ma6622, ernesto mordecki, cityu, hk, 2010. references for

TRANSCRIPT

22. Fixed Income Finance

MA6622, Ernesto Mordecki, CityU, HK, 2010.

References for this Lecture:

Marco Avellaneda and Peter Laurence, Quantitative Mod-

elling of Derivative Securities, Chapman&Hall (2000).

P. Willmot, Derivatives, Wiley (1998).

Hong Kong Monetary Authority (HKMA) Web Page:http://www.info.gov.hk/hkma/

1

Plan of Lecture 22

(22a) Fixed Income

(22b) Fixed Income Securities

(22c) Bond Yields

(22d) Computing YTM (Newton-Raphson)

2

22a. Fixed income

Fixed income refers to any type of investment that yields aregular or fixed payment:

• If you borrow money and have to pay interest once amonth, you have issued a fixed income security.

•When this is done by the government, or a company, wehave a bond.

• The Hong Kong Government (through the HK MonetaryAuthority - HKMA) issues bonds, under the denominationof Exchange Fund Bills and Exchange Fund Notes.

3

22b. Fixed income securities

Fixed income securities can be contrasted with variable re-turn securities: a bond is the typical fixed income security,whereas a stock is the typical variable return security.

A Zero Coupon Bond is a contract paying a known fixedamount, the principal or face value at some given date inthe future, the maturity. For analysis we fix the principalto be 100 (one hundred points). Examples of zero couponbonds are

• Treasury Bills or T-Bill issued by the US Government,commonly with maturity dates of 28 days (4 weeks), 91days (3 months) and 182 days (6 months).

4

• Exchange Fund Bills or EFB, issued by the Hong KongMonetary Authority (HKMA) with maturities of

– 91 days ∼ three months, or Quarter,

– 182 days ∼ six months, or Half year,

– 364 days ∼ one Year.

A Coupon Bearing Bond is similar to the above, with thedifference that, as well as paying the principal, they alsopay smaller quantities, the coupons, at intervals up to andincluding the maturity date. Examples of Coupon BearingBonds are:

• Treasury notes or T-Notes issued by the US Government,that mature in two to ten years. They have a couponpayment every six months, and are commonly issued withmaturities dates of 2, 3, 5 or 10 years.

5

• Exchange Fund Notes or EFN issued by the HKMA havematurities between 2 and 10 years, and pay a fixed couponevery six months.

Floating rate notes are bonds that have a variable coupon,equal to a money market reference rate, like LIBOR1, plusa constant spread. A typical coupon would look like:

3 months USD LIBOR+0.20%.

For instance, if the payment coupon date was June 6, as theLibor in USD for 3 months2 was 5.27000, the coupon willpay 5.47 points.

1LIBOR (London Interbank Offered Rate) is the rate of interest at which banks borrow fundsfrom each other in the London interbank market. LIBOR fixings are provided in ten currencies,

including GBP, USD, Euro, and JPY.2Taken from http://www.bba.org.uk/, the web site of the British Bankers’ Association (BBA),

that calculates the Libor rates.

6

22c. Bond Yields

In order to consistently compare the variety of fixed incomeproducts, we examine the yield to maturity (YTM).

The YTM y is the discount rate such that, the sum of thediscounted face value plus the discounted coupon paymentsequals the market price of the bond.

Discrete vs. Continuous compounding As we have time-discount rate computations the YTM depends on using

• Continuous compounding interest rate

•Discrete compounding interest rate, mainly

– accrued once a year (ω = 1)

– accrued twice a year (ω = 2)

7

YTM of a zero coupon bond.

The simplest situation is a zero coupon bond. If the bondmatures at time T , and the market price of the bond attime t (say, today) is Z(t, T ), then the YTM, denoted y, isdefined by the relation:

Z(t, T ) = 100e−(T−t)y

where T − t is time to expiration measured in years

From this we obtain that

y =1

T − tlog

[ 100

Z(t, T )

]

.

8

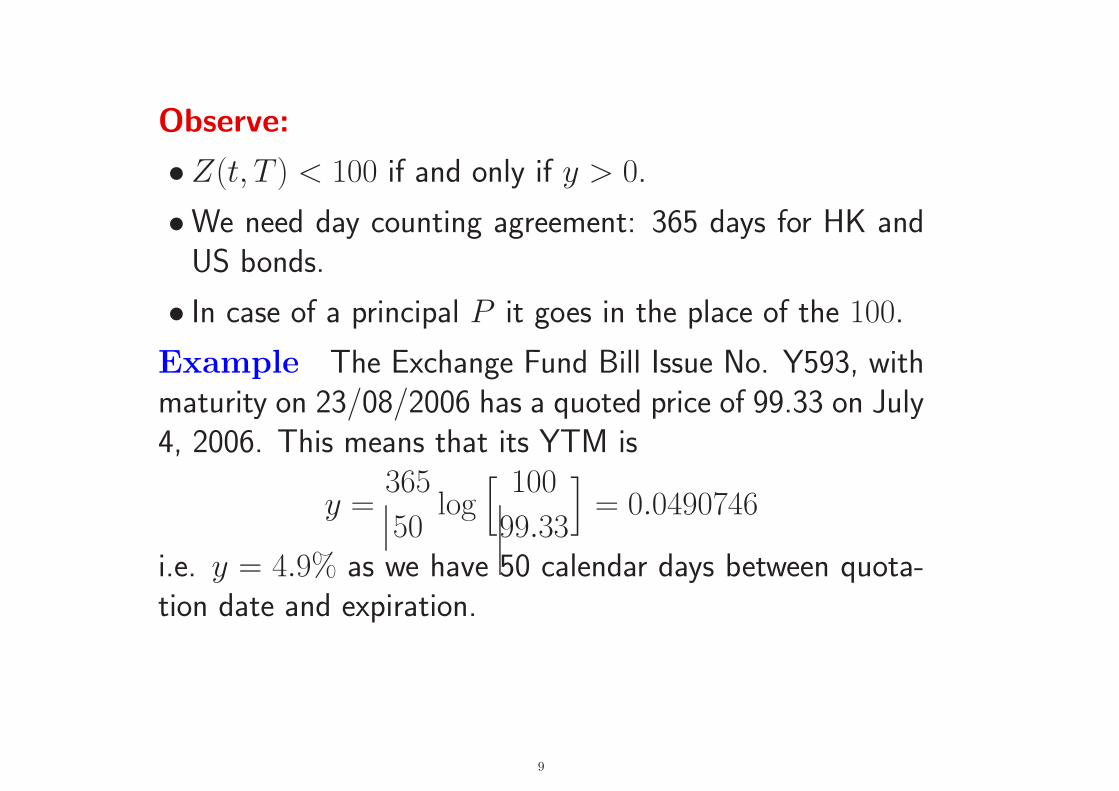

Observe:

• Z(t, T ) < 100 if and only if y > 0.

•We need day counting agreement: 365 days for HK andUS bonds.

• In case of a principal P it goes in the place of the 100.

Example The Exchange Fund Bill Issue No. Y593, withmaturity on 23/08/2006 has a quoted price of 99.33 on July4, 2006. This means that its YTM is

y =365

50log

[ 100

99.33

]

= 0.0490746

i.e. y = 4.9% as we have 50 calendar days between quota-tion date and expiration.

9

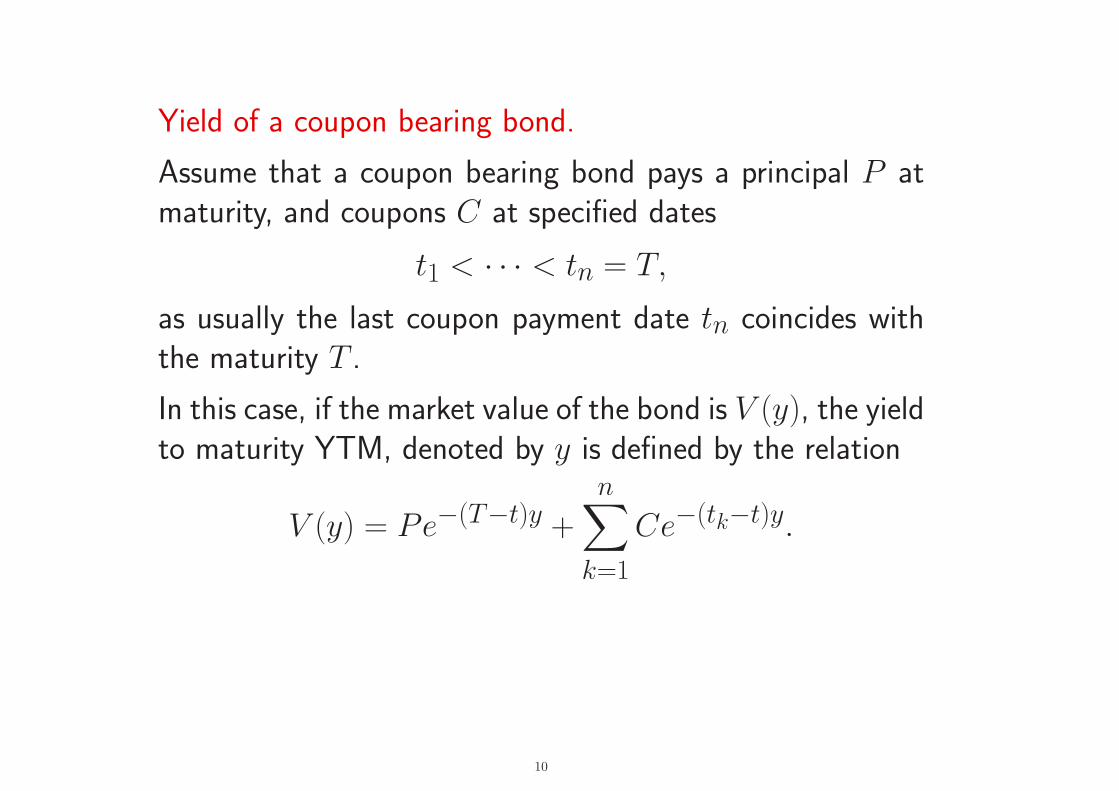

Yield of a coupon bearing bond.

Assume that a coupon bearing bond pays a principal P atmaturity, and coupons C at specified dates

t1 < · · · < tn = T,

as usually the last coupon payment date tn coincides withthe maturity T .

In this case, if the market value of the bond is V (y), the yieldto maturity YTM, denoted by y is defined by the relation

V (y) = Pe−(T−t)y +

n∑

k=1

Ce−(tk−t)y.

