p-cards done right - iofm · p2p process card p2p process difference average process costs $90.0...

TRANSCRIPT

P-Cards Done Right Katie Beatty

Community Engagement Manager

About the NAPCP

• We are an association committed to

advancing YOU and other Commercial Card and Payment professionals worldwide by

providing continuing educational and peer networking through our conferences, regional forums, webinars, newsletters and

community engagement.

About the NAPCP

Established in February 2000

Work with 15,000+ members & subscribers Over 2,000+ pages of industry updates, whitepapers, best practices and much

more on our Resource Center

The Next Hour

• Introduction to Commercial Cards

• The Value Proposition

• Developing a Program Model

• Program Implementation

• Policies and Procedures

• Controls

• Communications and Training

The Next Hour

• Partnering with Suppliers

• Ongoing Management

• Common Pitfalls

• Questions & Discussion

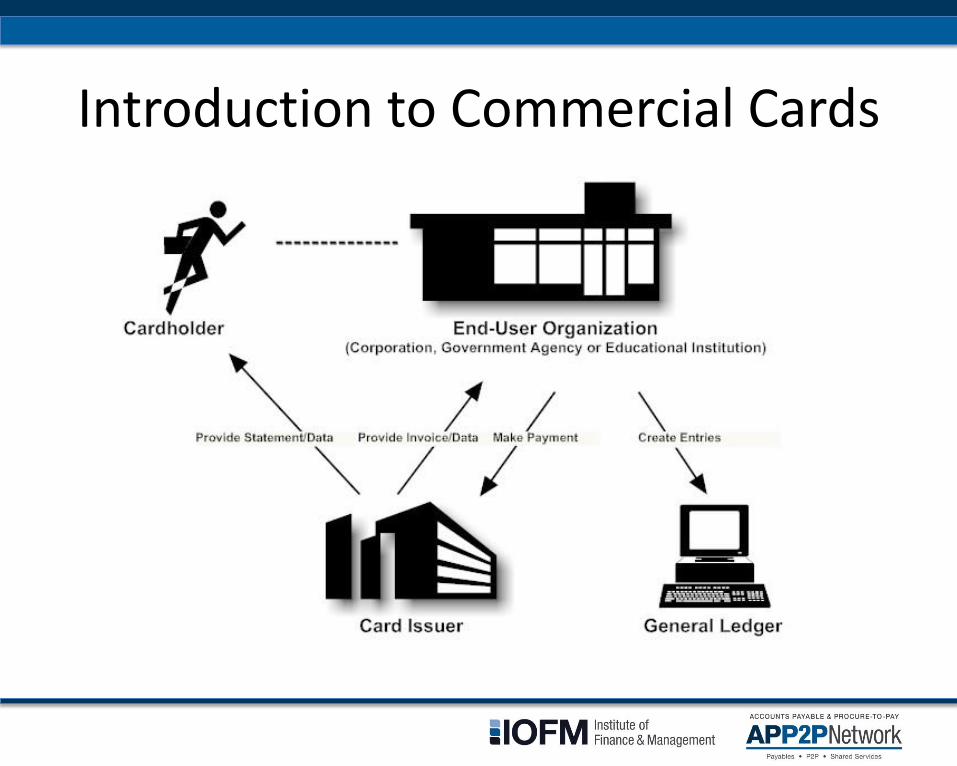

Introduction to Commercial Cards

• What is a P-Card? – T&E, Corporate, ePayables, Event Card, Lodge Card, Prepay,

Declining, etc.

• Who is Involved? – P-Card Program Manager (PM) – Cardholders – Suppliers – Issuers – Merchant Acquirers – Networks – Processors

• What is Level III Data? – Why are we ALWAYS talking about it?

