permian crude takeaway & pricing - the energy forum · g~ 450 mb/d processed in permian...

TRANSCRIPT

©2017 Morningstar, Inc. All rights reserved.

Sandy Fielden

Director of Research, Commodities and Energy

November 9, 2017 – New York Energy Forum

Permian Crude Takeaway & Pricing

Agenda

2

gOil Shale Boom & Plumbing

gPermian Takeaway

gChanging Gulf Coast Balance 2010 - 2017

gExport Infrastructure

gPrices and the Permian Spigot

3

U.S Crude Production Since 1970

Oil Shale Boom & Plumbing

Source: EIA, Morningstar

0

2

4

6

8

10

12

Mm

b/d

October 1970 –

10 mmb/d

April 2015 –

9.6 mmb/d

Shale

Boom

August 2017 –

9.2 mmb/d

4

0

1

2

3

4

5

6

Jan-

11

Jun-

11

Nov

-11

Apr

-12

Sep-

12

Feb-

13

Jul-1

3

Dec

-13

May

-14

Oct

-14

Mar

-15

Aug

-15

Jan-

16

Jun-

16

Nov

-16

Apr

-17

mm

b/d

Eagle Ford

Bakken

Permian

Three Plays That Shook the World

Source: EIA

gPermian 100 years old - up 1.5 mmb/d since 2011

gBakken up 0.7 mmb/d since 2011

gEagle Ford up 1.1 mmb/d since 2011

5

0

1

2

3

4

5

6

7

8

9

10

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

Mm

b/d 50 + API

40.1 - 50 API

30.1 - 40 API

<30 API

Frothy Crude – Getting Lighter

Source: EIA, Morningstar

gAPI measures crude density

gShale crude is light and sweet

gRefineries configured for heavier crude

gCreates a quality mismatch

Gulf Coast Refinery average

= 31.4 API

6

New Plumbing at the Gulf Coast

Houston

Corpus

St James

Permian

Cushing

BPA

LOOPEagle Ford

• 47 Refineries & 5 Condensate splitters

– 9.8 mmb/d capacity (1.2 added since 2010)

