supervisory insights: vol. 4, issue 1 - summer 2007 from the director 2 issue at a glance volume 4,...

TRANSCRIPT

Inside

Third-Party Arrangements

Staying Alert to Mortgage Fraud

Wind Hazard Insurance

The e-Exam

Recent DevelopmentsAffecting the Accountingfor Split-Dollar LifeInsurance Arrangements

Supervisory InsightsSupervisory InsightsDevoted to Advancing the Practice of Bank Supervision

Vol. 4, Issue 1 Summer 2007

Supervisory Insights

Supervisory Insights is published by theDivision of Supervision and ConsumerProtection of the Federal DepositInsurance Corporation to promotesound principles and best practicesfor bank supervision.

Sheila C. BairChairman, FDIC

Sandra L. ThompsonDirector, Division of Supervision andConsumer Protection

Journal Executive Board

George French, Deputy Director andExecutive Editor

Christopher J. Spoth, Senior DeputyDirector

John M. Lane, Deputy DirectorRobert W. Mooney, Acting Deputy

DirectorWilliam A. Stark, Deputy DirectorJohn F. Carter, Regional DirectorDoreen R. Eberley, Regional DirectorStan R. Ivie, Regional DirectorJames D. LaPierre, Regional DirectorSylvia H. Plunkett, Regional DirectorMark S. Schmidt, Regional Director

Journal Staff

Bobbie Jean NorrisManaging Editor

Christy C. JacobsFinancial Writer

Eloy A. VillafrancaFinancial Writer

Supervisory Insights is availableonline by visiting the FDIC’s website atwww.fdic.gov. To provide comments orsuggestions for future articles, to requestpermission to reprint individual articles,or to request print copies, send an e-mailto [email protected].

Letter from the Director......................................................... 2

Issue at a Glance

Volume 4, Issue 1 Summer 2007

Regular Features

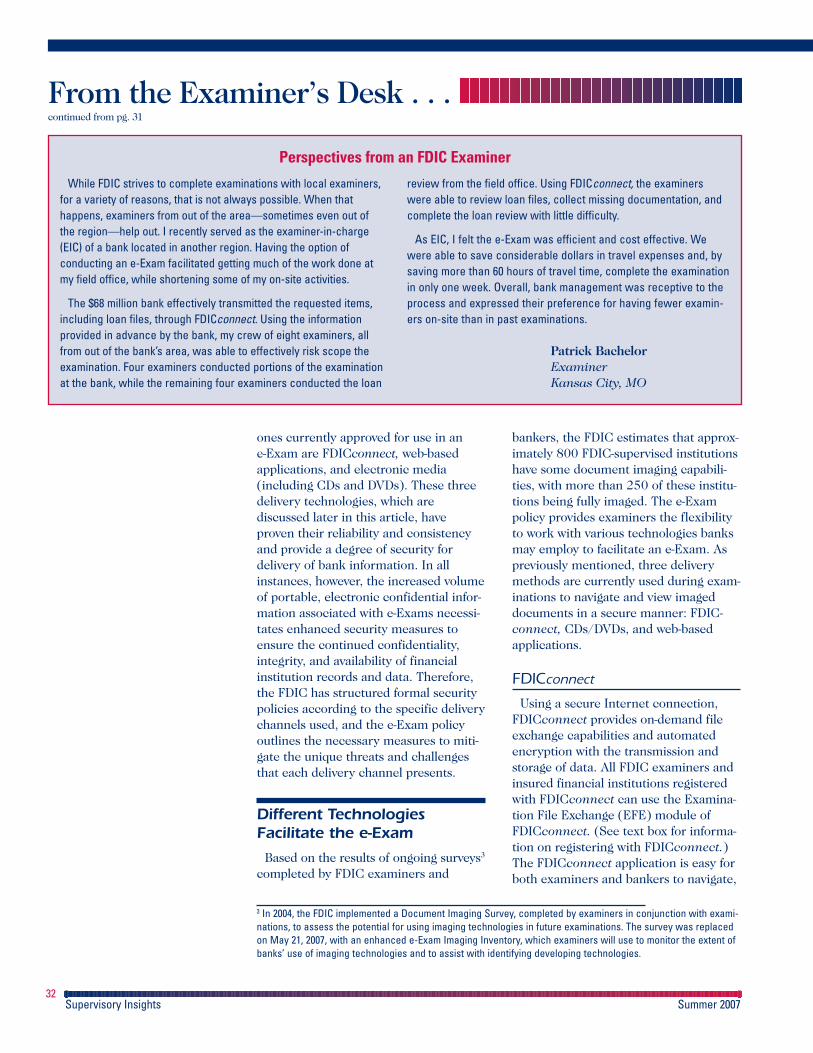

From the Examiner’s Desk . . . The e-Exam 30An e-Exam, or electronic examination, isa financial institution examination inwhich electronic data are exchangedthrough a secure delivery method, thusimproving examination efficiencies forboth banks and examiners. Banks gener-ally maintain a wide variety of informa-tion—written policies and procedures,customer disclosures, board minutes,and even loan files—in electronic format.This article discusses the FDIC’s e-Exampolicy and the impact that being able toexchange documents electronically ishaving on examinations.

