staples company valuation jackie phan latrisha searcy anna dai

TRANSCRIPT

STAPLES COMPANY VALUATIONJACKIE PHAN

LATRISHA SEARCY

ANNA DAI

STAPLES INC.

Founded in 1985 by Tom Stemberg

First store opened in 1986 to serve the needs of small businesses and consumers

Staples operates in over 26 countries in the retail, business to business, and e-commerce areas

Sells office supplies, furniture, computers, and technology products and services

INDUSTRY AND COMPETITORS

Staples is the leading office supply retailer

Office Depot, Amazon.com Inc., and United Stationers Inc., who all offer similar office supplies, furniture, and equipment

OfficeMax and Office Depot were the No. 2 and No. 3 office supply retailers behind Staples Inc. until the two companies merged

Customers now look beyond office supply superstores when buying office supplies

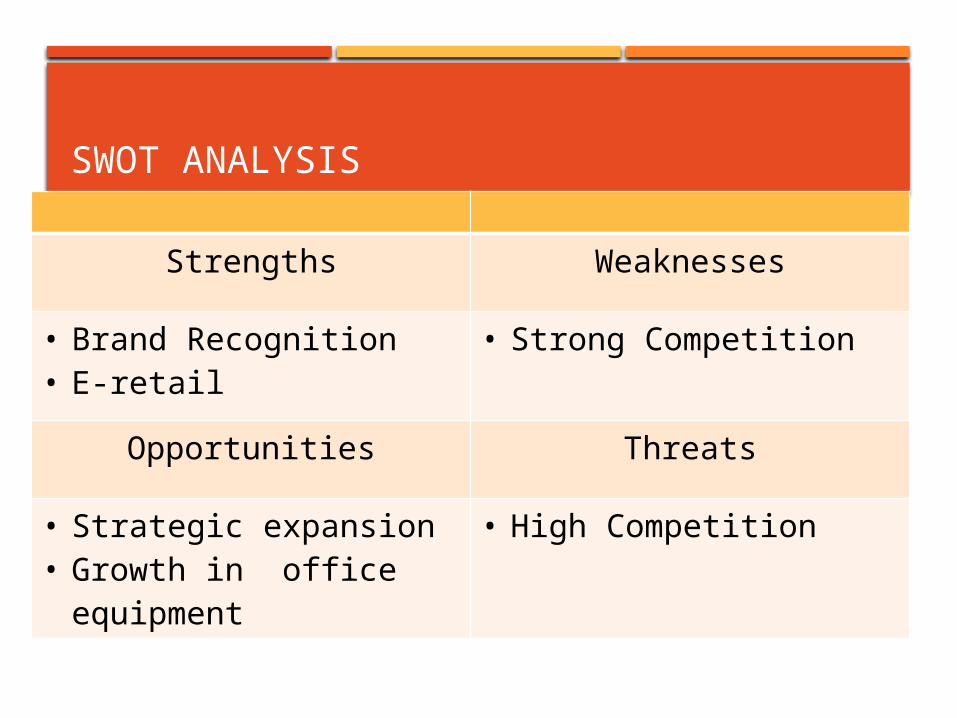

SWOT ANALYSIS

Strengths Weaknesses

• Brand Recognition• E-retail

• Strong Competition

Opportunities Threats

• Strategic expansion• Growth in office

equipment

• High Competition

VALUE DRIVERS

Staples refers to their key values as Staples Soul

Staples Soul is divided into four categories

Community, Environment, Diversity, and Ethics

FINANCIAL ANALYSIS Company Values Industry Values

2012 2011 2010 2012 2011 2010

Liquidity Ratio

Current 1.4 1.54 1.51 1.5 1.3 1.3

Quick 0.88 1.04 0.96 0.8 0.8 0.8

Asset Management Ratio

