september 2009 hsbc gif bric equity · hsbc gif bric equity . september 2009. for investment...

TRANSCRIPT

HSBC GIF BRIC Equity September 2009

For investment professionals only

Brazil

3

Source: Consensus by Brazilian Central Bank, HSBC Forecasts.

CPI Forecast 12M ahead(Grey lines = center and band of the target)

0

1

2

3

4

5

6

7

8

9

10

11

12

2003 2004 2005 2006 2007 2008 2009 2010

Macroeconomic framework: Successful inflation control…

•

Inflation target since Jun/99

•

Operational independence of CB

•

Full transparency

•

Proven track record

4

Household credit composition

Source: Brazilian Central Bank.

4

6

8

10

12

14

16

18

2001 2003 2005 2007 2009

Corporate Individuals

Credit volume(% of GDP)

… supported by credit expansion...

31,7%

28,1%

1,3%38,9%

Payroll Vehicles Mortgage Personal

31.7%

28.1%

1.3%38.9%

5

48%

50%

52%

54%

56%

58%

60%

62%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Source: MDIC, Funcex, Brazilian Central Bank, HSBC.

Ranking* Products

1st

Quartz and Niobium

2nd

Iron Ore and Bauxite

3rd

Manganese

5th

Tin Ore

Source: US Department of the Interior and US Geological Survey

*Production

Ranking* Products

1st

Ethanol

1st

Sugar

1st

Beef

1st

Coffee

2nd

Soybeans

2nd

Corn

2nd

Poultry

3rd

Pork

Source: USDA

*Production

Commodities exports(Exports directly or indirectly related to commodities)

Brazil is a key global commodities supplier…

6

Urban population% of total

Source: UN.

0

10

20

30

40

50

60

70

80

90

100

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Brazil More developed countries Less developed countries

From the domestic point of view, Brazil has an attractive consumer market…

E E

7

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Investment rate(Investments over GDP; Constant prices)

“PAC” project(In billion USD)

0

50

100

150

200

250

300

Energy Social /Urban

Logistics Total

Source: IBGE; Federal Government. “PAC” refers to Growth Acceleration Program.

“PAC”

project is a proxy for the size of potential investments…

E

8

What typeInvestments costs(Estimative in USD billion)

Source: “Valor Especial” Magazine based on Federal and Regional Governments.

World Cup offers an opportunity for speeding up these investments

Stadiums

Airports

Metro

Light Rail Vehicle construction

Port improvement

Highway expansion

Hotel construction

Bridges

Urban mobility works

Downtown revitalization

Training and Marketing in tourism

Drainage works and sanitation

Manaus 0.8Fortaleza 5.1Natal 1.9Recife 2.7Salvador 2.7Cuiabá 1.6Brasília 1.9São Paulo 18.1Rio de Janeiro 5.9Belo Horizonte 0.8Curitiba 2.4Porto Alegre 2.7

Total 46.6

9

67%

47%

5%

21%24%

53%

21%

14%

37%39%

26% 22%

0

20

40

60

80

100

120

Net

herla

nds

UK

US

Irela

nd

Spa

in

S A

frica

Chi

le

Hun

gary

Mex

ico

Cze

ch R

epub

lic

Pol

and

Bra

zil

Mortgage / GDP (%) Mortgage / Total Loan

4,5

5,0

5,5

6,0

6,5

7,0

7,5

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Housing credit(as % of GDP by country)

Brazil housing deficit

Source: BNDES/SAE, IBGE.

Some measures could have a huge impact on the housing market

7.5

7.0

6.5

6.0

5.5

5.0

4.5

Million

10

Source: OECD, Abrapp, Previ, Watson Wyatt, HSBC Global Asset Management.

Pension funds equities allocation as % of total assets

-

10

20

30

40

50

60

70

Hong K

ong

Austra

liaIre

land

Finlan

d

United

King

dom

United

Stat

es

Peru

Nether

lands

Icelan

dSwitz

erlan

dCan

ada

Fran

ceColo

mbiaPola

ndPor

tugal

Brazil

Chile

Denmar

kMex

ico

Average = 34%

Brazilian equity allocation is still low compared with other countries…

11

Source: IBES, MSCI.

Selected emerging markets forward P/E

02

46

810

1214

1618

20

Russia

Turk

eyHun

gary

Brazil

Ex -

Pet

ro &

Vale

Czech

Rep

ublic

Thail

and

South

Afri

ca

Brazil

South

Kor

ea

China

Indon

esia

Mexico

Poland

Philip

pines

Malays

ia

India

Chile

Taiw

an

Expected EPS Growth 2010/2008 2010/2009MSCI Brazil 11,9% 27,0%MSCI EM 10,6% 24,3%

