investor presentation - ypf · investor presentation second quarter 2015 . 2 ... ms. charvay mr....

TRANSCRIPT

1

Investor Presentation Second Quarter 2015

2

Safe harbor statement under the US Private Securities Litigation Reform Act of 1995.

This document contains statements that YPF believes constitute forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995.

These forward-looking statements may include statements regarding the intent, belief, plans, current expectations or objectives of YPF and its management,

including statements with respect to YPF’s future financial condition, financial, operating, reserve replacement and other ratios, results of operations, business strategy, geographic concentration, business concentration, production and marketed volumes and reserves, as well as YPF’s plans, expectations or objectives with respect to future capital expenditures, investments, expansion and other projects, exploration activities, ownership interests, divestments, cost savings and dividend payout policies. These forward-looking statements may also include assumptions regarding future economic and other conditions, such as future

crude oil and other prices, refining and marketing margins and exchange rates. These statements are not guarantees of future performance, prices, margins, exchange rates or other events and are subject to material risks, uncertainties, changes and other factors which may be beyond YPF’s control or may be difficult to predict.

YPF’s actual future financial condition, financial, operating, reserve replacement and other ratios, results of operations, business strategy, geographic concentration, business concentration, production and marketed volumes, reserves, capital expenditures, investments, expansion and other projects, exploration activities, ownership interests, divestments, cost savings and dividend payout policies, as well as actual future economic and other conditions, such

as future crude oil and other prices, refining margins and exchange rates, could differ materially from those expressed or implied in any such forward-looking statements. Important factors that could cause such differences include, but are not limited to, oil, gas and other price fluctuations, supply and demand levels, currency fluctuations, exploration, drilling and production results, changes in reserves estimates, success in partnering with third parties, loss of market share, industry competition, environmental risks, physical risks, the risks of doing business in developing countries, legislative, tax, legal and regulatory developments,

economic and financial market conditions in various countries and regions, political risks, wars and acts of terrorism, natural disasters, project delays or advancements and lack of approvals, as well as those factors described in the filings made by YPF and its affiliates with the Securities and Exchange Commission, in particular, those described in “Item 3. Key Information—Risk Factors” and “Item 5. Operating and Financial Review and Prospects” in YPF’s

Annual Report on Form 20-F for the fiscal year ended December 31, 2014 filed with the US Securities and Exchange Commission. In light of the foregoing, the forward-looking statements included in this document may not occur.

Except as required by law, YPF does not undertake to publicly update or revise these forward-looking statements even if experience or future changes make it

clear that the projected performance, conditions or events expressed or implied therein will not be realized.

These materials do not constitute an offer for sale of YPF S.A. bonds, shares or ADRs in the United States or otherwise.

Important Notice

3 3

Company Overview 1

Upstream and Downstream 2

Financial Results 3

2015 Outlook 4

Agenda

4

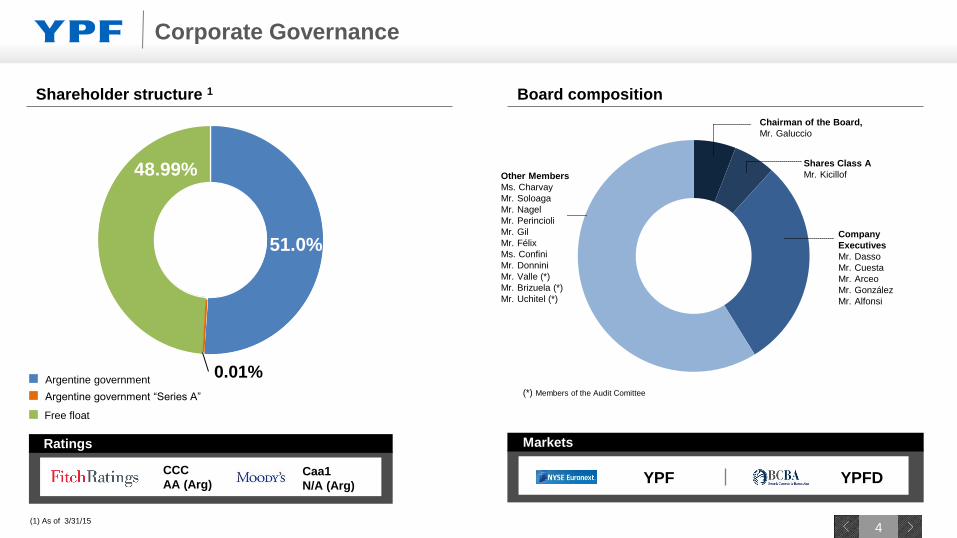

Argentine government

Argentine government “Series A”

Free float

51.0%

48.99%

0.01%

Ratings

CCC

AA (Arg)

Markets

YPFD YPF

(1) As of 3/31/15

Caa1

N/A (Arg)

