import trends - acsa · web viewimporters of dried fruit in romania increasing buy in bulk and...

TRANSCRIPT

The Romanian Market for Dried FruitsTarget Market Confirmation Study

Conducted by CAMIB for USAID/CNFA’s Agribusiness Development Project

February 2007

CONTENTS

Key observations and recommendations.....................................................................1

Background................................................................................................................2Global Production and Trade in Dried Fruits...........................................................2

Market access requirements and tariffs...................................................................7Legislative requirements..............................................................................................7

Food Safety, General...................................................................................................8

Marketing standards.....................................................................................................8

Other market requirements..........................................................................................9

Information on Companies Interviewed...................................................................9Channels of distribution..............................................................................................12

Produce Requirements and Preferences...................................................................12

Packaging.................................................................................................................. 13

Labeling......................................................................................................................14

Price data..................................................................................................................14Major competitors....................................................................................................16Moldovan Dried Fruits: Perceptions and Recommendations..............................17Annex 1 . List of reference materials..........................................................................18

Key observations and recommendations

This study looks at sales of dried fruits on the Romanian Market, including sales of retail packs of dried fruit. The key findings were as follows:

Many exporting countries supply dried fruits to Romania, including the Netherlands, Germany, Poland, Hungary, Austria, Belgium, China, Turkey, Taiwan and Malaysia.

According to the companies surveyed, the only Moldovan dried fruits sold in Romania are dried prunes.

Supermarkets and hypermarkets have taken an increasing share of consumer spending, concentrating buying power with fewer and fewer key buyers, who favor buying from large suppliers offering a wide range of products.

Importers of dried fruit in Romania increasing buy in bulk and repack products into retail packs labeled with the brands/labels of their supermarket customers.

The industrial market is considered to be the largest end user segment of the dried fruits market, and Moldovan exporters might consider looking for opportunities in this area.

Moldovan growers and exporters need to be aware that in order to supply the Romanian market, they will have to meet European Union standards for consumer health and safety requirements, (eg HACCP requirements), phytosanitary requirements, product quality and packaging standards, and importer’s requirements for quantity and frequency of delivery.

Since the arrival of the first international store in 1996, retail marketing in Romania has changed dramatically and rapidly. By the end of 2005, 182 huge new international supermarkets and hypermarkets were in operation1,2, with numbers continuing to increase during 2006, and new stores and retailers (eg the French chain Auchan) planned for 2007.

Initially concentrated around Bucharest, the supermarket chains have now expanded to other towns and cities across Romania. Comfortable shopping environments - warm in winter and air-conditioned in summer – they offer a wide range of competitively priced products to attract customers. Supermarkets and hypermarkets now account for 33% of all consumer spending in Romania, and are expected to account for 50% by 2010.

The majority of large retail chains in Romania have central buying and distribution centers based in Bucharest, that are responsible for purchasing products for all the stores in the Romanian chain. This system of centralized buying, combined with the rise in the volumes of products being sold in supermarkets and hypermarkets, has resulted in i) a small number of individuals/retail buyers responsible for buying huge volumes of food products, and ii) a significant reduction in the number of buyers for products retailed in Romania. In addition, strong price competition between the many retail chains to attract consumers, has resulted in downward pressure on prices paid to suppliers.

The 0% tariff Trade Agreement between Moldova and Romania ended in January 2007, when Romania joined the EU, and Moldovan exports to Romanian are now subject to EU tariffs. Under the EU’s Generalized System of Preference Plus System, (GSP+ system), a trade agreement between Moldova and the EU, dried fruits and vegetables produced and exported from Moldova to the EU will continue to attract a 0% tariff.

Moldovan exporters of dried fruits are advised to be aware of requirements and standards for organically produced dried fruits as demand for these products is increasing, including in Romania, and this sector represents an opportunity for entering international markets.

1 Source: Magazin Progresiv

2 14 hypermarkets (Carrefour, Cora, Intermarche, Kaufland); 71 supermarket (Billa; G’Market; Univers’All, Mega Image –; La Fourmi); 63 discount stores (Penny Market, ; XXL Mega Discount; Plus Discount; Profi; miniMAX DISCOUNT) and 34 Cash&Carry stores (Metro Cash&Carry; Selgros Cash&Carry )

Background

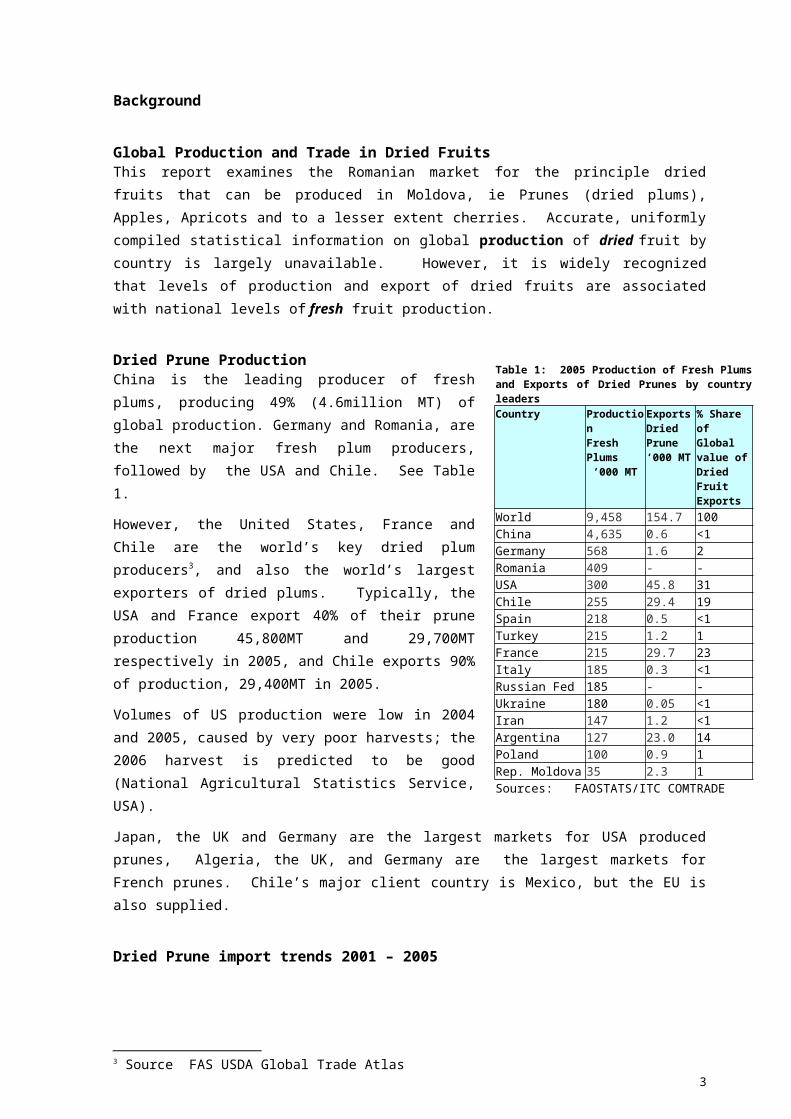

Global Production and Trade in Dried FruitsThis report examines the Romanian market for the principle dried fruits that can be produced in Moldova, ie Prunes (dried plums), Apples, Apricots and to a lesser extent cherries. Accurate, uniformly compiled statistical information on global production of dried fruit by country is largely unavailable. However, it is widely recognized that levels of production and export of dried fruits are associated with national levels of fresh fruit production.

Dried Prune ProductionChina is the leading producer of fresh plums, producing 49% (4.6million MT) of global production. Germany and Romania, are the next major fresh plum producers, followed by the USA and Chile. See Table 1.

However, the United States, France and Chile are the world’s key dried plum producers3, and also the world’s largest exporters of dried plums. Typically, the USA and France export 40% of their prune production 45,800MT and 29,700MT respectively in 2005, and Chile exports 90% of production, 29,400MT in 2005.

Volumes of US production were low in 2004 and 2005, caused by very poor harvests; the 2006 harvest is predicted to be good (National Agricultural Statistics Service, USA).

Japan, the UK and Germany are the largest markets for USA produced prunes, Algeria, the UK, and Germany are the largest markets for French prunes. Chile’s major client country is Mexico, but the EU is also supplied.