… but it is still relatively attractive in terms of valuation and

earnings growth

11.9%

10.6%

27.0%

24.3%

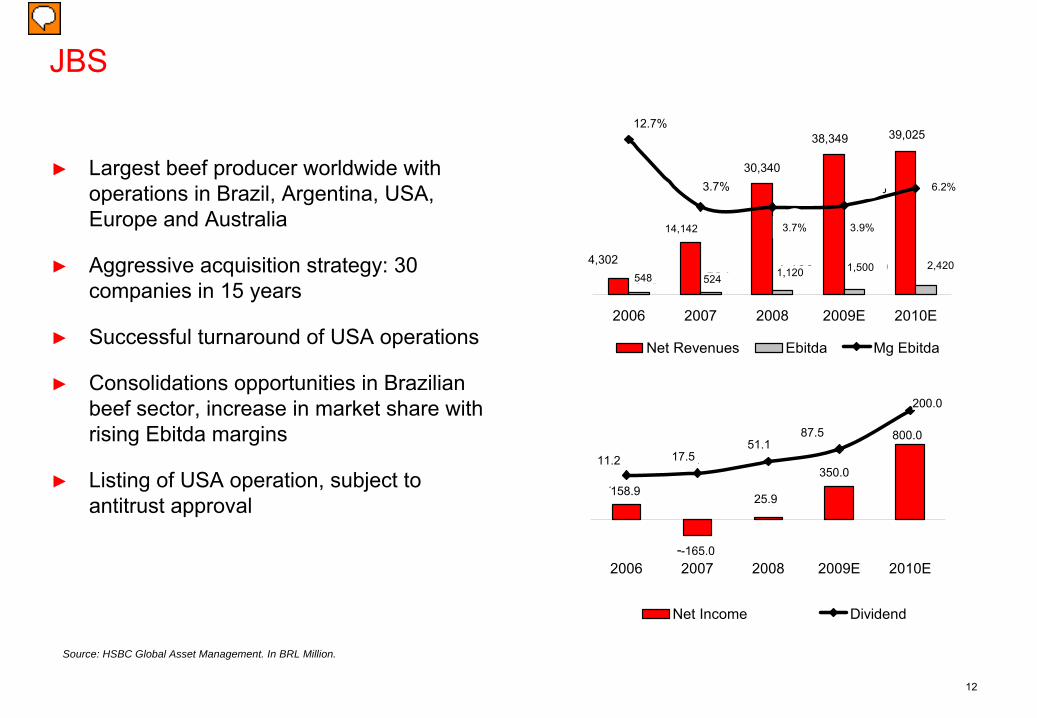

12

3.7%

JBS

►

Largest beef producer worldwide with operations in Brazil, Argentina, USA, Europe and Australia

►

Aggressive acquisition strategy: 30 companies in 15 years

►

Successful turnaround of USA operations

►

Consolidations opportunities in Brazilian beef sector, increase in market share with rising Ebitda margins

►

Listing of USA operation, subject to antitrust approval

158,9

-165,0

25,9

350,0

800,0

11,2 17,551,1

87,5

200,0

2006 2007 2008 2009E 2010E

Net Income Dividend

4.302

39.02538.349

30.340

14.142

2.4201.5001.120524548

6,2%3,9%

3,7%

3,7%

12,7%

2006 2007 2008 2009E 2010E

Net Revenues Ebitda Mg Ebitda

Source: HSBC Global Asset Management. In BRL Million.

12.7%

3.7%30,340

38,349 39,025

4,302

3.7% 3.9%

6.2%

2,4201,5001,120524

14,142

548

11.2 17.551.1

87.5

200.0

158.9

-165.0

25.9

350.0

800.0

13

Russia

14

Summary

►

Russian equities have de-rated relative to own history and peers

►

While YTD one of best performing markets in the world, on a 12-month scale still the worst, thus valuations are cheap

►

Economic indicators remain negative, although signs of turnaround are appearing, driven by stronger commodity prices. A return of consumer confidence and investment would enhance recovery

►

Long-term investment case remains solid: Macroeconomic base remains healthy

Stronger for longer commodity prices will drive growth

Secular growth case remains in place

Infrastructure spend increasing

►

Corporate earnings is expected to recover in 2010

►

More than just an oil play

15

Valuations: relative to peers

12-month forward P/E versus 2009-11E earnings CAGR for Russia and Global Markets

Russia’s P/E discount to GEM

Source: Goldman Sachs Research estimates. Data as at September 2009. Source: IBES, Troika Dialog estimates. Data as at August 2009.

%

India

US ChinaEurope

Brazil

Russia

20.0x

15.0x

10.0x

5.0x

0 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

12M FW P/E

2009-2011E Earnings CAGR

125

100%

75%

50%

25%

0%’09 ’00 ’02 ’04 ’06 ’08

Trailing P/BV Forward P/E Forward EV/EBITDA

12M

FW

P/E

16

Market drivers -

oil price, currency, global risk appetite

►

S&P 500 –

correlation reached 70% in spring this year, and remains high.

►

Oil prices –

correlation increased as oil price dipped below “threshold”

level of taxation. Remains high, but likely to fall provided oil price remains strong.

►

Strong inverse correlation between RTS and Ruble, Russian Bond Eurobonds yields and spreads

►

Two peaks in correlation –

in 3Q08 as devaluation weighed on market, then in 2Q09 as stronger Ruble contributed to equity market recovery

►

Negative correlation increased in Autumn ’08 as reassessment of Russia Risk translated to sell off in Russian equities

►

Correlation now strong and close to peak as yields and spreads have now declined

►

Stock return drivers likely to become more nuanced as the recovery progresses

Correlation of the RTS Index vs S&P500, oil price and Rb/basket rate

Correlation of the RTS Index vs Russia Eurobonds yields and Russia’s Eurobond spreads

Source: Bloomberg, Deutsche Bank. Data as at August 2009.