Corporate Governance

Other Members

Ms. Charvay

Mr. Soloaga

Mr. Nagel

Mr. Perincioli

Mr. Gil

Mr. Félix

Ms. Confini

Mr. Donnini

Mr. Valle (*)

Mr. Brizuela (*)

Mr. Uchitel (*)

Company

Executives

Mr. Dasso

Mr. Cuesta

Mr. Arceo

Mr. González

Mr. Alfonsi

Chairman of the Board,

Mr. Galuccio

Shares Class A

Mr. Kicillof

Shareholder structure 1 Board composition

(*) Members of the Audit Comittee

5

Revenues LTM 1

US$ 17,449 mm

Adj. EBITDA LTM 1 2

US$ 5,186 mm

Net income LTM 1

US$ 1,048 mm

Employees 4

22,032

Exploration

and production • Production 7: 250 Kbbl/d of crude oil, 39 Kbbl/d of NGL and 45 Mm3/d of natural gas

• Proved Reserves 3 4 in 2014: 675 mm bbl of liquids and 537 mm boe of gas

• Unique unconventional opportunities: Vaca Muerta, Lajas, Pozo D-129

Downstream -

refining and

logistics

• Total refining Capacity: 320 Kbbl/d 4 5 (more than 50% 4 of Argentina’s total capacity)

• High level of conversion and complexity

• Nearly 2,700 km 4 of crude oil and 1,801 km 4 of refined products pipeline

Downstream -

petrochemicals • The petrochemical business is integrated with the rest of the production chain

• Output Capacity: 2.2 4 mm ton per annum

Downstream -

marketing

• The country’s leading company in fuel marketing (56.5% 4 market share in diesel and gasoline)

• 1,542 4 6 service stations

Major Affiliates • MEGA: Liquids separation and a fractioning plant

• Metrogas: Largest local gas distribution company

• Refinor: Refining, transportation and marketing of refined products

• Profertil: Fertilizer producer (urea and ammonia)

• AESA: Engineering, manufacturing, construction, operating

and maintenance services to power and energy companies

Leading Integrated Energy Co. in Argentina

(1)YPF financial statements values in IFRS converted to US$ using LTM Q2 2015 average FX of 8.4. (2) Adjusted EBITDA = Net income attributable to shareholders + Net income for non controlling interest - Deferred income tax - Income tax - Financial

income (losses) gains on liabilities - Financial income gains (losses) on assets - Income on investments in companies + Depreciation of fixed assets + Amortization of intangible assets + Unproductive exploratory drillings. (3) Includes oil, condensates

and liquids; converted using 1 boe = 5.615 mmcf of gas as per 20-F 2014. (4) As per 20-F 2014 (5) Does not includes 50% of Refinor (13 kbbl/d). (6) Excludes 71 Refinor service stations. (7) Q2 2015 5

6

45%

19%

6%

5%

4%

4%

17%

35%

15% 11% 6%

6%

27%

59%

13%

6%

15%

7%

42%

16% 9%

9%

5%

3%

16%

Market Share Breakdown (%)

Source: IAPG

(1) Cumulative Jan - May 2015

(2) Cumulative Jan - Jun 2015

(3) As of December 2014

Market Share Breakdown (%)

Upstream Downstream

Gasoline 2 Diesel 2

Crude Processing 3 No. of Gas Stations 3

55%

15%

9%

13%

8%

57%

18%

5%

14% 6%

Others Others

Others

Others

Others

Gas

Production 1

Others Oil

Production 1

Leading Argentine O&G Company

7

Production figures as of June 2015 / Domestic Market Sales of natural only correspond to YPF (does not include YSUR)

Oil

business

Natural gas

business

Production

250 Kbbl/d Refining

305 Kbbl/d

Domestic

market

Domestic market

72% Domestic prices (gasoline, diesel)

18% International prices (FO, bunker, jet fuel,

petrochemicals, lubricants, LPG and others)

90%

10% Exports International prices

(naphtha, LPG, jet fuel, crude, petrochemicals,

fuel oil, soybean oil and meal and others)

Purchases

Imports (Gas purchased

by ENARSA)

+ Purchases

+

Domestic

market

Exports 0.2%

99%

Residential

+ CNG

Industrial

Power

plants

59% 17%

24%

Upstream

45 mm m3/d

Export

market

Integrated Across Value Chain

8 8

15 + years of industry experience each

Local and international experience

Seasoned Management Team

Miguel Galuccio Chairman & CEO • Before rejoining YPF, he was part of the management team of Schlumberger in London

• More than 20 years of international experience in the oil and gas industry, leading companies

and working teams in the United States, Middle East, Asia, Europe, Latin America, Russia and China