Accounting News: Recent Developments Affecting the Accounting for Split-Dollar Life Insurance Arrangements 35Over the past year, the FinancialAccounting Standards Board’s EmergingIssues Task Force has addressed theaccounting for endorsement and collat-eral assignment split-dollar life insurancearrangements under which employersand employees share the rights to thecash surrender value and death benefitsof insurance policies. The consensusesreached by the Task Force will changehow many banks have accounted fortheir existing split-dollar arrangementsand will require them to recognize aliability at the beginning of 2008. Thisarticle discusses the principal elementsof this recent accounting guidance andits effect on banks’ capital and futureearnings.

Regulatory and Supervisory Roundup 42This feature provides an overview ofrecently released regulations and super-visory guidance.

Articles

Third-Party Arrangements: Elevating Risk Awareness 4Many community banks provide products and servicesthrough arrangements with third parties. Appropriatelymanaged third-party relationships can enhance competitive-ness, provide diversification, and ultimately strengthen thesafety and soundness of insured institutions. Third-partyarrangements can also help institutions attain key strategicobjectives. But third-party arrangements also present risks. Inthis article, we show how failure to manage these risks canexpose a financial institution to everything from financial lossto regulatory action and loss of customer relationships.

Staying Alert to Mortgage Fraud 12The Federal Bureau of Investigation reports having more thanone thousand pending mortgage fraud investigations, withover half involving financial institutions as victims. However,they estimate the actual number of mortgage fraud cases tobe closer to 36,000. This article discusses the housing boomof the early 2000s and how the resultant demand led toincreases in mortgage fraud activity. The authors share exam-ples from FDIC examiners and offer fundamental mitigationsteps as well as links to other resources.

Wind Hazard Insurance: No Longer Just a Technical Exception 22Hazard insurance has played a big role in mitigating the risk ofloss of collateral value from catastrophic damage. Examinershave traditionally cited inadequacies in collateral insurancecoverage as technical exceptions when reviewing loan files.But in the current environment, potentially widespread issuesregarding insurance availability and affordability could result inconsequences reaching beyond anything considered techni-cal. This article explores the impact of the rising costs (and insome cases, the lack of availability) of wind hazard insurance,with a focus on Florida.

1Supervisory Insights Summer 2007

Letter from the Director

2Supervisory Insights Summer 2007

The risk management examinationand the compliance examinationhave long been regarded as sepa-

rate disciplines. These examinationshave traditionally been performed byseparate teams of examiners, and eachdiscipline had its own specialized train-ing and a somewhat distinctive set ofexamination objectives. More recently,as the volume and variety of new bankproducts and services have evolved, anexus between consumer protectionand risk management in certain typesof situations has become increasinglyapparent. What once were perceived asstrictly compliance issues or strictly riskmanagement issues now are understoodto share many common risk attributes.For example, abusive or predatory lend-ing practices raise both asset quality andmanagement considerations for riskmanagement examiners, and also raiseserious concerns on the compliance sideabout adherence to consumer protectionlaws and regulations. Cooperation andcollaboration between the examinationdisciplines will be more important thanever as we strive to address these risksand maintain supervisory vigilance.

The FDIC has taken several steps toachieve greater synergy between thedisciplines. We created Joint Examina-tion Teams (JETs) made up of compli-ance and risk management examinerswho work together on financial institu-tion examinations to identify risks andcollaboratively apply supervisory strate-gies. We have revised the assistantexaminer training program to ensure amultidiscipline approach to training anddeveloping examination staff, and weencourage all examiners to pursue inter-and cross-divisional training. This sharedapproach is needed to address bothcompliance and safety and soundnessissues arising in the banking industry.High-risk products, including certaintypes of subprime and nontraditionalloans, and issues such as overdraftprotection programs, third-partyarrangements, and identity theft all

have risk management and consumerprotection components that necessitate acoordinated supervisory response. Betterconsumer education, along with clearand accurate disclosures and marketingmaterials, might have prevented some ofthe problems we are seeing today.

In response to emerging issues in themortgage industry, the FDIC and theother federal financial institution regula-tory agencies (the agencies) issued Inter-agency Guidance on NontraditionalMortgage Product Risks in September2006. The publication addresses recentregulatory concerns with interest-onlyand payment-option adjustable rate mort-gages (ARMs). In addition, in March ofthis year, the agencies and the NationalCredit Union Administration issued anInteragency Proposed Statement onSubprime Lending. This Statementproposes two clear guidelines for lenders:approve loans based on the borrower’sability to repay at the fully indexed rate,and provide borrowers with clear andaccurate information to help themunderstand the transaction. These guide-lines build on basic and long-standingconsumer protection and risk manage-ment principles. We look forward toreviewing and considering all commentsreceived on this Statement.