Inventory Turnover 10.54 10.29 10.4 3.72 3.77 3.6

Total Asset Turnover 1.99 3.98 1.76 1 1 1

DSO 27.18 days

29.67 29.3 110.95 94.53 106.57

Fixed Assets Turnover 12.42 12.03 11.43 6.58 7.3 5.75

Profitability Ratio

Net Profit Margin -1% 4% 4% 39.4 38.9 38.7

ROA -17% 7% 6% 3.9 3.5 2.3

ROE -3% 14% 13% 14.8 10.2 5.8

Debt Management Ratio

Total Debt Ratio 50.03% 47.71% 50.03%

77.6% 73.5% 71.9%

Times Interest Earned 3.14 9.37 7.32 2.8 2.9 1.9

Market Value Ratio

P/E Ratio -54.85 11.25 17.9

Market/Book Ratio 9.17 10.11 9.71

LIQUIDITY

In conclusion, Staples does not have as good ability to use assets to cover the cost of liabilities as they come due.

Not as good as others in industry

2012 2011 2010 2012

Liquidity Ratio

Current 1.4 1.54 1.51 1.5

Quick 0.88 1.04 0.96 0.8

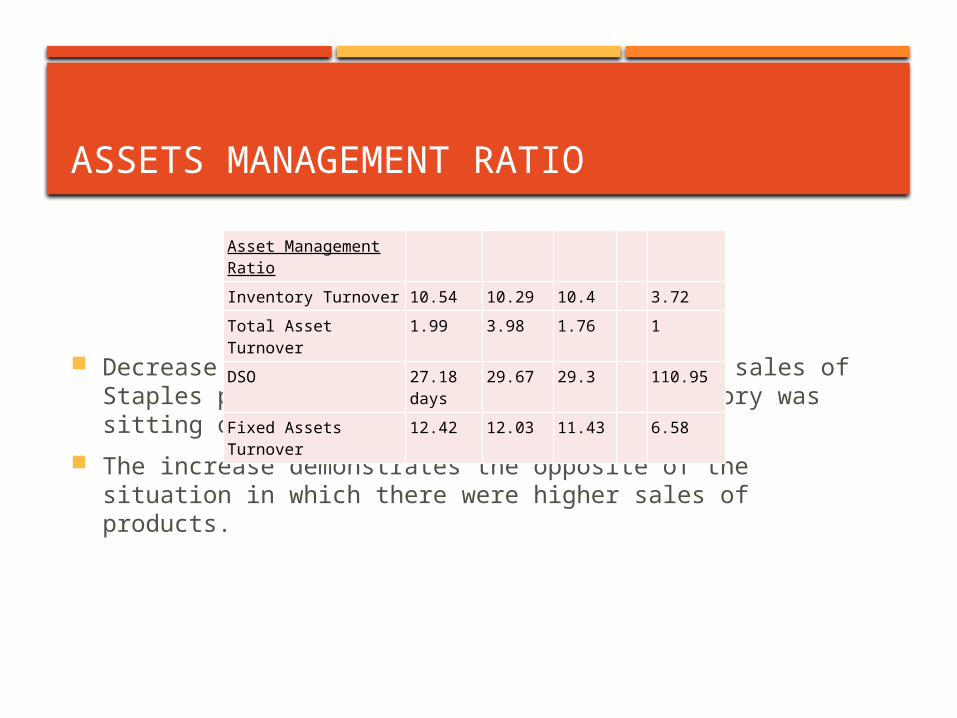

ASSETS MANAGEMENT RATIO

Decrease in 2010 to 2011 shows decreases in sales of Staples products or that more of the inventory was sitting on shelves or warehouses.

The increase demonstrates the opposite of the situation in which there were higher sales of products.

Asset Management Ratio

Inventory Turnover 10.54 10.29 10.4 3.72

Total Asset Turnover 1.99 3.98 1.76 1

DSO 27.18 days

29.67 29.3 110.95

Fixed Assets Turnover 12.42 12.03 11.43 6.58

TOTAL ASSET TURNOVER

This 2.22 point increase measures the company’s efficiency at using their assets to generate sales or revenue.

