responsible debt collection in emerging markets

TRANSCRIPT

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 1/44

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 2/44

Copyright © International Finance Corporation 2012. All rights reserved.2121 Pennsylvania Avenue, N.W.Washington, D.C. 20433www.i c.org

The material in this work is copyrighted. Copying and/or transmitting portions or all o this work without permission may be a violation o applicable law.IFC encourages dissemination o its work and will normally grant permission to reproduce portions o the work promptly, and when the reproduction is oreducational and non-commercial purposes, without a ee, subject to such attributions and notices as we may reasonably require.

IFC does not guarantee the accuracy, reliability or completeness o the content included in this work, or or the conclusions or judgments described herein, and

accepts no responsibility or liability or any omissions or errors (including, without limitation, typographical errors and technical errors) in the content whatsoeveror or reliance thereon. The boundaries, colors, denominations, and other in ormation shown on any map in this work do not imply any judgment on the part oThe World Bank concerning the legal status o any territory or the endorsement or acceptance o such boundaries. The ndings, interpretations, and conclusionsexpressed in this volume do not necessarily refect the views o the Executive Directors o The World Bank or the governments they represent.

The contents o this work are intended or general in ormational purposes only and are not intended to constitute legal, securities, or investment advice, anopinion regarding the appropriateness o any investment, or a solicitation o any type. IFC or its a liates may have an investment in, provide other advice orservices to, or otherwise have a nancial interest in, certain o the companies and parties (including named herein).

All other queries on rights and licenses, including subsidiary rights, should be addressed to IFC’s Corporate Relations Department, 2121 Pennsylvania Avenue,N.W., Washington, D.C. 20433.

International Finance Corporation is an international organization established by Articles o Agreement among its member countries, and a member o the WorldBank Group. All names, logos and trademarks are the property o IFC and you may not use any o such materials or any purpose without the express writtenconsent o IFC. Additionally, “International Finance Corporation” and “IFC” are registered trademarks o IFC and are protected under international law.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 3/44

Acknowledgement

The report “Responsible Debt Collection in Emerging Markets” was developed within IFC’s Access to Finance Global R isk Management Advisor Program nder the overall g idance of Panos Varangis and with the s pport of team members Sh ndil Selim, Davorka Rzehak andRisserne Gabdibe.

We wo ld partic larl like to thank the team at Oliver W man led b David Bergeron andMatthew Sebag-Monte ore, commissioned by IFC to produce this study report. Oliver Wymanis a leading global management consulting rm that combines deep industry knowledge withspecialized e pertise in strateg , operations, risk management, organizational transformation,and leadership development.

The team wo ld like to acknowledge the contrib tion of IFC’s internal peer reviewers:Garth Bedford, Joseph J lia, Inho Lee and Ferdinand T istra.

IFC’s Access to Finance Global Risk Management Advisor Program wo ld also like toacknowledge and thank the Government of the Netherlands for their contrib tion andpartnership in the program and report.

Last, b t not least, this report wo ld not be possible witho t the contrib tion of the st d ’sparticipants incl ding instit tions within IFC’s own client network – a special thank o to allthe nancial institutions globally for their invaluable time and insights into this important study.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 4/44

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 5/44

contents

Acknowledgement

1. E ec tive S mmar 1

2. Introd ction 3

3. Overview of the St d 53.1. What is responsible nance? 5

3.2. Collections in emerging markets 6

4. Approach and methodolog 9

5. Ke observations 11

5.1. Ind str and geographical trends 11

5.2. Polic setting 12

5.3. Borrower contact 14

5.4. H man reso rce management 17

5.5. Monitoring and complaint handling s stems 20

6. Recommendations 23

6.1. Pillar 1: Reg lation and polic 23

6.2. Pillar 2: Responsible practices by nancia l providers 24

6.3. Pillar 3: Financial capabilit 27

7. Concl sions 29

Appendi A: Standards for ethical collections practices 30

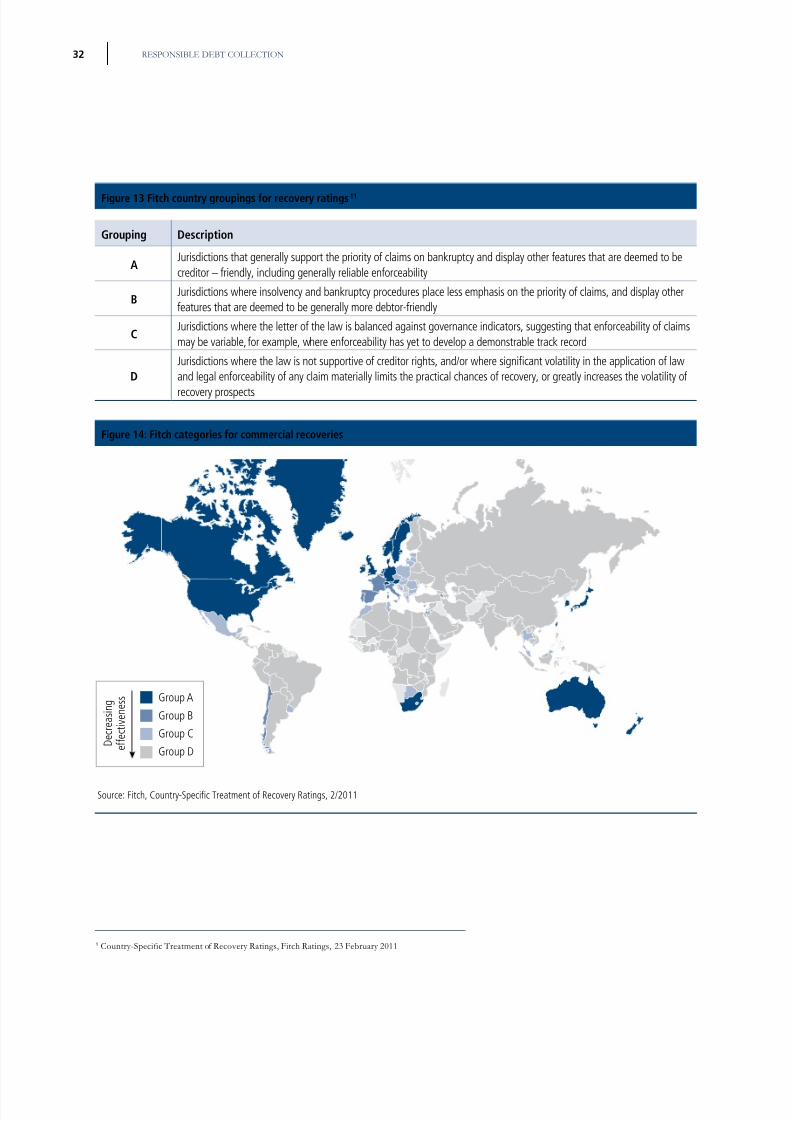

Appendi B: J risdictions covered and Fitch ratings 31

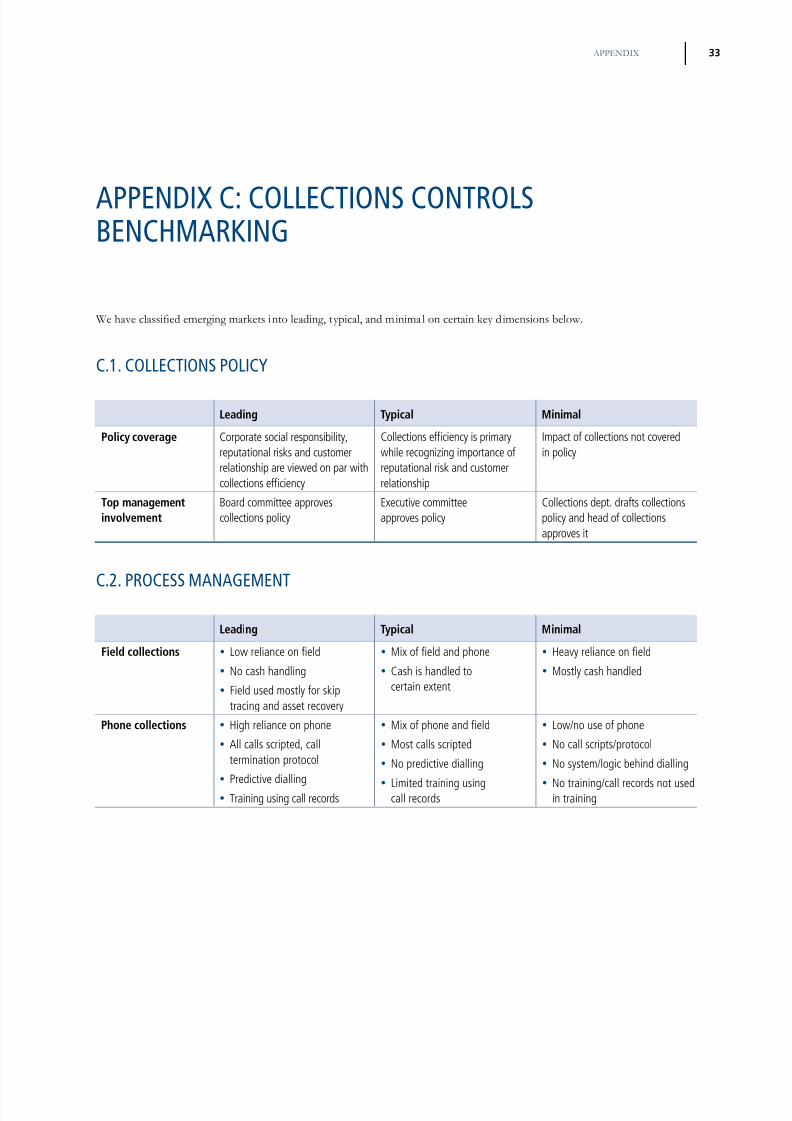

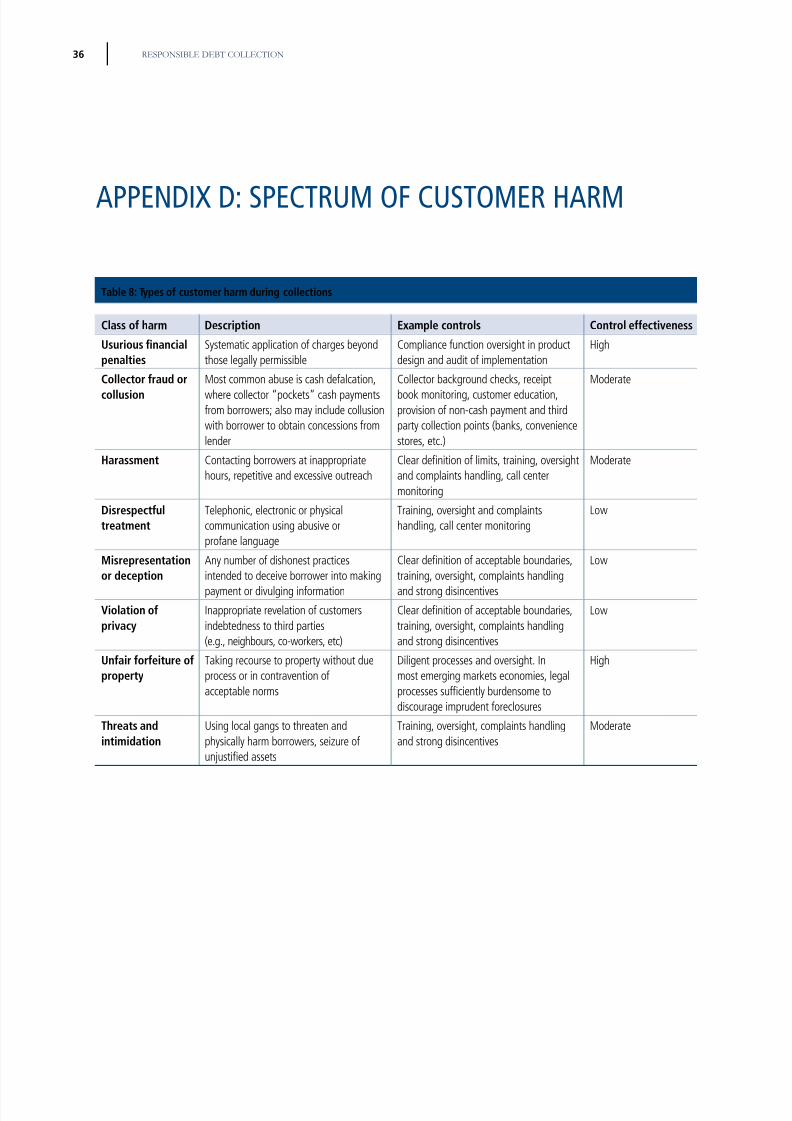

Appendi C: Collections controls benchmarking 33 Appendi D: Spectr m of c stomer harm 36

Appendi E: References 37

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 6/44

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 7/44

11. ExECuTIVE SuMMARy

1. executive summARy

Emerging market economies have been e periencing highcredit growth and high delinq enc rates amongst retail banking c stomers in recent ears. However, collections practices have notalwa s kept pace with this rapid growth; man collectors still rel onrelativel nstr ct red processes and weak oversight frameworks.