10

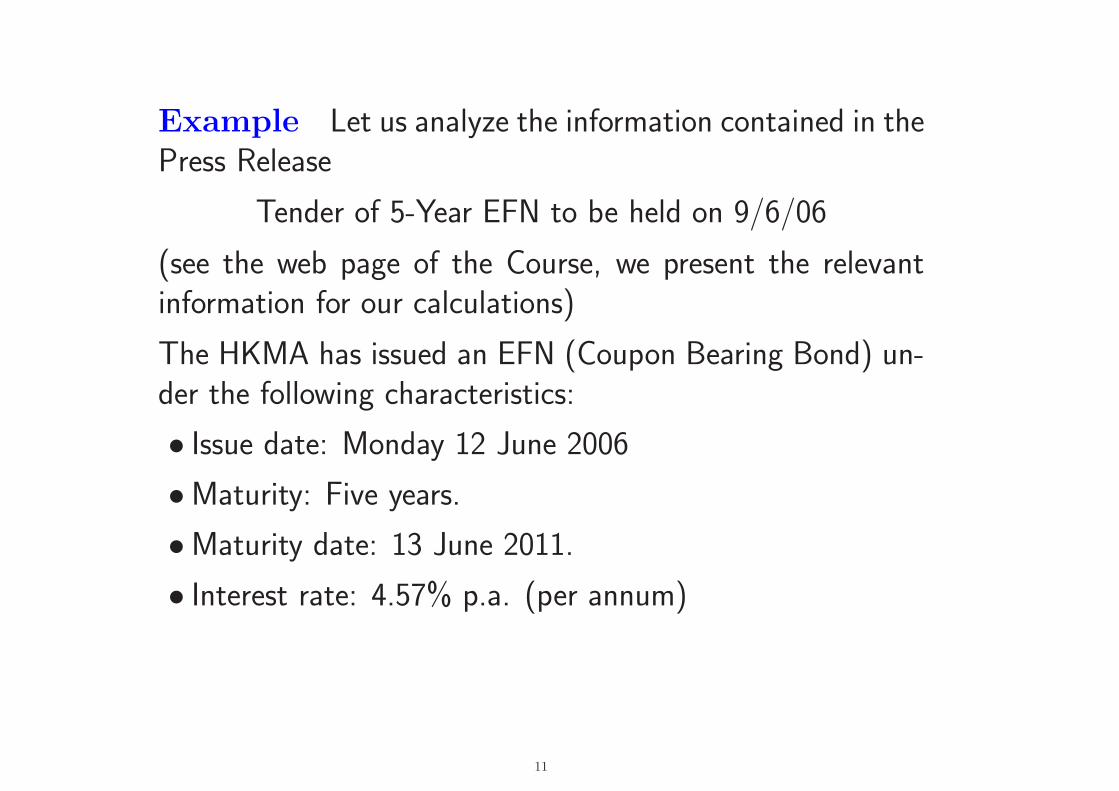

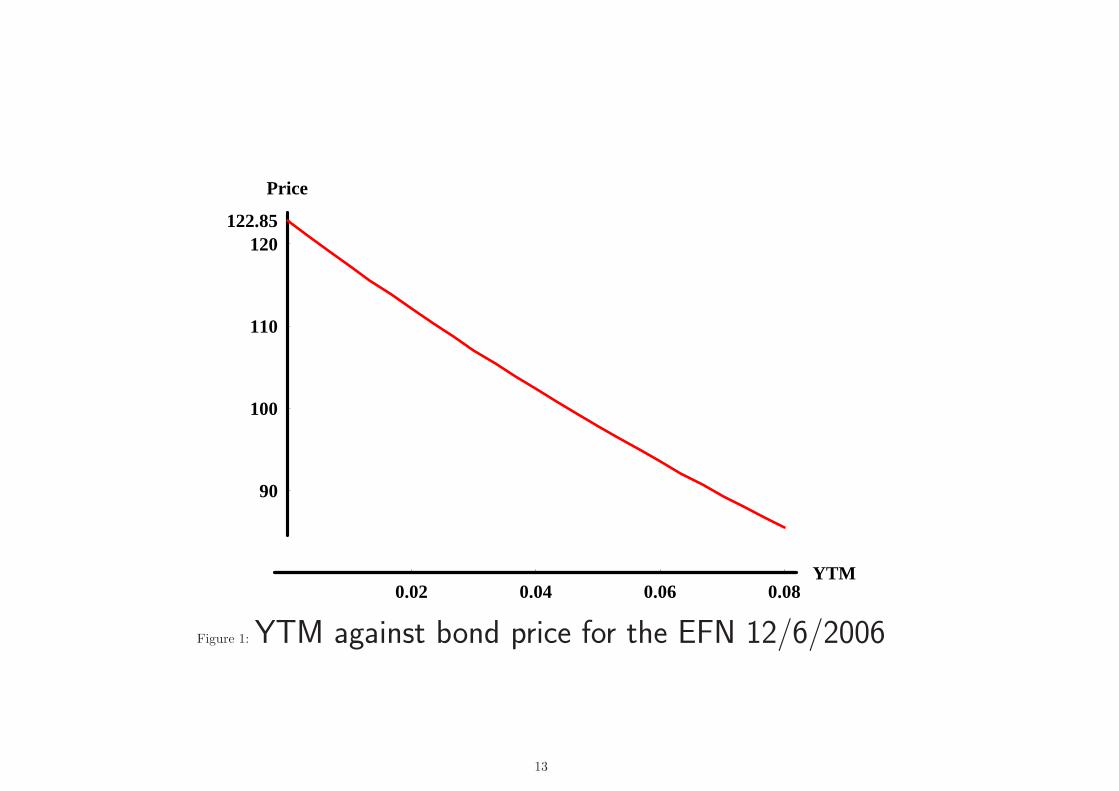

Example Let us analyze the information contained in thePress Release

Tender of 5-Year EFN to be held on 9/6/06

(see the web page of the Course, we present the relevantinformation for our calculations)

The HKMA has issued an EFN (Coupon Bearing Bond) un-der the following characteristics:

• Issue date: Monday 12 June 2006

•Maturity: Five years.

•Maturity date: 13 June 2011.

• Interest rate: 4.57% p.a. (per annum)

11

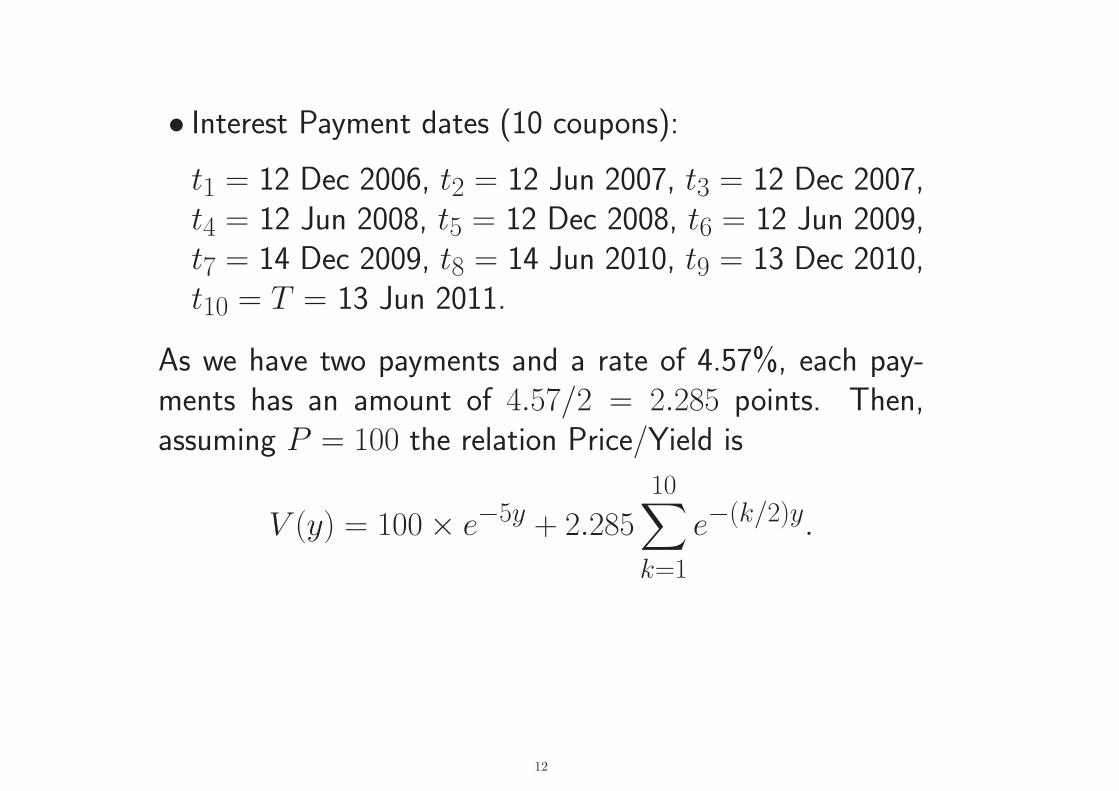

• Interest Payment dates (10 coupons):

t1 = 12 Dec 2006, t2 = 12 Jun 2007, t3 = 12 Dec 2007,t4 = 12 Jun 2008, t5 = 12 Dec 2008, t6 = 12 Jun 2009,t7 = 14 Dec 2009, t8 = 14 Jun 2010, t9 = 13 Dec 2010,t10 = T = 13 Jun 2011.

As we have two payments and a rate of 4.57%, each pay-ments has an amount of 4.57/2 = 2.285 points. Then,assuming P = 100 the relation Price/Yield is

V (y) = 100 × e−5y + 2.285

10∑

k=1

e−(k/2)y.

12

0.02 0.04 0.06 0.08YTM

90

100

110

120122.85

Price

Figure 1: YTM against bond price for the EFN 12/6/2006

13

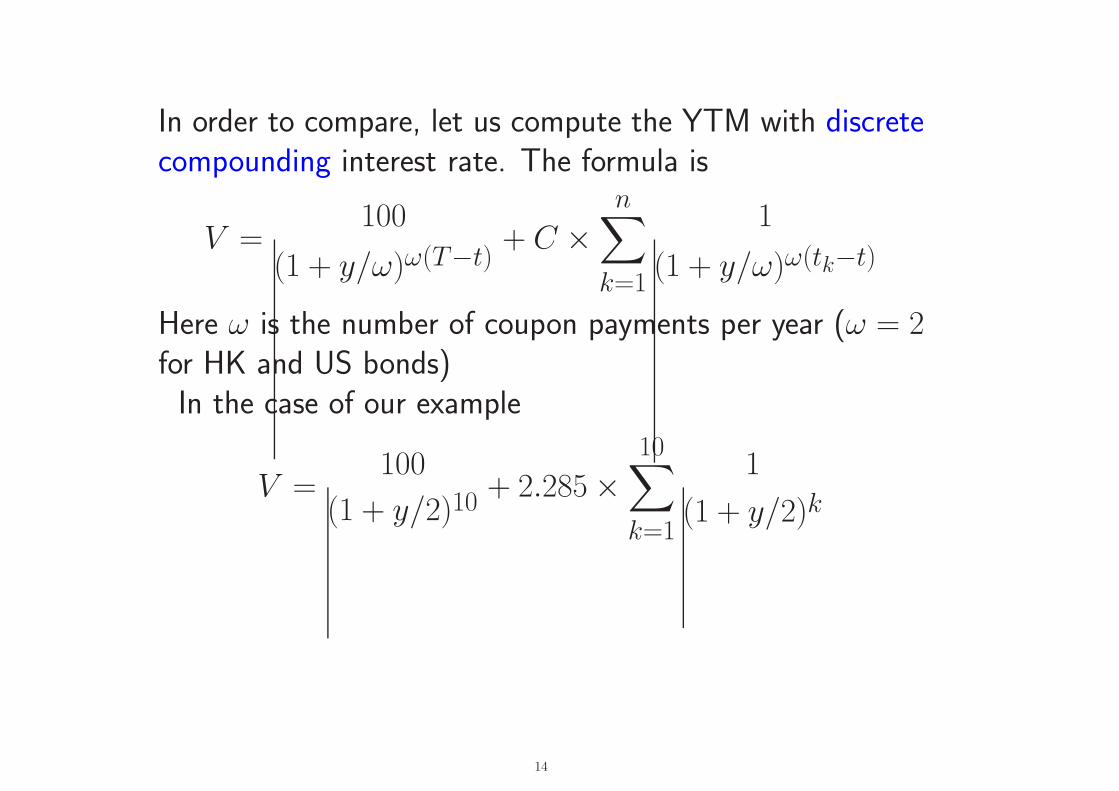

In order to compare, let us compute the YTM with discretecompounding interest rate. The formula is

V =100

(1 + y/ω)ω(T−t)+ C ×

n∑

k=1

1

(1 + y/ω)ω(tk−t)

Here ω is the number of coupon payments per year (ω = 2for HK and US bonds)In the case of our example