Problems in the subprime lendingmarket also highlight the importance ofproper due diligence when entering intothird-party arrangements. In this issue,“Third-Party Arrangements: Elevat-ing Risk Awareness” addresses boththe benefits and potential risks associ-ated with third-party agreements andoffers some best practices for avoidingthe financial losses and reputation risksthat can result from poorly managedthird-party arrangements. The articlealso highlights how, as third-partyarrangements become more prevalentin all institutions, they present a broadspectrum of risks crossing all examina-tion disciplines—risk management,compliance, trust, and informationtechnology. As the examples in the arti-

cle point out, the risks in many of theserelationships (such as information tech-nology or merchant processing) are wellknown, but others are often overlooked.Inadequate management and control ofthird-party risks can result in a signifi-cant financial impact on an institution,including legal costs, credit losses,increased operating costs, and loss ofbusiness. The problems highlighted inthe article might have been avoided ifthe institutions had conducted thoroughrisk assessments, conducted proper duediligence on the parties with whom theywere partnering, thoroughly reviewedcontracts, and ensured that the third-party product or service meshed withthe institution’s goals and business planand that those products or serviceswere consistent with applicable supervi-sory policies. Examiners from all disci-plines will continue to review banks’third-party arrangements to ensure thatfinancial institutions understand andmitigate the potential risks.

Ineffective due diligence by financialinstitutions can have another unfortunateconsequence: an increase in mortgage-related fraud. The explosive growth inmortgage lending over the past severalyears and competitive pressures onlenders to relax underwriting standardscreated a situation that was ripe foropportunists. “Staying Alert to Mort-gage Fraud” discusses this increasingproblem, explores common types ofmortgage fraud, and provides some miti-gating steps banks can take. The exam-ples in the article demonstrate how a fewsimple, fundamental risk managementpractices by lenders might have signifi-cantly reduced fraud-related losses:monitoring concentration risks, provid-ing training and oversight, establishingclear lending and quality control guide-lines, and conducting due diligence whendealing with third parties or new employ-ees, among others.

The devastating effects of the 2004 and2005 hurricane seasons highlighted theimportance of flood insurance in protect-

ing real estate collateral values. As theUnited States gears up for the 2007hurricane season, coastal communitiesare dealing with a new crisis in the insur-ance area: the rising cost and scarcity ofproperty insurance coverage. “WindHazard Insurance: No Longer Just aTechnical Exception” explores theissues arising from the reduced availabil-ity of wind hazard insurance coverage,including the impact on borrowers’ cashflow and the larger economic impact inaffected communities, particularly inFlorida. Underinsured or uninsuredcollateral, declining collateral values, anddeclining debt service coverage exposelenders to more risk of default and loss.At the FDIC, community and consumeraffairs staffs are working to educateconsumers about this issue, while riskmanagement examiners are reemphasiz-ing the importance of insurance cover-age in the overall assessment of loanquality. Bankers, in turn, must ensurethat lending policies and loan agree-ments address insurance requirements,make reasonable efforts to maintainsufficient insurance coverage on collat-eral, and consider the increasing cost ofwind hazard insurance when assessingrepayment capacity.

Also in this issue are our two regularfeatures. “From the Examiner’s Desk”discusses how the FDIC’s e-Exam policyis improving examination efficiencies,while “Accounting News” addressesrecent developments affecting theaccounting for split-dollar life insurancearrangements.�

We encourage our readers to continueto provide comments on articles, to askfollow-up questions, and to suggest topicsfor future issues. All comments, ques-tions, and suggestions should be sent [email protected].

Sandra L. ThompsonDirectorDivision of Supervision andConsumer Protection

3Supervisory Insights Summer 2007

Third-Party Arrangements:Elevating Risk Awareness

4Supervisory Insights Summer 2007

find security breakdowns that presentboth compliance and safety and sound-ness issues.

The purpose of this article is toheighten banker and examiner aware-ness of third-party risks and the effectthese risks can have on financial insti-tutions and the consumers they serve.Through examples drawn from actualexaminer experiences, the authorsprovide some insights on identifyingand managing third-party risk and howexaminers assess third-party arrange-ments. The authors also provide a listof additional resources for furtherinformation.

“Third Party” Defined

For purposes of this article, “thirdparty” is broadly defined to include anyentity that has entered into a businessrelationship with an insured depositoryinstitution. Often, these third parties aredeeply involved in the delivery of finan-cial services to the consumer. The thirdparty may be positioned, directly or indi-rectly, between the financial institutionand its customers or otherwise haveunfettered access to the institution’scustomers. Consequently, the quality ofthat third party’s performance is criti-cally important to the financial institu-tion’s long term success. A third partycan be a bank or a nonbank, affiliated ornot affiliated, regulated or nonregulated,domestic or foreign.

The scope of the definition of thirdparty is expansive by necessity. Withinthe banking industry, third-party relation-ships are pervasive. Financial institutionsuse third parties to

n Perform functions on their behalf;

n Facilitate customer access to the prod-ucts and services of third-partyproviders; and

Community banks increasinglyprovide products and servicesthrough arrangements with third

parties. Appropriately managed third-party relationships can enhance competi-tiveness, provide diversification, andultimately strengthen the safety andsoundness of insured institutions. Third-party arrangements can also help institu-tions attain key strategic objectives. Butthird-party arrangements also presentrisks. Failure to manage these risks canexpose a financial institution to regula-tory action, financial loss, litigation, andreputational damage, and may evenimpair the institution’s ability to estab-lish new or service existing customerrelationships. Successful third-party rela-tionships, therefore, start with financialinstitutions recognizing those risks andimplementing an effective risk manage-ment strategy.