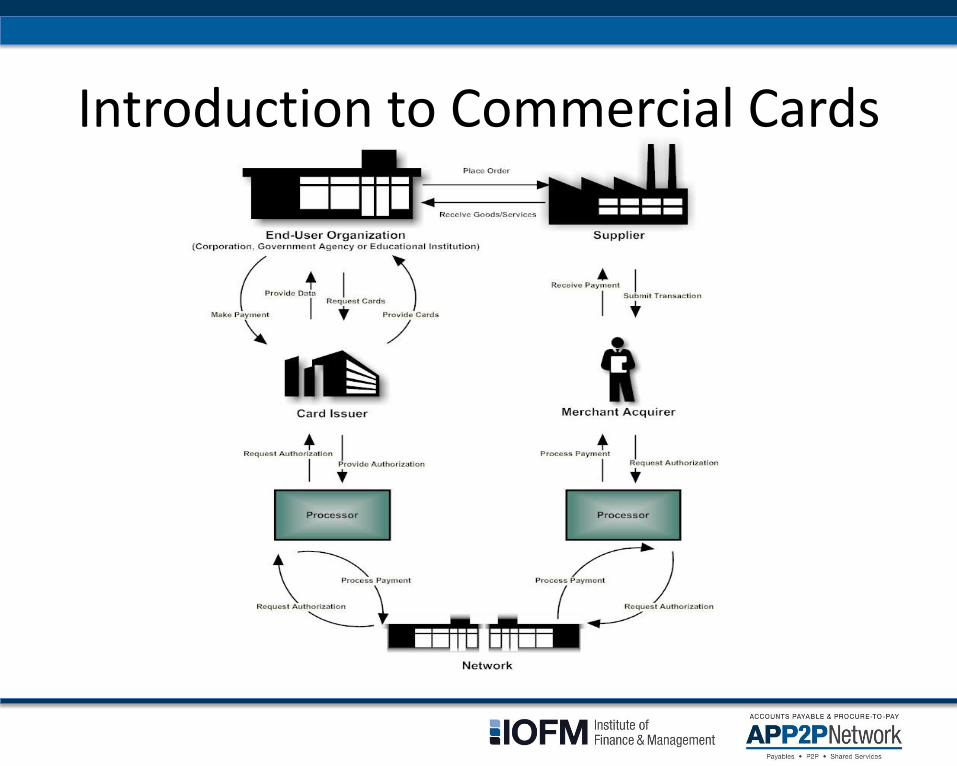

Introduction to Commercial Cards

Introduction to Commercial Cards

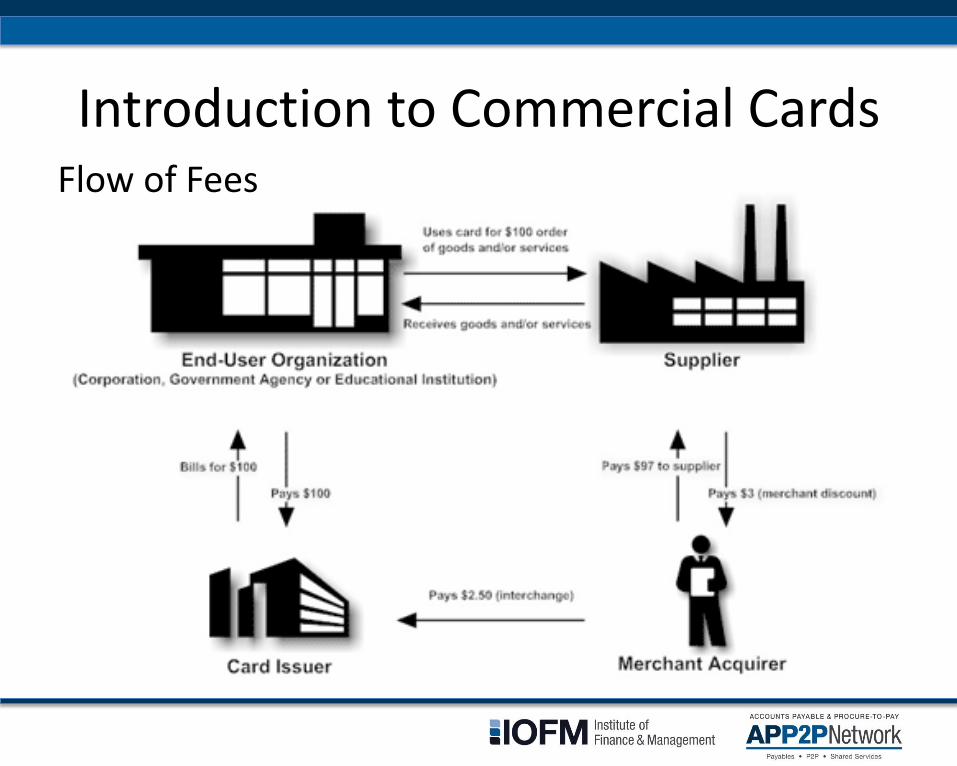

Introduction to Commercial Cards Flow of Fees

The Value Proposition

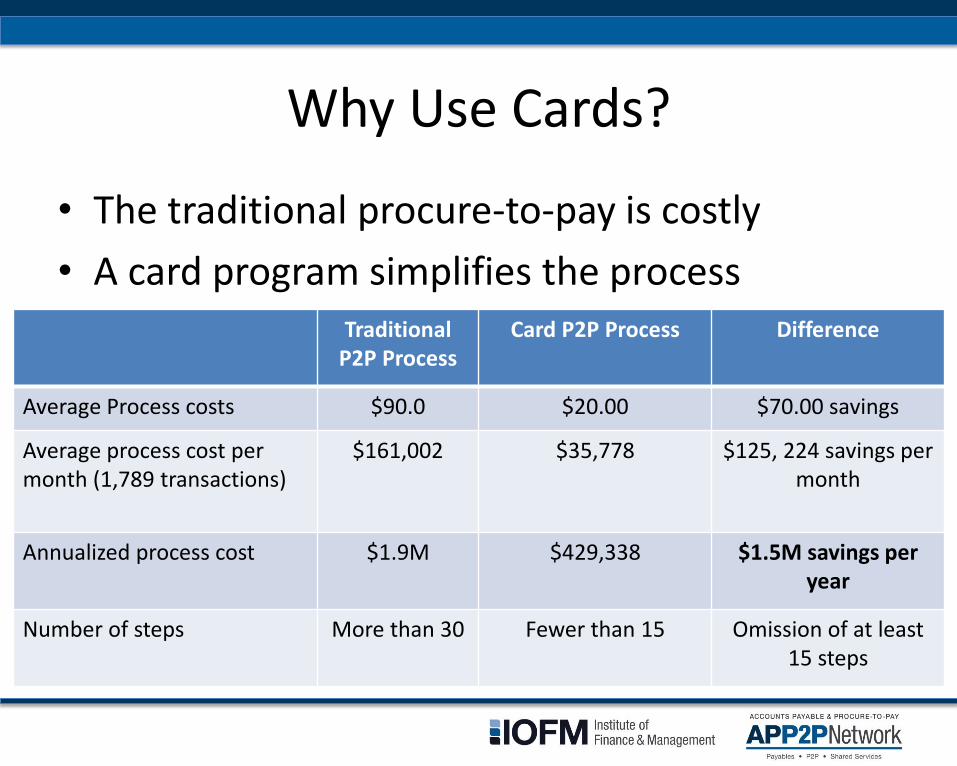

Why Use Cards?