V =100

(1 + y/2)10+ 2.285 ×

10∑

k=1

1

(1 + y/2)k

14

0.02 0.04 0.06 0.08YTM

90

100

110

120122.85

Price

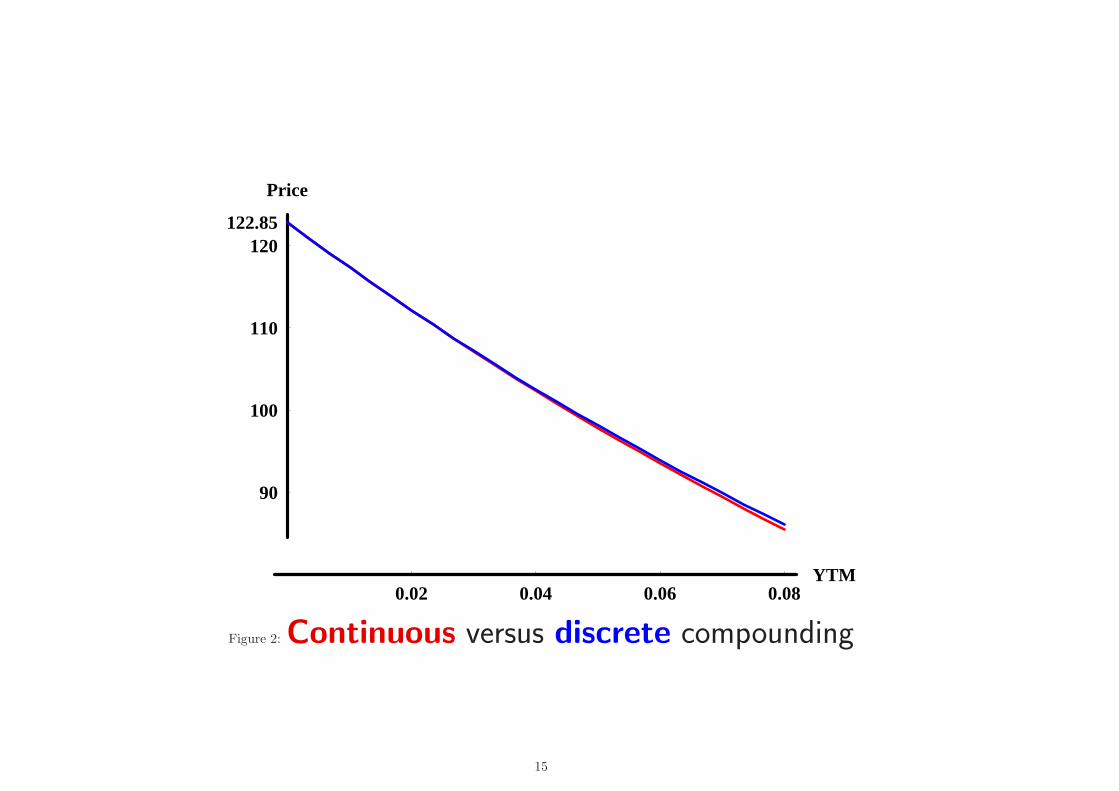

Figure 2: Continuous versus discrete compounding

15

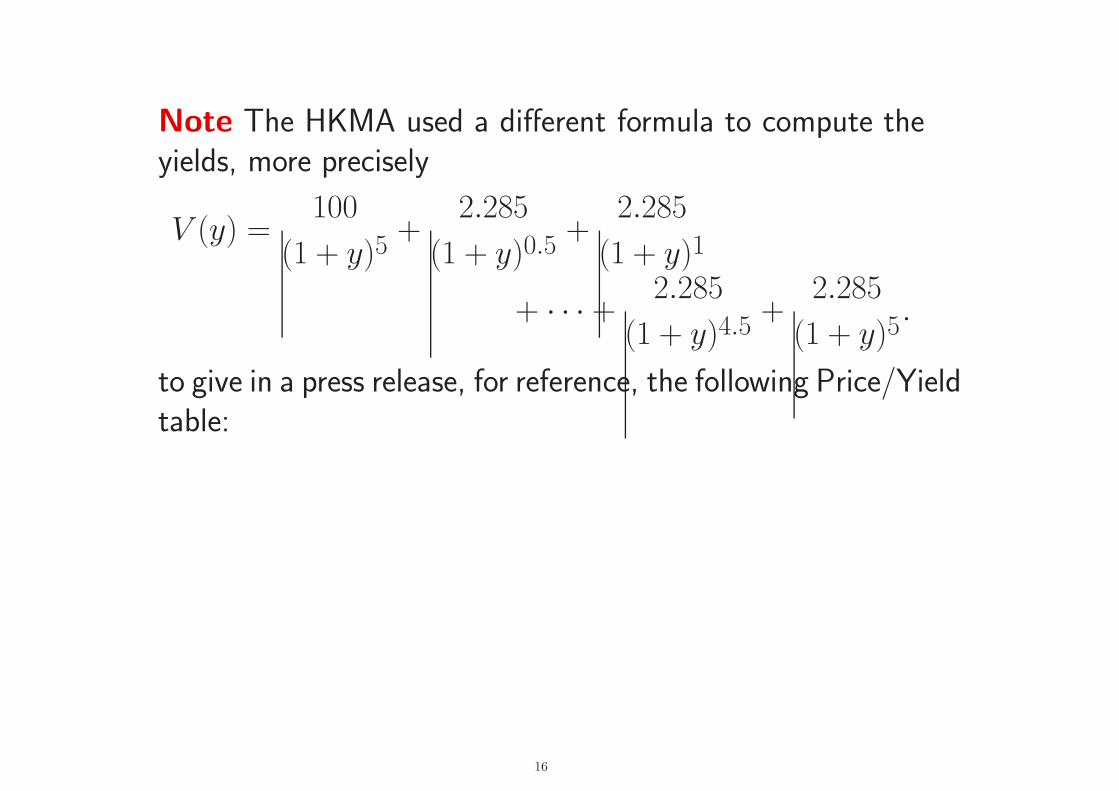

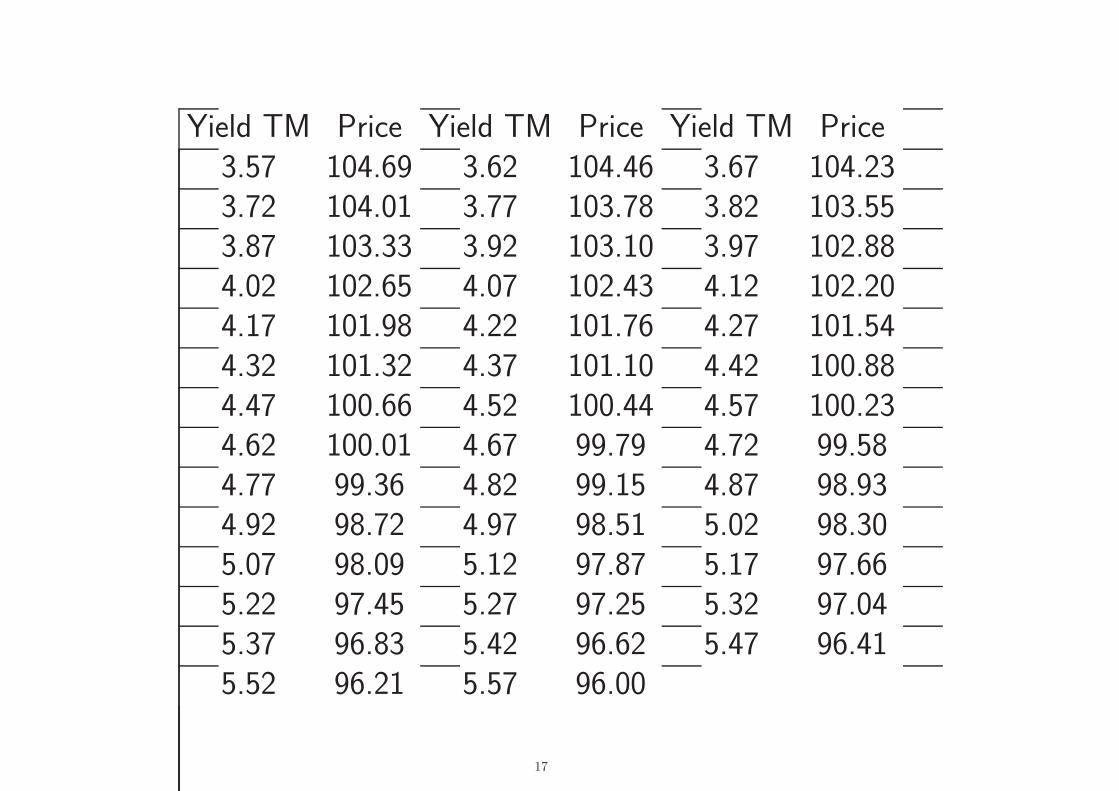

Note The HKMA used a different formula to compute theyields, more precisely

V (y) =100

(1 + y)5+

2.285

(1 + y)0.5+

2.285

(1 + y)1

+ · · · +2.285

(1 + y)4.5+

2.285

(1 + y)5.

to give in a press release, for reference, the following Price/Yieldtable:

16

Yield TM Price Yield TM Price Yield TM Price3.57 104.69 3.62 104.46 3.67 104.233.72 104.01 3.77 103.78 3.82 103.553.87 103.33 3.92 103.10 3.97 102.884.02 102.65 4.07 102.43 4.12 102.204.17 101.98 4.22 101.76 4.27 101.544.32 101.32 4.37 101.10 4.42 100.884.47 100.66 4.52 100.44 4.57 100.234.62 100.01 4.67 99.79 4.72 99.584.77 99.36 4.82 99.15 4.87 98.934.92 98.72 4.97 98.51 5.02 98.305.07 98.09 5.12 97.87 5.17 97.665.22 97.45 5.27 97.25 5.32 97.045.37 96.83 5.42 96.62 5.47 96.415.52 96.21 5.57 96.00

17

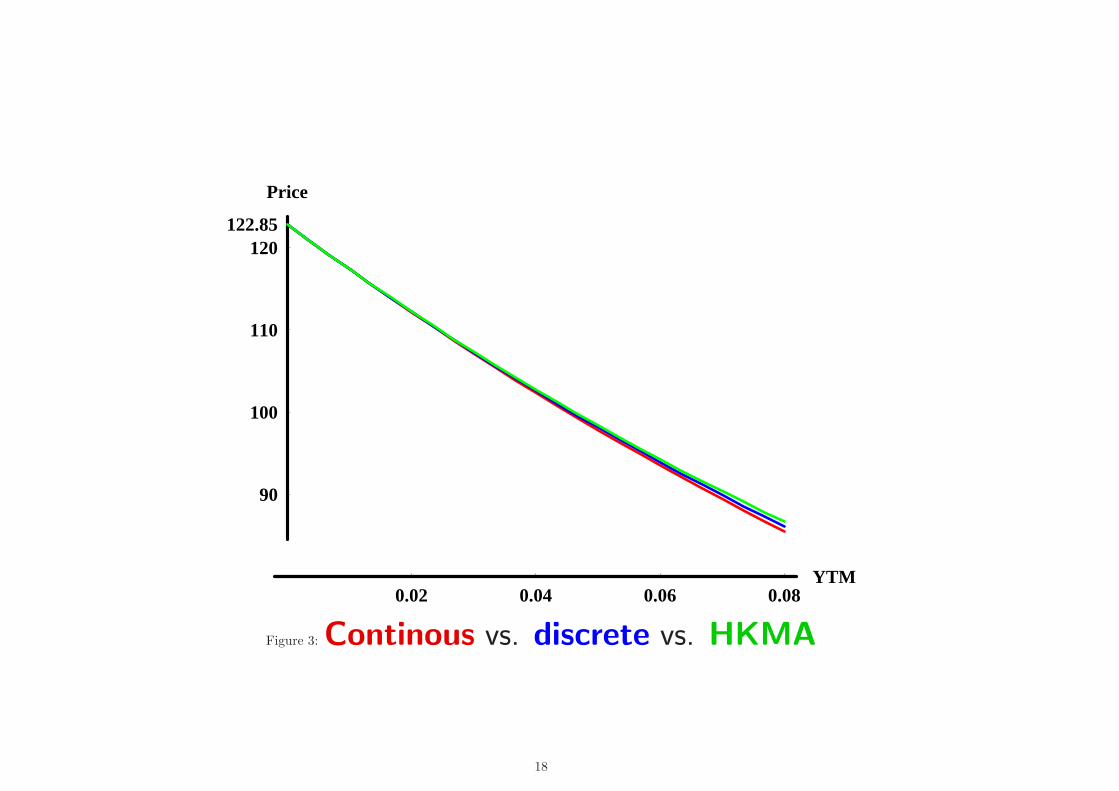

0.02 0.04 0.06 0.08YTM

90

100

110

120122.85

Price

Figure 3: Continous vs. discrete vs. HKMA

18

In fact, the proximity of the curves is not surprising, in viewof the Taylor expansions:

• Continuous compounding

e−ty = 1 − yt +1

2y2t2 + O(y3)

•Discrete compounding

1

(1 + y/2)2t= 1 − yt +

1

2y2

(

t2 +t

2

)

+ O(y3)

• HKMA1

(1 + y)t= 1 − yt +

1

2y2

(

t2 + t)

+ O(y3)

