short-term energy and summer fuels outlook guy caruso administrator, energy information...

TRANSCRIPT

Short-Term Energy and Summer Fuels Outlook

Guy CarusoAdministrator,

Energy Information Administration

2006 Summer Transportation Fuels Outlook Conference

April 11, 2006Washington, DC

Several Key Factors Drive the Short-Term Fuels Forecast

1) Rising world oil consumption;

2) Low global surplus production capacity and tight crude oil supply relative to demand;

3) Supply concerns in international oil markets (such as in Nigeria, Iraq, and Iran);

4) The challenges of: Stricter sulfur standards under the Tier 2 Gasoline program; MTBE phase-out; A shift to ultra low sulfur diesel.

All these factors contribute to higher prices for petroleum products, particularly in the coming months.

World Oil Consumption Growth Slowed in 2005; Projected to Increase in 2006-2007

Source: EIA, Short-Term Energy Outlook, April 2006

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1991-1999Avg.

2000 2001 2002 2003 2004 2005 2006 2007

Million Barrels

per Day

US

Rest of World

China

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Ang

ola

Rus

sia

Bra

zil

Aze

rbai

jan

Can

ada

US

Kaz

akhs

tan

Suda

nC

hina

Aus

tral

iaM

alay

sia

Viet

nam

Ecua

dor

Gab

onO

man

Egyp

tTu

nisi

aC

olom

bia

Indi

aSy

ria

Oth

er N

orth

Sea

Mex

ico UK

Nor

way

Million barrelsper day(AnnualChange)

2005 2006 2007

Non-OPEC Supply Growth Projected to Reach 0.8 million bbl/d in 2006 and 1.5 million bbl/d in 2007

Hurricane recovery

Hurricane damage

OPEC 34

Non-OPEC 51.1

World Liquids Production 2006

Source: EIA, Short-Term Energy Outlook, April 2006

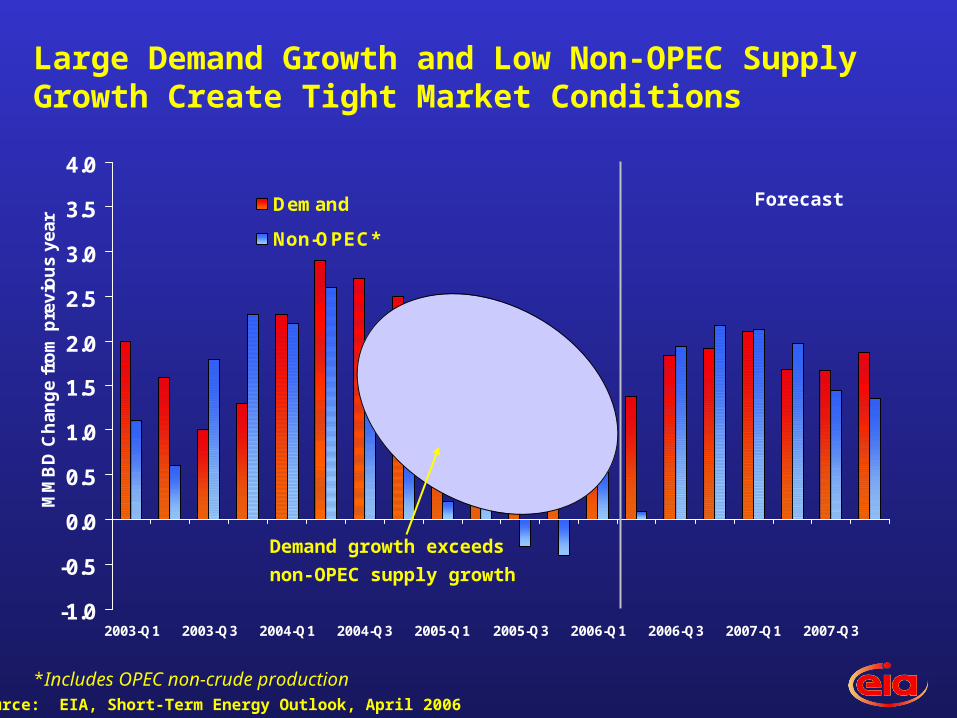

Large Demand Growth and Low Non-OPEC Supply Growth Create Tight Market Conditions

