staying ahead - tm forum · pdf filemobile revenues and kpi forecast (eu estimates are low) 40...

TRANSCRIPT

© 2013 TM Forum | 1

V2013.5

Staying Ahead

of a rapidly

changing

industry

Joann O’Brien VP, Collaborative R&D

© 2013 TM Forum | 2

V2013.5

Agenda

9:00am: Joann O’Brien, VP, Collaborative R&D

Welcome & Evolving Collaboration to meet current and future Industry needs

Bill Ahlstrom, President & COO, TM Forum

9:10 – 9:25am: Nik Willetts, CSO, TM Forum

9:25 – 9:50am: Jesús Romero, Corporate Strategy Director, Telefonica How he sees the industry shifting and the impacts this is having on the telecommunications strategy

9:50am – 10:05am: Laurent Leboucher, Vice President APIs and Digital Ecosystems,

Orange & Chair TM Forum Strategy & Adoption Sub-Committee Outlining how the changes in the industry impact on Forum activities

10:05 – 10:15am

Eric Troup, Chief Technical Officer, Worldwide Communications & Media Industries

10:15am – 10:30am: Ken Lipnickey, Director Project Management TM Forum Action Week Logistics

© 2013 TM Forum | 3

V2013.5

Welcome

Bill Ahlstrom

President & COO

TM Forum

© 2013 TM Forum | 4

V2013.5

inform innovate accelerate optimize

Action Week

2014

Good morning! February 10, 2014

© 2013 TM Forum | 5

V2013.5

Who we are

TM Forum is a

global trade

association for

enterprises,

service providers

and their suppliers.

We’re trusted by

the world’s largest

companies to help

them continuously

transform and

succeed in the

digital economy.

85,000+ Member

Professionals

900+ Member

Companies

Global Coverage

1 Forum

© 2013 TM Forum | 6

V2013.5

Is your business a digital native?

agile

fast

efficient

innovative

customer centric

software centric

partner centric

data-driven

secure

mobile

Defining the Digital Business

© 2013 TM Forum | 7

V2013.5

Solving three core challenges for any business

Agile

Business and

IT

Program

Transform

IT & operations

to reduce costs,

minimize risk and

improve time-to-

market

Business

Growth

Program

Maximize

market share,

customer loyalty

and enable new

growth

Open

Digital

Program

Deliver new

services

quickly, easily

and securely

with partners

Rapid Partner

Onboarding

Digital Partner

Security

End-to-End

Service Quality

Managing Money

between Partners

Business

Process

Optimization

Revenue

Management

Cloud,

SDN and NFV

IT & Operations

Transformation

Big Data

Analytics Cyber Security

Big Data

Analytics

Experience

Management

Customer

Privacy

© 2013 TM Forum | 8

V2013.5

This week…

Collaborate

Share

Learn

Network

Create

Enjoy!

Corporate Strategy

Telefónica, S.A.

10 February 2014

Telecoms sector

Time to invest in long term sustainability

DISCOVER. DISRUPT. DELIVER

Executive summary

10

#1: Revenue growth is the main TSR driver; must focus on customer needs Investors reward sustainable revenue growth, ahead of margin trends

#2: Dividend yield was not a key TSR driver in 2013; higher capex and M&A Telco average TSR +27.2% (5.8% DY), ICT average TSR +48.2% (1.6% DY)

#3: Growth outlook in 2014 remains stronger for ICT players … … but long term sustainability is the key issue for all (AAPL -8% post Q4)

#4: IT plays a critical role in the required transformation for all telcos Overcome complexity using standards to facilitate interaction with 3rd parties

DISCOVER, DISRUPT, DELIVER 11

1. The big picture - revenue growth forecasts

2. ICT Hypersector – 2013 TSR performance

3. Growth outlook, sustainability and bundling

4. IT plays a critical role in our transformation

DISCOVER. DISRUPT. DELIVER

Telcos are in a key position in the ICT industry

12

$ 1,116 bn $ 1,627 bn

Devices

+HW2

Digital

Content + IT

solutions3

Connectivity1

Customer

$ 1,574 bn

$ 4,317 bn Total size of the ICT Hypersector (2012)

1. Includes Mobile voice and data, fixed voice and data. 2. Includes Consumer Electronics & mobile devices contributing $788Bn

(phones, PCs, tablets, game consoles, Flat panel TVs, and other CE) + hardware and telecom equipment. 3. Includes Information

Technology (IT services, software) + Digital contents (TV/Filmed, B2B, internet advertising, video games, radio/music,

newspapers/magazines/books)

12

Smartphones and tablets

(linked to telecom networks)

drive growth

• Core telco business

• >35% of the hypersector, led

by mobile voice and data

• >$200bn growth in 2012-16

• Customers increasingly

access content and apps

in the cloud

• Telecom networks are

key to use cloud services

DISCOVER. DISRUPT. DELIVER 13

Global Telecom revenues forecast (+$234bn by 2016F)

1,326

1,536

1,770

2008 2012 2016F

Telecom market (USD Bn)

3.8%

CAGR

3.6%

CAGR

North America

309 353 417

2008 2012 2016F

3.4% 4.2%

308 287 277

63 87 90

2008 2012 2016F

-1.7% -0.9%

Europe

223 220 235

186 252 334

2008 2012 2016F

-0.3%

Asia / Pacific (APAC)

138 188 246 99

149 171

2008 2012 2016F

10.6% 3.6%

Emerging Regions

8.1% 6.8%

1 – Developed countries in Asia / Pacific: Australia, Honk Kong,

Japan, Korea, Singapore, Taiwan

Source: IDC Black Book 2013

7.8% 7.3%

1.7%

8.4% 1.0%

LatAm

ME&A

Developed (1)

Emerging

W Europe

E Europe

DISCOVER. DISRUPT. DELIVER 14

Mobile revenues and KPI forecast (EU estimates are low)