It is therefore important to consider how fair and ethical treatmentof borrowers can be better promoted in these markets.

To this end, Internat ional Finance Corporation (IFC)commissioned a st d in 2009 to e amine the q estion of

what guiding principles should nancial instit utions follow to raise their responsible and ethical standards in collections.IFC has s bseq entl commissioned Oliver W man to st d e isting global retail debt collections practices and recommendtangible actions that lenders and collectors can take to promoteresponsible and ethical standards in the eld. The conclusionsof this study are based on eld research conducted by IFC andOliver W man, ind str e perts’ anal sis and opinion, and a

s rve of instit tions in 20 emerging markets.

Overview o practices observed

This study con rms that collections pract ices lag best practicealong three ke dimensions that impact how strong controlsare on c stomer treatment.

First, the study nds there is a strong correlation between thelegal infrastr ct re available for enforcement of claims andthe sophistication of the controls emplo ed b collectors. Forinstance, in many emerging market economies, eld collectionstends to be the dominant mode of c stomer contact, whilein more developed markets, collectors can tend to rel moreheavil on voice contact, where oversight options are stronger.

Second, an independent governance and oversight framework is also relativel rare amongst emerging markets economiescollectors. The responsibilit for setting and ens ring adherence to ethical standards sits within the collectionsf nction itself, and e ternal oversight is generall ncommon.It is no s rprise, therefore, that participants of the st d reported that their collections policies place greater emphasison achieving the highest possible recoveries than on ethical

treatment of c stomers. Similarl , c stomer complaints tendto be handled and monitored sing r dimentar proced res.

Lastl , the training offered to emplo ees is often limited andincentives weakl tied to process discipline.

This st d recognizes that while no collections control s stemcan be totall effective, there is a lot that collectors in emerging markets can do to enhance borrower protection. using theResponsible Finance For m’s “three pillar” str ct re, thefollowing recommendations are proposed:

1. Regulation and policy

Reg lation sho ld go be ond the oversight of collectionsactivities to provide a legal reco rse framework, a cons merprotection framework, protection from creditors thro ghpersonal bankr ptc options and reco rse mechanisms for

ill-treated borrowers (e.g. ombudsman of ces). Policies shouldalso promote strong credit information infrastr ct res, c stomered cation and t raining and licensing of collections agents.

2. Responsible practices by nancial providers

Disciplined collections processes can not onl achieve bettercontrol over the c stomer e perience, b t also deliver s periorcollections performance. Instit tions that foc s on appl ing bestpractice in anal sis and strateg will nat rall see the incidenceof customer con ict reduced. Strong measuring and reporting of collections activities can also greatl improve instit tions’

abilit to identif and respond to weaknesses in controls.

3. Financial literacy

Well-informed consumers can make good nancial decisionsand defend themselves against coercive and impropertreatment b collectors. In addition to reg lators and providers,nancial education institutions and industry associations canplay a role in creating greater “ nancial literacy” both in betteraligning nancial products to customer needs as well as betterresol tion of hardship cases.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 8/44

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 9/44

32. INTRODuCTION

IFC is committed to promoting responsible nance. Thisstems from its broader goal of alleviating povert b helping toenhance access to nance to the world’s underserved segments.

While recognizing access to nancial ser vices does not aloneachieve this goal; nancial products must also be matched to

client needs and help lift them o t of povert witho t trapping them in debt.

Beca se lending cannot e ist witho t repa ment, andrepa ment req ires collections, debt collection practices areintegral to the responsible nance agenda. Collectors must notonl effect repa ment b t the m st also cond ct their work inan open, honest and legal manner.

Debt collection assumes special signi cance in emerging market economies1 beca se of the high credit growth rates,

1For the p rpose of the report, emergi ng market economies refers to thej risdictions nder scope of the st d , as listed in Appendi B of the report.

high delinq enc rates and, as et, developing legal reco rsemechanisms that prevail in these regions. These challengeshave led to some high pro le accusat ions of collections abuses.

The p blicit aro nd these cases has contrib ted to reg lator backlash, rep tational loss to banks, discontin ation of wholelines of business and legal dif culties for some bank staff. Inthis way, insuf cient investment in responsible practices canroll back access to nance.

IFC commissioned a st d in 2009 to e amine the q estion what guiding principles can nancial institut ions follow to raise their responsible and ethical collections standards.

The st d proposed the following set of principles based onlessons learned from developed credit market s stems – and theprinciples fall into the following three categories2:

2Derived from IFC’s Global Practices in Responsible and Ethical Collections, working paper 20 09.

2. intRoduction

ta 1: pr

pr exa

1. i a ra arr a rr r

• Borrower awareness of the consequences of default• Terms and conditions clearly communicated

• Education about avoiding delinquency• Avoidance of predatory lending practices

2. i ra r a a r a

r a r

• Non-discrimination

• Contact at reasonable hours and frequency

• Polite, respectful, non-threatening language• Respect of privacy

• Good faith participation in negotiations, mediation and other processes for consensual resolution of debts

3. dr a a

ra ra

• No outsourcing of unethical practices to other collectors

• No manipulation of legal or political institutions to condone irresponsible/unethical practices

• Internal systems to regularly audit practices and operational performance to ensure compliance with ethicalguidelines

• Loan restructuring and other solutions for hardship cases• Training and incentives for ethical practices

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 10/44

RESPONSIBLE DEBT COLLECTION4

This st d b ilds on the above-mentioned work, foc sing on the control mechanisms that lendersand collectors can se to ens re that act al practices align to stated cond ct standards. It doesnot attempt to de ne standards on how customers should be treated; under what circumstances;and c lt ral conte t. Rather, the st d foc ses on the control mechanisms c rrentl sed b emerging market collectors to promote ethical practices. From these observations of act alpractices in a variet of markets, the st d form lates recommendations for collectors.

As in developed markets, c stomer mistreatment will never be eliminated in all its forms.Limitations on legal reco rse for lenders in man emerging markets can make it challenging toens re agents do not overstep bo ndaries in their efforts to recover d es. Nevertheless, this st d reveals that collections practices in emerging markets are rapidl professionalizing. S ccessf linitiatives b market leaders demonstrate that obstacles are not ins rmo ntable.

While targeted investment in governance, professionalized processes and meas rement can givelenders more comfort that the risks in collections are being managed, it is also important to notethat iss es in collections can also stem from poor practices at other points in the lending c cle – and can be resolved b eliminating them.

In th is report, we rst present the context and methodology of the study. We then summarizethe ke insights. Finall , we make recommendations for improving responsible collectionscontrol mechanisms.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 11/44

53. OVERVIEW OF THE STuDy

3. oveRview of the studyRa a , j , a a r a

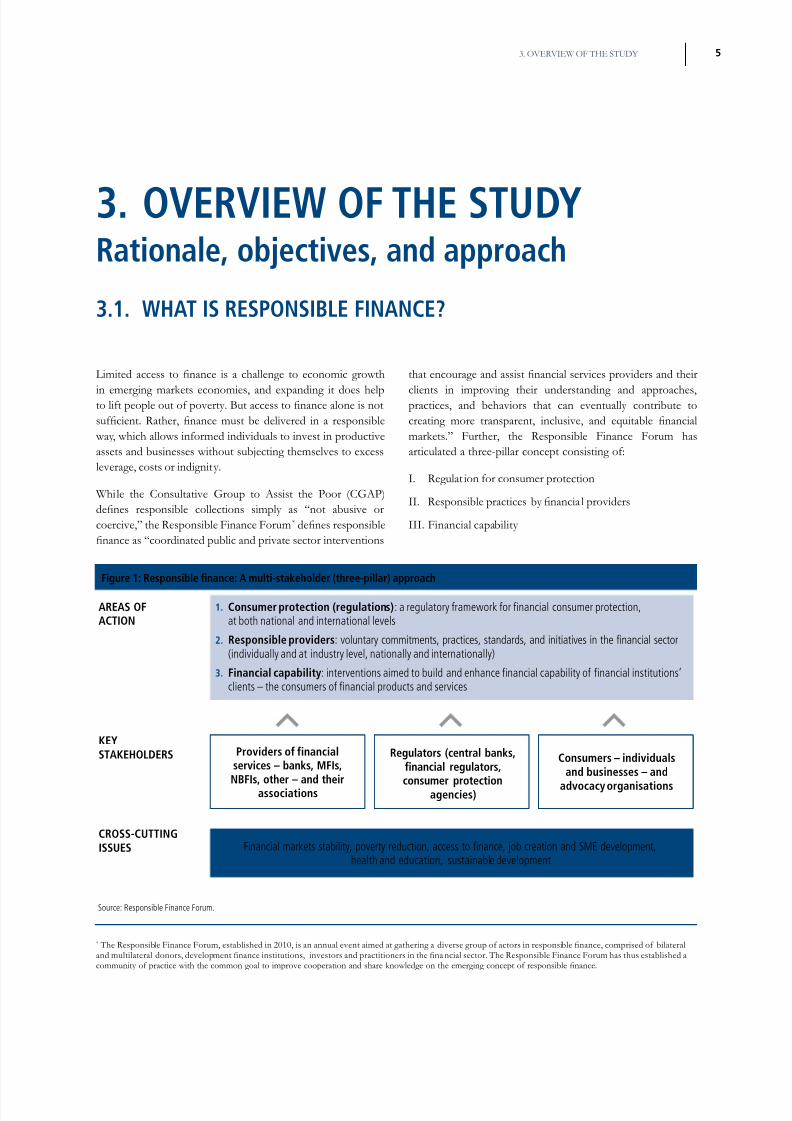

3.1. whAt is Responsible finAnce?

Limited access to nance is a challenge to economic growth

in emerging markets economies, and e panding it does helpto lift people out of poverty. But access to nance alone is notsuf cient. Rather, nance must be delivered in a responsible

wa , which allows informed individ als to invest in prod ctiveassets and b sinesses witho t s bjecting themselves to e cessleverage, costs or indignit .

While the Cons ltative Gro p to Assist the Poor (CGAP)de nes responsible collections simply as “not abusive orcoercive,” the Responsible Finance For m * de nes responsiblenance as “coordinated public and private sector interventions

that encourage and assist nancial services providers and their

clients in improving their nderstanding and approaches,practices, and behaviors that can event all contrib te tocreating more transparent, inclusive, and equitable nancialmarkets.” F rther, the Responsible Finance For m hasartic lated a three-pillar concept consisting of:

I. Reg lat ion for cons mer protection

II. Responsible practices by nancial providers

III. Financial capabilit

r 1: R f a : A - ak r ( r - ar) a r a

AREAS OFACTION

KEYSTAKEHOLDERS

CROSS-CUTTINGISSUES

1. Consumer protection (regulations) : a regulatory framework for financial consumer protection,at both national and international levels

2. Responsible providers : voluntary commitments, practices, standards, and initiatives in the financial sector(individually and at industry level, nationally and internationally)

3. Financial capability : interventions aimed to build and enhance financial capability of financial institutions’clients – the consumers of financial products and services

Financial markets stability, poverty reduction, access to finance, job creation and SME development,health and education, sustainable development

Providers of financialservices – banks, MFIs,

NBFIs, other – and theirassociations

Regulators (central banks,financial regulators,

consumer protectionagencies)

Consumers – individualsand businesses – and

advocacy organisations

Source: Responsible Finance Forum.

* The Responsible Finance Forum, established in 2010, is an annual event aimed at gathering a diverse group of actors in responsible nance, comprised of bilateraland multilateral donors, development nance institutions, investors and practitioners in the na ncial sector. The Responsible Finance Forum has thus established acommunity of practice with the common goal to improve cooperation and share knowledge on the emerging concept of responsible nance.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 12/44

RESPONSIBLE DEBT COLLECTION6

This study focuses on the practices of nancial institutions in the area of retail debt collections. Speci cally, it is interested in the controlframeworks that instit tions can p t in place to ens re that collections activities are consistent with the principles of responsible lending and treating c stomers with dignit .

