research market forecast mid-year 2011 - poland

TRANSCRIPT

Accelerating success.

POLAND

RESEARCH & FORECAST REPORT

MID-YEAR 2011

2011 | RESEARCH & FORECAST MID-YEAR REVIEW | POLAND

TABLE OF CONTENTS

Executive summary 3

Economic overview 4

Investment market 5

Land market 6

Industrial market 8

Office market 10

Retail market 12

Key metric definitions 14

3 | COLLIERS INTERNATIONAL

RECENT TRENDS

• Economy: In H1 2011 the Polish economy expanded steadily, despite a slightly

weaker performance recorded in Q2. The GDP is estimated to have grown at a pace

exceeding 4.0%.

• Investment: Poland is still perceived by the international investment community as the

main marketplace in the region. H1 2011 a stabilisation of core yields across all asset

classes was observed in H1 2011. Over 50% of total transaction volume recorded in

the discussed period refered to office investments.

• Land: A continuing trend of buyer‟s domination in the transaction process can be

observed. H1 2011 brought several significant transactions. Investors and developers

have bought land worth EUR 150 million.

• Industrial: H1 2011 resulted in an apparent increase in the number of new warehouse

investments. The transaction volume was about 800,000m². Compared to the first

three months of the year, the transaction volume increased by nearly 7%. Vacancy

rate showed a slight downward trend and at the end of H1 was at 13.3%. Rents in

general remained stable with a slight upward trend.

• Offices: The year so far has been marked by pre-lets. The share of pre-lease

agreements in the total volume of leased space is increasing, which is a sign of a real

revival in the market and its healthy condition.

• Retail: The retail market in Poland saw revival as both developers as well as retailers

presented their expansion plans. In H1 2011 over 250,000m² of retail space was

delivered to the market. Another 400,000m² is planned to be completed by the end of

2011. Increasing supply of modern retail space in secondary cities is facilitating the

expansion of retail chains in regional locations.

MARKET PROGNOSIS

• Economy: The second half of the year will witness a slowdown in the pace of

economic growth. The upcoming months will bring a gradual decrease in both inflation

and unemployment. However, a considerable rise in the number of FDI is expected.

• Investment: It is anticipated that overall activity in 2011 will approach 2010 levels. The

pricing gap between core and non-core assets is expected to increase further in H2

2011.

• Land: As a result of the crisis break in investments, the lack of available dwellings has

influenced a significant recovery in residential developers‟ activity. Developers are now

aiming at large and medium-sized cities. Investment plots intended for shopping malls

and retail parks are of interest to many Polish and foreign companies.

• Industrial: An increase in planned investments can be observed in most markets.

Further growth in demand is predicted, both in Warsaw and in other regions. It is

expected that rents will remain stable with a slight upward trend.

• Offices: Due to a relatively low amount of vacant space in Warsaw‟s non-central

locations tenants may be forced to search for space in buildings within the CBD.

Effective rents in non-central locations may move upwards, whereas they should

remain stable or even slightly decrease in the city centre.

• Retail: Developers are targeting mainly small and medium-sized cities, which still are

not saturated in terms of modern retail space. Top international retail chains will follow

this direction and enter regional markets. Anticipating higher activity from retailers,

rents in prime locations will begin to increase. The trend of tenants switching to the

best retail destinations and newly opened high quality shopping centres will continue.

MARKET INDICATORS

2010* 2011*

GDP GROWTH

UNEMPLOYMENT

WAGES

INFLATION

INVESTMENT VOLUMES

OFFICE RENTS

INDUSTRIAL RENTS

RETAIL RENTS

YIELDS

* COMPARED TO THE PREVIOUS YEAR

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | EXECUTIVE SUMMARY

Executive summary

4 | COLLIERS INTERNATIONAL

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | ECONOMIC OVERVIEW

Source: Central Statistical Office, Ministry of Finance

Source: Central Statistical Office, Ministry of Finance

Source: Central Statistical Office, Ministry of Finance

Economic overview

SUMMARY

• The Polish economy expanded steadily in H1 2011 as the GDP grew at a pace

exceeding 4%. Preliminary estimates show that the economic performance recorded in

Q2 was slightly weaker than in comparison to the previous period, yet the Central

Statistical Office predicts that the GDP will maintain dynamics similar to Q1.

• The GDP growth in Q2 was mainly driven by strong consumer demand and high

dynamics in the construction sector. In comparison to the previous quarter a decrease

in industrial output was reported. An upswing in investment demand recorded in Q1

(6% in a yoy analysis) is expected to be continued in the following quarter.

• As it was expected during H1 2011 an upward trend in the consumer price index was

observed. The inflation rate in Q1 amounted to 3.8% and reached 4.6% in Q2. To

tame the increasing inflation the Monetary Policy Council decided to raise the interest

rates four times throughout the six past months.

• Despite a drop in Q2 (12.2% against 13.1% in Q1 2011), the unemployment rate

remained relatively high during H1 2011. The unemployment rate in June stood at

11.8% and was the lowest value reported during the last six months.

• The average monthly nominal salary in the enterprise sector in June 2011 reached

PLN 3600.47 (EUR 900.11), which was a 5.8% increase in comparison to the same

period of 2010. The average monthly wages in H1 2011 grew by 4.6% in

a yoy analysis.

• The Ministry of Economy estimates that the inflow of foreign direct investments in the

first five months of 2011 amounted to EUR 4.2 bln. Poland remained an attractive

location for investors, thanks to its steady economic and political situation, skilled work

force and competitive labour costs. It is also worth mentioning that during the first six

months of 2011, rising investment activity within the special economic zones was

recorded.