However in 2012 the ratio shows that there was a decrease of 1.99 from 3.98. therefore reducing their revenue or sales.

Had a net loss

Asset Management Ratio

Inventory Turnover 10.54 10.29 10.4 3.72

Total Asset Turnover 1.99 3.98 1.76 1

DSO 27.18 days

29.67 29.3 110.95

Fixed Assets Turnover 12.42 12.03 11.43 6.58

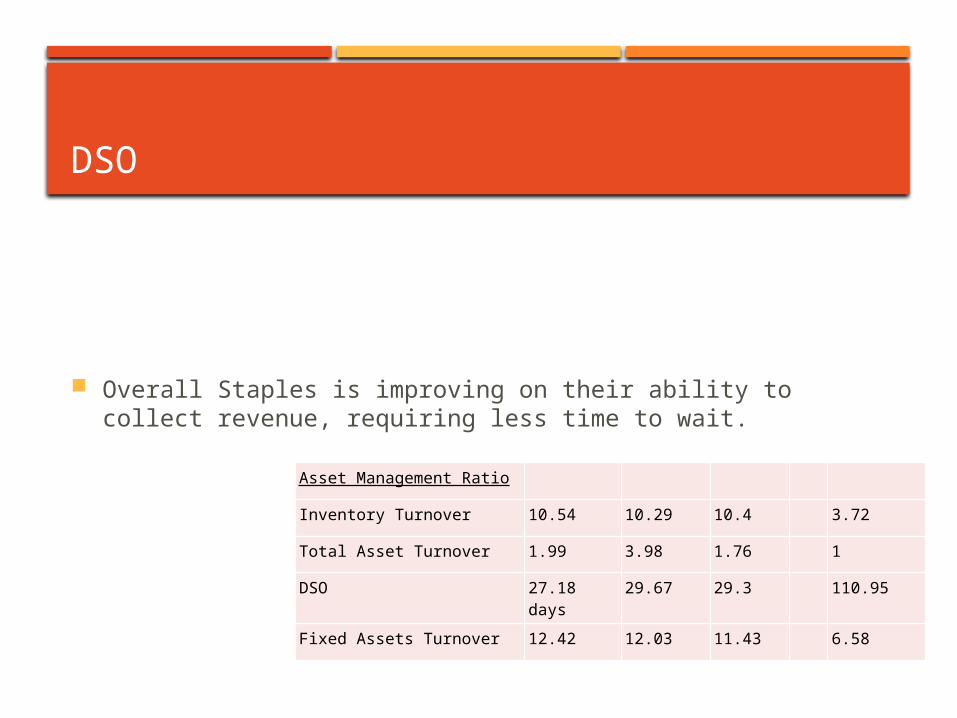

DSO

Overall Staples is improving on their ability to collect revenue, requiring less time to wait.