40 72 105 32

82

164

37

65

77

13

33

64

9

30

38

73

104

32 17 12

31 25 20 19 12 10 11 11 12

8 7 6

2016F

24 21 20 26 21 23 24 14 11 36

12 8

15 7 5

84 57 46

109 111 98

116 84

73

59 79 100

57 84 91

123 172 206

Mobile Broadband Mobile Voice

Source: IDC, Pyramid Research (Sept-13), Yankee Group (Dec-12)

Revenues (US$ Bn) Revenues (US$ Bn)

2008 2012 2016F 2008 2012 2016F

2008 2012

2008 2012 2016F 141 282 448 103

318

606 129

380

607 29

222

673 48

244

532 53

657

Revenues per data enabled access

(US$ / month & subscription)

2008 2012 2016F

2008 2012 2016F

Data enabled accesses

(millions 3G+/4G/Wimax subscriptions)

450

2103

5361

167

345

544

10.5%

18.1%

4.4%

19.0%

10.0%

CAGR

12-16

-3.7%

-3.2%

-5.2%

1 – Developed countries in Asia / Pacific: Australia,

Honk Kong, Japan, Korea, Singapore, Taiwan

2 – Rest of the World: Emerging countries in Asia /

Pacific (China, India…) and Eastern Europe

548 587 614

2.1%

6.2%

218 273 311 288 368 401 518 562 623 450 573 661 577 991 1308

8070 Accesses (millions mobile lines)

4044

6325

CAGR

12-16

3558 4766

1993

20

Developed in APAC1 North America

LATAM RoW2

Western Europe

ME&A

2494

Monthly revenues per mobile line (US$)

DISCOVER. DISRUPT. DELIVER

What are industry analysts missing? Three main points

15

European telecoms are currently experiencing a triple-bottom in the

economic, regulatory and product cycles. Key highlights include:

Economy – After two years of negative GDP growth (-0.7% and -0.3%

in 2012-13), a recovery is on the way (2014 +1.0% and 2015 +1.5%)

Regulation – The tide could be turning in Brussels. A stable

investment framework and in-market consolidation are expected.

Product – The need to provide best-in-class customer experience

and superior network quality applies to Europe as well (FTTH/LTE)

Fixed broadband customer experience will radically improve with

superior network speeds and beyond connectivity bundles.

Rapidly declining prices for smartphones will drive mobile data

penetration much higher than currently anticipated across all markets.

Industry forecasts extrapolate for the next few years the main trends

from the recent past. Revenue growth in Europe should be higher.

DISCOVER, DISRUPT, DELIVER 16

1. The big picture – revenue growth forecasts

2. ICT Hypersector – 2013 TSR performance

3. Growth outlook, sustainability and bundling

4. IT plays a critical role in our transformation

DISCOVER. DISRUPT. DELIVER

Coverage universe (100 stocks)

TELCO

1.AMERICA MOVIL 26.OTE

2.AT&T 27.PORTUGAL TELECOM

3.BELGACOM 28.ROGERS

4.BELL CANADA 29.SINGTEL

5.BHARTI 30.SOFTBANK

6.BT 31.SPRINT

7.CABLEVISION 32.SWISSCOM

8.CHINA MOBILE 33.TDC

9.CHINA UNICOM 34.TEF BRAZIL

10.CHINA TELECOM 35.TEF DEUTSCHLAND

11.COMCAST 36.TELE2

12.DEUTSCHE TELEKOM 37.TELECOM ARGENTINA

13.ELISA 38.TELECOM ITALIA

14.ENTEL 39.TELEFONICA

15.ILIAD 40.TELEKOM AUSTRIA

16.KDDI 41.TELENOR

17.KPN 42.TELIASONERA

18.LIBERTY 43.TELSTRA

19.MILLICOM 44.TIM Br

20.MTN 45.TIME WARNER

21.NEXTEL 46.VERIZON

22.NTT 47.VIMPELCOM

23.NTT DOCOMO 48.VIVENDI

24.Oi 49.VODAFONE

25.ORANGE 50.ZIGGO

INTERNET, MEDIA AND TECHNOLOGY

1.21C FOX 26.IBM

2.ACCENTURE 27.INTEL

3.ADOBE 28.JUNIPER

4.ALCATEL 29.LENOVO

5.AMAZON 30.LINKEDIN

6.APPLE 31.MICROSOFT

7.ARM HOLDINGS 32.NASPERS

8.ASML 33.NETFLIX

9.BAIDU 34.ORACLE

10.BLACKBERRY 35.PRICELINE

11.BROADCOM 36.QUALCOMM

12.BSKYB 37.SAMSUNG

13.CANON 38.SAP

14.CISCO 39.SONY

15.CORNING 40.TAIWAN SEMI

16.CRM 41.TELEVISA

17.DIRECTV 42.TENCENT

18.DISCOVERY 43.TEXAS INSTR.

19.EBAY 44.TIME WARNER

20.EMC 45.VIACOM

21.ERICSSON 46.VMWARE

22.FACEBOOK 47.WALT DISNEY

23.GOOGLE 48.WPP

24.HONHAI 49.YAHOO

25.HP 50.ZTE

17

DISCOVER. DISRUPT. DELIVER

Telcos 2013 – TSR +27.2% (only 5.8% from dividend yield)

TSR performance in TELCO companies in 2013 (%)

Capital appreciation in 2013 (EUR bn)

51.1 48.1

27.6 21.6

16.9 16.2 14.9 14.3 13.9 12.2 7.8 7.5 7.4 7.2 5.8 5.6 5.0 4.6 3.4 3.3 3.3 3.0 2.9 2.4 1.8 1.7 1.7 1.6 1.4 1.2 1.1 1.0 0.9 0.8 0.6 0.6 0.4 0.4 0.3