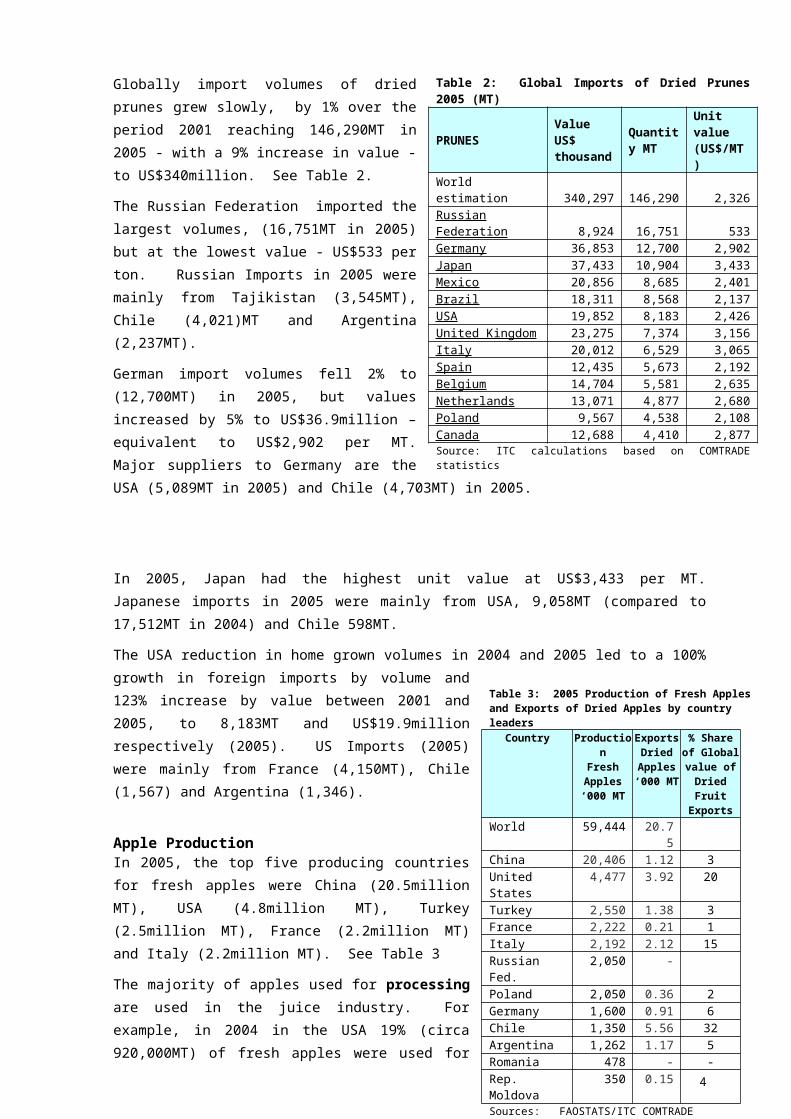

Dried Prune import trends 2001 – 2005Globally import volumes of dried prunes grew slowly, by 1% over the period 2001 reaching 146,290MT in 2005 - with a 9% increase in value - to US$340million. See Table 2.

The Russian Federation imported the largest volumes, (16,751MT in 2005) but at the lowest value - US$533 per ton. Russian Imports in 2005 were mainly from Tajikistan (3,545MT), Chile (4,021)MT and Argentina (2,237MT).

German import volumes fell 2% to (12,700MT) in 2005, but values increased by 5% to US$36.9million – equivalent to US$2,902 per MT. Major suppliers to Germany are the USA (5,089MT in 2005) and Chile (4,703MT) in 2005.

3 Source FAS USDA Global Trade Atlas

Table 1: 2005 Production of Fresh Plums and Exports of Dried Prunes by country leaders Country Production

Fresh Plums ‘000 MT

Exports Dried Prune‘000 MT

% Share of Global value of Dried Fruit Exports

World 9,458 154.7 100China 4,635 0.6 <1Germany 568 1.6 2Romania 409 - -USA 300 45.8 31Chile 255 29.4 19Spain 218 0.5 <1Turkey 215 1.2 1France 215 29.7 23Italy 185 0.3 <1Russian Fed 185 - -Ukraine 180 0.05 <1Iran 147 1.2 <1Argentina 127 23.0 14Poland 100 0.9 1Rep. Moldova 35 2.3 1Sources: FAOSTATS/ITC COMTRADE

Table 2: Global Imports of Dried Prunes 2005 (MT)

PRUNES Value US$ thousand

Quantity MT

Unit value (US$/MT)

World estimation 340,297 146,290 2,326Russian Federation 8,924 16,751 533Germany 36,853 12,700 2,902Japan 37,433 10,904 3,433Mexico 20,856 8,685 2,401Brazil 18,311 8,568 2,137USA 19,852 8,183 2,426United Kingdom 23,275 7,374 3,156Italy 20,012 6,529 3,065Spain 12,435 5,673 2,192Belgium 14,704 5,581 2,635Netherlands 13,071 4,877 2,680Poland 9,567 4,538 2,108Canada 12,688 4,410 2,877Source: ITC calculations based on COMTRADE statistics

2

In 2005, Japan had the highest unit value at US$3,433 per MT. Japanese imports in 2005 were mainly from USA, 9,058MT (compared to 17,512MT in 2004) and Chile 598MT.

The USA reduction in home grown volumes in 2004 and 2005 led to a 100% growth in foreign imports by volume and 123% increase by value between 2001 and 2005, to 8,183MT and US$19.9million respectively (2005). US Imports (2005) were mainly from France (4,150MT), Chile (1,567) and Argentina (1,346).

Apple ProductionIn 2005, the top five producing countries for fresh apples were China (20.5million MT), USA (4.8million MT), Turkey (2.5million MT), France (2.2million MT) and Italy (2.2million MT). See Table 3

The majority of apples used for processing are used in the juice industry. For example, in 2004 in the USA 19% (circa 920,000MT) of fresh apples were used for juice and cider production, and only an estimated 2% two percent of the fresh crop, around 97’000MT, was used in the drying industry4.

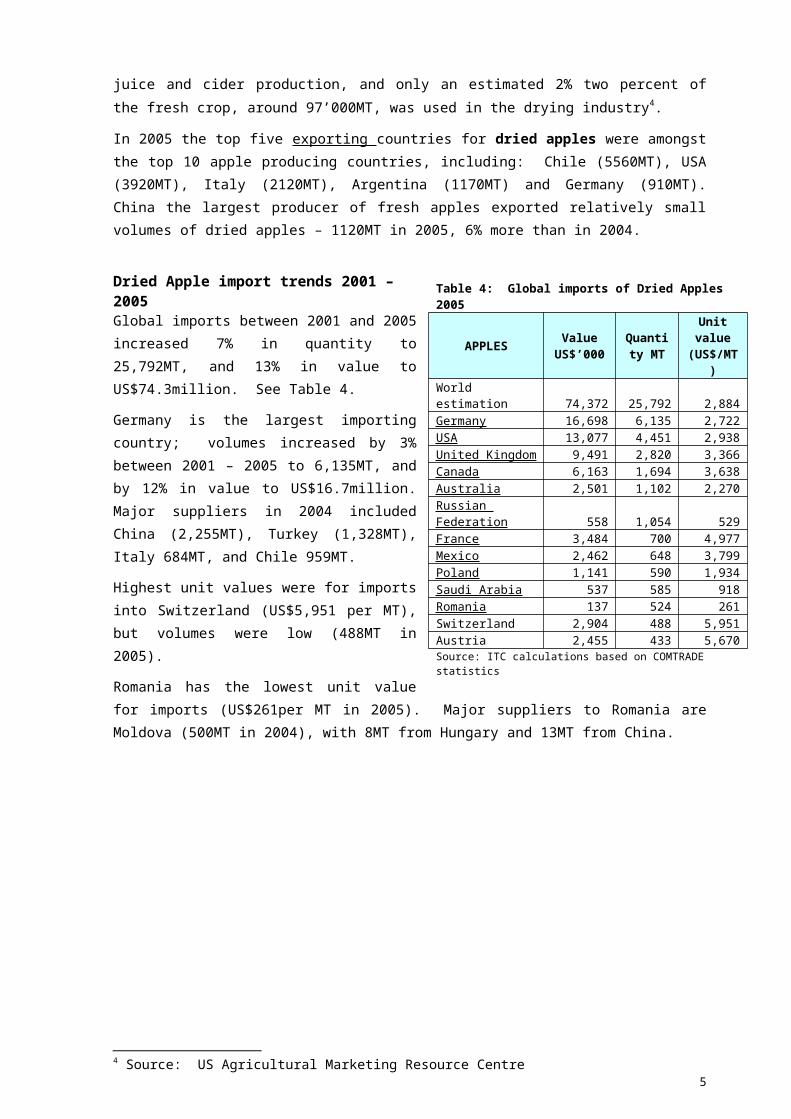

In 2005 the top five exporting countries for dried apples were amongst the top 10 apple producing countries, including: Chile (5560MT), USA (3920MT), Italy (2120MT), Argentina (1170MT) and Germany (910MT). China the largest producer of fresh apples exported relatively small volumes of dried apples – 1120MT in 2005, 6% more than in 2004.

Dried Apple import trends 2001 – 2005Global imports between 2001 and 2005 increased 7% in quantity to 25,792MT, and 13% in value to US$74.3million. See Table 4.

Germany is the largest importing country; volumes increased by 3% between 2001 – 2005 to 6,135MT, and by 12% in value to US$16.7million. Major suppliers in 2004 included China (2,255MT), Turkey (1,328MT), Italy 684MT, and Chile 959MT.

Highest unit values were for imports into Switzerland (US$5,951 per MT), but volumes were low (488MT in 2005).

Romania has the lowest unit value for imports (US$261per MT in 2005). Major suppliers to Romania are Moldova (500MT in 2004), with 8MT from Hungary and 13MT from China.