PROGNOSIS

• H2 2011 will witness a slowdown in the pace of economic growth. The National Bank

of Poland estimates that the GDP in 2011 will amount to 4%.

• Analysts predict that the inflation rate will drop during H2 2011.

• The upcoming months will bring a slow decrease in the unemployment rate – mainly

because of increasing seasonal work. Experts predict that unemployment will fall to

11.5% by the end of the year.

• According to the Ministry of Economy the total inflow of foreign direct investment in

2011 might exceed EUR 10 bln. The peak of investors‟ activity is anticipated in the

second half of the year.

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

0

80

160

240

320

400

480

560

GDP Annual ChangeGDP (bln)

0

5

10

15

20

25

UNEMPLOYMENT (%)

0

1

2

3

4

5

INFLATION (%)

Key Economic Figures

GDP Growth 4.2%

Unemployment 12.2%

Inflation 4.6%

5 | COLLIERS INTERNATIONAL

SUMMARY

• Stabilisation of core yields across all asset classes can be witnessed in H1 2011. Any

further movement in pricing is expected to depend largely on the impact of the

sovereign debt crisis.

• Poland is still perceived by the international investment community as the main

marketplace in the region and the liquidity has remained high in H1 2011. It‟s

recognition as a largely „core market‟ in the CEE region has been upheld.

• Approximately EUR 960 million of investment transacted in H1 2011 across all asset

classes. The market has been driven by office investment transactions (53.5% of total

volume), followed by retail (38.5%) and logistics (8%). There have been no hotel

transactions this year to date.

• Austrian (due to the sale of the stake in the Europolis portfolio by CA Immo) and

German investors dominated the market in terms of volume of closed transactions,

followed by UK investors.

• Warsaw has dominated the market in terms of volume, accounting for approx. 83% of

all transactions closed in H1 2011, which translates into EUR 795 mln. Ca. EUR 165

mln of investment product was traded in regional cities, which indicates sustained

liquidity which stretches beyond Warsaw.

PROGNOSIS

• Poland is still on-track to drive the investment volumes in the region, primarily due to

healthy macro-economic dynamics and the availability of product.

• We expect the pricing gap between core and non-core assets to continue to grow

through the second half of this year.

• Investors perceive favourable leasing dynamics and their anticipation of a „supply gap‟

in major cities as one of the main drivers of the market.

• Core funds are expected to continue to dominate the investment landscape for the

medium term, given their ability to conduct “all equity” transactions, or at low leverage

levels.

• Notwithstanding the above, we note that certain funds are approaching their

investments more selectively and may be inclined to sell if the pricing can match their

expectations.

• Stabilisation of core yields in the mid-term continues to be dependent on the

macroeconomic fundamentals of the Euro Zone and the CEE region in the wake of the

sovereign debt crisis.

• As several transactions are currently either in due diligence or are approaching that

stage, we expect that overall transaction activity in 2011 will approach 2010 levels.

Source: Colliers International

Source: Colliers International

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | INVESTMENT MARKET

Key Investment Figures

H1 Investment Turnover EUR 960 mln

Prime Office Yields 6.7%

Prime Retail Yields 6.7%

Prime Industrial Yields 8.0%

Investment market

0

1000

2000

3000

4000

5000

INVESTMENT VOLUME(EUR mln)

0%

2%

4%

6%

8%

10%

12%

14%

PRIME YIELDS

Industrial Retail Office

6 | COLLIERS INTERNATIONAL

GENERAL OVERVIEW

• The land market has started to revive after the crisis. The first signs of this were

transactions concluded in the last few weeks of 2010. A further market upswing was

recorded in the first half of 2011, during which the value of land transactions exceeded

EUR 125 mln.

• Contrary to H2 2010, an increased number of companies with their own or confirmed

debt funds, interested in buying investment land was observed.

• For investment sites with valid Development Conditions or covered by a Local Plan,

the sales process – from offer to the transfer of ownership – extended considerably

over time and can take up to twelve months. In the case of land without Conditions or

a Plan or with documents requiring changes, the process can take up to two years.

• Despite the concluded and pending transactions, today‟s market cannot be compared

to the market before the crisis. The only similarity which can be observed is the unique

investment opportunity to acquire land in a very good location at a reasonable price.

Good investment sites attract several or even a dozen potential investors, whose

financial capabilities and investment potential should be verified.

• Areas well-prepared for the investment process, in terms of technical, legal and

planning are attracting the highest prices. As always, location is a major factor

determining the value.

TRENDS

• The trend of buyers‟ domination continues.

• In terms of transactions, their number is still low due to the continuing difficulty in

financing commercial projects. However, the volume of those concluded is still

impressive.

• Fluctuations in the global economy and turmoil in the European Union are impacting

on the market. This is influencing transactions, leading to reconsideration of offers,

price, and even to postponement of the closure process.

• Sluggishness among some local authorities, particularly in Kraków and Warsaw, in

issuing building permits continues to have a negative impact on the market, and is

prolonging the investment process.

PRICES AND TRANSACTION

• The first half of the year has brought several significant transactions. Investors and

developers have bought land worth EUR 150 million. This volume is impressive,

despite the small number of transactions.

• Prices of investment sites in all sectors have stabilised. This applies both to areas

where the price declines were the greatest, and to those, where prices have reached

their upper level.