The FDIC routinely assesses third-partyarrangements. The FDIC is concernedwhen an arrangement unduly heightensthe risk to an insured depository institu-tion or has potential adverse effects forconsumers. The risks cross all examina-tion disciplines and necessitate closecommunication among examinationteams to thoroughly understand therisk presented by a bank’s particularthird-party arrangements. For example,compliance examiners may find legalproblems with how a third party ismanaging a credit card operation.Those legal problems could result insubstantial liability for the bank thatcould, in turn, affect its capital position.Conversely, risk management examinersreviewing suspicious activity reportsfiled by the institution about third-partymortgage brokers may find informationabout potentially unfair or deceptivepractices that compliance examinersshould review. Information technologyexaminers who review the operationof a third-party service provider may

5

n Increase revenue by allowing thirdparties to conduct business on behalfof the financial institution by usingthe institution’s name on the thirdparties’ products and services.

The Risks Are Familiar . . .Sometimes

Third-party risk is not a simple, easilyidentifiable risk attribute, but rather acombination of risks ranging from thefamiliar to the highly complex. Third-party risk can vary greatly, dependingon each individual third-party arrange-ment. The risks are more widely recog-nized in certain arrangements, such asinformation technology and merchantprocessing. However, in many otherarrangements, the risks can seem moreinnocuous—sometimes leading to criti-cal gaps in bank management’s plan-ning and oversight of third-partyarrangements.

Some of the risks are associated withthe underlying activity itself—similar tothe risks faced by an institution directlyconducting the activity. Other potentialrisks arise from or are heightened by theinvolvement of a third party. Significantor more complex third-party arrange-ments will have identifiable risk attrib-utes falling into the following broadcategories.

Strategic risk includes the risk arisingfrom ill-advised business decisions orthe failure to implement appropriatebusiness decisions in a manner consis-tent with an institution’s strategic plan-ning objectives. The use of a third partyto perform banking functions or offerproducts or services that do not helpthe financial institution achieve corpo-rate strategic goals presents an obviousstrategic risk. Third-party arrangementsthat do not provide a return commen-surate with the level of risk assumedexpose the financial institution tostrategic risk.

Reputation risk is the risk arising fromnegative public opinion. Dissatisfiedcustomers, breaches of an institution’spolicies or standards, and violations oflaw can potentially harm the reputationof a financial institution in the commu-nity it serves. Negative publicity involvingthe third party, even if it is not related tothe specific third-party arrangement,presents reputation risk to a financialinstitution.

Transaction risk is the risk arisingfrom problems with customer service orproduct delivery. A third party’s failureto perform as expected by the financialinstitution or by customers—because ofinadequate capacity, technological fail-ure, human error, or fraud—exposes theinstitution to transaction risk. Inade-quate business resumption or otherappropriate contingency plans alsoincrease transaction risk. Weak controlover information technology couldresult in the inability to transact busi-ness as expected, unauthorized transac-tions, or breaches of data security.

Credit risk is the risk that a thirdparty, or any other creditor necessaryto the third-party relationship, is unableto meet the terms of the contractualarrangements with the financial institu-tion or to otherwise financially performas agreed. The basic form of credit riskinvolves the financial condition of thethird party itself. Some contracts withthird parties provide assurance of somemeasure of performance relating to theunderlying obligations arising from therelationship, such as loan originationprograms. Whenever indemnificationor any type of guarantee is involved,the financial condition of the thirdparty is a factor in assessing credit risk.Credit risk to the institution can alsoarise from arrangements where thirdparties market or originate loans,solicit and refer customers, or analyzecredit. Appropriate monitoring of third-party activities is necessary to ensure

Supervisory Insights Summer 2007

predictable results. Institutions often“buy” the types of loans they cannotoriginate in their normal trade area;however, those institutions may lacklenders with sufficient expertise toanalyze the participation loan. At othertimes, a financial institution’s manage-ment may wish, in hindsight, that theyhad known more—not only about theborrowers, but also about the thirdparty with whom they did business.Purchased loans, especially those fromoutside a financial institution’s lendingarea, present the opportunity formisrepresentation or fraud. In additionto strategic and due-diligence issues,there are a multitude of risks specific toany given transaction.

Addressing the Risks. Institutionsentering into participation arrangementscan avoid common pitfalls and mitigatethird-party risks by

n Conducting a thorough risk assess-ment. Ensure that the proposed rela-tionship is consistent with theinstitution’s strategic plan and overallbusiness strategy;

n Conducting a thorough due dili-gence. Focus on the third party’sfinancial condition, relevant experi-ence, reputation, and the scope andeffectiveness of its operations andcontrols;

n Reviewing all contracts. Ensure thatthe specific expectations and obliga-tions of both the bank and the thirdparty are outlined and formalized;

n Reviewing applicable accountingguidance. Determine if the participa-tion agreement meets the criteria fora loan sale or a secured borrowing.Key issues to consider include rightsto repurchase and recourse arrange-ments. In some cases, participationloans meet applicable sales criteria,but warrant consideration under risk-based capital standards; and

n Developing a comprehensive monitor-ing program. Periodically verify that

that credit risk is understood andremains within established limits.