19

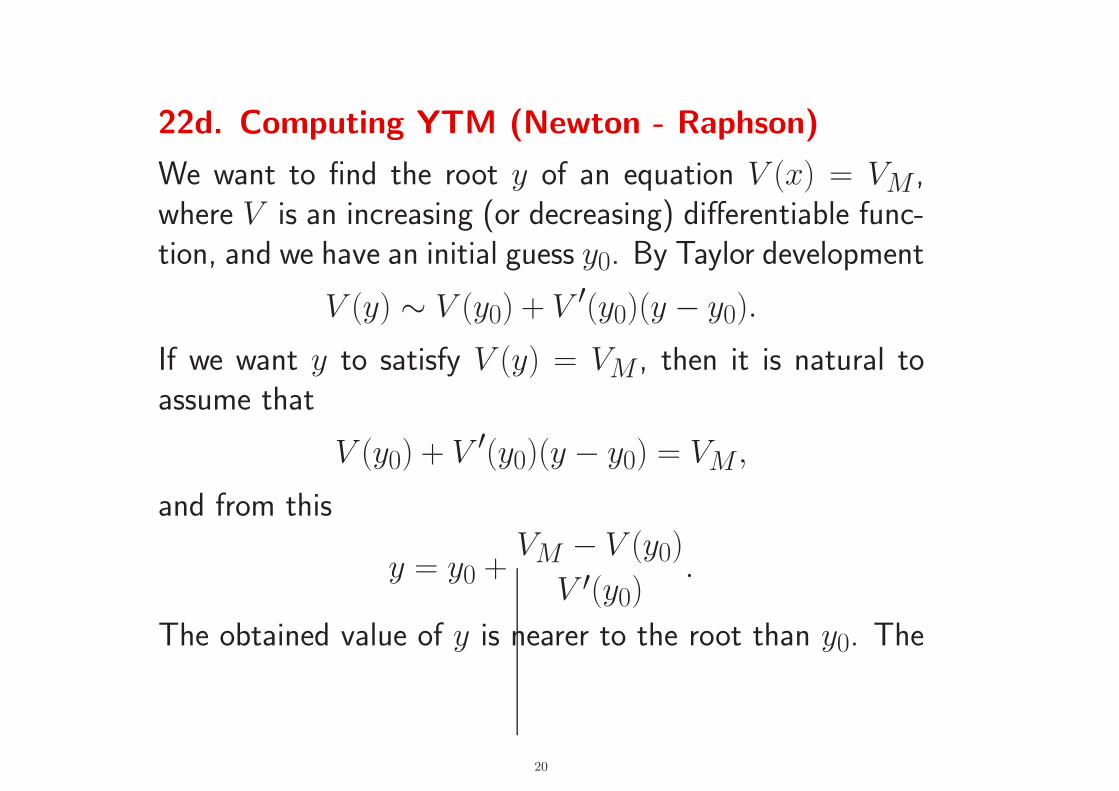

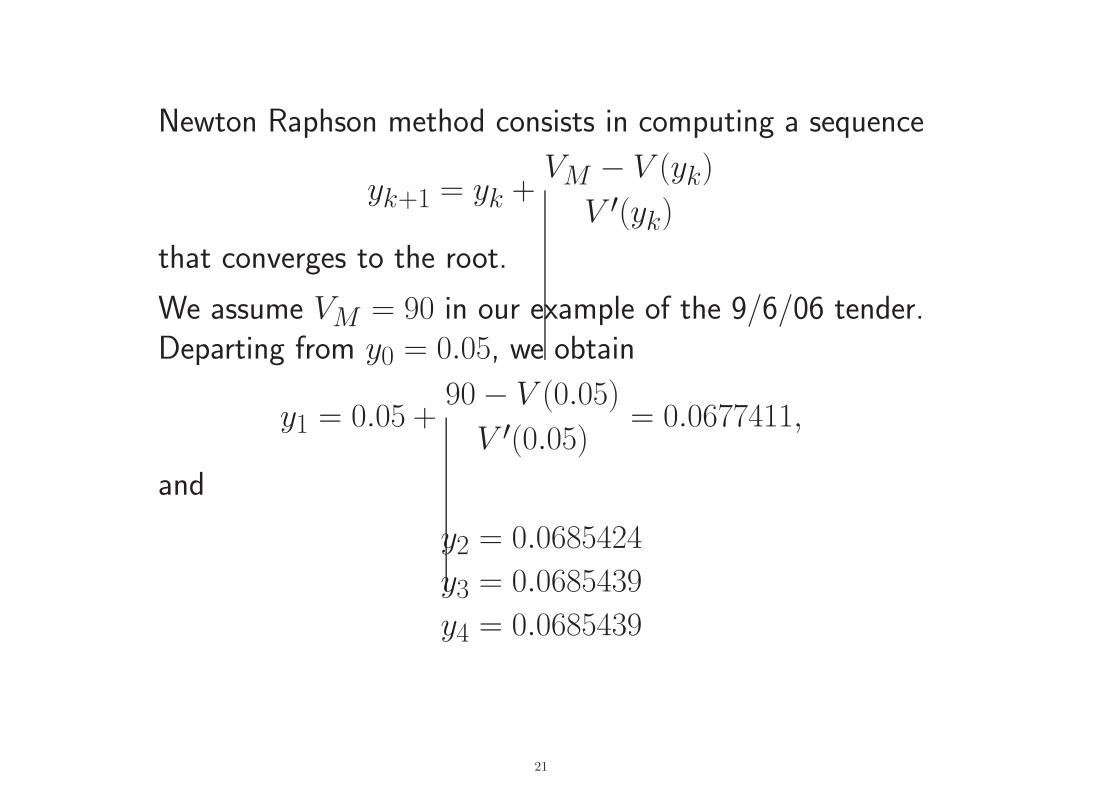

22d. Computing YTM (Newton - Raphson)

We want to find the root y of an equation V (x) = VM ,where V is an increasing (or decreasing) differentiable func-tion, and we have an initial guess y0. By Taylor development

V (y) ∼ V (y0) + V ′(y0)(y − y0).

If we want y to satisfy V (y) = VM , then it is natural toassume that

V (y0) + V ′(y0)(y − y0) = VM ,

and from this

y = y0 +VM − V (y0)

V ′(y0).

The obtained value of y is nearer to the root than y0. The

20

Newton Raphson method consists in computing a sequence

yk+1 = yk +VM − V (yk)

V ′(yk)

that converges to the root.

We assume VM = 90 in our example of the 9/6/06 tender.Departing from y0 = 0.05, we obtain

y1 = 0.05 +90 − V (0.05)

V ′(0.05)= 0.0677411,

and

y2 = 0.0685424

y3 = 0.0685439

y4 = 0.0685439

21

23. Duration, Convexity and Yield Curves

MA6622, Ernesto Mordecki, CityU, HK, 2010.

References for this Lecture:

Marco Avellaneda and Peter Laurence, Quantitative Mod-

elling of Derivative Securities, Chapman&Hall (2000).

P. Willmot, Derivatives, Wiley (1998).

Hong Kong Monetary Authority (HKMA) Web Page:http://www.info.gov.hk/hkma/

22

Plan of Lecture 23

(23a) Yield to maturity of a EFN during its life

(23b) Bond Duration

(23c) Yield Curve

(23d) Cash Flows

(23e) Other Fixed Income securities

23

23a. Yield to maturity of a EFN during its life

The yield to maturity is also computed during the life of thebond.

Example We take for reference the Exchange Fund Note5709. in the “Reference Prices and Yields for Exchange FundNotes, from 11:00 a.m. July 4, 2006” issued by the HKMA.Relevant bond characteristics information for us are:

• EFN Issue Nr 1801,

•Maturity: Jan 21, 2008,

• Coupon interest rate: 9.89%,

• Price: VC = 108.06 (clean price)

24

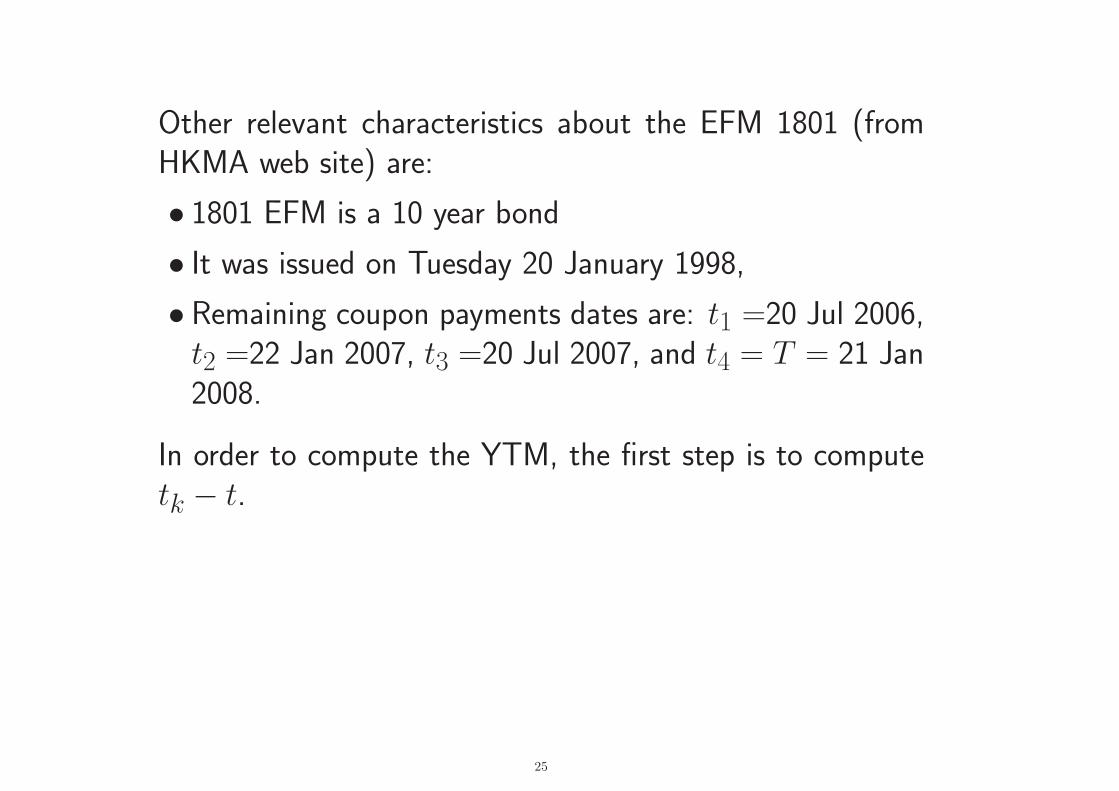

Other relevant characteristics about the EFM 1801 (fromHKMA web site) are:

• 1801 EFM is a 10 year bond

• It was issued on Tuesday 20 January 1998,

• Remaining coupon payments dates are: t1 =20 Jul 2006,t2 =22 Jan 2007, t3 =20 Jul 2007, and t4 = T = 21 Jan2008.

In order to compute the YTM, the first step is to computetk − t.

25

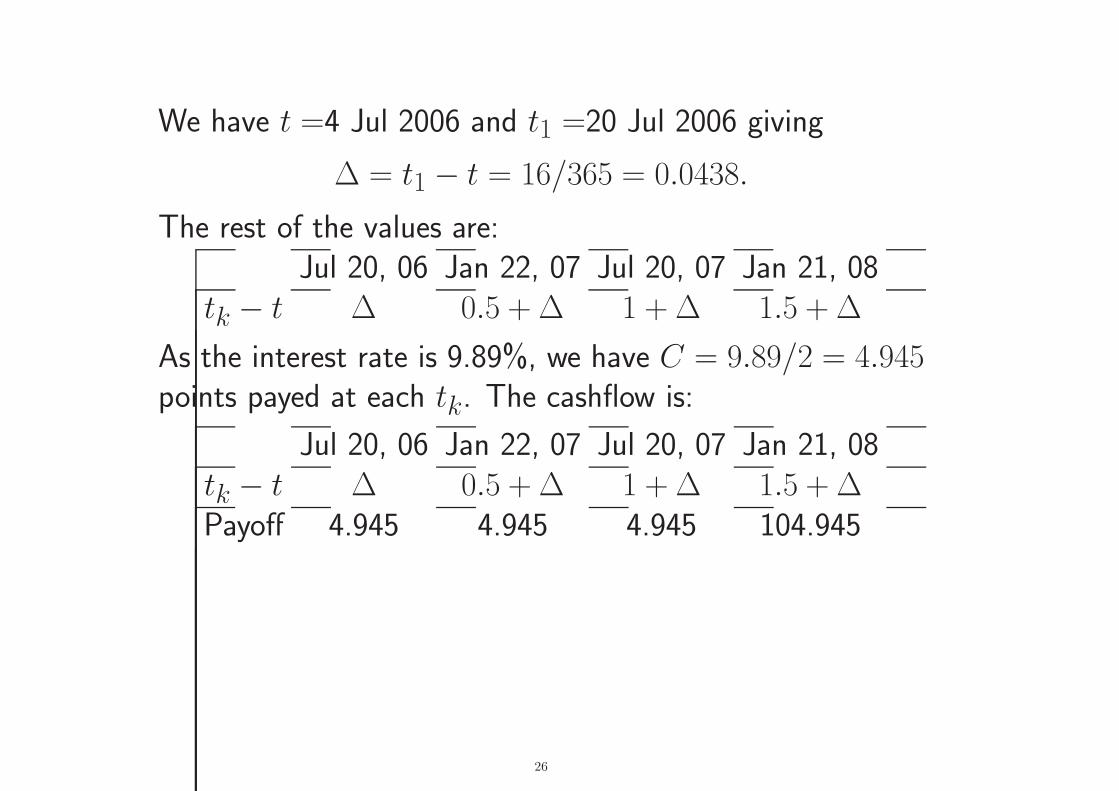

We have t =4 Jul 2006 and t1 =20 Jul 2006 giving

∆ = t1 − t = 16/365 = 0.0438.

The rest of the values are:Jul 20, 06 Jan 22, 07 Jul 20, 07 Jan 21, 08

tk − t ∆ 0.5 + ∆ 1 + ∆ 1.5 + ∆

As the interest rate is 9.89%, we have C = 9.89/2 = 4.945points payed at each tk. The cashflow is:

Jul 20, 06 Jan 22, 07 Jul 20, 07 Jan 21, 08tk − t ∆ 0.5 + ∆ 1 + ∆ 1.5 + ∆Payoff 4.945 4.945 4.945 104.945

26

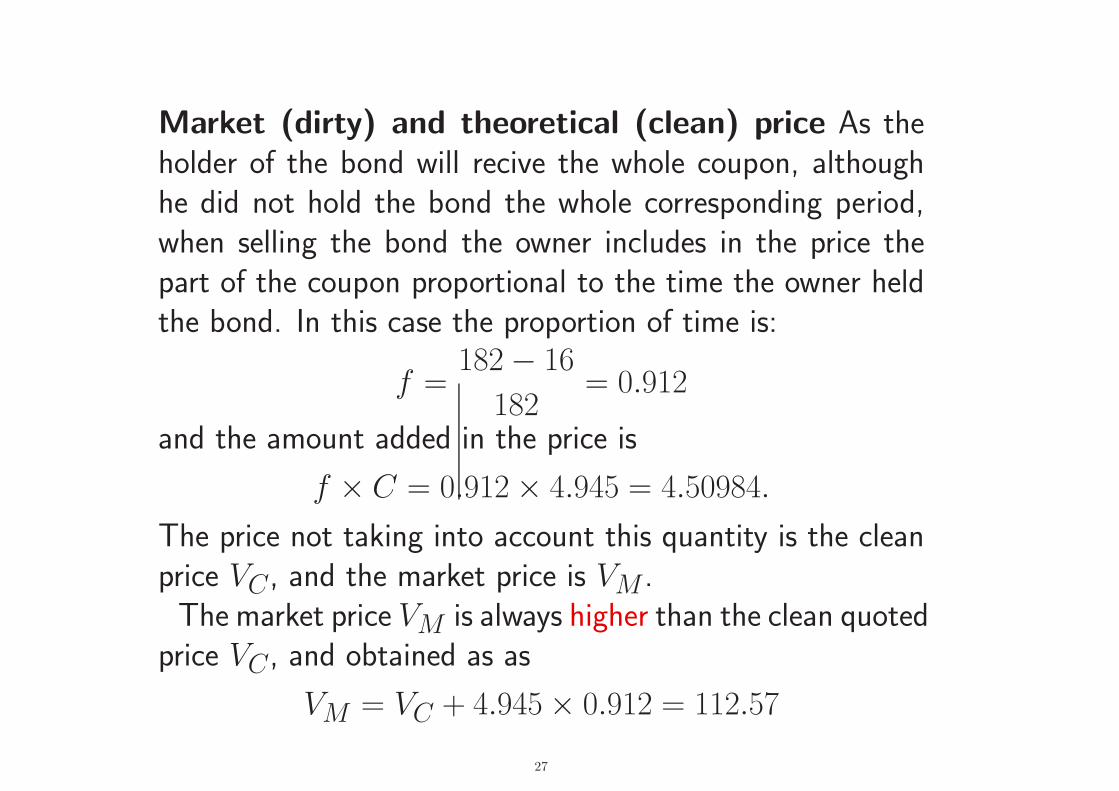

Market (dirty) and theoretical (clean) price As theholder of the bond will recive the whole coupon, althoughhe did not hold the bond the whole corresponding period,when selling the bond the owner includes in the price thepart of the coupon proportional to the time the owner heldthe bond. In this case the proportion of time is:

f =182 − 16

182= 0.912

and the amount added in the price is

f × C = 0.912 × 4.945 = 4.50984.

