investor presentation: kirin holdings

TRANSCRIPT

1

September, 2011

Kirin HoldingsKirin Holdings

2

KIRIN at a glance

18%26%

6%

19%

31%

Domestic Alcohol BeveragesDomestic Alcohol Beverages

FY2011Sales (E)*1,782bnY

FY2011Sales (E)*1,782bnY

Domestic Non-alcohol BeveragesDomestic Non-alcohol BeveragesOverseas BeveragesOverseas Beverages

Pharmaceuticals and Biochemical

Pharmaceuticals and Biochemical

OtherOther

Unique business portfolio “Integrated beverage group”

Strong R&D capability and rich seeds for new product development fostered in Japan, the world’s most demanding and challenging beverage market

Kirin is building strong relationships with great partners in Asia and Oceania

*excluding liquor tax

3

More international, more integrated…

1. Pursue an integrated beverages group strategy1. Pursue an integrated beverages group strategy

2. Internationalize business2. Internationalize business

3. Establish health food & functional food business pillar to follow alcohol beverages, soft drinks and pharmaceutical businesses

3. Establish health food & functional food business pillar to follow alcohol beverages, soft drinks and pharmaceutical businesses

Approx. 30%18%Sales excl.

liquor taxOverseas composition

OP margin

Sales (yen)

Approx. 30%

10% plus

2.5 trillion

3 trillion

2015

27%Operating income

9%Excl. liquor tax

1.27 trillionExcl. liquor tax

1.68 trillionIncl. Liquor tax

2006KV2015 targets

[ Key Scenarios for Kirin Group Vision 2015 (KV2015)*]

Unit: billion yen

Quantum growth trajectory

Current trajectory

0

500

1,000

1,500

2,000

2,500

3,000

1997 98 99 00 01 02 03 04 05 06 Est. 2015

0

50

100

150

200

250

Sales (left axis)Operating income (right axis)

Historic growthline

300

Quantum Leap

Becoming a leading food, health and wellbeing company in Asia and Oceania

*announced May 2006

Vision for an ambitious new growth trajectory

4MTBP = Three-year Medium-term Business Plan

Profitability

Business scale

Stage 1: 2007 MTBP(2007-2009)

Stage 1: 2007 MTBP(2007-2009)

Stage 1 Stage 2 Stage 3

Stage 2: 2010 MTBP(2010-2012)

Stage 2: 2010 MTBPStage 2: 2010 MTBP(2010(2010--2012)2012)

Three years of implementation focus on increasing profitability

Stage 3: 2013 MTBP(2013-2015)

Stage 3: 2013 MTBP(2013-2015)

Three years to Kick- start growth

2010 MTBP—from quantity to quality

KV2015KV2015KV2015

We are here

5

Target

2012

1,835.2 1,782.0 (2.9)% 2,130.0

193.6 191.3 (1.1)% 231.0

10.5 10.7 +0.2 10.8

8.8 10.4 +1.6 10% plus

25.0 30.0 +5.0 29%

EBITDA 269.3 294.0 +9.1% 341.0

D/E ratio 0.81 0.94 +0.13 0.5

Total assets turnover ratio(%) 0.67 0.64 (0.03) 0.80 plus

2010 actual 2011 plan ** YoY change

Cash ROE (%)

Overseas sales ratio(%)

Net sales excluding liquor tax

Operating income

Operating margin(%)*

[Quantitative targets and results] ( billion yen )

*Before goodwill amortization**Revised on August 5,2011

Steadily increasing substantive profit and becoming more global

Poised to realize Cash ROE and Overseas sales ratio targets prior to 2012

6

Domestic: Building greater strength and competitiveness

Brand Value Improvement Group synergy

All for becoming strong Integrated Beverage Group

For top line growth, profitability and efficiency improvement

Profit Structure Reform

Site optimization at KB

Drastic reform at KBC

Trading system reform at ME

Value proposition than pricing

Concentrated investment on leading core brands at KB,KBC,ME

KB: Kirin Brewery, KBC: Kirin Beverage, ME: Mercian

Synergy generation through CCT

Collaboration in sales between KB-ME, KB-KBC

Cross Group Collaboration “Kirin Plus-i”