• Oil engineer from the Technological Institute of Buenos Aires

Daniel Gonzalez CFO

• Before joining YPF, he served for 14 years in the investment bank Merrill Lynch & Co in Buenos Aires

and New York, holding the positions of Head of Mergers and Acquisitions for Latin America and President

for the Southern Cone (Argentina, Chile, Peru and Uruguay), among others

• Bachelor in Business Administration from the Argentine Catholic University

Carlos Alfonsi VP Downstream

• Since 1987, he has held various positions at YPF, serving as an operations manager; the director of the La Plata

refinery; operation planning director; director of commerce and transportation for Latin America; director of refinery

and marketing in Peru; country manager for Peru; and R&M for Peru, Chile, Ecuador and Brazil

• Bachelor in Chemistry from Argentina’s Technological University of Mendoza. In addition, he earned degree

in IMD Managing Corporate Resources from Lausanne University and has studied at the MIT

Jesus Grande VP Upstream

• Before YPF, he held various positions at Schlumberger, serving as Director of Human Resources; president

of one of its service lines; head of Corporate Strategy Implementation. He has also served in executive

and operational positions in Kuwait, Argentina, Brazil, Angola and the United States

• Engineer from the National University of Tucumán

Fernando Giliberti VP Strategy and Business Development

• He previously served at YPF as Business Development Manager and Exploration and Production Business

Development Director

• CPA from the Argentine Catholic University; earned an MBA from the Argentine University of the Enterprise,

a Postgraduate Diploma in Management and Economics of Natural Gas from the College of Petroleum Studies,

Oxford University, and master’s degree in the Science of Management at Stanford University.

5

9 9

Company Overview 1

Upstream and Downstream 2

Financial Results 3

2015 Outlook 4

Agenda

10

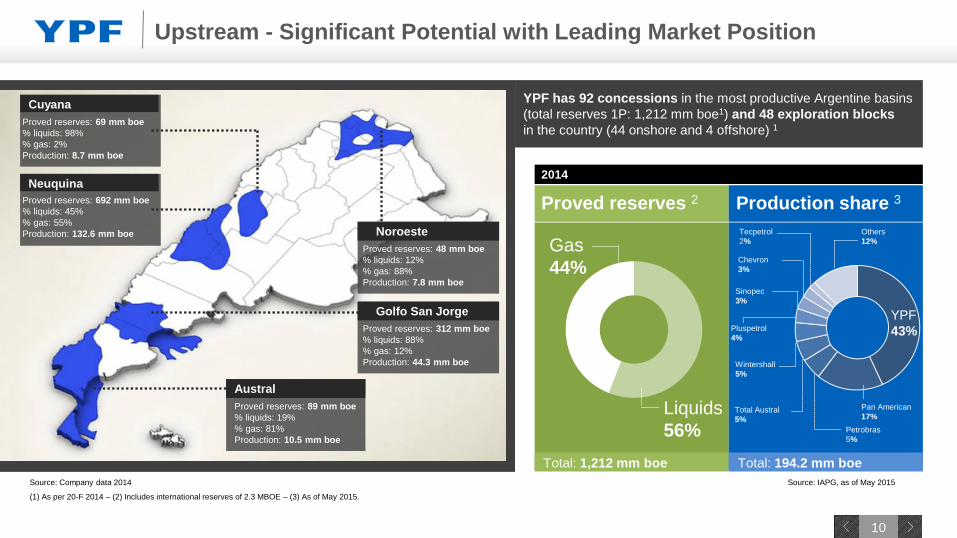

Source: Company data 2014

(1) As per 20-F 2014 – (2) Includes international reserves of 2.3 MBOE – (3) As of May 2015.

