policyholders’ satisfaction towards services offered...

TRANSCRIPT

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 80

POLICYHOLDERS’ SATISFACTION TOWARDS SERVICES OFFERED BY LIFE

INSURANCE CORPORATION OF INDIA - A STUDY WITH REFERENCE TO

NAGAPATINAM DISTRICT

K. Sankaranarayanan

Ph.D Research Scholar, PG & Research Department of Commerce,

A.V.C. College (Autonomous), Mannampandal - 609 305, Mayiladuthurai,

Dr. R. Rajanbabu

Assistant Professor and Research Advisor, PG & Research Department of Commerce,

A.V.C. College (Autonomous), Mannampandal - 609 305, Mayiladuthurai

ABSTRACT

The majority of the policy holders are satisfied with LIC`s service. The major objectives of this research

are to ascertain the socio-economic profile of sample respondents and identify the satisfaction level of

policyholders in LIC`s services. This research has also endeavors to develop the customer satisfaction. Primary

data has been collected for this present study. The primary data was collected from 560 sample respondents

from Nagapattinam District, by proportionate stratified random sampling method. Suggested this study, the

analysis it is identified that educational qualification and monthly income are found to be associated with policy

holder’s satisfaction. LIC should spread its wings in rural areas; it will enable the policy holders rather they

approach in urban area. LIC has to create awareness among female policy holders, regarding the benefits of

the LIC policies. This article highlights policyholders’ satisfaction towards services offered by life insurance

Corporation of India - a study with reference to Nagapattinam district.

KEY WORDS :Policyholders‟ satisfaction, Policyholders‟ Awareness and Satisfaction, Services offered, Life

Insurance Corporation of India, Malhotra Committee, Problems faced by the Policyholders, LIC housing Loan

Finance

INTRODUCTION

Insurance is defined as a co-operative device to spread the loss caused by particular risk over a number

of persons who are exposed to it and who agree to ensure themselves against that risk. Every risk involves the

loss of one or other kind. The function of insurance is to spread the loss over a large number of persons who

have agreed to co-operate each other at the time of loss. The risk cannot be averted but loss occurring due to

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 81

certain risk can be distributed amongst the agreed persons. The insurance, as a social device to accumulate

funds and to meet the uncertain losses arising through a certain risk to a person insured the risk.

STATEMENT OF THE PROBLEM

Insurance sector, as a whole has contributed to the development of economy through generation of

employment opportunities, acceleration of industrial growth and so on. Although Life insurance Corporation of

India has its own significance and place in the economy, it is not free from problems. Policyholders‟ satisfaction

is the true differentiator for the success of any business and is more so in insurance, where the products are

perceived to be intangible. The six main aspects namely assess the policyholders, satisfaction level of

policyholders, service quality, LIC housing finance, switching behaviour and problem faced by policyholders.

In today‟s challenging business environment, customer service and policyholders‟ satisfaction are

emerging as key competitive advantages. Life Insurance is customer based business where retention of existing

policyholders is the biggest challenge in present-day cut throat market competition. LIC enjoyed monopoly in

life Insurance sector during the pre-nationalized period up to 1999. So public are forced to accept the policies

issued by LIC. After liberalization in 2000, many Indian and foreign companies are entered in insurance

business. Due to the advent of stiff competition, both public sector and private sector introduce new polices

with low cost. So LIC has a variety of plans to cater the needs of various categories of people and their diverse

needs. LIC makes effective awareness among public about its product and give better service to its

policyholders. Hence, the present study focuses on policyholders‟ satisfaction towards services offered by Life

Insurance Corporation of India- a study with reference to Nagapattinam district.

Life is full of risk and uncertainties. They believe in future rather than the present and desire to have a

better and secured future. In this direction, life insurance service has its own value in terms of minimizing risk

and uncertainties. Indian economy is developing and having huge middle class societal status and salaried

persons. Their money value for current needs and future desires has the pendulum moves to another side which

generate the reasons behind holding a policy. Insurance industry is a service-oriented unit. It renders services

like available space, display adequate information, suggestion box and so on to the policyholders. It is essential

that insurance schemes should attract and satisfy the policyholders in different ways. Life insurance has today

become a mainstay of any market economy since it offers plenty of scope for garnering large sums of money

for long periods of time. Ever since its inception in 1956, the life insurance companies in India have been

providing better service to the society. The policyholders once when they become a part of the LIC feel free

about the safety of their wards. The families of the non-policyholders meet out uncertainty on the death of the

bread winner. So, there is an attraction towards life insurance. People who care much about them and their

families become policyholders of life insurance. The tastes and preferences of policyholders are indifferent.

The LIC of India has been introducing variety of policies suiting the tastes and preferences of the

policyholders. It is observed that many policyholders have taken more than one policy. It is a clear indication

that they are very much interested in utilizing maximum benefits from LIC. Some people give due importance

to money value and high returns on their investments. But greater risks are inherent advantages expected from

LIC products. It is in this context this study has been undertaken to the “policyholders‟ satisfaction towards

services offered by Life Insurance Corporation of India - a study with reference to Nagapattinam district”.

