may 31, 2017 lithium supply and markets 2017 montreal

TRANSCRIPT

NEW PROCESSES AND THEIR IMPACTS ON LITHIUM MARKETS – Say Hello to POSCO

May 31, 2017Lithium Supply and Markets 2017Montreal, Canada

Jon Hykawy/Tom Chudnovsky

1

• We are a consultancy• Our specialty is the study of opaque commodity markets• Even more specifically, we study the supply, demand and future pricing of critical materials

• We are a registered securities dealer• Not because we chase public deals, we are too small to make that work• Because many of our larger clients eventually ask the question “So what do we do?”• Being a securities dealer makes it easier for us to get paid!

• Today, we are here to give you what we hope you will agree is an unbiased look at lithium• A hot topic, but too much sizzle and not enough steak is never good• We have no junior company to pitch, no deposit to sell• Our work has been conservative, and largely correct, in the past

What is Stormcrow?

2

• Categorize processes• Some processes are “concentrative”, some “extractive”, some both• Important to differentiate, because often a concentrative process without new extraction can be useless

• Old Process (concentrating on brine)• Let’s be clear we understand what we do today, and why• This might make advantages/disadvantages of new processes more apparent

• New processes• Several groups are developing new processes

• Analysis• There are some new processes/entrants that make more sense than others• Money talks…

• Implications• If there is a potential winner, what are the implications for the market?

• Conclusions• What might happen over the next few years

What We Will Do…

3

• Let’s dwell for just a moment on what we are trying to accomplish in the field• We want to produce lithium

• Remember that lithium metal is reactive, we want something a little more stable• Typically, we ship lithium as carbonate (good), metal (bad) and hydroxide (kind of ugly)• Some lithium also shipped as chloride, but not huge volumes, comparatively

• First we “extract”• We bring brine containing lithium chloride in solution to the surface, or;• We dig ore containing a lithium-bearing mineral out of the ground

• Then we “concentrate”• Brine is subjected to solar evaporation or selective adsorption/elution, or;• Minerals are separated and leached to make a concentrated leach liquor

• Then we “extract”• In both cases, we remove impurities and we precipitate lithium by reacting with soda ash

Lithium Extraction and Recovery

4

• In all reasonable cases, we can all probably agree that brine processing is cheaper than hard-rock processing for lithium• So we are going to concentrate on cheap brine processing

• So why the solar evaporation?• Ponds are expensive and impact the environment (but are most importantly expensive)

• Answer is that we need to concentrate to economically extract• A cheap way of removing lithium from brine is to add soda ash; lithium falls out as Li2CO3

• But solubility of Li2CO3 at ambient temperature is 13,300 mg/l, not zero• In metal terms, this is about 2,500 mg/l lithium• Since natural brines are no higher than about 1,000 mg/l, we can’t extract lithium directly using

soda ash, we need to increase the natural grade• We also need to worry about magnesium and calcium, since both have high solubility as chlorides

(546,000 mg/l and 745,000 mg/l, respectively) and low as carbonates (390 mg/l and 6 mg/l, respectively)

The Old Process

5

• So, the old extraction process for brine is simple enough:• Extract by pumping shallow brine to surface• Concentrate lithium using solar evaporation or selective adsorption• Deal with contaminants, especially magnesium and calcium (but also boron, and strontium, etc.)• Precipitate clean lithium carbonate by adding soda ash• Press, dry, bag

• But the evaporation process obviously has drawbacks:• Native lithium grades are too low, concentration is necessary (and expensive)• Contaminants are present and expensive (if too much, then too expensive)• Evaporation takes time (the higher the desired lithium grade, the longer)

The Old Process

6

• Let’s dwell on evaporation for a second• We need 2,501 mg/l just to get anything

at all out of solution using carbonate precipitation, so concentration using a process like evaporation is necessary

• Concentration adds cost• Let’s say we start with 700 mg/l brine• Want to get to only 10,000 mg/l• This is best illustrated as the following (at

100% efficiency)…• We need to evaporate 93% of our water!

