r etail pharmacy business in jordan dr. amjad i. aryan ceo- pharmacy 1 ®

TRANSCRIPT

Retail Pharmacy Business in Jordan

Dr. Amjad I. AryanCEO- Pharmacy 1®

Outline

• Overview• Barriers of Entry• Competition:• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Outline

• Overview• Barriers of Entry• Competition:• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Overview

• The total population in Jordan reached around 5.85 million in 2008.

• Jordan has experienced significant changes in the age structure of its population over the past 20 years.

• The age structure in Jordan exhibits a relatively young population (over 40 percent of the population is 15 years of age or younger).

• The proportion of aged population (65+) also rose from 2.7 percent to 3.9 percent in the last two decades

• Community-based treatment in the community—both acute and chronic—has escalated medication use.

• Higher prescription volumes attributable to a growing elderly population with multiple medications, an increased number of prescription and over-the-counter medications, increased consumer reliance on self-care, have all placed the pharmacist in a more prominent position to provide more information and services to the public.

• Self-medication is a common practice among Jordanians (42.5%).

Overview

Overview

• The healthcare system in Jordan has undergone major changes in the past 10 years. Even though the government and military remain to be two largest providers of healthcare, the private sector has grown significantly.

• In 2007, around 950,000 people (19% of the total population) had private health coverage. In addition, it is expected that the government will privatize the provision of healthcare services within the coming 5 years.

• The average pharmacy in Jordan earned approximately JD80, 000 annually from prescription (Rx) drugs. In

addition, pharmacies offer over-the-counter (OTC) items, cosmetics, medicated cosmetics, health supplies, and other items. Sales of these items is estimated to be JD40,000, which brings the annual average sales per pharmacy to over JD120,000 ( JD10,000/month).

• The distribution of the retail pharmacy sales in Jordan is disproportionate. The city of Amman accounts for about 45% of total retail sales in the country. Zarqa and Irbid account for more than 35% of sales, and the rest of the country account for the remaining 20%.

Overview

• The practice of retail pharmacy in Jordan (as well as the entire region) is changing. Just a few years ago, all of the retail pharmacies in Jordan were owned by a pharmacist, and managed as independent units (independent pharmacies). The activities performed by these pharmacies were restricted to purchasing and selling Rx drugs and a limited selection of OTC items. However, the outlook for retail pharmacy business has changed with the opening of chain pharmacies.

Overview

• Consumers have shown that they value the services provided by the chain-type pharmacy, which was reflected in the financial performance of these chains. This success could be attributed to several reasons, including

– The range of clinical services provided to patients

– Consistency in appearance and services across all locations, (

– Store size,

– Wide range of products.

Collectively, these reasons helped create a brand name that consumers recognized and sought.

Overview

• Based on changes in the structure and dynamics of the health care systems in Middle East and North African (MENA) countries, it is expected that pharmacy practice in the entire region( including Jordan) will transform from solo independent “mom and pop” shops into chain-type pharmacies.

• With this transformation, the key success factors in the retail pharmacy business will also change. The players’ ability to compete on price (current practice) will erode, or be limited to certain segments of the market. Competitiveness will depend more on the ability to offer differentiated services both clinical and clerical, as well as implementing prudent inventory management systems.

Overview

Outline

• Overview• Barriers of Entry• Competition:• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Barriers of Entry

The major barriers of entry:

• Restriction on ownership; only a registered pharmacist or incorporation entity whose shareholders are all registered pharmacist may own a pharmacy.

• Restriction on locations; the distance between pharmacies is 100m-250m depending on the location.