OBJECTIVES OF THE STUDY

The main objectives of the study are as under:

1. To analyse the policyholders‟ awareness and satisfaction towards insurance policies in Life Insurance

Corporation of India.

2. To ascertain the policyholders‟ level of satisfaction relating to services offered by Life Insurance

Corporation of India in Nagapattinam district.

3. To find out the problems faced by the policyholders towards Life Insurance Corporation of India in

Nagapattinam district.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 82

HYPOTHESIS OF THE STUDY

H0: 1 H0: 2 “There is no significant association between type LIC plans and awareness of the

policyholders”.

H0: 2 “There is no significant association between reasons for the preference of LIC policy and the

policyholders”.

H0: 3 “There is no significant difference between demographic profile and policyholders‟ level of

satisfaction”

H0: 5 “There is no significant difference between demographic profile and problems faced by

policyholders”.

METHODOLOGY

The study was based on survey method. This study both primary and secondary data. The primary data

was collected from one five hundred and sixty sample respondents by using interview method from

Nagapattinam District. Samples were chosen by adopting convenient sampling method. The interview schedule

has been prepared in such a way that the respondents are able to express their opinion freely and frankly. A well

structured interview schedule was framed with the help of the Research Supervisor, the research experts and the

LIC managers in the study area. Interview schedule was the main tool used to collect the pertinent data from the

selected sample respondents.

Primary Data

Primary data refer to data that are collected a fresh for the first time and that is original in nature. The

required primary data are collected through interview schedule for policyholders.

Secondary Data

Secondary data are that data that have been collected by someone else and which have already been

passed through the statistical process. Secondary data here have been collected from company records, product

profile of the company, article, journal, newspapers, magazines, books and general discussion with company

channels.

Sampling Design

The researcher had adopted Proportionate Stratified Random Sampling Method was used to select the

sample policyholders in Life Insurance Corporation of India, Nagapattinam district. To conduct this study with

regard to the utilization of the Life Insurance Corporation services by the policyholders particularly the

policyholders in early 2015. This sampling involved in drawing sample from each stratum in proportion to the

latter‟s share in the total policyholders. 0.5 per cent of each taluk namely Kevalur, Kuthalam, Mayiladuthurai,

Nagapattinam, Sirkali, Tharangambadi, Thirukuvalai and Vetharanyam were selected for the study. The sample

size constituted 0.5 per cent of the universe (total 1, 12,000) i.e., 560 sample policyholders were selected. For

selecting the respondents the following process was adopted: Out of the total respondents scattered in 8 Taluks

of the Nagapattinam District and among nearly 1.12 lakhs policyholders continuously paying the premium at

present. Thus, the total sample selected is 560 in the whole district of Nagapattinam.

Statistical Tools and Analysis

The collected data have been consolidated, tabulated and analyzed by using relevant statistical tools like,

Percentage analysis, Descriptive analysis, One Way ANOVA, t-Test, Regression analysis, Kruskal-Wallis Test,

Multivariate Test, Reliability test for Cronbach‟s alpha and Factor Analysis. The SPSS 20.0 package was

utilized for analyzing the data.

SCOPE OF THE STUDY

The study covers only policyholders‟ satisfaction towards services offered by Life Insurance

Corporation of India- in Nagapattinam district, such as factors influencing policyholder, assess the satisfaction

of the policyholders (product attributes, product services, product information, risk coverage and knowledge

levels of agents), switching over from LIC to other private companies, services offered by LIC of India,

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 83

respondent‟s satisfaction level regarding various factors of LIC housing finance and problems faced by the

policyholders. The study pertains to a period from April 2014 to March 2015. Further, the literature available on

life insurance industry is also very limited and hence, the scope of the present study is made narrower.

AREA OF THE STUDY

This study is restricted to the Nagapattinam District which comes under the Thanjavur Division of

Tamilnadu, which is considered as one of the top divisions of Southern Zone of LIC of India. The respondents

are selected only from Nagapattinam District and only those policyholders who have Life insurance policies of

Life Insurance Corporation of India alone were interviewed.

PILOT STUDY

The interview schedule was given to some research experts for a critical view regard to its content,

format and sequence and their feedback was incorporated. Then interview schedule was distributed to 20

respondents for pre-testing and pilot study was also conducted. Pre-testing was done to ensure reliability and

validity of the interview schedule. It was done to check whether the instrument was correctly framed in an

understandable manner. Taking into consideration the suggestions of the selected sample respondents, necessary

modifications and changes were incorporated in the interview schedule after the pilot study. The respondents

included in the pilot study were not included as samples for the final study.

PERIOD OF THE STUDY

The studies cover recent one year from April 2014 to March 2015 for analysis of secondary data relating

to various aspects of marketing in Life Insurance Corporation of India. The primary data relating to the opinion

of policyholders of LIC of India have been collected during the last year of the study April 2015 to March 2016.