Concentration Costs…

7

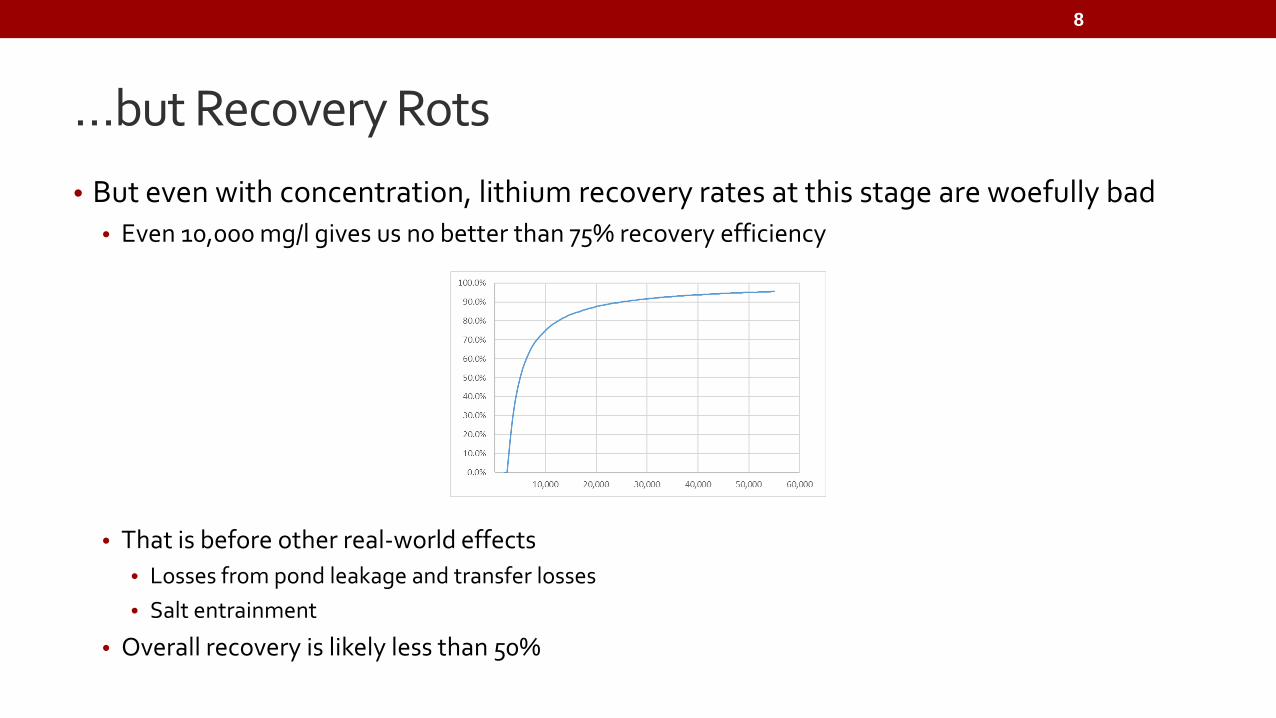

• But even with concentration, lithium recovery rates at this stage are woefully bad• Even 10,000 mg/l gives us no better than 75% recovery efficiency

• That is before other real-world effects• Losses from pond leakage and transfer losses• Salt entrainment

• Overall recovery is likely less than 50%

…but Recovery Rots

8

• New processes aim to overcome these drawbacks• Some are new concentrative technology

• Tenova-Bateman has developed a method to pull concentrated, clean lithium into a process feed for extraction

• Others like Voltaic or MGX Minerals want to process different brines in different ways• Some are examining new ion exchange methods, allowing them to pluck out lithium only

• Some are new extractive technology• While they don’t work with natural lithium brine, Nemaska’s technology processes concentrated

lithium sulfate in solution to lithium hydroxide, Neo Metal does the same with lithium chloride• POSCO has developed and tested a method to extract lithium at lower concentrations and make

clean hydroxide or carbonate

New Processes

9

• At core, Tenova’s LiSX is solvent extraction• Concentrative technology, touted as direct extraction from native brine• Organic chemical mixed with brine, the organic chosen to selectively extract lithium• One pass significantly upgrades lithium in solution, once stripped from organic• Now, we have a much more concentrated and pure lithium solution

• Pros:• Purifies and concentrates (gets rid of contaminants while upgrading lithium)• Compact and fast (no ponds, lithium concentration done in hours not months)

• Cons:• Column can only extract what’s in it, so dilute brine means one column can’t make much

• Conclusion:• Should work, maybe not cost-effective using raw salar brine• Good for hard rock?