YPF has 92 concessions in the most productive Argentine basins

(total reserves 1P: 1,212 mm boe1) and 48 exploration blocks

in the country (44 onshore and 4 offshore) 1 Proved reserves: 69 mm boe

% liquids: 98%

% gas: 2%

Production: 8.7 mm boe

Cuyana

Proved reserves: 48 mm boe

% liquids: 12%

% gas: 88%

Production: 7.8 mm boe

Noroeste

Proved reserves: 312 mm boe

% liquids: 88%

% gas: 12%

Production: 44.3 mm boe

Golfo San Jorge

Proved reserves: 89 mm boe

% liquids: 19%

% gas: 81%

Production: 10.5 mm boe

Austral

Proved reserves: 692 mm boe

% liquids: 45%

% gas: 55%

Production: 132.6 mm boe

Neuquina 2014

Proved reserves 2 Production share 3

Liquids

56%

Gas

44%

Total: 1,212 mm boe Total: 194.2 mm boe

Pan American

17%

Wintershall

5%

Others

12%

Sinopec

3%

Tecpetrol

2%

Chevron

3%

Total Austral

5%

Petrobras

5%

YPF

43% Pluspetrol

4%

Source: IAPG, as of May 2015

Upstream - Significant Potential with Leading Market Position

11

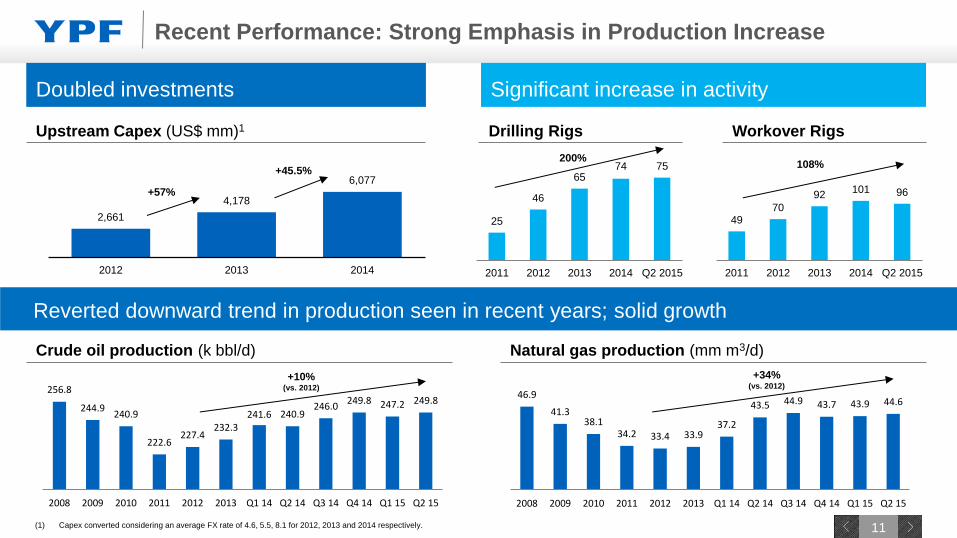

Significant increase in activity Doubled investments

49 70

92 101 96

2011 2012 2013 2014 Q2 2015

46.9

41.3 38.1

34.2 33.4 33.9 37.2

43.5 44.9 43.7 43.9 44.6

2008 2009 2010 2011 2012 2013 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

256.8

244.9 240.9

222.6 227.4

232.3 241.6 240.9

246.0 249.8 247.2 249.8

2008 2009 2010 2011 2012 2013 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

2,661

4,178

6,077

2012 2013 2014

Reverted downward trend in production seen in recent years; solid growth

Upstream Capex (US$ mm)1 Drilling Rigs Workover Rigs

200% 108%

Crude oil production (k bbl/d) Natural gas production (mm m3/d)

(1) Capex converted considering an average FX rate of 4.6, 5.5, 8.1 for 2012, 2013 and 2014 respectively.

Recent Performance: Strong Emphasis in Production Increase

+57%

+10% (vs. 2012)

+34% (vs. 2012)

+45.5%

25

46

65 74 75

2011 2012 2013 2014 Q2 2015

12

1,083

1,212

2013 2014

455

537

2013 2014

628

675

2013 2014

Liquids (Mbbl) Natural Gas (Mboe)

Total Hydrocarbon (Mboe)

+6.4% +18.0% +11.9%

Boosted proved reserves by 11.9%. Solid results coming from secondary recovery

projects, tight gas and shale formations, extension of concessions and acquisitions.

163% RRR 144% RRR 184% RRR

Reserves

13

NEUQUINA

GOLFO

SAN JORGE

AUSTRAL

CUYANA

NOROESTE

4,4

CHACO

PARANAENSE

Other Opportunities

Pozo D-129 (shale oil / tight oil)

Noroeste - Tarija

Los Monos (shale gas)

Noroeste - Cretaceous

Yacoraite (shale / tight oil & gas)

Chaco Paranaense

Devonian – Permian (shale oil)

Cuyana

Cacheuta (shale oil)

Potrerillos (tight oil)

Austral

Inoceramus

Neuquina

Los Molles (shale/ tight gas)

Golfo San Jorge

Neocomiano (shale oil / gas)

Tested & Producing

Upside from Unique Unconventional Opportunities

Vaca Muerta (shale oil / gas)

Agrio (shale oil)

Lajas (tight gas)

Mulichinco (tight gas)