LIMITATIONS OF THE STUDY

As the study made with Primary and Secondary research, there are certain limitations to the study to be

noticed.

1. Sufficient number of respondents from all the LIC service could not be included.

2. The study is confined only to policyholders‟ satisfaction of LIC and other related issues are beyond

the purview of present study.

3. The study does not deal with other diversified activities of LIC like mutual funds and other services

and also the General Insurance Corporation of India (GICI).

4. The study aims to analyze only individual life insurance policies and not the group insurance policies,

health insurance policies, postal life insurances and Employees State Insurance, taken by the women

policyholders.

5. Convenient sampling method was used to frame the sample for indefinite population and its

limitations are also applicable.

6. It is difficult to know if all the respondents gave accurate information; some respondents tend to give

misleading information.

POLICYHOLDERS’ SATISFACTION TOWARDS LIC OF INDIA –AN ANALYSIS

Individual policyholders selected from the Life Insurance Corporation of India constituted the sample of

customers. The demographic profile of prospective customers is strategically very relevant and significant is

designing and marketing of insurance products. More importantly, a clear understanding of demographic

characteristics of customer is very essential for diagnosing the difference in the attitude and perception of the

policyholders. The studies also focus on customer satisfaction services offered by the Life insurance

Corporation.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 84

Table 1: Demographic Profile of the Respondents

Demographic profile Number of Respondents Percentage

Gender

Male 427 76.25

Female 133 23.75

Total 560 100.00

Age

Below 20 39 6.96

21 to 30 86 15.36

31 to 40 182 32.50

41 to 50 116 20.71

51 – 60 73 13.04

60 and above 64 11.43

Total 560 100.00

Marital Status

Unmarried 98 17.50

Married 434 77.50

Others (Divorce/Widow /

Single) 28 5.00

Total 560 100.00

Geographic Locality

Rural 341 60.89

Urban 219 39.11

Total 560 100.00

Education

Illiterate 32 5.71

Upto school level 169 30.18

Graduate/ Diploma 217 38.75

Post graduate/ Professional 142 25.36

Total 560 100.00

Occupation

Government employee 143 25.54

Private employee 161 28.75

Businessmen 94 16.79

Students 47 8.39

House wife 28 5.00

Farmers 87 15.54

Total 560 100.00

Monthly Income

UP to 25,000 363 64.82

25,001 to 50,000 134 23.93

50,001 to 1,00,000 52 9.29

Above 1,00,000 363 1.96

Total 560 100.00

Size of the Family

Members

Small (≤3) 131 23.21

Medium (3-5) 332 59.46

Large (above 5 ) 97 17.32

Total 560 100.00

Nature of Family

Joint 197 35.18

Nuclear 363 64.82

Total 560 100.00

Source: Primary data

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 85

Table 1 shows that demographic profile of the policyholders. Gender is the important distinguishing

segmentation variable. As far as insurance is concerned, men had greater idea about the insurance products and

female also significant role in the taking critical decisions in the purchase of products. Therefore, it is pertinent

to study the association between gender of the respondents and their satisfaction towards services of the LIC of

India. Analysis of gender segmentation shows that male consists 76.25 per cent of the policyholders and only

23.75 per cent belonging to female category.

Age is the important demographic variable for distinguishing segment. The policyholders from different

age groups are requested to state their level of satisfaction towards services of the LIC of India and an attempt

was made to find out the association between age and satisfaction. Age wise segmentation of policyholders

shows that about 32.50 per cent belong to the age group of 31 to 40 which is a common trend in the insurance

sector. The age category of 41 to 50 years, 21 to 30 years, 51 to 60 years, 60 and above constitutes 20.71 per

cent, 15.36 per cent, 13.04 per cent and 11.43 per cent towards the respondents in the life insurance

policyholders. However, policyholders belonging to age category of below 20 constitute only 6.96 percent of

the total in the insurance sector.

The married category of respondents constitutes 77.50 per cent, unmarried category of respondents

constitutes 17.50 per and 5 per cent are other (Divorce/Widow / Single) category of respondents. The

geographic location of the respondents constitutes highest of 60.89 per cent of the respondents belong to rural,

39.11 per cent of the respondents belong to urban.

The education of the policyholders influences their satisfaction towards services of the LIC of India.

Therefore, the respondents from different educational status are requested to state their level of satisfaction

towards services of the LIC of India and an attempt was made to find out the association between educational

status and satisfaction. Education wise segments show that individuals having graduate/diploma qualification

constitutes 38.75 of the policyholders followed by up to school qualification constitutes 30.18 percent and Post

graduate/Professional qualification constitutes 25.36 per cent. Hardly 5.71 percent of the policyholders belong

to illiterate respondents in the life insurance policyholders.