• Investment plots intended for shopping malls and retail parks are seeing interest from

Polish and foreign companies. The prices for land suitable for shopping malls in

Warsaw range between EUR 300-600 per m². Outside of Warsaw prices are lower at

around EUR 120-450 per m². Land for retail parks is priced in the range between

EUR 150-190 per m². The price depends on location; local market saturation and the

plot‟s investment potential.

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | LAND MARKET

Land market

TRENDS 2011

Office investment sites

SUPPLY

DEMAND

PRICES

TRENDS 2011

Residential investment sites

SUPPLY

DEMAND

PRICES

TRENDS 2011

Retail investment sites

SUPPLY

DEMAND

PRICES

Source: Colliers International

Source: Colliers International

Source: Colliers International

7 | COLLIERS INTERNATIONAL

Source: Colliers International

Source: Colliers International

PROGNOSIS

• Ongoing negotiations and concluded preliminary agreements may allow the land

market in 2011 to reach a value of EUR 0.3-0.375 billion.

• Land intended for offices in Warsaw, Wrocław and Kraków attract the highest interest.

As for TriCity and Poznań, projects started during the crisis have been

re-established and new transactions may well be on the horizon, although these

markets remain less buoyant than in Warsaw or Wrocław.

• As a result of the hiatus in investments caused by the crisis, the lack of available

dwellings has influenced a significant recovery in residential developers‟ activity.

These developers are focusing on large and medium-sized cities.

• The growth of the tourist market and the upcoming Euro 2012 in Poland, will continue

to contribute significantly to the development of both hotel chains and individual hotel

units. However, the finalised and upcoming transactions are of a lower value

compared to the rest of the real estate market.

LAND DEPARTMENT – ONGOING PROJECTS IN 2011

– SELLER’S REPRESENTATION PORTFOLIO

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | LAND MARKET

PRICES AND TRANSACTIONS

INVESTOR LOCATION

PLOT

SIZE

(ha)

TRANSACTION

VALUE

(mln PLN)

J.W.

Construction

Kasprzaka,

Warsaw

8.1 174

Dom

Development

Powązkowska,

Warsaw

9.9 168

Echo

Investment

Konstruktorska,

Warsaw

7.4 63

Echo

Investment

Hotel Mercure,

Warsaw

n/a 125

PRICES FOR THE OFFICE DEVELOPMENT

SITES (EUR/m² of GLA)

TOWN/ REGION MIN MAX AVERAGE

Warsaw CBD 300 850 575

Kraków 150 350 250

Łódź 100 150 125

Poznań 165 300 233

Upper Silesia 75 150 113

TriCity 100 350 225

Wrocław 100 450 275

Source: Colliers International

PRICES FOR THE RESIDENTIAL

DEVELOPMENT SITES (EUR/m² of PUM)

TOWN/ REGION MIN MAX AVERAGE

Warsaw:

CBD

300 700 500

Warsaw:

outside CBD

140 350 245

Kraków 120 450 285

Łódź 80 200 140

Poznań 80 300 190

Upper Silesia 60 200 130

TriCity 100 300 200

Wrocław 130 350 240

CLIENT PROJECT FUNCTIONPLOT SIZE

(ha)

INVESTMENT

POTENTIAL (m²)

ASKING

PRICES

(mln PLN)

FSO SA Toruńska, Warsaw Commercial 6.00 50,000 38

FSO SAŻerański Chanel,

WarsawMixed-use 8.26 50,000 47

FSO SA Falenica, Warsaw Residential 2.80 25,000 12

KCI SA Poznańska, Kraków Residential 2.50 33,000 n/a

KCI SA Rybitwy, Kraków Commercial 14.80 n/a n/a

Sita Suez Group Brzezińska, Łódź Residential 11.00 n/a 12

Sita Suez Group Darwina, Kraków Residential 1.80 n/a 5

IGD Silesia Sp. z o.o. Bukowińska, Warsaw Residential 0.60 21,500 45

IGD Mokotów Sp. z o.o.Emerald Tower,

WarsawOffice 0.40 20,000 45

BRJ InvestmentBeethovena II,

WarsawOffice 0.91 16,000 34

BP Investment Beethovena I, Warsaw Office 4.41 n/a 70

Hala Koszyki Savleigh Hala Koszyki, Warsaw Mixed-use 0.94 20,000 48

Metsa Tissue/Konstans Konstancin-Jeziorna Mixed-use n/a 120,000 n/a

Mor Eden Towers Grzybowska, Warsaw Residential 0.60 26,850 72

Drewnica DevelopmentShipyard City Gdańsk,

GdańskMixed-use 20.20 230,000 136

Vantage DevelopmentPromenady

Wrocławskie, WrocławMixed-use 15.10 n/a n/a

Nowe Ogrody 4 Sp. z

o.o.

Droga Męczenników

Majdanka, LublinResidential 6.90 75,600 65

Source: Colliers International

8 | COLLIERS INTERNATIONAL

Source: Colliers International

Source: Colliers International

GENERAL OVERVIEW

• The first half of 2011 saw an apparent increase in the number of new warehouse

investments. In the first two quarters, almost 140,000 m² was delivered through ten

projects, of which over 75% was supplied to the market in Q2. The total supply of

warehouse space in Poland at the end of H1 2011 was approximately 6.5 million m².

Currently, around 347,000 m² of modern warehouse space is under construction.

• In the first half of 2011 the transaction volume was about 800,000 m², of which over

51% was signed in Q2. Compared to the first three months of the year, transaction

volume increased nearly by 7%. More than 64% of the total transactions were new

contracts, with the remaining 36% being renegotiations and expansions.

• Vacancy rate showed a slight downward trend and, at the end of Q2 2011, was at

13.3%.