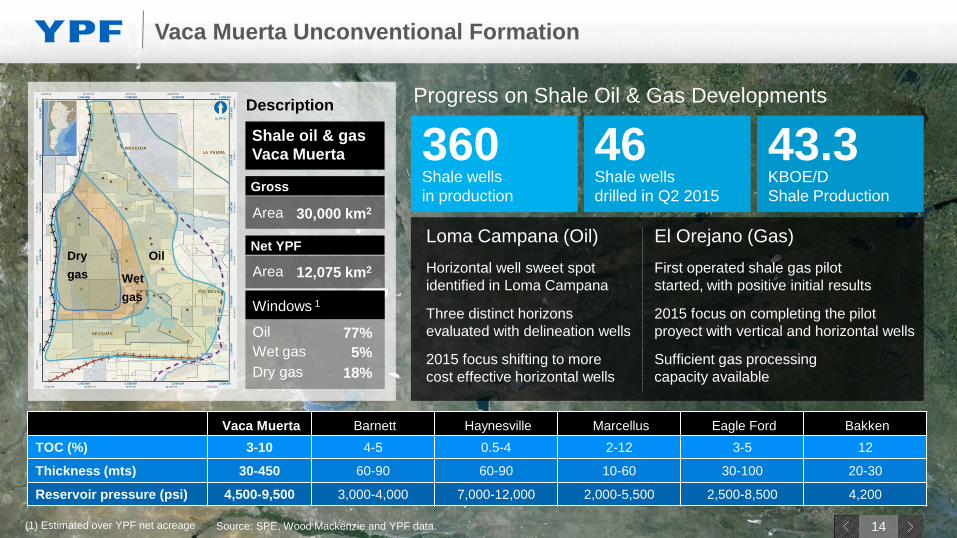

14 14

Description

Area 30,000 km2

Gross

Shale oil & gas Vaca Muerta

Area 12,075 km2

Net YPF

Oil 77%

Wet gas 5%

Dry gas 18%

Windows 1

Oil

Wet

gas

Dry

gas

Source: SPE, Wood Mackenzie and YPF data. (1) Estimated over YPF net acreage

Vaca Muerta Unconventional Formation

Progress on Shale Oil & Gas Developments

Vaca Muerta Barnett Haynesville Marcellus Eagle Ford Bakken

TOC (%) 3-10 4-5 0.5-4 2-12 3-5 12

Thickness (mts) 30-450 60-90 60-90 10-60 30-100 20-30

Reservoir pressure (psi) 4,500-9,500 3,000-4,000 7,000-12,000 2,000-5,500 2,500-8,500 4,200

Shale wells

in production

360 Shale wells

drilled in Q2 2015

46 KBOE/D

Shale Production

43.3

Loma Campana (Oil)

Horizontal well sweet spot

identified in Loma Campana

Three distinct horizons

evaluated with delineation wells

2015 focus shifting to more

cost effective horizontal wells

El Orejano (Gas)

First operated shale gas pilot

started, with positive initial results

2015 focus on completing the pilot

proyect with vertical and horizontal wells

Sufficient gas processing

capacity available

15 15

JV Partners: Chevron, Dow, Petrolera Pampa and Petronas

Loma Campana (395 km2 - 97,607 acres)

Objective: Vaca Muerta

Shale Oil with Chevron

Republic of ArgentinaNeuquina Basin

Neuquén Province

3.3% of total YPF’s VM acreage 1

(1) 395 Km2 / 12,075 Km2

Development model

290 Km2 (71,661 acres)

Directional wells upside

105 Km2 (25,946 acres)

Pilot: 130 wells and US$1.24 bn

YPF Operates

Full program

of ~1,500 wells (US$15 bn+)

• Estimated oil production: + 50 Kbbl/d

• Estimated gas production: 3 mm m3/d

La Amarga Chica (187 km2 - 46,189 acres)

Objective: Vaca Muerta

Shale Oil with Petronas

1.55% of total YPF’s VM acreage 2

(2) 187 Km2 / 12,075 Km2

Pilot consisted

on US$550 mm investment

~ 35 wells to be drilled

both verticals and horizontal

YPF Operates

El Orejano (395 km2 - 97,607 acres)

Objective: Vaca Muerta

Shale Gas with Dow

0.37% of total YPF’s VM acreage 3

(3) 45 Km2 / 12,075 Km2

Initial investment

of US$188 mm

16 wells to be drilled

YPF Operates

Rincón del Mangrullo (183 km2 - 45,200 acres)

Objective: Mulichinco Tight

Gas with Petrolera Pampa

1st stage

40 km2 of 3D seismic

34 wells to be drilled

YPF Operates

2nd stage

15 wells to be drilled

16 16

0.04 0.14

0.87

1.22

1.41

1.80

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015

0.7 0.6 0.7

1.8

2.7

3.3

4.1 4.0 4.3 4.4

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Tight gas production

in Q2 2015 represents

12% of total gas

production, compared

to 8% in Q2 2014.

(1) Refers to Lajas prospective area called

“Segmento 5” in Loma La Lata block.

Loma La Lata (121 km2 – 29,900 acres)(1)

Objective: Lajas formation

• 100% YPF

• 4 wells drilled in Q2 2015

(93 total wells drilled)

• Depth: 2,600 m to 2,800 m

Total Gross Production (Mm3/d)

Rincón del Mangrullo (183 km2 - 45,200 acres)

Objective: Mulichinco formation

• 50% YPF – 50% Petrolera Pampa

• 12 wells drilled in Q2 2015

(61 total wells drilled)

• Depth: 1,600 m to 1,800 m

Total Gross Production (Mm3/d)

Tight Gas Developments

17

59%

13%

6%

15%

7%

Source: 20-F 2014 – (1) YPF owns 50% of Refinor (not operated) – (2) As of December 2014