-0.1 -0.2 -0.5 -0.6 -0.9 -1.5 -1.8 -2.2 -2.9 -3.0

-18.4

SFBK

VO

D

CM

CS

KD

DI

DT

NTT

DO

CO

MO BT S

VZ

TW

C

LBTY

TEF

TLSTRA

TN

OR

ATT

MTN

TLSN

TIM

Br

ST

SW

CM

VIP

VIV

OTE

BCE

ORA

ZIG

GO

TEO

TD

C

AM

X

ILIA

D

RO

G

MIL

LIC

OM TI

BH

RT

CVIS

ION

ELI

KPN

O2D

TKA

BCO

M

NEXTEL

PT

EN

TEL

TEF B

r

CU

TELE2

Cte

l

Oi

Cm

ob

1

8

195%

118% 107% 90%

69% 63% 61% 56% 56% 45% 43% 43% 43% 42% 41% 40% 35% 31% 30% 29% 26% 25% 25% 20% 19% 19% 18% 16% 15% 15% 14% 12% 11% 10% 9% 9% 4% 4% 4%

0% -3% -5% -7% -7% -8% -11% -25%

-49% -61%

SFBK

KD

DI

TEO

OTE

BT

VO

D

NTT

TIM

BR

DT

DO

CO

MO

ZIG

GO

TW

C

TDC

CM

CS

LBTY

VIP

TN

OR

TLSTRA

TLSN

MTN

SW

CM

ELI

CVIS

ION

VIV

TEF

VZ

MIL

LIC

OM ST

ILIA

D

ORA

BCE

O2D

RO

G

ATT TI

BCO

M

BH

RT

KPN

AM

X

TEF B

R

TKA

CU

CTel

CM

ob

PT

TELE2

EN

TEL Oi

NEXTEL

TEF

TEF B

r

O2D

TEF

O2D

TEF B

r

Source: Bloomberg (TSR and Consensus Tracker), Dec 2013

CM

ob

CTel

DISCOVER. DISRUPT. DELIVER

Average 12M FWD EPS declined 5% but PE re-rated by +40%

193%

112% 100% 94% 90%

64% 56% 53% 50% 45% 41% 39% 39% 39% 34% 31% 29% 23% 22% 22% 20% 20% 20% 16% 15% 14% 14% 14% 13% 11% 8% 8% 6% 6% 4% 4% 4% 4% 2%

-3% -4% -7% -9% -9% -11% -16% -28% -38%

-57% -61%

SFBK

KD

DI

TEO S

OTE

BT

NTT

VO

D

TIM

Br

DT

LBTY

TW

C

DO

CO

MO

CM

CS

ZIG

GO

TD

C

TN

OR

VIP

MTN

TLSN

TLSTRA

CVIS

ION

SW

CM

TEF

ELI

ILIA

D

MIL

LIC

OM VZ

VIV ST

ORA

BCE

RO

G TI

ATT

BH

RT

KPN

O2D

AM

X

BCO

M

TKA

CU

TEF B

r

Cte

l

Cm

ob

PT

EN

TEL

TELE2 Oi

NEXTEL

442%

51% 36% 32% 28% 24% 22% 13% 13% 12% 12% 12% 10% 9% 9% 9% 8% 8% 8% 7% 6% 5% 5% 2% 1% 1%

0% -1% -1% -3% -4% -4% -13% -14% -14% -16% -19% -19% -19% -21% -24% -29% -36% -37% -48%

-61% -61% -69% -74%

NEXTEL

ILIA

D

TEO

CU

CM

CS

KD

DI

VZ

SFBK

TN

OR

BT

NTT

TLSTRA

TW

C

ZIG

GO

MTN

VIP

Cte

l

RO

G

BH

RT

OTE

TLSN

TKA

ATT

ST

DO

CO

MO

TD

C

DT

ELI

BCE

SW

CM

Cm

ob

TIM

Br

Oi

AM

X

TEF B

r

ORA

BCO

M

VO

D

TEF

LBTY

EN

TEL

MIL

LIC

OM TI

VIV

CVIS

ION

TELE2

PT

KPN

O2D

294% 240% 159% 130%

119%

88% 79% 79% 78% 71% 64% 63% 61% 57% 47% 46% 45% 43% 39% 37% 31% 29% 27% 23% 23% 19% 19% 16% 14% 14% 14% 12% 9% 9% 9% 8% 7% 0%

-1% -2% -3% -5% -7% -9% -10% -19% -24% -31% -50%

O2D

KPN

SFBK

CVIS

ION

PT

VO

D

VIV

LBTY

OTE

KD

DI

TI

MIL

LIC

OM

TELE2

TIM

Br

TEO

BT

DT

TEF

NTT

DO

CO

MO

TD

C

ORA

TW

C

SW

CM

ZIG

GO

AM

X

BCO

M

ELI

TLSN

TN

OR

VIP

MTN

BCE

ST

CM

CS

TSTRA

TEF B

r

NEXTEL

ATT

RO

G

BH

RT

EN

TEL

VZ

TKA

CM

ob

CTel

ILIA

D

CU Oi

Capit

al R

etu

rn (

%)

∆ 1

2m

FW

D E

PS

∆ 1

2m

FW

D P

E

1

9

TEF

TEF B

r

O2D

TEF

TEF B

r

O2D

TEF

TEF B

r

O2D

Source: Bloomberg (TSR and Consensus Tracker), Dec 2013

CM

ob

CTel

CM

ob

CTel

CM

ob

CTel

DISCOVER. DISRUPT. DELIVER

EPS cuts driven by weak revenues and lower margins

20

Revenue

Gro

wth

(%

)

EBIT

Marg

in

Change (

%)

Share

s C

hange &

Rest

* (%

)

*Rest = Changes in Net Income margin vs. EBIT Margin

79% 67%

37%

17% 15% 15% 15% 12% 9% 8% 8% 8% 5% 5% 5% 5% 4% 3% 3% 3% 3% 3% 3% 2% 2% 1% 1% 1% 1% 1% 0%