• Outdated laws; the pharmacy law has been in place since 1974

Outline

• Overview• Barriers of Entry• Competition• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

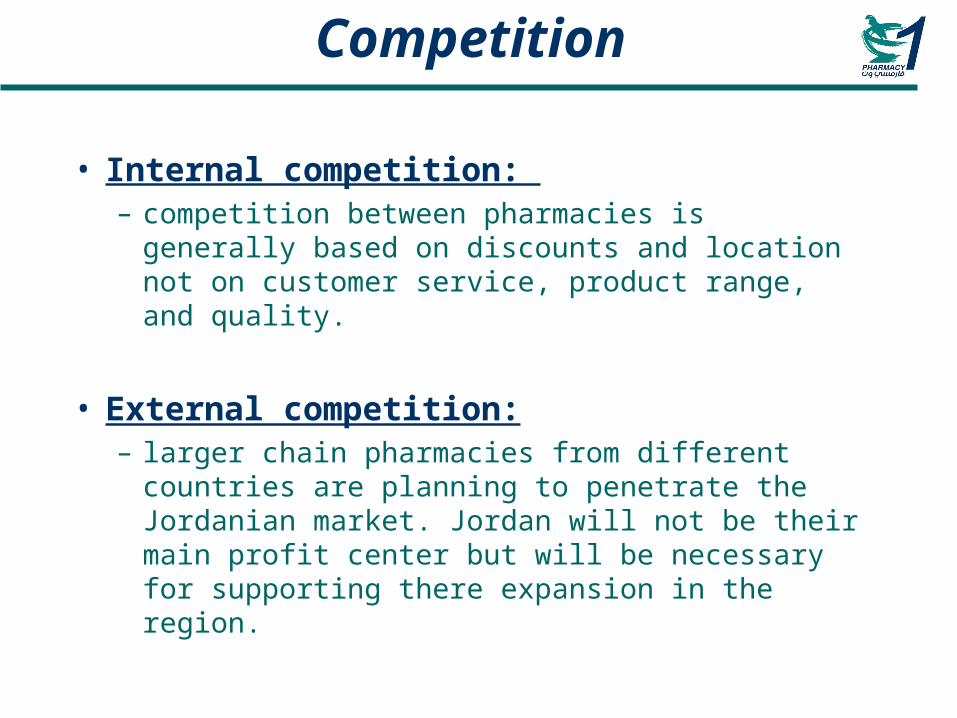

Competition

• Internal competition: – competition between pharmacies is generally based on

discounts and location not on customer service, product range, and quality.

• External competition: – larger chain pharmacies from different countries are

planning to penetrate the Jordanian market. Jordan will not be their main profit center but will be necessary for supporting there expansion in the region.

Competition

• Supermarkets: – big retailers’ area pushing for amending the laws pertaining

to allowing the sale of OTC products and baby milk formulas in supermarkets.

• High acquisition value: – ageing pharmacist tend to view their business as their

superannuation and asking for high sale prices.

• Insurance companies: – will try to sign exclusive agreement with large chains or

establish their own pharmacy change to cut costs.

Outline

• Overview• Barriers of Entry• Competition• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Profits and loss analysis -Revenue

Pharmacies sell three main types of products:

1. Prescription medications

2. Non-prescription medications( OTC)

3. General retail (e.g. vitamins, health and beauty, baby,ect)

• Over 70% of pharmacies revenue comes from the sale of prescription medications.

• The government fixes the prices on prescription medications which is 20.50% of the public price.

• Extra revenues are generated through bulk purchases( bonus)

Profits and loss analysis -Revenue

Profits and loss analysis -Revenue

• The average pharmacy in Jordan has total monthly sales of about JD10, 000 (based on an average annual sale of about JD120, 000).

• The average size of the pharmacy outlet in Jordan is about 40 square meters. Therefore, the average monthly sales per square meter reaches about JD250.

Profits and loss analysis -Revenue

• In the case of chain pharmacies , the average size of an outlet will be about 100 square meters. Therefore, if we apply the national average sales of JD 250 per square meter to chain pharmacies, the average monthly sales per pharmacy outlet is expected to reach about JD25, 000.

Profits and loss analysis –Costs

The initial cost of opening a new outlet includesI. Cost of signing the lease agreement

II. Cost of interior decorations and shelves,

III. Cost of initial stock.

• Fixed costs : (rent, salaries, and cost of support functions) are usually higher for chain-type pharmacy.