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2003-Q1 2003-Q3 2004-Q1 2004-Q3 2005-Q1 2005-Q3 2006-Q1 2006-Q3 2007-Q1 2007-Q3

MM

BD

Ch

ang

e fr

om

pre

vio

us

year

Demand

Non-OPEC*

*Includes OPEC non-crude production

Demand growth exceeds

non-OPEC supply growth

Source: EIA, Short-Term Energy Outlook, April 2006

Forecast

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1991-1997

Average

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Million Barrels

per Day

Forecast

2005 World Oil Spare Production Capacity Reached Lowest Level in 30 Years

Source: EIA, Short-Term Energy Outlook, April 2006

West Texas Intermediate Crude Oil Price Projected to Peak in mid-2006, then Gradually Decline.

0

10

20

30

40

50

60

70

80

90

100

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Dollarsper

barrel

Forecast

Source: EIA, Short-Term Energy Outlook, April 2006

1) High crude oil costs (up 13 percent from 2005 - summer to summer);

2) Increased gasoline demand growth (up 1.5 percent from 2005 – summer to summer);

3) Adequate stocks but refining capacity constraints;

4) Tighter constraints on sulfur content in gasoline and phase-out of MTBE;

Several Factors Are Driving 2006 U.S. Summer (April – September) Outlook for Motor Fuels

Source: EIA, Short-Term Energy Outlook, April 2006

Projected Increases in Personal Income and Miles Traveled Drive Up U.S. Gasoline Demand

-10%

-5%

0%

5%

10%

15%

20%

25%

2004-2005 2005-2006 2006-2007

Real Personal Income Real Fuel Cost per Mile

Vehicle Miles Traveled Motor Gas Demand

Forecast

PercentChange

Source: EIA, Short-Term Energy Outlook, April 2006

Motor Gas Demand

Motor Gasoline and Distillate Stocks Projected to Remain Within 5-year Min/Max Range

60

100

140

180

220

260

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

MillionBarrels

NOTE: Colored bands represent previous 5-year minimum/maximum ranges

ForecastTotal Motor Gasoline Inventory

Total Distillate Fuel Inventory

Source: EIA, Short-Term Energy Outlook, April 2006

Days of Supply of OECD* Commercial Oil Stocks Decline Gradually Through 2007

* Organization for Economic Cooperation and Development

46

48

50

52

54

56

58

60

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Daysof

Supply

Forecast

Source: EIA, Short-Term Energy Outlook, April 2006

U.S. Motor Gasoline Market Faces New Challenges This Year

1) Final stage of the phase-in of EPA’s Tier 2 gasoline program, which began in 2004:

Not expected to create significant problems for domestic refining and distribution;

May constrain foreign suppliers’ ability to respond to unexpected local supply disruptions or demand shocks.