0% -1% -1% -2% -2% -5% -5% -5% -6% -8% -8% -8% -9% -12% -17% -20% -27% -34%

SFBK

LBTY

TEO

EN

TEL

KD

DI

ILIA

D

CU

CTEL

CM

OB

BH

RT

CM

CS

MIL

LIC

OM

DT

BCE

TIM

Br

VZ

TN

OR

DO

CO

MO

RO

G

MTN

TLSTRA

TEF B

r

SW

CM

ATT

TW

C

NTT

BT Oi

TKA

ZIG

GO

VO

D

ELI

AM

X

BCO

M

VIP

TLSN

KPN

ORA

O2D

TD

C ST

PT

CVIS

ION

TEF

OTE TI

VIV

TELE2

NEXTEL

TEF

O2D

TEF B

r

299%

109%

42% 42% 26% 23% 22% 17% 17% 14% 12% 11% 10% 10% 9% 4% 2% 1% 1% 0%

-2% -2% -3% -5% -6% -8% -9% -10% -13% -13% -14% -17% -18% -19% -22% -23% -24% -28% -34% -36% -53% -55% -57% -61% -68% -73% -82%

-136% -353%

NEXTEL Oi

ILIA

D

TKA

BH

RT

KD

DI

VZ

CU

OTE

TLSN

TN

OR

BT

TLSTRA

CM

CS

TD

C

RO

G

MTN

BCE

VIP

NTT

DT

TW

C

ELI

DO

CO

MO

ZIG

GO

SW

CM

TIM

Br

ATT

VO

D

TEF

ORA TI

CM

OB

BCO

M

AM

X

ST

PT

CTEL

TEF B

r

EN

TEL

MIL

LIC

OM

KPN

TELE2

O2D

VIV

TEO

SFBK

CVIS

ION

LBTY

TEF

TEF B

r

O2D

265% 177% 96%

53% 50% 32% 24% 23% 17% 16% 15% 14% 12% 11% 10% 10% 9% 8% 4% 4% 3% 3% 3% 2% 2% 2% 2% 0% 0%

0% 0% -1% -2% -3% -3% -4% -5% -5% -6% -6% -7% -7% -8% -10% -14% -27% -30% -38%

-143%

LBTY

NEXTEL

CVIS

ION

TEO

VIV ST

CTEL

TELE2

TEF B

r

MIL

LIC

OM

SFBK

ZIG

GO

ATT

CM

CS

NTT

TW

C

VIP

AM

X

CM

OB

MTN

TEF

DO

CO

MO

ELI

ORA

SW

CM

BCO

M

OTE

RO

G

BT

CU

TIM

Br

TLSTRA TI

TD

C

TN

OR

DT

VZ

EN

TEL

VO

D

TLSN

ILIA

D

BCE

O2D

KPN

KD

DI

BH

RT

PT

TKA Oi

TEF

TEF B

r

O2D

CM

ob

CTel

CM

ob

CTel

CM

ob

CTel

DISCOVER. DISRUPT. DELIVER

ICT (ex Telcos) 2013 - TSR +48.2% (1.6% dividend yield)

TSR performance in ICT (Ex Telcos) companies in 2013 (%)

Capital appreciation in 2013 (EUR bn)

298%

242%

105% 103% 103% 101% 99% 93% 89% 87% 77% 68% 60% 59% 59% 58% 57% 55% 49% 46% 45% 44% 44% 43% 42% 38% 38% 31% 31% 27% 25% 22% 18% 17% 16% 16% 15% 14% 12% 8% 8% 4% 2% 1% 0%

0% -5% -9% -10% -37%

NFLX

ALCATEL

FB

YH

OO

NPN

HP

TCN

T

SO

NY

LKD

PCLN

BID

U

VIA

WPP

AM

ZN

AD

BE

GO

OG

21CFO

X

DIS

TW

X

TXN

GLW

MSFT

ARM

ASM

L

DIS

C

LEN

OVO

DTV

CRM

INTC

ACN

ERIC

QCO

M

ZTE

CSCO

TELEVIS

A

ORCL

JN

ET

BSY

TSEM

AAPL

EBAY

SAP

CN

ON

HO

NH

AI

EM

C

IBM

VM

WR

BCO

M

SM

SG

BBRY

2

1 Source: Bloomberg (TSR and Consensus Tracker), Dec 2013

100.2

64.9

52.3 49.5 43.3

34.3

21.3 20.0 19.7 19.5 19.4 18.4 16.1 15.6 15.2 15.1 14.4 11.9 11.3 10.7 10.3 8.9 8.6 8.1 8.0 7.8 7.3 7.1 6.6 6.3 5.8 5.6 5.5 5.2 4.9 3.6 2.3 2.0 1.7 1.5 1.1 0.8

-0.1 -0.2 -0.2 -1.4 -1.5 -1.7 -3.2

-14.5

GO

OG

MSFT

FB

AM

ZN

TCN

T

DIS

21C F

OX

PCLN

BID

U

HP

INTC

AAPL

ORCL

NPN

YH

OO

QCO

M

TW

X

NFLX

VIA

CSCO

TXN

ASM

L

LKN

D

AD

BE

WPP

ACN

DTV

DIS

C

ALCATEL

SO

NY

CRM

GLW

ARM

TSEM

ERIC

EBAY

LEN

OVO

SAP

TELEVIS

A

BSY

JN

ET

ZTE

CN

ON

EM

C

HO

NH

AI

VM

WR

BCO

M

BBRY

IBM

SM

SG

DISCOVER. DISRUPT. DELIVER

12M FWD EPS growth (>20%) and PE re-rating (>30%) C

apit

al R

etu

rn (

%)

∆ 1

2m

FW

D E

PS

∆ 1

2m

FW

D P

E

298% 242%

105% 103% 102% 99% 96% 91% 89% 87% 77%

66% 59% 59% 58% 56% 55% 53% 46% 43% 42% 42% 42% 41% 40% 38% 34% 31% 26% 24% 21% 20% 18% 15% 15% 15% 14% 10% 9% 8% 5% 3%