• Rents for warehouse space in general remained stable. An increase in rental rates

was observed in the regions with a low level of available space such as in Kraków,

Poznań and Upper Silesia.

SUPPLY

• Warsaw – the total supply of warehouse space in Warsaw‟s three zones at the end of

Q2 2011 amounted to nearly 2.5 million m² (compared to Q1, the supply has increased

by over 48,000m²). More than 65.8% of warehouse space is located in Zone II. At the

end of Q2, over 26,000 m² of modern warehouse space (Zone I and II) was under

construction, with 1.2 million m² in the planning stage of which 61% is in Zone II.

• Central Poland – the total supply of warehouse space at the end of Q2 amounted to

more than 930,000m². Just one project has been delivered to the market – Tulipan

Park Łódź, comprising the so-called ”small business units”, offering small warehouse

modules. Currently, about 22,000m² of industrial area is under construction.

• Poznań – warehouse space in H1 2011 increased by nearly 21,500m². Two buildings

in Panattoni Park Poznań I were completed. The existing supply has now increased to

almost 824,000m², while projects under construction constitute about 54,500m².

• Upper Silesia – current supply is more than 1.23 million m² and this remains the

second largest warehouse market in Poland. Currently, over 80,000m² of warehouse

space is under construction.

• Kraków – in terms of existing supply Kraków is one of the smallest warehouse markets

in Poland. The existing supply as of the end of H1 of 2011 amounted to slightly more

than 81,000m². In the first half of the year over 13,000m² of modern warehouse space

was delivered to the market.

• Wrocław – the total supply of modern warehouse space exceeded 617,000m². At the

end of Q2 around 67,000m² was under construction

• Gdańsk – the total stock of warehouse space at the end of H1 2011 was approximately

134,000m².

• Toruń – currently, the total supply of warehouse space is 95,600 m². Only one project

with an area of 1,100m² is under construction, while at the planning stage, there is

around 100,000m².

• Szczecin – Szczecin remains Poland‟s smallest warehousing market. Overall supply at

the end of H1 amounted to less than 42,000m².

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | INDUSTRIAL MARKET

Industrial market

TRENDS 2011

SUPPLY

DEMAND

RENTS

VACANCY

39%

8%18%

4%

4%

2%

24%

1%

DEVELOPERS MARKET SHARE BY EXISTING SUPPLY

ProLogis SEGRO

Panattoni MLP

Europolis PointPark Properties

Other Goodman

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

TOTAL SUPPLY BY REGIONS

9 | COLLIERS INTERNATIONAL

Source: Colliers International

Source: Colliers International

DEMAND

• Warsaw – the demand for warehouse space in H1 2011 was relatively high. Nearly

371,000m² of warehouse space was leased, which represented 43% of the total

transaction volume in Poland. Most of the lease agreements were signed in Zone I –

over 184,000m².

• Central Poland – total leased space in amounted to 78,800m², of which approximately

77% was leased in Q2.

• Poznań – rented space in H1 reached the level of over 70,000m², of which more than

56% was leased in Q1.

• Upper Silesia – in the first six months of 2011, 32 leases for a total area of over

159,000m² were signed. In terms of transaction volume, Upper Silesia ranks second

after Warsaw.

• Kraków – five leases for 28,000m² were signed. The majority of them in Q2.

• Wrocław – in H1 2011, 14 lease agreements were signed for a total area of over

84,000m²

• Gdańsk – in the period from January to June 2011 nearly 25,000m² was leased.

• Szczecin – the market here observed limited tenant activity. There were just two

contracts signed during the first half of the year for a total area of 9,000m².

• Toruń – in H1 2011, there were no lease transactions due to the lack of availability of

warehouse space in this market.