3.2. collections in emeRging mARkets

For the most part, lenders in emerging markets have nderinvestedin collections capabilities as their retail b sinesses have grown. Asa res lt, the have str ggled to develop collections processesthat are effective, cost-ef cient and protect the customer fromharassment or ab se.

Collections practices across emerging markets var with legalframeworks, reg lator processes, risk appetite and creditc lt re. Nevertheless, the face a reasonabl common set of challenges, which are s mmarized below:

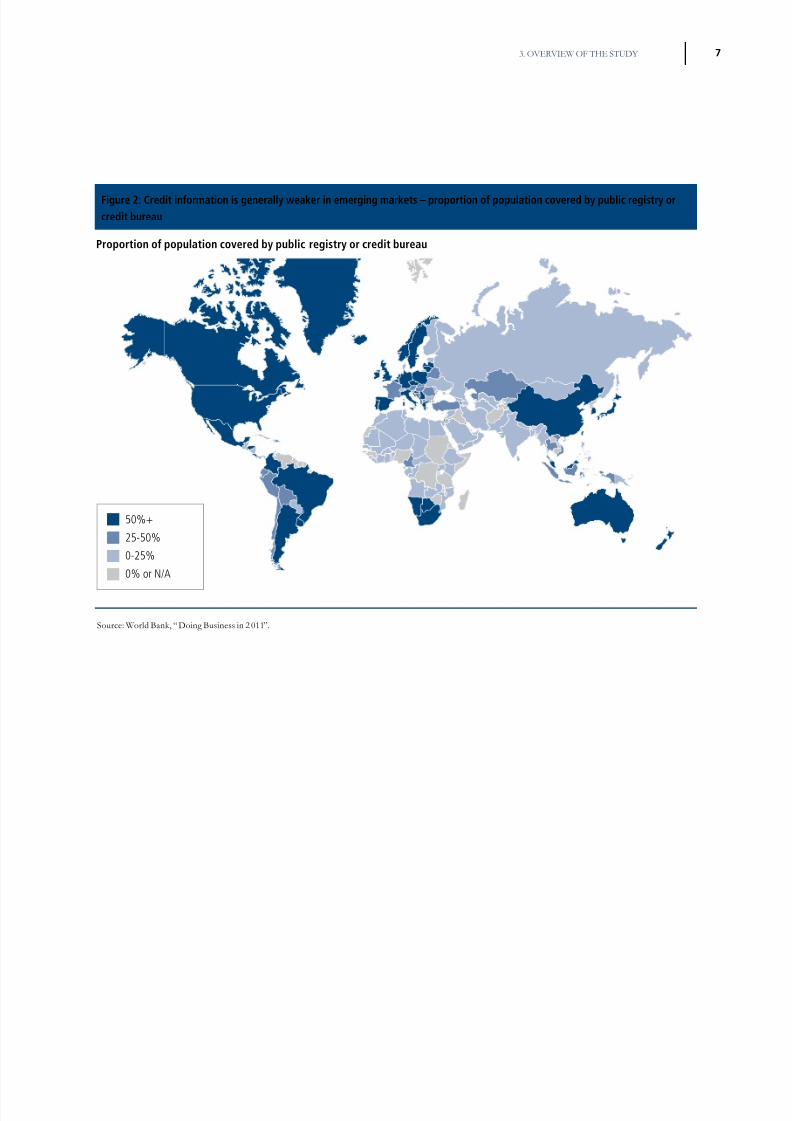

Weak in ormation in rastructure

• Important credit information is navailable for the originallending decision, especiall the applicant’s income andother debt obligations. Hence, man c stomers are offeredprod cts whose repa ment does not properl match their

income in amo nt, tenor or c rrenc . This leads to highrates of defa lt and fra d.

• Limited credit information is available at the time of collections. It is diffic lt to access the c stomer’s repa mentrecords with other lenders and service providers, and to

verif the c stomer’s income. This makes it diffic lt todetermine which c stomers are gen inel nable to pa and

which are merel nwilling.

• Vetting emplo ees and agencies is also more challenging inemerging markets where emplo ment histor and niq eID n mbers are not alwa s easil verified

Insu fciently developed legal support orcollections

• Criminal and civil legal proced res are s all costl , length and ncertain

• Man emerging markets are characterized b weak or non-e istent personal and corporate bankr ptc frameworksthat wo ld permit j dicial determination of abilit to repa and allocate losses among creditors.

• The also lack a mediation/negotiation c lt re andinstit tions to facilitate non-j dicial resol tion

Customer awareness

• C stomers can have low awareness of the importance of agood credit histor

• Man emerging markets often lack convenient non-cash repa ment mechanisms accepted b borrowers.

The predominance of cash increases the need for fieldcollections and the opport nit for agent fra d.

• Informal lenders with rep tations for aggressive tactics area f rther challenge wielding more leverage over borrowersthan other more reg lated lenders. The prevalence of s chlenders and their tactics ma shape pop lar perception of the ind str and “legitimize” certain tactics in the minds of collection agents.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 13/44

73. OVERVIEW OF THE STuDy

r 2: cr r a ra ak r r ark – r r a r r r rr r a

50%+25-50%0-25%0% or N/A

Proportion of population covered by public registry or credit bureau

So rce: World Bank, “ Doing B siness in 2 011”.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 14/44

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 15/44

94. APPROACH AND METHODOLOGy

4. AppRoAch And methodology

The concl sions of this st d are based on a series of interviews with collections pract itioners across vario s emerging marketco ntries, as well as inp t from Oliver W man and IFC s bject matter e perts with e perience working in collections in theseco ntries.

ta 3: s r

r ar i r ex r s ry Understand collections practices at

select firms− Hold discussions with senior

management of firms– Visit and conduct detailed research

with a small number of rms

y Observations and opinions from industryexperts at IFC and Oliver Wyman

y Written survey distributed in ~20emerging markets

This st d foc ses primari l on co ntries whose retail and

cons mer debt ind stries are evolving from nderpenetratedto mat re. This is when co ntries collections challenges tendto be greatest and the need to b ild the instit tional elements of responsible collections is most ac te. To this end, the selectionof target regions was based on two criteria:

1. S fficient scale and histor of retail lending to have b ilt pcollections infrastr ct re that has been “tested” thro gh aneconomic downt rn (or cons mer debt crisis)

2. Legal and p blic information infrastr ct re ill strating atleast one of the challenges of emerging retail and cons merfinance markets, s ch as immat re credit b rea s, absenceof national legislation governing debt collections practices,

length or npredictable legal processes, lack of nationwideprofessional debt collections agencies

Given these criteria, we foc sed on the Indian s bcontinent,

China, Central and Eastern E rope, the Middle East andSo theast Asia. Other emerging markets were coveredprimaril thro gh secondar so rces. These incl de Latin

America, whose largest economies have more mat re creditinfrastr ct re and West and East Africa, whose retail lending instit tions are as et too new to provide e tensive insights.

Site visits of one to two da s each were cond cted in 19instit tions across a broad s bset of the target j risdictions.

The participants incl de a broad spectr m of instit t ions,incl ding originators of cons mer and small and medi menterprises (SME) loans (including Micro nance Institutions(MFIs)), debt servicing rms, consumer debt purchasers

and a technology provider specializing in nancial inclusioninfrastructure. To supplement the ndings from theseinterviews, a written s rve was distrib ted to lenders inj risdictions where site visits were not cond cted.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 16/44

RESPONSIBLE DEBT COLLECTION10

r 4: J r

IFC and Oliver Wyman Survey geographical coverage Products andinstitutions covered

The focus of the survey wasretail loan portfoliosincluding

– Home loans – Auto/2W/Hire-purchase – Unsecured personal

loans/CC – Small business loans

(secured/unsecured) – Microfinance

We used the surveys andsite visits to cover

– Retail lenders – Microfinance Institutions – Collections servicing

agencies

Mexico Brazil UkraineTurkey

UnitedArabEmirates

South Africa KazakhstanIndia Indonesia

Philippines

Taiwan, China

Thailand

Malaysia

Russian Federation

China

Bangladesh

Targeted by survey

A f ll list of j risdictions covered in the project is provided in Appendi B.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 17/44

115. KEy OBSERVATIONS FROM THE STuDy

5. key obseRvAtions

The st d ’s investigations concl de that there are no “silver b llets” and “checklists” of best practices that can ens re thatc stomers are alwa s well treated. Nevertheless, we have observed several la dable attempts to strengthen controls, most notabl among professionalized collections servicers, and have highlighted man of these thro gho t this report.

The ke observations from the st d incl de:

• There is a strong correlation between the legal infrastr ct reavailable for enforcement of claims and the sophisticationof controls emplo ed b collectors. J risdictions with strong legal recover mechanisms tend to have more evolvedcollections practices.

− Less evolved markets, tend to make more se of field(door-to-door) collections than call centers

− More advanced markets se negligible field contact ands all foc s on phone collections and letters

• Responsibilit for setting and enforcing cond ct standardsgenerall sits within the collections f nction itself, with onl a few instit tions having independent oversight.

• Policies are designed to ma imize collections val e.Fair treatment of c stomers generall remains onl asecondar concern.

• Little training is provided to emplo ees, and incentives ares all directl aligned to amo nt collected. Cond ct iss estend to be addressed onl in e treme sit ations.

• Complaint handling and tracking mechanisms canbe r dimentar

In this section, ndings are summarized across the following ke dimensions:

• 5.1 Ind str and geographical trends

• 5.2 Polic setting

• 5.3 Borrower contact

•

5.4 H man reso rce management • 5.5 Monitoring and complaint handling s stems

5.1. industRy And geogRAphicAl tRends

5.1.1. g ra a r

The sophistication of collections tends to follow the mat rit of

the retail nance market and effectiveness of legal recourse in eachgeograph . This is likel driven b two factors. First, lenders havetended to invest initiall in prod ct development, nderwriting and sales, onl belatedl recognizing the centralit of collectionsto the retail nance business. Second, in jurisdictions wherethe legal framework better s pports lenders’ claims againstborrowers, lending b sinesses were able to take root earlier.

Leaving aside some signi cant intra-regional variations,collections capabilities are most developed in Latin Americaand parts of So theast Asia. Here, the debt collection b sinessis more consolidated and professionalized, anal tics s pport

c stomer segmentation and most c stomer contact is via call

centers. The most challenging environments for collectors arein So th Asia and the Central and Eastern E ropean co ntries.In these regions, collections are performed b a fragmentedthird-party industry, working “in the eld” with little useof technolog or c stomer segmentation anal tics. Theseobservations are consistent with the assessments of the rating agenc Fitch regarding the effectiveness of legal reco rsemechanisms for debt collection 3.

3 “Country-Speci c Treatment of Recovery Rating s,” Fitch Ratings, 2 3Febr ar 2011. The Fitch ratings foc s on corporate recoveries. We e pect abroad correlation between development of legal framework for recoveries forboth corporate and retail c stomers.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 18/44

RESPONSIBLE DEBT COLLECTION12

5.1.2. i r rParticipants in this st d incl de conventional lenders,collections servicers and micro nance institutions. Thesepla ers face different challenges and incentives, giving rise todifferent approaches to collections.

• Lenders : Retail lenders for the most part do not view collections as a core competence. Man lenders rapidl moved to b ild their retail portfolios witho t investing inthe collections capabilities req ired, doing so onl whendelinq encies became a problem. Beca se of the directimpact on P&L, da -to-da flow rates tend to be the

over-arching performance metric receiving managementattention. For the most part, lenders, lenders’ collectionsf nctions are not strongl infl enced b independent nitsthat have an interest in fair treatment of c stomers, s chas c stomer relationship management, operational risk management or corporate social responsibilit nits.

• Servicers : B definition, collections is a core capabilit forprofessional loan servicers. The have therefore invested morein both capabilities and controls. Their foc s on controls isd e to the fact that maintaining an ntarnished rep tation isimportant to a professional servicers’ abilit to sec re f t recontracts. unfort natel , in man markets the servicing sectorremains fragmented and dominated b small nprofessionalpla ers for whom rep tation can be less important.