The price not taking into account this quantity is the cleanprice VC , and the market price is VM .The market price VM is always higher than the clean quoted

price VC , and obtained as as

VM = VC + 4.945 × 0.912 = 112.57

27

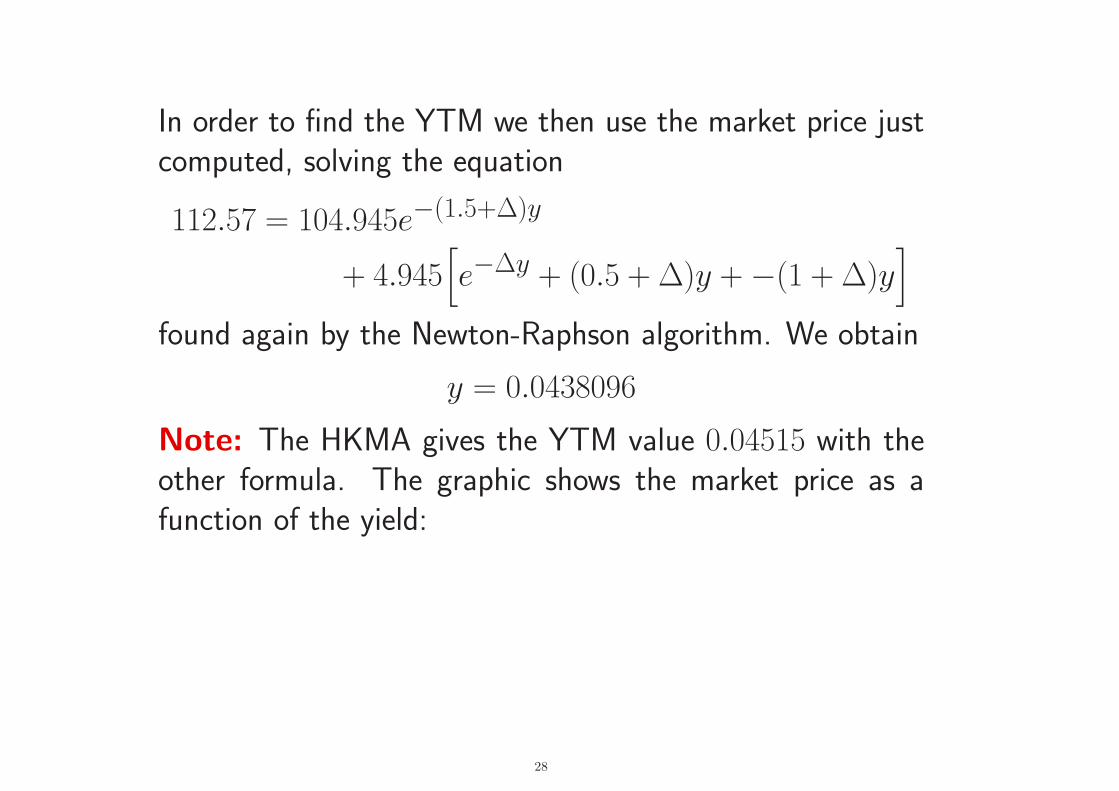

In order to find the YTM we then use the market price justcomputed, solving the equation

112.57 = 104.945e−(1.5+∆)y

+ 4.945[

e−∆y + (0.5 + ∆)y + −(1 + ∆)y]

found again by the Newton-Raphson algorithm. We obtain

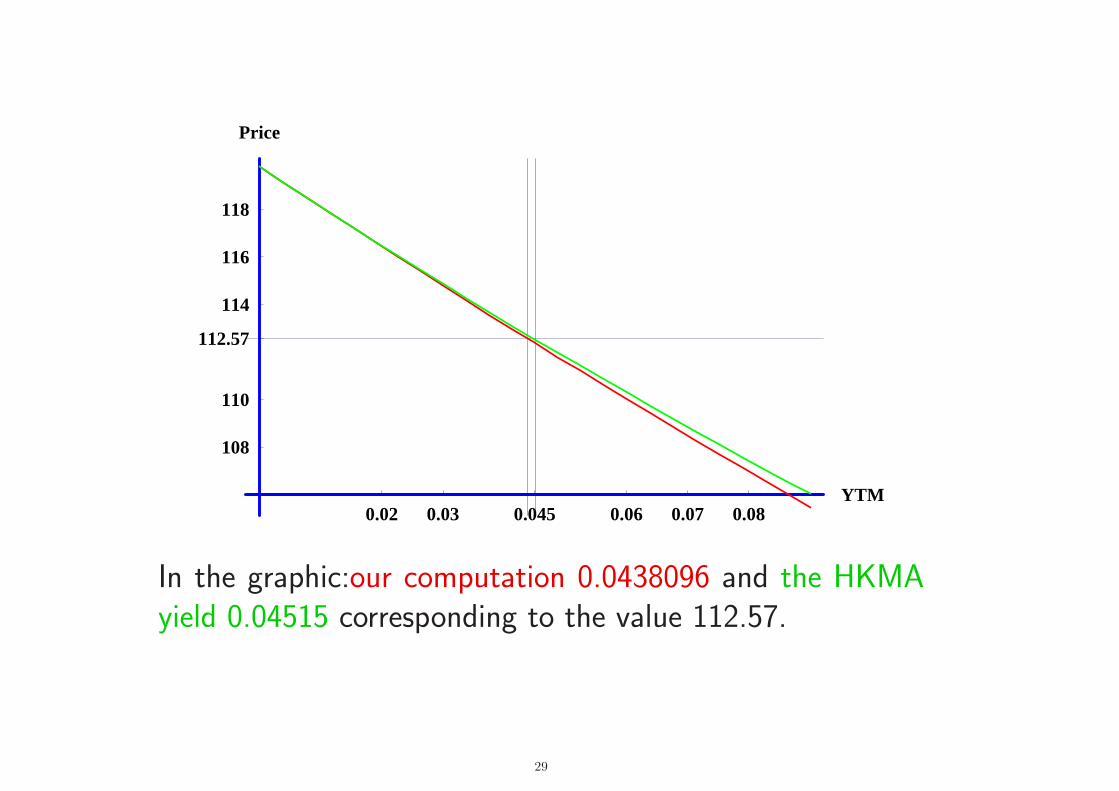

y = 0.0438096

Note: The HKMA gives the YTM value 0.04515 with theother formula. The graphic shows the market price as afunction of the yield:

28

0.02 0.03 0.045 0.06 0.07 0.08YTM

108

112.57

110

114

116

118

Price

In the graphic:our computation 0.0438096 and the HKMAyield 0.04515 corresponding to the value 112.57.

29

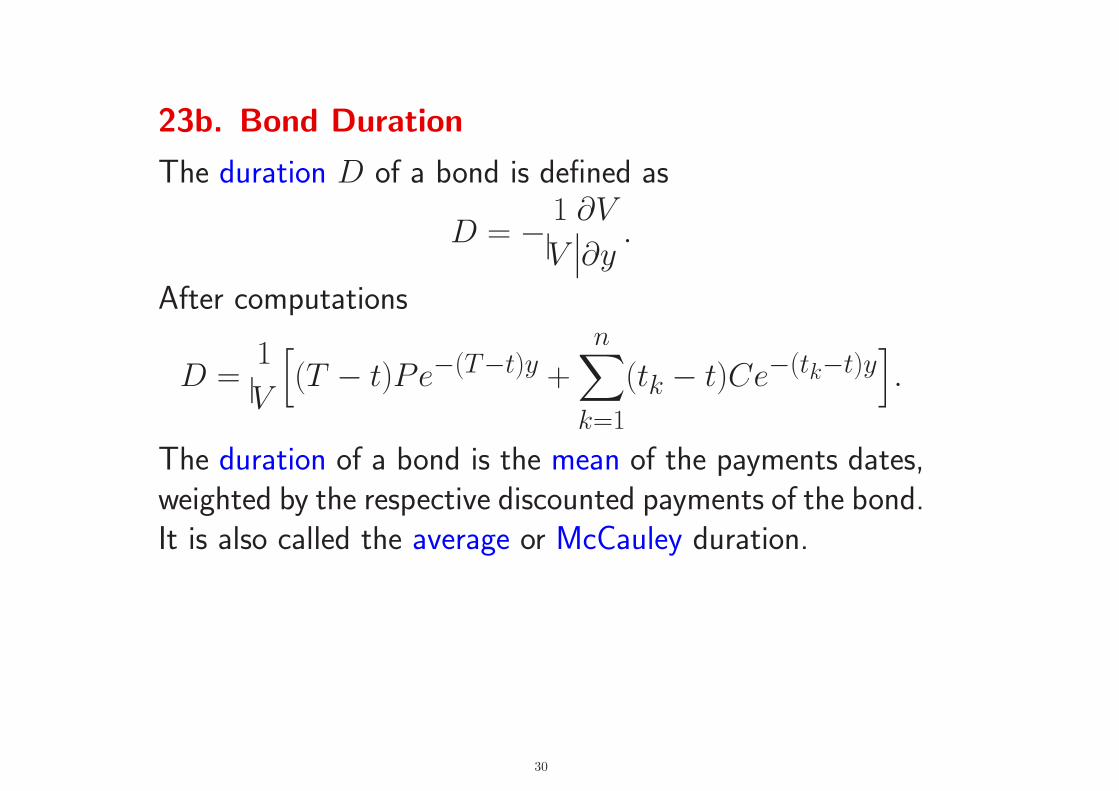

23b. Bond Duration

The duration D of a bond is defined as

D = −1

V

∂V

∂y.

After computations

D =1

V

[

(T − t)Pe−(T−t)y +

n∑

k=1

(tk − t)Ce−(tk−t)y]

.

The duration of a bond is the mean of the payments dates,weighted by the respective discounted payments of the bond.It is also called the average or McCauley duration.

30

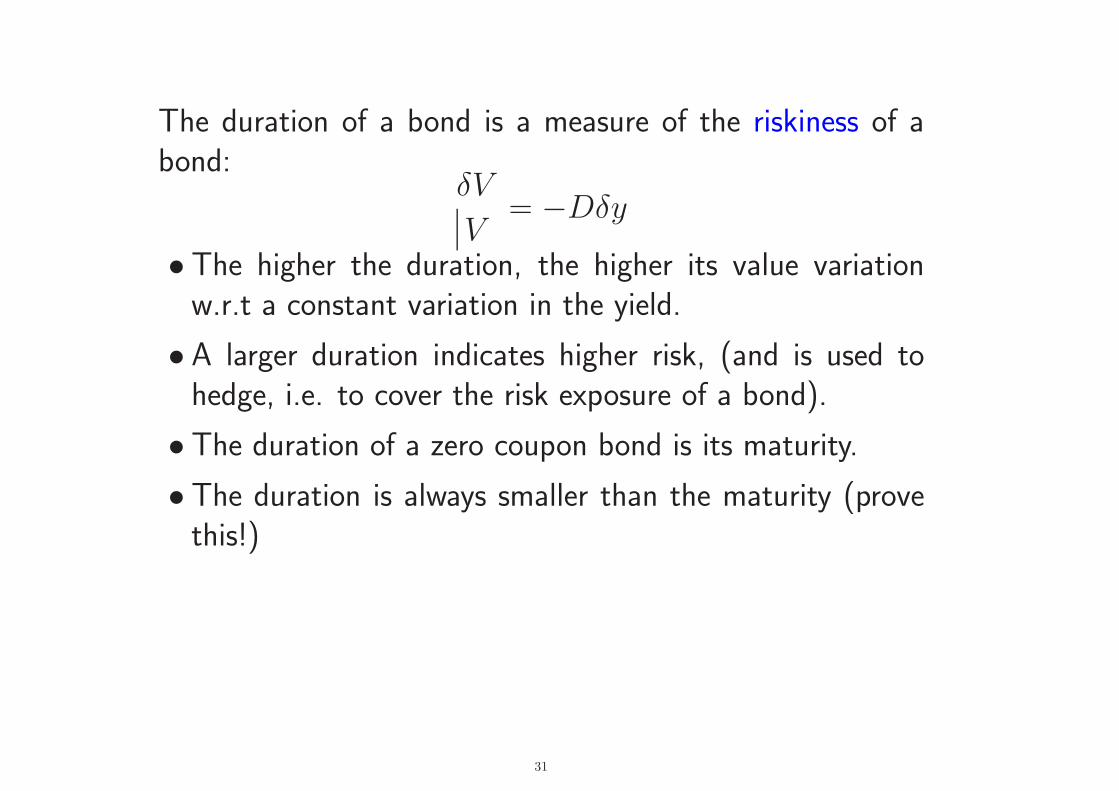

The duration of a bond is a measure of the riskiness of abond:

δV

V= −Dδy

• The higher the duration, the higher its value variationw.r.t a constant variation in the yield.

