a pot of cinnamon sticks, or put a dab of vanilla on cold light bulbs before turning them on. If you have pets or if someone in your home smokes, the odors can linger and lessen your home’s appeal. You might not notice these smells if you live with them every day, but an unclean cat box or an ashtray filled with cigarette butts can mean your home will get no further attention.

9. Improve the front entrance. A coat of paint on the door; brass accents such as house numbers, a door knob, and a kick plate; and prune bushes and blooming plants can help your home make a good first impression.

10. Make sure your doorbell works.

11. Paint. Light, neutral colors such as beige, white, off-white, or gray have a broader appeal and can make small rooms seem larger and airier. If you have dated wallpaper, remove the paper and paint the walls. Choose premium quality paint. Caulk and fill nail holes before painting.

18

Forty Tips For A Faster Sale

12. Repair a leaky roof, and then paint over any water marks on the ceiling. Don’t paint to hide a problem, always fix and then paint.

13. Repair a wet basement. The problem can be as easy as installing covers over window wells. If the moisture problem calls for more extensive repairs and you are not able to make them, be prepared to explain the problem to a buyer. Don’t try to cover up the signs of a wet basement.

14. Exterminate. One bug, dead or alive, can make a bad impression on a buyer. Call in a professional to rid your home of insects, and allow time for the smell of the pesticide to disappear before showing your home.

15. Organize the kitchen. Clear off the counters. Add drawer organizers to suggest efficient use of space. Store seldom-used small appliances and large baking pans.

16. Update the bath. If cleaning and painting can’t make a dingy bath dynamite, consider replacing the vanity and sink, installing a new floor covering, or resurfacing a stained bathtub.

17. If you have a deck, patio, porch, or other outdoor entertainment area such as a pool or hot tub, make the most of them. Keep these areas, as well as your backyard, clean and clutter free, put debris in covered trash cans.

18. Install outdoor lighting that properly illuminates your entrances, walkways, and driveways. Turn on all those outdoor lights when your home is being shown.

19. Put potted flowering plants by the front door. Give shutters a fresh coat of paint. A window box full of flowers is an inexpensive way to add an accent of color to your home’s exterior.

20. Buy a new doormat.

21. Pick up tools and toys from the yard. Put garbage cans in the garage and shut the door. Make sure the garage is swept and try to remove any stains from the floor.

22. Paint your mailbox and lamppost.

23. Clean gutters and downspouts. Straighten and paint if necessary.

24. Depending on the season, hose down the house, walkway and drive at least once a week.

25. Repair cracks and pull weeds from walkways and driveways.

26. Carpeting has a major impact on the look of your home. If yours is badly worn, outdated, or stained, consider replacing it.

19

Forty Tips For A Faster Sale

27. Hardwood floors add to the beauty and value of a home and deserve special attention. If you live in a older home, check for hardwood floors under the carpeting. You may be able to pull up the carpeting and refinish by simply cleaning and waxing the floors to create a classic fresh look.

28. Ask a friend to care for your pets or take them to the kennel when your home is being shown. Park your camper, boat or extra car at another location.

29. Buy or cut fresh flowers for a dramatic arrangement in any room.

30. Take a picture - it will last longer. If your home is surrounded by flowering or fruit-bearing trees, low-maintenance landscapes, and herbal or flower gardens, be sure to take pictures when everything is in full bloom. Photographs and proof of the breathtaking view of your lawn and garden and tell prospective buyers the full story of your home - no matter the season.

31. Edge around your lawn, drive and walkways.

32. Remove dead leaves, limbs, and other debris from lawn.

33. Trim trees and hedges. Prune evergreens and shrubs.

34. Put fresh mulch around trees, shrubs, or hedges.

35. Put away lawn equipment and gardening tools.

36. Make sure the exterior paint and siding is in good condition, and that the roof, gutters and spouts are in good repair.

37. Weed and cultivate flower gardens.

38. Repair fences and gates and give them a fresh coat of paint if necessary.

39. Mow your lawn. For more lushness, be sure to water, now and fertilize regularly. Remove dandelions and other weeds that are visible. A good rule of thumb for mowing is to never cut off more than one-third of the blade at one time. For example, if the recommended height is 2 inches, mow when your grass is 3 inches.

40. If you are an absentee seller, make arrangements for lawn care, keep utilities on, set heat at 62 degrees and air conditioning at 78 degrees.

20

How to Prepare for a Showing in Ten

Minutes or Less...

1. Put the dishes in the dishwasher. (Or quickly wash them!)

2. Make the beds.

3. Wipe the counters.

4. Empty the garbage.

5. Hide dirty clothes in the washer.

6. Take a deep breath!

7. Run a quick vacuum.

8. Turn on the lights.

9. Leave the house before showing!

10. Smile! You did it!

We are working hard to get your Home Sold!