Compliance risk is the risk arising fromviolations of laws, rules, or regulations,or from noncompliance with internalpolicies or procedures or with the institu-tion’s business standards. Activities of athird party that are not consistent withlaw, policies, or ethical standards exposefinancial institutions to compliance risk.This risk is exacerbated by inadequateoversight or a weak audit function. Athird party’s failure to appropriatelymaintain the privacy of customer recordswill also create undue risk.

Other risks. Third-party relationshipsmay also subject financial institutions toa variety of unique risks: liquidity, inter-est rate, price, foreign currency transla-tion, and country risks, among others. Acomprehensive list of other types of riskthat arise from an institution’s decisionto enter into a third-party relationship isnot possible without a complete under-standing of the arrangement.

Don’t Neglect the Basics

A simple participation loan is a verycommon third-party arrangement andprovides a good introduction to ourexamples of third-party risk. The par-ticipating financial institution (orpurchaser) does not underwrite theloan, and the borrower does notdirectly interact with the institution.A third party, perhaps not even aninsured financial institution, assumesmany critical functions in the under-writing and servicing processes. In thevast majority of participation loans, theoutcome is as expected: the borrowerpays as agreed and the arrangement isprofitable for the bank. However, themyriad things that can go wrong high-light the basics of third-party risk.

Examiners sometimes find that aparticipation loan does not meet thefinancial institution’s established under-writing standards, too often with

6

Third-Party Arrangementscontinued from pg. 5

Supervisory Insights Summer 2007

7

the third party is abiding by the termsof the contractual agreement and thatidentified risks are appropriatelycontrolled.

As demonstrated in the examplesdiscussed below, these key steps—riskassessment, due diligence, contractreview, and oversight—are the basicelements of an effective third-party riskmanagement process, regardless of thetype of activity carried out by the thirdparty.

Beyond Credit Risk

Financial institutions sometimes focusalmost exclusively on credit risk andoverlook the potential for other risks. Inone case, an institution decided to enterthe credit card market by partneringwith an entity that purported to special-ize in marketing and processing creditcards. These credit cards, which werepromoted as a product that providedcustomers with “benefits” and “satisfac-tion,” were also marketed as a means ofbuilding or rebuilding a consumer’scredit rating.

According to the agreement with thethird party, the financial institutionwould underwrite and originate creditcards under its own name and immedi-ately sell any related receivables to thethird party. In return, the institutionwould receive a small amount everymonth for each outstanding card. If anindividual cardholder was able to makethe required payments in a timelymanner, he or she could earn a refundof some, or all, of the origination fee.However, the program was structured sothat only a small percentage of cardhold-ers would ever use the card in a tradi-tional manner. More often than not, thesmall credit line was completelyconsumed by fees at origination, leaving

the cardholder with no available creditupon receipt of the card.

Examiners took exception to theproduct being marketed as a credit-building instrument because the institu-tion was unable to provide substantiveevidence that consumers’ credit profilesactually improved by using the creditcard. Examiners were also concernedthat the card had minimal usefulnessfrom the outset because of the highinitial fees. Despite the claims of “satis-faction,” a significant portion of card-holders canceled their credit cardswithin three to six months of issuance.The institution was found to be inviolation of Section 5 of the FederalTrade Commission Act (relating tounfair and deceptive acts or practices),1

was required to make customer reim-bursements, and suffered damage toits reputation.

The Importance of Effective RiskIdentification. There are numerousrisks that may arise from an institution’suse of third parties. In this case, the insti-tution was focused on credit risk ratherthan on compliance and reputation risk.As part of the risk assessment process,management should analyze the poten-tial risks associated with the third partyand the proposed activity. In retrospect,the financial institution could have miti-gated many of the risks resulting fromthis arrangement by

n Conducting a thorough risk assess-ment;

n Making certain promotional materi-als were well-supported and notmisleading;

n Reviewing the third party’s previousexperience with the product as wellas monitoring results of the third-party arrangement, including records

Supervisory Insights Summer 2007

1 The Winter 2006 issue of Supervisory Insights contains a thorough discussion of Section 5 of the Federal TradeCommission Act (unfair or deceptive practices affecting commerce) and cites situations similar to this example.See “Chasing the Asterisk: A Field Guide to Caveats, Exceptions, Material Misrepresentations, and Other Unfairor Deceptive Acts or Practices,” Supervisory Insights, Vol. 3, Issue 2, Winter 2006, www.fdic.gov/regulations/examinations/supervisory/insights/siwin06/index.html.

8

of those customers who canceledtheir cards within a few months ofissuance; and

n Reviewing the product for compliancewith governing laws and regulations.

Costly Lessons fromUnsupervised Outsourcing

Institutions often use third parties, suchas mortgage brokers, to generate mort-gage loans. In such cases, financial insti-tutions are expected to ensure that therisk management processes for loanspurchased from or originated throughthird parties are consistent with applica-ble supervisory policies.