80%

70%

60%

50%

40%

30%

20%

10%

0%

10%

30%

2005 2006 2007 2008 2009 2010

Correlation of RTS vs

Russia’s spread

Correlation of RTS vs

Urals oil price Correlation of RTS vs

S&P500Correlation of RTS vs

Rb/basket

Correlation of RTS vs

Russia’s yield

10%

-10%

-30%

-50%

-70%

-90%

2005 2006 2007 2008 2009 2010

-80%S&P500

Oil prices

Roub le(inverted, RHS)

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

17

Domestic growth: signs of the bottom

►

Economic indicators are declining at double-digit rates

►

Data are showing signs of a bottom

►

Retail sales showing most resilience, declining only 4.0% YoY

Russia’s key economic indicators

Source: Rosstat, Deutsche bank research estimates. Data as at August 2009.

Retail sales, YoY, real, % Construction, YoY, real, %

40%

30%

20%

10%

0%

-10%

-20%

-30%Jan-06 Jul-06

IP, YoY, real, % Fixed investment, YoY, real, %Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

18

Aggressive fiscal stimulus underway

Ministry of Finance announced anti-crisis measures

Source: Ministry of Finance. Data as at May 2009.

MeasuresUSD bn % of GDP

Tax measuresReduction of corporate profit tax from 24% to 20% 12.0-15.0 1.0%-1.3%Reduction of the amortization premium from 30% to 10% 4.5 0.4%Change in the calculation mechanism of the oil export duty 7.5 0.6%Other (increase in housing benefits, reduction of taxes for small business, etc) 3.0 0.3%TOTAL tax measures 26.9-29.9 2.3%-2.6%Budget expenditure measuresInjections of funds into the equity of Russian corporates, of which: 13.1 1.1%

RosSelkhozBank (support for agriculture) 2.2 0.2%State Mortgage Agency (restructuring of mortgages) 1.8 0.2%

RosAgroLeasing (support for the agroindustrial complex) 0.9 0.1%VEB (support for the corporates) 2.2 0.2%

Deposit Insurance Agency (support for deposit holders) 6.0 0.5%Subordinated loans: 13.4 1.1%

VTB 6.0 0.5%RosSelkhozBank 0.7 0.1%

others 6.7 0.6%Subsidization of interest rates for the agroindustrial

complex 0.5 0.0%Support for airliners 1.0 0.1%Support for autoproducers 1.2 0.1%Support for exporters 0.2 0.0%Support for SME 0.2 0.0%Support for military-industrial complex 1.5 0.1%Support package for the labour

market (unemployment benefits, etc) 2.6 0.2%Other 0.6 0.1%TOTAL budget expenditure measures 34.3 2.9%GRAND TOTAL 61.2-64.2 5.2%-5.5%Source: Ministry of Finance

Total amount

19

Budget balance sensitivity to the oil price Current account balance sensitivity to oil price

M2 Growth sensitivity to oil price

Source: Ministry of Finance., Renaissance Capital Estimates. Data as at April 2009.

Domestic growth drivers: oil price sensitivity

Budget Balance 2009, % GDP

GDP growth, %

Current account deficit, % GDP

M2 growth, %

GDP growth sensitivity to oil price

US

$30

US

$40

US

$50

US

$60

US

$70

US

$80

US

$90

US

$100

6.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

10.0

8.0

6.0

4.0

2.0

0.0

-2.0

-4.0

-6.0

-8.0

-10.0

US

$30

US

$40

US

$50

US

$60

US

$70

US

$80

US

$90

US

$100

6.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

US

$30

US

$40

US

$50

US

$60

US

$70

US

$80

US

$90

US

$100

45.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

US

$30

US

$40

US

$50

US

$60

US

$70

US

$80

US

$90

US

$100

20

Russian domestic growth drivers –

rise of the consumer

►

Russian wages (in terms of US dollar) increased 7 fold between 1999 and 2008

►

Wage distribution has also materially shifted in a positive direction

►

This may sparked a retail boom, although by global standards remains in its infancy

►

Top five retailers account for only 5.5% of total market –

consolidation will accelerate top line and enhance already high margins

►

Food retailing CAGR 2006 –

2010E is 20%

►

Consumer spending has been more resilient than the broader economy during recent turmoil

Wage distribution by share of wage earners (RUB per month)

Source: Rosstat, Nomura estimates. Data as at January 2009

100%90%80%70%60%50%40%30%20%10%

0%

2002

Above 12,000 8,000 to 12,000 4,500 to 8,000 2,500 to 4,000 Less than 2,500

2004 2006 2008

21

Long-term investment case remains

►

Macroeconomic backdrop is relatively healthy

►

Sovereign and household debt is low

►

Currency reserves remain substantial

►

Stronger for longer commodity prices will support growth

►

Secular growth story remains in place

►

Infrastructure spend

►

China effect

Debt/GDP levels 2008E

Source: IMF, Troika estimates. Data as at April 2009.