• A larger duration indicates higher risk, (and is used tohedge, i.e. to cover the risk exposure of a bond).

• The duration of a zero coupon bond is its maturity.

• The duration is always smaller than the maturity (provethis!)

31

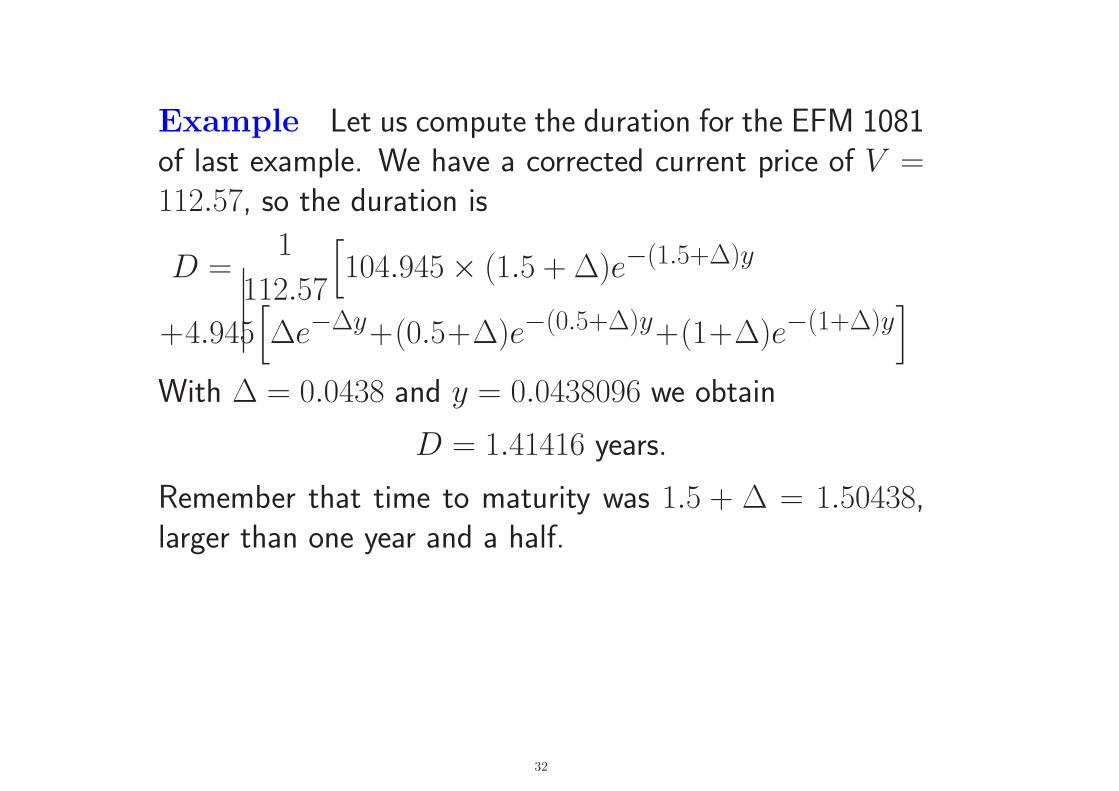

Example Let us compute the duration for the EFM 1081of last example. We have a corrected current price of V =112.57, so the duration is

D =1

112.57

[

104.945 × (1.5 + ∆)e−(1.5+∆)y

+4.945[

∆e−∆y+(0.5+∆)e−(0.5+∆)y+(1+∆)e−(1+∆)y]

With ∆ = 0.0438 and y = 0.0438096 we obtain

D = 1.41416 years.

Remember that time to maturity was 1.5 + ∆ = 1.50438,larger than one year and a half.

32

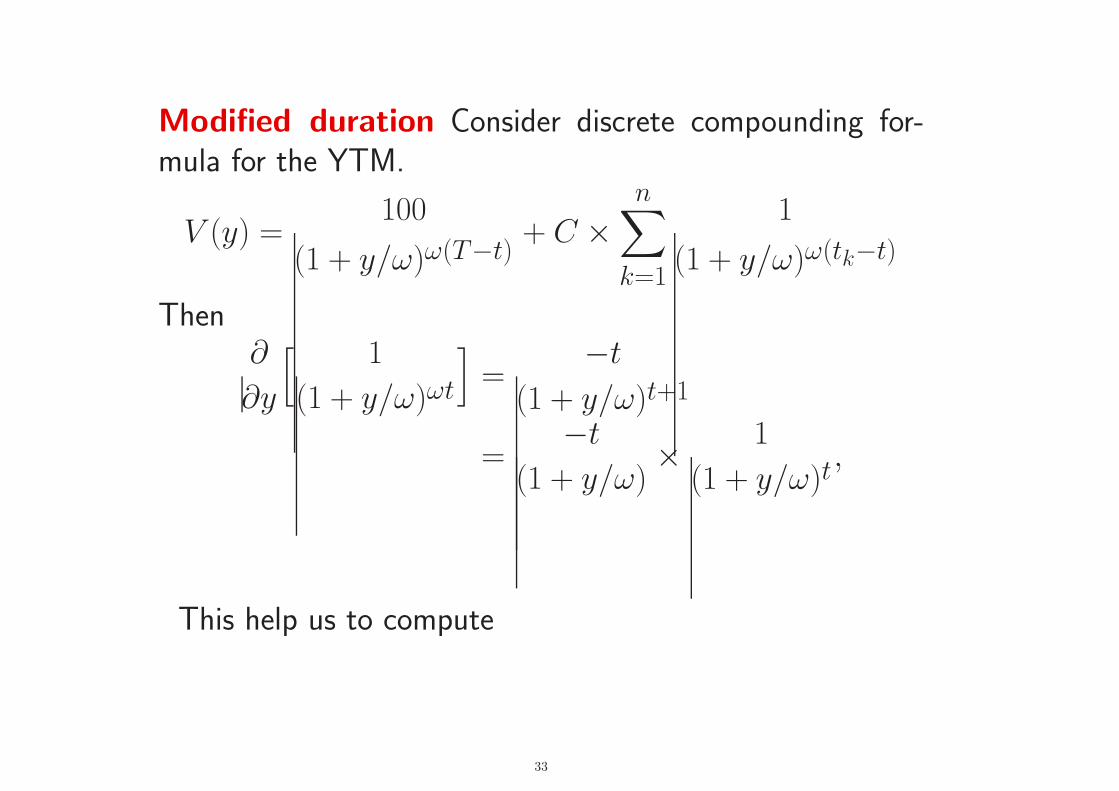

Modified duration Consider discrete compounding for-mula for the YTM.

V (y) =100

(1 + y/ω)ω(T−t)+ C ×

n∑

k=1

1

(1 + y/ω)ω(tk−t)

Then∂

∂y

[ 1

(1 + y/ω)ωt

]

=−t

(1 + y/ω)t+1

=−t

(1 + y/ω)×

1

(1 + y/ω)t,

This help us to compute

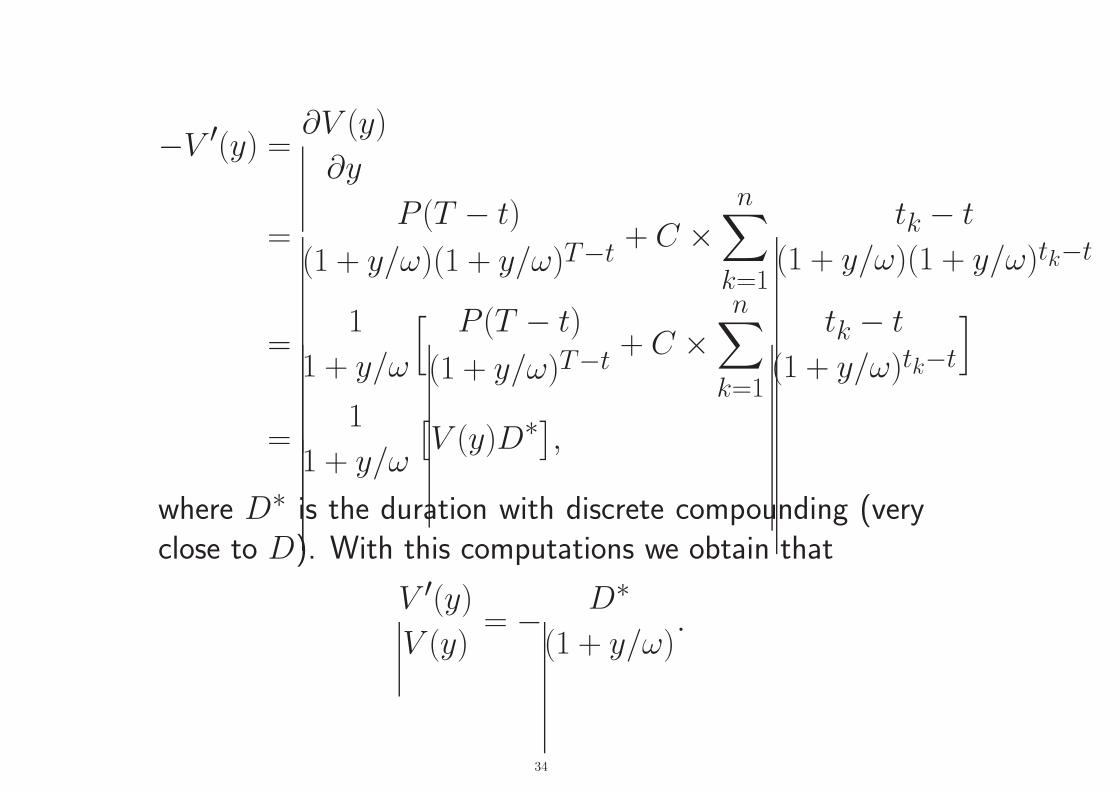

33

−V ′(y) =∂V (y)

∂y

=P (T − t)

(1 + y/ω)(1 + y/ω)T−t+ C ×

n∑

k=1

tk − t

(1 + y/ω)(1 + y/ω)tk−t

=1

1 + y/ω

[ P (T − t)

(1 + y/ω)T−t+ C ×

n∑

k=1

tk − t

(1 + y/ω)tk−t

]

=1

1 + y/ω

[

V (y)D∗]

,

where D∗ is the duration with discrete compounding (veryclose to D). With this computations we obtain that

V ′(y)

V (y)= −

D∗

(1 + y/ω).

34

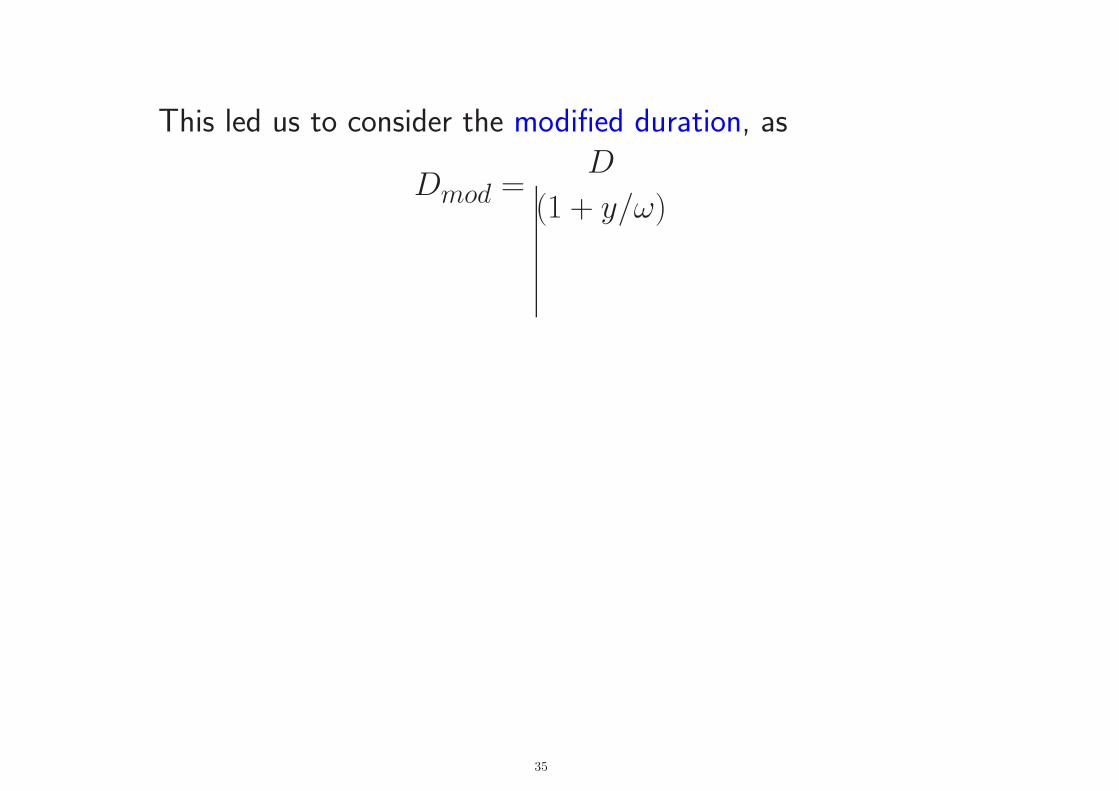

This led us to consider the modified duration, as

Dmod =D

(1 + y/ω)