0% -1% -1% -2% -5% -10% -11% -37%

NFLX

ALCATEL

FB

YH

OO

NPN

TCN

T

HP

SO

NY

LKD

PCLN

BID

U

VIA

AM

ZN

AD

BE

GO

OG

21CFO

X

WPP

DIS

TW

X

ARM

DIS

C

TXN

ASM

L

GLW

MSFT

DTV

LEN

OVO

CRM

INTC

ACN

ERIC

QCO

M

ZTE

TELEVIS

A

ORCL

JN

ET

CSCO

BSY

TSEM

EBAY

AAPL

SAP

CN

ON

EM

C

HO

NH

AI

IBM

VM

WR

SM

SG

BCO

M

BBRY

330% 147%

92% 75% 73%

46% 41% 37% 36% 35% 29% 28% 28% 25% 23% 23% 18% 17% 17% 16% 16% 16% 16% 14% 13% 12% 11% 9% 9% 8% 7% 7% 7% 7% 7% 5% 3% 2% 1% 0% 0% 0%

-4% -8% -8% -9% -12% -15% -17%

-158%

NFLX

BBRY

SO

NY

LKD

FB

YH

OO

ARM

AM

ZN

NPN

PCLN

LEN

OVO

TCN

ZTE

ASM

L

JN

ET

TXN

VM

WR

QCO

M

TW

X

WPP

DIS

C

VIA

DIS

EBAY

DTV

GO

OG

HP

IBM

ERIC

ORCL

BSY

CN

ON

GLW

EM

C

BID

U

ACN

SAP

TELEVIS

A

CRM

CSCO

SM

SG

TSEM

HO

NH

AI

21CFO

X

INTC

MSFT

AAPL

AD

BE

BCO

M

ALCATEL

724%

88% 78% 70% 62% 53% 51% 48% 43% 41% 40% 39% 37% 34% 33% 32% 30% 25% 22% 22% 20% 18% 18% 16% 15% 14% 14% 13% 11% 8% 8% 6% 4% 3% 3% 2% 1% 0% 0% 0%

-1% -6% -7% -7% -7% -8% -10% -10% -19%

-88%

BBRY

AD

BE

HP

21CFO

X

BID

U

MSFT

TCN

T

NPN

VIA

GO

OG

YH

OO

PCLN

INTC

WPP

DIS

GLW

CRM

TW

C

DIS

C

DTV

AAPL

FB

ACN

AM

ZN

TXN

CSCO

ASM

L

TELEVIS

A

ERIC

BCO

M

LKD

ORCL

LEN

OVO

HO

NH

AI

BSY

QCO

M

ARM

SAP

SM

SG

TSEM

SO

NY

EBAY

CN

ON

EM

C

JN

ET

NFLX

IBM

ZTE

VM

WR

ALCATEL

2

2 Source: Bloomberg (TSR and Consensus Tracker), Dec 2013

DISCOVER. DISRUPT. DELIVER

EPS growth driven by strong revenue growth and margins

23

Revenue

Gro

wth

(%

)

EBIT

Marg

in

Change (

%)

Share

s C

hange &

Rest

* (%

)

*Rest = Changes in Net Income margin vs. EBIT Margin

50% 49% 38% 38% 34% 32% 32% 30% 30% 28% 22% 22% 17% 17% 14% 14% 10% 9% 8% 8% 7% 7% 6% 6% 6% 4% 4% 3% 3% 3% 2% 2% 1% 0% 0% 0%

0% 0% -1% -1% -3% -3% -3% -5% -5% -6% -11% -26%

-76%

LN

KD

FB

BID

U

TCN

T

PCLN

NPN

CRM

NFLX

ASM

L

ARM

DIS

C

DIS

C

SO

NY

AM

ZN

EBAY

QCO

M

VM

WR

WPP

LEN

OVO

GO

OG

GLW

BSY

JN

ET

EM

C

CN

ON

DTV

MSFT

TELEVIS

A

ALCATEL

TXN

VIA

TW

X

ACN

ERIC

SAP

TSEM

AD

BE

ORCL

BCO

M

YH

OO

HP

ZTE

INTC

IBM

CSCO

AAPL

21C F

OX

HO

NH

AI

BBRY

644% 488% 291% 118% 101%

38% 31% 29% 28% 27% 23% 20% 20% 17% 15% 13% 11% 11% 10% 9% 9% 8% 8% 8% 7% 6% 5% 3% 3% 2% 1% 0%

-3% -5% -6% -6% -7% -7% -10% -17% -17% -20% -22% -31% -32% -40% -41% -41%

-315%

BBRY

NFLX

ZTE

LN

KD

SO

NY

FB

VM

WR

TXN

GLW

LEN

OVO

JN

ET

HO

NH

AI

21C F

OX

AM

ZN

TW

X

WPP

ERIC HP

VIA

GO

OG

YH

OO

EBAY

IBM

ARM

SAP

PCLN

CSCO

BCO

M

ACN

EM

C

ORCL

TSEM

QCO

M

CN

ON

ASM

L

TELEVIS

A

BSY

DTV

INTC

TCN

T

NPN

MSFT

AAPL

CRM

AD

BE

BID

U

DIS

C

DIS

C

ALCATEL

153%

38% 36% 36% 21% 16% 16% 15% 8% 8% 7% 7% 6% 6% 6% 5% 5% 5% 5% 4% 3% 3% 3% 2% 2% 1% 1% 1% 0%