21

Need Relocation Assistance?

If you are planning to purchase a home in your destination city, let Aldridge &

Southerland contact a real estate professional in advance. The agent can provide you a wealth of information in advance, such as: information about schools, neighborhoods and any other specific interests you have. Additionally, the agent can send you information on the available homes that meet your specific needs and wants, so you waste no time in your home search upon your arrival.

Aldridge & Southerland will personally call the Realtor’s office in your destination city and select the most productive, most concerned realtor to work with you. That agent will call you to collect all the pertinent information about the price and style of home you want, the neighborhood you desire and provide general information about your destination. He/she can arrange a finance interview, insurance quotes and a comfortable, non-pressure home search that saves you time, money and effort.

Simply tell Aldridge & Southerland where you are moving… we’ll do the rest.

Aldridge & Southerland, I am moving to: ___________________________________________________________________________________________ I would like city/area information about the following homes: Price range $_________________________ to $_________________________ Bedrooms _________________ Baths _________________ Square Ft. ________________ Other (age, lot size, setting, etc.) Special interests/needs: Please have the destination agent contact me at: My phone #________________________________________________________________ My Name _________________________________________________________________

22

Inspectors

HOME INSPECTORS

Advanced Termite and Home Inspections Chris Matthews 252-229-7221 Dependable Inspections, Inc. Derek Hedgepeth (252) 355-5480 (252) 531-2455 Jeff Mathis (252) 714-1809 Quality Home Inspections Bill Fell (252) 756-1602 Off. (252) 341-8373 Cell Tarheel Home Inspections James Keel (252)813-8447

SEPTIC INSPECTIONS Cannon’s Septic Tank Service (252) 524-4282 Jim’s Liquid Waste (252) 830-1016 Matthews Septic Tank Service (252) 753-4097 Dr. Pumper (252) 756-7867

TERMITE INSPECTORS

Advanced Termite and Home Inspections Chris Matthews 252-229-7221 Clegg’s Termite & Pest Control (252) 752-5175 Doc Moore (252)752-2065 Russ Pest Control (252)746-8098 Pestech Of Greenville Chris Rhodes - Operator (252) 353-4760