• The traditional procure-to-pay is costly

• A card program simplifies the process

Traditional P2P Process

Card P2P Process Difference

Average Process costs $90.0 $20.00 $70.00 savings

Average process cost per month (1,789 transactions)

$161,002 $35,778 $125, 224 savings per month

Annualized process cost $1.9M $429,338 $1.5M savings per year

Number of steps More than 30 Fewer than 15 Omission of at least 15 steps

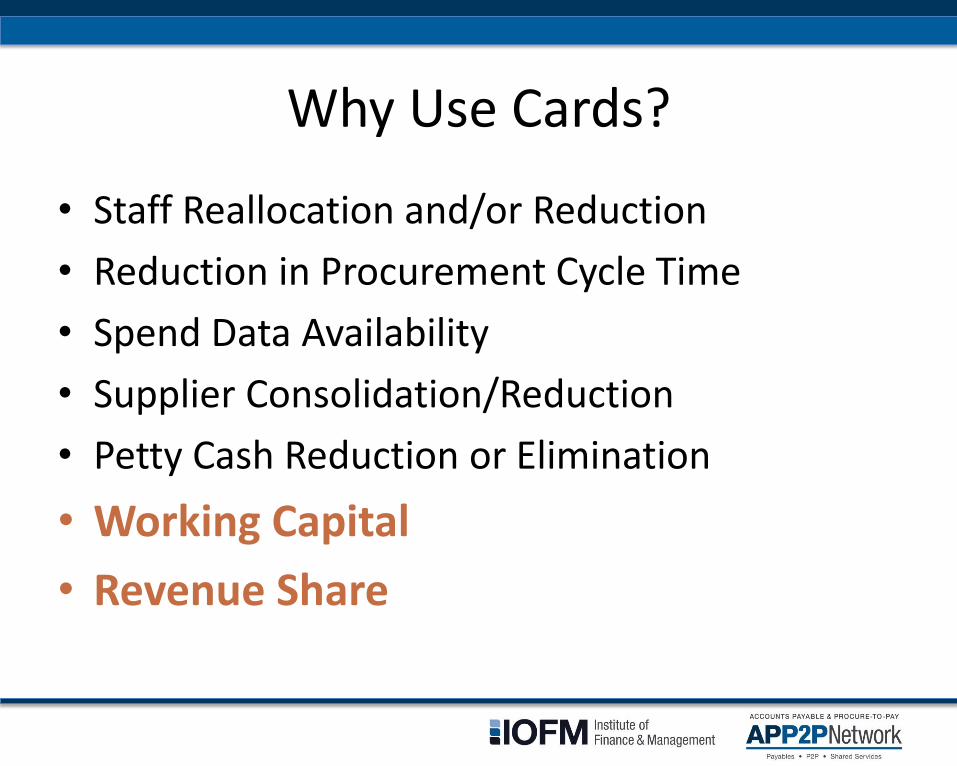

Why Use Cards?