An examination of an institution wellversed in mortgage lending revealedsubstantial problems related to itsmortgage broker network. Productofferings by both the institution andits third-party mortgage brokers hadrapidly evolved and expanded. To meetgrowing demand, the institution shiftedits product and delivery channel strate-gies. In only a brief period of time, theinstitution’s broker network expandedsignificantly.

At the same time, the institution’sdue diligence process for brokers wasrelaxed. The institution’s financialstandards for the third-party mortgagebrokers it used quickly became moreliberal than the institution’s lendingstandards. Simple background checks,costing only a few dollars, were fore-gone for the sake of expediency.Monitoring processes were lax. Thelending-volume threshold to triggercloser reviews of loan quality was setso high that practically no brokers wereever subject to the reviews. Underwrit-ing standards were also relaxed. Ineffect, the institution became relianton the brokers to protect its financialinterest and reputation. Further,

management reporting was cumber-some and incomplete. While the insti-tution used a watch list, essentiallybrokers were placed on the list onlyif suspicious activity (i.e., fraud) wasactually reported to federal authoritiesor if specific misconduct was identified.Even when a watch designation wasassigned, the institution’s systemsallowed for continued funding withoutfurther review. Unfortunately, but notsurprisingly, the institution recognizedthese inadequacies only after creditlosses increased substantially.

No Substitute for Due Diligence andOversight. Problems arise not from theabsolute volume of relationships, butfrom the quality of the risk manage-ment processes employed. In thisexample, controls over the networkwere perfunctory at best. The institu-tion appeared to have a process but,in practice, the process controlled verylittle. The institution could have miti-gated the risks discussed as well as theresulting impact on the institution by

n Exercising appropriate due diligenceprior to entering into a third-partyrelationship and providing ongoing,effective oversight and controls;

n Conforming to supervisory standards,including those reiterated in theSeptember 2006 Interagency Guid-ance on Nontraditional MortgageProduct Risks;2 and

n Monitoring loan originations to ensurethat loans met the institution’s lend-ing standards and were in compliancewith applicable laws and regulations.

Hitting the Bottom Line

One financial institution outsourcedmuch of the development and adminis-tration of a new credit product for itscustomers. However, the third party was

Supervisory Insights Summer 2007

2 FIL-89-2006, Guidance on Nontraditional Mortgage Product Risks, and Addendum to Credit Risk ManagementGuidance for Home Equity Lending, October 5, 2006, www.fdic.gov/news/news/financial/2006/fil06089.html.

Third-Party Arrangementscontinued from pg. 7

9

not fully aware of the various requireddisclosures or the annual percentage rate(APR) and finance charge calculationsnecessary for compliance with the Truthin Lending Act. As a result, customersreceived disclosure statements thatsignificantly understated the financecharges related to the product.

The institution had already beencautioned by examiners to review newproducts carefully, as a result of duediligence inadequacies identified in pastexaminations. Despite these cautions,bank management did not invest suffi-cient resources to ensure a successfulnew product offered through the thirdparty. Examiners discovered the inaccu-rate disclosure shortly after productlaunch. The institution suspended theproduct but not until numerous loanswith faulty disclosures had been origi-nated. The amount of reimbursementsto customers was significant, along withthe expense and embarrassment thatcame with rectifying the mistake. Hadthe problem not been identified early,the reimbursements required could haveeasily reached an amount large enoughto jeopardize the capital accounts of thefinancial institution.

Unidentified Risks Can Be Costly.Following an assessment of risks and adecision to proceed with a new productline developed and administered by athird party, the institution’s managementmust carefully select a qualified entity toimplement the program. Due diligenceshould be performed not only prior toselecting a third party, but also periodi-cally during the course of the relation-ship. In this example, the institutioncould have mitigated the risks discussedas well as the resulting impact on theinstitution by

n Conducting a comprehensive duediligence that involved a review of allavailable information, including thethird party’s qualifications and experi-ence with the product; and

n Monitoring the third party’s activitiesto make sure the products producedwere in compliance with existing laws,rules, and regulations, as well as theinstitution’s internal policies, proce-dures, and business standards.

A Supervisory Perspective

Before engaging in any third-partyarrangement, a financial institutionshould ensure that the proposed activi-ties are consistent with the institution’soverall business strategy and risk toler-ances, and that all involved parties haveproperly acknowledged and addressedcritical business risk issues. These issuesinclude the costs associated with attract-ing and retaining qualified personnel,investments in the technology poten-tially needed to monitor and managethe intended activities, and the estab-lishment of appropriate feedback andcontrol systems. If the activity involvesconsumer products and services, theboard and management should establisha clear solicitation and origination strat-egy that allows for after-the-fact assess-ment of performance, as well asmid-course corrections.

Proper due diligence should beperformed prior to contracting with athird-party vendor and on an ongoingbasis thereafter. Management shouldensure that exposures from third-partypractices or financial instability areminimized. Negotiated contracts shouldprovide the institution with the ability tocontrol and monitor third-party activities(e.g., growth restrictions, underwritingguidelines, outside audits) and discon-tinue relationships that do not meet highquality standards.