The occupation segments, represents that 28.75 per cent of policyholders are employed in the private

sector, 25.54 per cent of the policyholders are employed in the government sector, 16.79 per cent of the

policyholders are businessmen, 15.54 per cent of the policyholders are farmers, 8.39 per cent of the

policyholders are students, and house wife category policyholders constitutes 5 per cent.

The income wise analysis of customer segmentation indicates that 64.82 per cent of the policyholders

have monthly income of up to Rs.25,000, 23.93 per cent of the policyholders have monthly income of

Rs.25,001 to 50,000, 9.29 per cent of the policyholders have monthly income of Rs. Rs.50,001 to 1,00,000 and

1.96 per cent of the policyholders have monthly income of 1.96 towards the respondents.

Out of total 59.46 per cent of the respondents are medium family size of 3 to 5 members, 23.21 per cent

of the respondents are small family size of less than are equal to 3 members and 17.32 per cent of the

respondents are large family size of above 5 members.

The nature of family size represents that 64.82 per cent are nuclear family and 35.18 per cent of the

respondents are joint family towards the policyholders.

MULTIVARIATE TEST

Multivariate testing is a technique for testing a hypothesis in which multiple variables are modified. The

goal of multivariate testing is to determine which combination of variations performs the best out of all of the

possible combinations.

Websites and mobile apps are made of combinations of changeable elements. A multivariate test will

change multiple elements, like changing a picture and headline at the same time. Three variations of the image

and two variations of the headline are combined to create six versions of the content, which are tested

concurrently to find the winning variation.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 86

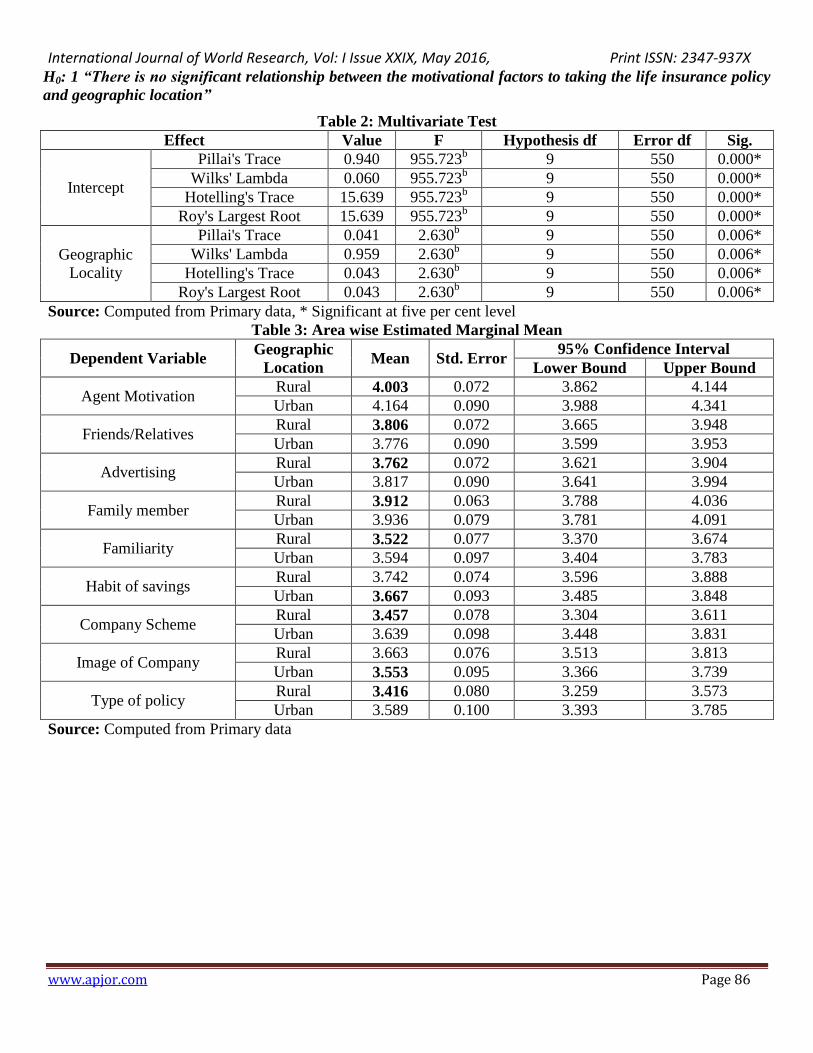

H0: 1 “There is no significant relationship between the motivational factors to taking the life insurance policy

and geographic location”

Table 2: Multivariate Test

Effect Value F Hypothesis df Error df Sig.