Quality Pest Control

Kevin Blackburn (252) 756-1602

WATER QUALITY CHECK Environment One

(252) 756-6208

23

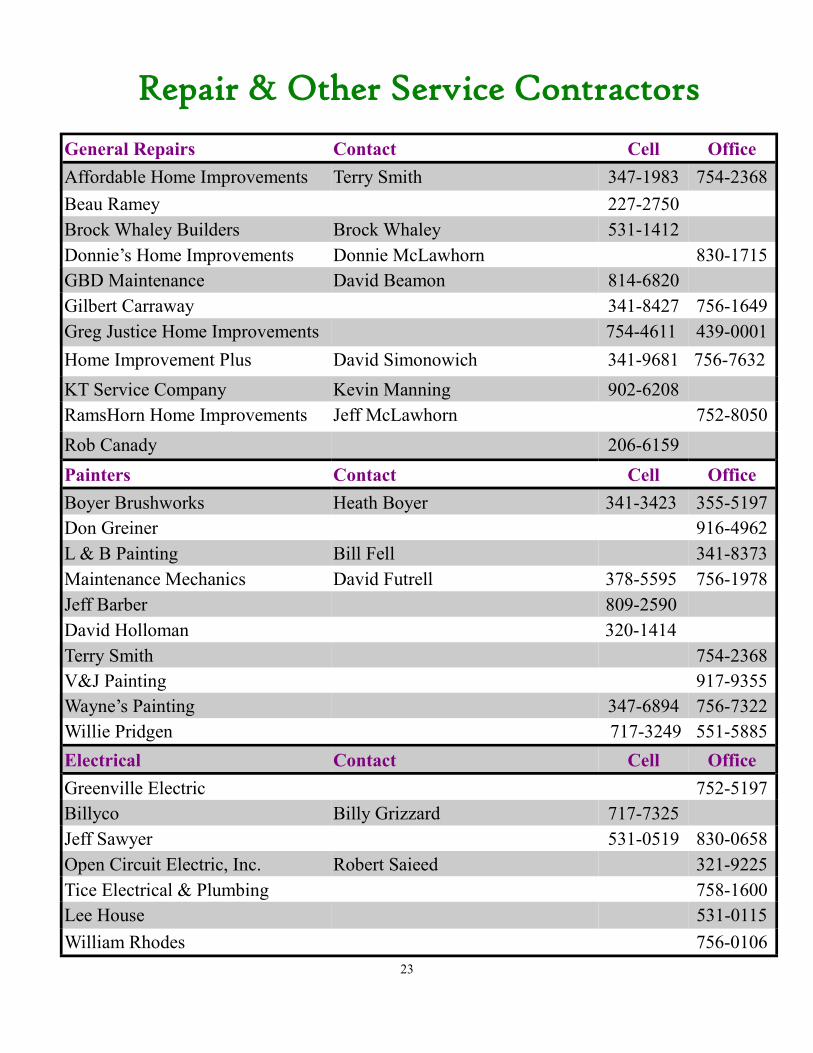

Repair & Other Service Contractors

General Repairs Contact Cell Office

Affordable Home Improvements Terry Smith 347-1983 754-2368

Beau Ramey 227-2750

Brock Whaley Builders Brock Whaley 531-1412

Donnie’s Home Improvements Donnie McLawhorn 830-1715

GBD Maintenance David Beamon 814-6820

Gilbert Carraway 341-8427 756-1649

Greg Justice Home Improvements 754-4611 439-0001

Home Improvement Plus David Simonowich 341-9681 756-7632

KT Service Company Kevin Manning 902-6208

RamsHorn Home Improvements Jeff McLawhorn 752-8050

Rob Canady 206-6159

Painters Contact Cell Office

Boyer Brushworks Heath Boyer 341-3423 355-5197

Don Greiner 916-4962

L & B Painting Bill Fell 341-8373

Maintenance Mechanics David Futrell 378-5595 756-1978

Jeff Barber 809-2590

David Holloman 320-1414

Terry Smith 754-2368

V&J Painting 917-9355

Wayne’s Painting 347-6894 756-7322

Willie Pridgen 717-3249 551-5885

Electrical Contact Cell Office

Greenville Electric 752-5197

Billyco Billy Grizzard 717-7325

Jeff Sawyer 531-0519 830-0658

Open Circuit Electric, Inc. Robert Saieed 321-9225

Tice Electrical & Plumbing 758-1600

Lee House 531-0115

William Rhodes 756-0106

24

Repair & Other Service Contractors

Plumbers Contact Cell Office

A-1 Plumbing Tim Morris 752-0543

Conger Plumbing Mike Conger 353-1111

Eastern Plumbing & Maintenance 758-7579

Jimmy Holton 551-7703 756-2870

Maintenance Mechanics David Futrell 378-5595 756-1978

Mike Harrell 717-7217 355-5405

Sam Pollard & Son 752-3661

Taylormade Plumbing Michael Taylor 341-3102

Tice Electrical & Plumbing 758-1600

Heating & Air Contact Cell Office

Advanced Mechanical 355-9191

Blount & Williams 758-1277

Brann’s Heating & Air 753-2550

Carolina Heat & Air 756-2166

Comfort Master 531-7304

Elite Mechanical Cullen Lane 717-5776 746-6200

Enesco East 752-3686

McCollam Heating & Air Jay McCollam 268-8052

Pollard & Sons 752-3661

Steve Rhodes 756-0106