Reputation, compliance, and legalrisks are dependent, in part, upon theintended activities as well as the publicperception of both the financial institu-tion’s and the third party’s practices.Therefore, careful review is warranted,

Supervisory Insights Summer 2007

10

and an adequate compliance manage-ment program is critical. In some cases,an institution may need processes inplace to handle potential legal action.In any case, management should estab-lish systems to monitor consumercomplaints and ensure appropriateaction is taken to resolve legitimatedisputes.

Finally, an institution’s audit scopeshould provide for comprehensive, inde-pendent reviews of third-party arrange-ments as well as the underlying activities.Findings should be provided to the finan-cial institution’s board of directors andexceptions should be immediatelyaddressed.3

A financial institution’s board ofdirectors and senior management areultimately responsible for identifyingand controlling risks arising from third-party relationships. The financial insti-tution’s responsibility is no differentthan if the activity was handled directlyby the institution. In fact, as the exam-ples in this article illustrate, greatercare may be necessary depending onthe risks inherent in the third-partyarrangement.

FDIC examiners assess how financialinstitutions manage their significantthird-party relationships. Trust,consumer protection, informationtechnology, and safety and soundnessexaminations all include reviews ofthird-party arrangements. Examinersreview bank management’s record ofand process for assessing, measuring,monitoring, and controlling risks asso-ciated with significant third-partyrelationships. The depth of the exami-nation review depends on the scope ofactivity conducted through or by thethird party and the degree of risk asso-ciated with the activity and the rela-

tionship. The FDIC considers theresults of the review in its overall evalu-ation of management and its ability toeffectively control risk. The use ofthird parties can have a significanteffect on other key aspects of perfor-mance, such as earnings, asset quality,liquidity, rate sensitivity, and the insti-tution’s ability to comply with laws andregulations.

FDIC examiners address findings andrecommendations relating to an institu-tion’s third-party relationships in theReport of Examination and within theongoing supervisory process. Appropri-ate corrective actions, including enforce-ment actions, may be pursued fordeficiencies related to a third-party rela-tionship that pose significant safety andsoundness concerns or result in viola-tions of applicable federal or state lawsor regulations.

Conclusion

Bankers and examiners alike deal withthird-party arrangements on a regularbasis. Third-party arrangements canhelp financial institutions attain strate-gic objectives by increasing revenue orreducing costs and can facilitate accessto needed expertise or efficiencies relat-ing to a particular activity. However,inadequate management and control ofthird-party risks can result in a signifi-cant financial impact on an institution,including legal costs, credit losses,increased operating costs, and loss ofbusiness.

As illustrated in the preceding exam-ples, the risks inherent in third-partyarrangements are not significantlydifferent from other risks financialinstitutions face. In fact, the risks areoften the same—the difference is whereto look for them. Likewise, the frame-

Supervisory Insights Summer 2007

3 From the FDIC’s Risk Management Manual of Examination Policies, www.fdic.gov/regulations/safety/manual/index.html.

Third-Party Arrangementscontinued from pg. 9

11

work for risk management is verysimilar. Risks should be identified,activities managed and controlled,information monitored, and processesperiodically audited. Identified weak-nesses should be documented andpromptly addressed. As with any otherundertaking by a financial institution,poor strategic planning, inadequatedue diligence, insufficient manage-ment oversight, and a weak internalcontrol environment are commonelements in problem situations. Simi-larly, the primary element for successis effective management.

Kevin W. HodsonField Supervisor (RiskManagement),Des Moines, IA

Todd L. HendricksonField Supervisor(Compliance),Fargo, ND

Acknowledgments: The authors wishto acknowledge the assistance of FieldSupervisors Brent J. Klanderud (RiskManagement), Omaha, NE, andRandy S. Rock (Risk Management),Sioux Falls, SD, in developing thisarticle. Messrs. Klanderud and Rock,along with the authors, recently ledan Examiner Forum, an internal semi-nar for FDIC examiners in the FDIC’sRisk Analysis Center, on the topic ofthird-party risk. The authors are alsograteful for the encouragement andassistance provided by Mira Marshall,Senior Policy Analyst, CompliancePolicy Section, Washington Office;Kenyon Kilber, Senior ExaminationSpecialist, and Suzy Gardner, Exami-nation Specialist, Planning andProgram Development Section, Wash-ington Office; and the talented exam-iners who identified the situationscited as examples in this article.

Supervisory Insights Summer 2007

List of Resources:FDIC Risk Management Manual of Exami-

nation Policies, Related Organizations,Section 4.3, “Examination and Investiga-tion of Unaffiliated Third Parties,”www.fdic.gov/regulations/safety/manual/section4-3.html.

FDIC Risk Management Manual of Exami-nation Policies, Loans, Section 3.2,“Subprime Lending,” www.fdic.gov/regulations/safety/manual/section3-2.html#subprime.

FIL-89-2006, Guidance on NontraditionalMortgage Product Risks, and Addendumto Credit Risk Management Guidance forHome Equity Lending, October 5, 2006,www.fdic.gov/news/news/financial/2006/fil06089.html.