Intercept

Pillai's Trace 0.940 955.723b 9 550 0.000*

Wilks' Lambda 0.060 955.723b 9 550 0.000*

Hotelling's Trace 15.639 955.723b 9 550 0.000*

Roy's Largest Root 15.639 955.723b 9 550 0.000*

Geographic

Locality

Pillai's Trace 0.041 2.630b 9 550 0.006*

Wilks' Lambda 0.959 2.630b 9 550 0.006*

Hotelling's Trace 0.043 2.630b 9 550 0.006*

Roy's Largest Root 0.043 2.630b 9 550 0.006*

Source: Computed from Primary data, * Significant at five per cent level

Table 3: Area wise Estimated Marginal Mean

Dependent Variable Geographic

Location Mean Std. Error

95% Confidence Interval

Lower Bound Upper Bound

Agent Motivation Rural 4.003 0.072 3.862 4.144

Urban 4.164 0.090 3.988 4.341

Friends/Relatives Rural 3.806 0.072 3.665 3.948

Urban 3.776 0.090 3.599 3.953

Advertising Rural 3.762 0.072 3.621 3.904

Urban 3.817 0.090 3.641 3.994

Family member Rural 3.912 0.063 3.788 4.036

Urban 3.936 0.079 3.781 4.091

Familiarity Rural 3.522 0.077 3.370 3.674

Urban 3.594 0.097 3.404 3.783

Habit of savings Rural 3.742 0.074 3.596 3.888

Urban 3.667 0.093 3.485 3.848

Company Scheme Rural 3.457 0.078 3.304 3.611

Urban 3.639 0.098 3.448 3.831

Image of Company Rural 3.663 0.076 3.513 3.813

Urban 3.553 0.095 3.366 3.739

Type of policy Rural 3.416 0.080 3.259 3.573

Urban 3.589 0.100 3.393 3.785

Source: Computed from Primary data

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 87

Table 4: Tests of Between-Subjects Effects

Source Dependent Variable Type III Sum of

Squares df

Mean

Square F Sig.

Corrected

Model

Agent Motivation 3.476a 1 3.476 1.973 0.161

Friends/Relatives .122b 1 0.122 0.068 0.794

Advertising .402c 1 0.402 0.227 0.634

Family member .077d 1 0.077 0.057 0.812

Familiarity .684e 1 0.684 0.334 0.563

Habit of savings .756f 1 0.756 0.403 0.526

Company Scheme 4.407g 1 4.407 2.114 0.146

Image of Company 1.621h 1 1.621 0.817 0.366

Type of policy 3.974i 1 3.974 1.824 0.177

Intercept

Agent Motivation 8895.476 1 8895.476 5049.110 0.000

Friends/Relatives 7667.593 1 7667.593 4316.231 0.000

Advertising 7661.745 1 7661.745 4325.194 0.000

Family member 8213.706 1 8213.706 6026.896 0.000

Familiarity 6752.020 1 6752.020 3299.390 0.000

Habit of savings 7319.527 1 7319.527 3904.841 0.000

Company Scheme 6716.286 1 6716.286 3222.055 0.000

Image of Company 6942.492 1 6942.492 3501.482 0.000

Type of policy 6544.616 1 6544.616 3003.496 0.000

Geographic

Locality

Agent Motivation 3.476 1 3.476 1.973 0.161

Friends/Relatives 0.122 1 0.122 0.068 0.794

Advertising 0.402 1 0.402 0.227 0.634

Family member 0.077 1 0.077 0.057 0.812

Familiarity 0.684 1 0.684 0.334 0.563

Habit of savings 0.756 1 0.756 0.403 0.526

Company Scheme 4.407 1 4.407 2.114 0.146

Image of Company 1.621 1 1.621 0.817 0.366

Type of policy 3.974 1 3.974 1.824 0.177

Source: Computed from Primary data

The estimated marginal mean and MANOVA Tables 4.14, 4.15, and 4.16, indicates that the mean scores

of nine variables in motivating factors to taken together vary over the policy in the area location, and that the

motivating factors in urban is higher than rural, as the mean values are very low in rural of agent motivation

(4.003), friends/relatives (3.806) advertising (3.762), family member (3.912), familiarity (3.522), company

scheme (3.457), and type of policy (3.416). The mean value is low in urban in habit of savings (3.667) and

image of the company (3.553). The statistical significance of the variation of the mean confirms this. Moreover,

the MANOVA characterized by powerful Pillai‟s Trace test is significant at five per cent level (F 2.634 with

p=0.005<005). However, the nine variables for the two geographic location are taken independently, variation

not found statistically significant in the test of between-subjects effects (p>0.05).

It is concluded that, the area-wise motivation are taken independently, all the motivation to take the

policy except savings and image of the company are found higher in rural areas than the urban areas, variation

can also be found statistically significant in the test of motivation of to take life insurance products.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 88

DEMOGRAPHIC PROFILE AND POLICYHOLDERS SATISFACTION ON SERVICES OFFERED

BY THE LIC

This section is devoted to testing the significant difference between demographic profile of the

respondents with respect to policyholders satisfaction on services offered by the LIC (Product Attributes,

Product Services, Product Information, Risk Coverage, Knowledge of Agents, Physical facilities in the LIC, and

service representative) in Nagapattinam District. The following null hypothesis has been formulated.