Riddle Brothers 353-5588

Roofers Contact Cell Office

Greenville Contractors, Inc. 830-1280

Chuck Hester 704-634-3399

Family Home Improvement Tony Vargas 754-8335

Walker Co. Roofing Jeff Walker 355-8111

Roof Cleaning Contact Cell Office

Scuzzy Roof/We Clean Richard Elwell 321-2665

Sparkle Right Keith Cox 252-286-6300 717-7717

25

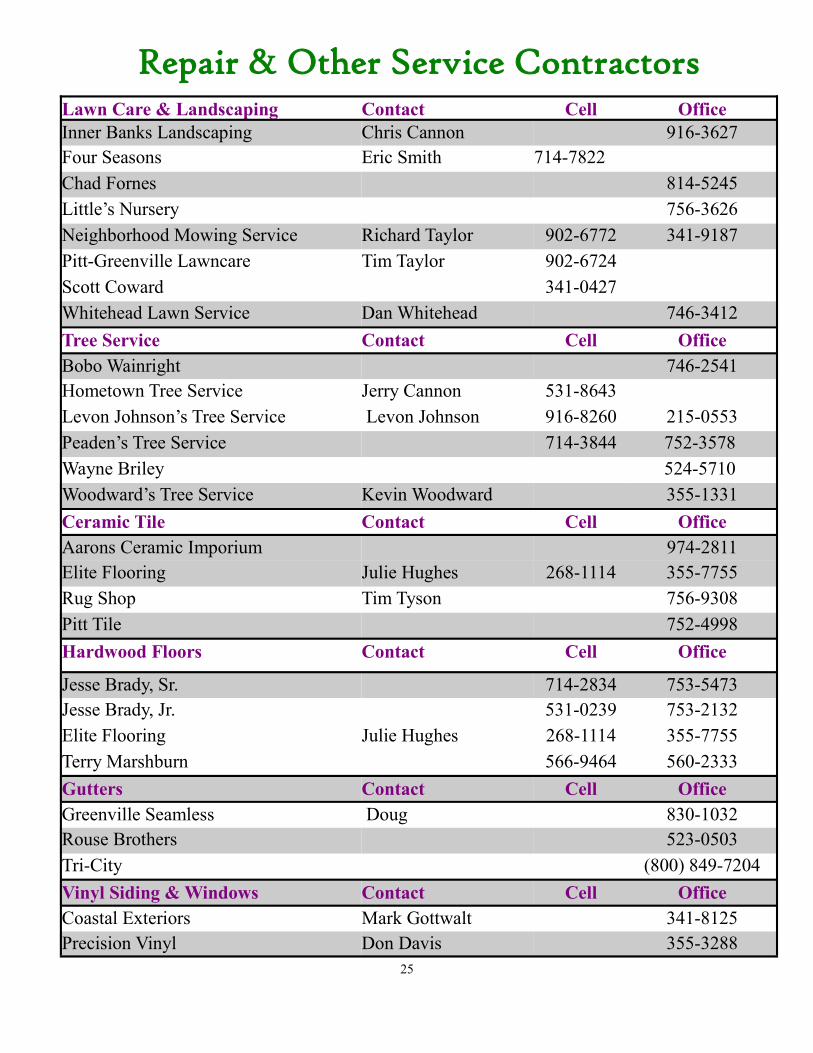

Repair & Other Service Contractors

Lawn Care & Landscaping Contact Cell Office

Inner Banks Landscaping Chris Cannon 916-3627

Four Seasons Eric Smith 714-7822

Chad Fornes 814-5245

Little’s Nursery 756-3626

Neighborhood Mowing Service Richard Taylor 902-6772 341-9187

Pitt-Greenville Lawncare Tim Taylor 902-6724

Scott Coward 341-0427

Whitehead Lawn Service Dan Whitehead 746-3412

Tree Service Contact Cell Office

Bobo Wainright 746-2541

Hometown Tree Service Jerry Cannon 531-8643

Levon Johnson’s Tree Service Levon Johnson 916-8260 215-0553

Peaden’s Tree Service 714-3844 752-3578

Wayne Briley 524-5710

Woodward’s Tree Service Kevin Woodward 355-1331

Ceramic Tile Contact Cell Office

Aarons Ceramic Imporium 974-2811

Elite Flooring Julie Hughes 268-1114 355-7755

Rug Shop Tim Tyson 756-9308

Pitt Tile 752-4998

Hardwood Floors Contact Cell Office

Jesse Brady, Sr. 714-2834 753-5473

Jesse Brady, Jr. 531-0239 753-2132

Elite Flooring Julie Hughes 268-1114 355-7755

Terry Marshburn 566-9464 560-2333

Gutters Contact Cell Office

Greenville Seamless Doug 830-1032

Rouse Brothers 523-0503

Tri-City (800) 849-7204

Vinyl Siding & Windows Contact Cell Office

Coastal Exteriors Mark Gottwalt 341-8125

Precision Vinyl Don Davis 355-3288

26

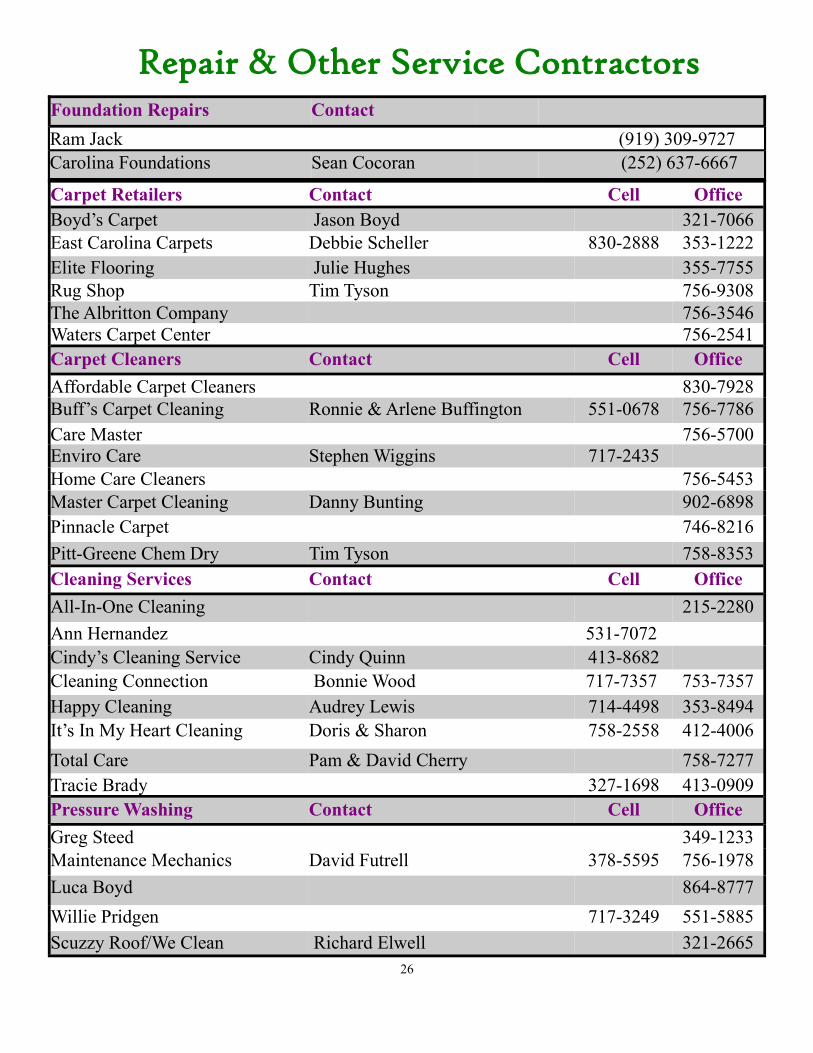

Repair & Other Service Contractors

Foundation Repairs Contact

Ram Jack (919) 309-9727

Carolina Foundations Sean Cocoran (252) 637-6667

Carpet Retailers Contact Cell Office

Boyd’s Carpet Jason Boyd 321-7066

East Carolina Carpets Debbie Scheller 830-2888 353-1222

Elite Flooring Julie Hughes 355-7755

Rug Shop Tim Tyson 756-9308

The Albritton Company 756-3546

Waters Carpet Center 756-2541