Current account deficit, 2009E

0%

30%

60%

90%

120%

150%

Government Household Corporate Financial

US Russia Eastern Europe

-21.5-13.3

-8.7-8.7-8.3

-6.1-5.7

-4.7-2.5

1.42.8

-25 -20 -15 -10 -5 0 5

BulgariaRomania

Estonia

LithuaniaLatvia

Hungary

PolandSlovak Republic

Czech Republic

Russia at $30/bbl oilRussia at $60/bbl oil

22

Source: IMF, AEB, Troika estimates and Euromonitor. Data as at April 2009.

Population, 2007, mn Beer sales volumes, 2007, bn I

Secular growth story: large internal market

►

Largest population in Europe and already the largest market for most consumer goods

Rus

sia

Ger

man

y

Turk

ey

Fran

ce UK

Italy

Ukr

aine

Spa

in

Pol

and

5

0

30

60

90

120

1 0

0

2

4

6

10

8

12

Rus

sia

Ger

man

y

Rom

ania

Fran

ceUK

Italy

Ukr

aine

Spa

in

Pol

and

0 1 2 3 4

Car sales in Europe, 2008E, mnGermany

RussiaItalyUK

FranceSpain

BelgiumNetherlands

AustriaGreece

23

Secular growth story: low penetration levels

►

Russia has much lower levels of penetration of key consumer goods and services than the rest of Europe

Mortgage loans / GDP, 2008E Internet penetration

Source: ECB, Central bank, ComScore. Data as at December 2008.

0% 10% 20% 30% 40% 50% 60%

Netherlands

Spain

Germany

France

Belgium

Italy

Russia

Netherlands

0% 20% 40% 60% 80% 100%

Spain

UK

Germany

France

Belgium

Italy

Russia

24

Secular growth: infrastructure spend

►

Investment/GDP ratio has been very low since early 1990s, in both absolute terms and relative to rest of world

►

Commodity investment in Far East

►

Sochi Winter Olympics

Index of Russian investment

Investment as a % of GDPInvestment / GDP, 2007

Source: CIA world factbook. Data as at January 2009 Source: IMF, State statistics service. Data as at January 2009.

Kaz

akhs

tan

Sou

th K

orea

Sou

th A

frica

50%

40%

30%

20%

10%

0%

50%

40%

30%

20%

10%

0%

Chi

na

Indi

a

Ukr

aine

Japa

n

Wor

ld

Pol

and

EU

Turk

ey

Rus

sia

US

2008

E20

09E

120%

100%

80%

60%

40%

20%

0%

120%

100%

80%

60%

40%

20%

0%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

40%

35%

30%

25%

20%

15%

10%

40%

35%

30%

25%

20%

15%

10%

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

E

Global Emerging markets Emerging Asia Russia

25

Year Investor Country Target company/ project

Industry Amount ($mn) Stake (%)

2004-2006 ConocoPhilips US Lukoil Oil and gas $7,500 20%

2005 Coca-cola US Multon Food $600mn 100%

2005 Sta

da Germany Nizhphaarm Pharma $108mn 97%

2006 Societe

Generale France Rosbank Banking $2,334 50%+1

2007 E.On Germany OGK-4 Utilities $5,740 61%

2007-10 13 automakers (Peugeot-Citroen, Suzuki, Hundai, Ford, Volkswagen, Toyota, volvo, etc)

New plants Automobile $1,800 in 2-3 years

YTD Shell, Mitsui, Mitsubishi Holland

/ Japan Sakhalin-2 Oil and gas $14,100 49%

0100

2 003 004 005006 00

19 98 2000 20 02 200 4 2 006 200 8 2 010

Y ea r

FD I inf lows

FD I sto ck

Foreign Direct Investment (FDI) Inflows and FDI stock ($bn)

FDI: High and rising –

an attractive market for multinationals

1998 2000 2002 2004 2006 2008 2010

FDI inflowsFDI stock$b

n

0100200300400500600

Data as at May 2009

26

India

27

Incredible India –

seductive investment story

►

Strong GDP growth

►

Favourable

demographics

►

Improving macro economic trends

►

Poor infrastructure to improve –

social & physical >> investment spend

►

Renewed focus on rural India

28

Incredible India vs

China –

great growth potential

►

GDP growth to accelerate compared to past decade

►

India liberalisation

began in 1991 -

12 years after China brought reforms in 1979

Source: World Economic Outlook, IMF, Deutsche Bank. Data as at April 2009

Nominal GDP (US$ bn)

0100020003000400050006000700080009000

Yea

r 1Y

ear 2

Yea

r 3Y

ear 4

Yea

r 5Y

ear 6

Yea

r 7Y

ear 8

Yea

r 9Y

ear 1

0Y

ear 1

1Y

ear 1

2Y

ear 1

3Y

ear 1

4Y

ear 1

5Y

ear 1

6Y

ear 1

7Y

ear 1

8Y

ear 1

9Y

ear 2

0Y

ear 2

1Y

ear 2

2Y

ear 2

3Y

ear 2

4Y

ear 2

5Y

ear 2

6Y

ear 2

7Y

ear 2

8Y

ear 2

9Y

ear 3

0Y

ear 3

1Y

ear 3

2Y

ear 3

3Y

ear 3

4Y

ear 3

5

China (1980 onwards) India (1991 onwards)

China's 2009 GDP

India's 2009 GDP

29

Great growth potential >> GDP per capita on a ppp

basis

►

India > China in 1991

►

China > 2 x India in 2009

India China

China inflection point

India inflection point?