• That is because:– The size of the outlet is usually larger than the typical

size of independent pharmacies.

– The number of pharmacists and supporting staff needed to run the individual branches.

– The same applies to overhead and cost of management, as chain pharmacies require larger and specialized management teams.

Profits and loss analysis –Costs

• Variable costs (which largely consist of the cost of goods sold “COGS”) can be significantly reduced in a chain-type pharmacy.

• That can be achieved by

– Establishing centralized purchasing in order to capitalize of the collective size of the business.

– Utilizing computerized systems for inventory management both at the chain as well as branch levels.

Profits and loss analysis –Costs

The following is a detailed set up cost for a Pharmacy in the Jordanian market:

– Initial cost of opening a new location– Fixed costs– Variable costs– Overhead

Profits and loss analysis –Costs

Initial Cost of Opening a New Location

• Interior design, shelves, and computer network: These costs can range between JD20, 000 – JD50, 000.

• COGS depends on the size of the pharmacy and is estimated at JD1000 per square meter depending on the size of the pharmacy( 40 SM pharmacy COGS= JD40,000)

Fixed Costs• Fixed costs include:

rent, salaries, and cost of supporting functions.

– Rent: The average yearly rent for a prime location can range from JD140 – JD500 per square meter per year.

– Pharmacy Staff: An average pharmacy outlet needs 2 pharmacists (one pharmacists for every 8-hour shift), and an office boy. Total monthly salary for the staff equals JD800.

– Supporting Staff: This item include accounting and tax advisor

Variable cost

• Variable cost includes the monthly COGS.

• The gross margin for retail pharmacy is determined by the Jordanian Pharmacist Association, and is fixed at 20.5% of the public price .

• However, pharmacies are usually offered a bonus (free goods) when they purchase products from drug companies and their agents increasing the margin to around 30%.

• Therefore, the cost of inventory in a pharmacy with a total monthly sales of JD10, 000 is estimated at JD7,000 (or 70% of total sales).

Overhead

• Overhead costs in a retail pharmacy setting include the cost of:– Electricity.

– Water.

– License.

– Maintenance.

– Cost of expired items.

– Promotional items.

• These costs depending on the size of the pharmacy can reach JD25 per SM

Outline

• Overview• Barriers of Entry• Competition• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Balance sheet issues

Stock/Inventory Management:

• The stock is generally the most significant physical asset on the balance sheet.

• The ability to manage and control stock is vital to the success of a pharmacy. A good stock control system should be utilized to order stock, reduce inventory costs and increase stock turnover.

• An IT system connecting the pharmacies to suppliers and wholesalers with next day delivery will help reduce pharmacy inventory cost.

Balance sheet issues

Capital /Debt

• Pharmacy value mainly comprises GOODWILL.

• Most suppliers provide pharmacies with limited credit facilities.

Outline

• Overview• Barriers of Entry• Competition• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Taxation

• Large chain pharmacies will follow local taxation laws and will not be able to reduce taxes unlike individual pharmacies.

• This will be an eye opener to the tax authorities which will force the small pharmacy owner to pay the same percentage on sales.

Outline

• Overview• Barriers of Entry• Competition• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Regulations

The pharmacy industry is regulated by several legislations:– The Ministry of Health

– The Jordanian Food and Drug Administration.

– Health Authorities.

– The Jordanian Pharmaceutical association.

– Consumer protection agencies.

Outline

• Overview• Barriers of Entry• Competition• Profits and loss analysis

– Revenue– Costs

• Balance sheet issues:– Stock/Inventory Management:– Capital/ Debt

• Taxation• Regulations:• Industrial Outlook:

– Deregulations– Other factors

Industrial Outlook

Deregulations:

• While the government is coming under increasing pressure from international pharmacy chains, the restrictions on ownership remains.

Other factors

• The ageing Jordanian population and the increase in drug utilization.

• The increase Jordanian population.

• Raising the disposable incomes and increasing health consciousness among consumers.