result update emamibreport.myiris.com/es1/himani_20130208.pdf · · 2013-02-11antiseptic cream...

TRANSCRIPT

Edelweiss Research is also available on www.edelresearch.com,

Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset.

Edelweiss Securities Limited

Emami’s Q3FY13 sales and PAT came bang in line with our estimates. Key

positives were: (i) sustained 16% YoY volume growth in domestic market;

(ii) continued improvement in international business while a few

companies have reported slowdown (up 25% YoY against 3% YoY in

Q2FY13 and 30% YoY decline in Q1FY13); (iii) 30% YoY growth in Boroplus

with 28-30% YoY volume growth and 270bps YoY market share gains (to

78%); (iv) 300bps YoY market share gain in Navratna oil to 58%, with

market leadership in UP and Bihar; and (v) robust CSD, modern trade and

rural growth (12%, 30% and 31% YoY respectively). The only negative was

3-4% YoY growth in Himani Fast Relief. Emami will benefit from

correction in mentha oil in FY14. Maintain ‘BUY’.

This report also contains Q3FY13 earnings call highlights

Volume growth robust; higher expenses nip margins

Emami’s Q3FY13 net sales rose 21.3% YoY to INR5.5bn led by 16% YoY domestic

volume growth backed by early onset of winter (led by power brands). International

business surged 25% YoY with robust spurt in SAARC, particularly Bangladesh (up 90%

YoY) and Africa (up 30% YoY); CIS continues to face problems. EBITDA margin declined

110bps YoY owing to rise in staff cost (up 63bps YoY) and ad spending (up 82bps YoY)

despite lower other costs (down 18bps YoY). PAT before exceptional increased 16.4%

YoY. Bangladesh unit commenced operations during the quarter.

Navratna well oiled; resurgence of Fair and Handsome

The company reported robust 21.7% YoY growth in domestic market. Boroplus

Antiseptic Cream grew 30% plus YoY, Zandu Pancharishta grew 3x YoY, balm category

grew 17% YoY, Fair and Handsome grew 19% YoY and OTC, ethicals grew 25% YoY.

Navratna portfolio rose 13% YoY with 300bps YoY market share gain (to 58%).

Outlook and valuations: Positive; maintain ‘BUY’

We like Emami’s focus on strengthening its brand equity, mass market product

portfolio and enhancing rural penetration. At CMP, the stock is trading at P/E of 27.9x

and 23.0x on FY13E and FY14E EPS, respectively. We maintain ‘BUY/Sector Performer’.

RESULT UPDATE

EMAMI Double delight: Domestic, global businesses shine

EDELWEISS 4D RATINGS

Absolute Rating BUY

Rating Relative to Sector Performer

Risk Rating Relative to Sector High

Sector Relative to Market Underweight

MARKET DATA (R: EMAM.BO, B: HMN IN)

CMP : INR 576

Target Price : INR 675

52-week range (INR) : 658 / 358

Share in issue (mn) : 151.3

M cap (INR bn/USD mn) : 87 / 1,625

Avg. Daily Vol.BSE/NSE(‘000) : 98.5

SHARE HOLDING PATTERN (%)

Current Q2FY13 Q1FY13

Promoters *

72.7 72.7 72.7

MF's, FI's & BK’s 4.0 3.6 4.0

FII's 14.3 14.6 14.7

Others 8.9 9.0 8.6

* Promoters pledged shares

(% of share in issue)

: 8.0

PRICE PERFORMANCE (%)

Stock Nifty

EW Consumer

Goods Index

1 month (0.1) (1.0) 4.9

3 months 1.6 4.4 13.5

12 months 59.1 11.8 45.0

Abneesh Roy

+91 22 6620 3141

Hemang Gandhi

+91 22 6620 3148

Pooja Lath

+91 22 6620 3075

India Equity Research| Consumer Goods

February 8, 2013

Financials (INR mn)

Year to March Q3FY13 Q3FY12 % change Q2FY13 % change FY12 FY13E FY14E

Net sales 5,487 4,524 21.3 3,607 52.1 14,535 17,174 20,566

EBITDA 1,369 1,178 16.2 641 113.6 2,968 3,521 4,268

PAT 1,150 945 21.6 592 94.2 2,588 3,127 3,782

Dil. EPS (INR) 7.6 6.2 21.6 3.9 94.2 17.1 20.7 25.0

Diluted P/E (x) 33.7 27.9 23.0

EV/EBITDA (x) 28.7 23.9 19.2

ROAE (%) 37.1 41.7 44.3

Consumer Goods

2 Edelweiss Securities Limited

Q3FY13 Conference call: Key highlights

Sales growth: Sales surged 21.3% YoY to ~INR5.5bn; international business growth

improved significantly at 25% YoY (against 3% growth in Q2FY13 and 30% YoY decline in

Q1FY13). Domestic business revenue grew 21.7% YoY backed by strong volume growth of

16% YoY (16% YoY in Q2FY13) due to robust surge across portfolio (aided by early winters).

Rural sales: Rural India contributed 52-53% to total revenue. Direct route in rural markets

grew an impressive 31% YoY. 25% of total direct reach is dedicated to rural areas.

International business: International portfolio grew 25% YoY (against 3% in Q2FY13 and

30% YoY decline in Q1FY13).

Growth was robust in SAARC, particularly Bangladesh (up 90% YoY; 60% YoY in Q2FY13).

The manufacturing plant in Bangladesh will be operational from FY14 which will lead to

huge tax savings as Bangladesh has import duties which range from 70-100%. The plant will

help reduce 90% of imports. Bangladesh offers huge scope for growth and management

expects to garner sales of INR550-600mn in FY13E and INR900mn in FY14E.

Africa business grew a strong 30% YoY. However, CIS continued to disappoint with a 10%

YoY decline in revenue. Management will be focusing more on SAARC, Africa and Middle

East business.

