powerpoint-presentation€¦ · 1.7 112 exploration assets oman block 3 & 4 34,610 30% cc...

TRANSCRIPT

Q3 2014 4 November 2014

Q3 Highlights

• Record net sales of MSEK 296, up 21% compared to Q2

• EBITDA of MSEK 232, up 21% compared to Q2

• Net result MSEK 167, up 56% compared to Q2

• Earnings per share SEK 4.71 for Q3

• Exploration and appraisal continues:

– New production record each quarter in 2014

– Over 8,000 bopd each month in Q3 2014

– A total of 8 wells completed on Blocks 3 and 4 during Q3

2014

2

Tethys’ assets

Producing

Assets

Country Licence Area,

km2

Tethys

share

Partners* 2P reserves

31 Dec 2013

(mmbo)

Production

Q3 2014

(bopd)

Oman Block 3 & 4 34,610 30% CC Energy, Mitsui 15.2** 8,287

Lithuania Gargzdai 884 25% Odin Energi,

Geonafta

1.7 112

Exploration

assets

Oman Block 3 & 4 34,610 30% CC Energy, Mitsui

Oman Block 15 1,389 40% Odin Energy

Lithuania Rietavas 1,594 30% Odin Energi, Private

investors

Lithuania Raseiniai 1,535 30% Odin Energi, Private

investors

Other

assets

France Attila 1,986 40% Galli Coz

France Alès 215 37.5% Private investors

* Operator in bold

** Not including interim report of Lower Buah reserves as at 30 June 2014

3

Reserves Oman

(31 Dec 2013, mmbo)

1P 2P 3P

Farha South 8.9 11.7 13.5

Saiwan East 0.7 1.3 2.8

Area 4

(Lower Buah) 1.2 2.2 3.7

Total 10.8 15.2 20.0

Reserves Lithuania* (mmbo)

1P 2P 3P

Gargzdai 0.8 1.7 2.8

Reserves Independent petroleum consultant

DeGolyer and MacNaughton

(“D&M”) reviews Tethys Oil’s reserves in

Oman annually.

Following successful drilling during the

first six months of 2014 of the Lower

Buah reservoirs on Block 4, D&M has

delivered an interim report of Lower Buah

reserves as at 30 June 2014.

* As per reserve report 31 Dec 2012, by Miller and

Lents, Ltd., reduced with 2013 year’s production.

Development of the Lower Buah reserves

(30 Jun 2014, mmbo)

1P 2P 3P

Total 31 Dec 2013 1.2 2.2 3.7

Production from Lower

Buah 2014

-0.4 -0.4 -0.4

Revisions/discoveries 1.5 3.2 4.1

Total 30 Jun 2014 2.3 5.0 7.4

4

• Over 8,000 bopd each month in Q3-14

• 16% higher production in Oman compared with Q2-14

• Lithuanian production amounted to 112 bopd in Q3-14

Average daily production in Oman

5

8 239 8 221 8 404

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

July

Augu

st

Septe

mb

er

Octo

be

r

No

ve

mbe

r

De

ce

mbe

r

Janu

ari

Feb

ruary

Ma

rch

April

Ma

y

June

July

Augu

st

Septe

mb

er

Q3-13 Q4-13 Q1-14 Q2-14 Q3-14

6

• Total production in Q3 2014 highest ever

• 75% increase in average daily production compared with Q3-13

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1 800 000

2011 2012 2013

Total production Ave daily production

Production

Barrels Barrels

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

900 000

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Total production Ave daily production