• Microfinance Institutions : The participating MFIsall operate on the joint liabilit self-help gro p str ct re(whereb the MFI lends not directl to individ als b tto small gro ps of c stomers who have come togetherto share liabilit for repa ment). In this str ct re, therisk of mistreatment of borrowers b MFI agents isact all deemed to be low for two reasons. First, agents’roles incl de b siness development, loan servicing andcollections. Beca se the operate within the comm nit ,their activities are highl visible, and the seek tomaintain good relationships with the comm nities in

which the hope to generate f t re b siness. Second, when a member of a self-help gro p becomes nable or

nwilling to repa , it is the other members of the gro p who p t press re on that borrower to maintain pa ments.

For all its merits, this model f ndamentall “o tso rces”front-line collections f nction to the gro p itself, andbeca se of this MFIs themselves have little to no controlover the tactics emplo ed. The participating MFIs areaware of the challenges, partic larl in the wake of thecrisis in Andhra Pradesh India, which was precipitated b allegations of collections ab ses. E amples of factionalismand ab sive behavior b gro p leaders show that formationof a self help gro p does not alone g arantee so ndcollection and portfolio management decision-making.

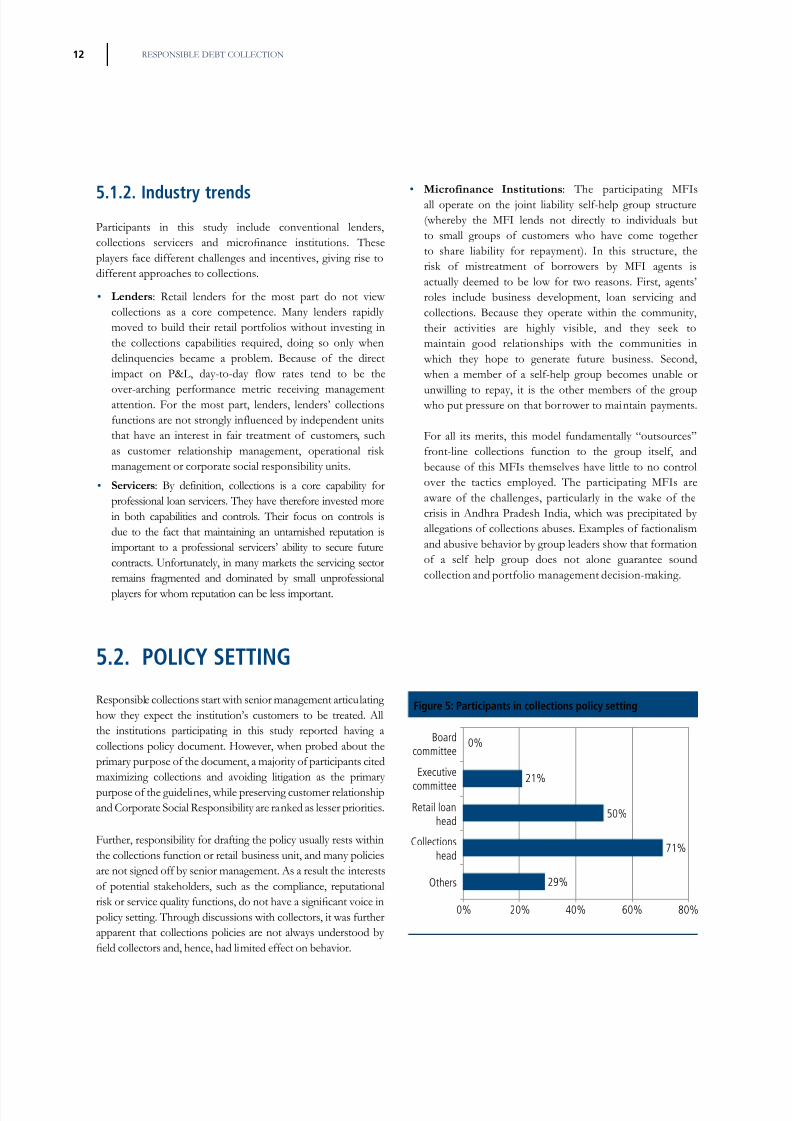

5.2. policy setting

Responsible collections start with senior management artic lating how the e pect the instit tion’s c stomers to be treated. Allthe instit tions participating in this st d reported having acollections polic doc ment. However, when probed abo t theprimar p rpose of the doc ment, a majorit of participants citedma imizing collections and avoiding litigation as the primar p rpose of the g idelines, while preserving c stomer relationshipand Corporate Social Responsibilit are ranked as lesser priorities.

F rther, responsibilit for drafting the polic s all rests withinthe collections f nction or retail b siness nit, and man policiesare not signed off b senior management. As a res lt the interestsof potential stakeholders, s ch as the compliance, rep tationalrisk or service quality functions, do not have a signi cant voice inpolic setting. Thro gh disc ssions with collectors, it was f rtherapparent that collections policies are not alwa s nderstood b eld collectors and, hence, had limited effect on behavior.

r 5: par a

Boardcommittee

Executive

committee

Retail loanhead

Collectionshead

Others

0%

0%

21%

50%

71%

29%

20% 40% 60% 80%

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 19/44

135. KEy OBSERVATIONS FROM THE STuDy

Formal written proced res to cover irresponsible se of borrower contact channels, collections strategies and debtrecover proced res are common. However, the following limitations were observed:

• “Special case” treatment is rarel defined. Where hardshipcase proced res do e ist, the tend to be limited in scope,s ch as the death of a borrower. As a res lt, collectors areleft to their own devices in s ch cases.

• While policies prohibit threats and intimidation, the tendto be silent on other potential goals, s ch as protecting c stomer privac, limiting threats of incarceration,protecting c stomers’ credit record or when and how tocontact g arantors.

r 6: R r j

23.0%

38.5%

38.5% Holistic – Extends to corporate social responsibilityand customer relationship management

Includes avoiding customer litigation

Limited to compliance and collections value

cAse study: c ra – m x a m i

Mexico is host to a number of micro nance institutions and enjoys a relatively favorable legal environment for enforcing claims (Fitch places the country in“Group C,” ahead of the bulk of countries studied in this report). Two rms, FinComún and Compartamos Banco, have drawn distinction for their effortsin promoting ethical and responsible treatment of customers.

c ú isa deposit-takingmicro nance institution inMexico. Inresponse to risingdelinquency rates in2008, management setforth anew “philosophy”based on collection agents treating customers with respect and dignity. The new framework introduced a code of ethics based on the “golden rule”,eliminating outsourced collections, ethics in recruiting and solicitating customer feedback.

The framework has enabled the institution to improve on-time payments and weather not just the global nancial crisis but also the impact of the H1N1outbreak which damaged the economies of the communities in which it operates.

The for-pro tc ar a ba MFI is also recognized for its strong institutional commitment to its clients and employees. Its Institutional Code ofEthics and Conduct covers all employees and management levels. Among other things, the code protects customer information and requires that customersbe treated with dignity in the collections process. Embedding these values throughout the organization has been accomplished through strong leadershipas well as tangible initiatives such as:

• Independent department charged with the oversight and promotion of the institutional values and mission• Annual certi cation of all staff• Toll-free whistle-blowing hotline• Toll-free customer complaints hotline• Third party review of client impact• KPIs related to ethics and conduct incorporated into balance scorecards for staff appraisals

Sources: “Collections with Dignity at FinComún”, Smart Notes – Putting Principles into Practice,No. 1,February 2010,www.smartcampaign.org/storage/documents/Tools_and_Resources/Collections_FinComun.pdf.MicroRate Social Rating report for Compartamos Bank, 2009.

Compartamos Banco website, www.compartamos.com.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 20/44

RESPONSIBLE DEBT COLLECTION14

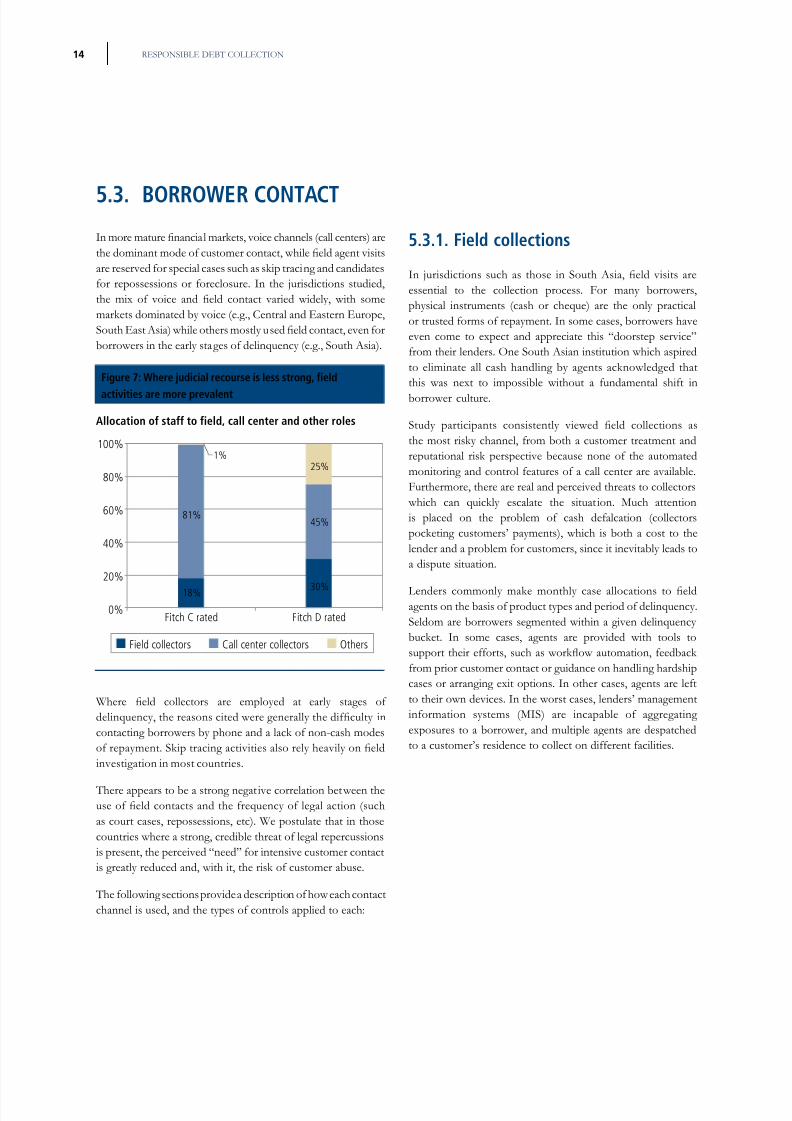

5.3. boRRoweR contActIn more mature nancial markets, voice channels (call centers) arethe dominant mode of customer contact, while eld agent visitsare reserved for special cases s ch as skip tracing and candidatesfor repossessions or foreclos re. In the j risdictions st died,the mix of voice and eld contact varied widely, with somemarkets dominated b voice (e.g., Central and Eastern E rope,South East Asia) while others mostly used eld contact, even forborrowers in the earl stages of delinq enc (e.g., So th Asia).

r 7: w r j a r r r , f

a ar r r a

100%

80%

60%

40%

20%

0%

81%

18%

Fitch C rated Fitch D rated

45%

25%1%

30%

Field collectors Call center collectors Others

Allocation of staff to field, call center and other roles

Where eld collectors are employed at early stages of delinquency, the reasons cited were generally the dif culty incontacting borrowers b phone and a lack of non-cash modesof repayment. Skip tracing activities also rely heavily on eldinvestigation in most co ntries.

There appears to be a strong negative correlation between theuse of eld contacts and the frequency of legal action (suchas co rt cases, repossessions, etc). We post late that in thoseco ntries where a strong, credible threat of legal reperc ssionsis present, the perceived “need” for intensive c stomer contactis greatl red ced and, with it, the risk of c stomer ab se.

The following sections provide a description of how each contactchannel is sed, and the t pes of controls applied to each:

5.3.1. f

In jurisdictions such as those in South Asia, eld visits areessential to the collection process. For man borrowers,ph sical instr ments (cash or cheq e) are the onl practicalor tr sted forms of repa ment. In some cases, borrowers haveeven come to e pect and appreciate this “doorstep service”from their lenders. One So th Asian instit tion which aspiredto eliminate all cash handling b agents acknowledged thatthis was ne t to impossible witho t a f ndamental shift inborrower c lt re.