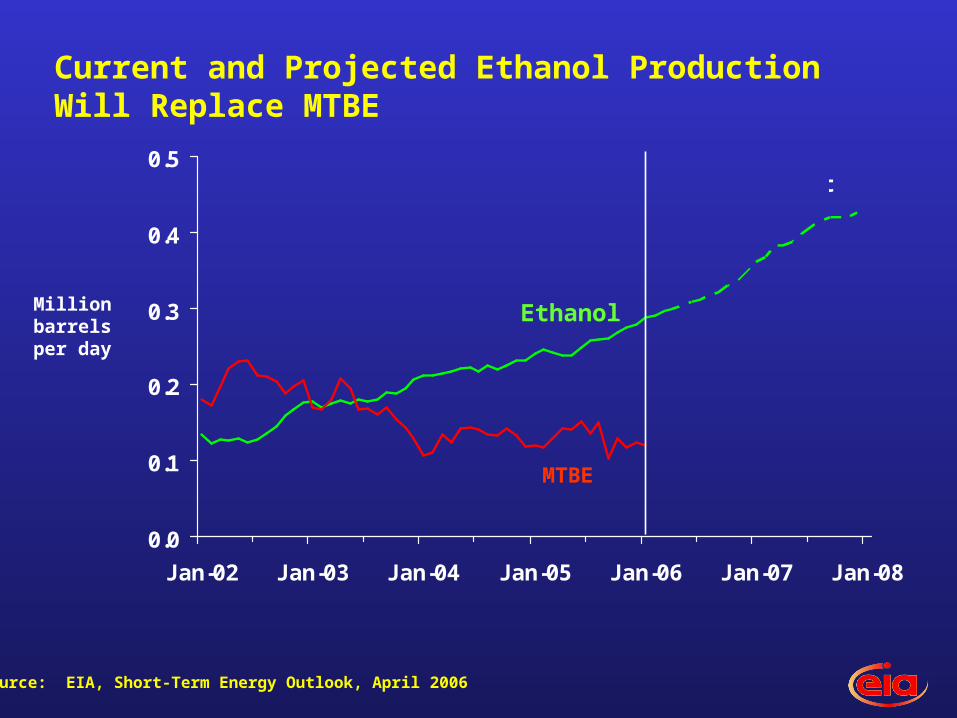

2) Phase-out of methyl tertiary butyl ether (MTBE) as a motor gasoline blendstock:

Projected to slightly increase average price of all gasoline due to lost production capability, fewer import sources, and tight ethanol markets;

Raises potential for localized price spikes arising from a complex transition in a tight market over a fairly short time period.

Source: EIA, Short-Term Energy Outlook, April 2006

0.0

0.1

0.2

0.3

0.4

0.5

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Forecast

Ethanol

MTBE

Current and Projected Ethanol Production Will Replace MTBE

Millionbarrelsper day

Source: EIA, Short-Term Energy Outlook, April 2006

0.00

0.25

0.50

0.75

1.00

1.25

1.50

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Finished Gasoline Total Gasoline

ForecastHurricanes Katrina and Rita

Million barrels per day

Gasoline and Blending Components Imports Projected to Average 9.9% of Summer Demand

Source: EIA, Short-Term Energy Outlook, April 2006

80%

85%

90%

95%

100%

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Hurricanes Katrina and Rita

Refinery Utilization Rates Projected to Average About 94%, up from 92% Last Summer

Forecast

Utilization Rate = Distillation inputs / atmospheric distillation operable capacity

Source: EIA, Short-Term Energy Outlook, April 2006

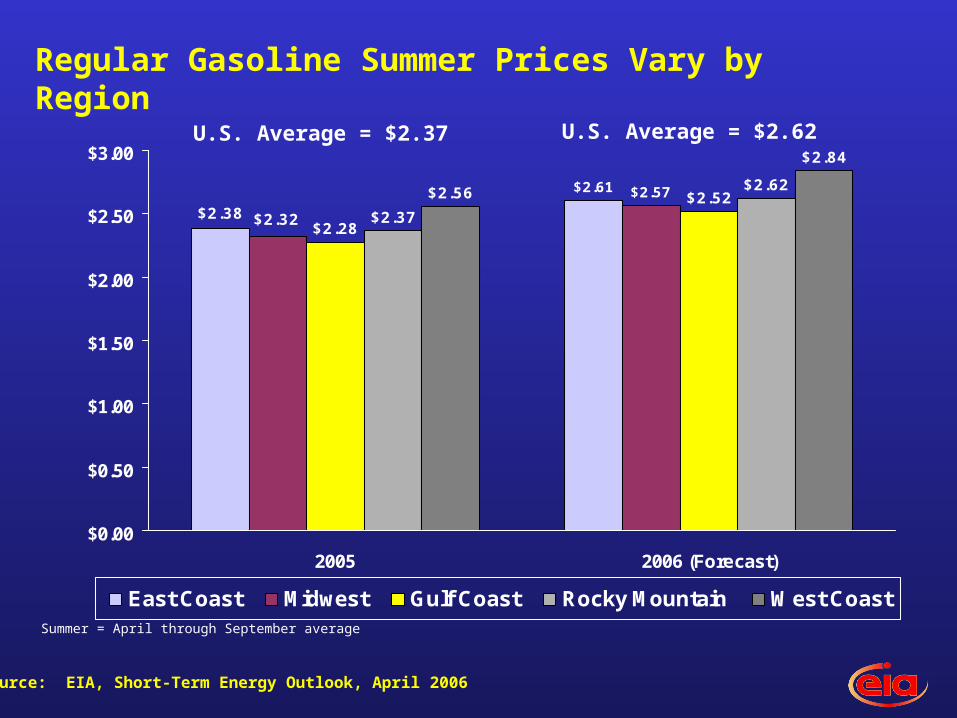

Summer Retail Gasoline Prices* Projected to Average $2.62 per Gallon, 25 cents More than Last Summer