7

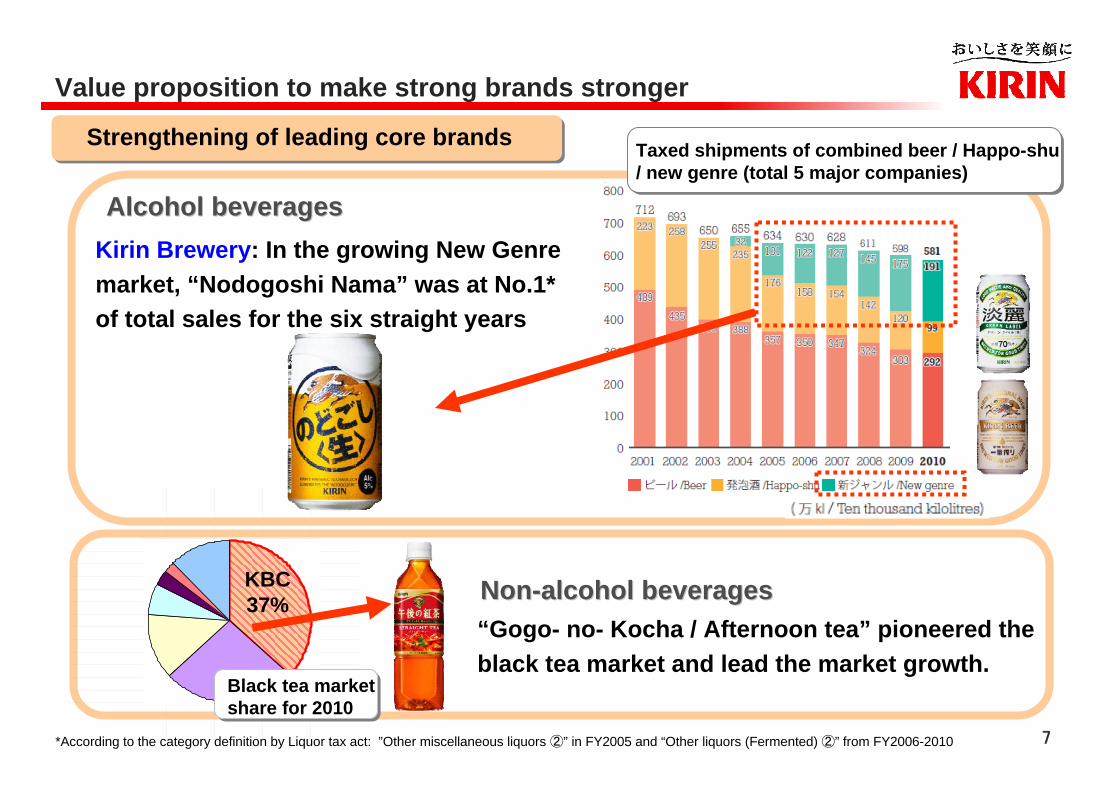

Value proposition to make strong brands stronger

Strengthening of leading core brands

Kirin Brewery: In the growing New Genre market, “Nodogoshi Nama” was at No.1*of total sales for the six straight years

“Gogo- no- Kocha / Afternoon tea” pioneered the black tea market and lead the market growth.

Alcohol beveragesAlcohol beverages

NonNon--alcohol beveragesalcohol beveragesKBC37%

Black tea market share for 2010

Taxed shipments of combined beer / Happo-shu / new genre (total 5 major companies)

*According to the category definition by Liquor tax act: ”Other miscellaneous liquors ②” in FY2005 and “Other liquors (Fermented) ②” from FY2006-2010

8

New Value Creation

KIRIN FREE / Mercian FREE*

The world’s first 0.00% alcohol, beer and wine taste beverage

Developed untapped market potential beyond established categories

[Black tea x Espresso] [Tea x CSD]

Value proposition to make strong brands stronger

Joint developmentMercian x LION

Synergy creation across KIRIN group

[KB x KBC] [ME x KB]

Launched the joint-developed products between Japan-Australia and the series of health and functional products across group companies under the same brand with common ingredient

* Scheduled to be launched in November, 2011

Health and functional foods project “ Kirin Plus-i ”by group companies

9

Domestic: Becoming more profitable and efficient

CCT* 2010 targets 2010 results 2011 targetsTarget for

2010 MTBP Production andlogistics 0.8 3.8 4.7 5.0

Procurement 4.6 8.2 4.0 10.1

IT/other 2.1 2.9 0.7 4.0

Total 7.5 14.9 9.4 19.1

(Unit: billion yen)

2010 targets 2010 actual 2011 targetsTarget for

2010 MTBP

Asset liquidation Approx.40.0 plus 57.6 Approx.100.0 150.0 plus

* Group-wide functionally organized “Cross Company Team”

Cost reduction and asset liquidation target for 2012 will be achieved ahead of schedule.