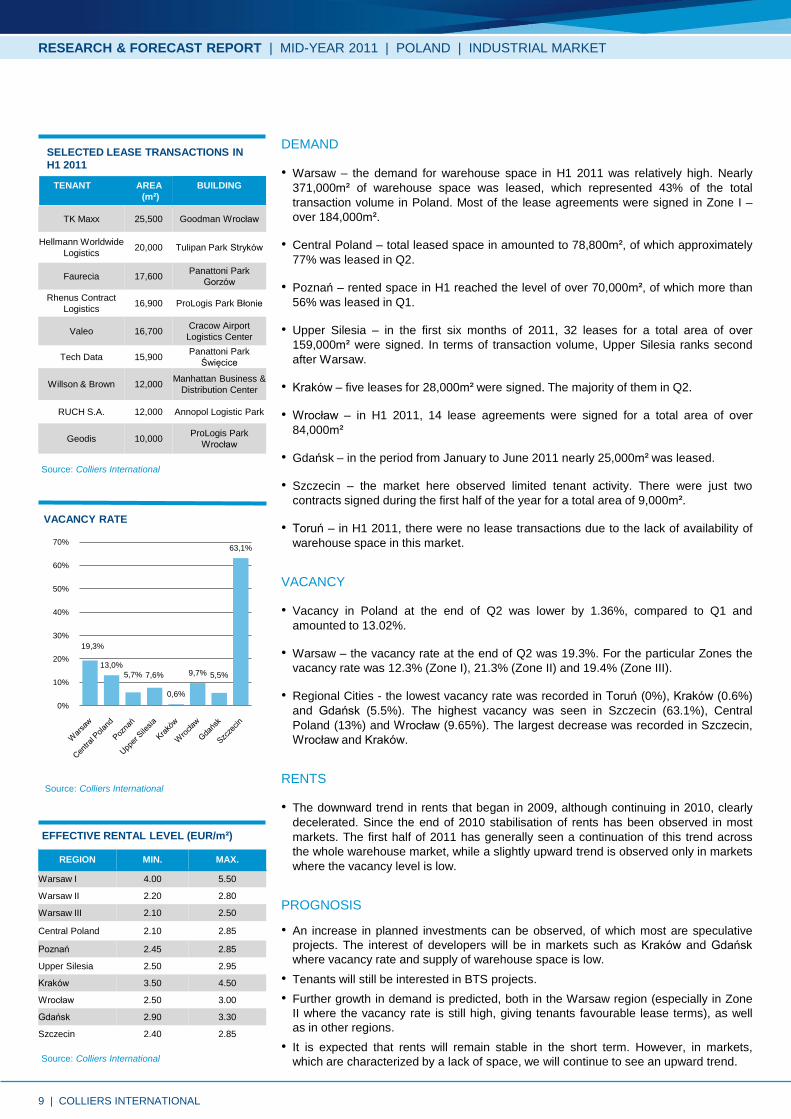

VACANCY

• Vacancy in Poland at the end of Q2 was lower by 1.36%, compared to Q1 and

amounted to 13.02%.

• Warsaw – the vacancy rate at the end of Q2 was 19.3%. For the particular Zones the

vacancy rate was 12.3% (Zone I), 21.3% (Zone II) and 19.4% (Zone III).

• Regional Cities - the lowest vacancy rate was recorded in Toruń (0%), Kraków (0.6%)

and Gdańsk (5.5%). The highest vacancy was seen in Szczecin (63.1%), Central

Poland (13%) and Wrocław (9.65%). The largest decrease was recorded in Szczecin,

Wrocław and Kraków.

RENTS

• The downward trend in rents that began in 2009, although continuing in 2010, clearly

decelerated. Since the end of 2010 stabilisation of rents has been observed in most

markets. The first half of 2011 has generally seen a continuation of this trend across

the whole warehouse market, while a slightly upward trend is observed only in markets

where the vacancy level is low.

PROGNOSIS

• An increase in planned investments can be observed, of which most are speculative

projects. The interest of developers will be in markets such as Kraków and Gdańsk

where vacancy rate and supply of warehouse space is low.

• Tenants will still be interested in BTS projects.

• Further growth in demand is predicted, both in the Warsaw region (especially in Zone

II where the vacancy rate is still high, giving tenants favourable lease terms), as well

as in other regions.

• It is expected that rents will remain stable in the short term. However, in markets,

which are characterized by a lack of space, we will continue to see an upward trend.

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | INDUSTRIAL MARKET

TENANT AREA

(m²)

BUILDING

TK Maxx 25,500 Goodman Wrocław

Hellmann Worldwide

Logistics 20,000 Tulipan Park Stryków

Faurecia 17,600Panattoni Park

Gorzów

Rhenus Contract

Logistics 16,900 ProLogis Park Błonie

Valeo 16,700Cracow Airport

Logistics Center

Tech Data 15,900Panattoni Park

Święcice

Willson & Brown 12,000Manhattan Business &

Distribution Center

RUCH S.A. 12,000 Annopol Logistic Park

Geodis 10,000ProLogis Park

Wrocław

SELECTED LEASE TRANSACTIONS IN

H1 2011

REGION MIN. MAX.

Warsaw I 4.00 5.50

Warsaw II 2.20 2.80

Warsaw III 2.10 2.50

Central Poland 2.10 2.85

Poznań 2.45 2.85

Upper Silesia 2.50 2.95

Kraków 3.50 4.50

Wrocław 2.50 3.00

Gdańsk 2.90 3.30

Szczecin 2.40 2.85

EFFECTIVE RENTAL LEVEL (EUR/m²)

Source: Colliers International

19,3%

13,0%

5,7% 7,6%

0,6%

9,7% 5,5%

63,1%

0%

10%

20%

30%

40%

50%

60%

70%

VACANCY RATE

10 | COLLIERS INTERNATIONAL

OVERVIEW

• The first half of 2011 saw modest supply of new office space coming to the Polish

market. Slightly over 95,000 m2 of office space was completed both in Warsaw and in

the 8 main regional markets. This amount of space constitutes only 37% of new supply

delivered in H1 2010.

• Leasing activity remains at a high level. Increasing demand for office space combined

with the modest supply is pushing vacancy rates downwards in Warsaw and in all

regional markets.

• Tenants act with greater confidence with respect to the future of their business

activities and they are attempting to secure large space units at favourable lease

conditions.

• 2011 so far is marked by pre-lets. The share of pre-lease agreements in the total

volume of leased space is increasing, which is a sign of a real revival in the market

and its healthy condition.

SUPPLY

• Warsaw – the total stock of office space grew insignificantly in H1 2011. Thanks to

completion of 28,353m2 within four office schemes it amounted to 3,505,035m2.

Two office projects were completed in the Upper South Zone (Mokotów) – Platinium IV

(13,000m2) and Racławicka Point (1,918m2) and two other projects were completed in

the City Centre – Pałac Młodziejowskiego (4,964m2) and Mokotowska Square

(8,471m2). Currently ca 115,000m2 of office space is under construction for delivery

before the year end. The largest amount of space will be completed in the CBD and in

the Upper South Zone.

• Regional cities – the total stock of regional markets grew by almost 68,000 m2 during

the first half of the year. The largest increase in total stock was recorded in Kraków,

where almost 26,400m2 was delivered onto the market with, among others, two

buildings of Bonarka4Business (15,694m2) and the first phase of the Green Office

scheme (8,000m2). Lublin saw the second largest new supply among regional

markets, as 13,500m2 of office space was completed within the Gray Office Park A.