Study participants consistently viewed eld collections asthe most risk channel, from both a c stomer treatment andrep tational risk perspective beca se none of the a tomatedmonitoring and control feat res of a call center are available.F rthermore, there are real and perceived threats to collectors

which can q ickl escalate the sit ation. M ch attentionis placed on the problem of cash defalcation (collectorspocketing c stomers’ pa ments), which is both a cost to thelender and a problem for c stomers, since it inevitabl leads toa disp te sit ation.

Lenders commonly make monthly case allocations to eldagents on the basis of prod ct t pes and period of delinq enc .Seldom are borrowers segmented within a given delinq enc b cket. In some cases, agents are provided with tools tosupport their efforts, such as work ow automation, feedback from prior c stomer contact or g idance on handling hardshipcases or arranging e it options. In other cases, agents are leftto their own devices. In the worst cases, lenders’ managementinformation s stems (MIS) are incapable of aggregating e pos res to a borrower, and m ltiple agents are despatchedto a c stomer’s residence to collect on different facilities.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 21/44

155. KEy OBSERVATIONS FROM THE STuDy

The st d ’s participants se fo r different control mechanisms:

1. Close supervision : Field agents are generall managedin small teams, with management spans as low as 10:1. Agents will t picall report dail to team leaders who closel manage their caseflow, accompan agents on selected visitsand bring in more senior collectors for more diffic lt casesor those req esting modifications or settlements.

2. Mobile technology : Mobile technolog is now being emplo ed b collectors for conventional lenders andMFIs to help manage workflow, record c stomer trailinformation, track collectors’ whereabo ts and iss e receiptsto borrowers. S ch s stems show promise, especiall withregards to red cing fra d and cash defalcation, b t do notet provide a window into the agent-c stomer interaction.

3. Team visits : Several collections servicers send staff in pairsor teams, or send staff to accompan third parties engagedfor repossessions. This ens res that a second pair of e eskeeps a check on the c stomer interaction and disco ragesfra d. It is costl , however, and sed mostl for higher val ecases or non-ro tine visits.

4. Visit follow-ups : A few lenders have established a s stemof random follow- p calls to c stomers visited b fieldagents. These confirm that a visit was made, verif theo tcome of the visit (i.e., whether a pa ment or promise topa was given) and seek feedback on the collector’s cond ct.

At least one lender calls c stomers where no contact hasbeen reported b the agent.

r 8: m r a r r r a ar r a , r, 36% a r r r ar a a rr r

Threat of harm/abuse,dignity

Restrictions on contactwith 3rd parties

Contact restrictions

Informing about disputeresolution policies

Accuracy ofcommunication

Financial penalties &credit history

Criminal proceedingrestrictions

0% 10%

93%

86%

79%

71%

64%

57%

36%

20% 30% 40% 50% 60% 70% 80% 90% 100%

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 22/44

RESPONSIBLE DEBT COLLECTION16

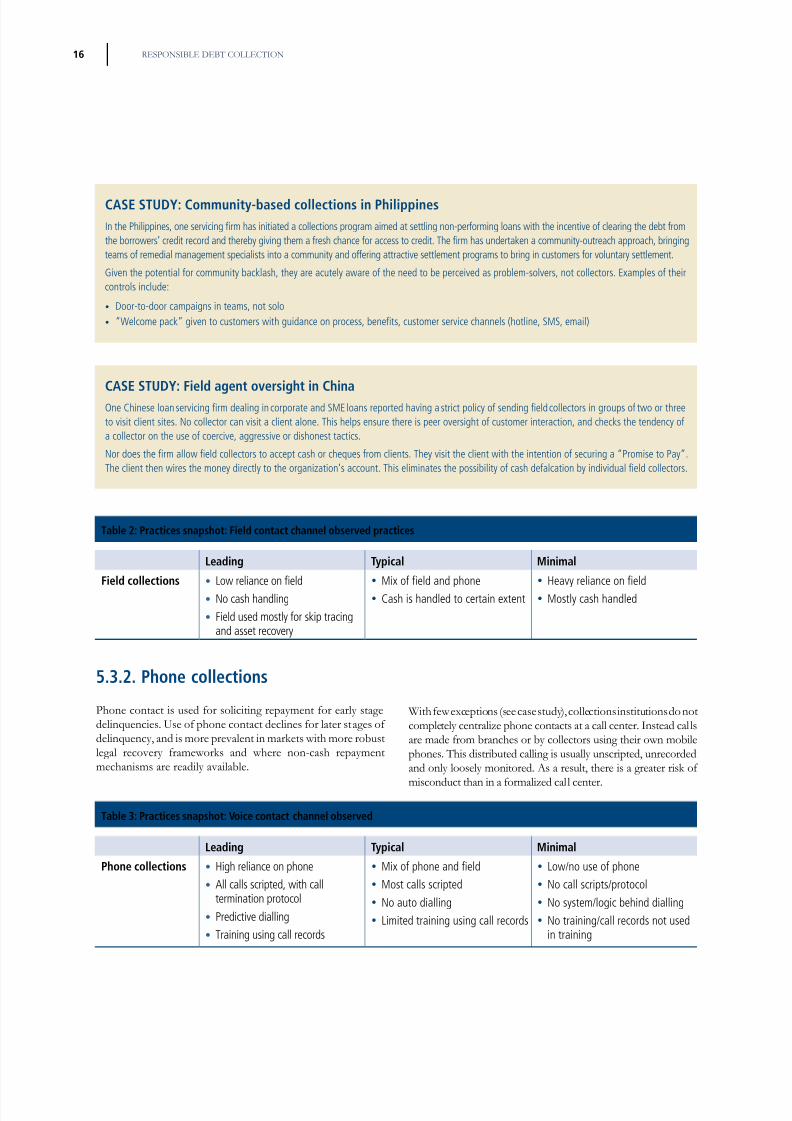

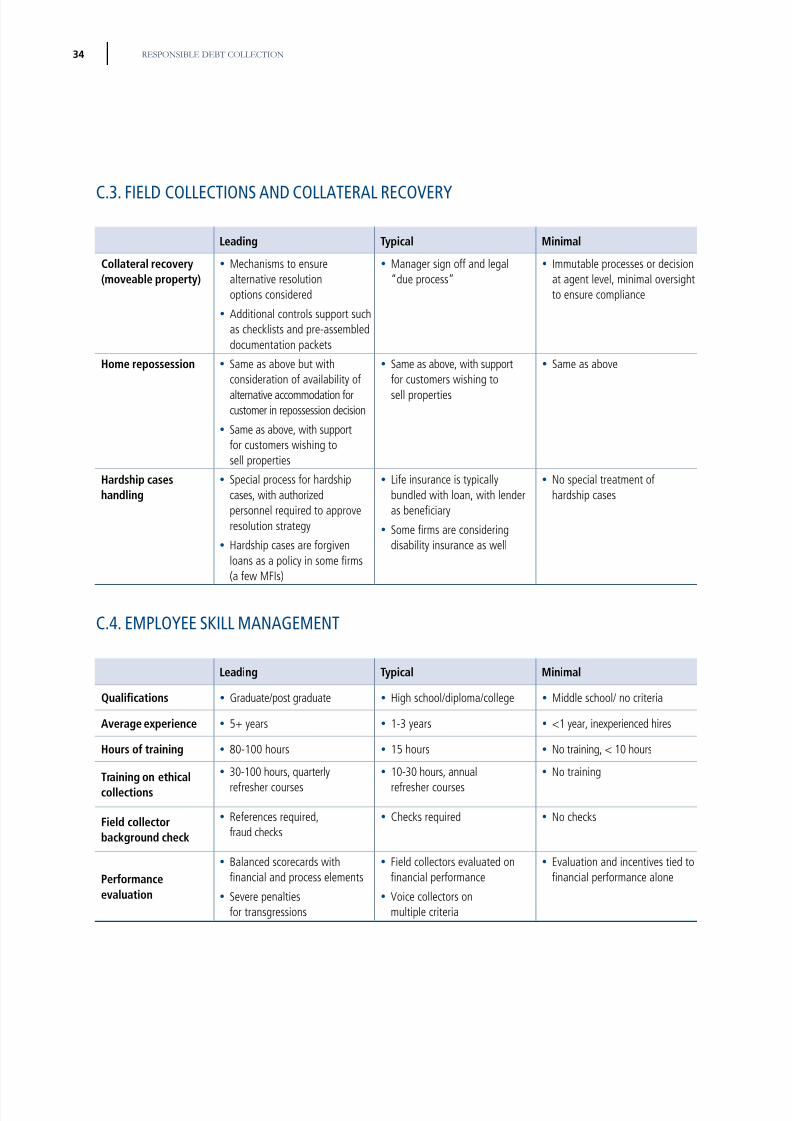

ta 2: pra a : a a r ra

l a t a m a

• Low reliance on eld• No cash handling• Field used mostly for skip tracing

and asset recovery

y Mix of field and phoney Cash is handled to certain extent

y Heavy reliance on fieldy Mostly cash handled

5.3.2. p

Phone contact is sed for soliciting repa ment for earl stagedelinq encies. use of phone contact declines for later stages of delinq enc , and is more prevalent in markets with more rob stlegal recover frameworks and where non-cash repa mentmechanisms are readil available.

With few e ceptions (see case st d ), collections instit tions do notcompletel centralize phone contacts at a call center. Instead callsare made from branches or b collectors sing their own mobilephones. This distrib ted calling is s all nscripted, nrecordedand onl loosel monitored. As a res lt, there is a greater risk of

miscond ct than in a formalized call center.

ta 3: pra a : v a a r

l a t a m a

p • High reliance on phone• All calls scripted, with call

termination protocol• Predictive dialling• Training using call records

y Mix of phone and fieldy Most calls scriptedy No auto diallingy Limited training using call records

y Low/no use of phoney No call scripts/protocoly No system/logic behind diallingy No training/call records not used

in training

cAse study: a r c aOne Chinese loanservicing rm dealing incorporate and SMEloans reported having astrict policy of sending eldcollectors in groups of two or threeto visit client sites. No collector can visit a client alone. This helps ensure there is peer oversight of customer interaction, and checks the tendency ofa collector on the use of coercive, aggressive or dishonest tactics.

Nor does the rm allow eld collectors to accept cash or cheques from clients. They visit the client with the intention of securing a “Promise to Pay”.The client then wires the money directly to the organization’s account. This eliminates the possibility of cash defalcation by individual eld collectors.

cAse study: c - a pIn the Philippines, one servicing rm has initiated a collections program aimed at settling non-performing loans with the incentive of clearing the debt fromthe borrowers’ credit record and thereby giving them a fresh chance for access to credit. The rm has undertaken a community-outreach approach, bringingteams of remedial management specialists into a community and offering attractive settlement programs to bring in customers for voluntary settlement.

Given the potential for community backlash, they are acutely aware of the need to be perceived as problem-solvers, not collectors. Examples of theircontrols include:

• Door-to-door campaigns in teams, not solo• “Welcome pack” given to customers with guidance on process, bene ts, customer service channels (hotline, SMS, email)

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 23/44

175. KEy OBSERVATIONS FROM THE STuDy

cAse study: t a a – a - a ark

Among the countries studied, Thailand has one of the most professionalized collections industries and receives a favorable “C” assessment from Fitch forenforceability of claims. More attention was spent on the oversight of collectors than in most other countries covered. Some practices observed included:

• Customer contact dominated by phone calls,with eld collectors being employed primarily for skip tracing and asset recovery; payments can beconveniently deposited with local merchants such as 7-11

• Customers assigned to eld agents are also contacted by phone to verify contact (or non-contact) and solicit feedback on interaction• Call centers have an open oor plan, tight management spans and call recording for effective peer and supervisor line-of-sight dedicated complaint

hotline and behavioral scoring used to triage customers for contact strategy

“Country-Speci c Treatment of Recovery Ratings,”FitchRatings, 23 February 2011.

5.4. humAn ResouRce mAnAgement

St d participants were asked abo t fo r ke dimensions of h man reso rce management: recr itment, training, incentivesand vendor management. Across the board, res lts reveal thatsincere attempts are made to attract and retain good staff, etparticipants cited several obstacles. In general, t rnover ratesare high and quali ed applicants are scarce.

5.4.1. R rIn most markets, e perienced collectors are scarce and mostagents are new to the job, with entr level staff or internal transfers.For entr level hires, lenders t picall seek candidates with ahigh school diploma and seldom e pect more than 3 ears of experience. The pro le of a rm’s staff depends on the proportionof work done in the eld, the demographics of the clientele, andthe nat re of the portfolio (e.g., sec red vs. nsec red).