4 Source: US Agricultural Marketing Resource Centre

Table 3: 2005 Production of Fresh Apples and Exports of Dried Apples by country leaders

Country Production Fresh

Apples ‘000 MT

Exports Dried

Apples‘000 MT

% Share of Global

value of Dried Fruit

ExportsWorld 59,444 20.75China 20,406 1.12 3United States 4,477 3.92 20Turkey 2,550 1.38 3France 2,222 0.21 1Italy 2,192 2.12 15Russian Fed. 2,050 -Poland 2,050 0.36 2Germany 1,600 0.91 6Chile 1,350 5.56 32Argentina 1,262 1.17 5Romania 478 - -Rep. Moldova 350 0.15Sources: FAOSTATS/ITC COMTRADE

Table 4: Global imports of Dried Apples 2005

APPLES Value US$’000

Quantity MT

Unit value

(US$/MT)World estimation 74,372 25,792 2,884Germany 16,698 6,135 2,722USA 13,077 4,451 2,938United Kingdom 9,491 2,820 3,366Canada 6,163 1,694 3,638Australia 2,501 1,102 2,270Russian Federation 558 1,054 529France 3,484 700 4,977Mexico 2,462 648 3,799Poland 1,141 590 1,934Saudi Arabia 537 585 918Romania 137 524 261Switzerland 2,904 488 5,951Austria 2,455 433 5,670Source: ITC calculations based on COMTRADE statistics

3

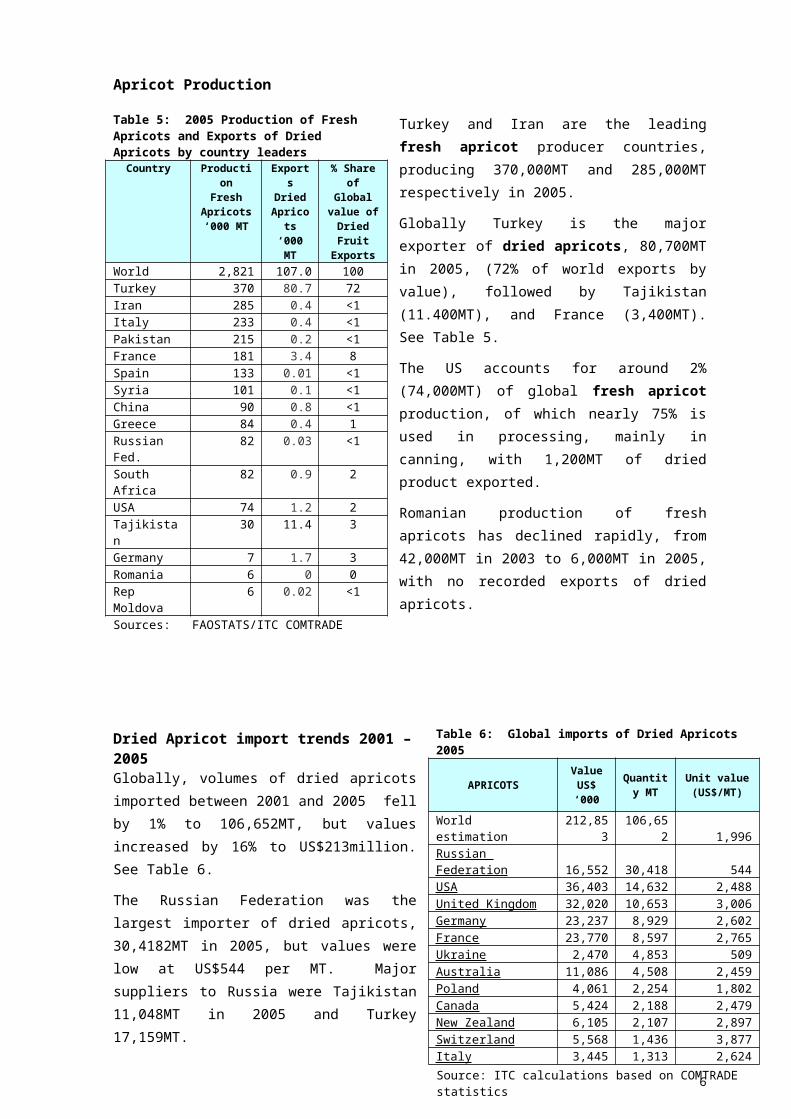

Apricot Production

Turkey and Iran are the leading fresh apricot producer countries, producing 370,000MT and 285,000MT respectively in 2005.

Globally Turkey is the major exporter of dried apricots, 80,700MT in 2005, (72% of world exports by value), followed by Tajikistan (11.400MT), and France (3,400MT). See Table 5.

The US accounts for around 2% (74,000MT) of global fresh apricot production, of which nearly 75% is used in processing, mainly in canning, with 1,200MT of dried product exported.

Romanian production of fresh apricots has declined rapidly, from 42,000MT in 2003 to 6,000MT in 2005, with no recorded exports of dried apricots.

Dried Apricot import trends 2001 – 2005Globally, volumes of dried apricots imported between 2001 and 2005 fell by 1% to 106,652MT, but values increased by 16% to US$213million. See Table 6.

The Russian Federation was the largest importer of dried apricots, 30,4182MT in 2005, but values were low at US$544 per MT. Major suppliers to Russia were Tajikistan 11,048MT in 2005 and Turkey 17,159MT.

The US is a major importer, (14,632MT) followed by the UK (10,653MT), France (8,597MT), Germany (8,929MT). Turkey is a major supplier to these three countries. In 2005 Turkey exported 14,022MT to the USA, 8,587MT to the UK, 8,349MT to France, and 7,898MT to Germany.

Romanian dried apricots imports in 2004 were worth US$138,000 (volumes not available). Major suppliers to Romania in 2004 were Turkey value US$107,000, and Netherlands US$24,000.

Table 5: 2005 Production of Fresh Apricots and Exports of Dried Apricots by country leaders

Country Production Fresh

Apricots‘000 MT

Exports Dried

Apricots‘000 MT

% Share of Global value of

Dried Fruit Exports

World 2,821 107.0 100Turkey 370 80.7 72Iran 285 0.4 <1Italy 233 0.4 <1Pakistan 215 0.2 <1France 181 3.4 8Spain 133 0.01 <1Syria 101 0.1 <1China 90 0.8 <1Greece 84 0.4 1Russian Fed. 82 0.03 <1South Africa 82 0.9 2USA 74 1.2 2Tajikistan 30 11.4 3Germany 7 1.7 3Romania 6 0 0Rep Moldova 6 0.02 <1Sources: FAOSTATS/ITC COMTRADE

Table 6: Global imports of Dried Apricots 2005

APRICOTSValue US$ ‘000

Quantity MT

Unit value (US$/MT)

World estimation 212,853 106,652 1,996Russian Federation 16,552 30,418 544USA 36,403 14,632 2,488United Kingdom 32,020 10,653 3,006Germany 23,237 8,929 2,602France 23,770 8,597 2,765Ukraine 2,470 4,853 509Australia 11,086 4,508 2,459Poland 4,061 2,254 1,802Canada 5,424 2,188 2,479New Zealand 6,105 2,107 2,897Switzerland 5,568 1,436 3,877Italy 3,445 1,313 2,624Source: ITC calculations based on COMTRADE statistics

4

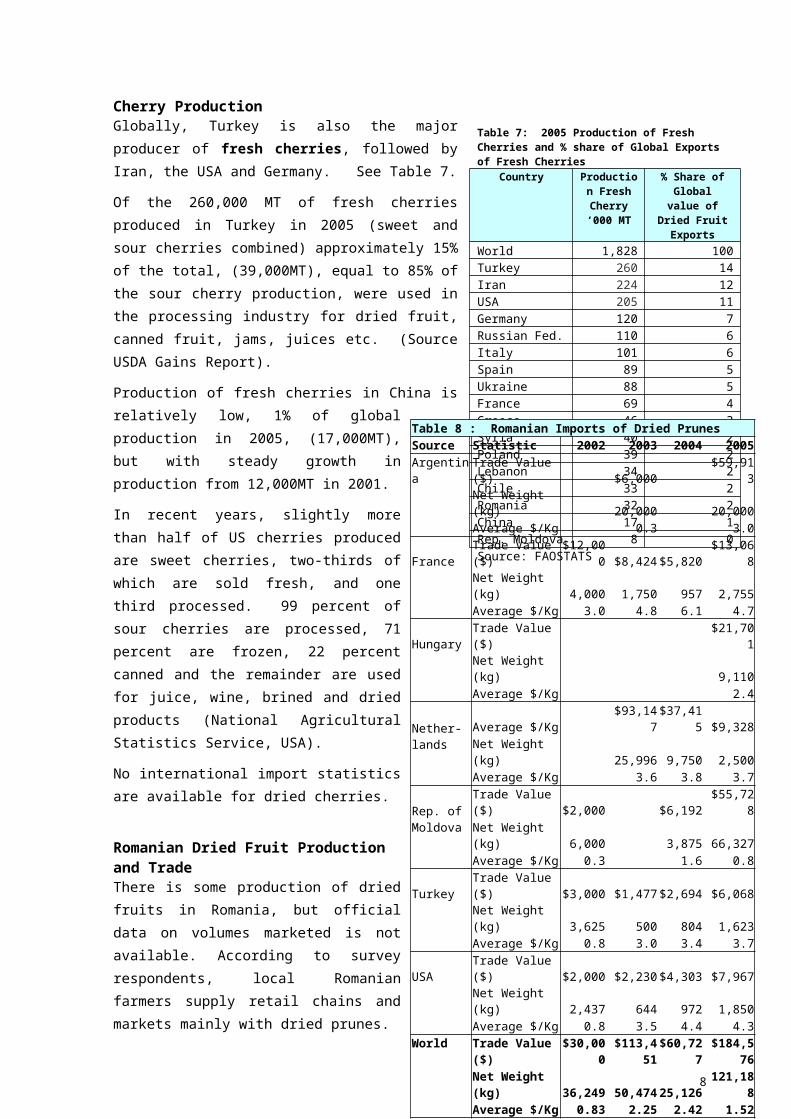

Cherry ProductionGlobally, Turkey is also the major producer of fresh cherries, followed by Iran, the USA and Germany. See Table 7.