• Staff Reallocation and/or Reduction

• Reduction in Procurement Cycle Time

• Spend Data Availability

• Supplier Consolidation/Reduction

• Petty Cash Reduction or Elimination

• Working Capital

• Revenue Share

Developing a Program Model

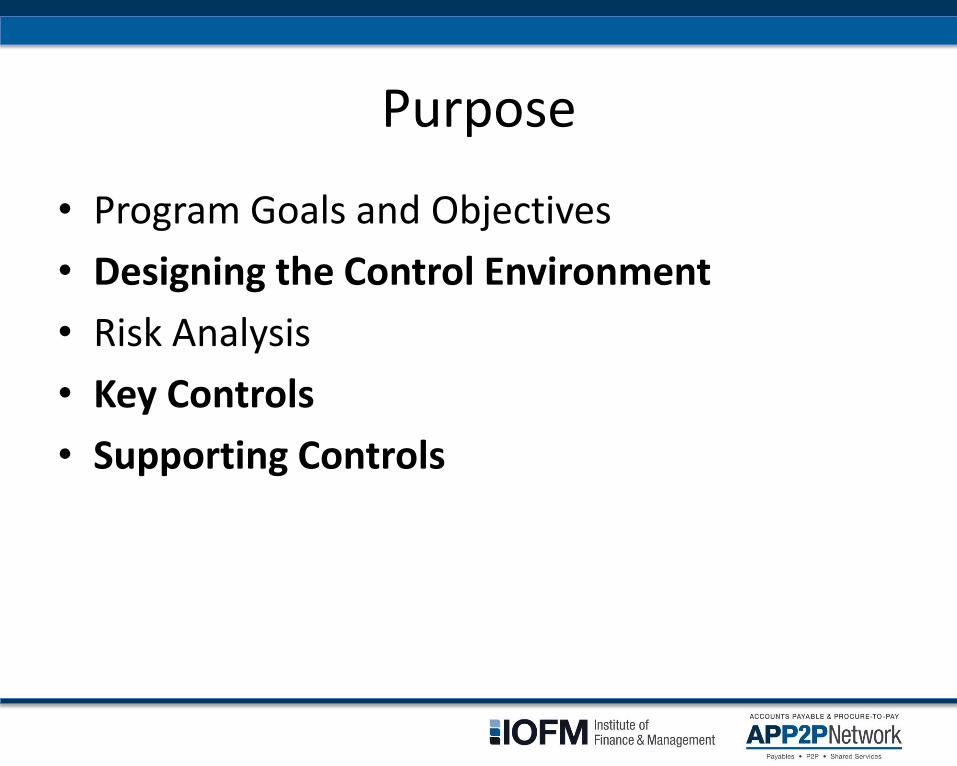

Purpose

• Program Goals and Objectives

• Designing the Control Environment

• Risk Analysis

• Key Controls

• Supporting Controls

Program Implementation

Implementation

• Roles & Responsibilities

• Technology & Reporting

• Account Set-up

• Infrastructure

• Communications

The Pilot

• Key Success Factors

• Preparing Suppliers

• Planning for Issue Resolution

• The Pilot Period

• Monitoring and Evaluating the Pilot

• Conducting Satisfaction Surveys

• Make modifications to model as necessary

• Plan rollout

• Identify goals by business unit

• Communicate organization-wide

• Set up accounts and train participants

Full Program Rollout

Policies & Procedures

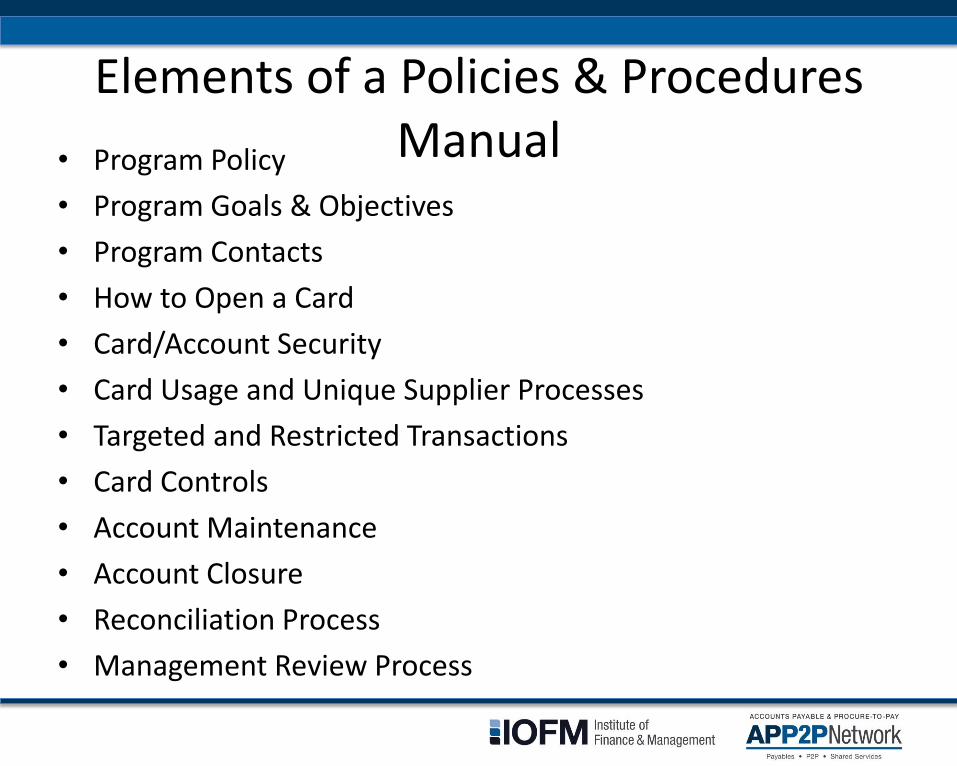

Elements of a Policies & Procedures Manual • Program Policy

• Program Goals & Objectives

• Program Contacts

• How to Open a Card

• Card/Account Security

• Card Usage and Unique Supplier Processes

• Targeted and Restricted Transactions

• Card Controls

• Account Maintenance

• Account Closure

• Reconciliation Process

• Management Review Process

Controls

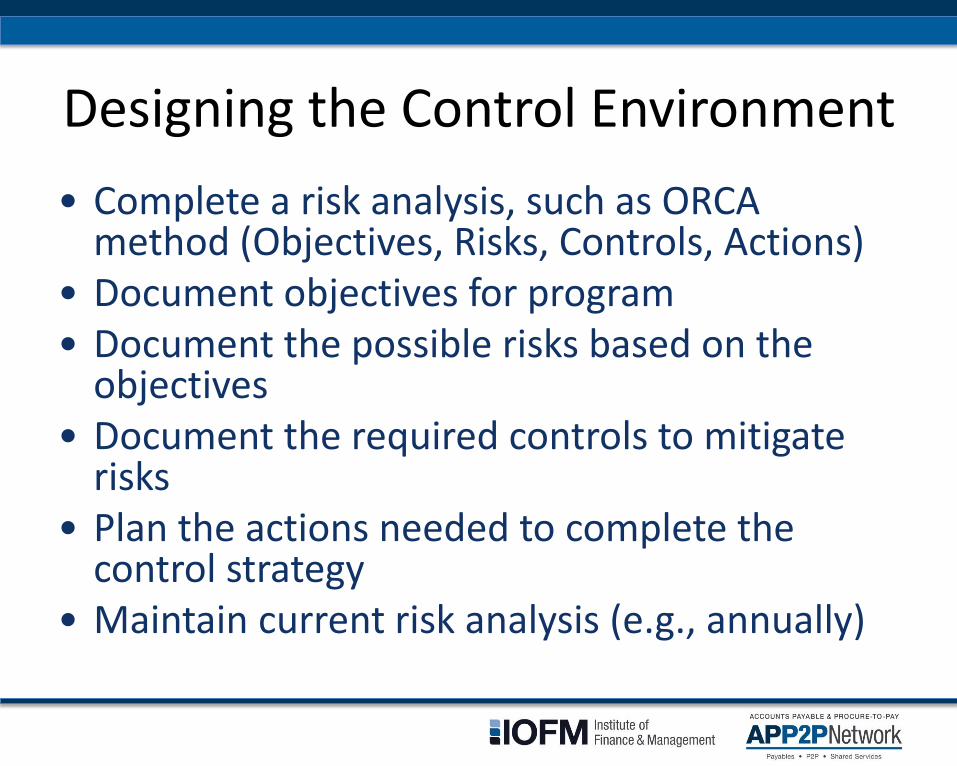

Designing the Control Environment

• Complete a risk analysis, such as ORCA method (Objectives, Risks, Controls, Actions)

• Document objectives for program • Document the possible risks based on the

objectives • Document the required controls to mitigate

risks • Plan the actions needed to complete the

control strategy • Maintain current risk analysis (e.g., annually)