Asset Management Ratio

Inventory Turnover 10.54 10.29 10.4 3.72

Total Asset Turnover 1.99 3.98 1.76 1

DSO 27.18 days 29.67 29.3 110.95

Fixed Assets Turnover 12.42 12.03 11.43 6.58

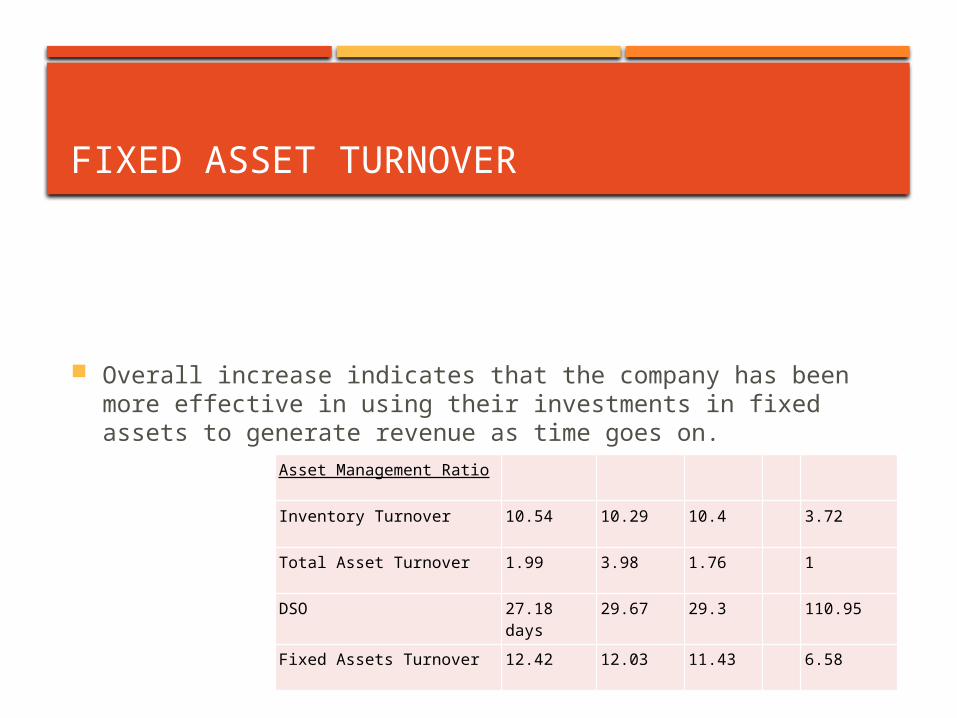

FIXED ASSET TURNOVER

Overall increase indicates that the company has been more effective in using their investments in fixed assets to generate revenue as time goes on.