Carpet Cleaners Contact Cell Office

Affordable Carpet Cleaners 830-7928

Buff’s Carpet Cleaning Ronnie & Arlene Buffington 551-0678 756-7786

Care Master 756-5700

Enviro Care Stephen Wiggins 717-2435

Home Care Cleaners 756-5453

Master Carpet Cleaning Danny Bunting 902-6898

Pinnacle Carpet 746-8216

Pitt-Greene Chem Dry Tim Tyson 758-8353

Cleaning Services Contact Cell Office

All-In-One Cleaning 215-2280

Ann Hernandez 531-7072

Cindy’s Cleaning Service Cindy Quinn 413-8682

Cleaning Connection Bonnie Wood 717-7357 753-7357

Happy Cleaning Audrey Lewis 714-4498 353-8494

It’s In My Heart Cleaning Doris & Sharon 758-2558 412-4006

Total Care Pam & David Cherry 758-7277

Tracie Brady 327-1698 413-0909

Pressure Washing Contact Cell Office

Greg Steed 349-1233

Maintenance Mechanics David Futrell 378-5595 756-1978

Luca Boyd 864-8777

Willie Pridgen 717-3249 551-5885

Scuzzy Roof/We Clean Richard Elwell 321-2665

27

Repair & Other Service Contractors

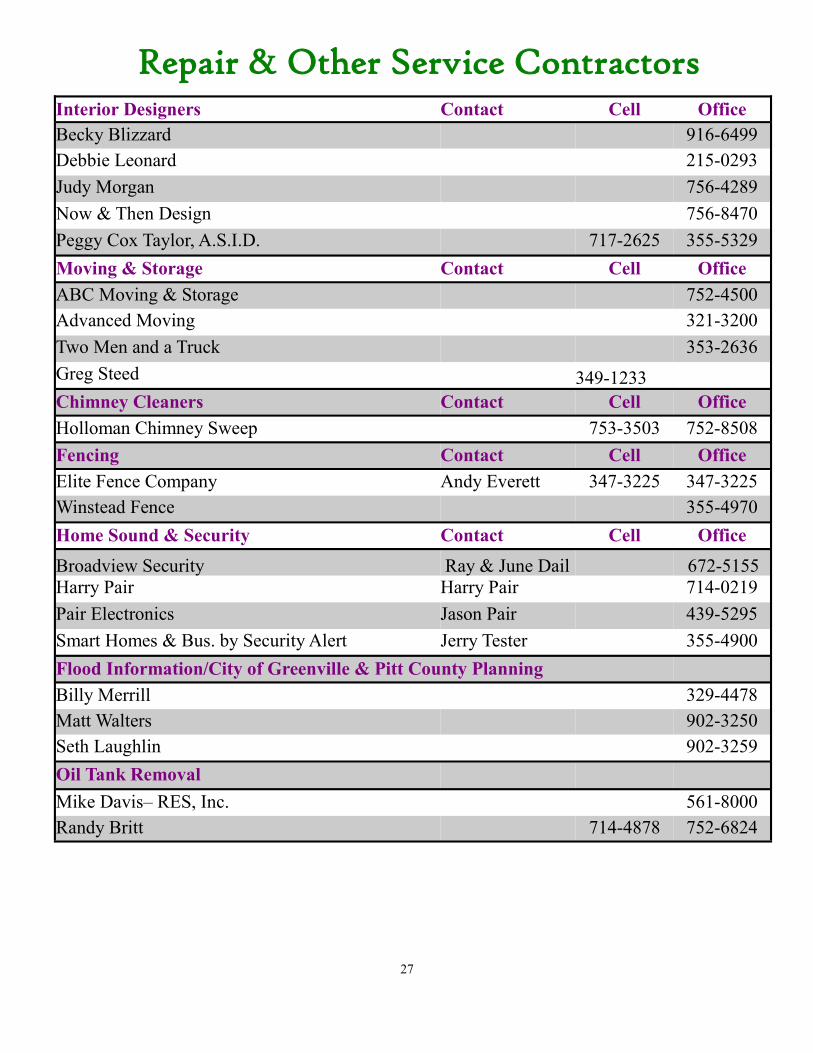

Interior Designers Contact Cell Office

Becky Blizzard 916-6499

Debbie Leonard 215-0293

Judy Morgan 756-4289

Now & Then Design 756-8470

Peggy Cox Taylor, A.S.I.D. 717-2625 355-5329

Moving & Storage Contact Cell Office

ABC Moving & Storage 752-4500

Advanced Moving 321-3200

Two Men and a Truck 353-2636

Greg Steed 349-1233

Chimney Cleaners Contact Cell Office

Holloman Chimney Sweep 753-3503 752-8508

Fencing Contact Cell Office

Elite Fence Company Andy Everett 347-3225 347-3225

Winstead Fence 355-4970

Home Sound & Security Contact Cell Office

Broadview Security Ray & June Dail 672-5155

Harry Pair Harry Pair 714-0219

Pair Electronics Jason Pair 439-5295

Smart Homes & Bus. by Security Alert Jerry Tester 355-4900

Flood Information/City of Greenville & Pitt County Planning

Billy Merrill 329-4478

Matt Walters 902-3250

Seth Laughlin 902-3259

Oil Tank Removal

Mike Davis– RES, Inc. 561-8000

Randy Britt 714-4878 752-6824

28

Home Owners Insurance Companies Allstate

Jennifer Edmundson

3105 Evans St

Greenville, NC 27858

(252)756-5055