Of the 260,000 MT of fresh cherries produced in Turkey in 2005 (sweet and sour cherries combined) approximately 15% of the total, (39,000MT), equal to 85% of the sour cherry production, were used in the processing industry for dried fruit, canned fruit, jams, juices etc. (Source USDA Gains Report).

Production of fresh cherries in China is relatively low, 1% of global production in 2005, (17,000MT), but with steady growth in production from 12,000MT in 2001.

In recent years, slightly more than half of US cherries produced are sweet cherries, two-thirds of which are sold fresh, and one third processed. 99 percent of sour cherries are processed, 71 percent are frozen, 22 percent canned and the remainder are used for juice, wine, brined and dried products (National Agricultural Statistics Service, USA).

No international import statistics are available for dried cherries.

Romanian Dried Fruit Production and TradeThere is some production of dried fruits in Romania, but official data on volumes marketed is not available. According to survey respondents, local Romanian farmers supply retail chains and markets mainly with dried prunes.

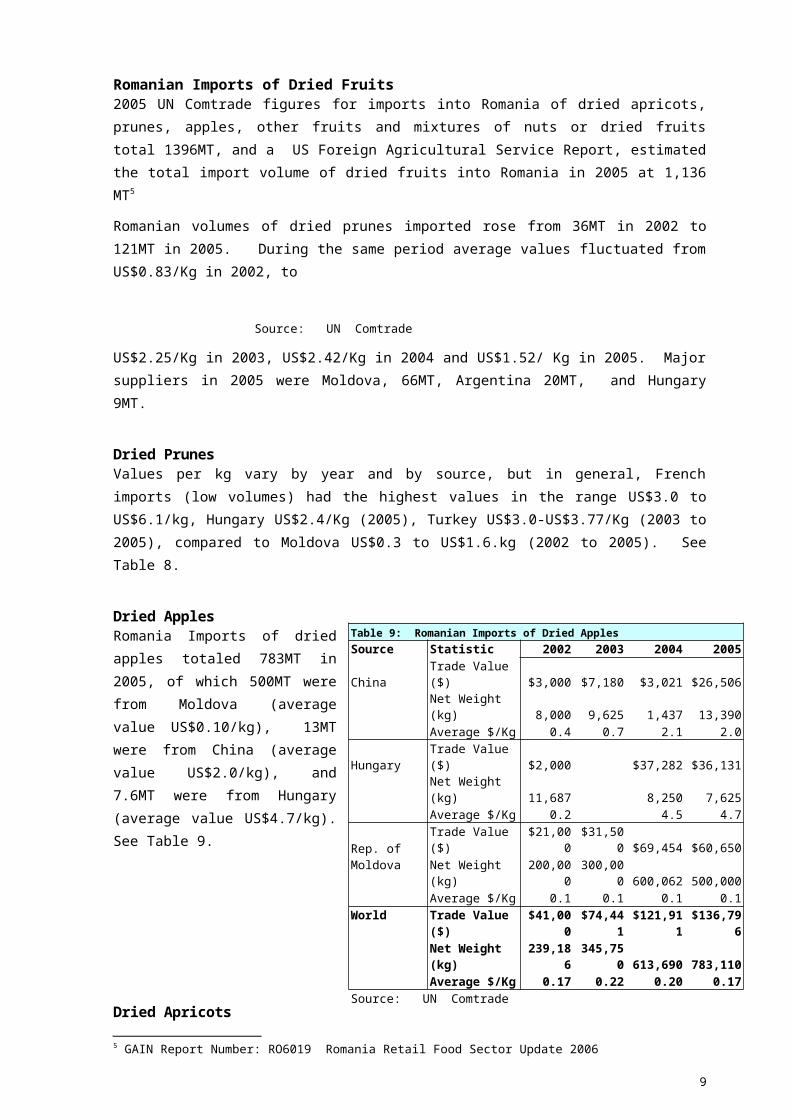

Romanian Imports of Dried Fruits2005 UN Comtrade figures for imports into Romania of dried apricots, prunes, apples, other fruits and mixtures of nuts or dried fruits total 1396MT, and a US Foreign Agricultural Service Report, estimated the total import volume of dried fruits into Romania in 2005 at 1,136 MT5

Romanian volumes of dried prunes imported rose from 36MT in 2002 to 121MT in 2005. During the same period average values fluctuated from US$0.83/Kg in 2002, to

Source: UN Comtrade

5 GAIN Report Number: RO6019 8Romania Retail Food Sector Update 2006

Table 7: 2005 Production of Fresh Cherries and % share of Global Exports of Fresh Cherries

Country Production Fresh Cherry‘000 MT

% Share of Global value of

Dried Fruit Exports

World 1,828 100Turkey 260 14Iran 224 12USA 205 11Germany 120 7Russian Fed. 110 6Italy 101 6Spain 89 5Ukraine 88 5France 69 4Greece 46 3Syria 40 2Poland 39 2Lebanon 34 2Chile 33 2Romania 32 2China 17 1Rep. Moldova 8 0Source: FAOSTATS

Table 8 : Romanian Imports of Dried PrunesSource Statistic 2002 2003 2004 2005Argentina Trade Value ($) $6,000 $59,913 Net Weight (kg) 20,000 20,000 Average $/Kg 0.3 3.0France Trade Value ($) $12,000 $8,424 $5,820 $13,068 Net Weight (kg) 4,000 1,750 957 2,755 Average $/Kg 3.0 4.8 6.1 4.7Hungary Trade Value ($) $21,701 Net Weight (kg) 9,110 Average $/Kg 2.4Nether-lands

Average $/Kg $93,147 $37,415 $9,328Net Weight (kg) 25,996 9,750 2,500

Average $/Kg 3.6 3.8 3.7Rep. of Moldova

Trade Value ($) $2,000 $6,192 $55,728

Net Weight (kg) 6,000 3,875 66,327 Average $/Kg 0.3 1.6 0.8Turkey Trade Value ($) $3,000 $1,477 $2,694 $6,068 Net Weight (kg) 3,625 500 804 1,623 Average $/Kg 0.8 3.0 3.4 3.7USA Trade Value ($) $2,000 $2,230 $4,303 $7,967 Net Weight (kg) 2,437 644 972 1,850 Average $/Kg 0.8 3.5 4.4 4.3World

Trade Value ($) $30,000$113,45

1 $60,727$184,57

6Net Weight (kg) 36,249 50,474 25,126 121,188Average $/Kg 0.83 2.25 2.42 1.52

5

US$2.25/Kg in 2003, US$2.42/Kg in 2004 and US$1.52/ Kg in 2005. Major suppliers in 2005 were Moldova, 66MT, Argentina 20MT, and Hungary 9MT.

Dried PrunesValues per kg vary by year and by source, but in general, French imports (low volumes) had the highest values in the range US$3.0 to US$6.1/kg, Hungary US$2.4/Kg (2005), Turkey US$3.0-US$3.77/Kg (2003 to 2005), compared to Moldova US$0.3 to US$1.6.kg (2002 to 2005). See Table 8.

Dried ApplesRomania Imports of dried apples totaled 783MT in 2005, of which 500MT were from Moldova (average value US$0.10/kg), 13MT were from China (average value US$2.0/kg), and 7.6MT were from Hungary (average value US$4.7/kg). See Table 9.