• 18 Unload Rail Terminals

– ~1.7 mmb/d built since 2012

• Storage

– 291 mmBbl tank capacity Sep 2016

– 85 mmBbl added since 2011

• 17 Marine Ports in use to transfer crude

• 26 Long distance transmission pipelines

– ~ 6.5 mmb/d capacity

7

Permian Takeaway Infrastructure

Source: Company Filings, Morningstar

0

1000

2000

3000

4000

5000

6000

Mb/

d

Rail

Cactus 2

Basin Expansion

Sunrise Expansion

EPIC

South Texas Gateway

Midland Sealy

PELA

Cactus

Bridgetex

Permian Express II & III

Existing Pipelines

Refinery Consumption

Production Forecast

Forecast

Proposed

gRapid pipeline build out in response to growing production

gProduction forecast to double from 2.6 mmb/d at end 2017 to 5.2 mmb/d in 2020

gAdditional 1.6 mmb/d pipeline capacity proposed

8

-

1,000

2,000

3,000

4,000

5,000

6,000

1Q 2

014

3Q 2

014

1Q 2

015

3Q 2

015

1Q 2

016

3Q 2

016

1Q 2

017

3Q 2

017

1Q 2

018

3Q 2

018

1Q 2

019

3Q 2

019

1Q 2

020

3Q 2

020

mb/

d

Gulf Coast

Cushing/Midwest

Refinery Consumption

Permian Takeaway Capacity: Destinations

Source: Company Reports, Morningstar

g~ 450 mb/d processed in Permian refineries

g Traditional market = Cushing & Midwest

gMost new production goes to Gulf Coast

9

0

2

4

6

8

10

12

2010 Supply 2010 Demand 2017 Supplythru August

2017 Demandthru August

$/ba

rrel

Exports

Sent to other PADDs

Refinery Throughput

Received from other PADDs

Imports

Production

Changing Gulf Coast Crude Balance 2010 - 2017

Source: EIA, Morningstar

g2010 - 8.8 mmb/d, 2017 supply mostly imports, demand all domestic - balanced

g2017 – 10.3 mmb/d, supply, 10.8 mmb/d demand – stock draw and exports

10

0

50

100

150

200

250

300

Jan-2013 Jan-2014 Jan-2015 Jan-2016 Jan-2017

mill

ion

barr

els

Gulf Coast Inventory

Source: EIA

g Increasing since 2013 as new flows reach Gulf Coast

gRecord high 281 mmbbl in early April 2017

g Falling since then (except Harvey) 219 mmbbl Nov 3, 2017

11

-5

0

5

10

15

20

25

30

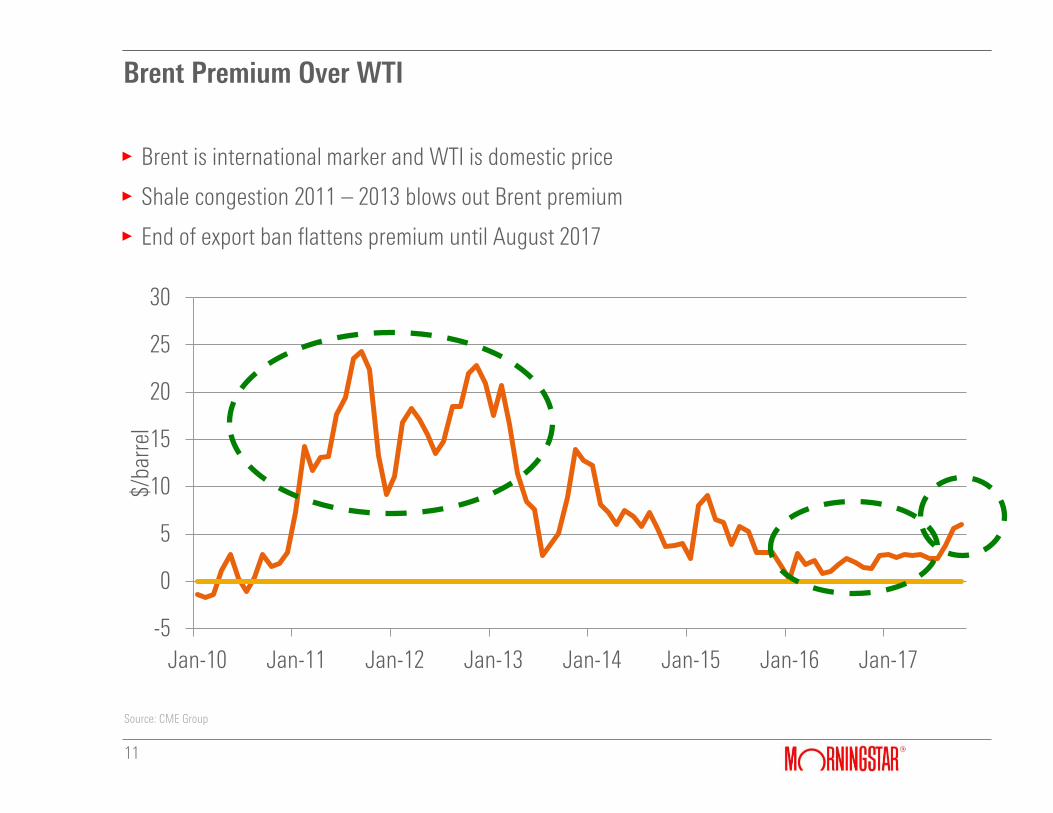

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

$/ba

rrel

Brent Premium Over WTI

Source: CME Group

gBrent is international marker and WTI is domestic price

gShale congestion 2011 – 2013 blows out Brent premium

gEnd of export ban flattens premium until August 2017

12

gExports restricted prior to December 2015

g2016 average 280 mb/d

gMore than doubled to 638 mb/d average through August 2017

Gulf Coast Exports - Monthly

Source: U.S. Customs, Morningstar

0

100

200

300

400

500

600

700

800

900

Mb/

d

13

0

500

1000

1500

2000

2500

0

1

2

3

4

5

6

7

Mb/

d

$/ba

rrel

Brent Premium Total Exports

(Total) Crude Exports and Brent Premium

Source: EIA, CME Group, Morningstar

gBrent premium above $3/barrel encourages exports

gOctober 27, 2017 peak = 2.1 mmb/d exports, Brent premium = $6.16/bbl

14

0

1

2

3

4

5

6

7

8

$/ba

rrel

Brent

LLS

WTI Houston

Gulf Coast Premiums to WTI Cushing

Source: Argus Media, CME Group, Morningstar

gBrent premium over WTI Cushing does not account for Gulf Coast transport

g LLS at Gulf Coast is priced too close to Brent for export

gWTI Houston premium supports exports

15

4.00

4.50

5.00

5.50

6.00

6.50

40

45

50

55

60

65

Jan-

18

Jun-

18

Nov

-18

Apr

-19

Sep-

19

Feb-

20

Jul-2

0

Dec

-20

May

-21

Oct

-21

Mar

-22

Aug

-22

Jan-

23

Jun-

23

Nov

-23

Apr

-24

$/ba

rrel

pre

miu

m

$/ba

rrel

Brent WTI Brent Premium

Forward Curves November 7, 2017

Source: CME Group, Morningstar

gBrent & WTI curves backwardated through 2021

gBrent premium declines in 2018 but recovers to $6/barrel in 2020

gExports likely to continue

16

0

1

2

3

4

5

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

Apr

-17

Jul-1

7

mm

b/d

Diesel Gasoline NGL Other Refined Crude

g2010 average daily refined product export was 1.7 mmb/d

g2016 average was 3.6 mmb/d – more than double (2017 to August = 3.9 mmb/d)

gCrude exports small by comparison (14% in 2017)