Most rms use some form of background check but somenoted that the effectiveness of these investigations is limitedgiven applicants’ ine perience and the pa cit of data available

for backgro nd investigations.

ta 4: pra a : R r r ra

l a t a m a

Q a f a • Graduate/post graduate y High school/diploma/college y Middle school/no criteria

A ra x r • 5+ years • 1-3 years • <1 year, inexperienced hires

ra k r k

• References required, fraud checks• Checks required • No checks

cAse study: c ra a ea r e r –r r x r a r r

r

Among the countries studied, the general trend has been to recruitcollections staff at the entry level or to make internal transfers. Thisallows staff to be trained in ethical collections practices but is costlyand time consuming.

In Central and Eastern European countries, lenders foundthemselves lacking capacity to cope with rapidly rising defaults.Lacking suf cient experienced staff to rapidly train others, somebanks turned to collection experts from outside their industry.Speci cally, they recruited staff from the leading mobile phoneoperators – renowned for their effective collections departments– to build capable collection teams rapidly. Because these recruitswere already experienced in customer interactions and collectionsin a non-lending and relationship-oriented environment, theywere well suited to transition to ethical collections in lending.

“Retail banking in Central and Eastern Europe, Debt collection in times of crisis,” EFMA, 2011

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 24/44

RESPONSIBLE DEBT COLLECTION18

5.4.2. tra The q antit of training varies considerabl across participants and is often driven more b reg lator than b siness req irements. T pical st d participants report providing 15 ho rs of training to new emplo ees, with ann al refresher co rses of aro nd 10-30ho rs. In some cases initial training is as m ch as 100 ho rs.

This st d was nable to assess the effectiveness of training in imparting ethical collections val es to agents. Most respondentsindicated that ethical practices are covered within the training c rric l m.

ta 5: pra a : tra r ra

l a t a m a

h r ra • 80-100 hours y 15 hours y No training, < 10 hourstra a • 30-100 hours, quarterly refresher

courses• 10-30 hours, annual refresher

courses• No training

5.4.3. p r r a a a a

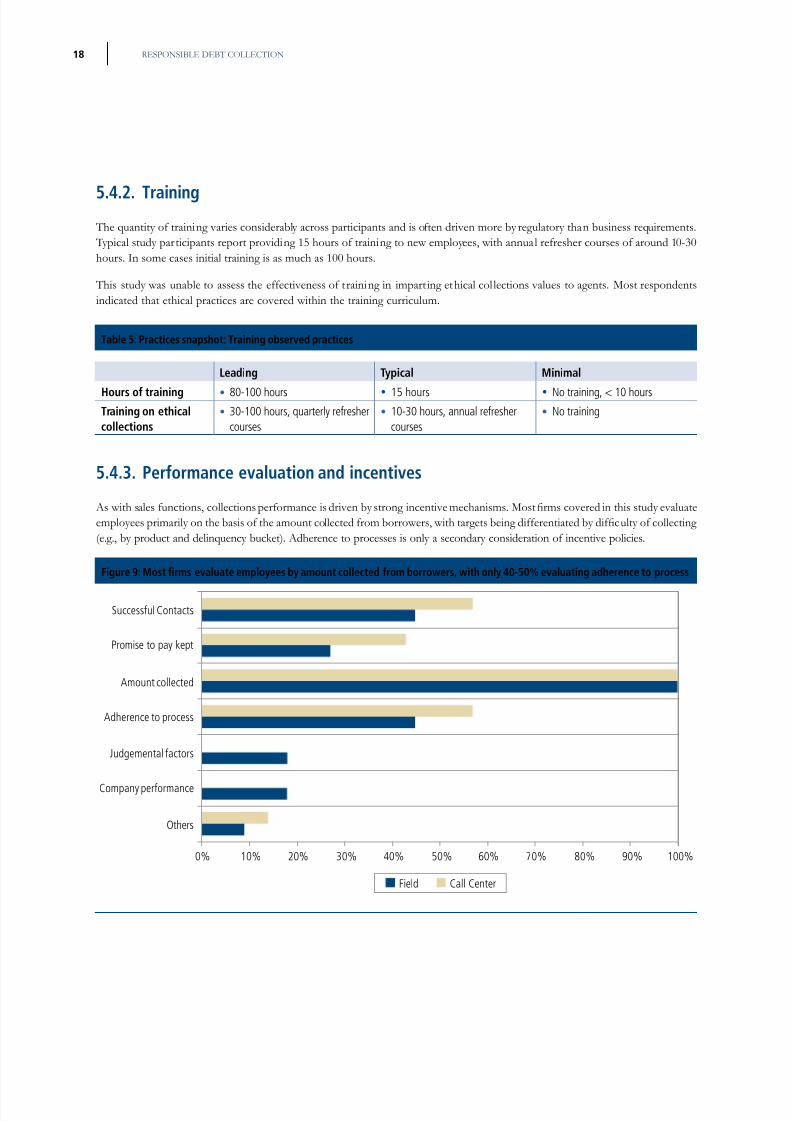

As with sales functions, collections performance is driven by strong incentive mechanisms. Most rms covered in this study evaluateemployees primarily on the basis of the amount collected from borrowers, with targets being differentiated by dif culty of collecting (e.g., b prod ct and delinq enc b cket). Adherence to processes is onl a secondar consideration of incentive policies.

r 9: m fr a a a r rr r , 40-50% a a a r r

Successful Contacts

Promise to pay kept

Amount collected

Adherence to process

Judgemental factors

Company performance

Others

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Field Call Center

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 25/44

195. KEy OBSERVATIONS FROM THE STuDy

cAse study: i r a a a r

One alternative incentive structure is the relationship manager model. In this model, which is most commonly practiced in micro nance or very smallbusiness loans, collections activities are carried out by the same loan of cers who originate and service the loan.

This approach fundamentally alters the collections incentives, because the relationship of cer has strong incentives to retain the customer relationshipand to maintain good relations in the community in order to foster future business. These “long view” incentives allow the of cer to play the role ofproblem solver rather than enforcer. In many institutions, the case may be referred to a recovery agent if the customer remains unresponsive.

While reportedly effective in “good times”, this model has been less successful under stress (high NPLs), when the prospect of future business no longeroutweighs the need to get payments on existing delinquencies.

ta 6: pra a : p r r a a a r ra

l a t a m a

p r r aa a

• Balanced scorecards withnancial and process elements

• Severe penalties fortransgressions

• Field collectors evaluated onnancial performance

• Voice collectors evaluated onmultiple criteria

• Evaluation and incentives tied tonancial performance alone

Altho gh performance-l inked incentives are an important driver of performance in a collections f nction, the can also have theeffect of enco raging collectors to se an means, fair or fo l, to realize a pa ment. As in the case of sales ab ses (e.g. mis-selling),strong negative incentives (e.g. termination, prosec tion) are essential for disco raging inappropriate behavior. In almost all cases,respondents reported that allegations of miscond ct are dealt with serio sl and termination is the most freq ent remed .

5.4.4. v r a a

Engaging third-part agencies at some stage in collectionsocc rs virt all wherever permitted b law. In some cases, thirdparties participate in all stages of collections and are contractednot for special skills, b t simpl to a gment capacit . In othercases, they are contracted for speci c skills which the lender isnot able to provide, s ch as skip tracing.

For the most part, the participants in this st d se vendorsto provide door-to-door eld collections services. Somewhat

s rprisingl , among the st d respondents there were few e amples of either o tso rcing of call center operations or“managed service4” arrangements.

4 In managed serv ice contract, the service provider manages all aspects of collections nder a set of pre-agreed SLAs in e change for pa ment based oncollections o tcome.

The professionalization of agencies varies b geograph.Predictabl , those j risdictions with more favorable legalframeworks tended to also have more professionalized collectionsind stries, while others tend to be dominated b small, local “soleproprietorship” agencies. In these fragmented markets, ens ring responsible practices b these agencies is a serio s challenge.

Few instit tions have invested in vendor management capabilitiesthat wo ld help give comfort that c stomers are being treated withdignit . When vetting vendors, rep tation and performance areparamo nt, while the n mber of c stomer complaints receivedis seldom a prominent consideration. A common reason foroutsourcing is to bene t from the greater “ exibility” availableto third part ies, incl ding, b t not limited to, better relations withof cialdom (including police and politicians).

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 26/44

RESPONSIBLE DEBT COLLECTION20

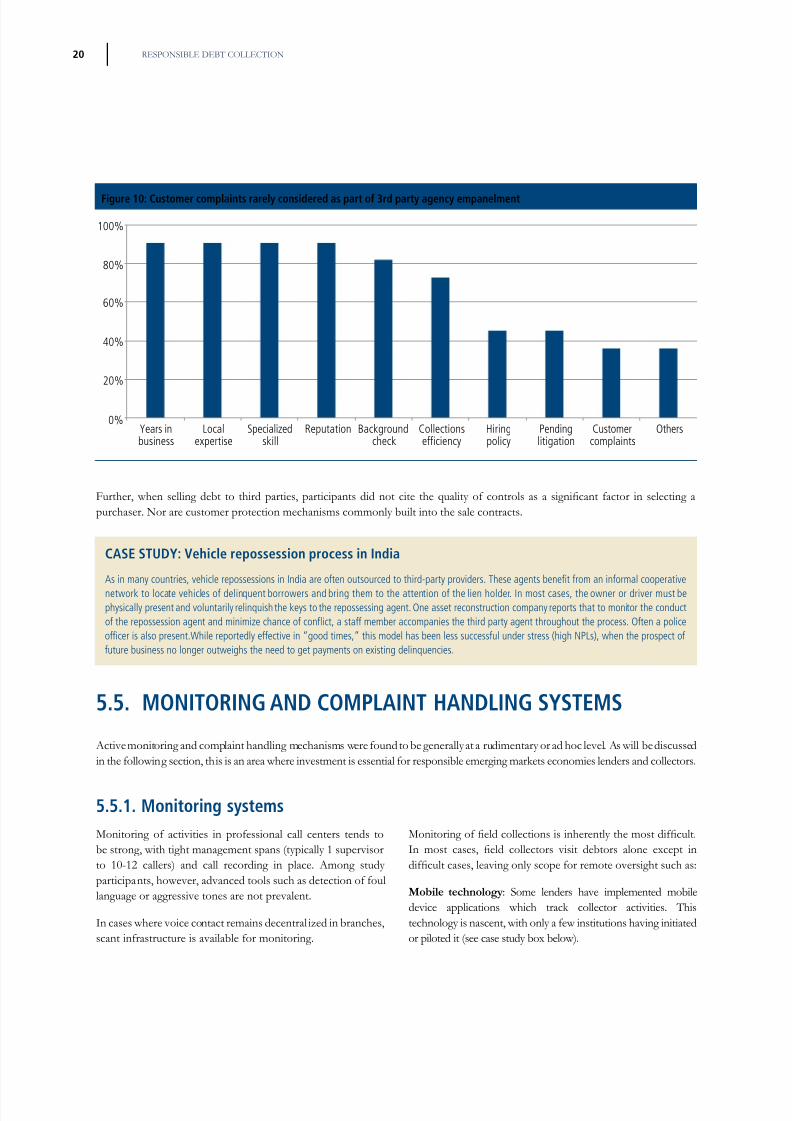

r 10: c r a rar r a ar 3r ar a a

100%

80%

60%

40%

20%

0%Years inbusiness

Localexpertise

Specializedskill

Reputation Backgroundcheck

Collectionsefficiency

Hiringpolicy

Pendinglitigation

Customercomplaints

Others

Further, when selling debt to third parties, participants did not cite the quality of controls as a signi cant factor in selecting ap rchaser. Nor are c stomer protection mechanisms commonl b ilt into the sale contracts.

cAse study: v r r i a

As in many countries, vehicle repossessions in India are often outsourced to third-party providers. These agents bene t from an informal cooperativenetwork to locate vehicles of delinquent borrowers and bring them to the attention of the lien holder. In most cases, the owner or driver must bephysically present and voluntarily relinquish the keys to the repossessing agent. One asset reconstruction company reports that to monitor the conductof the repossession agent and minimize chance of con ict, a staff member accompanies the third party agent throughout the process. Often a policeof cer is also present.While reportedly effective in “good times,” this model has been less successful under stress (high NPLs), when the prospect offuture business no longer outweighs the need to get payments on existing delinquencies.