Navratna oil: Navratna portfoilio grew 13% YoY (led by 5% YoY volume surge). Market

share was up 300bps YoY to 58% (against 57.7% in Q2FY13) and has seen good growth

across the country. Cooling Oil grew 13% YoY and saw strong growth in Uttar Pradesh and

Bihar (gained 5% market share YoY to 30%).

Balms: The balm category grew 17% YoY led by strong volume growth of 18-20% YoY. Value

market share was maintained at 57% in 9mFY13.

Boroplus: Boroplus brands grew a robust 33% YoY. Boroplus Antiseptic Cream (contributed

12% to revenue) grew 30% YoY with 28-30% YoY volume growth. Market share was up

270bps YoY to 78%. Boroplus Winter Lotion grew 40% plus YoY and market share increased

100bps YoY to 7.5% in Q3FY13.

Fair & Handsome: Fair and Handsome (contributed 10% to revenue) revenue posted

recovery with 19% YoY growth led by 10-12% volume growth. Despite fierce competition

from the market leader (Fair & Lovely), Fair and Handsome’s market share has increase

400bps YoY at the cost of likely loss by market share by the leader.

Zandu ethical business: This portfolio has grown 25% YoY led by strong performance in

Lalima and Pancharishta.

Himani Fast Relief: The brand grew a mere 3-4% YoY.

New products: New products like Baby Talc and Glucose received lukewarm response.

Management believes brand strategy of these products may need a change.

CSD: CSD sales saw a good revival, with 12% growth YoY (posted flat growth in Q2FY13 and

10% YoY dip in Q1FY13).

Emami

3 Edelweiss Securities Limited

Modern trade: Modern trade grew 50% YoY and LTL growth stood at 30% YoY (on a small

base). Management expects 35% plus growth to sustain in modern trade.

Raw material: Gross margin expanded 18bps YoY to 62% helped by efficient cost

management and price hikes. Mentha oil prices have seen some cooling off QoQ, but

remained higher YoY. Market price for Mentha oil is ~INR1,550-1,600; cost for Emami was

INR1,900 till March 2013 due to contracts signed earlier. Average mentha oil price for the

year is ~INR1,700-1,800. Management believes that if current prices persist, gross margin

will improve in from Q1FY14.

Ad spends: Ad spends were up 82bps YoY to 18.6% as percentage of sales. Management

has maintained that ad spending will be around 17.0-17.5% of sales in FY13E (Q4FY13 will

not see aggressive ad spending).

Employee costs: Employee costs increased 63bps YoY to 5.7% as percentage of sales on

back of recruitment in the international business and in R&D team.

Tax rate: Management has guided for a tax rate of 17% for FY14, which will increase going

forward (20% FY15 onwards).

Distribution network: Emami has 1,600 frontline people with direct reach 600,000 (500,000

in Q3FY12).

Capex: Total capex will be in the INR500-600mn range in FY14E and FY15E.

Outlook and valuations: Positive; maintain ‘BUY’

We like Emami’s focus on continuous strengthening of its brand equity, focus on the mass-

market product portfolio, scale up of Zandu brands, and increasing rural penetration, and

believe commissioning of new plant in Bangladesh will boost volume. We maintain target

PE multiple of 27x arriving at target price of INR675. At CMP, the stock is trading at P/E of

27.9x and 23.0x on FY13E and FY14E EPS, respectively. We maintain ‘BUY’ with ‘Sector

Performer’ rating on the stock

Consumer Goods

4 Edelweiss Securities Limited

Table 1: Volume versus value growth

Source: Company, Edelweiss research

Chart 1: EBITDA margin dips 110bps YoY

Source: Company, Edelweiss research

Chart 2: Softening in mentha oil prices to benefit margins

Source: Company, Edelweiss research

% value growth % volume growth

Navratna 13.0 5.0

Boroplus 30+ 28-30

Balm 17.0 18-20

Zandu ethical 25.0 NA

Fair and Handsome 19.0 10-12

Q3FY13

0.0

7.0

14.0

21.0

28.0

35.0

Q1

FY

11

Q2

FY

11

Q3

FY

11

Q4

FY

11

Q1

FY

12

Q2

FY

12

Q3

FY

12

Q4

FY

12

Q1

FY

13

Q2

FY

13

Q3

FY

13

(%)

0

648

1,296

1,944

2,592

3,240

Jul-

09

Oc

t-0

9

Jan

-10

Ap

r-1

0

Jul-

10

Oc

t-1

0

Jan

-11

Ap

r-1

1

Jul-

11

Oc

t-1

1

Jan

-12

Ap

r-1

2

Jul-

12

Oc

t-1

2

Jan

-13

(IN

R)