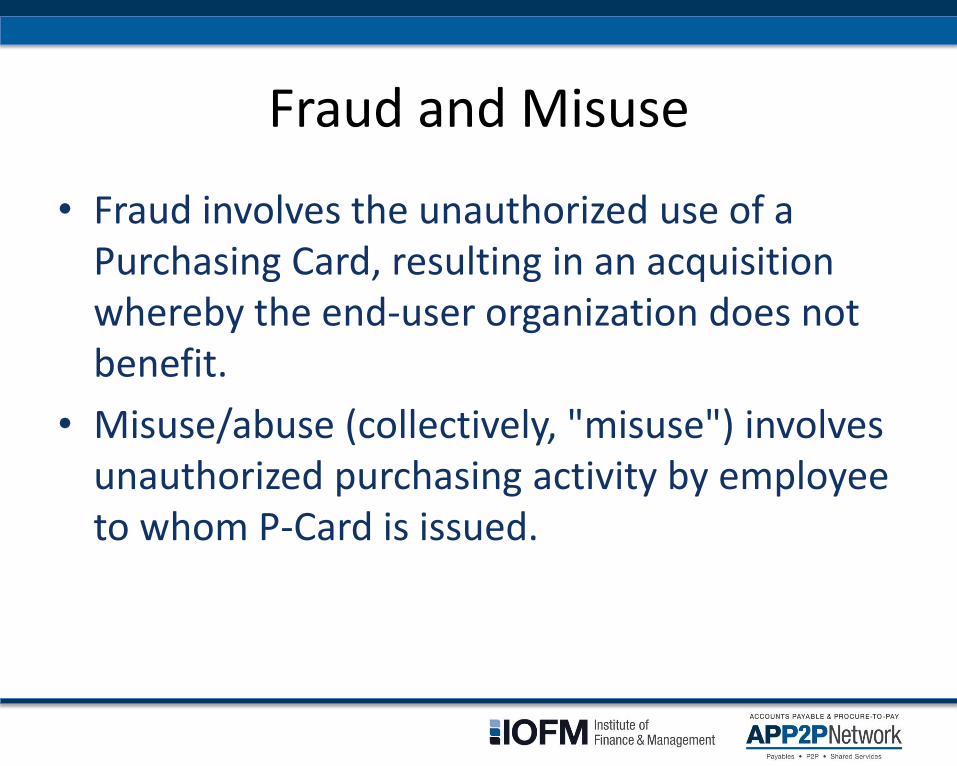

Fraud and Misuse

• Fraud involves the unauthorized use of a Purchasing Card, resulting in an acquisition whereby the end-user organization does not benefit.

• Misuse/abuse (collectively, "misuse") involves unauthorized purchasing activity by employee to whom P-Card is issued.

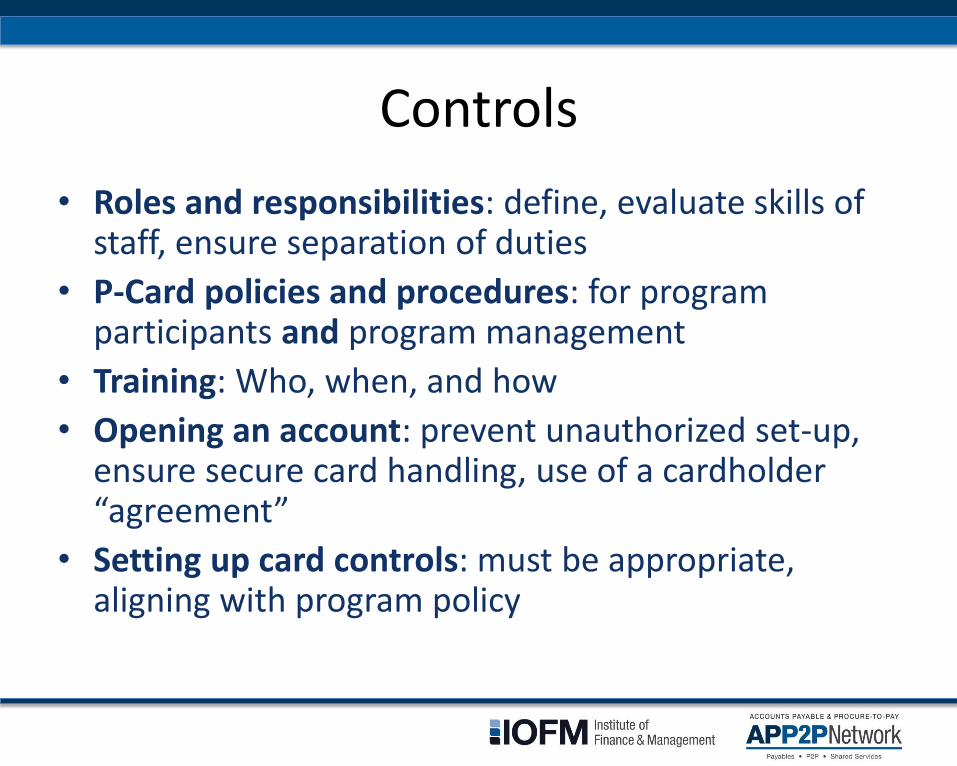

Controls

• Roles and responsibilities: define, evaluate skills of staff, ensure separation of duties

• P-Card policies and procedures: for program participants and program management

• Training: Who, when, and how

• Opening an account: prevent unauthorized set-up, ensure secure card handling, use of a cardholder “agreement”

• Setting up card controls: must be appropriate, aligning with program policy

Controls

• Single purchase/transaction dollar limit

• Daily transaction limit

• Daily dollar limit

• Monthly/cycle limit

• Merchant Category Code (MCC) restrictions – MCCs are four-digit codes, maintained by the networks and assigned to card-accepting suppliers, used to identify a supplier’s principal trade, profession or line of business.

• Automated Teller Machine (ATM) blocking

Controls

• Changing account limits/restrictions: who can make changes, approval process, documentation, monitoring

• Closing an account: notification, card collection and disposal, handling posted transactions after account is closed

• P-Card accounting process: determine appropriate entries, accuracy of process, how entries are tracked

Controls

• Transaction documentation: requirements and records retention

• Review, approval, and audit: the process, who is involved, frequency

• Preventing duplicate payments

• Program reporting: types of reports, who generates and reviews, retention

• Auditing: who, what, when and how

• Program technology: access levels/roles and data security

Controls

• Role of the card issuer in fraud detection: detection methods, how they communicate fraud, etc.