Proved reserves: 85 M boe

% liquids: 98

% gas: 2

Production: 8.8 M boe

Capacity: 105.5 kbbl/d

Luján de Cuyo refinery A

Proved reserves: 85 M boe

% liquids: 98

% gas: 2

Production: 8.8 M boe

Capacity: 189 kbbl/d

La Plata refinery B

Capacity: 25 kbbl/d

Plaza Huincul refinery C

Capacity: 26.1 kbbl/d

Refinor(1)

D

C

D

B

Terminals

Products pipeline

Oil pipeline

A

(3) Cumulative Jan-May 2015

Downstream - Solid Market Leadership

Market Share Breakdown (%)

Gasoline 3 Diesel 3

Crude Processing 2 No. of Gas Stations 2

55%

15%

9%

13%

8%

57%

18%

5%

14% 6%

Others Others

Others

35%

15% 11% 6%

6%

27%

Others

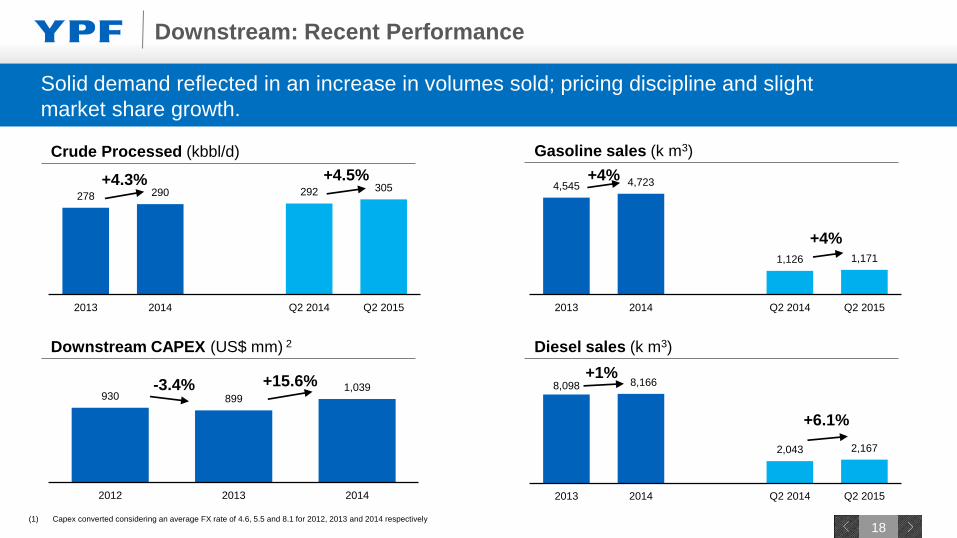

18

4,545 4,723

1,126 1,171

2013 2014 Q2 2014 Q2 2015

8,098 8,166

2,043 2,167

2013 2014 Q2 2014 Q2 2015

278 290 292 305

2013 2014 Q2 2014 Q2 2015

930 899 1,039

2012 2013 2014

Solid demand reflected in an increase in volumes sold; pricing discipline and slight

market share growth.

(1) Capex converted considering an average FX rate of 4.6, 5.5 and 8.1 for 2012, 2013 and 2014 respectively

+6.1%

+4%

Downstream: Recent Performance

Crude Processed (kbbl/d)

Downstream CAPEX (US$ mm) 2 Diesel sales (k m3)

Gasoline sales (k m3)

+15.6%

+4.5% +4.3% +4%

+1% -3.4%

19

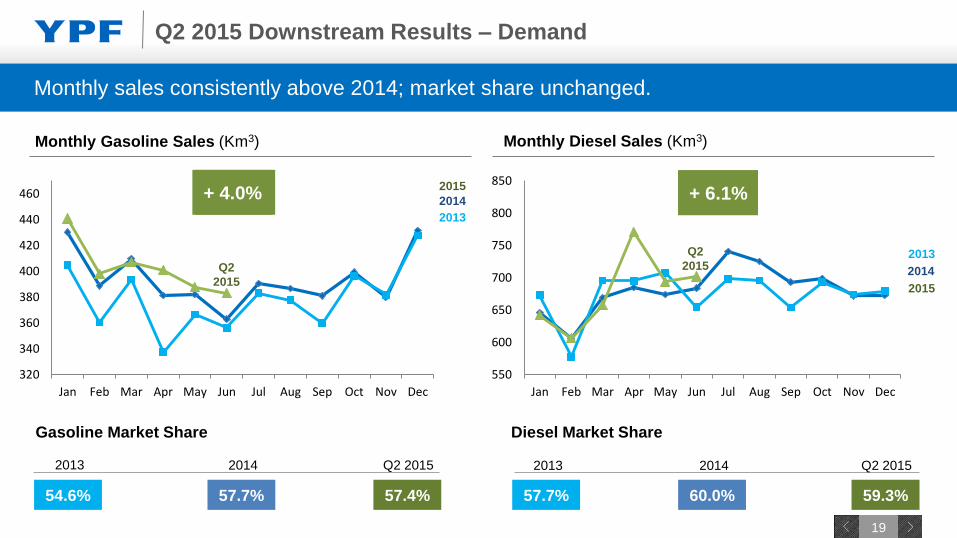

550

600

650

700

750

800

850

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013

2014

2015

320

340

360

380

400

420

440

460

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013

2014

2015

Monthly Gasoline Sales (Km3)

Monthly sales consistently above 2014; market share unchanged.