Asset Management Ratio

Inventory Turnover 10.54 10.29 10.4 3.72

Total Asset Turnover 1.99 3.98 1.76 1

DSO 27.18 days

29.67 29.3 110.95

Fixed Assets Turnover 12.42 12.03 11.43 6.58

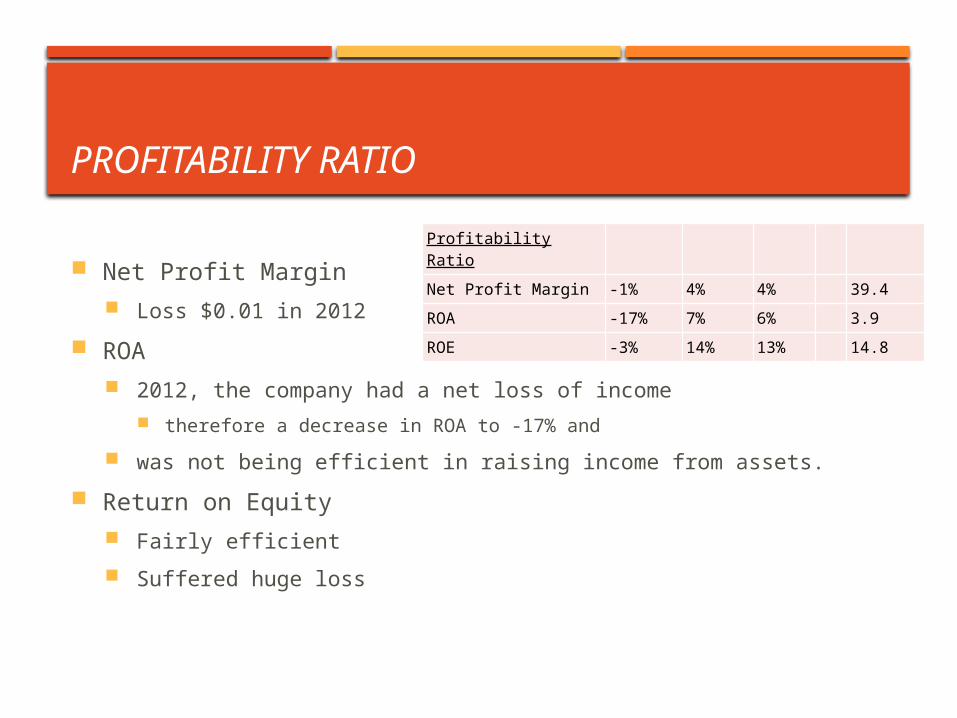

PROFITABILITY RATIO

Net Profit Margin Loss $0.01 in 2012

ROA 2012, the company had a net loss of income

therefore a decrease in ROA to -17% and

was not being efficient in raising income from assets.

Return on Equity Fairly efficient

Suffered huge loss

Profitability Ratio

Net Profit Margin -1% 4% 4% 39.4

ROA -17% 7% 6% 3.9

ROE -3% 14% 13% 14.8

DEBT MANAGEMENT RATIO

total debt ratio staying constant.

debt ratio of less than 1,

More assets than debt, not much risk

Time Interest Earned ratio High Times Interest Earned ratio

does not have much debt or is paying down too much debt with earnings that could be used for other projects.

With a significantly lower ratio, Staples may perhaps have invested their earnings in other projects or has taken on more debt.

Debt Management Ratio

Total Debt Ratio 50.03% 47.71% 50.03%

77.6%

Times Interest Earned 3.14 9.37 7.32 2.8

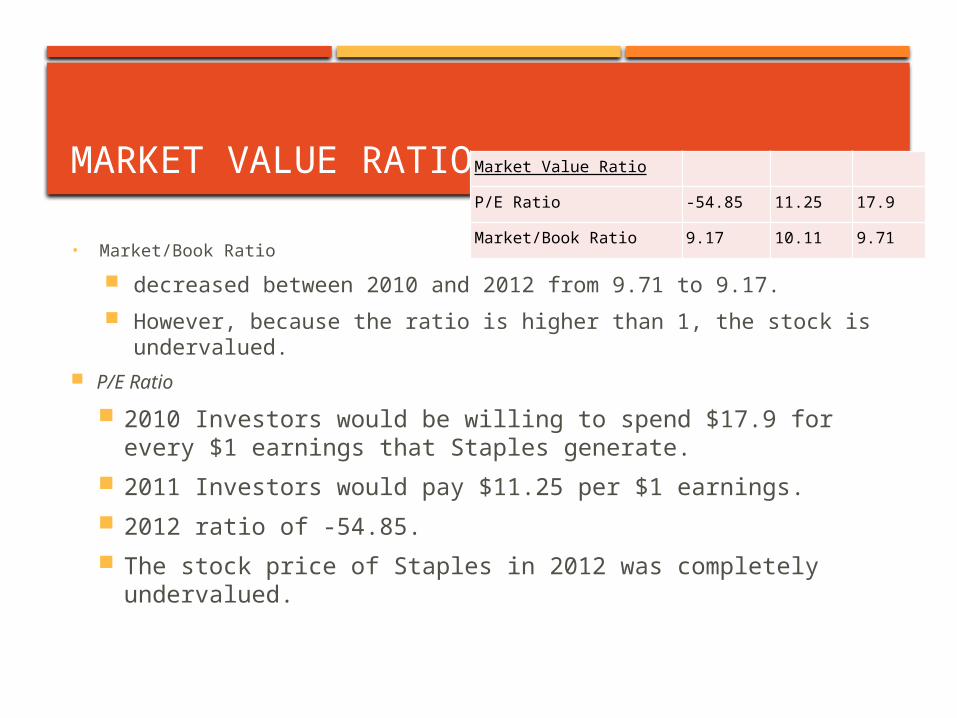

MARKET VALUE RATIO

• Market/Book Ratio

decreased between 2010 and 2012 from 9.71 to 9.17.