Emami

5 Edelweiss Securities Limited

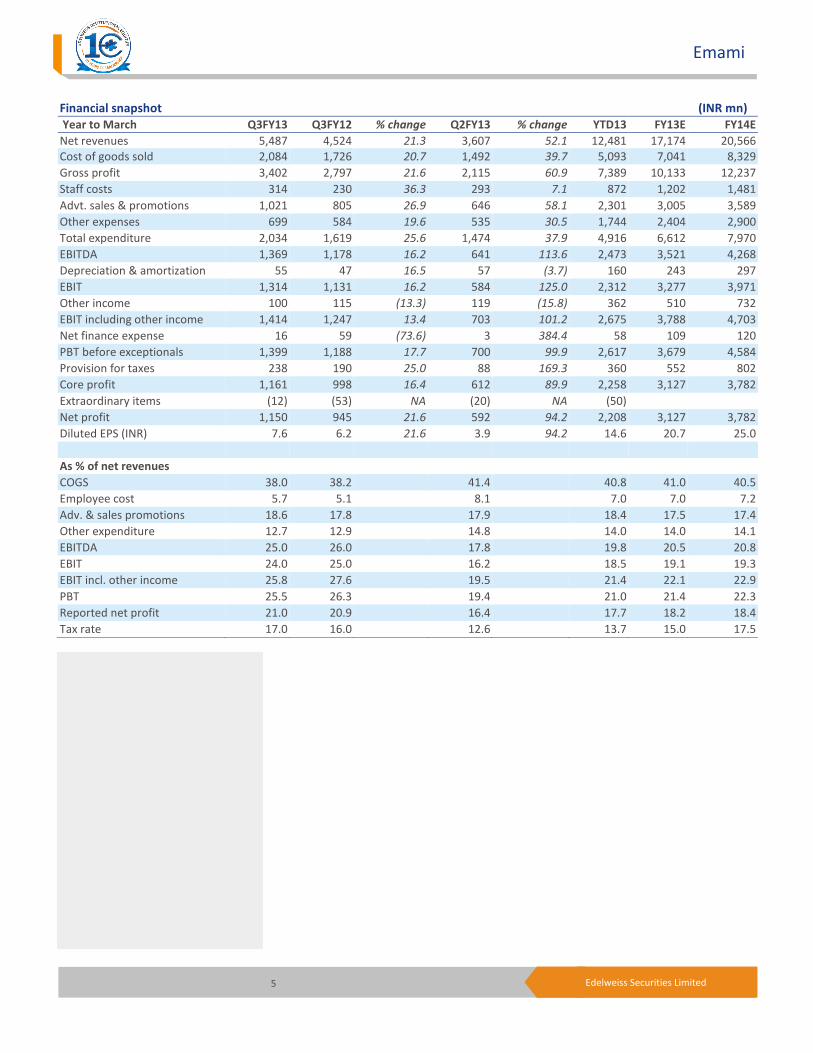

Financial snapshot (INR mn)

Year to March Q3FY13 Q3FY12 % change Q2FY13 % change YTD13 FY13E FY14E

Net revenues 5,487 4,524 21.3 3,607 52.1 12,481 17,174 20,566

Cost of goods sold 2,084 1,726 20.7 1,492 39.7 5,093 7,041 8,329

Gross profit 3,402 2,797 21.6 2,115 60.9 7,389 10,133 12,237

Staff costs 314 230 36.3 293 7.1 872 1,202 1,481

Advt. sales & promotions 1,021 805 26.9 646 58.1 2,301 3,005 3,589

Other expenses 699 584 19.6 535 30.5 1,744 2,404 2,900

Total expenditure 2,034 1,619 25.6 1,474 37.9 4,916 6,612 7,970

EBITDA 1,369 1,178 16.2 641 113.6 2,473 3,521 4,268

Depreciation & amortization 55 47 16.5 57 (3.7) 160 243 297

EBIT 1,314 1,131 16.2 584 125.0 2,312 3,277 3,971

Other income 100 115 (13.3) 119 (15.8) 362 510 732

EBIT including other income 1,414 1,247 13.4 703 101.2 2,675 3,788 4,703

Net finance expense 16 59 (73.6) 3 384.4 58 109 120

PBT before exceptionals 1,399 1,188 17.7 700 99.9 2,617 3,679 4,584

Provision for taxes 238 190 25.0 88 169.3 360 552 802

Core profit 1,161 998 16.4 612 89.9 2,258 3,127 3,782

Extraordinary items (12) (53) NA (20) NA (50)

Net profit 1,150 945 21.6 592 94.2 2,208 3,127 3,782

Diluted EPS (INR) 7.6 6.2 21.6 3.9 94.2 14.6 20.7 25.0

As % of net revenues

COGS 38.0 38.2 41.4 40.8 41.0 40.5

Employee cost 5.7 5.1 8.1 7.0 7.0 7.2

Adv. & sales promotions 18.6 17.8 17.9 18.4 17.5 17.4

Other expenditure 12.7 12.9 14.8 14.0 14.0 14.1

EBITDA 25.0 26.0 17.8 19.8 20.5 20.8

EBIT 24.0 25.0 16.2 18.5 19.1 19.3

EBIT incl. other income 25.8 27.6 19.5 21.4 22.1 22.9

PBT 25.5 26.3 19.4 21.0 21.4 22.3

Reported net profit 21.0 20.9 16.4 17.7 18.2 18.4

Tax rate 17.0 16.0 12.6 13.7 15.0 17.5

Consumer Goods

6 Edelweiss Securities Limited

Company Description

Emami is the flagship company of Emami group. It is a leading FMCG player in India,

operating in certain attractive segments such as skin care and hair oil. The company is

promoted by Kolkata-based industrialists, Mr. R.S. Agarwal and Mr. R. S. Goenka. The

company has been operating in health, beauty and personal care products for the past 30

years and has sustained a prominent position in therapeutic and Ayurvedic based products,

ensuring strong entry barriers for competition.

Over the years, Emami has innovated and built block-buster brands such as Navratna,

Boroplus, and Fair and Handsome. With the acquisition of ‘Zandu’, another strong Ayurvedic

brand was added to the portfolio. ~80% of the business is from wellness categories,

ensuring strong brand loyalty and ~80% of the company’s production is in tax exempt zones.

Recently, the Emami Group Company announced plans to enter the edible oil business as

well as a tie up with Disney for making toys. Since margins in both of these businesses are

very different from the listed Emami business, these businesses are launched through

different legal entities with no impact on the listed FMCG business.

Investment Theme

Emami’s product portfolio provides a play on Indian FMCG spend by virtue of its strong

presence in less penetrated and high growth categories. More than 80% of Emami’s

products have Ayurvedic base. The therapeutic usage gives customer loyalty leading to high

gross margins, high barriers to entry, strong brand equity, mass acceptance and superior

growth opportunities. Emami has a superior track record of launching new brands (Fair &

Handsome, first fairness cream for men in India) and transforming them into blockbusters.

Emami does not compete with any large multinational or domestic player in its key

segments (except skin creams). Introduction of lower SKUs for Zandu balm and rejuvenating

more than 200 of Zandu’s Ayurvedic-based prescription products will be another growth

driver for Emami.