The TriCity was third thanks to delivery of the Allcon Park 3 (9,116m2). At the end of

June 2011 almost 90,000m2 of office space was under construction, and planned for

delivery in 2011.

DEMAND

• Warsaw – mid-year take-up in the Warsaw market surpassed 320,000m2, which in

comparison with the results recorded in H1 2010 constitutes a 46% increase.

35% of leasing activity in H1 took place in the central locations. Among non-central

locations the Upper South Zone enjoyed the most popularity and its share in the total

volume of leased space amounted to 32%. The majority of lease transactions were

concluded for lease of small units below 1,000 m2. The average deal size for the

period was 1,063m2. Nine lease agreements surpassed 5,000m2. In comparison with

H1 2010 the share of renegotiations and renewals in the total volume of leased space

decreased by 6 pp and was at the level of 30%, whereas the share of pre-lets

significantly increased (25% against 5% in the same period of 2010). The largest

agreements include 43,500m2 pre-leased by TP SA and 11,000m2 renewed by Ernst

& Young in Rondo 1.

• Regional cities – slowly but steadily regional markets are regaining their importance. In

H1 2011 transactions surpassing 155,000m2 took place, with the largest leasing

activity recorded in Kraków (almost 50,000m2) and Poznań (over 30,000m2). The

majority of transactions were new agreements. Renegotiations and renewals

constituted 27% of the total recorded take-up and pre-lets had a 26% share in the total

volume of leased space. H1 2011 was characterised by a high leasing activity

performed by tenants from the BPO sector.

Source: Colliers International

Source: Colliers International

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | OFFICE MARKET

Office market

CITY TOTAL STOCK (m2) VACANCY (%)

Warsaw 3,505,035 6.2

Kraków 414,420 11.7

Wrocław 311,330 4.3

Poznań 195,580 11.3

TriCity 225,180 14.6

Katowice 184,730 19.3

Łódź 181,590 22.3

Lublin 61,980 10.5

Szczecin 43,060 4.4

Source: Colliers International

TRENDS 2011

SUPPLY

DEMAND

RENTS

VACANCY

KEY OFFICE FIGURES

H1 2011

6%

30%

39%

25%

Expansions

Renewals & Renegotiations

New agreements excluding pre-lets

Pre-let agreements

TAKE-UP COMPOSITION

TAKE-UP (in thous. m2)

0

50

100

150

200

250

300

350

2008 H1

2008 H2

2009 H1

2009 H2

2010 H1

2010 H2

2011 H1

11 | COLLIERS INTERNATIONAL

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | OFFICE MARKET

The largest agreements include 16,000m2 renewed by Shell in KBP 400 in Kraków,

14,600m2 pre-leased by Grupa Allegro in Pixel in Poznań and 11,500m2 preleased by

Infosys BPO Poland in Green Horizon in Łódź.

VACANCY

• Warsaw – the average vacancy rate for the city as a whole has been decreasing for

the last twelve months and at the end of H1 2011 stood at 6.17%. The vacancy rate in

the CBD, which was growing since the end of 2008, has stabilized above 8%. In non-

central locations, due to the small amount of new supply, the vacancy rate continues to

drop. At the end of H1 2011 it stood at 5.2%.

• Regional cities – vacancy rates range from 4.3% in Wrocław to 22.3% in Łódź. In

comparison with rates recorded at the end of 2010 and in Q1 2011 almost all cities

recorded a decrease in the amount of vacant offices. This can be attributed to the high

leasing activity recorded in H1 2011 and very limited supply of new office space.

RENTS

• Warsaw – asking rents remain stable with the average at the level of ca. EUR 21.5

/m2 per month in the CBD and EUR 15.5 /m2 per month in non-central locations. Due

to the relatively high amount of unleased space in the central area some office

buildings in the CBD offer space in the range of EUR 16-19 /m2 per month. A-class

buildings in prime locations leased to a high degree offer space at even EUR 25-28

/m2 per month.

• Regional cities – rental rates generally continue to range between EUR 12 and

15 /m2 per month. Lowest asking rates remain in Katowice and Łódź, and the highest

in Poznań and Wrocław.

PROGNOSIS

• Due to a relatively low amount of vacant space in Warsaw‟s non-central locations

tenants may be forced to search for space in buildings within the CBD.

• Delivery of further schemes in the central area which remain vacant to a high degree,

may result in a further increase in vacancy rates for CBD.

• Effective rents in non-central locations may move upwards, whereas they should

remain stable or even slightly decrease in the city centre.

• Pre-lease agreements will continue to be popular among tenants as a means of

securing space in desired locations at favourable conditions.

• As regards regional markets, new supply scheduled for delivery in H2 2011 will be

higher than the amount of space which entered the market in H1 2011. If demand for

space remains at the current level, this new supply will allow for further stabilisation in

most markets.

• TriCity will experience the largest increase among regional markets and may

experience a significant growth in vacancy rates. In order to attract tenants landlords

may offer more favourable leasing terms.

SELECTED LEASE TRANSACTIONS

IN H1 2011

TENANT SIZE (m2) BUILDING

TP SA Pre-lease: Miasteczko

TP / Warsaw 43,700

Shell

Renegotiation/

renewal: KBP 400 /

Kraków16,000

Grupa AllegroPre-lease:

Pixel / Poznań

14,600

Infosys BPO

Poland

Pre-lease: Green

Horizon /

Łódź 11,500

Ernst & Young

Renegotiation/

renewal: Rondo 1 /

Warsaw11,000

SABRERenewal + expansion: Buma Square

/ Kraków8,900

Frontex Renewal + expansion: Rondo 1 /

Warsaw8,800

Rabobank

Group

Pre-lease: Senator /

Warsaw2,840

Source: Colliers International

VACANCY RATE IN CENTRAL AND

NON-CENTRAL LOCATIONS

Source: Colliers International

CITYMIN.