H0: 2 “There is no significant difference between demographic profile and policyholders’ level of

satisfaction”

H0:2(a) “There is no significant difference between age and policyholders’ satisfaction on product

attributes”

One way ANOVA is applied to ascertain if there were any significant difference between age and the

satisfaction of services provided by the LIC.

Table 5: Age and Satisfaction of Services

Statements Age N Mean Std.

Deviation Std. Error F Value P Value

Product

Attributes

Below 20 39 31.28 11.82 1.89

4.762 0.001*

21 to 30 86 35.44 10.29 1.11

31 to 40 182 36.85 12.97 0.96

41 to 50 116 37.03 11.21 1.04

51 – 60 73 42.00 14.26 1.67

60 and above 64 38.72 10.75 1.34

Total 560 37.17 12.30 0.52

Product Services

Below 20 39 15.13 6.16 0.99

4.113 0.001*

21 to 30 86 16.73 5.07 0.55

31 to 40 182 17.53 6.97 0.52

41 to 50 116 17.77 6.29 0.58

51 – 60 73 20.21 8.48 0.99

60 and above 64 18.81 4.86 0.61

Total 560 17.79 6.62 0.28

Product

Information

Below 20 39 31.13 11.51 1.84

5.031 0.001*

21 to 30 86 35.44 9.83 1.06

31 to 40 182 36.86 12.74 0.94

41 to 50 116 37.17 10.87 1.01

51 – 60 73 42.00 14.26 1.67

60 and above 64 38.64 10.60 1.33

Total 560 37.18 12.07 0.51

Risk Coverage

Below 20 39 15.44 5.89 0.94

5.320 0.001*

21 to 30 86 17.41 5.32 0.57

31 to 40 182 18.31 6.51 0.48

41 to 50 116 17.90 5.78 0.54

51 – 60 73 21.05 7.06 0.83

60 and above 64 19.09 5.67 0.71

Total 560 18.33 6.25 0.26

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 89

Knowledge

Levels of Agents

Below 20 39 12.00 4.80 0.77

3.952 0.002*

21 to 30 86 13.50 3.78 0.41

31 to 40 182 14.19 5.54 0.41

41 to 50 116 14.42 5.18 0.48

51 – 60 73 16.16 6.78 0.79

60 and above 64 14.78 3.83 0.48

Total 560 14.31 5.27 0.22

Physical

facilities in the

LIC

Below 20 39 30.28 12.03 1.93

3.673

0.003*

21 to 30 86 33.85 9.90 1.07

31 to 40 182 35.19 14.05 1.04

41 to 50 116 35.68 12.65 1.17

51 – 60 73 40.41 16.95 1.98

60 and above 64 36.88 11.01 1.38

Total 560 35.69 13.32 0.56

Response of

Service

Representative

Below 20 39 21.87 8.10 1.30

5.928 0.001*

21 to 30 86 23.59 7.60 0.82

31 to 40 182 25.39 9.02 0.67

41 to 50 116 24.97 8.26 0.77

51 – 60 73 29.56 9.71 1.14

60 and above 64 26.48 7.99 1.00

Total 560 25.45 8.76 0.37

Source: Computed from Primary data

The obtained „F‟ value is 4.762 and it is significant at 5 per cent level. The value indicates that there is a

significant mean difference between policyholders satisfaction with product attributes. Hence, the stated

hypothesis of (H0: 5(a)) “there is no significant difference between age and policyholders satisfaction on

product attributes” is rejected. The obtained „F‟ value is 4.113 and it is significant at 5 per cent level. The value

indicates that there is a significant mean difference between policyholders satisfaction with product services.

Hence, the stated hypothesis of (H0: 5(b)) “there is no significant difference between age and policyholders

satisfaction on product services” is rejected. The obtained „F‟ value is 5.031 and it is significant at 5 per cent

level. The value indicates that there is a significant mean difference between policyholders satisfaction with

respect to product information. Hence, the stated hypothesis of (H0: 5(c)) “there is no significant difference

between age and policyholders satisfaction on product information” is rejected. The obtained „F‟ value is 5.320

and it is significant at 5 per cent level. The value indicates that there is a significant mean difference between

policyholders satisfaction with respect to risk coverage. Hence, the stated hypothesis of (H0: 5(d)) “there is no

significant difference between age and policyholders satisfaction on risk coverage” is rejected. The obtained „F‟

value is 3.952 and it is significant at 5 per cent level. The value indicates that there is a significant mean

difference between policyholders satisfaction with respect to agent knowledge. Hence, the stated hypothesis of

(H0: 5(e)) “there is no significant difference between age and policyholders satisfaction on agent knowledge” is

rejected. The obtained „F‟ value is 3.763 and it is significant at 5 per cent level. The value indicates that there is

a significant mean difference between policyholders satisfaction with respect to physical facility. Hence, the

stated hypothesis of (H0: 5(f)) “there is no significant difference between age and policyholders satisfaction on

physical facility” is rejected. The obtained „F‟ value is 5.928 and it is significant at 5 per cent level. The value

indicates that there is a significant mean difference between policyholders satisfaction with respect to service

personal. Hence, the stated hypothesis of (H0: 5(g)) “there is no significant difference between age and

policyholders satisfaction on response of service personal” is rejected.