Key Risks

Seasonality risk is one of the biggest risks to Emami. Summer products (like Talc) and winter

products (like Boroplus) sales depend upon the weather conditions. Any disruption in

weather conditions can result in volatile sales of some of these products. With the

popularisation and increase in mass consumption of herbal products, several key ingredients

might be difficult to source.

Ayurvedic products are produced by more than a thousand small companies in India,

though only about a dozen are big national players. Given Emami’s success, entry of new

competitors cannot be ruled out. Hence, Emami, like other FMCG players, will need to

continuously invest in A&P to build superior brand equity and gain customer loyalty.

7 Edelweiss Securities Limited

Emami

Financial Statements

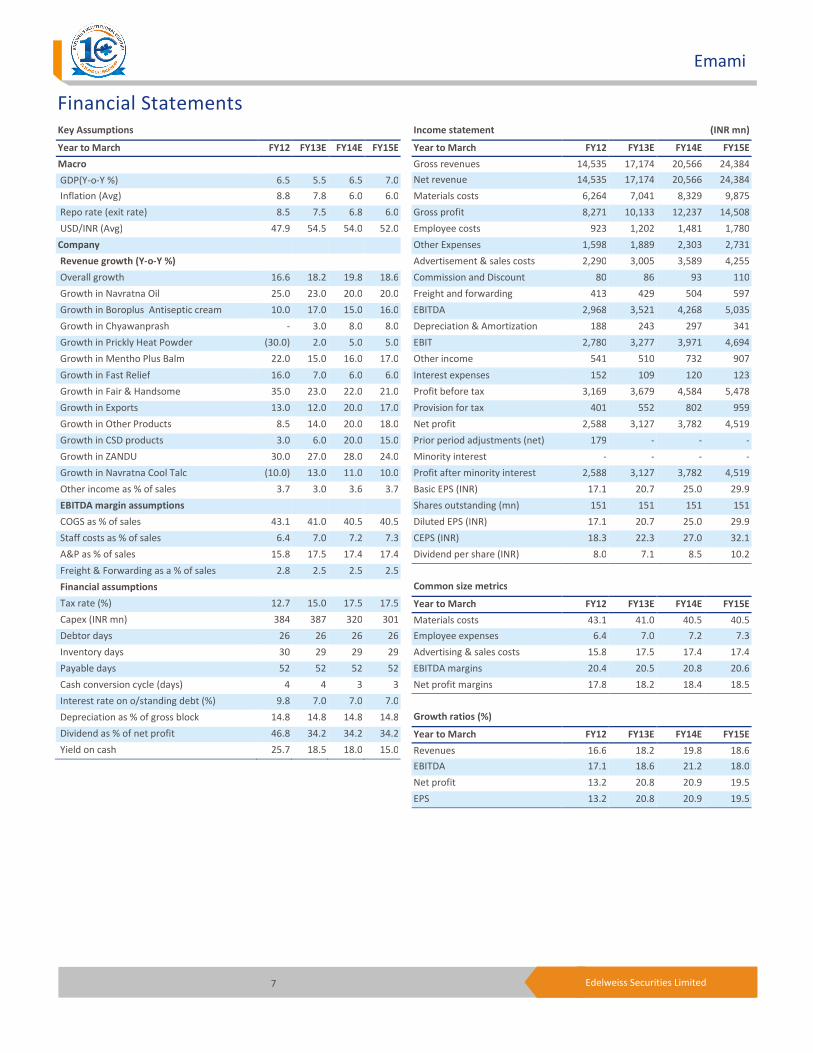

Income statement (INR mn)

Year to March FY12 FY13E FY14E FY15E

Gross revenues 14,535 17,174 20,566 24,384

Net revenue 14,535 17,174 20,566 24,384

Materials costs 6,264 7,041 8,329 9,875

Gross profit 8,271 10,133 12,237 14,508

Employee costs 923 1,202 1,481 1,780

Other Expenses 1,598 1,889 2,303 2,731

Advertisement & sales costs 2,290 3,005 3,589 4,255

Commission and Discount 80 86 93 110

Freight and forwarding 413 429 504 597

EBITDA 2,968 3,521 4,268 5,035

Depreciation & Amortization 188 243 297 341

EBIT 2,780 3,277 3,971 4,694

Other income 541 510 732 907

Interest expenses 152 109 120 123

Profit before tax 3,169 3,679 4,584 5,478

Provision for tax 401 552 802 959

Net profit 2,588 3,127 3,782 4,519

Prior period adjustments (net) 179 - - -

Minority interest - - - -

Profit after minority interest 2,588 3,127 3,782 4,519

Basic EPS (INR) 17.1 20.7 25.0 29.9

Shares outstanding (mn) 151 151 151 151

Diluted EPS (INR) 17.1 20.7 25.0 29.9

CEPS (INR) 18.3 22.3 27.0 32.1

Dividend per share (INR) 8.0 7.1 8.5 10.2

Common size metrics

Year to March FY12 FY13E FY14E FY15E

Materials costs 43.1 41.0 40.5 40.5

Employee expenses 6.4 7.0 7.2 7.3

Advertising & sales costs 15.8 17.5 17.4 17.4

EBITDA margins 20.4 20.5 20.8 20.6

Net profit margins 17.8 18.2 18.4 18.5

Growth ratios (%)

Year to March FY12 FY13E FY14E FY15E

Revenues 16.6 18.2 19.8 18.6

EBITDA 17.1 18.6 21.2 18.0

Net profit 13.2 20.8 20.9 19.5

EPS 13.2 20.8 20.9 19.5

Key Assumptions

Year to March FY12 FY13E FY14E FY15E

Macro

GDP(Y-o-Y %) 6.5 5.5 6.5 7.0

Inflation (Avg) 8.8 7.8 6.0 6.0

Repo rate (exit rate) 8.5 7.5 6.8 6.0

USD/INR (Avg) 47.9 54.5 54.0 52.0

Company

Revenue growth (Y-o-Y %)