• Record net oil sales of 399,352 barrels

• Underlift position decreased with 2,917 bbl to 27,188 bbl from Q2-14

to Q3-14

Barrels Barrels

7

Sold barrels

147 228

776 248 850 926

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

900 000

2011 2012 2013

Sold volumes

Sold volumes

213 397

271 175

280 782

350 059

399 352

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

Q3 2014 Q4 2014 Q1 2014 Q2 2014 Q3 2014

Sold volumes

Sold volumes

• Net oil sales of MSEK 296 in Q3-14, up 21% compared to Q2-14

• The Q-o-Q sales increase is composed of 14% increase in barrels sold,

5% USD/SEK change and 2% oil price increase

MSEK MSEK

8

Sales MSEK

104

584 592

0

100

200

300

400

500

600

700

2011 2012 2013

Sales of oil and gas

142

193 195

245

296

0

50

100

150

200

250

300

350

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Sales of oil and gas

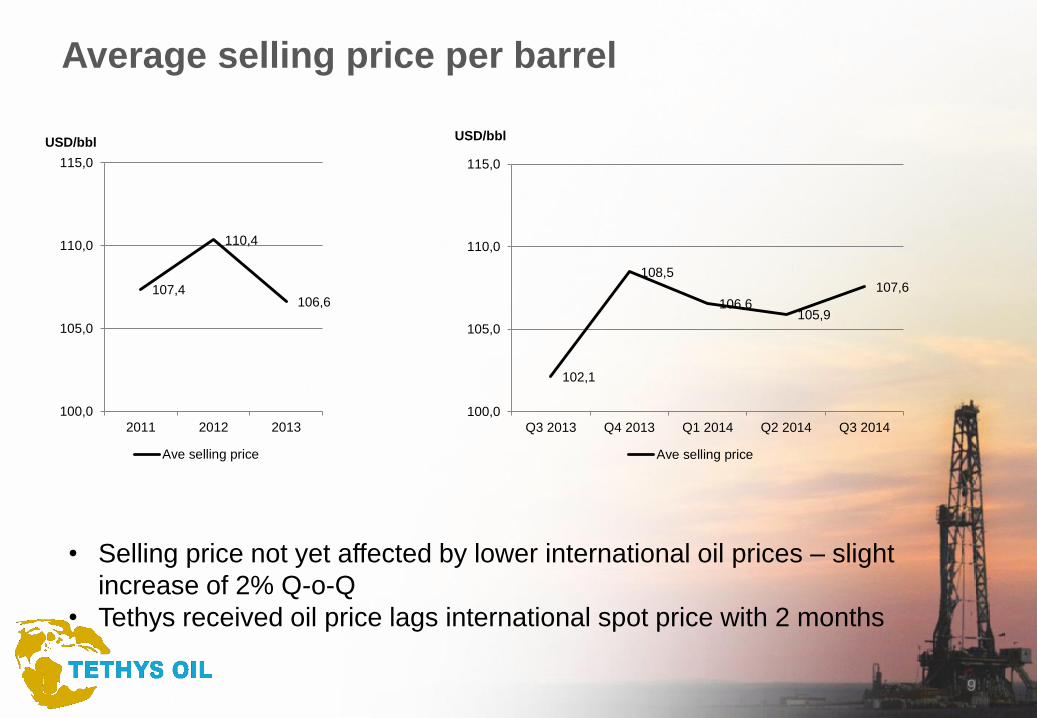

Average selling price per barrel

• Selling price not yet affected by lower international oil prices – slight

increase of 2% Q-o-Q

• Tethys received oil price lags international spot price with 2 months

USD/bbl

107,4

110,4

106,6

100,0

105,0

110,0

115,0

2011 2012 2013

Ave selling price

USD/bbl

9

102,1

108,5

106,6 105,9

107,6

100,0

105,0

110,0

115,0

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Ave selling price

EBITDA

• EBITDA of MSEK 232 in Q3, up 21% compared to Q2-14

• EBITDA margin the last five quarters has been in the range 67%-78%

10

MSEK MSEK

96

148

130

192

232

68%

77%

67%

78%

78%

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

80%

0

50

100

150

200

250

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

EBITDA EBITDA Margin

84

509 479

553

0

100

200

300

400

500

600

2011 2012 2013 9M 2014

EBITDA

Expenses

• Operating expenses increased 24% compared with Q2-14, in line with

the sales development

• Opex in Q1-14 affected by late incoming expenses from 2013

• Most opex is fixed

MSEK MSEK

11

0

96

152

20

28

31

0

25

50

75

100

125

150

175

200

2011 2012 2013

Operating expenses Administrative expenses

42 37

59

46

57

6 8

6

8

8

0

10

20

30

40

50

60

70

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Operating expenses Administrative expenses

Adjusted net back and opex per barrel*

12 * After current government take

• Adjusted for timing differences, net back has been stable around

USD 40-45 per barrel last 5 quarters

• Adjusted opex between USD 10 and 15 per barrel, of which direct

lifting cost accounts for 50-60%

USD/bbl USD/bbl

11,9 14,1

45,5 41,3

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

2012 2013

Opex/bbl (USD/bbl) Netback (USD/bbl)

13,2 14,5 11,0 11,9 10,5

40,0 41,9

44,4 43,2 45,4

0,0

10,0

20,0

30,0

40,0

50,0

60,0

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Opex/bbl (USD/bbl) Netback (USD/bbl)