872

910

956

1,00

7

1,06

9

1,14

7

1,23

3

1,28

6

1,35

2

1,44

2

1,50

9

1,57

6

1,65

1

1,77

4

1,95

0

2,15

7

2,40

6

2,65

9

2,88

6

3,12

9

3,39

6 3,69

4 4,01

0

796

888 1,02

5

1,18

2

1,35

0

1,51

2

1,67

7

1,84

5

1,99

3

2,15

8

2,37

2

2,61

2

2,88

1 3,21

7 3,61

4 4,06

4

4,65

8

5,37

8 5,96

3 6,37

9 6,78

6

7,41

3

8,20

2

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E

2012

E

(US$)

Source: IMF, Deutsche Bank. Data as at April 2009

30

China’s present GDP, India’s future GDP?

►

At 8% GDP growth, India is expected to take about 9 years to get

to where China is today

Source: India Infoline. Data as at 26 August 2009.

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

2008

2009

2010

E

2011

E

2012

E

2013

E

2014

E

2015

E

2016

E

2017

E

2018

E

2019

E

2020

E

2021

E

US$bn

China Real GDPIndia's Real GDP @ 6%7%8%9%

31

So, where are we in the cycle?

►

Services which is at > 50% of GDP still growing at > 9%

►

Slowing exports hurt industry and services; agriculture to hurt going forward

►

But resilient rural economy

►

Very aggressive monetary easing, 3 fiscal stimulus packages, falling price points and pent up demand growth to recover

►

US$100bn stimulus = 10% of GDP 10.0 Real GDP %y/y

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Jun-

08

Sep-

08

Dec-0

8

Mar-0

9

Jun-

09

Sep-

09E

Dec-0

9E

Mar-1

0E

Jun-

10E

Sep-

10E

Dec-1

0E

Mar-1

1E

Recovery in growth

%y/y

-15

-10

-5

0

5

10

15

20

25

Mar-9

8

Mar-9

9

Mar-0

0

Mar-0

1

Mar-0

2

Mar-0

3

Mar-0

4

Mar-0

5

Mar-0

6

Mar-0

7

Mar-0

8

Mar-0

9

Mar-1

0E

Mar-1

1E

Services Industry (from Mar-09 changed to incl. constr.)Real GDP Agriculture, Forestry and Fishing

Source: UBS. Halbis As at 16 September 2009. Quarters are calendar year wiseSource: UBS. As at 31st August 2009.

32

Favourable

Demographics >> positive for consumer stories

Source: UBS. Data as at 16 September 2009.

13.7

17.5

20.4

20.5

22.0

26.4

27.4

31.7

10 15 20 25 30 35

Germany

UK

US

China

Thailand

Brazil

Indonesia

India

Percentage of the population below the age of 15

33

-

5

10

15

20

25

30

CY97 CY98 CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06 CY07 CY08

India ChinaCar/1000

Penetration –

2 wheelers and cars

►

Higher 2 wheeler penetration in India!

►

Higher car penetration too till CY1999

►

Potential for higher car penetration in India given Chinese experience

-

10

20

30

40

50

60

70

80

CY97 CY98 CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06 CY07 CY08

India China2Ws/1000

Source: Bloomberg, CEIC database. Data as at 15 September 2009.

34

Domestic car sales volumes

India: Domestic car sales volumes

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CY04 CY05 CY06 CY07 CY08 CY09

Festival season boosts in Sep-Oct

Sales spike up in March

Dip in Dec due to model-year change

Source: SIAM. Data as at 15 September 2009.

Unit

35

Maruti

Suzuki (Auto company) –

stock positioning

Source: Factset ( Provisional). Data as at 31 Aug 2009. Example included for illustration purposes. Does not constitute investment advice

Overweight

Underweight

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0Ja

n-04

Mar

-04

May

-04

Jul-0

4

Sep-

04

Nov

-04

Jan-

05

Mar

-05

May

-05

Jul-0

5

Sep-

05

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Maruti

Suzuki India Ltd.

36

Maruti relative to Nifty

100.00

150.00

200.00

250.00

300.00

18-Ju

l-03

18-Ju

l-04

18-Ju

l-05

18-Ju

l-06

18-Ju

l-07

18-Ju

l-08

18-Ju

l-09

Maruti

Suzuki –

relative to market

►

Over 50% market share in Indian market

►

Cash rich –

its key competitor have cash flow/debt issues

►

Most extensive distribution network

►

Exporting small cars to Europe for Nissan and Suzuki

►

Record exports to Europe

Source: Bloomberg. Data as at 31 August 2009. The figures used are for illustrative purposes only, actual asset allocation may differ. Individual stock performance does not represent fund performance.