Overall growth 16.6 18.2 19.8 18.6

Growth in Navratna Oil 25.0 23.0 20.0 20.0

Growth in Boroplus Antiseptic cream 10.0 17.0 15.0 16.0

Growth in Chyawanprash - 3.0 8.0 8.0

Growth in Prickly Heat Powder (30.0) 2.0 5.0 5.0

Growth in Mentho Plus Balm 22.0 15.0 16.0 17.0

Growth in Fast Relief 16.0 7.0 6.0 6.0

Growth in Fair & Handsome 35.0 23.0 22.0 21.0

Growth in Exports 13.0 12.0 20.0 17.0

Growth in Other Products 8.5 14.0 20.0 18.0

Growth in CSD products 3.0 6.0 20.0 15.0

Growth in ZANDU 30.0 27.0 28.0 24.0

Growth in Navratna Cool Talc (10.0) 13.0 11.0 10.0

Other income as % of sales 3.7 3.0 3.6 3.7

EBITDA margin assumptions

COGS as % of sales 43.1 41.0 40.5 40.5

Staff costs as % of sales 6.4 7.0 7.2 7.3

A&P as % of sales 15.8 17.5 17.4 17.4

Freight & Forwarding as a % of sales 2.8 2.5 2.5 2.5

Financial assumptions

Tax rate (%) 12.7 15.0 17.5 17.5

Capex (INR mn) 384 387 320 301

Debtor days 26 26 26 26

Inventory days 30 29 29 29

Payable days 52 52 52 52

Cash conversion cycle (days) 4 4 3 3

Interest rate on o/standing debt (%) 9.8 7.0 7.0 7.0

Depreciation as % of gross block 14.8 14.8 14.8 14.8

Dividend as % of net profit 46.8 34.2 34.2 34.2

Yield on cash 25.7 18.5 18.0 15.0

8 Edelweiss Securities Limited

Consumer Goods

Peer comparison valuation

Market cap Diluted PE (X) EV/EBITDA (X) ROAE (%)

Name (USD mn) FY13E FY14E FY13E FY14E FY13E FY14E

Emami 1,625 27.9 23.0 23.9 19.2 41.7 44.3

Asian Paints 8,095 37.1 30.2 23.7 19.6 38.8 39.9

Bajaj Corp 632 20.3 16.8 20.0 16.6 37.1 39.7

Colgate 3,381 35.3 30.1 26.1 21.9 109.9 112.6

Dabur 4,263 30.3 25.4 22.1 18.2 39.0 37.1

Godrej Consumer 4,580 35.7 29.4 25.1 21.0 20.8 21.8

Hindustan Unilever 18,261 30.5 27.7 22.8 20.4 75.0 64.9

ITC 44,375 31.3 26.8 20.4 17.4 36.8 38.6

Marico 2,628 33.1 26.5 21.0 17.0 30.9 30.0

AVERAGE 37.8 29.5 23.6 19.6 46.0 45.6

Source: Edelweiss research

Cash flow metrics

Year to March FY12 FY13E FY14E FY15E

Operating cash flow 3,688 2,907 3,877 4,639

Investing cash flow (384) (387) (320) (301)

Financing cash flow (1,557) (1,210) (1,583) (1,881)

Net cash flow 1,747 1,310 1,974 2,457

Capex (384) (387) (320) (301)

Dividends paid (1,405) (1,251) (1,513) (1,808)

Profitability & efficiency ratios

Year to March FY12 FY13E FY14E FY15E

ROAE (%) 37.1 41.7 44.3 45.1

ROACE (%) 32.4 37.1 39.8 40.8

Inventory day 30 29 29 29

Debtors days 26 26 26 26

Payable days 52 52 52 52

Cash conversion cycle (days) 4 4 3 3

Current ratio 1.1 1.3 1.4 1.5

Debt/Equity 0.2 0.2 0.2 0.2

Interest coverage 18.3 30.0 33.2 38.1

Operating ratios

Year to March FY12 FY13E FY14E FY15E

Total asset turnover 1.6 1.9 2.0 2.0

Fixed asset turnover 3.0 3.9 6.0 10.2

Equity turnover 2.1 2.3 2.4 2.4

Valuation parameters

Year to March FY12 FY13E FY14E FY15E

Diluted EPS (INR) 17.1 20.7 25.0 29.9

Y-o-Y growth (%) 13.2 20.8 20.9 19.5

CEPS (INR) 18.3 22.3 27.0 32.1

Diluted PE (x) 33.7 27.9 23.0 19.3

Price/BV (x) 12.3 11.0 9.5 8.0

EV/Sales (x) 5.9 4.9 4.0 3.3

EV/EBITDA (x) 28.7 23.9 19.2 15.8

Dividend yield (%) 1.4 1.2 1.5 1.8

Balance sheet (INR mn)

As on 31st March FY12 FY13E FY14E FY15E

Equity capital 151 151 151 151

Reserves & surplus 6,915 7,770 9,017 10,707

Shareholders funds 7,066 7,921 9,169 10,859

Minority interest (BS) 1 1 1 1

Short term debt 555 598 615 633

Long term debt 1,003 1,110 1,142 1,175

Borrowings 1,558 1,708 1,758 1,808

Deferred tax liability 145 145 145 145

Sources of funds 8,771 9,775 11,073 12,813

Tangible assets 2,366 1,977 1,459 398

Intangible assets 1,669 1,169 669 669

CWIP (incl. intangible) 768 780 800 800

Total net fixed assets 4,803 3,926 2,929 1,868

Goodwill on consolidation 42 42 42 42

Non current investments 68 68 68 68

Current Investments 736 736 736 736

Cash and equivalents 2,759 4,069 6,043 8,501

Inventories 1,122 1,387 1,655 1,956

Sundry debtors 1,005 1,232 1,469 1,735

Other current assets 1,239 1,239 1,239 1,239

Total current assets (ex cash) 3,366 3,857 4,363 4,929

Total current liabilities & 3,003 2,921 3,107 3,330

Net current assets (ex cash) 363 935 1,256 1,600

Uses of funds 8,771 9,775 11,073 12,813

Book value per share (INR) 46.7 52.4 60.6 71.8

Free cash flow (INR mn)