• Lost/stolen cards: communication chain, process, financial impact

• Liability waiver insurance: type of liability, contract provisions, considerations

Communication & Training

Know Your Audience

The audience/recipients of communications will vary:

• All levels of management • Departments/business units • Site coordinators, if applicable • Cardholders • Approving officials • Functional areas, such as A/P and

procurement • Suppliers

Initial Strategy

• Introduce the P-Card program

• Explain P-Card’s benefits

• Describe how processes will change

• Promote P-Card use in accordance with policies and procedures

• Use a variety of methods, making educational resources and learning opportunities readily available; for example:

– open house

– meetings with business units/departments

Ongoing Strategy

• Use a variety of methods, making educational resources and learning opportunities readily available; for example:

– Intranet to post program P&P, benefits, key metrics (e.g., process savings)

• Keep management appraised of program status

• Consider steering committee or similar

Developing a Training Program

• Who will create and deliver the training? Who will review regularly and revise as needed?

• Who needs to be trained?

• What does each audience need to learn?

• When will training occur?

• Will training be mandated for one or more groups?

• What training methods are possible?

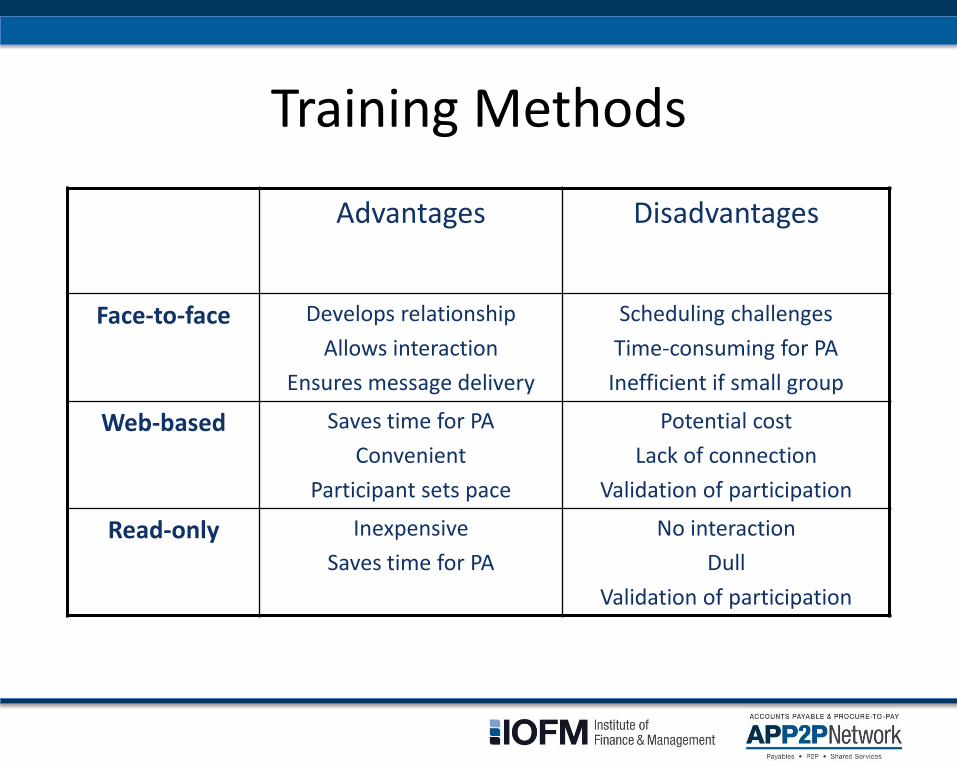

Training Methods

Advantages Disadvantages

Face-to-face Develops relationship

Allows interaction

Ensures message delivery

Scheduling challenges

Time-consuming for PA

Inefficient if small group

Web-based Saves time for PA

Convenient

Participant sets pace

Potential cost

Lack of connection

Validation of participation

Read-only Inexpensive

Saves time for PA

No interaction

Dull

Validation of participation

Evaluating Training Success

• Testing training recipients’ knowledge

– After training program completion

– Could mandate a certain passing score before card issuance

– Could have recurring tests (“refresher training”)

• Surveying recipients, questioning the training:

– Effectiveness

– Appeal

– Convenience

Partnering with Suppliers

• Work with your issuer or third-party organization

• Be familiar with: – acquiring process

– economics for P-Card acceptance

– Payment Card Industry Data Security Standards (PCI DSS)

• Identify suppliers

• Partner with key suppliers to make P-Card acceptance a win-win situation

• Help educate suppliers

• Suppliers should not simply add P-Card on top of current processes; re-engineering is important

Building a Supplier Program

• Merchant agreements vary, depending on supplier/acquirer relationship

• Information gathered during process: tax identification number (TIN), merchant category code (MCC), incorporation status and socio-economic data