35

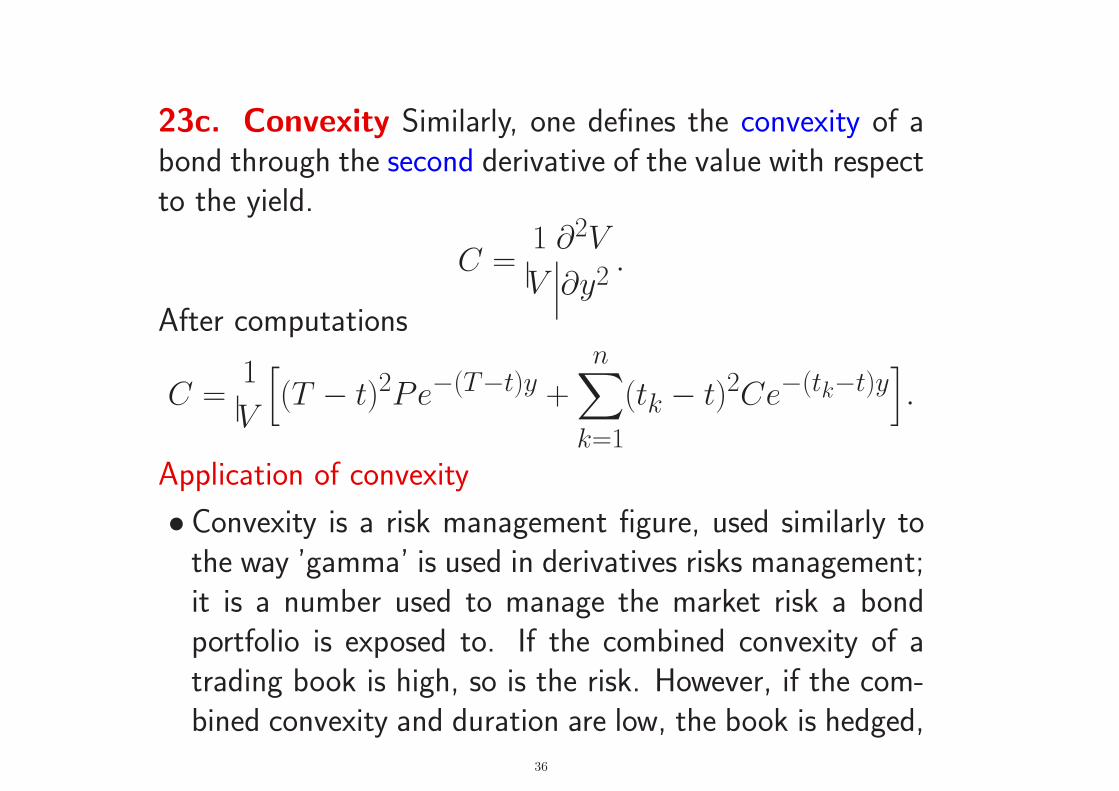

23c. Convexity Similarly, one defines the convexity of abond through the second derivative of the value with respectto the yield.

C =1

V

∂2V

∂y2.

After computations

C =1

V

[

(T − t)2Pe−(T−t)y +

n∑

k=1

(tk − t)2Ce−(tk−t)y]

.

Application of convexity

• Convexity is a risk management figure, used similarly tothe way ’gamma’ is used in derivatives risks management;it is a number used to manage the market risk a bondportfolio is exposed to. If the combined convexity of atrading book is high, so is the risk. However, if the com-bined convexity and duration are low, the book is hedged,

36

and little money will be lost even if fairly substantial in-terest movements occur. (Parallel in the yield curve.)

• The second-order approximation of bond price movementsdue to rate changes uses the convexity:

δV ∼ V[C

2(δy)2 − D(δy)

]

The idea is to hedge with other bonds with similar du-ration and convexity. (this is Taylor expansion of ordertwo)

37

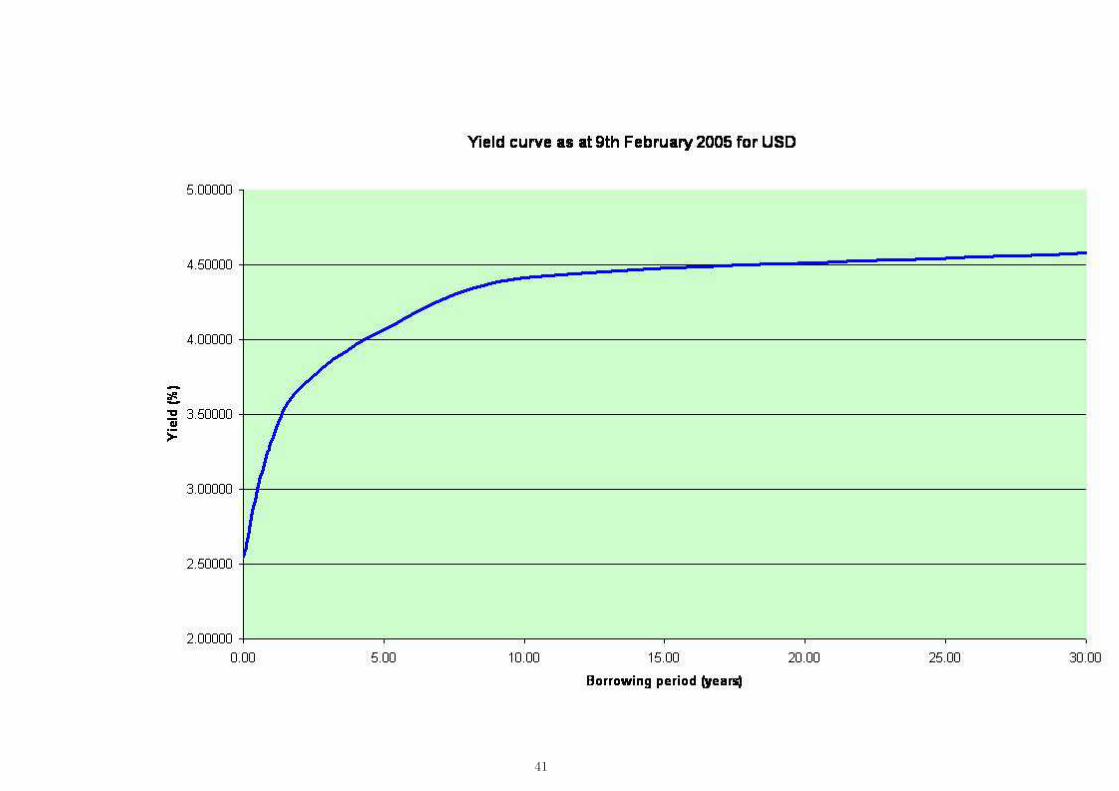

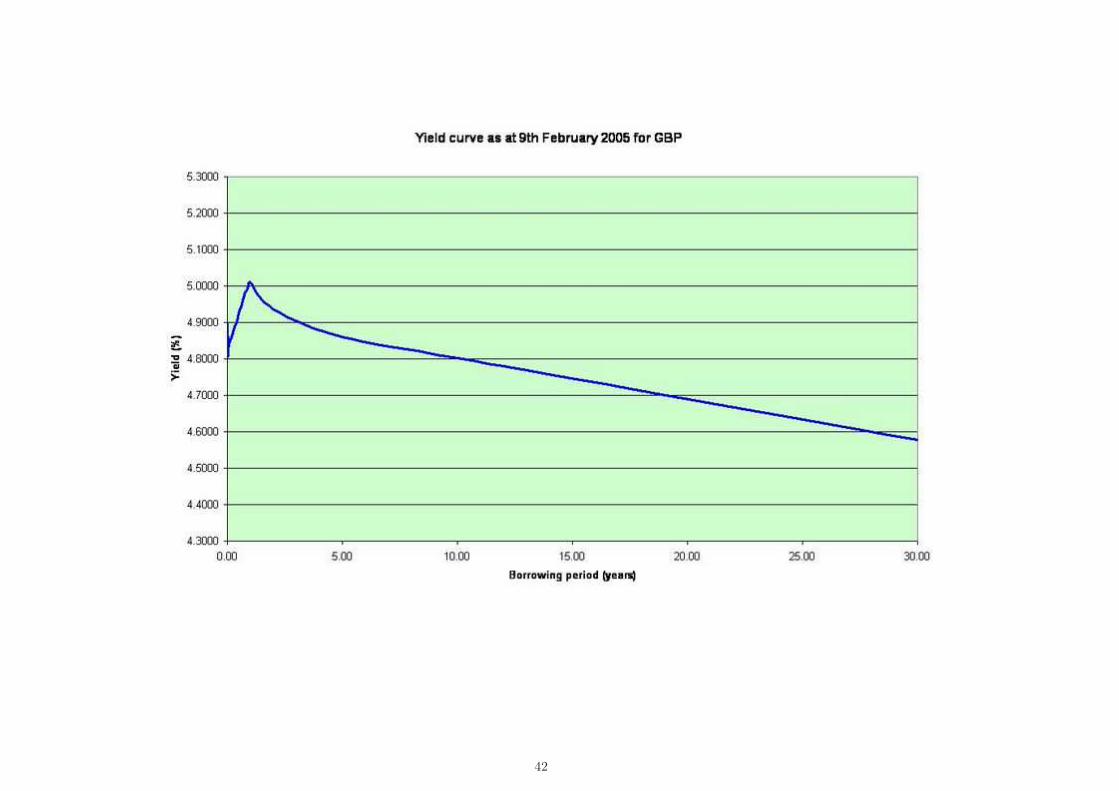

23d. Yield Curve

The yield curve is the relation between the cost of borrowing,or yield, and the maturity of the debt for a given borrowerin a given currency.

For example, the current U.S. dollar interest rates paid onU.S. Treasury securities for various constitute the US yieldcurve.

Let us compute the yield curve for the HKD.

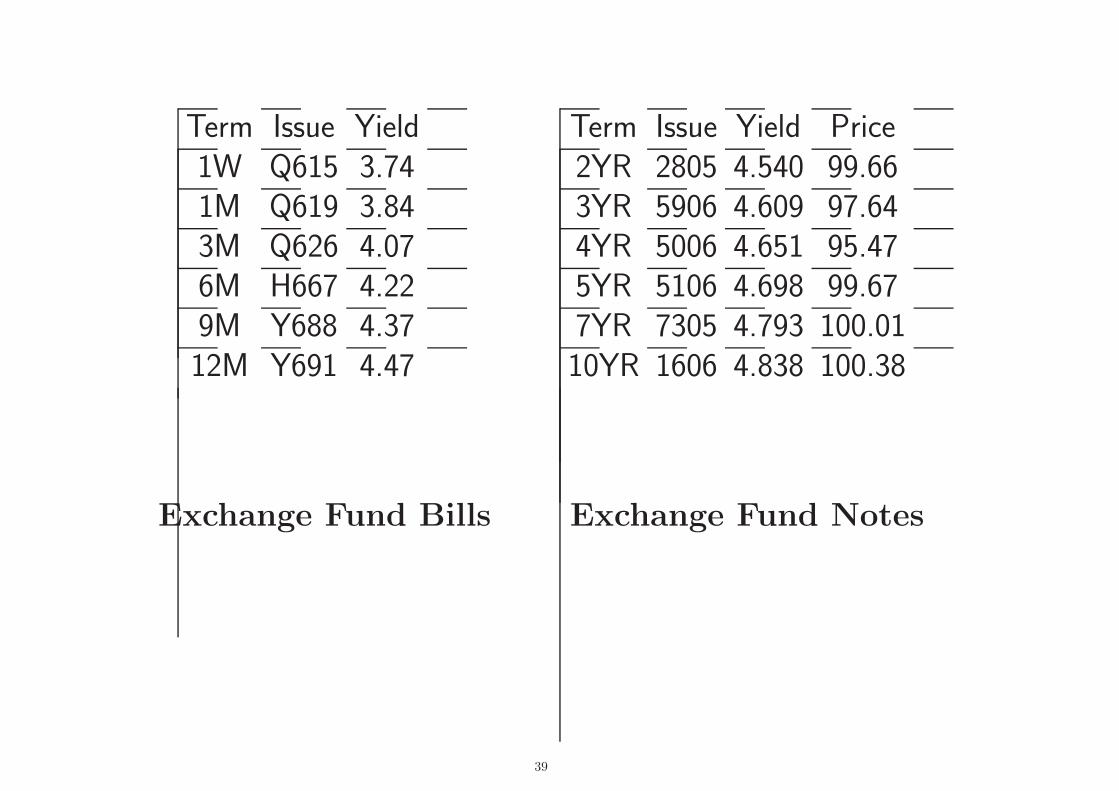

We take the fixings of the HKMA release 4 July 2006, de-tailed in the following tables:

38

Term Issue Yield1W Q615 3.741M Q619 3.843M Q626 4.076M H667 4.229M Y688 4.3712M Y691 4.47

Term Issue Yield Price2YR 2805 4.540 99.663YR 5906 4.609 97.644YR 5006 4.651 95.475YR 5106 4.698 99.677YR 7305 4.793 100.0110YR 1606 4.838 100.38