0% -2% -5% -5% -5% -5% -5% -6% -7% -8% -14% -17% -20% -22% -26% -29%

-93% -186%

-261% -425%

ALCATEL

YH

OO

DIS

C

DIS

C

NPN

AD

BE

DTV

AAPL

BID

U

MSFT

BSY

ORCL

QCO

M

CN

ON

IBM

TCN

T

INTC

ARM

TELEVIS

A

AM

ZN

ERIC

VIA

ASM

L

HP

HO

NH

AI

ACN

CRM

CSCO

TSEM

TW

X

EM

C

GO

OG

SAP

PCLN

TXN

WPP

JN

ET

LEN

OVO

EBAY

FB

21C F

OX

BCO

M

VM

WR

SO

NY

GLW

LN

KD

NFLX

ZTE

BBRY

DISCOVER, DISRUPT, DELIVER 24

1. The big picture – revenue growth forecasts

2. ICT Hypersector - 2013 TSR performance

3. Growth outlook, sustainability and bundling

4. IT plays a critical role in our transformation

DISCOVER. DISRUPT. DELIVER

Telco: Revenue growth and EBIT growth

25

Telco: Revenue growth and EBIT growth (2015/14 calendar year)

Revenue growth

(2yr vs. 1yr FWD)

EBIT

gro

wth

(2yr

vs.

1yr

FW

D)

*Data as of 22 January 2014

DISCOVER. DISRUPT. DELIVER

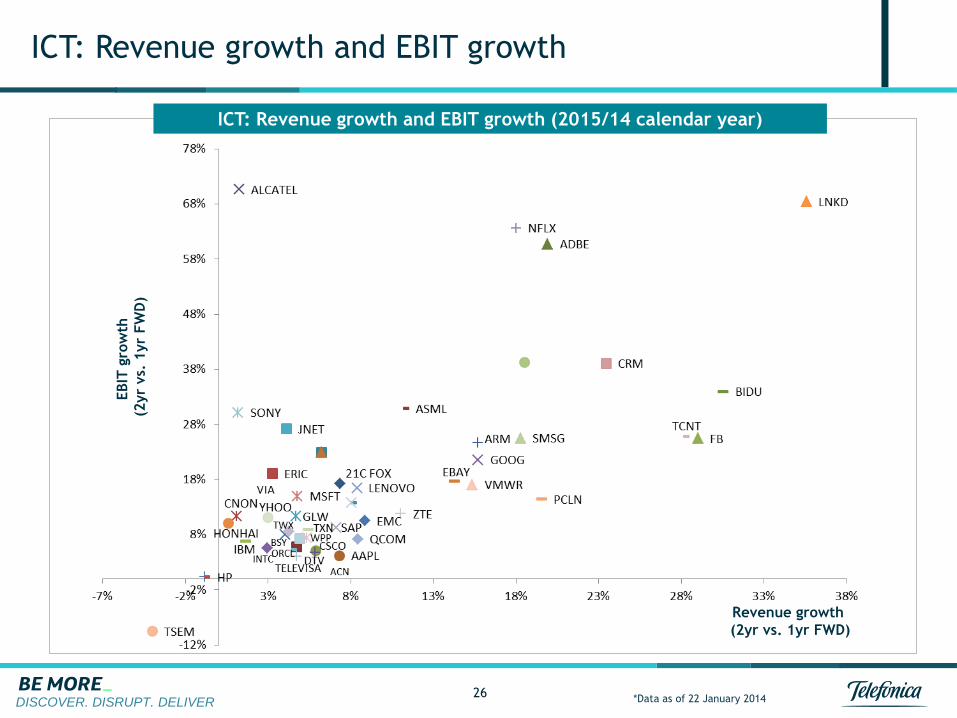

ICT: Revenue growth and EBIT growth

26

ICT: Revenue growth and EBIT growth (2015/14 calendar year)

Revenue growth

(2yr vs. 1yr FWD)

EBIT

gro

wth

(2yr

vs.

1yr

FW

D)

*Data as of 22 January 2014

DISCOVER. DISRUPT. DELIVER

Long term sustainability is critical – AAPL vs. AMZN/GOOG

27

EV / EBITDA

5x

$57.6Bn

32.5

25.1

3Q13

+6% 25.6

3Q13

16.8

3Q13

x%

+20% +17%

Crec. anual ing

x% EBIT %

30%

23%

• iPhone revenues are larger than all of Amazon or Google but they are growing less and there is no certainty about the long term

• What if average prices per unit fall below current $600+ level? What if units sold peak in the future?

Revenues Q4 2013 calendar ($Bn)

2%

EV / EBITDA

24x

EV / EBITDA

13x

EV / OpFCF

6.5x

EV / OpFCF

62x

EV / OpFCF

17x

DISCOVER. DISRUPT. DELIVER

Telcos less profitable and lower growth, same multiples

28

Absolute Valuation

€Bn

Multiples Comparison

Telcos

ICT (ex Telcos)

Telcos

ICT (ex Telcos)

We track the top

100 stocks in the

ICT Hypersector

(50 telcos and 50

from the Internet,

Media and

Technology space).

For full details see

TSR and Consensus

Tracker – ICT

Hypersector (31st

Dec 2013).

1.5x

-0.7x

Net Debt/

EBITDA

32% 23%

17% 6%

16% 17% 9%

14%

x% Margin as % of revenues

1,193

387

201 187 107

1,349

313

80

233 187

Revenues EBITDA CAPEX OpFCF FCF

2,178

1,599

579

2,773 3,006

(233)

EV Market cap Net debt

5.6x

11.7x

6.7%

8.9x

11.9x

6.2%

EV/EBITDA EV/OPFCF FCF YIELD

Big Picture Comparison

€Bn

DISCOVER. DISRUPT. DELIVER

Follow three rules for sustainable exceptional performance

29

Deloitte researched 25,000 listed companies over a 45 year period (1966-2010) and concluded that only 344 (1.4%) generated sustained exceptional performance based on three rules:

Rule #1: Better Before Cheaper Compete on differentiators other than price

Rule #2: Revenue Before Cost Prioritize increasing revenue over reducing costs

Rule #3: Change anything to follow rules 1 and 2

DISCOVER. DISRUPT. DELIVER

Client life time value – bundle connectivity plus services

30

ARPU

£

Churn

(annualized)