Billy Byrd Insurance Agency

Nationwide

200 Arlington Blvd

Greenville, NC 27858

(252)756-9900

Challender Insurance Co.

Chris Challender

2115 S.E. Greenville Bvd.

Greenville, NC 27858

(252)321-8555

Clement Companies

105 E. Arlington Blvd.

Greenville, NC 27858

(252)756-8300

Briley & Goodson Erie Insurance

2413 S. Charles Blvd.

Greenville, NC 27858

(252)353-5880

Farm Bureau Insurance Jay Surles/Jack Metts/Allen Hill

402 SW Greenville Blvd

Greenville, NC 27834

(252)756-3165

The Gavigan Agency

Jon Gavigan

Nationwide

252-565-3226

Hardee’s Insurance

Wayland Hardee

NC 102 East

Ayden, NC 28513

(252)717-9130

Hooker & Buchanan

Jeff Gibson

509 S. Evans St.

Greenville, NC 27858

(252)752-6186

Polly Piland Insurance

State Farm

1160 E. Arlington Blvd

Greenville, NC 27858

(252)756-8886

Mack Beale Insurance

State Farm

3011 S. Memorial Dr

Greenville, NC 27834

(252)756-7280

The Styons Agency

Nationwide—Raymie Styons

2424 S. Charles Blvd

Greenville, NC 27858

(252)756-1400

Stephen West Insurance Nationwide (252)321-7717

2755-A S. Charles Blvd

Greenville, NC 27858

WA Moore Insurance

Todd Brown

600 Lynndale Ct #D

Greenville, NC 27858

(252)321-7717

Winterville Insurance Co. Tim Harrell

2621 Railroad St (252)756-0317

Winterville, NC 28590

29

Brown, Whit

321 S. Evans St., Ste. 200

Greenville, NC 27858

(252) 758-2400

Dixon, Phil

110 E. Arlington Blvd.

Greenville, NC 27858

(252) 355-8100

Christian Porter

1698 E. Arlington Blvd.

Greenville, NC 27858

(252) 321-2020

Griffin, Richard

202 Arlington Blvd., Suite B

Greenville, NC 27858

(252) 355-4619

Hahn, Allen L.

504 A Red Banks Rd.

Greenville, NC 27858

(252) 756-6970

Harrington, Danny 211 W. 14th Street

Greenville, NC 27834

(252) 830-8840

Horne, Stephen F. II

300 Cotanche

Greenville, NC 27834

(252) 758-4333

James, Gregory K.

315 S. Evans Street

Greenville, NC 27858

(252) 752-2400

Jones, Steve

115 W. 4th St.

Greenville, NC 27834

(252)758-5628

Mattox, Davis, & Barnhill

315 W. 2nd Street

Greenville, NC 27858

(252) 758-3430

Poole, Richard C.