Year to March FY12 FY13E FY14E FY15E

Net profit 2,588 3,127 3,782 4,519

Add : Non cash charge 519 352 416 464

Gross cash flow 3,108 3,479 4,198 4,983

Less: Changes in WC (581) 572 321 344

Operating cash flow 3,688 2,907 3,877 4,639

Less: Capex 384 387 320 301

Free cash flow 3,304 2,520 3,557 4,338

9 Edelweiss Securities Limited

Emami

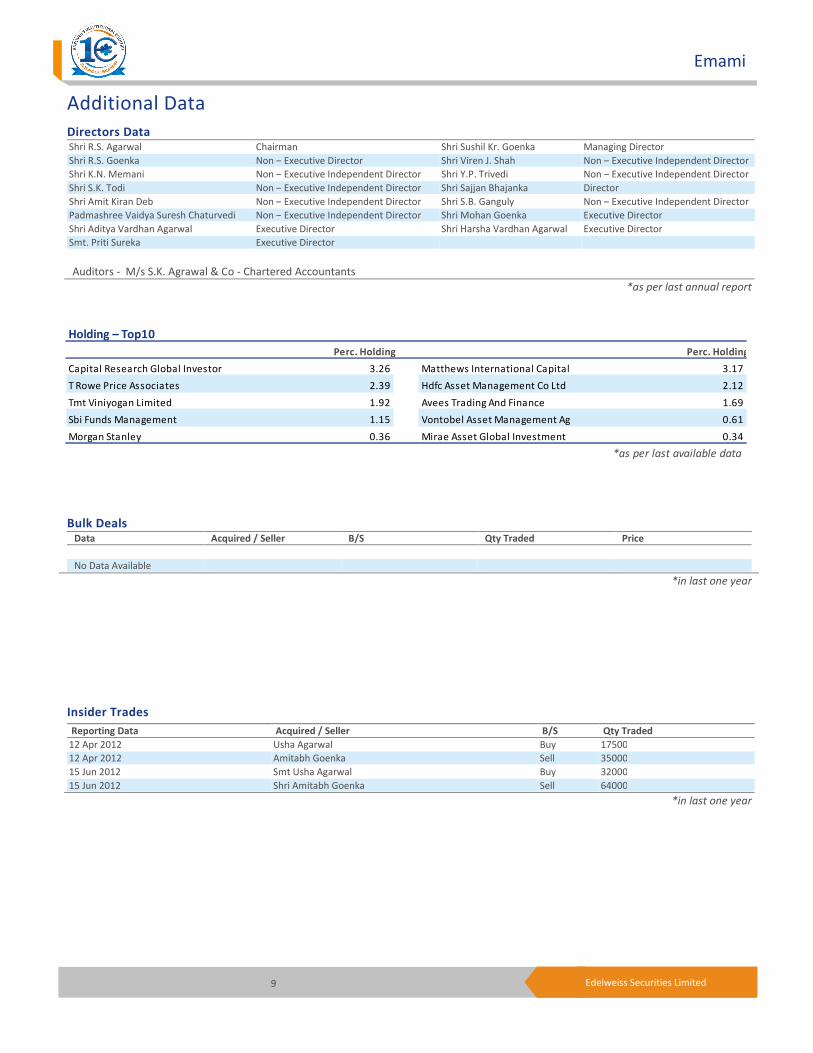

Holding – Top10

Perc. Holding Perc. Holding

Capital Research Global Investor 3.26 Matthews International Capital 3.17

T Rowe Price Associates 2.39 Hdfc Asset Management Co Ltd 2.12

Tmt Viniyogan Limited 1.92 Avees Trading And Finance 1.69

Sbi Funds Management 1.15 Vontobel Asset Management Ag 0.61

Morgan Stanley 0.36 Mirae Asset Global Investment 0.34

*as per last available data

Insider Trades Reporting Data Acquired / Seller B/S Qty Traded

12 Apr 2012 Usha Agarwal Buy 17500

12 Apr 2012 Amitabh Goenka Sell 35000

15 Jun 2012 Smt Usha Agarwal Buy 32000

15 Jun 2012 Shri Amitabh Goenka Sell 64000

*in last one year

Bulk Deals Data Acquired / Seller B/S Qty Traded Price

No Data Available

*in last one year

Additional Data

Directors Data

Shri R.S. Agarwal Chairman Shri Sushil Kr. Goenka Managing Director

Shri R.S. Goenka Non – Executive Director Shri Viren J. Shah Non – Executive Independent Director

Shri K.N. Memani Non – Executive Independent Director Shri Y.P. Trivedi Non – Executive Independent Director

Shri S.K. Todi Non – Executive Independent Director Shri Sajjan Bhajanka Director

Shri Amit Kiran Deb Non – Executive Independent Director Shri S.B. Ganguly Non – Executive Independent Director

Padmashree Vaidya Suresh Chaturvedi Non – Executive Independent Director Shri Mohan Goenka Executive Director

Shri Aditya Vardhan Agarwal Executive Director Shri Harsha Vardhan Agarwal Executive Director