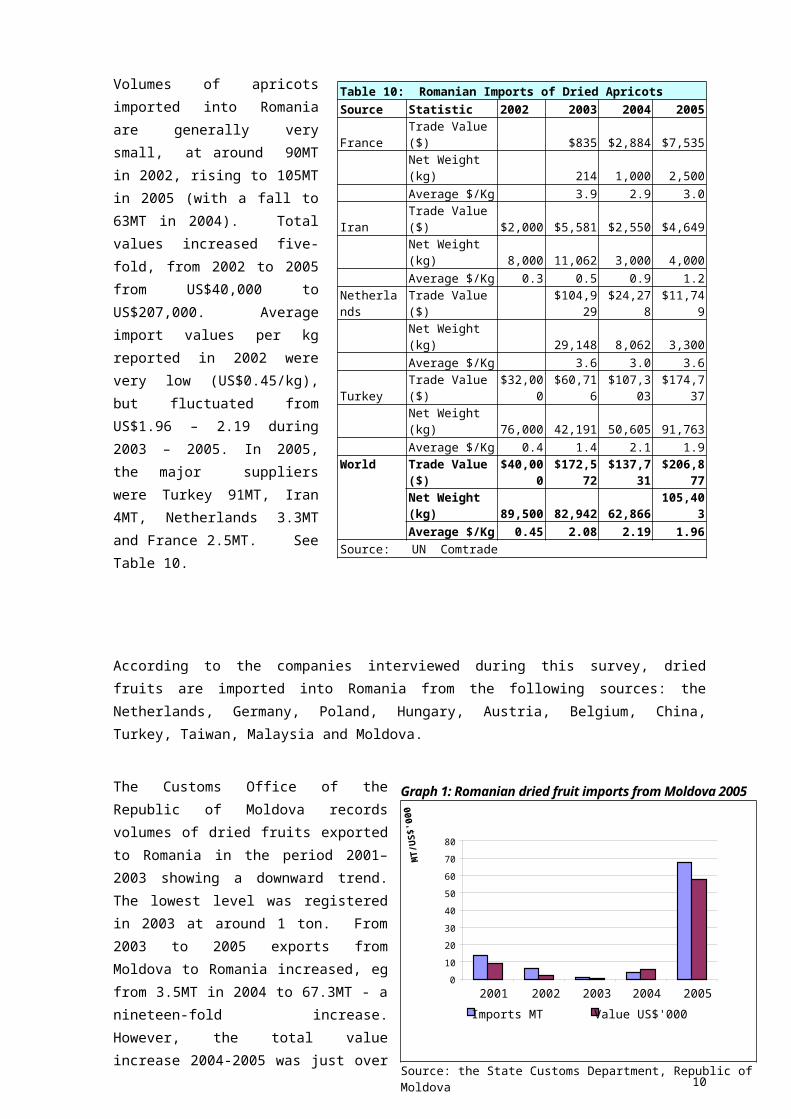

Dried ApricotsVolumes of apricots imported into Romania are generally very small, at around 90MT in 2002, rising to 105MT in 2005 (with a fall to 63MT in 2004). Total values increased five-fold, from 2002 to 2005 from US$40,000 to US$207,000. Average import values per kg reported in 2002 were very low (US$0.45/kg), but fluctuated from US$1.96 – 2.19 during 2003 – 2005. In 2005, the major suppliers were Turkey 91MT, Iran 4MT, Netherlands 3.3MT and France 2.5MT. See Table 10.

According to the companies interviewed during this survey, dried fruits are imported into Romania from the following sources: the Netherlands, Germany, Poland, Hungary, Austria, Belgium, China, Turkey, Taiwan, Malaysia and Moldova.

Table 9: Romanian Imports of Dried ApplesSource Statistic 2002 2003 2004 2005China Trade Value ($) $3,000 $7,180 $3,021 $26,506 Net Weight (kg) 8,000 9,625 1,437 13,390 Average $/Kg 0.4 0.7 2.1 2.0Hungary Trade Value ($) $2,000 $37,282 $36,131 Net Weight (kg) 11,687 8,250 7,625 Average $/Kg 0.2 4.5 4.7Rep. of Moldova

Trade Value ($) $21,000 $31,500 $69,454 $60,650

Net Weight (kg) 200,000 300,000 600,062 500,000 Average $/Kg 0.1 0.1 0.1 0.1World Trade Value ($) $41,000 $74,441 $121,911 $136,796

Net Weight (kg) 239,186 345,750 613,690 783,110Average $/Kg 0.17 0.22 0.20 0.17

Source: UN Comtrade

Table 10: Romanian Imports of Dried ApricotsSource Statistic 2002 2003 2004 2005France Trade Value ($) $835 $2,884 $7,535 Net Weight (kg) 214 1,000 2,500 Average $/Kg 3.9 2.9 3.0Iran Trade Value ($) $2,000 $5,581 $2,550 $4,649 Net Weight (kg) 8,000 11,062 3,000 4,000 Average $/Kg 0.3 0.5 0.9 1.2

Netherlands Trade Value ($) $104,92

9 $24,278 $11,749 Net Weight (kg) 29,148 8,062 3,300 Average $/Kg 3.6 3.0 3.6

Turkey Trade Value ($) $32,000 $60,716$107,30

3$174,73

7 Net Weight (kg) 76,000 42,191 50,605 91,763 Average $/Kg 0.4 1.4 2.1 1.9World

Trade Value ($) $40,000$172,57

2$137,73

1$206,87

7Net Weight (kg) 89,500 82,942 62,866 105,403Average $/Kg 0.45 2.08 2.19 1.96

Source: UN Comtrade

6

The Customs Office of the Republic of Moldova records volumes of dried fruits exported to Romania in the period 2001–2003 showing a downward trend. The lowest level was registered in 2003 at around 1 ton. From 2003 to 2005 exports from Moldova to Romania increased, eg from 3.5MT in 2004 to 67.3MT - a nineteen-fold increase. However, the total value increase 2004-2005 was just over ten-fold, from $5,000 to $57,000 – resulting in a unit price (price per kg) decrease from $1.58/kg to $0.9kg. See Graph 1.

Market access requirements and tariffsUnder the Free Trade Agreements between Moldova and Romania, exports of fruits and vegetables, including dried fruits, from Moldova to Romania were subject to zero percent tariff. Since 1 January 2007 when Romania acceded to the EU, Moldovan products exported to Romania have been subject to standard EU tariffs.

Preferential trade tariffs have been set for some products, under an EU/Moldova trade agreement – the Generalized System of Preferences Plus (GSP+), which is effective for the period 1 January 2006 to 31 December 2008. This sets a 0% General Tariff, on some products, including dried fruits (International customs codes: 0813.20 – prunes, 0813.30 – dried apples, 0813.50 – dried fruits mixes, 0813.40 – others – e.g. cherries) provided that the share of Moldovan product on the EU market does not exceed 15% of all imported volumes6, and is a competitive advantage for Moldovan producers and exporters.

Table 11 below presents an overview of EU conventional and GSP+ import tariffs for dried fruit products7.

Table 11: EU tariffs for products from conventional and GSP+ status countriesHS code Product Conventional GSP+0813 20 00 dried prunes 9.6% 0%0813 30 00 dried apples 3.2% 0%0813 40 70/95 other dried fruit 2.4% 0%0813 50 12/15/19/91/99 mixtures of dried fruit 4-9.6% 0%

Source: http://export-help.cec.eu.int

Legislative requirementsExporters to EU countries, including Romania, have to meet many legislative requirements. These include, but are not limited to:

1. Food Safety Requirements eg HACCP

2. Packaging Requirements (Food Safety and Environmental Issues)

3. Environmental requirements in the country of production

4. Worker Health and Safety Requirements

Food Safety, GeneralExporters to EU countries must be aware of the following:6 Source: List of goods benefiting from the EU’s GSP PLUS System7 Import tariffs change frequently and depend on trade agreements between the EU and countries with GSP+ status, and the sensitivity of the product for EU producers. An up-to-date list of import tariffs can be downloaded at http://exporthelp.cec.eu.int.

Graph 1: Romanian dried fruit imports from Moldova 2005

Source: the State Customs Department, Republic of Moldova

7

0

10

20

30

40

50

60

70

80

2001 2002 2003 2004 2005ar

Imports MT Value US$'000

MT/

US$

'000

Since 1 January 2006, Regulation (EC) 852/2004, EU importers are only allowed to buy from processed food manufacturers – anywhere in the world - who are HACCP Food Safety systems in place.

EU Food Safety Directives and Regulations exist setting limits for:

Additives and levels of additives in food, eg. levels of sulphur dioxide

Dried fruit Additive Max. concentrationApricots, peaches, grapes, plums, figs

Sulphur dioxide 2000 mg/kg

Bananas Sulphur dioxide 1000 mg/kgOthers Sulphur dioxide 500 mg/kgSource: EU Directive 95/2/EC on food additives (CBI EU Market Brief – Dried Fruit - November 2005)

Levels of microbial contamination, or contamination with microbial toxins eg aflatoxins, Ochratoxin A

Maximum levels of heavy metals in fruits (eg mercury, copper, cadmium etc)

Maximum Residue levels (MRLs) of pesticides in foods

All packaging which comes into contact with food must comply with EU food safety legislation, referring mainly to the components used in the manufacture of the packaging.

Requirements and residue levels currently can vary in different EU countries, and should be discussed with importers/potential clients in export destination countries. (Where there are no individual country levels specified, standard EU levels are applied). For background information, an English language overview and analysis of requirements can be found in the CBI’s Access Guide8, (h ttp://www.cbi.nl/marketinfo/cbi/?action=showDetails&id=61 ).

Marketing standardsThere are no EU marketing standards for dried fruits. However, rules governing EU minimum standards for prunes (which form part of aid schemes intended for EU growers - not marketing standards) can be found in 20 languages at: http://europa.eu.int/smartapi/cgi/sga_doc?smartapi!celexplus!prod!CELEXnumdoc&numdoc=31999R0464&lg=en These standards should be of interest to dried fruit producers.

Globally there are marketing standards, and Moldovan exporters would be wise to familiarize themselves with these standards, and not to offer products inferior to these standards, to EU importers.

1. UN/ECE standards

The Economic Commission for Europe of the United Nations (UN/ECE) has established standards for the marketing and quality control of a range of dried fruit including dried apples, apricots, dates, figs, grapes, pears and prunes.

These standards are in line with the demands of EU countries and can be downloaded in English, French or Russian from: http://www.unece.org/trade/agr/standard/dry/dry_e.htm

8 This website is free of charge, and has much interesting information. Visitors however are required to register their contact details in order to obtain a login name and password.

8

2. USA standards

These standards are only offered in the English language, and they do not legally apply to European countries. However, they are worth consideration by Moldovan exporters as they set out the minimum standards applied by the USA as a major dried fruit manufacturer, consumer and exporter to markets of interest to Moldovans.