E. Arlington Blvd

Greenville, NC 27858

(252) 353-4455

Snyder, Vernon G., III

498 Red Banks Road

Greenville, NC 27858

(252) 321-7111

King, Jeremy 219 Cotanche Street

Greenville, NC 27834

(252) 752-5505

Closing Attorneys

30

Glossary of Terms

Abstract of Title: A summary of the public records relating to the ownership of a particular piece of land. It represents a short legal history of an individual piece of property, and traces the ownership of that property from the time of the first recorded transfer to present.

Acceptance: Consent to an offer to enter into contract.

Adjustable-rate mortgage (ARM): A mortgage that allows the interest rate to be changed periodically.

Agency: A legal relationship in which an owner-principal engages a broker-agent in the sale of property or a buyer-principal engages a broker-agent in the purchase of property.

American Society of Home Inspectors (ASHI): A professional trade association that provides training and education in home inspections. Members must meet qualification requirements to join.

Amortization: The gradual repayment of a mortgage by periodic installments.

Annual percentage rate (APR): The total finance charge (interest, loan fees, points) expressed as a percentage of the mortgage amount.

Appraisal: An evaluation of a piece of property to determine its value.

Appreciation: Increase in value due to any cause.

Asbestos: A mineral fiber used in some building materials such as flooring, siding, insulation and roofing. It is presently banned for most uses in real property.

Assessed value: The valuation placed on property by a public tax assessor as the basis of property taxes.

Assumption of mortgage: An agreement whereby the buyer assumes responsibility for a mortgage owed by the seller.

Balloon mortgage: A mortgage where the amount financed is not fully amortized over the period of the loan. When the loan becomes due, a large sum or “balloon” payment is required to satisfy the mortgage.

Bridge loan: A short-term mortgage made until a longer-term can be made; it’s sometimes used when a person needs money to build or purchase a home before the present one has been sold.

Broker: A person licensed by a state real estate commission to act independently in conducting a real estate brokerage business. Although requirements vary from state to state, an individual must usually have at least one year of experience in the industry and pass an examination to earn a broker’s license.

Building codes: State and local laws that regulate the construction of new property and the rehabilitation of existing property.

Cap: The maximum amount an interest rate or monthly payment can change, either at adjustment time or over the life of the mortgage.

Closing: The final step in the sale and transfer of ownership of a property. The title is transferred from the seller to the buyer; the buyer signs the mortgage and pays costs of settlement; any money due the seller and purchaser are paid.

Closing costs: Fees and expenses, not including the price of the home , payable by the seller and the buyer at the closing (e.g., brokerage commissions, title insurance premiums, home inspections, appraisal, recording and attorney fees).

31

Glossary of Terms

Closing Statement: A financial statement rendered to the buyer and seller at the time of transfer of ownership, giving an account of all funds received or expended.

Cloud on the title: Any condition which affects the clear title to real property.

Commercial bank: A financial institution authorized to provide a variety of financial services, including consumer and business loans (generally short-term), checking services, credit cards and savings accounts.

Comparables: Properties similar in size and character to the one being bought or sold.

Condominium: Ownership of a unit only, rather than of the entire building with the land.

Consideration: Anything of value to induce another to enter into a contract (i.e. money, services, a promise).

Contingency: A condition that must be satisfied before a contract is binding.

Contract: An agreement to do or not to do a certain thing.

Conventional mortgage: A fixed rate, fixed-term mortgage not insured by the federal government.

Deed: A legal document conveying title to a property.

Deed (quit claim): A deed that transfers only that title or right to a property that the holder of that title has at the time of the transfer. It does not warrant or guarantee a clear title.

Department of Housing and Urban Development (HUD): A U.S. Government agency established to implement certain federal housing and community development programs.

Disclosure laws: State and federal regulations which require sellers to disclose such conditions as whether a house is located in a flood plain or whether there are known defects in or affecting the property.

Earnest money: A portion of a down payment given to the seller by a potential buyer indicating the buyer’s intent to complete the purchase of the property.

Easement: A right to use the land of another.

Encroachment: A condition that limits the interest in a title to property such as a mortgage , deed restrictions, easement, unpaid taxes, etc.

Equity: The value of real estate over and above the liens against it. It is obtained by subtracting the total leins from the value.

Equity Mortgage: A mortgage based on the borrowers’ equity in their home rather than on their credit worthiness.

Escrow: The placement of money or documents with a third party for safekeeping pending the fulfillment or performance of a specified act or condition.

Federal Housing Administration (FHA): An agency within the Department of Housing and Urban Development (HUD) that administers loan guarantee programs and loan insurance programs to make more housing available.