• Determination of the level of transaction data that a supplier will provide

• Suppliers agree to follow “merchant rules” related to card acceptance

Acquiring Process

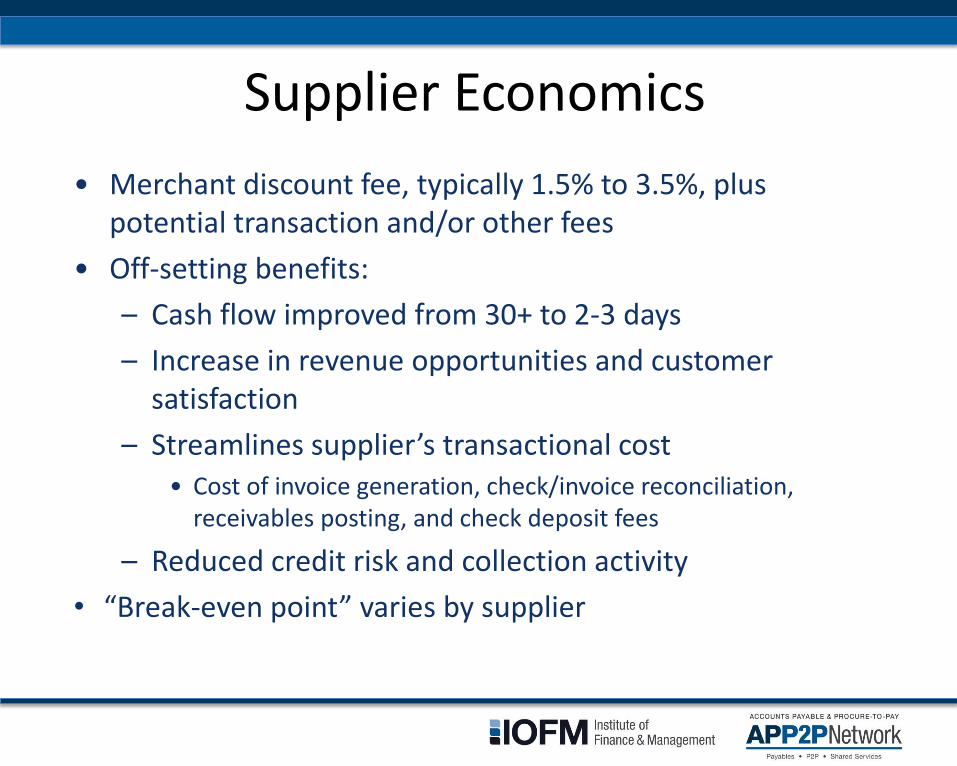

• Merchant discount fee, typically 1.5% to 3.5%, plus potential transaction and/or other fees

• Off-setting benefits:

– Cash flow improved from 30+ to 2-3 days

– Increase in revenue opportunities and customer satisfaction

– Streamlines supplier’s transactional cost • Cost of invoice generation, check/invoice reconciliation,

receivables posting, and check deposit fees

– Reduced credit risk and collection activity

• “Break-even point” varies by supplier

Supplier Economics

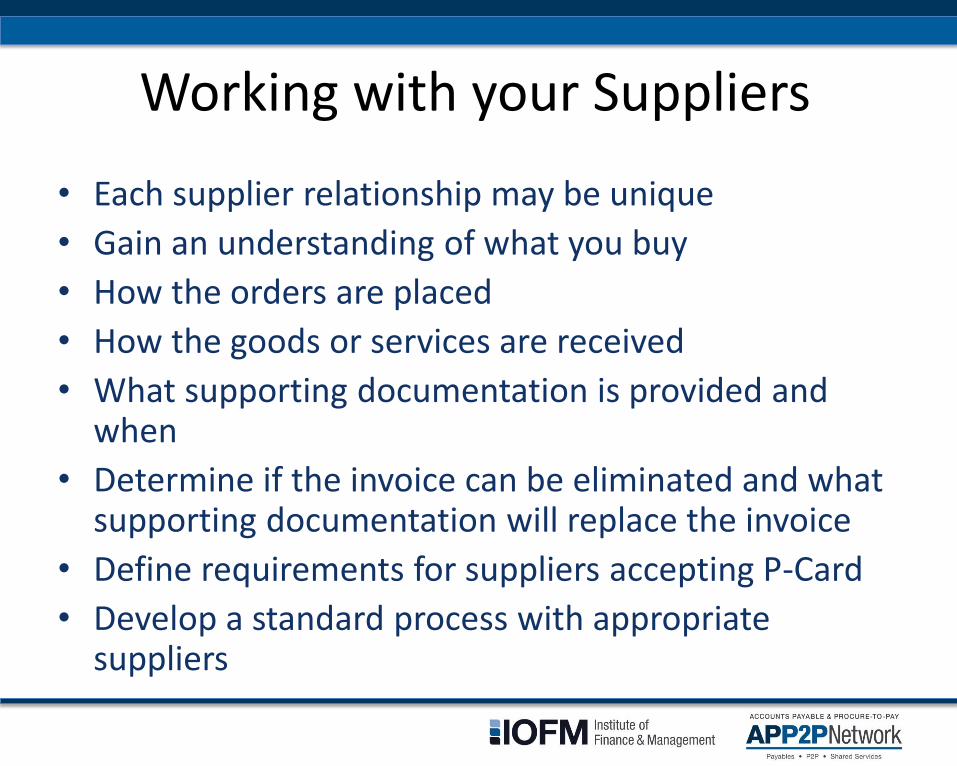

• Each supplier relationship may be unique

• Gain an understanding of what you buy

• How the orders are placed

• How the goods or services are received

• What supporting documentation is provided and when

• Determine if the invoice can be eliminated and what supporting documentation will replace the invoice

• Define requirements for suppliers accepting P-Card

• Develop a standard process with appropriate suppliers

Working with your Suppliers

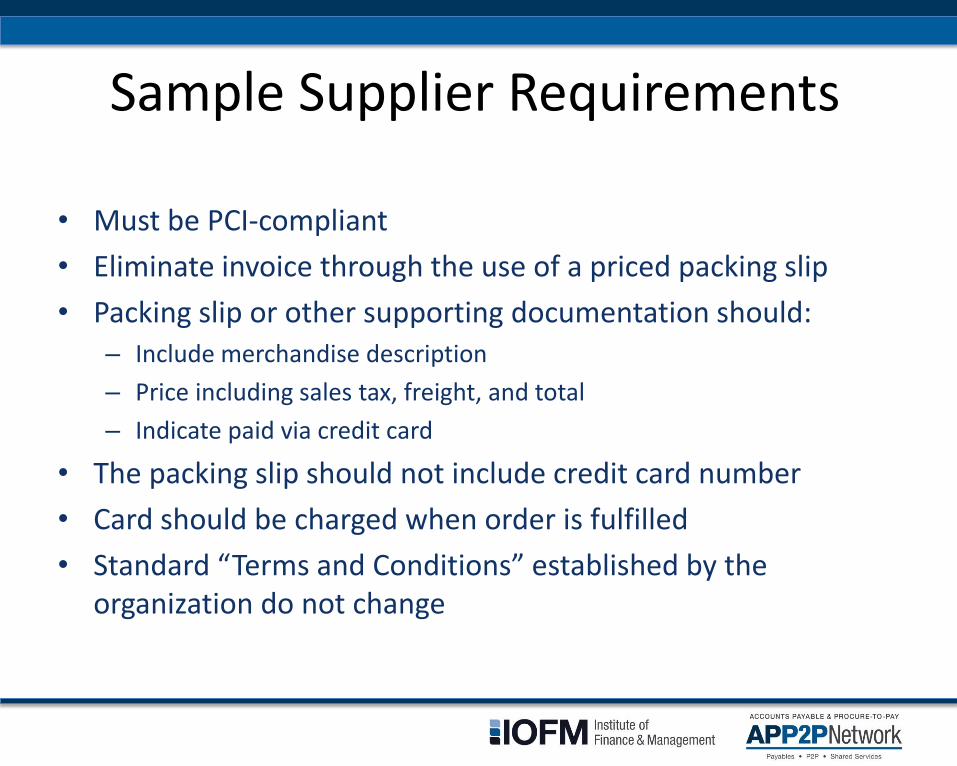

• Must be PCI-compliant

• Eliminate invoice through the use of a priced packing slip

• Packing slip or other supporting documentation should: – Include merchandise description