Tenova LiSX

10

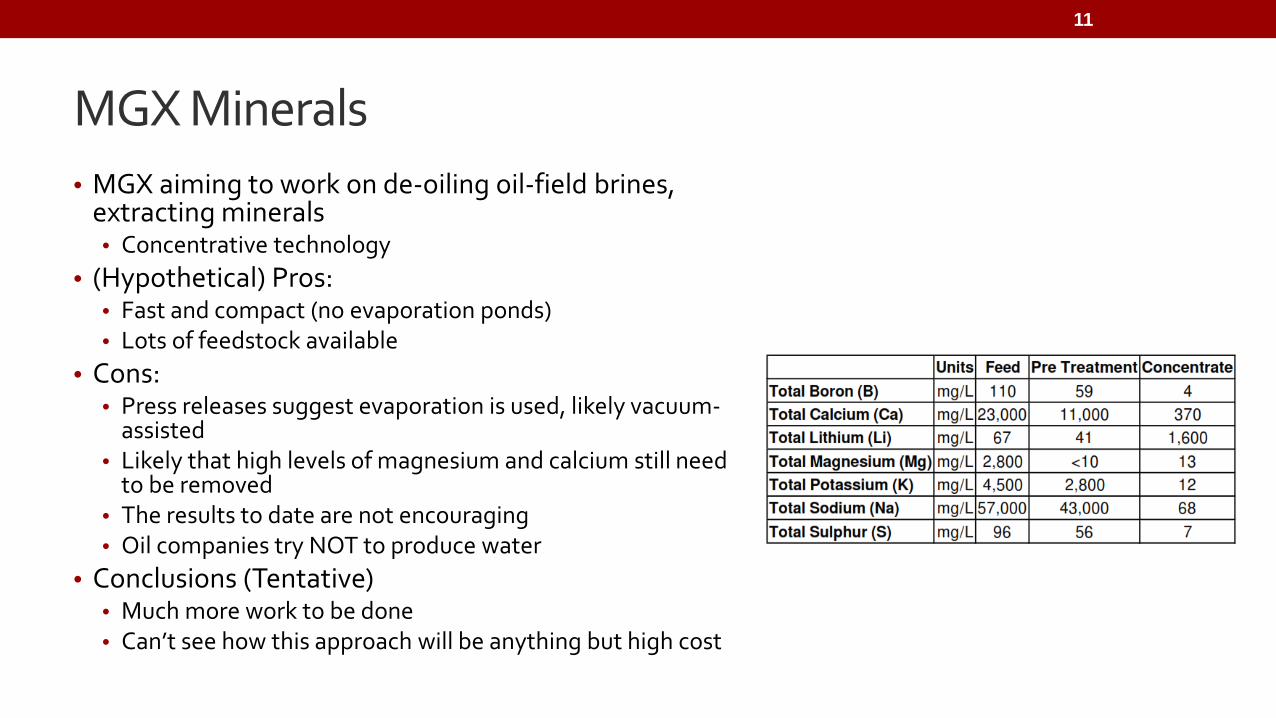

• MGX aiming to work on de-oiling oil-field brines, extracting minerals• Concentrative technology

• (Hypothetical) Pros:• Fast and compact (no evaporation ponds)• Lots of feedstock available

• Cons:• Press releases suggest evaporation is used, likely vacuum-

assisted• Likely that high levels of magnesium and calcium still need

to be removed• The results to date are not encouraging• Oil companies try NOT to produce water