(EUR/m2)

MAX.

(EUR/m2)

Warsaw

CBD 19.0 24.0

Warsaw

outside CBD13.0 16.0

Kraków 12.0 15.0

Wrocław 13.5 15.5

Poznań 14.5 16.5

TriCity 13.5 15.0

Katowice 12.0 13.5

Łódź 11.0 12.5

Source: Colliers International

AVERAGE ASKING RENTS

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2008 H1

2008 H2

2009 H1

2009 H2

2010 H1

2010 H2

2011 H1

Central Non-central

12 | COLLIERS INTERNATIONAL

GENERAL OVERVIEW

• The retail market in Poland revived in the first half of 2011, both on the supply and

demand side.

• Developers are returning to the market by presenting their expansion plans for the

coming years. In the first half of 2011 over 250,000 m² of retail space was delivered to

the market, which is a 13% increase yoy.

• The first half of 2011 can be described as moderately optimistic in terms of retailers‟

activity on the Polish market. One of the reasons is quite good economic conditions,

and in June 2011 retail sales in Poland increased by 10.9% yoy. Moreover, there are

still many potential locations which are seeing interest from retail chains. There were

also some new entries by brands which were yet not present on the Polish retail

market.

SUPPLY

• The total supply of modern retail stock in Poland amounted to almost 8.22 million m² at

the end of H1 2011.

• More than 60% of the stock is located in the eight main Polish agglomerations, which

translates into approximately 5 million m².

• Warsaw, the biggest Polish retail market, at the end of H1 2011 offered over 1.42

million m² of modern retail space, of which 78% is constituted by shopping centres.

• In the first half of 2011 more than 250,000m² of retail space was delivered on the

Polish market. The major projects completed in this time are: Galeria Słoneczna in

Radom (42,000m²), Turawa Park in Opole (41,000m²), Galeria Twierdza in Zamość

(27,500m²) and Galeria Leszno (32,000m²).

• Over 700,000m² of retail space is currently under construction in Poland. The majority

of this is located in small and medium-sized cities.

DEMAND

• Retailers are more eager to develop their chains, especially by entering regional

markets. There is still a big gap in terms of the brands present in medium-sized cities.

• Increasing supply of modern retail space in secondary cities is facilitating the

development of regional markets on the demand-side. Many top international brands,

present only in major Polish cities up to now, are opening their stores in smaller cities.

This is possible due to completion of modern retail schemes, suitable for their

expectations.

• In terms of new entries in the first half of 2011 the Polish market saw the arrival of

international fashion brands. Dorothy Perkins, Redgreen, Lindex, and a lingerie brand

from Serbia – Extreme Intimo in Manufaktura, Łódź. In addition, two international

childrens brands opened their first Polish store: Catimini in Stary Browar, Poznań and

the Australian Groovy Kids brand in Reduta Shopping Centre, Warsaw.

• A new national brand – Harpers Shoes – offering well-known international shoe

brands was established in Poland in H1 2011 and is planning to open as many as 10

new stores by the end of 2011.

Source: Colliers International

Source: Colliers International

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | RETAIL MARKET

Retail market

0

1

2

3

4

5

6

7

8

9

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

EVOLUTION OF RETAIL STOCK IN POLAND

Annual Supply Total Supply

mln m²m²

TRENDS 2011

SUPPLY

DEMAND

RENTS

VACANCY

MAIN RETAIL SCHEMES PLANNED

TO BE DELIVERED IN H2 2011

CITY PROJECT DEVELOPERSIZE

(m²)

KielceCH Echo

(extension)

Echo

Investment41,500

Rzeszów Millenium HallDevelop

Investment52,000

SzczecinGaleria

KaskadaECE 43,000

Toruń Toruń Plaza Plaza Centers 33,000

Ostrów

Wlk.

Galeria

Ostrovia

Saller Group

West

Investment

37,000

Kalisz Galeria TęczaEF Rank

Progress17,500

13 | COLLIERS INTERNATIONAL

VACANCY

• Vacancy levels in 8 major Polish agglomerations range between 0.5-3%.

• The lowest rates are recorded in Szczecin (0.52%) and Warsaw Agglomeration

(0.78%), while the highest vacancy level is noted in TriCity Agglomeration (almost 3%).

RENTS

• In the last few months a slight increase in rents has been observed in selected

locations, especially in the best shopping centres in major Polish cities.

• The highest rental levels are invariably recorded in Warsaw and Kraków. Prime rents

for units up to 100m², leased by fashion retailers can reach EUR 80 /m2 per month in

the best shopping centres in Kraków and EUR 90 /m2 per month in Warsaw.

• Rental levels in shopping centres in Warsaw range between EUR 70-90 /m2 per month

for units of 100m², in regional cities rents these are approximately 40% lower.

• In terms of the best high street locations Warsaw and Kraków are still the leaders. The

rents have remain unchanged and range between EUR 75-95 /m2 per month. Far

lower levels are recorded in Łódź (Piotrkowska Street) or Katowice (3 Maja Street),

where shopping centres attract the majority of retailers at the expense of high street

development.