USA standard for dried prunes: http://www.ams.usda.gov/standards/drdprune.pdf

USA standard for dried apricots: http://www.ams.usda.gov/standards/driaprco.pdf

USA standard for dried apples: http://www.agribusinessonline.com/regulations/grades/grades_us_dried/dhapples.pdf

3. Commercial Standards

Exporters should also be aware that individual processing and retailing companies generally have their own specifications for the products they will buy. These commercial specifications are generally of a far higher standard than UN or Country standards, with lower levels of tolerances for defects.

Other market requirementsWorker social, health and safety issues in the country of production are increasingly important to EU buyers, as is protection of the environment. These issues are therefore important for potential exports to the EU. EU Retailer and national protocols exist – eg EUREPGAP® and the widely required British Retail Consortium (BRC) Ethical Guide.

Romanian regulations also require that local importers obtain prior approval from phytosanitary officials for dried fruits.

Information on Companies InterviewedSupermarkets

1. Cora SRL - There are 81 Cora hypermarkets in France, Romania, Hungary, Belgium, and Luxembourg. Globally, Cora supermarkets’ annual turnover amounts to € 4.8 billion. There are three supermarkets in Romania: Cora Pantelimon, Cora Lujerului and Cora Cluj-Napoca.

2. Billa SRL - In Romania the Eurobilla group is represented by the network of Billa supermarkets. At present Billa has 18 branches all over Romania, each of which is about 1000-2400 square meters. Billa is a part of German Group REWE, that comprises about 1000 supermarkets in Austria and, through Eurobilla, 300 supermarkets in Italy, Czech Republic, Slovakia, Romania, Croatia, Ukraine, Bulgaria, and Russia.

3. Univers'all - is the brand name of the first exclusively national Romanian network of supermarkets. The first supermarket opened in 2002. Univers’all is a relatively new player in retail trade, offering a large assortment of food and nonfood products. Univers’all network has 6 supermarkets all over Romania and one hypermarket in Bucharest.

4. Kaufland Romania SCS The Kaufland Group is one of the most successful German retail companies, represented by 600 supermarkets in Germany, Czech Republic, Slovakia, Poland, Croatia, with one store in Romania. These supermarkets have a total commercial surface ranging from 2 500 sq.m. to 12 000 sq.m. and are known as „Kaufland“, "KaufMarkt“ and „Handelshof“.

5. Pic SRL – was opened in Pitesti, in 1991. It deals with production, acquizition, transportation and trade. At present, Pic distribution channels cover Pitesti, Bucuresti,

9

Brasov, Craiova, Sibiu, Constanta and Cluj. The products distributed by PIC are available in Metro, Carrefour, Selgros, Billa, XXL, Mega Image etc. Annual turnover is 0.3 bln Romanian lei (RON), and the company is planning to expand in the future.

Wholesalers1. METRO CASH&CARRY can be found in over twenty-seven countries, in Europe, Asia,

North Africa, and CIS regions. It was the first international retailer to enter the Romanian market (in 1996). The initial plans were to create only 10 cash & carry shops, but at the end of 2005 the network expanded to 23 stores, 4 of which are located in Bucharest. Metro will merge with its subsidiary REAL in 2007, when they hope to have a combined Metro/REAL chain of 40 stores

2. SC “Orlando Import Export 2001” SRL was set up in 1994. The company supplies well known retailers in Romania, including: Selgros, Carrefour, Cora, Kaufland, Univers'all, La Fourmi, Pic, etc. The company turnover on December 31, 2005 was 334200 Euro.

3. SC “BATUL MICRO IMPEX” SRL is one of the largest dried fruit importers in Romania importing a wide range of products, including dried apricots, raisins, dried pineapple, melon, cherries, prunes, peaches, mango, papaya and nuts.

4. SC “3SYS SOLUTIONS” SRL. is a Business-to-Business (B2B) company which organises the supply of raw material, trade of final products and services. The company has over 500 business partners from different countries such as China, Taiwan, Malaysia, Turkey, Vietnam and others.

5. SC “PARTENOPE FRUTTA” S.R.L. is a modern and dynamic plant with modern technologies, offering dried fruits, including cherries, of high quality and distributing them all over the world (America, Europe, Asia, Australia and South Africa etc.).

Sources of supplyThe companies interviewed, (including 3SYS Solutions Srl, Batul Micro Impex SRL, Partenope Frutta S.R.L., METRO Cash&Carry and Selgros Cash & Carry) all

sell dried prunes, dried apples and dried cherries. According to these companies:

80% of dried prunes, apples and cherries sold are of local origin, with only 20% imported from abroad.

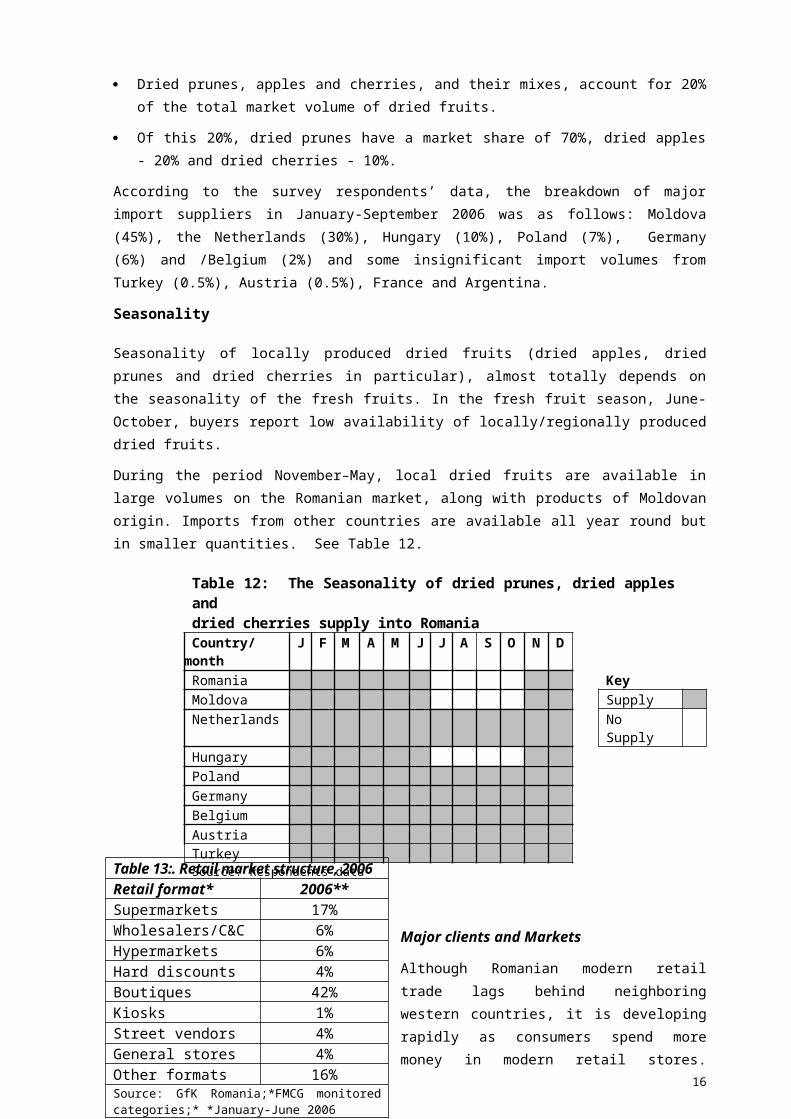

Dried prunes, apples and cherries, and their mixes, account for 20% of the total market volume of dried fruits.

Of this 20%, dried prunes have a market share of 70%, dried apples - 20% and dried cherries - 10%.

According to the survey respondents’ data, the breakdown of major import suppliers in January-September 2006 was as follows: Moldova (45%), the Netherlands (30%), Hungary (10%), Poland (7%), Germany (6%) and /Belgium (2%) and some insignificant import volumes from Turkey (0.5%), Austria (0.5%), France and Argentina.

Seasonality

Seasonality of locally produced dried fruits (dried apples, dried prunes and dried cherries in particular), almost totally depends on the seasonality of the fresh fruits. In the fresh fruit season, June-October, buyers report low availability of locally/regionally produced dried fruits.

10

During the period November–May, local dried fruits are available in large volumes on the Romanian market, along with products of Moldovan origin. Imports from other countries are available all year round but in smaller quantities. See Table 12.