Fannie Mae: Nickname for Federal National Mortgage Corp. (FNMA), a tax paying corporation created by Congress to support the secondary mortgages insured by FHA or guaranteed by VA, as well as conventional home mortgages.

32

Glossary of Terms FHA Insured mortgage: A mortgage under which the Federal Housing Administration insures loans made, according to its regulation, by approved lenders.

Fixed rate mortgage: A loan that fixes the interest rate at a prescribed rate for the duration of the loan.

Foreclosure: Procedure whereby property pledged as security for a debt is sold to pay the debt in the event of default.

Freddie Mac: Nickname for Federal Home Loan Mortgage Corp. (FHLMD), a federally controlled and operated corporation to support the secondary mortgage market. It purchases and sells residential conventional home mortgages.

Graduated-payment mortgage: A mortgage that starts with low monthly payment and increases at a predetermined rate.

Growing-equity mortgage: A mortgage loan in which the monthly payments increase by a specific amount each year, with the “Overpayments” applied to the principle.

Installment debts: Long-term debts that usually extend for more than one month.

Investor: The holder of a mortgage or the permanent lender for whom the mortgage maker services the loan. Any person or institution that invests in mortgages.

Joint & Survivorship Deed: (Also know as “Warranty deed creating tenants in common with right of survivorship”) Upon death of one of the owners, title to the interest transfers “by contract” to survivors.

Lease purchase agreement: Buyer makes a deposit for the future purchase of a property with the right to lease the property in the interim.

Lien: A legal claim against a property that must be paid when the property is sold.

Loan-to-value ratio: The relationship between the amount of a home mortgage and the total value of the property. Lenders may limit their maximum mortgage to 80-95 percent of value.

Lock-in-rate: A commitment made by lenders on a mortgage loan to “lock in” a civilian rate pending mortgage approval. Lock-in periods vary.

Market value: The highest price a buyer will pay for a property and the lowest price the seller will accept.

Mortgage: One type of document used to make property the security for the payment of a loan.

Mortgage broker: An individual or company that obtains mortgages for others by finding lending institutions, insurance companies, or private sources to lend the money; may also make collections and handle disbursements.

Mortgagee: The lender of money or the receiver of the mortgage.

Mortgagor: The borrower of money or the giver of the mortgage document.

Negative amortization: An increase in the outstanding balance of a mortgage resulting from the failure of periodic debt service payments to cover required interest charges on the loan.

Note: A written promise to pay a certain amount of money.

Origination fee: A fee or charge for work involved in the evaluation, preparation and submission of a

33

Glossary of Terms Pre-payment penalty: A fee paid to the mortgagee for paying the mortgage before it becomes due. Also known as a pre-payment fee or reinvestment fee.

Private mortgage insurance (PMI): Insurance issued to a lender by a private company to protect the lender against loss on a defaulted mortgage loan. Its use is usually limited to loans with high loan-to-value ratios. The borrower pays the premiums.

Promissory note: A written contract containing a promise to pay a definite amount of money at a definite future time.

Radon: A colorless, odorless gas formed by the breakdown of uranium in sub-soils. It can enter a house through cracks in the foundation or in water and is considered to be a health hazard.

REALTOR® and REALTOR®-Associate: Registered collective membership marks that identify real estate professionals who are members of the National Association of REALTORS® and who subscribe to its strict Code of Ethics.

Rent with option: A contract which gives one the right to lease property at a certain sum with the option to purchase at a future date.

Savings and loan association (S&Ls): Depository institutions that specialize in origination, servicing, and holding mortgage loans, primarily on owner-occupied residential property.

Savings Bank: A financial institution organized to hold individual depositors’ funds in interest-bearing accounts and to make long-term investments, such as home mortgage loans.

Second mortgage/Second deed of trust/Junior mortgage or Junior lien: An additional loan imposed on a property with a first mortgage. Generally a higher interest rate and shorter term than a “first” mortgage.

Severalty ownership: Ownership by one person only. Sole ownership.

Shared equity mortgage: A home loan in which an investor is granted a share of the equity, thereby allowing the investor to participate in the proceeds from resale.

Survey: The process by which a parcel of land is measured and its area ascertained.

Tenancy in common: Ownership by two or more persons who hold an undivided interest without right of survivorship. (In the event of the death of one owner, his/her share will pass to his/her heirs.)

Title: A document that’s evidence of ownership.

Title defect: An outstanding claim or encumbrance on property that affects marketability.

Title insurance: Protection for lenders and homeowners against financial loss resulting from legal defects in the title.

Veterans Administration (VA): A government agency that provides services for eligible veterans of the armed forces. Among other programs, it guarantees mortgage loans made by private lenders to veterans. Variance: A special suspension of zoning laws to allow the use of property in a manner not in accord with existing laws. Zoning restrictions: Local municipal ordinances that classify property according to specific uses such as single family, residential, commercial, industrial, multi-family, etc.