• Conclusions (Tentative)• Much more work to be done• Can’t see how this approach will be anything but high cost

MGX Minerals

11

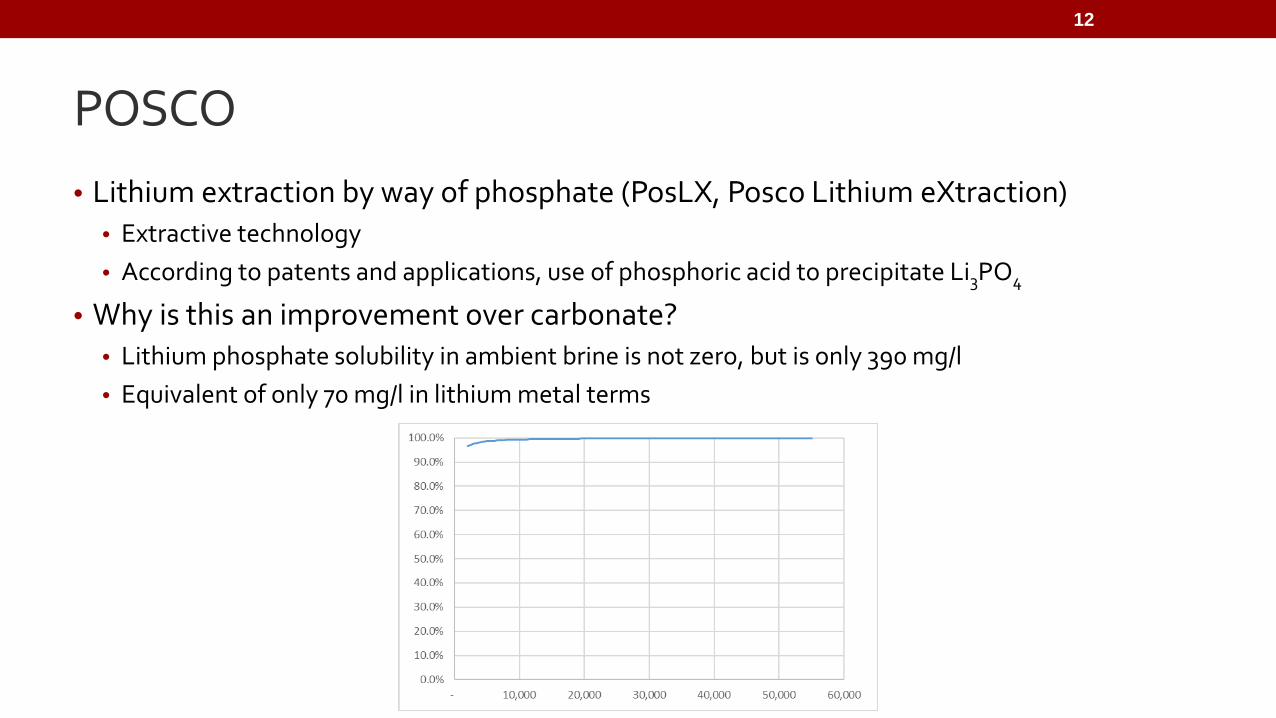

• Lithium extraction by way of phosphate (PosLX, Posco Lithium eXtraction)• Extractive technology• According to patents and applications, use of phosphoric acid to precipitate Li3PO4

• Why is this an improvement over carbonate?• Lithium phosphate solubility in ambient brine is not zero, but is only 390 mg/l• Equivalent of only 70 mg/l in lithium metal terms

POSCO

12

• Pros:• Could use a wide variety of feeds, with far lower lithium grade than carbonate precipitation• Feed brine levels of 2,000-3,000 mg/l lithium are workable• Much smaller ponds, if any, on input side• Can perhaps use alternative brines, maybe even directly

• Cons:• Still need to worry about the same contaminants as with conventional carbonate precipitation

• Conclusions• If this is cost effective, it opens the door to huge new supplies of lithium

• New brine can be used, in locations where solar evaporation is impossible• Existing brines might be harvested more efficiently