Monthly Diesel Sales (Km3)

54.6% 57.4% 57.7% 59.3%

Gasoline Market Share

2013 Q2 2015

Diesel Market Share

2013 Q2 2015

+ 3.9% + 0.8% + 4.0% + 6.1%

60.0%

2014

57.7%

2014

Q2

2015

Q2

2015

Q2 2015 Downstream Results – Demand

20 20

Company Overview 1

Upstream and Downstream 2

Financial Results 3

2015 Outlook 4

Agenda

21

857 1,041 1,115 1,048

191 258

2012 2013 2014 LTM Q2 2014 Q2 2015

1,737 2,202

2,445 2,260

743 627

2012 2013 2014 LTM Q2 2014 Q2 2015

14,762 16,514 17,576 17,449

4,413 4,443

2012 2013 2014 LTM Q2 2014 Q2 2015

4,391 5,128 5,186

1,367 1,392

27% 29% 30% 31% 31%

2013 2014 LTM Q2 2014 Q2 2015

EBITDA EBITDA Margin (%)

+17%

Revenues, Adj. EBITDA and Operating Income presented solid growth, mainly driven

by higher production and healthy margin increase.

Results

Revenues 1 (US$ mm) Adj. EBITDA 1 2 3 (US$ mm) & Adj. EBITDA Margin (%)

EBIT 1 2 (US$ mm) Net Income 1 2 (US$ mm)

-16%

(1) YPF financial statements values in IFRS converted to US$ using average FX of 4.6, 5.5, 8.1, 8.0, 8.6 and 8.9 for 2012, 2013, 2014, LTM Q2 2015, Q2 2014 and Q2 2015 respectively

(2) Considers non recurrent result for Q2 2013, not including a non cash provision of ARS 855 mm relating to claims arising from discontinuity of gas export contracts to Brazil in 2009

(3) Adjusted EBITDA = Net income attributable to shareholders + Net income for non controlling interest - Deferred income tax - Income tax - Financial income (Losses) gains on liabilities -

Financial income gains (Losses) on assets - Income on investments in companies + Depreciation of fixed assets + Amortization of intangible assets + Unproductive exploratory drillings

+2%

+35%

+6%

+11% +7%

+1%

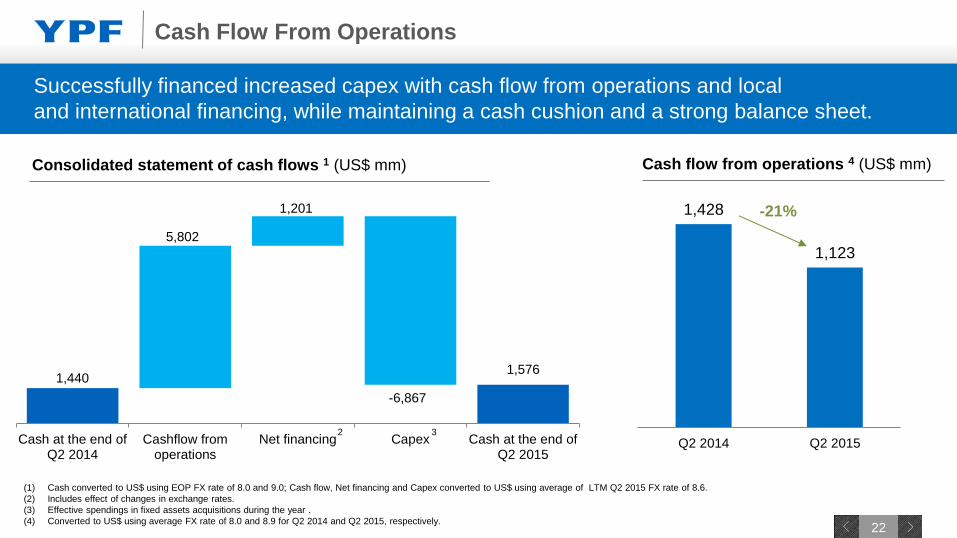

22

1,428

1,123

Q2 2014 Q2 2015

(1) Cash converted to US$ using EOP FX rate of 8.0 and 9.0; Cash flow, Net financing and Capex converted to US$ using average of LTM Q2 2015 FX rate of 8.6.

(2) Includes effect of changes in exchange rates.