37

Improving Macro Trends –

Foreign Direct Investment (FDI)

►

India attracting relatively more FDI

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

India China

FDI % of GDP

Source : India Infoline. Data as at 14 September 2009.

38

-4.0

0.0

4.0

8.0

12.0

1QC

Y00

2QC

Y00

3QC

Y00

4QC

Y00

1QC

Y01

2QC

Y01

3QC

Y01

4QC

Y01

1QC

Y02

2QC

Y02

3QC

Y02

4QC

Y02

1QC

Y03

2QC

Y03

3QC

Y03

4QC

Y03

1QC

Y04

2QC

Y04

3QC

Y04

4QC

Y04

1QC

Y05

2QC

Y05

3QC

Y05

4QC

Y05

1QC

Y06

2QC

Y06

3QC

Y06

4QC

Y06

1QC

Y07

2QC

Y07

3QC

Y07

4QC

Y07

1QC

Y08

2QC

Y08

3QC

Y08

4QC

Y08

1QC

Y09

2QC

Y09

3QC

Y09

QTD

Net FII Investments (US$B)

Net foreign direct & portfolio investments >>> inflection point in strategic buys

Source : RBI, Motilal Oswal. FDI data for 3QCY09 QTD is as at July 2009 and FII data for 3QCY09 QTD is as at 14 September 2009.

Big contrast

0.0

3.0

6.0

9.0

12.0

1QC

Y00

2QC

Y00

3QC

Y00

4QC

Y00

1QC

Y01

2QC

Y01

3QC

Y01

4QC

Y01

1QC

Y02

2QC

Y02

3QC

Y02

4QC

Y02

1QC

Y03

2QC

Y03

3QC

Y03

4QC

Y03

1QC

Y04

2QC

Y04

3QC

Y04

4QC

Y04

1QC

Y05

2QC

Y05

3QC

Y05

4QC

Y05

1QC

Y06

2QC

Y06

3QC

Y06

4QC

Y06

1QC

Y07

2QC

Y07

3QC

Y07

4QC

Y07

1QC

Y08

2QC

Y08

3QC

Y08

4QC

Y08

1QC

Y09

2QC

Y09

3QC

Y09

QTD

Net FDI (US$B)

39

Valuations >> Rapid reaction from lows

Source: FactSet, MSCI, Morgan Stanley. Data as at 15 September 2009.

9

12

15

18

21

24

27

30

33

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

MSCI India Trailing PE

5 Yr Avg

10 Yr Avg

MSCI India Trailing PE, 1995-2008

40

Portfolio strategy

►

Focus on domestic cyclicals

–

consumer discretionary, real estate, infrastructure –

and defensives –

consumer staples, healthcare

Sectors in Favour Key RationaleConsumer –

Discretionary & Staples

Declining demand recently but huge potential favourable demographics attractive interest rates and easing credit availability recovery in domestic consumption; Government focus on rural India

Real Estate Shortage of housing fast falling property prices affordability at record lows recovery in demand improvement in cash flows for real estate sector

Infrastructure

Healthcare

Poor infrastructure to improve Government stimulus packages lower commodity prices strong order books provide visibility

Undemanding valuations attractive growth profile defensive

41

China

42

Strong economic growth continues into 2009

►

GDP growth at 7.1% (1H09 --

1Q09: 6.1%, 2Q09: 7.9%)

►

Retail sales rose 15.1% y-o-y

(Jan –

Aug 09)

►

Fixed asset investment growth up 33.0% (Jan –

Aug 09) vs

26.1% in 2008

►

Export still down 22.2% y-o-y

(Jan –

Aug 09) vs. 17.2% growth in 2008

►

CPI inflation remained negative at -1.2% (Aug 09)

►

High foreign exchange reserve: US$2.18 trillion (Jun 09)

Source: Morgan Stanley.

43

Major impacts of global financial crisis on China

►

Sharp export decline forced weaker players out of business and new orders going to larger manufacturers which should improve China's production efficiency

and bargaining power over the longer run

►

China has become more focused on growing its domestic economy to

reduce reliance on export for the country’s long term economic growth

►

The crisis has opened a huge window of opportunity for Chinese companies to gain market share globally as many large foreign players face financial difficulties

►

With strong cash positions, Chinese companies have been able to buy quality assets around the world at distressed valuations during this credit crisis

44

Population becoming more affluent higher spending power

►

Strong GDP/capita growth

351 412 517 467601 699 771 817 861 946 1,038 1,132

1,2701,486

1,701

1,998

2,458

3,258

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

China's GDP / Capita (USD)CAGR (1991 -

2008) = 14.0%

32.5%

Source: CEIC, ABN Amro. Source: SIAM. Data as at 15 September 2009.