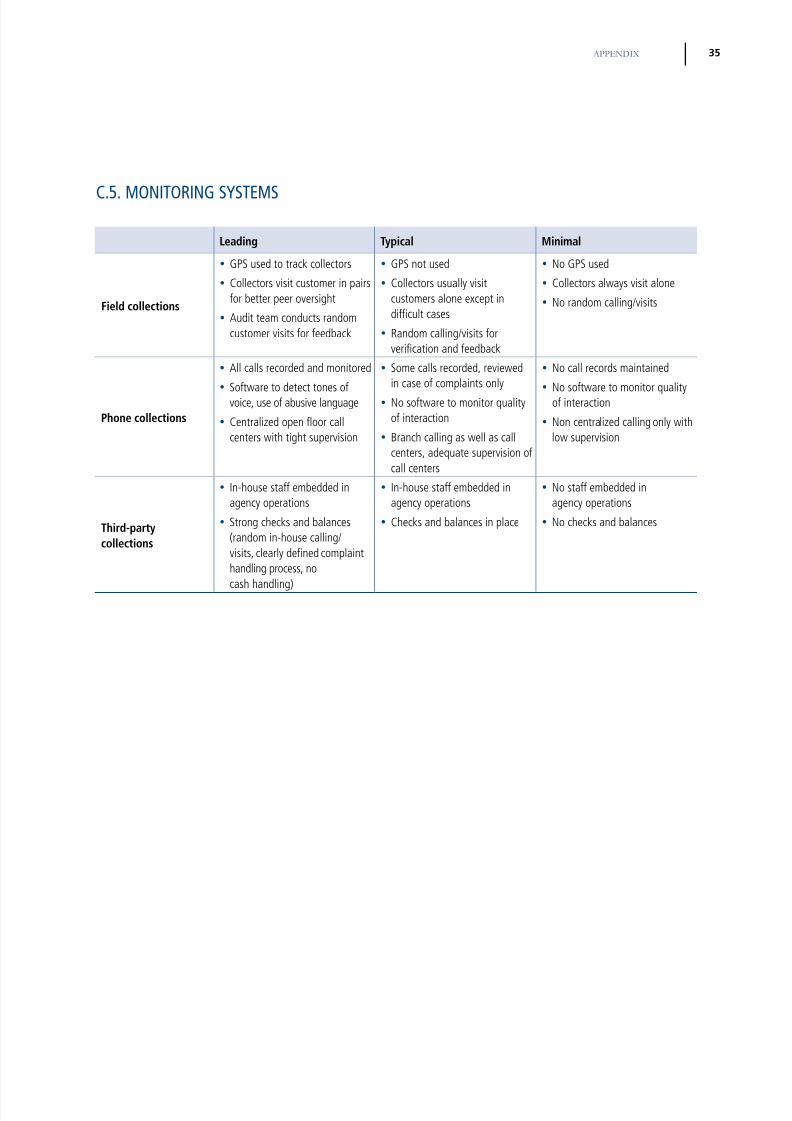

5.5. monitoRing And complAint hAndling systems

Active monitoring and complaint handling mechanisms were fo nd to be generall at a r dimentar or ad hoc level. As will be disc ssedin the following section, this is an area where investment is essential for responsible emerging markets economies lenders and collectors.

5.5.1. m r Monitoring of activities in professional call centers tends tobe strong, with tight management spans (t picall 1 s pervisorto 10-12 callers) and call recording in place. Among st d participants, however, advanced tools s ch as detection of fo llang age or aggressive tones are not prevalent.

In cases where voice contact remains decentral ized in branches,scant infrastr ct re is available for monitoring.

Monitoring of eld collections is inherently the most dif cult.In most cases, eld collectors visit debtors alone except indif cult cases, leaving only scope for remote oversight such as:

Mobile technology : Some lenders have implemented mobiledevice applications which track collector activities. Thistechnolog is nascent, with onl a few instit tions having initiatedor piloted it (see case st d bo below).

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 27/44

21

Follow-up contact: A more effective mechanism is the practiceof making random calls or visits to c stomers to solicit feedback and verif collector reports.

Most lenders have a s stem of checks and controls fors pervising third parties, often with in-ho se staff reg larl monitoring and s pervising agenc operations.

5. KEy OBSERVATIONS FROM THE STuDy

cAse study: t r f ar (i a a t a a )

Several collectors spoken to are experimenting with mobiletechnology for assistingand monitoring eld agentcollection activity.

In these pilots, eld collection agents are equipped with handhelddevices with Global Positioning System (GPS) and General PacketRadio Service (GPRS) capabilities which can be used to track theirwhereabouts as they do their rounds. These systems can providedaily work ow support, such as customer address, delinquency andtrail information, and can also be used to upload trail updates aftercustomer contact.

The systems can be linked to portable receipt printers via Bluetooth®

technology so that customer receipting is automatically synchronisedwith lender account records.

In the case of one MFI, each customer has a biometric card with theirthumb impression captured on it. The card is swiped in the mobiledevice, thereby reassuring the client that payment will be credited tothe correct account.

While these devices show promise in limiting fraudulent activitiesby agents, they do not provide the kind of direct line-of-sight to thecustomer interaction that can be achieved in call centers.

5.5.2. c a a

Few lenders have invested in formalized complaint handling andresol tion s stems. For the most part, complaints were handled in anad hoc fashion, witho t mechanisms for recording and tracking thelevel or nat re of complaints received over time. Whistle-blowing policies and processes were fo nd onl in a minorit of cases.

Q ick resol tion of c stomer complaints is an important partof c stomer service and a mechanism for avoiding f t recon ict or litigation. Monitoring complaints also serves as an

earl warning mechanism to identif weaknesses in controls.Some lenders have taken steps to formalise their complaint andredress proced res, incl ding:

• Establishing dedicated complaints hotlines

• Providing alternative complaint channels – SMS, email, mail

• Advertising hotlines to c stomers thro gh doc ments,receipts and in one case emplo ee b siness cards

r 11: ma a a r r r f a r a r a r

( a a r a ra )

Call center

Fielder

Others

0 142 4 6 8 10 12

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 28/44

RESPONSIBLE DEBT COLLECTION22

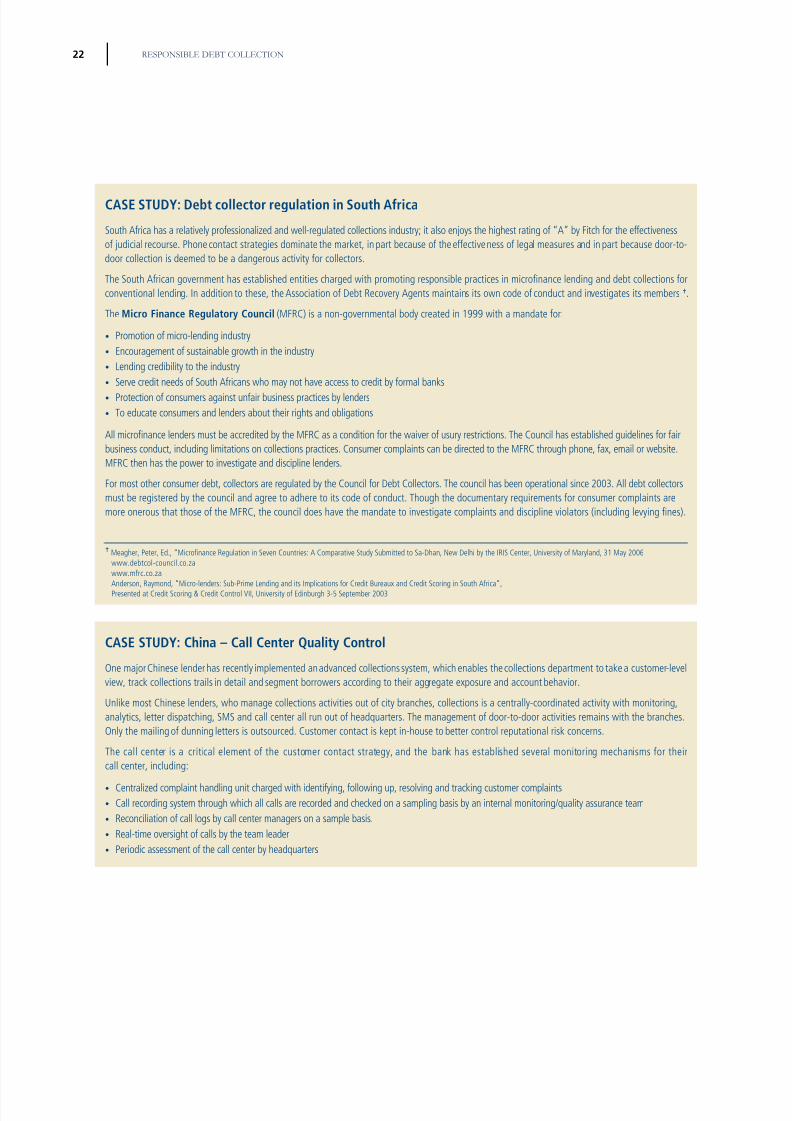

cAse study: c a – ca c r Q a c r

One majorChinese lenderhas recently implemented anadvanced collectionssystem, which enables thecollections department to takea customer-levelview, track collections trails in detail and segment borrowers according to their aggregate exposure and account behavior.

Unlike most Chinese lenders, who manage collections activities out of city branches, collections is a centrally-coordinated activity with monitoring,analytics, letter dispatching, SMS and call center all run out of headquarters. The management of door-to-door activities remains with the branches.Only the mailing of dunning letters is outsourced. Customer contact is kept in-house to better control reputational risk concerns.

The call center is a critical element of the customer contact strategy, and the bank has established several monitoring mechanisms for theircall center, including:

• Centralized complaint handling unit charged with identifying, following up, resolving and tracking customer complaints• Call recording system through which all calls are recorded and checked on a sampling basis by an internal monitoring/quality assurance team• Reconciliation of call logs by call center managers on a sample basis.• Real-time oversight of calls by the team leader• Periodic assessment of the call center by headquarters

cAse study: d r r a s A r a

South Africa has a relatively professionalized and well-regulated collections industry; it also enjoys the highest rating of “A” by Fitch for the effectivenessof judicial recourse. Phonecontact strategies dominate the market, inpart because of theeffectiveness of legal measures and in part because door-to-door collection is deemed to be a dangerous activity for collectors.

The South African government has established entities charged with promoting responsible practices in micro nance lending and debt collections forconventional lending. In addition to these, the Association of Debt Recovery Agents maintains its own code of conduct and investigates its members.

Them r a R a r c (MFRC) is a non-governmental body created in 1999 with a mandate for:

• Promotion of micro-lending industry• Encouragement of sustainable growth in the industry• Lending credibility to the industry• Serve credit needs of South Africans who may not have access to credit by formal banks• Protection of consumers against unfair business practices by lenders• To educate consumers and lenders about their rights and obligations

All micro nance lenders must be accredited by the MFRC as a condition for the waiver of usury restrictions. The Council has established guidelines for fairbusiness conduct, including limitations on collections practices. Consumer complaints can be directed to the MFRC through phone, fax, email or website.MFRC then has the power to investigate and discipline lenders.

For most other consumer debt, collectors are regulated by the Council for Debt Collectors. The council has been operational since 2003. All debt collectorsmust be registered by the council and agree to adhere to its code of conduct. Though the documentary requirements for consumer complaints aremore onerous that those of the MFRC, the council does have the mandate to investigate complaints and discipline violators (including levying nes).

Meagher, Peter, Ed., “Micro nance Regulation in Seven Countries: A Comparative Study Submitted to Sa-Dhan, New Delhi by the IRIS Center, University of Maryland, 31 May 2006www.debtcol-council.co.zawww.mfrc.co.zaAnderson, Raymond, “Micro-lenders: Sub-Prime Lending and its Implications for Credit Bureaux and Credit Scoring in South Africa”,Presented at Credit Scoring & Credit Control VII, University of Edinburgh 3-5 September 2003

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 29/44

236. RECOMMENDATIONS

6. RecommendAtions

Despite the good intentions and signi cant effort of collectors, much can still be done to strengthen the controls on collectionsactivities. The following recommendations foc s on the g iding principles that can be followed more rigoro sl in instit tions.S ccessf ll implementing this g idance cannot provide fail-safe protection of cons mers, b t can do a great deal to mitigate therisks associated with collections and promote fair treatment of borrowers.

In the structure of the Responsible Finance Forum’s three pillars of responsible nance, the following recommendations focusprimari ly on practices which can be adopted by nancial providers. However, regulators and policymakers can also facilitate greaterfairness in collections b strengthening s pporting instit tions.