POSCO

13

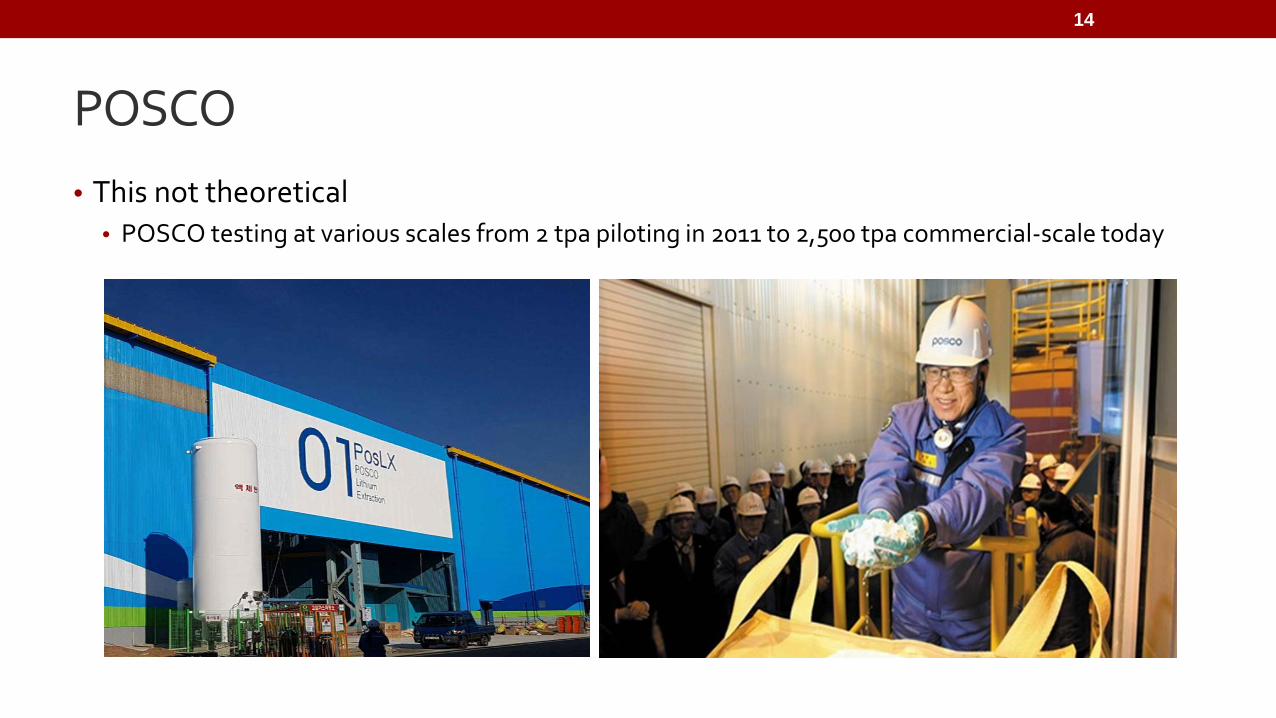

• This not theoretical• POSCO testing at various scales from 2 tpa piloting in 2011 to 2,500 tpa commercial-scale today

POSCO

14

• On costs, we can only speculate, publicly, at this point• Clearly, there are chemical and other processes to convert lithium phosphate to either lithium

carbonate or hydroxide• Ideal situation is to efficiently recover phosphoric acid while doing conversion• If the above can be done, then costs could reach lowest quartile levels• Every project claims this, reality is different

• There are two very important considerations here• Scale: We assume POSCO is not interested in lithium just to make 10,000 tpa…• Resources: POSCO has resources to execute (2016 revenues of USD$54 billion, 20x Albemarle)

• We believe PosLX represents the biggest change in this market in 30 years• Think about what happens to production if current producers were to double their lithium

recoveries, without pumping any additional brine, by applying PosLX

POSCO

15

• End-use data gives the following

Historical Lithium Consumption

16

Source: Roskill, Stormcrow

YearTotal Consumption (t

LCE)Battery Consumption

(t LCE)Other (t LCE)