However, because the ratio is higher than 1, the stock is undervalued.

P/E Ratio

2010 Investors would be willing to spend $17.9 for every $1 earnings that Staples generate.

2011 Investors would pay $11.25 per $1 earnings.

2012 ratio of -54.85.

The stock price of Staples in 2012 was completely undervalued.

Market Value Ratio

P/E Ratio -54.85 11.25 17.9

Market/Book Ratio 9.17 10.11 9.71

FIRM RISKINESS

Consumer base is relatively staple The growth rate can be limited

Vulnerabilities of the supply chain Low level of cost efficiency and low profit margins

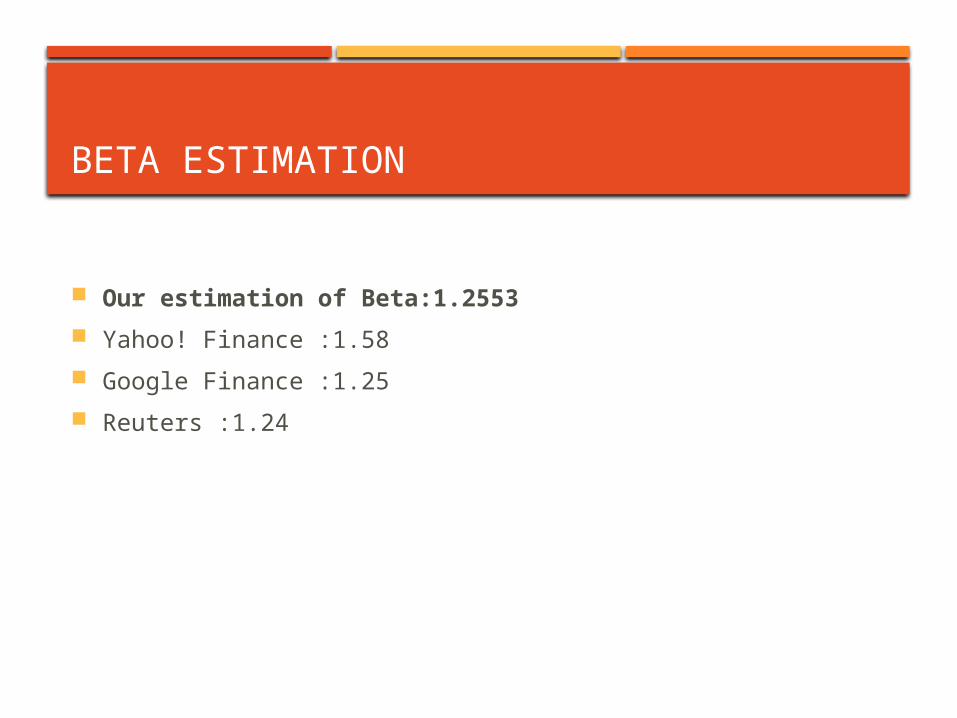

BETA ESTIMATION

Our estimation of Beta:1.2553