Major clients and Markets

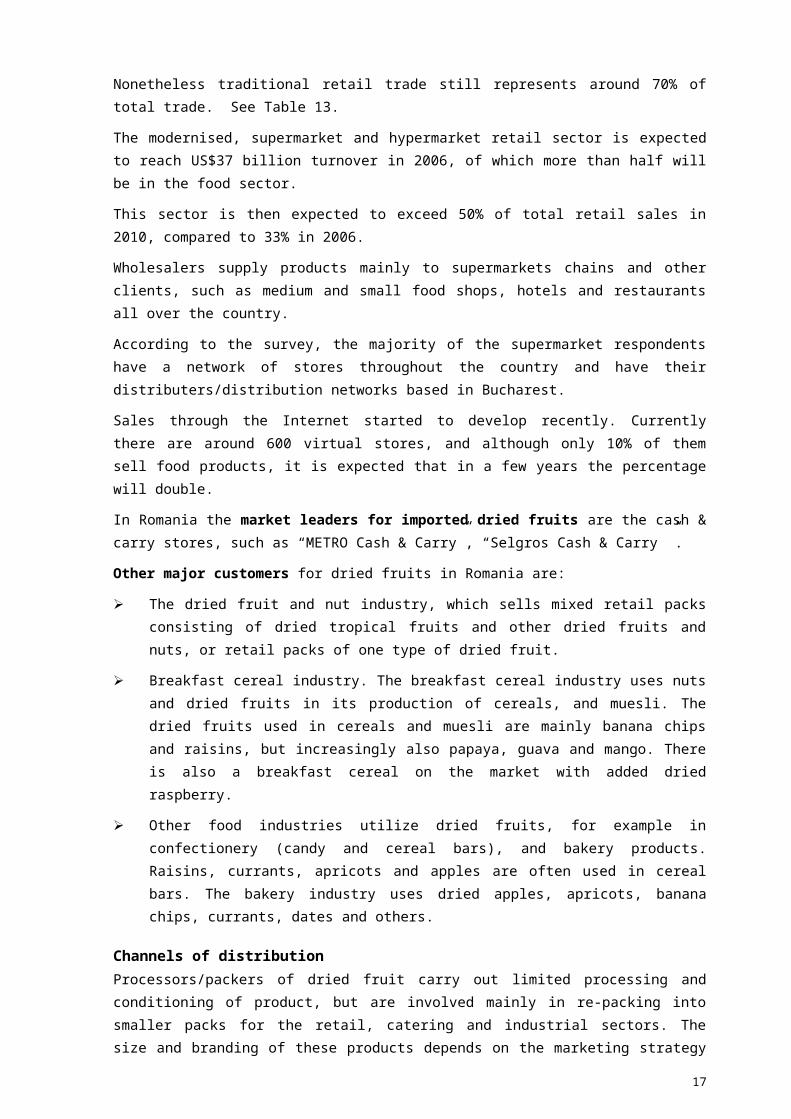

Although Romanian modern retail trade lags behind neighboring western countries, it is developing rapidly as consumers spend more money in modern retail stores. Nonetheless traditional retail trade still represents around 70% of total trade. See Table 13.

The modernised, supermarket and hypermarket retail sector is expected to reach US$37 billion turnover in 2006, of which more than half will be in the food sector.

This sector is then expected to exceed 50% of total retail sales in 2010, compared to 33% in

2006.

Wholesalers supply products mainly to supermarkets chains and other clients, such as medium and small food shops, hotels and restaurants all over the country.

According to the survey, the majority of the supermarket respondents have a network of stores throughout the country and have their distributers/distribution networks based in Bucharest.

Sales through the Internet started to develop recently. Currently there are around 600 virtual stores, and although only 10% of them sell food products, it is expected that in a few years the percentage will double.

In Romania the market leaders for imported dried fruits are the cash & carry stores, such as “METRO Cash & Carry”, “Selgros Cash & Carry ”.

Other major customers for dried fruits in Romania are:

The dried fruit and nut industry, which sells mixed retail packs consisting of dried tropical fruits and other dried fruits and nuts, or retail packs of one type of dried fruit.

Breakfast cereal industry. The breakfast cereal industry uses nuts and dried fruits in its production of cereals, and muesli. The dried fruits used in cereals and muesli are mainly

Table 12: The Seasonality of dried prunes, dried apples and dried cherries supply into RomaniaCountry/month J F M A M J J A S O N DRomania Key Moldova Supply Netherlands No Supply Hungary Poland Germany Belgium Austria Turkey Source: Respondents data

Table 13:. Retail market structure, 2006Retail format* 2006**Supermarkets 17%Wholesalers/C&C 6%Hypermarkets 6%Hard discounts 4%Boutiques 42%Kiosks 1%Street vendors 4%General stores 4%Other formats 16%Source: GfK Romania;*FMCG monitored categories;* *January-June 2006

11

banana chips and raisins, but increasingly also papaya, guava and mango. There is also a breakfast cereal on the market with added dried raspberry.

Other food industries utilize dried fruits, for example in confectionery (candy and cereal bars), and bakery products. Raisins, currants, apricots and apples are often used in cereal bars. The bakery industry uses dried apples, apricots, banana chips, currants, dates and others.

Channels of distributionProcessors/packers of dried fruit carry out limited processing and conditioning of product, but are involved mainly in re-packing into smaller packs for the retail, catering and industrial sectors. The size and branding of these products depends on the marketing strategy of the processor/packer. Some of them have their own brand, whilst others pack according to their customers' specifications, e.g. for supermarkets. Larger packers/processors are increasingly buying directly from processors/exporters in the countries of origin.

The industrial market is probably the largest end user. Slow expansion in sales of imported dried fruit reflects the growth in demand of convenience foods and especially those products perceived to have "healthy" ingredients.

The catering sector is a relatively unimportant buyer of dried fruit, with usage mainly confined to ingredients for food preparation.

According to the survey, retail sector sales are dominated by the supermarket sector, believed to market over 85% of all dried fruit sold directly to consumers in Romania Supermarkets buy pre-packed branded consumer packs, or sometimes contract packers to pack consumer packs using the supermarket’s own-label or brand. In the retail sector, "loose" dried/dehydrated fruit is hardly sold anymore, and is found only in health food shops, specialist dried fruit and nut shops, and in stalls at street markets.

Scheme 1. Distribution channels for imported dried fruits

Produce Requirements and PreferencesSize Requirements

Amongst the companies interviewed, the smallest acceptable prunes are 30-40 mm in diameter. Some importers, however, require the size of 40-50 mm. With regard to dried apples and cherries, no special requirements were required by the customers interviewed.

Samples of supplier specifications for dried fruits exported to Romania include:

12

Retail shops (supermarkets, shops, confectionery outlets)

Consumers

Small processing companies Wholesalers of confectionery products

Importers

Large processing companies

(Commercial use)

(Consumer use)

Wholesalers of food products

Processing companies

Foreign producers

Product Specification PictureApple dice

Moisture: 18-22 % Max Sо2: 2000PPM Max.

Dried Sour Cherry

Moisture:18-22% SO2:300ppm Max Sugar:65%+/-5%

Apple rings

Moisture: 18-22 % Max Sо2: 2000PPM Max

Apple rings Moisture 24% Max. So2:1700ppm Max.600ppm Max.

Prunes 30-40 mm40-50 mm

PackagingPresentation of a product, in particular the packaging, is important, making merchandise more or less saleable. When similar products, of similar quality and price are offered, packaging and presentation become very important. Attractive packaging sells merchandise and well-designed packaging can increase the turnover of a manufacturer.

According to the survey, Romanian products are still poorly packaged.

The exporter must consider the following general rules regarding packaging:

Packaging material must be strong enough to protect the product during transportation; Packaging should ensure that no contamination, mould growth, etc. can take place; Excessive packaging must be avoided (this increases cost and is less environmentally

friendly); The exporter must investigate thoroughly and use materials that are as environmentally

friendly as possible; The exporter must try to reduce the use of PVC, Chlorine, Cadmium and CFCs (in the EU,

the maximum permissible concentrations of lead, cadmium, mercury and chromium in packaging are 100ppm as of 30 June 2001);

The use of staples, nails or other metal should be avoided; If using different types of packaging materials is unavoidable, these must be separable; Information must be given on the nature and quantity of packaging materials; Vacuum packaging and/or nitrogen flushing are sometimes requested for bulk export

packaging. The effectiveness of the packaging in preserving good product quality depends on very clean packaging conditions, an absolute minimum of delay between processing and packaging, and complete air tightness of the package seals.

Retail and wholesale packaging: The most common bulk packaging for exported dry fruits is 10 kg and 12.5 kg carton boxes. Some respondents said that dried prunes are imported to Romania in paper bags of 20-25 kg, and cherries and apples in carton boxes of 3-5 kg.

13

The most common retail packaging used includes cellophane packs, trays and plastic bags of 200g, 250g or 500g capacity. Packs may be transparent, allowing the product to be seen, or totally opaque, imprinted with colors.

Plastic boxes 200gr, 250gr

Dried apples in 250gr, 500 gr plastic bags

Tray of 200gr, 250gr

Dried apples in 250gr, 500 gr plastic bags

Mixed fruits in 200gr, 250gr

500gr, 1kg packs*

Photographs from the Romanian web site www.orlandos.ro , (printed with the permission of Orlando).

Some retail chains prefer to sell products under their own Private Label. In Romania these include: Carrefour (Marca 1), METRO (two brands, Aro and METRO Quality), BILLA (CLEVER), Cora (Winny), Mega Image (365), KAUFLAND (K-Classic), PROFI and PLUS.

Samples of Logo/Brands used on the Romanian dried fruit market include:

Labeling Major requirements for labeling of dried fruits and vegetables are as follows: Name of the product(s) and type Name and address (code) of the packer/exporter Content of the product (ingredients, including colorings and additives) Net weight or quantity of units packed Producer, Country of origin Date of manufacturing, best-before date and - where necessary – storage conditions European bar code of the product (and batch number) Usage instructions

Price dataOfficial customs statistics in Romania shows that average import values for dried prunes fluctuated widely over the last five years, depending on the country of supply. The least expensive dried prunes were from Poland in 2004 (0.09€/kg) and the most expensive from Germany in 2001- 7.66€/kg.

No doubt prices reflect quality, packaging, volumes shipped and branding characteristics of the actual imports. German dried prunes, for instance, have been in the range 0.77 to 7.66 €/kg (See Table 14), the different prices reflecting different qualities, brands, packaging etc.