2008 120,968 20,026 100,942 2009 101,613 24,346 77,267 2010 125,726 29,058 96,668 2011 138,306 32,984 105,322 2012 151,048 39,463 111,585 2013 165,484 50,262 115,222 2014 182,903 64,398 118,505 2015 194,000 65,108 128,892 2016 212,719 77,821 134,897

• Available historical spot pricing for common lithium chemicals: is shown below• Yes, a lot of lithium chemicals are sold by contract• Some would argue that spot prices don’t matter, but, at minimum, they show us the direction of

the market

Historical Lithium Pricing Data

17

Source: Asian Metal

Year Tech Li2CO3Batt

Li2CO3Tech LiOH

2008 5.37$ -$ -$ 2009 4.10$ -$ -$ 2010 3.97$ -$ -$ 2011 3.91$ 4.51$ -$ 2012 4.80$ 5.05$ 6.48$ 2013 4.84$ 5.29$ 6.99$ 2014 4.46$ 5.06$ 6.54$ 2015 7.64$ 9.14$ 8.02$ 2016 18.83$ 22.17$ 23.37$

• The following is projected latent demand through 2025

• Batteries play an increasingly important role• With respect to batteries, we are going to use a

modified version of Avicenne’s base scenario, without the “Chinese battery explosion” and without grid storage

• Don’t forget ceramics and ceramic-glass, these maintain reasonable growth due to increases in consumer discretionary spending

Projected Lithium Demand

18

Source: Stormcrow (2017)

2017 2021 2025Rechargeable Batteries 93,294 153,303 212,820 Ceramics 30,367 39,657 51,788 Glass-Ceramics 26,029 33,992 44,390 Greases 14,970 16,849 18,964 Glass 16,841 18,955 21,334 Metallurgical Powders 13,015 16,996 22,195 Polymer 9,539 10,947 12,624 Air Treatment 9,539 10,947 12,624 Non-rechargeable Batteries 3,670 4,051 4,450 Aluminum 680 279 91 Other 16,841 18,955 21,334 Total 234,788 324,930 422,614