(3) Effective spendings in fixed assets acquisitions during the year .

(4) Converted to US$ using average FX rate of 8.0 and 8.9 for Q2 2014 and Q2 2015, respectively.

2 3

-21%

Consolidated statement of cash flows 1 (US$ mm) Cash flow from operations 4 (US$ mm)

Cash Flow From Operations

Successfully financed increased capex with cash flow from operations and local

and international financing, while maintaining a cash cushion and a strong balance sheet.

1,440 1,576

5,802

1,201

-6,867

Cash at the end ofQ2 2014

Cashflow fromoperations

Net financing Capex Cash at the end ofQ2 2015

23

1,434

Cash 2015 2016 2017 2018 2019 2020 +2020

Peso denominated debt:

26% of total debt

Financial debt amortization schedule (1) (2) (in millions of USD)

Average interest rates of 7.54%

in USD and 23.56% in pesos

(1) As of June 30, 2015, does not include consolidated companies

(2) Converted to USD using the June 30, 2015 exchange rate of Ps 9.0 to U.S.$1.00.

Cash position covers debt maturities for next 12 months.

Continued to extend the average life of debt.

Average life of almost

4.9 years

Debt profile highlights

Financial Situation Update (1)

24 24

Balance sheet 6/30/15 (Ps million)

12/31/14 (Ps million)

VAR % 2015/2014

Cash & ST investments 14,238 9,758 46%

Fixed assets 180,138 156,930 15%

Other assets 46,838 41,866 12%

Total assets 241,214 208,554 16%

Loans 68,941 49,305 40%

Liabilities 90,507 86,468 5%

Total Liabilities 159,448 135,773 17%

Shareholders’ equity 81,766 72,781 12%

Source: YPF financial statements

Consolidated Balance Sheet

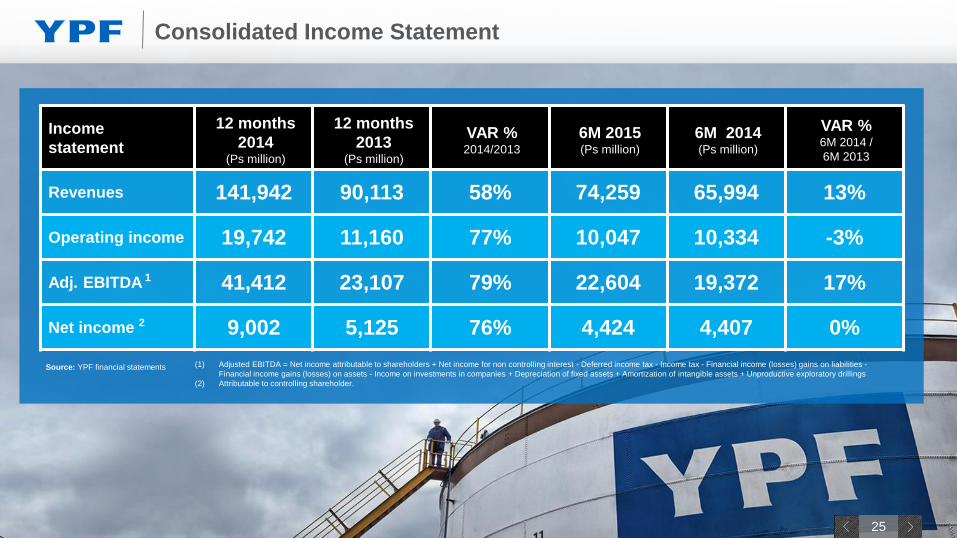

25 25

Income

statement

12 months

2014 (Ps million)

12 months

2013 (Ps million)

VAR % 2014/2013

6M 2015 (Ps million)

6M 2014 (Ps million)

VAR % 6M 2014 /

6M 2013

Revenues 141,942 90,113 58% 74,259 65,994 13%

Operating income 19,742 11,160 77% 10,047 10,334 -3%

Adj. EBITDA 1 41,412 23,107 79% 22,604 19,372 17%

Net income 2 9,002 5,125 76% 4,424 4,407 0%

Source: YPF financial statements (1) Adjusted EBITDA = Net income attributable to shareholders + Net income for non controlling interest - Deferred income tax - Income tax - Financial income (losses) gains on liabilities -

Financial income gains (losses) on assets - Income on investments in companies + Depreciation of fixed assets + Amortization of intangible assets + Unproductive exploratory drillings

(2) Attributable to controlling shareholder.

Consolidated Income Statement

26 26

Company Overview 1

Upstream and Downstream 2

Financial Results 3

2015 Outlook 4

Agenda

27 27

Continued to deliver solid results despite challenging

global oil price environment and the effects of a strong peso

Strong local demand for our main products

Sound cash position raised early in the year

Tight and shale gas development progressing well;

shale oil development addressing learning curve challenges

Summary

28

NUESTRA ENERGÍA