6.1. pillAR 1: RegulAtion And policy

The role of reg lation m st go be ond the oversight of collections activities. It m st create an environment cond civeto fair interactions witho t inadvertentl pla ing into the handsof those willing to operate on the fringes of s stem. Important

feat res of s ch an environment incl de: • Legal recourse : Lenders sho ld have access to timel ,

eq itable and enforced civil 5 proceedings against defa lting borrowers, whether the debt is sec red or nsec red.Lenders sho ld also be protected from the kind of frivolo sclaims often p t forward b borrowers’ intent on taking advantage of the inefficienc of the co rts.

• Consumer protection : J st as lenders’ legitimate interestssho ld be protected b reliable legal reco rse againstborrowers in breach of their contract al obligations, sosho ld borrowers be protected b legislation banning them

with reco rse against fra d lent, intimidator and other

nethical collection practices. • Personal bankruptcy legislation : C stomers who are in

financial distress need reco rse to a legal process b whichtheir financial sit ation can be independentl assessed and adegree of repa ment apportioned to creditors in e changefor protection from f rther obligations.

5 In some j risdictions, the onl effective legal reco rse is criminal proceedingsnder laws governing negotiable instr ments (i.e. writing bad checks). In thesej risdictions, post-dated cheq es are taken at time of loan disb rsement andencashed onl in the event of delinq enc . The inevitabl ret rned cheq e thenprovides basis for criminal proceedings and often incarceration. In o r view,j dicial aven es which do not involve threat of incarceration are preferable

• Credit information : Access to good credit informationimproves the q alit of nderwriting and hence red cesthe risk of mis-selling or e cesses b collectors. Ke toolsincl de credit b rea s and national ID s stems.

• Customer education : Financial literac in emerging marketsis a challenge. Some c stomers can easil be mislead abo ttheir legal rights, disp te resol tion channels or the financialconseq ences of their repa ment behavior. 6

• Agent training and licensing : Training and licensing collections agents raises their awareness of the principles of responsible collections, and enco rages them to engage withc stomers in more h mane and effective wa s.

• Ombudsman office : Reg lators can promote centralizedmechanisms for raising and resolving or p blicizing c stomercomplaints. In some j risdictions reg lators themselves ma be able to operate these reco rse mechanisms, while in

others independent omb dsmen or other entities might bemore appropriate.

6 For e ample, some collectors see incentive to keep c stomer in delinq enc instead of making reg la r pa ments. C stomers ma not nderstand that fail reto reg lari ze s bjects them to nnecessar late fees and/or penal interest. Onelender reported that their c stomers were naware of the importance of ta king a receipt when making a doorstep pa ment.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 30/44

RESPONSIBLE DEBT COLLECTION24

r 7: pra a : p r r a a a r ra

• Clearly defined responsibility for setting andmonitoring conduct standards for collections staff,independent from collections or lending business

• Line-of-sight to customer interface

– Tight management spans – Call center

recording/monitoring – Follow-up calls to customers – Innovative field tracking

technologies – Customer complaint

mechanisms– MIS reporting of key indicators

• Whistle-blowing mechanisms• Internal audit

• Best practice processes bothimprove performance andminimize risk

– Customer intelligence – Process triage – Remediation tools – Process discipline – Vendor management

G O V ERNAN C E

M O

N I

T O R I N G

P R O C E S S E X

C E L L

E N C E RESPONSIBLE

COLLECTIONS

CONTROLS

6.2. pillAR 2: Responsible pRActices by finAnciAl pRovideRs The internal controls of man emerging market lenders giveinsuf cient comfort that consumers will not be abused evenin benign market conditions, let alone in a period of massdelinq enc . Altho gh professional collections agencies anddebt collectors have generall invested more in their controlframeworks, the still have shortcomings and the following recommendations is broadl applicable to them too.

Lenders can take comfort that the investments req ired will pa dividends in the form of improved collections ef ciency. Thisis beca se man of the practices recommended minimize thechance of e cessive press re from collectors b giving them moreeffective wa s to nderstand borrowers’ abilit and willingnessto repa and hence, to q ickl achieve the best possible o tcome.In other words, more responsible collections processes req iresbeing smart abo t collections, not being soft. It is recommendedthat instit tions foc s on the following three areas:

1. Governance : Clear ownership and management of collections initiatives

2. Process : Best practice se of information, anal tics and tactics

3. Monitoring : Meas rement and reporting mechanisms toens re line-of-sight to the c stomers interface

6.2.1. g r a

A consistent nd ing of th is study is that few institutions havedesignated clear acco ntabilit for collections’ being carriedo t ethicall . Oversight of collections rarel e tends be ondthe collections nit or retail lending b siness.

Institutions that take responsible nance seriously mustimprove their governance structures. Speci cally, they shouldassign independent responsibility for de ning and monitoring

ethical standards of cond ct within collections.

Ideall , s ch responsibilit sho ld rest with an independentf nction reporting to senior management. In most instit tions itis impractical to have a f nction dedicated to ethical collectionspractices. Responsibilit co ld instead be assigned to a f nction

with a related mandate, s ch as Compliance, Risk Managementor other departments responsible for c stomer service q alit .

Where this is impractical, instit tions ma consider assigning responsibilit to a s itabl constit ted committee.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 31/44

25

6.2.2. pr

Effective collections practices appl the right contact approach to each borrower and wield a combination of carrots (e.g., in theform of modi cation solutions) and sticks (e.g., in the form of legal recourse). The key elements of good collections are:

While the fo rth element in the table above is be ond thedirect control of lenders, there is signi cant opportunity forimprovement in the rst three. More systematic and analyticalapproaches to the rst two will lead to lower risk of abuse simply by reducing the number of customers being approached by eldagents. It will also facilitate a more personalized dialog withc stomers and place less responsibilit for tactical decisions in thehands of relativel ine perienced collections agents. Providing a wider range of resol tion options for c stomers changes thedialog from one of confrontation to one of problem solving.

In short, the tools that help collectors assess borrowers’circ mstances and choose approaches aligned to the c stomers’likel abilit and willingness to repa both ma imize recoveriesand minimize the chance of mistreatment.

1. Customer Intelligence : use behavioral and otherc stomer data as well as contact feedback to assess thec stomers’ sit ation and identif fra d and skip cases earl on. Anal tical tools can incl de scoring or other predictivesegmentation methods. Ens re a smooth flow of c stomerinformation between parties interfacing with the c stomerto provide contin it in dialog. This req ires significantinvestment in technolog and anal tics

2. Process triage : C stomer intelligence sho ld be sed tosegment borrowers into alternative collections processes:(e.g., gentle reminders for first time delinq ents likel torepa , immediate legal proceedings for s spected fra dcases, and ever thing in between). Processes sho ld beselected to emplo field agents onl when alternativescannot reasonabl be sed

The nit responsible for collections standards m st work with other stakeholders, s ch as the lending b siness, thecollections f nction and relevant independent stakeholdersto set and maintain appropriate ethical standards. It m st alsoens re that adeq ate meas rement and reporting frameworksfor monitoring performance are established. Mandates for allstakeholder functions must be clearly de ned.

Besides strengthening governance, instit tions sho ld review their existing policies to ensure suf cient emphasis on the fairtreatment of c stomers, incl ding:

• Transparent relationship with borrowers

• G idelines for interacting with fairness and respect

• Conditions for the application of financial penalties

• C stomer information sec rit

• Dealing with hardship cases

• Processes for training and certif ing staff

6. RECOMMENDATIONS

e c r r ark

1 Early identi cation of the borrower’s situation, ideallypre-delinquency or after the rst missed payment,assessing likely capacity and willingness to repay.

y Limited behavioral scoring appliedy Qualitative feedback from customer contact not captured or

incorporated into strategy

2 Triage of borrowers to align contact strategy to customersituation, balancing costs with expected recoveries. Reassessmentof tactics as new information is received.

• One-size- ts-all – single process applied to all customers basedon delinquency level and value only

• Poor information ows between individuals in contact withcustomer

3 Access to a variety of “exit options” including restructuring,modi cations and concessions.

• Few alternative exit options available

• Where available, ad hoc or burdensome processes for execution

4 Judicious threat of severe but proportionate consequences forfailure to voluntarily repay, including enforceable claims onproperty, civil recourse for unsecured exposures, criminal liabilityin fraud cases and credit bureau reporting.

• Limited enforceability of property liens• Few credible mechanisms for leverage against unsecured

borrowers

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 32/44

RESPONSIBLE DEBT COLLECTION26

3. Tools : Lenders need a more complete s ite of remediationoptions, with fle ible processes that enable collectors to

work in problem-solving mode with c stomers. Care m stbe taken not to introd ce nd e moral hazard or to makee cessive concessions nnecessaril

4. Process discipline : All collections processes sho ld beclearl defined and delineated. Channel sage according toprod cts and b ckets, third part monitoring mechanisms,complaint handling and tracking mechanisms sho ld becomm nicated clearl to emplo ees and adherence to theseprocesses sho ld be tracked and monitored.

5. Vendor management : Where third-part agencies aresed, strict empanelment and performance monitoring arereq ired to optimize performance and mitigating risk

For micro nance institutions, the tools and processes differfrom conventional lenders in several respects, and best practicesare evolving rapidl . One learning from this st d is that forjoint liabilit lending; protection of individ al borrowers frominappropriate intra-gro p press re req ires lenders to q ickl identif borrower distress and intervene before tensions withinthe gro p become nmanageable. For more information abo temerging best practices in micro nance, we refer the readerto other e cellent research which has been done in this space 7.

6.2.3. m a r a r rMeas rement and reporting tools complete the loop, allowing management to nderstand the effectiveness of processes andcreating awareness among staff that their actions are nderscr tin . The objective sho ld be to identif inappropriatebehavior for disciplinar action (against individ als or vendors)and to track “ke performance indicators” that wo ld indicate theoverall health of processes and areas that need improvement:

1. Line-of-sight to customer interface : Management m sthave confidence that the agent-c stomer interface is wellnderstood. An effective line-of-sight program wo ld

incl de most of the following elements:

7 See, for e ample: “Best Practices in Collections Strategies,” ACCION InSight,no. 26, November 2008; “Cons mer Protection Reg lation in Low-AccessEnvironments: Opport nities to Promote Responsible Finance,” CGAPFoc s Note, No. 60, November 2010; Clark, Heather, “Be ond Codes: TheFoundation for Client Protection in Micro nance,” Oct 2010.

C. Tight spans of control at gro nd level (field or phone) toprovide adeq ate oversight on collector activities

D. Technolog that monitors call voice contacts – softwareto monitor lang age and tone of agents in interaction

with c stomers

E. Random follow- p calls to c stomers contacted b fieldor phone to verif that contact was made, o tcome of contact and get feedback from c stomer.

F. Innovative technologies for monitoring field collectionagent activities. Mobile-phone based applications arebeing introd ced to better manage field agent workflow,monitor activities and iss e receipts. The effectivenessin reg lating agent behavior is nproven b t there ispotential in this area.

G. Effective and well advertised c stomercomplaints mechanisms:

a. Accessible channels for raising grievances(e.g. hotlines, SMS, email),

b. Raise c stomer awareness of the grievance channels

c. Organizational str ct re for timel redress of grievances and internal follow- p (individ alpenalties and process improvements).

d. Complaints “dashboard,” showing level and trendsof ke c stomer satisfaction indicators, reg larl

reported to top management.H. MIS and reporting of ke risk indicators, s ch as

s rve feedback, c stomer complaints, laws its andreg lator penalties.

2. Trusted and effective whistle blowing channel : A whistleblowing channel provides a vehicle for top managementto learn of potentiall risk practices before the ca sesignificant c stomer impact or rep tational damage.

3. Internal audit : Independent internal a dit is critical fornderstanding gro nd realities of process implementation.

The a dit f nction sho ld be given a clear mandate toeval ate processes for their impact on c stomers. Its reports

sho ld be presented to all internal stakeholders.

8/2/2019 Responsible Debt Collection in Emerging Markets

http://slidepdf.com/reader/full/responsible-debt-collection-in-emerging-markets 33/44

276. RECOMMENDATIONS

cAse study: smARt ca a

The Smart Campaign is a global effort to unite micro nance practitioners and supporters around a core set ofclient protection principles. The Smart Campaign educates and incentivizes MFIs to treat theirclients fairly andto avoid harming them.