10

Kirin’s Global Expansion

Kirin Europe (Germany)

Kirin Brewery of America(US)

Coca-Cola Bottling Company of Northern New England

(US)

Four Roses Distillery(US)

Fraser & Neave(Singapore)

San Miguel Brewery(Philippines)

LION(Australia)

Kirin (China) Investment(China)

Industria Agricola Tozan LTDA

(Brazil)

Interfood(Vietnam)

Kirin HoldingsVietnam Kirin Beverage

(Vietnam)Siam Kirin Beverage (Thailand) Taiwan Kirin

(Taiwan)

While Kirin continues to implement its international integrated beverages group strategy in the Asia and Oceania regions, Kirin is also pursuing opportunities to expand its business platform to new profitable and high growth markets, and decided to invest in Brazil

China Resources Kirin Beverages Company Ltd

11

China Resources Kirin Beverages (Greater China)

International: Initiatives in China and Southeast Asia

- Kirin Holdings Singapore- Fraser and Neave- Kirin Beverage

San Miguel Brewery

JV established with China Resources Enterprise on August 19,2011, is aim to expand sales of Kirin brand products as quickly as possible utilizing the company’s sales network. Also, work on co-development of product.

Continue to maintain stable growth in the Philippines. Continue joint efforts aimed at strengthening the company’s overseas business base and creating new synergies.

Promote efforts aimed at sharing sales and production functions within the Group.

Efforts focused on expanding sales of Group products via shared sales channels. Also promote efforts for joint product development.

- Vietnam Kirin Beverage - Interfood

Singapore

Vietnam

China

Philippines

12

Non-alcohol beverages

Focus on core ‘power brands’Site optimizationEstablish best value chain for future growthStrengthen business resilience

Alcohol beveragesDrive the premiumisation and innovation

Enhance multi beverage strategy in NZ

Alcohol beverages business: Sustain high profitability through focusing on the growing categories and strong brands

Non-alcohol beverages business: Improve the business infrastructure through strengthening core brands and promoting business integration & optimization

International: Initiatives in Australasia

13

International: Schincariol in Brazil

Strong nationwide business platform & meaningful size both in the beer and soft drinks segments

2nd largest beer producer**

3rd largest share in CSD market***

Sales are expected to grow at 10% per year by leveraging our strengths

Kirin Holdings acquired all outstanding shares of Aleadri, a company that holds 50.45% of the outstanding shares of Schincariol.

[ Valuation & Funding ] - Based on the purchase price of BRL 3.95bn*, implied EV/EBITDA is 15.7x - Funded by cash on hand & loans and D/E multiple

after the acquisition expected to be within 1.0x

Note: * BRL1=¥50.35 (as of August 1, 2011) ** Based on Euromonitor and other sources *** Euromonitor. Off-trade basis

14

Strong pipelines:Kyowa Hakko Kirin have ample pipelines based on advanced R&DSubstantial contribution to Kirin Group with high profitabilityAcquired ProStrakan to establish strong sales network in the U.S. & EU

Strong presence in the ESA market with NESP® and ESPO®Outstanding base- technology in Antibody: Utilizing POTELLIGENT® & COMPLEGENT® technologies* and KM Mouse**, Kyowa Hakko Kirin will strive for the creation of new therapeutic antibodies in cooperation with its worldwide partners.

Kyowa Hakko Kirin will be Global Specialty Pharmaceutical Companyleveraging their outstanding biotechnology.

Global Specialty Pharmaceuticals

*For producing enhanced antibody activity **Fully Human Antibody Producing Mouse

15

Cash FlowCash Flow

Increased Operating CF

Increased Operating CF

Improved investment efficiency

Improved investment efficiency

Financial Strategy for 2010 MTBP

Shareholder returnsDividends:Consolidated payout ratios over 30% Aim to increase dividends inline with growth in real earnings, taking into consideration amortization of goodwill, etc. arising from investment for growth

Share buybacks:To be considered in the context of progress on qualitative expansion, on the basis of maintaining medium to long term credit rating

Investment for growthWe will intensively allocate resources as appropriate but have not established an investment framework as a guideline

Capital structurePursue debt repayment, targeting a D/E ratio of 0.5x at the end of 2012 (allowing a temporary upper limit of approximately 1.0x)

Further asset reduction

Further asset reduction

Significantly increase cashflow, through realizing group synergies, lean management, improved investment efficiency and asset reduction

2010-2012 capex ¥260 bn

2010-2012 operating CF¥620 bn

2010-2012 assets to beliquidated ¥150 bn

Debt repayment

Shareholderreturns

16

この資料は投資判断の参考となる情報の提供を目的としたものであり、投資勧誘を目的としたものではありません。銘柄の選択、投資の最終決定は、ご自身の判断でなさるようにお願いいたします。

This material is intended for informational purposes only and is not a solicitation or offer to buy or sell securities or related financial instruments.