Net result after tax

• Result is up 56% Q-o-Q mainly due to strong sales development,

lower DD&A per barrel and significantly lower financial expenses

69

314

240

0

50

100

150

200

250

300

350

2011 2012 2013

Result for the period

13

MSEK MSEK

52 45

58

107

167

0

20

40

60

80

100

120

140

160

180

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Result for the period

Balance Sheet Q3 2014

• Strong cash position of MSEK 194

• The MUSD 100 senior revolving reserve based lending facility is not

used by the end of the third quarter

14

(MSEK) 2014-09-30 2014-06-30 2013-12-31

Cash 194 33 295

Long term debt 33* 30* 422

Net debt -161 -3 127

Total assets 1,619 1,367 1,563

Shareholders’ equity 1,547 1,284 1,100

* Provision for site restauration costs

• Majority of investments were development, appraisal and exploration of Blocks 3&4

• Given the below budget investments ( MSEK 164) in relation to full year budget on Blocks 3&4 (MSEK 400) so far during the nine months 2014, it is unlikely that the full budget amount will be invested during 2014

– some infrastructure investments have been pushed forward

– fewer wells due to changes to the drilling programme following new data

15

MSEK MSEK

Oil and gas investments

44

875

290

0

200

400

600

800

1000

2011 2012 2013

Oil and Gas Investments

59

73

45

79

44

0

10

20

30

40

50

60

70

80

90

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Oil and Gas Investments

Wells in Oman

• 8 wells drilled in Q3 2014, including, 2 production wells, 3 wells in

previously undrilled fault blocks, 1 appraisal well and 2 water source

wells

• Exploration well in eastern part of Block 4 completed after Q3

22

37 35

0

5

10

15

20

25

30

35

40

2011 2012 2013

Wells drilled

16

8

10

15

12

8

0

2

4

6

8

10

12

14

16

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Wells drilled

Current activities

17

• Drilling on Raseiniai license

in Lithuania later this year or

early next year

• Farha South water injection

programme nearing

completion

• Exploration/appraisal along

Farha trend

• Exploration well LE-1 in

eastern part of Block 4 under

evaluation

• Further appraisal of Lower

Buah reservoir section

• Central Block 4 seismic study

ongoing

Ongoing 3D

seismic

Ongoing

exploration well

B4EW7

18

Current operations

Lower Buah areas and Saiwan East field (Khufai)

Q3 2014 4 November 2014

Important notice

This presentation and the information contained herein is being presented by Tethys Oil AB (publ) (the “Company”). By attending a meeting where this

presentation is presented, or by reading this presentation, you agree to be bound by the following limitations and notifications.

This presentation does not constitute an offer or invitation to purchase or subscribe for any securities and does not constitute any form of commitment or

recommendation on the part of the Company.

This presentation does not purport to be all-inclusive or to contain all the information that prospective investors may desire in analysing and deciding

whether or not to hold or transact in the Company’s shares.

Recipients of this presentation must rely on their own examination of the legal, taxation, financial and other consequences of any possible holding or

transaction involving the Company’s shares or other securities, including the merits and risks involved. Recipients should not treat the contents of this

presentation as advice relating to legal, taxation or other matters and are advised to consult their own professional advisors concerning the acquisition,

holding or disposal of shares or other securities in the Company.

Certain information contained in this presentation has been obtained from published sources prepared by other parties that the Company has deemed to be

relevant. However, neither the Company nor any other person assumes any responsibility whatsoever and makes no representation or warranty, express

or implied, for the contents of this presentation, including its accuracy, completeness or verification for any other statement made or purported to be made

by any of them, or on their behalf. Nothing in this presentation is, or shall be relied upon as, a representation or promise made, whether as to the past,

present or future. Accordingly, no responsibility is accepted by the Company, its subsidiaries or associates or any of their directors, officers, employees or

agents, in respect thereof.

This presentation contains forward-looking statements that reflect the Company’s current views with respect to certain future events and potential financial

performance. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be

given that such expectations will materialise. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of

various factors. To the extent that this presentation contains opinions, estimates, forecasts or other forward looking statements, no guarantees or

undertakings that these are correct or complete are given by the Company or any of its members, advisors, officers or employees or any other person.

Forecasts and assumptions which are subject to economic and competitive uncertainty are outside such person’s control and no guarantee can be given

that projected results will be achieved or that outcomes will correspond with forecasts. Information in this presentation may be changed, added to or

corrected without advance notification. The Company does not undertake any obligation to publicly update or revise any information contained herein.

This presentation as well as any other information provided by or on behalf of the Company shall be governed by Swedish law. Any dispute, controversy or

claim arising out of or in connection with such information or related matters shall be finally settled by arbitration in accordance with the Arbitration Rules of

the Arbitration Institute of the Stockholm Chamber of Commerce. The place of arbitration shall be Stockholm and the language to be used in the arbitration

proceedings shall be English.

IMPORTANT NOTICE

20