Further, the mean value indicates that the age category of below 20 years are less satisfied with the

products attributes, product services, information, risk coverage, agent knowledge, physical facilities and

service representative than the other age category of respondents.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 90

DEMOGRAPHIC PROFILE AND POLICYHOLDERS PROBLEMS

This section is devoted to testing the significant difference between demographic profile of the

respondents with respect to policyholders‟ problems in the services agents, general problems and compliant

behaviour in the Nagapattinam District. The following null hypothesis has been formulated.

H0: 1 “There is no significant difference between demographic profile and problems faced by policyholders”.

H0: 1(a) “There is no significant difference between demographic profile and problems in using agent

services”.

H0: 1(b) “There is no significant difference between demographic profile and policyholder general

problems”.

H0: 1(c) “There is no significant difference between demographic profile and policyholder problems in

compliant behaviour”.

5.3.1 To test the significant difference between age and policy holders problems in the LIC services. One way ANOVA is applied to ascertain the any significant difference between age and policy holders‟

problems in the LIC services.

Table 6: Age and Policy Holders Problems in the Services

Problems

in the

using of

services of

the Agents

Age N Mean Std.

Deviation

Std.

Error F value P value

Below 20 39 18.10 4.49 0.72

5.440 0.001*

21 to 30 86 20.85 2.42 0.26

31 to 40 182 20.52 3.15 0.23

41 to 50 116 19.90 3.81 0.35

51 – 60 73 21.07 2.74 0.32

60 and above 64 20.16 3.00 0.37

Total 560 20.30 3.31 0.14

General

Problems

Below 20 39 31.21 7.09 1.13

2.471 0.032*

21 to 30 86 31.21 5.71 0.62

31 to 40 182 31.36 6.37 0.47

41 to 50 116 31.07 6.40 0.59

51 – 60 73 31.85 5.76 0.67

60 and above 64 28.33 8.96 1.12

Total 560 30.98 6.65 0.28

Complaint

Behaviour

Below 20 39 16.13 2.99 0.48

3.289 0.006*

21 to 30 86 16.20 2.70 0.29

31 to 40 182 16.26 2.90 0.21

41 to 50 116 15.34 3.23 0.30

51 – 60 73 16.45 2.65 0.31

60 and above 64 14.95 3.71 0.46

Total 560 15.93 3.05 0.13

Source: Computed from Primary data

The calculated F value of 5.440 and it is significant five per cent level. The value indicates that there is a

significant difference between age and policy holder problems in using agent services. Hence, the stated

hypothesis of (H0:1(a)) “there is no significant difference between age and policy holder problems in using

agent services” is rejected.

The calculated F value of 2.471 and it is significant five per cent level. The value indicates that there is a

significant difference between age and policy holder general problems. Hence, the stated hypothesis of

(H0:1(b)) “there is no significant difference between age and policy holder general problems” is rejected.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 91

The calculated F value of 3.289 and it is significant five per cent level. The value indicates that there is a

significant difference between age and policy holder compliant behaviour. Hence, the stated hypothesis of

(H0:1(c)) “there is no significant difference between age and policy holder problems in compliant behaviour” is

rejected.

Further, the age category of 51 to 60 years is having more problems of agent services, general problems

and compliant behviour than the other category of policy holders.

SUMMARRY OF MAJOR FINDINGS

Most of the policy holders are clearly known the life insurance website of which constitutes 95.71 per

cent and rest of 4.29 per cent of the policy holders are not known the LIC website.

The usage of website is helpful and very helpful constitutes 32.14 per cent and 29.46 per cent

respectively. However, it is not useful to the policy holders and average level of helping constitutes

27.50 per cent and 6.61 per cent respectively.

Out total 143 policy holders constitutes 25.54 per cent, 295 policy holders constitutes 52.68 per cent and

47 policy holders constitutes 8.39 per cent are very high, high and moderate level awareness

respectively in the insurance plans of LIC. However, 17 policy holders constitutes 3.04 per cent and 58

policy holders constitutes 10.36 per cent low and very level awareness about the LIC insurance plans.

The surrender of policy is for a long period of time and the policyholders think about the legal

formalities is more at the time of settlement are dominant problem among the policyholders with

acceptance score of 4.09 and 3.99 respectively. The branch employees are not to treat the customers

politely with acceptance score of 2.76, undue favouritism to some policyholders with acceptance score

of 2.72, negative attitude of the agents and other officials for rendering service with acceptance score of

3.70 and rate of interest on loan is not reasonable also with acceptance score of 3.70 towards the policy

holders. The respondents assign the least score of 2.51 for the branches are never customer oriented.