Yahoo! Finance :1.58

Google Finance :1.25

Reuters :1.24

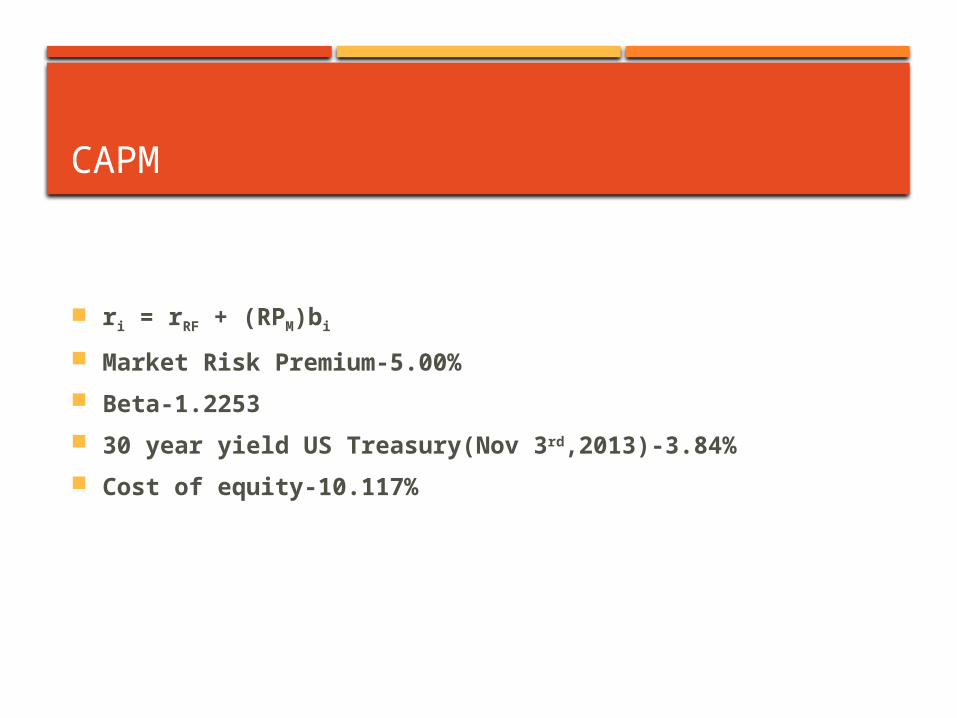

CAPM

ri = rRF + (RPM)bi

Market Risk Premium-5.00%

Beta-1.2253

30 year yield US Treasury(Nov 3rd,2013)-3.84%

Cost of equity-10.117%

DDM

Historical Perspective

Year 2012 2011 2010 2009 2008

Annual

Dividend

0.39 0.36 0.33 0.33 0.29

Dividend

Growth Rate

8.33% 9.09

%

3.13

%

0.00% 13.79

%

DDM

Analyst report dividend growth rates Yahoo Finance 3.10%

Bloomberg 3.10%

Google Finance 3.12%

ROE*plowback Since Staples run a loss in terms of the net income, our ROE became -

0.0343, which make our dividend growth rate -8.22%.