* Regular gasoline, average all formulations.** Retail price minus crude oil cost minus taxes, per gallon

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06

Dollars per

Gallon

Tax Crude Margin** Base

2003Avg. $1.56

2004Avg. $1.90

2005Avg. $2.37

2006Avg. $2.62

Source: EIA, Short-Term Energy Outlook, April 2006

Regular Gasoline Summer Prices Vary by Region

U.S. Average = $2.37 U.S. Average = $2.62

Source: EIA, Short-Term Energy Outlook, April 2006

Summer = April through September average

$2.61 $2.57

$2.28

$2.52$2.37

$2.62$2.56

$2.84

$2.38 $2.32

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2005 2006 (Forecast)

East Coast Midwest Gulf Coast Rocky Mountain West Coast

Summer Retail Diesel Prices Projected to Average $2.62 per gallon, up 21 cents from Last Summer

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06

Cents per

Gallon

Tax Crude Margin** Base

2003Avg. $1.47

2004Avg. $1.77

2005Avg. $2.41

2006Avg. $2.62

Source: EIA, Short-Term Energy Outlook, April 2006

** Retail price minus crude oil cost minus taxes, per gallon

High world oil demand, sparked by robust economic growth, is continuing to keep crude oil prices high and increase competition for gasoline imports.

Crude prices (WTI) are expected to remain above $60 per-barrel for the rest of 2006 and 2007;

In the United States, additional changes in gasoline specifications and tight refinery capacity can be expected to increase operating costs slightly and limit supply flexibility.

Gasoline prices are expected to average $2.62 over this summer;

Diesel prices also are expected to average $2.62 this summer.

Summary

Source: EIA, Short-Term Energy Outlook, April 2006

Extra Slides

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1999 2000 2001 2002 2003 2004 2005 2006 2007

Refiner Retail

Forecast

Dollars per

Gallon ($2005)

Inflation-Adjusted Summer Gasoline Margins Continue to Rise

Source: EIA, Short-Term Energy Outlook, April 2006

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

2004-2005 2005-2006 2006-2007

Consumption Production Stock Draw Net Imports

Summer Motor Gasoline Supply/Consumption Growth Balance (Change from Year Ago)