Smt. Priti Sureka Executive Director

Auditors - M/s S.K. Agrawal & Co - Chartered Accountants

*as per last annual report

10 Edelweiss Securities Limited

Company Absolute

reco

Relative

reco

Relative

risk

Company Absolute

reco

Relative

reco

Relative

Risk

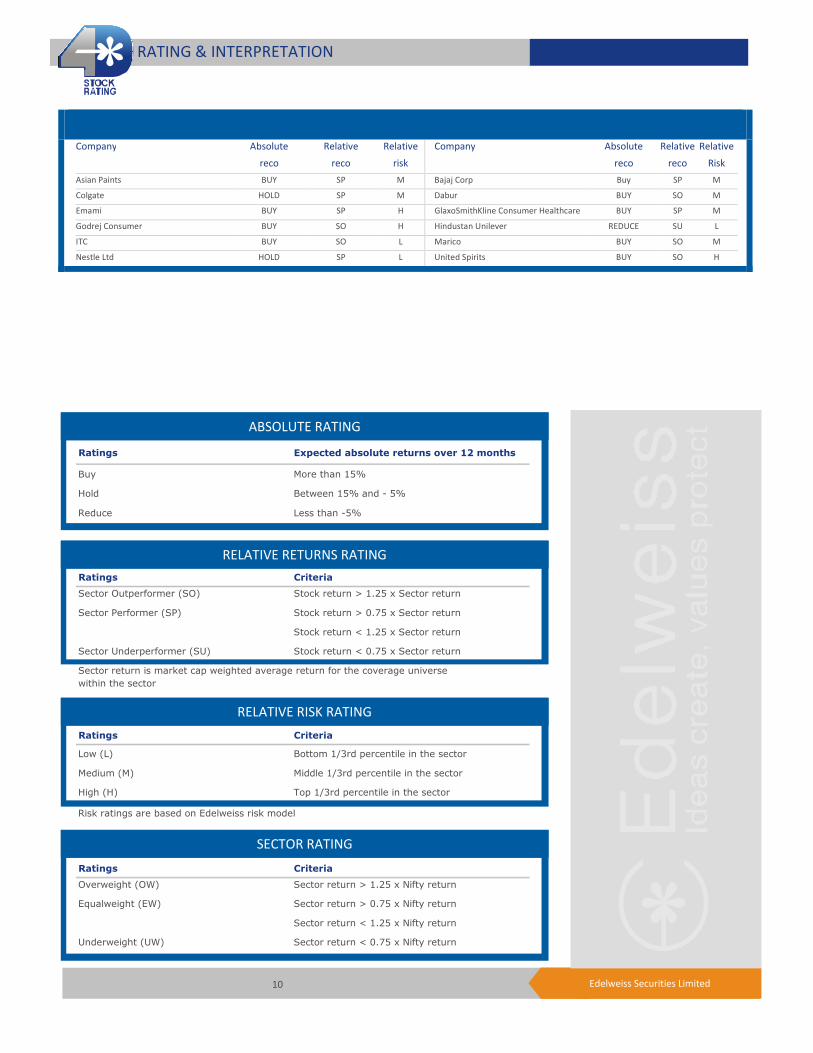

Asian Paints BUY SP M Bajaj Corp Buy SP M

Colgate HOLD SP M Dabur BUY SO M

Emami BUY SP H GlaxoSmithKline Consumer Healthcare BUY SP M

Godrej Consumer BUY SO H Hindustan Unilever REDUCE SU L

ITC BUY SO L Marico BUY SO M

Nestle Ltd HOLD SP L United Spirits BUY SO H

RATING & INTERPRETATION

ABSOLUTE RATING

Ratings Expected absolute returns over 12 months

Buy More than 15%

Hold Between 15% and - 5%

Reduce Less than -5%

RELATIVE RETURNS RATING

Ratings Criteria

Sector Outperformer (SO) Stock return > 1.25 x Sector return

Sector Performer (SP) Stock return > 0.75 x Sector return

Stock return < 1.25 x Sector return

Sector Underperformer (SU) Stock return < 0.75 x Sector return

Sector return is market cap weighted average return for the coverage universe

within the sector

RELATIVE RISK RATING

Ratings Criteria

Low (L) Bottom 1/3rd percentile in the sector

Medium (M) Middle 1/3rd percentile in the sector

High (H) Top 1/3rd percentile in the sector

Risk ratings are based on Edelweiss risk model

SECTOR RATING

Ratings Criteria

Overweight (OW) Sector return > 1.25 x Nifty return

Equalweight (EW) Sector return > 0.75 x Nifty return

Sector return < 1.25 x Nifty return

Underweight (UW) Sector return < 0.75 x Nifty return

11 Edelweiss Securities Limited

Emami

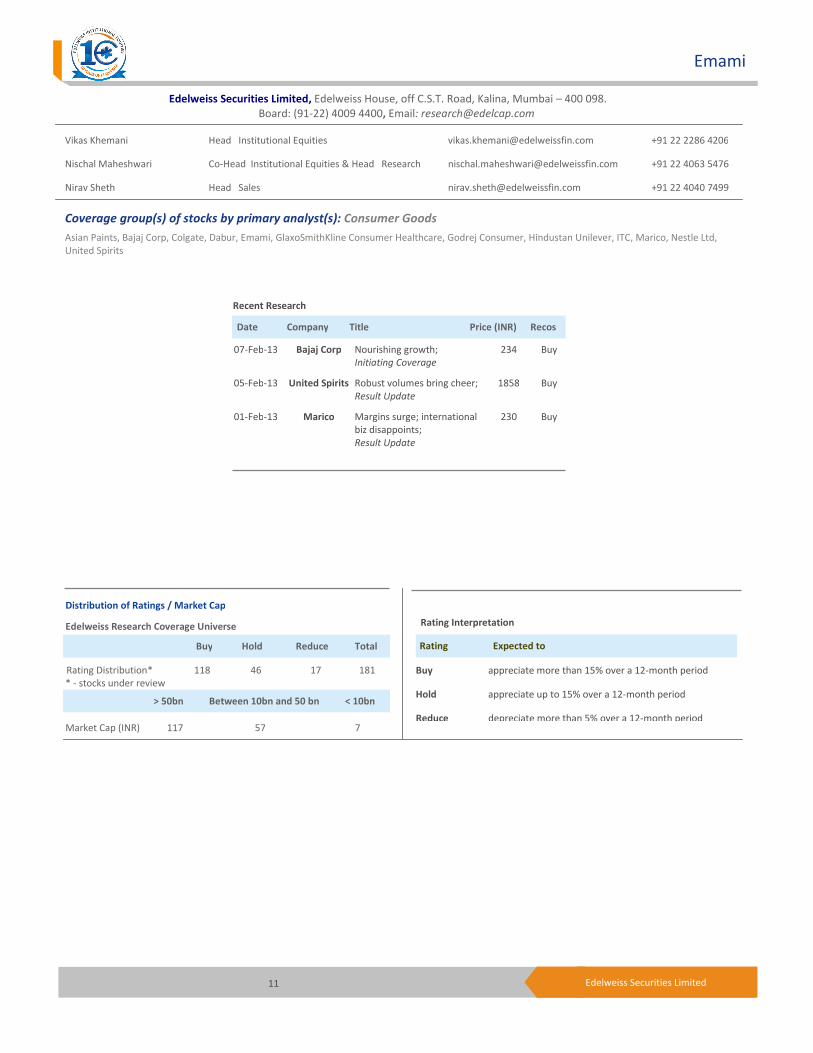

Edelweiss Securities Limited, Edelweiss House, off C.S.T. Road, Kalina, Mumbai – 400 098.

Board: (91-22) 4009 4400, Email: [email protected]

Vikas Khemani Head Institutional Equities [email protected] +91 22 2286 4206

Nischal Maheshwari Co-Head Institutional Equities & Head Research [email protected] +91 22 4063 5476

Nirav Sheth Head Sales [email protected] +91 22 4040 7499

Coverage group(s) of stocks by primary analyst(s): Consumer Goods

Asian Paints, Bajaj Corp, Colgate, Dabur, Emami, GlaxoSmithKline Consumer Healthcare, Godrej Consumer, Hindustan Unilever, ITC, Marico, Nestle Ltd,

United Spirits

Distribution of Ratings / Market Cap

Edelweiss Research Coverage Universe

Rating Distribution* 118 46 17 181

* - stocks under review

Market Cap (INR) 117 57 7

Date Company Title Price (INR) Recos

Recent Research

07-Feb-13 Bajaj Corp Nourishing growth;

Initiating Coverage

234 Buy

05-Feb-13 United Spirits Robust volumes bring cheer;

Result Update

1858 Buy

01-Feb-13 Marico Margins surge; international

biz disappoints;

Result Update

230 Buy

> 50bn Between 10bn and 50 bn < 10bn

Buy Hold Reduce Total

Rating Interpretation

Buy appreciate more than 15% over a 12-month period

Hold appreciate up to 15% over a 12-month period

Reduce depreciate more than 5% over a 12-month period

Rating Expected to

12 Edelweiss Securities Limited

Consumer Goods

Access the entire repository of Edelweiss Research on www.edelresearch.com

DISCLAIMER

General Disclaimer:

This document has been prepared by Edelweiss Securities Limited (Edelweiss). Edelweiss, its holding company and associate companies are a full service, integrated investment banking, portfolio

management and brokerage group. Our research analysts and sales persons provide important input into our investment banking activities. This document does not constitute an offer or solicitation for the

purchase or sale of any financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data or other sources believed to be reliable, but we

do not represent that it is accurate or complete and it should not be relied on as such. Edelweiss or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may

arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis

for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an

independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits

and risks of such investment. The investment discussed or views expressed may not be suitable for all investors. We and our affiliates, group companies, officers, directors, and employees may: (a) from time

to time, have long or short positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or

other compensation or act as advisor or lender/borrower to such company (ies) or have other potential conflict of interest with respect to any recommendation and related information and opinions. This