Average life

as client

(years)

Total

revenues

(£ per client)

1P 2P 4P

+

Example 3P

B2B

B2C

DISCOVER. DISRUPT. DELIVER

Focus on long term sustainability and superior TSRs

31

Gain revenue market share

with best network

Efficiency improvement

and strict financial discipline

In-market consolidation

Superior total shareholder returns

DISCOVER, DISRUPT, DELIVER 32

1. The big picture – revenue growth forecasts

2. ICT Hypersector - 2013 TSR performance

3. Growth outlook, sustainability and bundling

4. IT plays a critical role in our transformation

DISCOVER, DISRUPT, DELIVER

To be able to respond in this market, Global Telcos need to

overcome their current intrinsic complexity

33

• SLOW in responding to

business needs

• High COST of IT

solutions

• Complex USE OF DATA

and difficulty to obtain

CUSTOMER INSIGHTS

• Difficulty in BEING

DIGITAL

Impact

Drivers of Complexity

IT

• Business imposing

changes to IT but not

considering

implications and

business changes

needed

• Several systems not

convergent with

duplicate applications,

processes and products

per technology/segment

• False conception of

technology changing

web, without

evaluating real

requirements to offer

a multi-channel

experience • Lack of common IT

understanding or

integrity inside the

Operator

• Skills and experience

developed locally as

each local operator has

different processes and

products, avoiding

reutilization

• Product-centric

systems with high

customization to

develop specific

products and

increasing

complexity

• Rapid evolution of the

business and lack of

maturity of IT processes

and technologies

• Incremental changes with

focus on the short term

not considering the long

term vision of business

• Local regulation

imposing

specific products

• Acquisitions of

developed operators

with different systems

and processes

establishing a complex

architectures

panorama

DISCOVER, DISRUPT, DELIVER

Mature industry standards allow for a business led

transformation that will enable significant business benefits

Improve

customer

experience

Out of the box

• Software packaged by

3rd party provider

Full-stack solutions

• Pre-integrated suite of

components

• Best of suite (i.e. covers all

major domains)

Unique data

• Consumer

• Product catalogue

• Inventory

End-to-end processes

• Transform processes

in parallel with

applications

Enabled by standard based

processes (E-TOM),

architecture (TAM) and

information framework (SID) Easy to integrate with

• Loosely coupled (i.e. allows

for substitution of modules

with minimum disruption)

• Web-services/SOA

integration

Non “incremental”

investments

• Freeze legacy expenditure

(i.e. mostly evolutive)

• Fast implementation

minimizes coexistence (i.e.

double maintenance costs)

Enable

business agility

Exploit data

Enable

convergence

Improve and

enable

efficiencies

34

DISCOVER, DISRUPT, DELIVER

Integration will enable seamless interaction with Digital

Services Providers

Standards are a key enabler… … to the homogeneous integration of services

and reusable capabilities in OBs2 (via APIs)

• Common Interface

• Do once, reuse many times

• Faster implementation of new services

(TTM)

• Lower cost of integration with OBs

DSP1 –

Operator

3rd Party

CSP – OB1 CSP – OB2 CSP – OBn . . . .

35

1) DSP: Digital Service Provider; 2) OB: Operating Business

Consistent and

common

integration

surface; from

OBs to digital

service providers

and from digital

service providers

to OBs

Common language, via standards, for the integration of

digital services across the business and within the

supplier environment to ensure consistency of service

and benefits

Simple governance

process that allows

group wide

development and

“in life”

management of the

integration of digital

services

Common interface

with all OBs

© 2013 TM Forum | 37

V2013.4

inform innovate accelerate optimize

How does the digital wave

impact TMForum activities

Laurent Leboucher

TMForum SAS chair

Orange VP APIs and Digital Ecosystems

February 10th

© 2013 TM Forum | 38

V2013.4

The digital economy brings new

opportunities and new challenges …

© 2013 TM Forum | 39

V2013.4

… and will lead

very fast to new roles and

new combinations

© 2013 TM Forum | 40

V2013.4

The digital transformation is at the

core of TMForum programs …

Revenue Management Customer Experience

Management

Agile

Business

Program

Open

Digital

Program

Customer

Engagement

Program

Partner Management Business Process

Optimization

Cloud & Virtualization

IT Transformation

Product Lifecycle Management

Big Data Analytics & Policy Management

Security & Privacy

© 2013 TM Forum | 41

V2013.4

… but it stresses the importance of

the following deliverables for

Framework 14 (this is not exhaustive)

• NFV, SDN: impact on processes, impact on “OSS”

• Digital Services Reference Architecture

• Digital management APIs roadmap (trouble ticket, SLA

management, ordering, product catalog, product lifecycle,

service catalog, billing account, party, …)

• Big Data Analytics: from uses cases to proof of concepts

• CEM index and maturity model

• Digital security and privacy management

• And of course a solid set of frameworks which adresses all

these impacts without overspecifying!

© 2013 TM Forum | 42

V2013.4

To succeed, we need diversity:

CSP+DSP+vendors+adjacent

industries

© 2013 TM Forum | 43

V2013.4

Thank You!

© 2013 TM Forum | 44

V2013.5

DSRA Update Digital Services Reference Architecture

Part of the Open Digital Initiative Project

Eric Troup – Microsoft [email protected]

© 2013 TM Forum | 45

V2013.5

Relationship to Frameworks

Enterprise Management

Strategy, Infrastructure & Product Operations

Fulfillment Assurance Billing &

Revenue

Management

ProductLifecycleManagement

InfrastructureLifecycleManagement

Operations

Support &

Readiness

Customer Relationship Management

Service Management & Operations

Resource Management & Operations

Supplier/Partner Relationship Management

Strategy &

Commit

Marketing & Offer Management

Service Development & Management

Resource Development & Management

Supply Chain Development & Management

(Application, Computing and Network)(Application, Computing and Network)

Enterprise Effectiveness

ManagementKnowledge & Research

Management

Enterprise Risk

Management

Strategic & Enterprise

Planning

Financial & Asset

ManagementStakeholder & External

Relations Management

Human Resources

Management

© 2013 TM Forum | 46

V2013.5

Digital Services are Multi-Cloud

Application Framework (TAM) challenged by

Open Digital Services Ecosystem requirements

© 2013 TM Forum | 47

V2013.5

ETSI NFV Example

San Jose Workshop

• Single Service Provider Centric

• Scenario Specific SDP Functions

One OSS

(Application Framework?)