Exchange Fund Bills Exchange Fund Notes

39

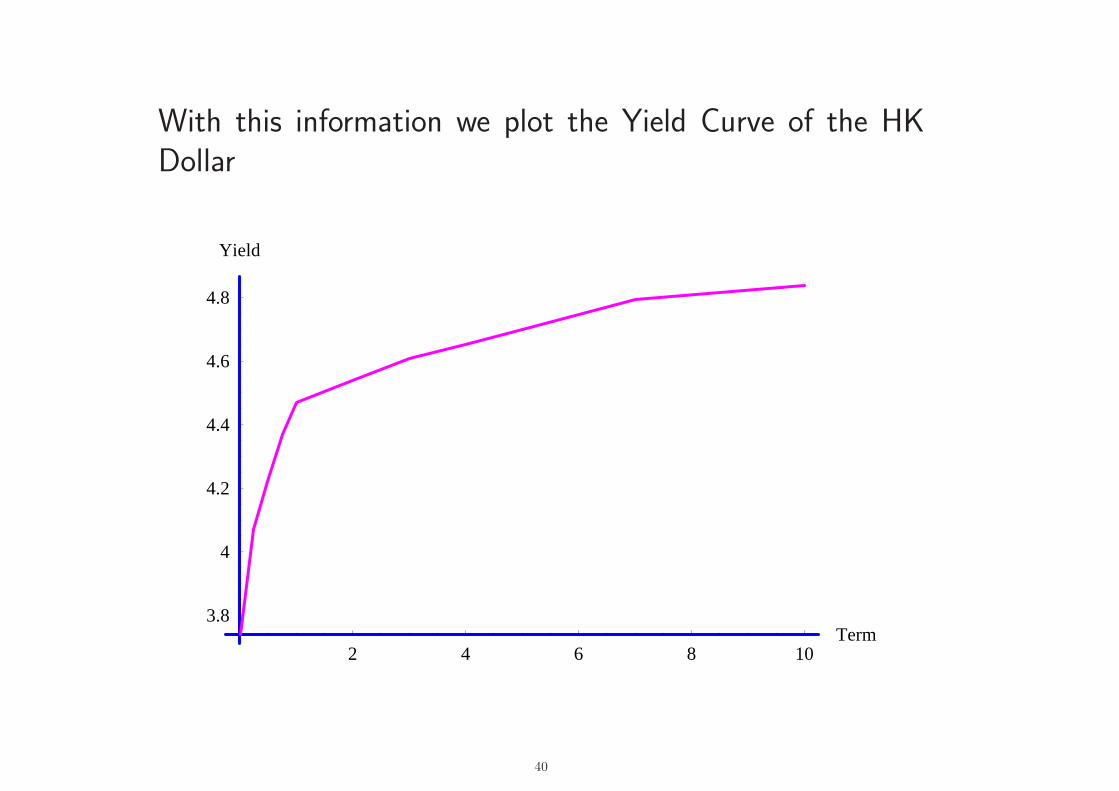

With this information we plot the Yield Curve of the HKDollar

2 4 6 8 10Term

3.8

4

4.2

4.4

4.6

4.8

Yield

40

41

42

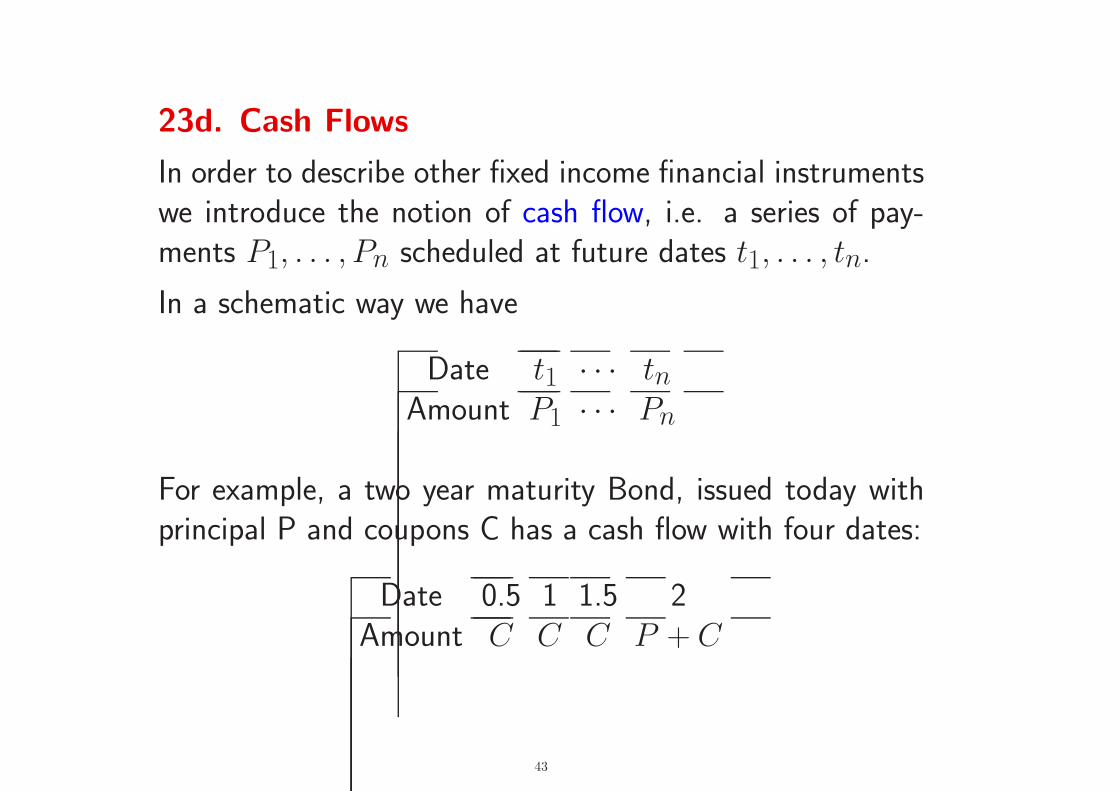

23d. Cash Flows

In order to describe other fixed income financial instrumentswe introduce the notion of cash flow, i.e. a series of pay-ments P1, . . . , Pn scheduled at future dates t1, . . . , tn.

In a schematic way we have

Date t1 · · · tnAmount P1 · · · Pn

For example, a two year maturity Bond, issued today withprincipal P and coupons C has a cash flow with four dates:

Date 0.5 1 1.5 2Amount C C C P + C

43

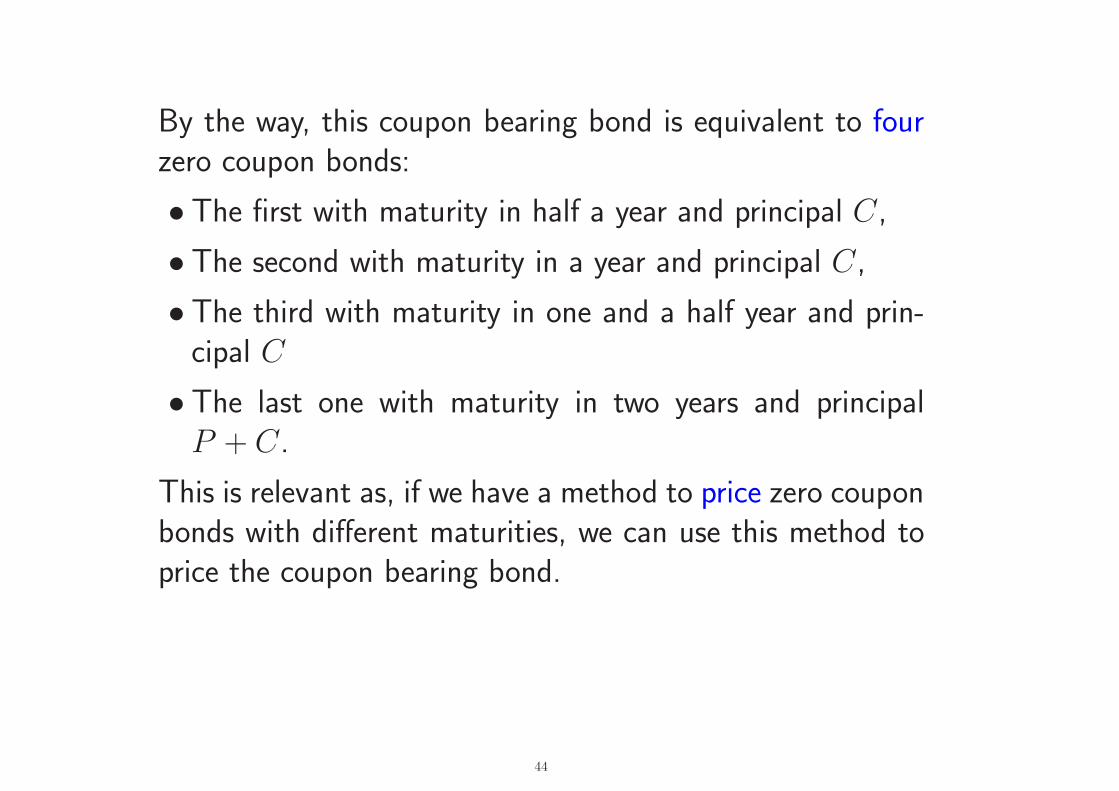

By the way, this coupon bearing bond is equivalent to fourzero coupon bonds:

• The first with maturity in half a year and principal C,

• The second with maturity in a year and principal C,

• The third with maturity in one and a half year and prin-cipal C

• The last one with maturity in two years and principalP + C.

This is relevant as, if we have a method to price zero couponbonds with different maturities, we can use this method toprice the coupon bearing bond.

44

23e. Other Fixed Income securities

A forward rate agreement (FRA) is a contract in which oneparty pays a fixed interest rate, and receives a floating in-terest rate equal to a reference rate (the underlying rate).

The payments are calculated over a notional amount over acertain period.

An interest swap is a contractual agreement between twoparties, in which they agree to make periodic payments toeach other according to two different indices.

In a plain vanilla swap, one party A makes fixed interestrates payments to receive from B floating rate payments.

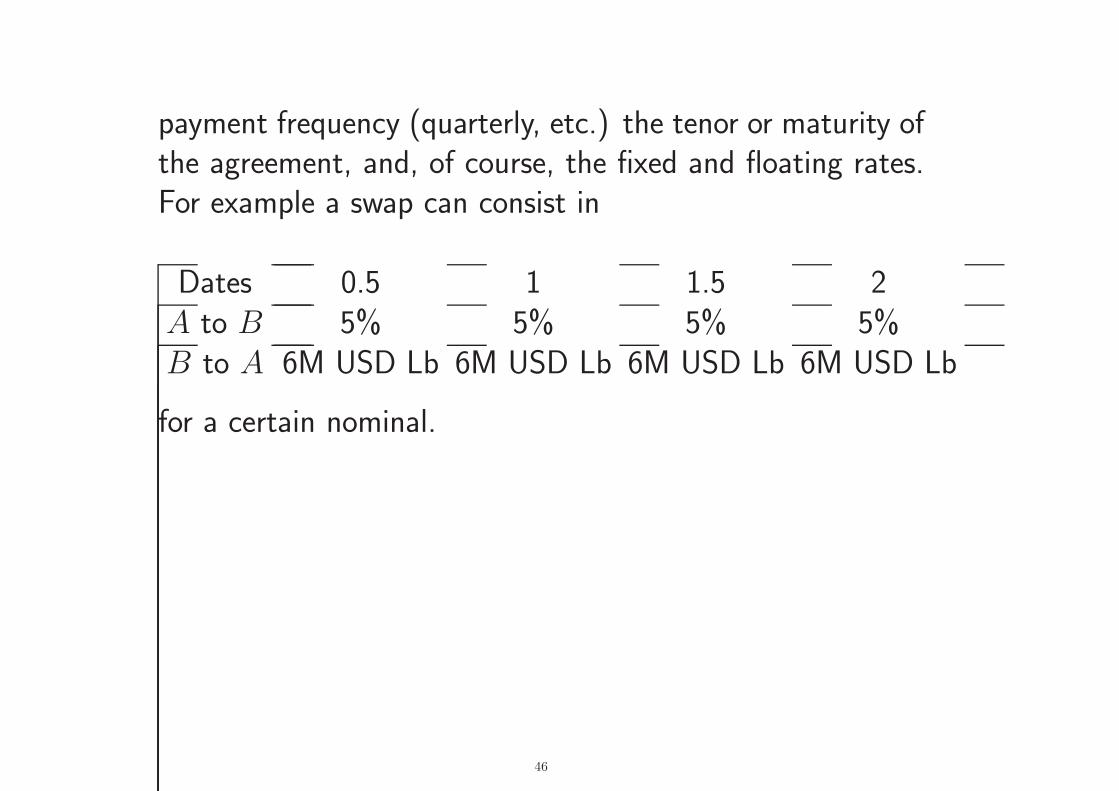

In other words, they agree to interchange a fixed rate cashflow for a floating rate cash flow. The agreement also in-cludes a notional amount or face value of the swap, the

45

payment frequency (quarterly, etc.) the tenor or maturity ofthe agreement, and, of course, the fixed and floating rates.For example a swap can consist in

Dates 0.5 1 1.5 2A to B 5% 5% 5% 5%B to A 6M USD Lb 6M USD Lb 6M USD Lb 6M USD Lb

for a certain nominal.

46

More sophisticated contracts include American features:

• A callable bond is a coupon bearing bond with the ad-ditional feature that the issuer has the right to call back(i.e. to buy from the holder) the bond, at specified dates,and at specific price.

• A swap can also include the possibility of one party tointerrupt the agreement.

More general, there are derivatives on fixed income instru-ments, the most typical being the bond option, identical toa stock option, with the difference that the underlying is abond

47