PROGNOSIS

• In Poland developers‟ activity is significant, and over 700,000m² of retail space is

currently under construction. Developers are aim mainly at small and medium-sized

cities, which still are not saturated in terms of modern retail space.

• By the end of 2011 it is expected that total retail stock will reach 8.6 mln m², as few big

retail schemes are planned to be delivered on the Polish market, e.g. Millenium Hall in

Rzeszów, Galeria Kaskada in Szczecin or Toruń Plaza.

• Retailers‟ activity is likely to increase. The macro situation in Poland is favourable and

retail chains will try to find possible gaps, especially on the markets in medium-sized

cities.

• The trend of retailers switching to the best newly opened retail schemes and high

quality existing shopping centres will continue.

• The vacancy rate should remain mostly unchanged. It will most likely fall in the best

shopping centres, which are targeted by retail chains, but increasing supply will offer

new retail space and stabilise the situation.

• Regarding retailers‟ activity, rental levels are expected to rise slightly, but this is

expected to be focused on the best retail destinations in major Polish cities.

Source: Colliers International

Source: Colliers International

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | RETAIL MARKET

SELECTED LEASE TRANSACTION

IN H1 2011

TENANT AREA

(m²)

LOCATION

Rossmann 1,350 Manufaktura, Łódź

Intermarché 2,800 Galeria Leszno

VIP Collection 130 Złote Tarasy, Warsaw

TK Maxx 2,870 RP Matarnia, Gdańsk

Catimini 56 Stary Browar, Poznań

Parfois 105 Krupówki, Zakopane

Massimo Dutti 420 Wzgórze, Gdynia

Groovy Kids 110 Reduta, Warsaw

United Colors of

Benetton123 Janki, Warsaw

0%

1%

2%

3%

VACANCY LEVELS IN MAJOR POLISH AGGLOMERATIONS

This publication does not necessarily deal with every

important topic nor cover every aspect of the topics with

which it deals. It is not designed to provide legal or other

advice.

Key metric definitions

• Prime Headline Capital Value (derived): This is a calculation of market value derived

from the annual prime headline rent divided by the prime (net initial) yield.

• Prime Net Initial Yield: The yield an investor is prepared to pay to buy a Grade A

building, fully-let to high quality tenants at an open market rental value in a prime

location. Lease terms should be commensurate with the market. As a calculation Net

Initial Yield = first years‟ net income/purchase price (prior to deducting fees and taxes)

• Prime Headline Rent: Represents the top open-market tier of rent that could be

expected for a unit of standard size commensurate with demand, of the highest quality

and specification in the best location in the market at the survey date. This should

reflect the level at which relevant transactions are being completed at the time but

need not be exactly identical to any of them, particularly if deal flow is very limited or

made up of unusual one-off deals. If there are no relevant transactions during the

survey period, the quoted figure will be more hypothetical, based on expert opinion of

market conditions, but the same criteria on building size and specification will apply.

• Prime Net Effective Rent: Prime Net Effective Rent is the lowest rent payable, based

on a calculation of the Prime Headline Rent, less the monetary equivalent of the

highest of either the rent-free period or fit-out contribution available at the time of the

survey date.

• Average Headline Rent: Average Headline Rent represents the average open-market

tier of rent that could be expected for a unit of standard size commensurate with

demand, based on a blend of Grade A & B space across a range of locations in the

market at the survey date.

• Total Competitive Stock: Includes the gross leasable floor space in all A and B class

buildings.

• Space Under Active Construction: Represents the total amount of gross leasable

floor space of properties where construction has commenced on a new development

or in existing properties where a major refurbishment/renovation is ongoing at the

survey date.

• Space Under Construction – Inactive: Represents the total amount of gross

leasable floor space of properties where construction had started/where a major

refurbishment/renovation was ongoing, but activity has since stopped for a period of 3

months or longer.

• Vacant Space: The total gross leasable floor space in existing properties that meet

the Competitive Stock definition, which is physically vacant and being actively

marketed at the survey date. Space should be available for immediate occupation.

COLLIERS RESEARCH

Colliers Research Services Group is recognized as a knowledge leader in the

commercial real estate industry, providing clients with valuable market intelligence to

support business decisions. Colliers research analysts provide multi-level support across

all property types, ranging from data collection to comprehensive market analysis.

Across the CEE-SEE-Russia region of EMEA, Colliers researchers regularly collect and

update data on key real estate metrics, set to consistent definitions. This information is

constantly managed using databases, enabling staff to readily produce analysis on key

regional markets including supply, demand, absorption, pricing and transaction data on

capital markets and the office, industrial and retail sector. In most CEE-SEE-Russian

markets, the office definitions used are consistent with those set out by the CEE

Research Forum – an umbrella group, of which Colliers is a founding member -

established to ensure consistent research methodologies are used, bringing greater

transparency and reliability to the analysis of real estate markets in the region.

512 offices in

61 countries on

6 continents

United States: 125

Canada: 38

Latin America: 18

Asia Pacific: 214

EMEA: 117

• $1.5 billion in annual revenue

• 978.6 million square feet under

management

• Over 12,500 professionals

CONTACT:

Research & Consultancy

Dominika Jędrak

Director

Mobile: + 48 666 819 242

Email: [email protected]

COLLIERS INTERNATIONAL POLAND

Pl. Piłsudskiego 3

00-078 Warsaw

Tel. + 48 22 331 78 00

www.colliers.com

RESEARCH & FORECAST REPORT | MID-YEAR 2011 | POLAND | KEY METRIC DEFINITIONS

www.colliers.com

Accelerating success.www.colliers.com