45

China income growth trend vs. other Asian economies

►

After reaching US$1,000 in GDP/capita, other Asian economies had

experienced an acceleration. China may follow the same trend

Source: Morgan Stanley. Data as at December 2008

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

GDP / Capita (USD)

19661971 2001

1977

JapanHong Kong

ChinaKorea

46

China has abundant cash deposits

Individual Bank Deposits (Rmb trn) Government Foreign Exchange Reserve (US$bn)

Source: JP Morgan. Data as at June 2009

7.48.7

10.412.0

14.1

16.217.3

21.8

24.9

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2001 2002 2003 2004 2005 2006 2007 2008 Jun-09

212.2286.4

403.3

609.9

818.9

1066.3

1528.2

1946.0

2131.6

0.0

500.0

1000.0

1500.0

2000.0

2500.0

2001 2002 2003 2004 2005 2006 2007 2008 Jun-09

47

All “China Shares”

are not created equal –

valuation comparison

2009 PBV (x)

2009 PE (x)

Mkt Cap (US$ bn)

No. of Listed Companies

'H' Shares 2.1 14.8 514.0 151

Red chips 2.1 14.1 456.9 91

Shanghai A 2.7 18.2 2,133.3 856

Shenzhen A 3.0 25.4 585.7 739

Shanghai B 1.5 14.8 9.3 54

Shenzhen B 1.5 15.3 10.5 55

Source: SSE; SZE; Wind Info; Bloomberg; BNP Paribas estimates. Data as at 31 August 2009

48

Valuation have rebounded but are still significantly below peak levels

MSCI China Index – Price/Book ratioMSCI China Index – Price/Earnings ratio

Source: Datastream, Goldman Sachs. Data from November 1994 to September 2009

0

20

40

60

80

100

120

140

160

94 95 96 98 99 00 01 02 03 04 05 06 08 09

Index Level

10X

20X

15X

25X

5X

0

50

100

150

200

250

300

94 95 96 98 99 00 01 02 03 04 05 06 08 09

Index Level

2.0X

4.0X

3.0X

5.0X

1.0X

49

Improving earnings growth outlook for Chinese companies

Source: Datastream. Data as at 15 September 2009

MSCI China 2009 earnings growth (Consensus)

-10%

-5%

0%

5%

10%

15%

20%

25%

Jan-08 Apr-08 Jul-08 Oct-08 Dec-08 Mar-09 Jun-09 Sep-09

50

Portfolio strategy

►

Sector focus

Sectors Key rationaleConsumer Discretionary Strong retail sales growth and domestic consumption driven by rising

income and favorable government policies

Commodities Strong fixed asset investment growth expected to generate rising

demand for selected commodities

Export Plays Export decline stabilised

with potential for demand pickup as global economic outlook improves

51

Investment conclusion

►

China has the policy tools and financial capacity to maintain strong domestic economic growth as demonstrated by strong GDP rebound

►

Beijing’s policies are effective in reviving domestic economic activities as seen in auto and property sales recovery

►

Domestic consumption and investment are expected to continue to drive China’s economic growth, export recovery a potential positive surprise

►

Potential upward corporate earnings revision in 2H09 may trigger

further market advance

►

The current financial crisis offers China a unique opportunity to gain global market shares and international political status

►

Renminbi will likely resume its appreciation as the global credit crisis subsides

►

China offers excellent value for long term investors despite potential short term market volatility

52

HSBC GIF BRIC Equity

53

Important information

►

The Fund invests primarily in Brazilian, Russian, Indian and Chinese equities.

►

The Fund is subject to the risks of investing in emerging markets.

►

The Fund’s investments may involve substantial market, currency, volatility, regulatory and political risks. Investors may suffer substantial loss of their investments in the Fund.

►

The investment decision is yours but you should not invest unless the intermediary which sells you the Fund has advised you that the Fund is suitable for

you and has explained why, including how investing in the Fund would be consistent with your investment objectives.

►

Investors should not invest in the Fund solely based on the information provided in this document and should read the offering document of the Fund for details.

54

How do the investment views translate into fund strategy?

►

Today we have a positive outlook for all four markets, hence the

near equal weightings in each market

►

Current preference for Brazil and Russia based on cheaper valuations, and strong commodity demand from India and China

Brazil Russia India China Cash

Current Target Portfolio Weight 26% 26% 24% 23% 1%

Portfolio Weight (Dec 08) 23% 22% 23% 30% 2%

Country PER 2009E PER 2010E EPS Growth 2010

Brazil 13.3x 10.9x 19.5%

Russia 13.1x 8.3x 57.4%

India 17.5x 14.6x 20.3%

China 17.9x 14.5x 23.0%

Asset allocation between the individual BRIC markets remains flexible, depending on market outlook and investment conditions

Source: Thomson Financial, UBS. Data as at 14 September 2009. Past performance should not be seen as an indication of future returns. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way.

55

The beauty of HSBC Global Investment Funds -

BRIC Freestyle

►

High conviction

Flexible asset allocation: e.g. single country allocation in the past has moved between 15-34%

The Fund can take relatively high weightings on specific stocks

►

Non-benchmark

The Fund does not follow the weightings of any particular index.

For example, the MSCI BRIC Index as at end August 2009 had the following weights –Brazil: 32.2%, Russia: 12.8%, India: 15.8%, China: 39.3%

►

Luxury of tapping the finest single country BRIC investment experts

Among the one of largest portfolio managers in the world for Brazilian, Russian, Indian and Chinese equities

Source: HSBC Global Asset Management. Data as at 31 August 2009.