Forecast

Million barrels per day

Note: Net imports and stock draw include blending components

Source: EIA, Short-Term Energy Outlook, April 2006

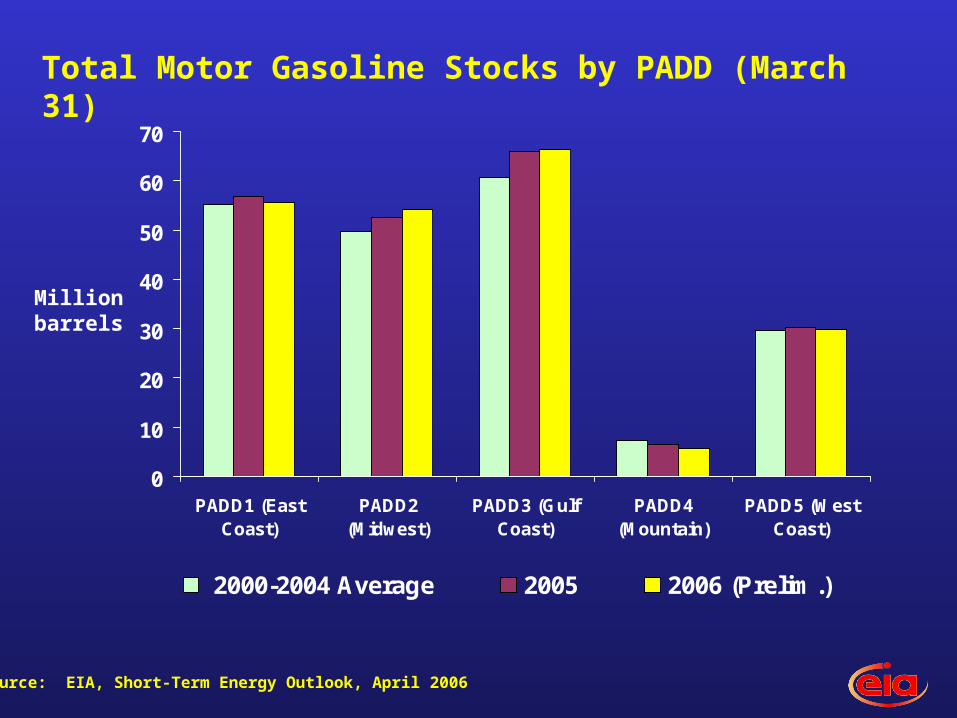

0

10

20

30

40

50

60

70

PADD1 (EastCoast)

PADD2(Midwest)

PADD3 (GulfCoast)

PADD4(Mountain)

PADD5 (WestCoast)

2000-2004 Average 2005 2006 (Prelim.)

Total Motor Gasoline Stocks by PADD (March 31)

Million barrels

Source: EIA, Short-Term Energy Outlook, April 2006

Natural Gas Spot Prices Projected to Dip During Spring and Summer ‘06, but Remain Relatively High

0

2

4

6

8

10

12

14

16

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Forecast

Dollars per

thousand cubic feet

Source: EIA, Short-Term Energy Outlook, April 2006

-100

0

1000 J

MontBilli

o

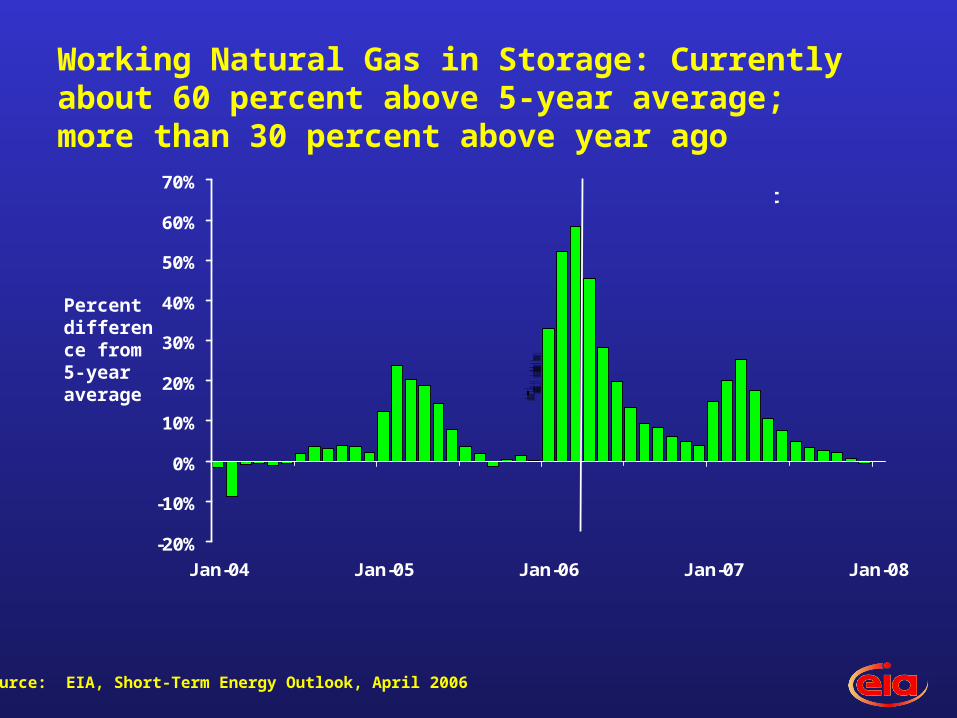

Working Natural Gas in Storage: Currently about 60 percent above 5-year average; more than 30 percent above year ago

-100

0

1000 J

MontBill

io

-100

0

1000 J

MontBill

io

-100

0

1000 J

MontBill

io

-500

0

500 A

MontBill

io

-70%

J

MontPer

ce

-70%

J

MontPe

rce

Source: EIA, Short-Term Energy Outlook, April 2006

Percent difference from 5-year average

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Forecast