Table 14: Import prices for dried prunes by country, registered at the Customs, 2001-200514

Year/Source 2001 2002 2003 2004 2005

Quant,t

Value, €

Price€/kg

Quant,t

Value, €

Price €/kg

Quant,t

Value, €

Price €/kg

Quant,t

Value, €

Price €/kg

Quant,t

Value, €

Price €/kg

AUSTRIA 1,8 2587 1,44 0,4 378 0,95

BELGIUM 0,4 2024 5,06 0,2 891 4,46 0,5 1295 2,59

GERMANY 0,4 3063 7,66 18,2 14000 0,77 1,9 6677 3,51 2,6 9812 3,77 5 20130 4,02

ESTONIA 0,2 260 1,3

HUNGARY 9,1 15494 1,7

NETHERLANDS 2,3 8804 3,83 3,1 8017 2,59 21,9 68374 3,12 9,7 29891 3,08 49,2 13593 0,28

POLAND 7 642 0,09 13,5 1729 0,13Sources: Eurostat Comext

Prices for dried apples imported by major supplying countries were generally more stable. From Germany, (2002-2005), prices were in the range 4.34-4.52€/kg, and from Austria (4.19 – 4.32€/kg)( See Table 15). Dutch imports fell in value from a high of 8.72€/kg in 2001, to 1.30€/kg in 2004, and 2.55€/kg in 2005.

Table 15: Import prices for dried apples, registered at the Customs, 2001-2005Year/

Source 2001 2002 2003 2004 2005Quant,

tValue,

€Price €/kg

Quant, t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

AUSTRIA 1,8 2587 1,44 0,4 378 0,95

BELGIUM 0,4 2024 5,06 0,2 891 4,46 0,5 1295 2,59

GERMANY 0,4 3063 7,66 18,2 14000 0,77 1,9 6677 3,51 2,6 9812 3,77 5 20130 4,02

ESTONIA 0,2 260 1,3

HUNGARY 9,1 15494 1,7

NETHERLANDS 2,3 8804 3,83 3,1 8017 2,59 21,9 68374 3,12 9,7 29891 3,08 49,2 13593 0,28

POLAND 7 642 0,09 13,5 1729 0,13Sources: Eurostat Comext

Dried apricots import prices from Poland and Netherlands increased resectively by 57% and 8% in 2005, compared to 2004 (See Table 16). Dried apricots import prices from Germany decreased by 9% in the same period.

Table 16: Import prices for dried apricot, registered at the Customs, 2001-2005Year/

Source2001 2002 2003 2004 2005

Quant,t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

Quant, t

Value, €

Price €/kg

AUSTRIA 0,6 450 0,8 0,3 388 1,3GERMANY 0,3 2556 8,5 0,5 1421 2,8 0,7 2025 2,9 2,3 8490 3,7 1,8 6050 3,4HUNGARY 0,1 234 2,3

NETHERLANDS

0,3 11283 37,6 3,8 7625 2,0 26,6 85330 3,2 9,1 21589 2,4 5,8 14840 2,6POLAND 0,2 635 3,2 0,2 999 5,0Sources: Eurostat Comext

According to the Customs statistics no import of dried sweet cherries is registered.

The survey of key players in the Romanian market revealed that prices for dried fruits (dried prunes, dried apples and dried cherries) fluctuate seasonally, with prices lowest during the period November-December.

15

Selling prices offered by Moldovan exporters/suppliers to Romanian supermarkets and wholesalers in 2005 and 2006 ranged from a minimum of 0.7€/kg to a maximum 1.5 €/kg. Local Romanian producers offered retail chains dried fruits at selling prices from 0.3 €/kg to 1.8€/kg. See Table 17.

Table 17: Selling prices for dried fruits offered by Romanian producers, €/kg 2005-2006 Dried prunes Dried apples Dried cherries

Min 0.3 0.5 0.8max 1.5 1.7 1.8Source: Respondents’ data

Selling prices for dried prunes offered by exporters from other countries to Romanian supermarkets and wholesalers, during 2005 and 2006, were generally lower than official average import prices, but higher than Moldovan prices. See Table 18.

Table 18: Selling prices for dried prunes offered by different exporters to Romania, 2005- September 2006, €/kg

Price/ Country Nether-lands

Hungary Germany Belgium Poland Austria Turcia

Min 1.80 1.50 2.00 2.00 2.30 2.00 2.00

Max 3.00 3.20 3.50 3.20 3.00 3.00 3.00Source: Respondents’ data

Selling prices for dried apples offered by exporters from other countries to Romanian supermarkets and wholesalers, during 2005 and 2006, ranged from a minimum of 2.0 €/kg to a maximum 4.5 €/kg. See Table 19.

Table 19: Selling Prices for dried apples offered by different exporters to Romania, 2005- September 2006, €/kg

Price/ Country

Nether-lands

Hungary Germany Belgium Austria Turcia

Min 2.30 2.50 3.50 2.00 2.50 2.50

Max 4.50 4.30 4.50 3.20 4.50 3.50Source: Respondents’ data

The survey of major buyers revealed that the highest prices for all types of dried fruit are paid in the period July – October. The season is not the only factor determining the prices. They are also influenced by the variety and size of the product, and the market situation/prices during the period of importation.

Interviewed supermarkets declared during the survey, that they buy only dried prunes from Moldova.

Major competitorsThe survey revealed that the major competitors for Moldovan exporters of dried fruits are suppliers from The Netherlands, Hungary, Poland and Germany. Turkish and Austrian suppliers as well as French and Argentinian exporters should also be taken into consideration as competitors for the Romanian market - their products are well presented, look attractive and are nicely packed, with clear branding/logo identity.

TrendsDuring the past decade there has been a trend for increased organic dried fruit production and consumption, which is also taking place in Romania.

16

The export of dried organic fruit offers exporters a higher possibility to penetrate new and existing markets. In order to be labeled as organic fruit, fruit must be grown, dried and handled in accordance with the rules and standards of an organic accreditation scheme, acceptable to the buyer, and be audited and certified by that accreditation scheme.

Moldovan Dried Fruits: Perceptions and Recommendations

Moldovan products still appear to have a reputation as flavorful and nutritious, according to the survey respondents. However, Moldovan products are unattractive when compared to products from other countries. This poor appearance is limiting their value in export markets, as well as in Moldova. According to the survey Romanian supermarkets sell Moldovan prunes in large quantities, received in bulk. Supermarkets buy only Moldovan prunes at present. Other dried fruits from Moldova are not known. Supermarkets re-pack dried prunes in small packaging and add their labels. As interviews showed, supermarkets are interested in good looking, clean fruits, (without any foreign matters), and dried without smoke.

Respondents recommended that Moldovan exporters develop improved packaging in order to add value and that they also develop a trade mark, as competitors have already done. It is also recommended to try to establish direct contacts with supermarkets for buyer delivery of Moldovan dried fruits in small retail packaging, possibly with the trade mark.

In order to be competitive on the Romanian market, Moldovan dried fruits exporters will have to meet European Union standards for consumer health and safety requirements, phytosanitary requirements, product quality and packaging standards and importer’s requirements for quantity and frequency of delivery.

Moldovan exporters of dried fruits should be aware of requirements for organic production as demand is growing on international markets, including EU countries such as France, Germany and Denmark; the trend is also growing in Romania, and markets further away, including Japan.

During this survey of Romanian buyers, respondents clearly stated that at present the use of dried fruits is increasing, but the food processing industry is the major buyer, with dried fruits being purchased in bulk. The buyers considered that opportunities may exist for Moldovan suppliers to work directly with processing factories.

NOTE: Contact information on buyers for this market may be obtained from Agribusiness Development Project (ADP): str. Bulgara 33/1, Chisinau, Republica Moldova 2001; Tel: (373 22) 577-930, Fax: (373 22) 577-931; Email: [email protected] Website: www.cnfa.md

17

Annex 1 . List of reference materials

1. State Customs Department, Moldova

2. www.kompass.md – international business catalog

3. www.ghidafaceri.ro – Romanian business catalog

4. www.ghidul.ro – Romanian business catalog

5. http://www.cotidianul.ro/index.php?id=45&art=9815&cHash=9c350c19e6 – information on the biggest hypermarkets in Romania

6. http://exporthelp.cec.eu.int

7. Market Study for Moldavian Dried Prunes on the German Market, CNFA, 2005

8. USDA FAS Gains Report Turkey Stone Fruit Annual Report 2005

9. Eurostat Comext

10. http://www.hotnews.ro/articol_34150-Marile-lanturi-de-magazine-o-duc-foarte-bine-in- Romania.htm

11. GAIN Report Number: RO6019 8Romania Retail Food Sector Update 2006

12. The EU’s on-line customs database, import duties http://europa.eu.int/comm/taxation_customs/dds/en/tarhome.htm.

13. CBI’s AccessGuide - complete overview and analysis of requirements that are applicable when exporting to the EU member states http://www.cbi.nl/accessguide.

14. General Food Law - http://www.europa.eu.int/comm/food/index_en.html

15. EU standards for organic food production and labeling http://www.imo.ch/imo_services_organic_eu_standard_en,1205,998.htmlAgriculturaL

16. Marketing Resource Center: Commodity Profiles17. ITC PACKit Export Product Profile : Dried Fruit and Vegetables

18