56

An experienced BRIC Freestyle Equity Team 6 leading investment professionals

Jose CuervoBased in LondonSenior Fund ManagerBrazil Equity

Douglas HelferBased in London

Senior Fund ManagerRussian Equity

Sanjiv DuggalBased in Singapore

Portfolio ManagerIndian Equity

Richard C. WongBased in Hong Kong

Portfolio ManagerChinese Equity

Nick TimberlakeNick TimberlakeBased in LondonBased in LondonBRIC Fund ManagerBRIC Fund ManagerHead of Global Emerging MarketsHead of Global Emerging Markets

Guillaume Guillaume RabaultRabaultBased in ParisBased in Paris

Global Head of GEMGlobal Head of GEMResearchResearch

57

Year-to-date performance is now top quartile

►

Following last year’s crash, emerging markets have bounced back strongly

►

The Fund has delivered excellent returns this year, achieving top quartile performance

►

Tactical country allocation has been a positive contributor to performance

1-Month 3-Month 6-Month YTD

HSBC GIF BRIC Freestyle 2.5% 11.6% 88.7% 72.9%

Morningstar’s mean -0.4% 5.8% 72.7% 58.7%

Fund ranking 1/7 1/7 1/7 1/7

Quartile ranking 1 1 1 1

Source: Morningstar, data as at 31 August 2009. Calendar year performance of the Fund – Since launch to 31 December 2005: 42.2%; 2006: 45.0%; 2007: 47.5%; 2008: -63.1%. Bid to Bid price with dividend reinvested in USD terms. Fund launch date: 1 April 2005 (Class M2C)

58

The potential of BRIC….

►

Key ingredients for BRIC success are abundant -

Growth, Liquidity, Balance sheet, Valuation

►

Structurally the centre of global economic activity is moving East

►

BRIC markets are becoming more closely linked and less reliant on outside drivers

►

There are always risks -

double dip, Inflation, policy miss steps, Bolt from the blue

►

One of the best times to invest in BRIC markets

59

Important information

This presentation is for professional clients only. The contents

of this presentation are confidential and may not be reproduced

or further distributed to any person or entity, whether in whole or in part, for any purpose. The material contained in this presentation is for information only and does not constitute investment advice or a recommendation to any reader of this material to buy or sell investments.

The HSBC Global Investment Fund (‘GIF’) range is a Luxembourg domiciled SICAV and is regulated by the CSSF. The funds mentioned in this document may not be registered for sale or available in all jurisdictions. For available funds please contact your local HSBC office.

HSBC Global Investment Funds range cannot be sold by anyone in any jurisdiction in which such offer or solicitation is not lawful or in which the person making such an offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make such offer or solicitation. All applications are made on the basis of the current HSBC Global Investment Funds Prospectus, simplified prospectus and most recent annual and semi-annual reports. These can be obtained on request and free of charge from HSBC Global Asset Management (UK) Limited or the local distributors. The value of investments may go down as well as up and you may not get back the full amount you invested. Where overseas investments are held the rate of exchange may cause the value of investments to go down as well as up. Markets in some countries can be described as ‘emerging markets’. Some of these may involve a higher risk than where an investment is within a more established market. Where a sub-fund invests predominately in one geographical area, any decline

in economic conditions may affect prices and the value of underlying investments.

The securities representing interests in the HSBC Global Investment Funds range have not been and will not be registered under the US Securities Act of 1933 and will not be offered for sale or sold in the United States of

America, its territories or possessions and all areas subject to its jurisdiction, or United States person, except in a transaction which does not violate the Securities Law of the United States of America.

This document is issued by HSBC Global Asset Management (UK) Limited, 8 Canada Square, Canary Wharf, London, E14 5HQ, UK. Authorised and regulated by the Financial Services Authority and registered as number 122335. ©

Copyright. HSBC Global Asset Management 2009. All Rights Reserved.

This product is marketed in a sub-distributing capacity on a principal –

to –

principal basis by the HSBC Global Asset Management MENA, a unit that is part of HSBC Bank Middle East Limited, PO Box 66, Dubai, UAE, which is incorporated and regulated by the Jersey Financial Services Commission. Services are subject to the Bank’s terms and conditions. HSBC Bank Middle East Limited is a member of the HSBC Group.

The information provided has not been prepared taking into account the particular investment objectives, financial situation and

needs of any particular investor. As a result, investors using this information should assess whether it is appropriate in the light of their own individual circumstances before acting on it. The information in this document is derived from sources believed to

be reliable, but which have not been independently verified. However, HSBC Bank Middle East Limited makes no guarantee of its accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor shall HSBC Bank Middle East Limited be liable for damages arising out of any person’s reliance upon this information. All charts and graphs are from

publicly available sources or proprietary data. The opinions in this document constitute the present judgment of the issuer, which is subject to change without notice.

This document is neither an offer to sell, purchase or subscribe

for any investment nor a solicitation of such an offer. This document is intended for the use of institutional and professional customers and is not intended for

the use of private customers. This document is intended to be distributed in its entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Any transaction will be subject to HSBC Bank’s Terms of Business.17387/ME/0909/MB

www.assetmanagement.hsbc.com/MENA