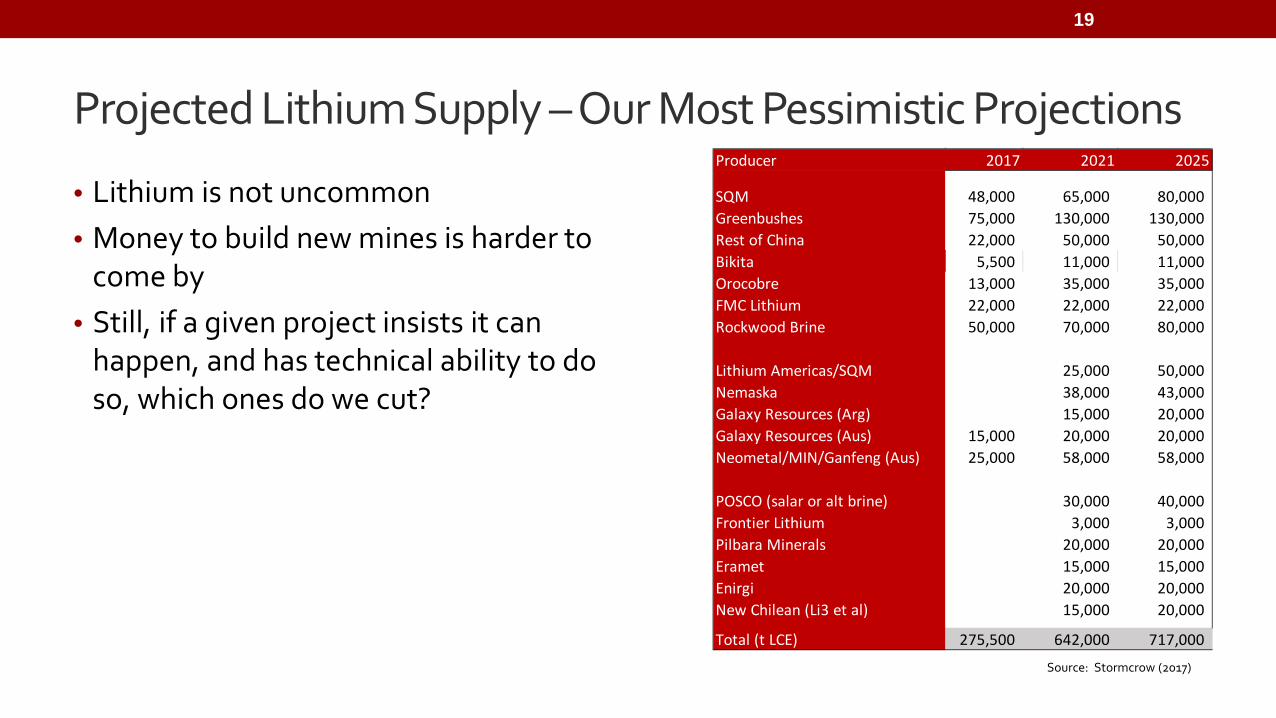

• Lithium is not uncommon• Money to build new mines is harder to

come by• Still, if a given project insists it can

happen, and has technical ability to do so, which ones do we cut?

Projected Lithium Supply – Our Most Pessimistic Projections

19

Source: Stormcrow (2017)

Producer 2017 2021 2025

SQM 48,000 65,000 80,000 Greenbushes 75,000 130,000 130,000 Rest of China 22,000 50,000 50,000 Bikita 5,500 11,000 11,000 Orocobre 13,000 35,000 35,000 FMC Lithium 22,000 22,000 22,000 Rockwood Brine 50,000 70,000 80,000

Lithium Americas/SQM 25,000 50,000 Nemaska 38,000 43,000 Galaxy Resources (Arg) 15,000 20,000 Galaxy Resources (Aus) 15,000 20,000 20,000 Neometal/MIN/Ganfeng (Aus) 25,000 58,000 58,000

POSCO (salar or alt brine) 30,000 40,000 Frontier Lithium 3,000 3,000 Pilbara Minerals 20,000 20,000 Eramet 15,000 15,000 Enirgi 20,000 20,000 New Chilean (Li3 et al) 15,000 20,000

Total (t LCE) 275,500 642,000 717,000

Pricing Rationale via Fundamental Scarcity

20

Factor of 15x!

• We develop a model, based on historical pricing

• There are some obvious issues with this approach…• First, the models are necessarily extrapolating, which is risky

• But we don’t have a choice, we’ve never seen these projected levels of demand or supply before• Second, these models are mathematical

• Others might say that, having worked in the space, they “know” or “feel” what the market is doing• Very likely nonsense; we saw industry experts get whip-sawed by the rare earths crisis in 2011, and by the

uranium price run in 2007• Again, we have never seen these levels of demand from these particular markets before, so precognitively

“knowing” what this suggests is impossible

• Our models are multivariate, generally incorporating a relevant demand level and a supply/demand gap