DDM

Forecasted dividends

Forecasted Dividends

2013 2014 2015 2016 2017 2018 2019 2020 2021 202

2

2023

0.4532

0.466796

0.4808

0.495224

0.510081

0.525383

0.541145

0.557379

0.5741

0.591323

0.609063

DDM

Dividend Discounted Model

Constant growth rate 5.00%

Dividend growth rate 5.75%

Length of growth

period

10 years

Cost of capital 10.12%

Horizon Value 12.8205

Price 7.84

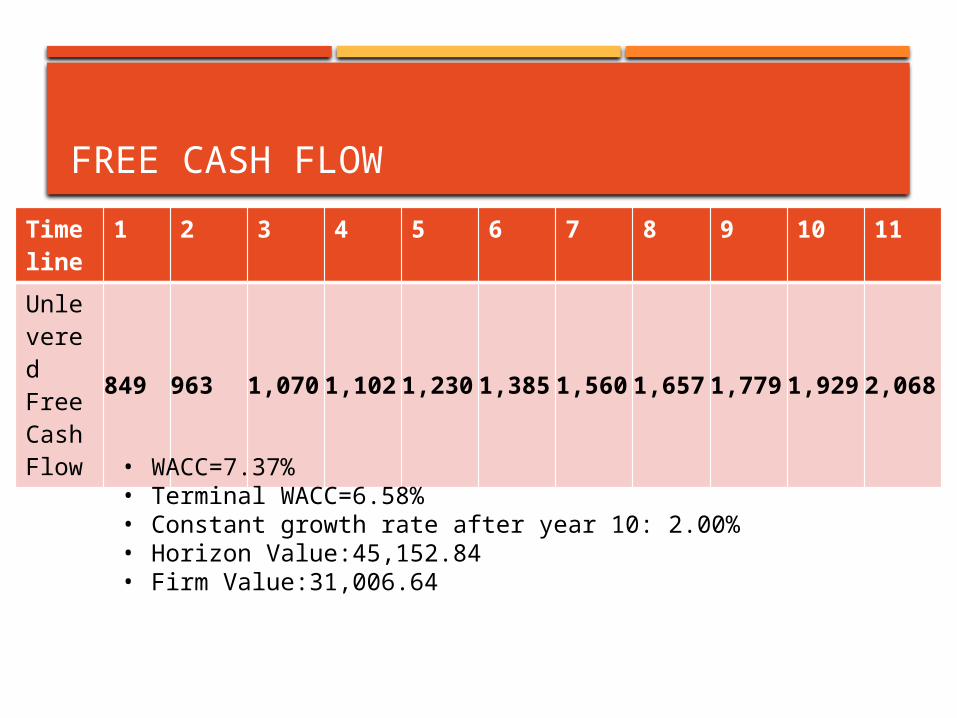

FREE CASH FLOW

Timeline

1 2 3 4 5 6 7 8 9 10 11

Unlevered Free Cash Flow

849 963 1,070 1,102 1,230 1,385 1,560 1,657 1,779 1,929 2,068

• WACC=7.37%• Terminal WACC=6.58%• Constant growth rate after year 10: 2.00%• Horizon Value:45,152.84• Firm Value:31,006.64

FREE CASH FLOW

Firm value $31,006.64

Add Cash and marketable securities $1,334.30

Subtract long term debt $1,733.23

Equity Value $

30,607.72

Final Stock price $46.82

Fiscal year 2012 2011 2010 2009 2008 2007

Total revenues25,002,1

9224,545,

11324,275,

45123,083,

77519,372,

68218,160,

789 Revenue growth rate ([Revenue(t)-Revenue(t-1)]/Revenue(t-1)] 1.86% 1.11% 5.16%19.16% 6.67%

2-year average 1.49%

6-year average 6.79%6-year average (2006-2001 excluding 2004) 6.79%

Conclusion

Because negative growth in revenue in 2004 was caused by discountinued operations, one can exclude from calculations as being non-representative

Conservative estimate 6.79%Aggressive estimate (assuming recent growth will persist) 1.49%

Yahoo analyst forecast for 2015-0.70%

See Yahoo Data

WACC calculation

Cost of equity 10.117% = Rrf +(Market risk premium)*beta = 3.84% + 5.00%* 1.2553 Beta 1.2553Source: Yahoo Market risk premium 5.00%Our assumption 10-year yield on a US Treasury 3.84% 21-Nov-13

Cost of debt 4.64% = 3.84% + 0.80% 10-year yield on a US Treasury 3.84% Credit rating BBB spread 0.80%

Debt to Value 37.92% Equity to Value 62.08%

Market value of equity 10,070 in million

Number of shares outstanding 653.68Need to use diluted shares

Market price per share 15.36Source: Yahoo Market value of debt 6,151 Assume that it equals book value of debt

Value 16,221

a

WACC 7.37% = rE*(E/V)+rD*(1-t)*(D/V)

It is reasonable to assume that when Target enters a constant growth phaze, its beta will approach 1 Terminal WACC 7.25% Terminal cost of equity 8.8400% Terminal growth rate 2.00%

MULTIPLE VALUATION

Multiply Staples’ most recent earnings per share (EPS) of 0.74 as of December 2, 2013 by the industry’s P/E ratio of 49.20 to get an answer of $36.41.

weighted average of the stock price

($7.84 +$46.82+ $36.41)

3

$30.35

RECOMMENDATION

Worth to invest

Compare with the current stock price of $15.7 from yahoo finance

The Staples stock price is undervalued