– Price including sales tax, freight, and total

– Indicate paid via credit card

• The packing slip should not include credit card number

• Card should be charged when order is fulfilled

• Standard “Terms and Conditions” established by the organization do not change

Sample Supplier Requirements

Ongoing Management

• Don’t “implement and forget”

• Status quo versus continuous improvement

• Review program regularly to find opportunities for improvements and growth

• Adjust goals as desired

• Keep policies and procedures current

• Make program changes as necessary or desired to meet goals

• Update training program to meet needs

• Revise user and administrator manuals as needed

Program Management

Various kinds of reports are useful for program management, fraud detection, spend analysis, etc. Report examples include:

• Monthly spend and transaction count by card

• Declined transactions

• New accounts and closed accounts

• Account limits and “available limit” by card

• Disputes

• Spend by supplier

• Reports related to sales tax

Reporting

• May be performed by a variety of individuals, each with a specific focus

• Process audits versus transaction audits

• Proper planning yields best results

• May be aided by technology tools

• Frequency may vary depending on what is being audited

Auditing

• High-dollar transactions

• Transactions with certain suppliers and/or MCCs

• Certain expense types

• High volume/activity P-Card users

• New cardholders

• Transactions occurring during non-business hours

Auditing

• What: Quantified, relative statistics used to rate program performance

• Why: Quantifying the P-Card opportunity using your own organization’s statistics is the essence of a compelling business case – A solid business case is essential to senior

management support – Metrics are essential to growth

• When: Use on a routine basis to communicate the progress and the value that the program actually delivers

Metrics Overview

• Cost savings and efficiencies

– Have P-Cards resulted in a reduction of staff? Or have employees been redirected to value-added activities?

– Can a process savings be calculated?

• Compare steps and associated cost of old/traditional process to P-Card process

• Analyze who does each step, how long each step takes, and the cost of each step

• Arrive at the cost per transaction for each process

Key Performance Indicators

• Another way to quantify savings per transaction is to compare the number of transactions processed per full-time equivalent (FTE) for A/P and P-Card

– For A/P productivity, divide the total number of transactions processed in A/P by the number of FTEs in A/P to give you the number of transactions per FTE

– For P-Card productivity, divide the total number of P-Card transactions by the number of P-Card FTEs

• Assign a dollar value to the FTE to get cost per transaction

KPI’s

• Card penetration:

– What percentage of employees are cardholders? Are any cards inactive (i.e., not used)?

• P-Card ratio:

– What percentage of payments are captured via P-Card? What is the number and percent of invoices eliminated in A/P?

• Monthly stats:

– What is the average number of transactions per card? What is the spend per card? Spend per transaction?

KPI’s

• Compliance – Instances of inappropriate use – Declined transactions – Timely submission of paperwork – Correct paperwork submitted – Correct tax modifications

• Program acceptance

– Rate of payment requests received in A/P that could be paid via P-Card

– Survey cardholders and management to gauge satisfaction with program

Other Important Metrics

• Ensure soundness of current program before pursuing extensive growth

• After resolving any issues with current program, prepare for expansion

• Process similar to program implementation—gain support, use project management, communicate throughout organization, etc.

• Present ideas to management, stakeholders, others and make final decisions

Growing a Program

• Evaluate the expansion possibilities to determine what will work best for your organization

– Which of the expansion ideas will your organization pursue?

– Which expansion methods offer the most reward with the least effort?

– Which methods will require more resources and may need to be pursued another time?

– Before discarding an idea, ask “Why not?” Is the decision based on logic?

Growing a Program

• Increase card penetration, if warranted

• Global expansion, if applicable

• Convert more suppliers to card payment

– Review A/P spend data for opportunities

– Target key suppliers

– Partnership between procurement and accounts payable is beneficial

Growth Opportunities

• Increase types of purchases

– inventory purchases

– capital equipment

– eProcurement purchases

– services, such as temp labor, consultants, meeting expenses, printing, catering, etc.

– travel

• Utilize card variations (complementary solutions to traditional P-Cards and Ghost Accounts)

Growth Opportunities

Keys to Success

• Administrator not suited for position

• Lack of infrastructure to support the process, including management support

• Ineffective training

• Unclear policies and procedures

• Lack of communication to suppliers

• Over- or under-controlling the program

• Too many manual processes

• Too many inactive accounts

Common Pitfalls

• Senior management support

• Re-engineer current processes

• Recognize many of the changes required are behavioral

• Commission a dedicated resource to manage and promote the program

• Establish a cross-functional team with members from Accounting, Internal Audit, Tax, Treasury and Purchasing

Keys to Success

• Clearly define program goals

• Establish a clearly defined process and appropriate procedures; don’t make P-Card difficult to use

• Automate as many processes as possible

• Effective and on-going communication throughout various levels of the organization

• Use of reporting tools and metrics

Keys to Success

• Establish Commercial Cards are the standard means of conducting business with key suppliers

• Seek ongoing support from your card provider to overcome supplier resistance

• Conduct regular spend analysis to identify additional categories to target for cards

• Integrate Commercial Card systems with other transaction systems (e.g., procurement, accounts payable, and finance—G/L)

Action Items