information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any

other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in

any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Edelweiss and affiliates/ group companies

to any registration or licensing requirements within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document

comes, should inform themselves about and observe, any such restrictions. The information given in this document is as of the date of this report and there can be no assurance that future results or events

will be consistent with this information. This information is subject to change without any prior notice. Edelweiss reserves the right to make modifications and alterations to this statement as may be

required from time to time. However, Edelweiss is under no obligation to update or keep the information current. Nevertheless, Edelweiss is committed to providing independent and transparent

recommendation to its client and would be happy to provide any information in response to specific client queries. Neither Edelweiss nor any of its affiliates, group companies, directors, employees, agents

or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.

Past performance is not necessarily a guide to future performance. The disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should not be

treated as endorsement of the views expressed in the report. Edelweiss Securities Limited generally prohibits its analysts, persons reporting to analysts and their dependents from maintaining a financial

interest in the securities or derivatives of any companies that the analysts cover. The information provided in these reports remains, unless otherwise stated, the copyright of Edelweiss. All layout, design,

original artwork, concepts and other Intellectual Properties, remains the property and copyright Edelweiss and may not be used in any form or for any purpose whatsoever by any party without the express

written permission of the copyright holders.

Analyst Certification:

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of

his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

Analyst holding in the stock: No.

Additional Disclaimer for U.S. Persons

This research report is a product of Edelweiss Securities Limited, which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report

is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and

is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject

company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Edelweiss Securities Limited only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act)

and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it

should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional

Investor.

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors,

Edelweiss Securities Limited has entered into an agreement with a U.S. registered broker-dealer, Enclave Capital, LLC ("Enclave").

Transactions in securities discussed in this research report should be effected through Enclave or another U.S. registered broker dealer.

Additional Disclaimer for U.K. Persons

The contents of this research report have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA").

In the United Kingdom, this research report is being distributed only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(5) of

the FSMA (Financial Promotion) Order 2005 (the “Order”); (b) persons falling within Article 49(2)(a) to (d) of the Order (including high net worth companies and unincorporated associations); and (c) any

other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”).

This research report must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this research report relates is available only to relevant

persons and will be engaged in only with relevant persons. Any person who is not a relevant person should not act or rely on this research report nor any of its contents. This research report must not be

distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person.

Edelweiss shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the

system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the Edelweiss to present the data. In no event shall the Edelweiss be liable

for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the Edelweiss through this

report.

Copyright 2009 Edelweiss Research (Edelweiss Securities Ltd). All rights reserved