Single Service Provider Centric

Application Specific

SDP Functions

© 2013 TM Forum | 48

V2013.5

Network Function Virtualization (NFV)?

Should be

Digital Service Function Virtualization (DSFV)

A Common Architecture

for Digital Service Management

NaaS

Network Virtualized CP

Resources

Network Trans/Access

Resources

SaaS

Cloud Virtualized Resources

Network Virtualized Resources

DSRA goal is a common set of reusable service lifecycle management

capabilities for use across virtualized data centers, networks and devices. DSRA

enables many different industry vertical scenarios such as Connected Car, Home,

Media, Healthcare, Government and Energy etc.

Focus

© 2013 TM Forum | 49

V2013.5

Service Enablement Layer or API Exchange Function

Digital Services

Reference Architecture

Development

Service

Deployment

Exposure

Consumption

Implementation

Commerce

Functions

API Broker/Platform (Functional and SMI)

Federated ID & Profile Management, Analytics,

Transaction Management, Events/Notification

Service Catalog Service End Point Catalog

Download /

Utilization

Application Map for the new Open Digital Services Economy

© 2013 TM Forum | 50

V2013.5

DSRA Key Characteristics

Key Pillars 1. Federated Identity &

2. Profile Management

3. Distributed (Multi-Cloud)

Transaction Management.

4. Service Event Notification &

Management

• SMI API

5. Analytics

Key Features 1. Transaction Traceability across Multi-Cloud

2. Eventing

3. Federated Identity / Data Security

4. Runtime Management in Multi-Cloud/Multi-

Tenant

5. Service Broker Model

6. Developer Support

7. Service Composition / Runtime Orchestration

8. Change Sets, Data Driven Architecture

9. End-to-End Analytics

10.Commercial Management of Services /

Partners

11.High Level CxO DSRA Positioning Message

Infrastructure Abstraction / Virtualization

© 2013 TM Forum | 51

V2013.5

Leveraging TOGAF Architecture

Development Model

Catalysts

Member Projects

Industry Initiatives

e.g. NFV (DSFV) Management

© 2013 TM Forum | 52

V2013.5

Need your Help to get this Right

© 2013 TM Forum | 53

V2013.5

Logistics

© 2013 TM Forum | 54

V2013.5

Emergency meeting location

Meeting rooms

Break schedule

Lunch schedule

Daily Agendas

General Sessions

Help and information

IPR statements for meetings

Agenda

© 2013 TM Forum | 55

V2013.5

Event Wi-Fi

Network – Swisscom

User – EVENT/TMFORUM

Password – TMFO3UM

Logistics

The Most Important Information

© 2013 TM Forum | 56

V2013.5

Meeting Location – The Blue Building

directly across the street from the main

hotel entrance.

c/ Padre Damian, 21

Logistics

Emergency

© 2013 TM Forum | 57

V2013.5

Logistics

Meeting Rooms

© 2013 TM Forum | 58

V2013.5

Morning Coffee Break 10:30am – 11:00am

Lunch 12:30pm - 1:30pm

Afternoon Coffee Break 3:00pm – 3:30pm

Logistics

Break Schedule

Activities with prizes at many of the break sessions

© 2013 TM Forum | 59

V2013.5

Coffee

Monday -

Thursday

Logistics

Break Locations

Praga

© 2013 TM Forum | 60

V2013.5

Monday – Thursday in the

upstairs restaurant, Florencia

Friday in Praga

Logistics

Lunch Locations

© 2013 TM Forum | 61

V2013.5

• The Daily Agenda is available at the registration area,

located just outside the main elevators.

• TM Forum staff are always available to help

Logistics

Daily Agendas

Registration

Area

© 2013 TM Forum | 62

V2013.5

Liaison Program on Tuesday

Internet of Things Panel Discussion on Wednesday

evening

Wrap up session on Thursday (reception following)

Future Collaborative Environment and Tools

Logistics

General Sessions

© 2013 TM Forum | 63

V2013.5

Blue shirts

Orange ties

Orange accessories

TM Forum name badges

Logistics

Help and Information

© 2013 TM Forum | 64

V2013.5

Project Meetings

Cross-Project Meetings

Informational Meetings

Logistics

IPR Statements for Meetings

© 2013 TM Forum | 65

V2013.5

Project Meetings

(Open to Project Participants Only)

This meeting is being conducted under the

terms of IPR Mode “xxxx” as defined in the By-

laws Annex 1: Policy on Intellectual Property

Rights. All IPR should be declared.

Logistics

IPR Statements for Meetings

© 2013 TM Forum | 66

V2013.5

Cross-Project Meetings

(Open to Eligible Persons Only, those who are

members of at least one project that is meeting)

This meeting is being conducted under the

terms of IPR Mode RAND as defined in the By-

laws Annex 1: Policy on Intellectual Property

Rights. All IPR should be declared.

Logistics

IPR Statements for Meetings

© 2013 TM Forum | 67

V2013.5

Informational Meetings

(Open Meetings, anyone can attend)

This is an open information meeting in which no

information or materials furnished or provided

by the attendee shall constitute or contain

intellectual property and will not be treated or

protected as such. All attendees understand

and accept this statement.

Logistics

IPR Statements for Meetings

© 2013 TM Forum | 68

V2013.5

Thank You!