Projecting Prices

21

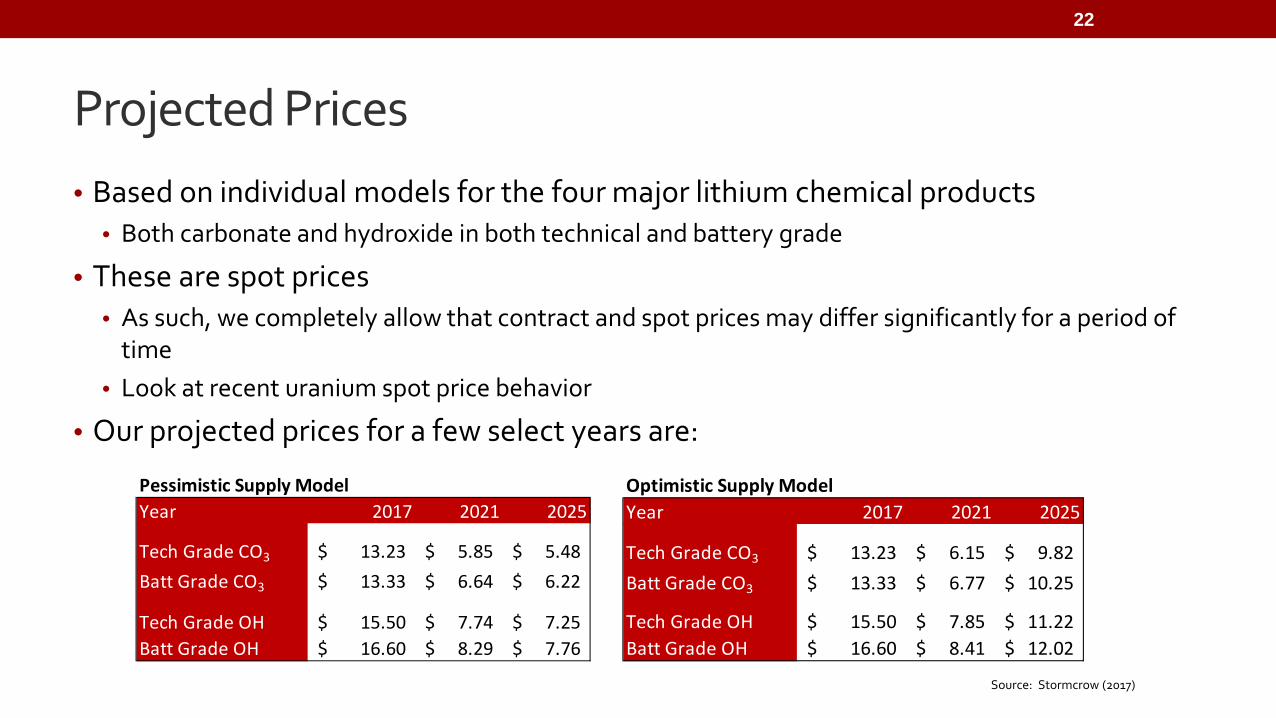

• Based on individual models for the four major lithium chemical products• Both carbonate and hydroxide in both technical and battery grade

• These are spot prices• As such, we completely allow that contract and spot prices may differ significantly for a period of

time• Look at recent uranium spot price behavior

• Our projected prices for a few select years are:

Projected Prices

22

Pessimistic Supply ModelYear 2017 2021 2025

Tech Grade CO3 13.23$ 5.85$ 5.48$ Batt Grade CO3 13.33$ 6.64$ 6.22$

Tech Grade OH 15.50$ 7.74$ 7.25$ Batt Grade OH 16.60$ 8.29$ 7.76$

Optimistic Supply ModelYear 2017 2021 2025

Tech Grade CO3 13.23$ 6.15$ 9.82$ Batt Grade CO3 13.33$ 6.77$ 10.25$

Tech Grade OH 15.50$ 7.85$ 11.22$ Batt Grade OH 16.60$ 8.41$ 12.02$

Source: Stormcrow (2017)

• Our projections developed assuming conventional sources and processing• If we assume new methods and unconventional sources, then our model pushes toward oversupply

and the pessimistic end of pricing• That would mean battery-grade carbonate pricing of more than US$6,000 per tonne, battery-

grade hydroxide pricing of more than US$7,500 per tonne• This is not anything like current levels, but not bad, especially if cost of production is relatively low

• Our conclusions regarding new processing technology are fairly simple• Much of the new technology is most useful for hard-rock sources, will remain high cost• POSCO’s PosLX is different, it can be targeted at unconventional brine, and may well be low cost• While oversupply in our models is dependent on capital market largesse, POSCO’s entry into the

space is not

• We believe the advent of new technology likely pushes prices back toward historical levels, so new technology has to bring low opex

Conclusions

23

Stormcrow

Jon Hykawy, PhD, MBAjon(at)stormcrow.caPresident647-407-6289

Tom Chudnovskytom(at)stormcrow.caManaging Partner416-558-8544

24