Infrastructure: Gulf Coast Dock Flows

Source: EIA

17

Storage at Terminals

Source: Company Reports, Morningstar

g 85 mmbbl added 2011 to 2017 in Gulf Coast region – helps staging for exports

g56 mmbbl more to come

18

gHouston – Galveston Dominates 2014-2015

gCorpus Christi hidden

g Louisiana and Port Arthur Growing in 2017

Gulf Coast Exports – Loading Region

Source: U.S. Customs, Morningstar

0

100

200

300

400

500

600

700

800

900

Jan-14 Jun-14 Nov-14 Apr-15 Sep-15 Feb-16 Jul-16 Dec-16 May-17

Houston-Galveston Lousiana Port Arthur Mobile, AL

19

Marine Dock Terminals

Source: Company Reports, Morningstar

gCorpus linked to Permian and Eagle Ford – Occidental Ingleside 300 mb/d

gVessel size is a constraint

g LOOP reversal key (Capline Announcement)

20

Permian Takeaway Balance – Constraints and Pricing

Source: Company Filings, Morningstar

0

1000

2000

3000

4000

5000

6000

Mb/

d

Rail

Cactus 2

Basin Expansion

Sunrise Expansion

EPIC

South Texas Gateway

Midland Sealy

PELA

Cactus

Bridgetex

Permian Express II & III

Existing Pipelines

Refinery Consumption

Production Forecast

gEarlier Constraint in 2014 – production exceeds takeaway in Q3 2014

21

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

Jan-14 Apr-14 Jul-14 Oct-14

$/ba

rrel

Midland WTI Discount

WTI Cushing

Midland Takeaway Constraint

Source: CME Group, Morningstar

g “Normal” Midland discount = $0.80/barrel – pipeline tariff to Cushing

g In August 2014 Midland price drops $20/barrel below Cushing as producers discount to find pipeline space

gBy November the constraint is over due to new pipe capacity -shippers bid $5/barrel premiums

22

Permian Takeaway Balance – Constraints and Pricing

Source: Company Filings, Morningstar

0

1000

2000

3000

4000

5000

6000

Mb/

d

Rail

Cactus 2

Basin Expansion

Sunrise Expansion

EPIC

South Texas Gateway

Midland Sealy

PELA

Cactus

Bridgetex

Permian Express II & III

Existing Pipelines

Refinery Consumption

Production Forecast

gSimilar constraints lie ahead as production exceeds capacity next year (2018)

g Further constraint in 2020

gProduction/drilling could slow if prices drop too low

How the Permian Spigot Works

23

gBreakeven is the low price

g Increased demand in international market will drive Brent premium and exports

gA wide premium and price above $50/barrel encourages Permian growth

gWTI Houston is the clearing price for exports

gDock infrastructure constraints will limit exports

g Takeaway constraints limit production

gCould see consistent 2 mmb/d exports and term contracts

g If prices and production decline then low sporadic exports

gU.S. Gulf Coast has become the swing market for crude exports and Permian is the spigot

24

Questions?

gResearch Focus: North America

/U.S. and Canadian crude production, takeaway infrastructure and pricing

/Refining and processing

/Trading, storage, blending, arbitrage

/Export markets and opportunities

/Downstream petrochemical impacts

25

Morningstar Crude and Refined Products Commodities Research

Recent Note

Any Morningstar ratings/recommendations contained in this presentation are based on the full research report available from

Morningstar or your adviser.

© Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content

contained herein to be accurate, complete or timely nor will they have any liability for its use or distribution. No part of this document

may be reproduced or distributed in any form without the prior written consent of Morningstar.

Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892)

and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Please refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the

advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment

Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information.

Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation,

contact a professional financial adviser. Some material is copyright and published under licence from ASX Operations Pty Ltd ACN 004

523 782 ("ASXO").

26