SUGGESTIONS

The study reveals that some of the policyholders are ready switch over from LIC to other insurance

company due to high return, low premium, maximum risk converge, further growth and popularity.

Hence, it is suggested to LIC of India has to evaluate the policyholders perception on the services at

fixed interval level to identify and fulfill their requirements to retain them.

The study also reveals that the policyholders dissatisfaction regarding the adequate seating arrangement

and drinking water facility the LIC office. It is to provide sufficient space for seating arrangement and

provided drinking water facility in the LIC office.

There is a need for the insurance services to reaffirm themselves in view of the stiff competition.

Therefore, the LIC of India shall have to reorient them in terms of the customer service parameters to

instill the concept of quality service in the mind of the policyholders and further in terms of growth.

In present competitive world, customer satisfaction has become an important aspect to retain the policy

holders, not only growth of the corporation but also to survive. Policy holders‟ service is the critical

success factor and insurers through their best services would be able to reposition and differentiate itself

from private life insurance.

The policyholders in the Life Insurance Corporation are to feel that the settlement process is more

formalities. Hence, it is suggested that the claim settlement process should be made fast and must not

involve lengthy decision making process.

A plan with high benefits at low premium rates should be planned to facilitate all sections of the

policyholders.

Extension branches can be opened in rural areas to facilitate the policyholders. Working hours can be

increased to facilitate the payment of premium to the policy holders.

International Journal of World Research, Vol: I Issue XXIX, May 2016, Print ISSN: 2347-937X

www.apjor.com Page 92

Some special focus should be laid on individual risk coverage while designing the products to

agriculturalists.

The company, if possible should invest in advertising, conduct road shows, and spend money on

hoardings, so that it can create awareness about its unknown products.

CONCLUSION

The present study concludes that, the LIC of India is the leading public sector insurance company in

India has facing very stiff competition from the new players entering the market. LIC of India is facing

increased competition on one front and a decline in the market share on the other hand. LIC has always been in

the forefront of utilizing its recourses effectively. It has been striving to achieve effectiveness and excellence in

its business operations. The present study suggested that the measures such as special events for policyholders,

providing of prompt service, reducing the time period of surrendering the policy, increase the loan amount with

policy, improvement in infrastructure, creativity and innovativeness, understanding the policyholders needs,

policyholders contact programmes, providing update information, staff involvement, user friendly skills,

customer compliant monitoring cell and quality improvement strategy will improve service quality of the LIC

of India. This study is also found that majority of them willing to continue with LIC. This shows their trust in

the Life Insurance Corporation. The LIC must know the need of their policyholders is to serve better than any

other private players” has made LIC to remain as the market leader.

REFERENCES

1. Ahmed A. & Kwatra N., “Level of Customers Satisfaction with their Perception on the Quality of

Insurance Services Galaxy”, International Interdisciplinary Research Journal (2014), Vol. 2(3),

pp. 188-193.

2. Balachandran, S., “Customer Driven Services Management”, Response books (A Division of Sage

Publications), New Delhi, 2001

3. Balasubramaniam A., “Postal Life Insurance: its Market Growth and Policyholders‟ Satisfaction”,

Samzodhana - Journal of Management Research (2014), Vol. 2(1), pp. 317-326.

4. Charles, P. Jones, “Investment Analysis and Management,” John Wiley and Sons (Asia) Pvt. Ltd.,

Singapore, 2002

5. Gopalakrisha, G, The Insurance Customer- the Consumer Protection act 1986 Volume VI, No. 3,

February 2008, Page No. 33

6. Keerthi, P. and Vijayalakshmi, R., “A Study on the Expectations and Perceptions of the Services in

Private Life Insurance Companies, SMART Journals, Vol. 5, 2009.

7. Krishna Swami G., “Principles and Practice of Life Insurance”, Excel Books, New Delhi, 2009

8. Mark S. Dorfman, “Introduction to Risk Management and Insurance”, Englewood Cliff, N.J., Prentice

Hall, New Delhi, 2002

9. Pranav Prashad, “Catalyst for Financial Inclusion – Insurance in the Rural and Social Sector”, IRDA,

Journal, April, 2009, p.20

10. Seshayyair, V., “Group Life Insurance Business”, Insurance Chronicle, the ICFAI University Press,

March, 2004, pp. 22-26.

11. Srivastava, D.C. and Srivastava, S., (Eds.) “Indian Insurance Industry – Transition and Prospects”, New

Century Publications, New Delhi, 2001

12. Vijaya Kumar, A., “Globalization of Indian Insurance Sector - Issues and Challenges”, The

Management Accountant, March, 2004, p.195

13. Yusuf T.O., Gbadamosi A. & Hamadu D., “Attitudes of Nigerians towards Insurance Services: an

Empirical Study”, African Journal of Accounting, Economics, Finance and Banking Research (2009),

Vol. 4(4), pp. 34-46