FDIC Compliance Examination Handbook,“Compliance Examinations,” Sections II,V, VII, and IX, www.fdic.gov/regulations/compliance/handbook/html/index.html.

FIL-52-2006, Foreign-Based Third-PartyService Providers: Guidance on ManagingRisks in These Outsourcing Relationships,June 21, 2006, www.fdic.gov/news/news/financial/2006/fil06052.html.

OCC Bulletin 2001-47, Third Party Relation-ships: Risk Management Principles,November 1, 2001, www.occ.treas.gov/ftp/bulletin/2001-47.doc.

OCC Advisory Letter 2000-9, Third PartyRisk, August 29, 2000, www.occ.treas.gov/ftp/advisory/2000-9.doc.

Thrift Bulletin 82a, Third Party Arrange-ments, September 1, 2004,www.ots.treas.gov/docs/8/84272.pdf.

Federal Financial Institutions ExaminationCouncil Information Security IT Exami-nation Handbook, July 2006, Appendix A:“Examination Procedures,” www.ffiec.gov/ffiecinfobase/booklets/information_security/information_security.pdf.

12

The housing boom of the early2000s affected many areas of theUnited States, as consumers and

investors took advantage of low interestrates to purchase, upgrade, and investin houses and condominiums. Theentry, and general acceptance, ofnumerous nontraditional mortgageloan products into the financial land-scape also bolstered many people’sgoal of achieving home ownership.The nontraditional products facilitatedan increase in the dollar amount ofmortgages individuals financed, whichhelped spur housing demand. As thisdemand increased, so did price appre-ciation, and the purchase of a housebecame more than just a home formany individuals: residential real estatebecame the new “golden egg.”

Historically, a mortgage transactioninvolved two parties: the lender andborrower. Borrowers conducted theirbusiness across a desk at a local bank,and the only other people involved in theprocess were bank employees (or individ-uals closely associated with the bank).Today, a single mortgage transaction caninvolve a wide number of independentparties who may never meet the borroweror the lender. In addition, the pressure toclose a loan quickly is paramount, as fast-paced consumers look for more conven-ience and less hassle. Unscrupulousindividuals are increasingly manipulatingthese types of circumstances to theiradvantage, resulting in a significant andgrowing mortgage fraud problemthroughout the country.

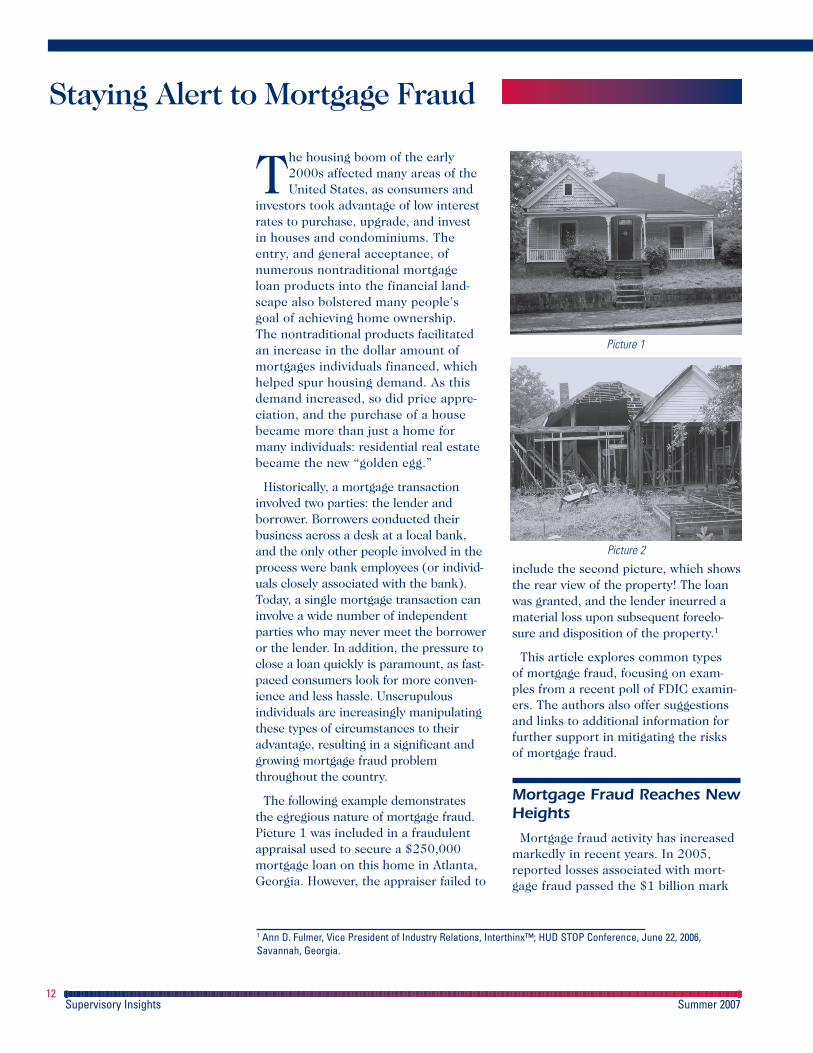

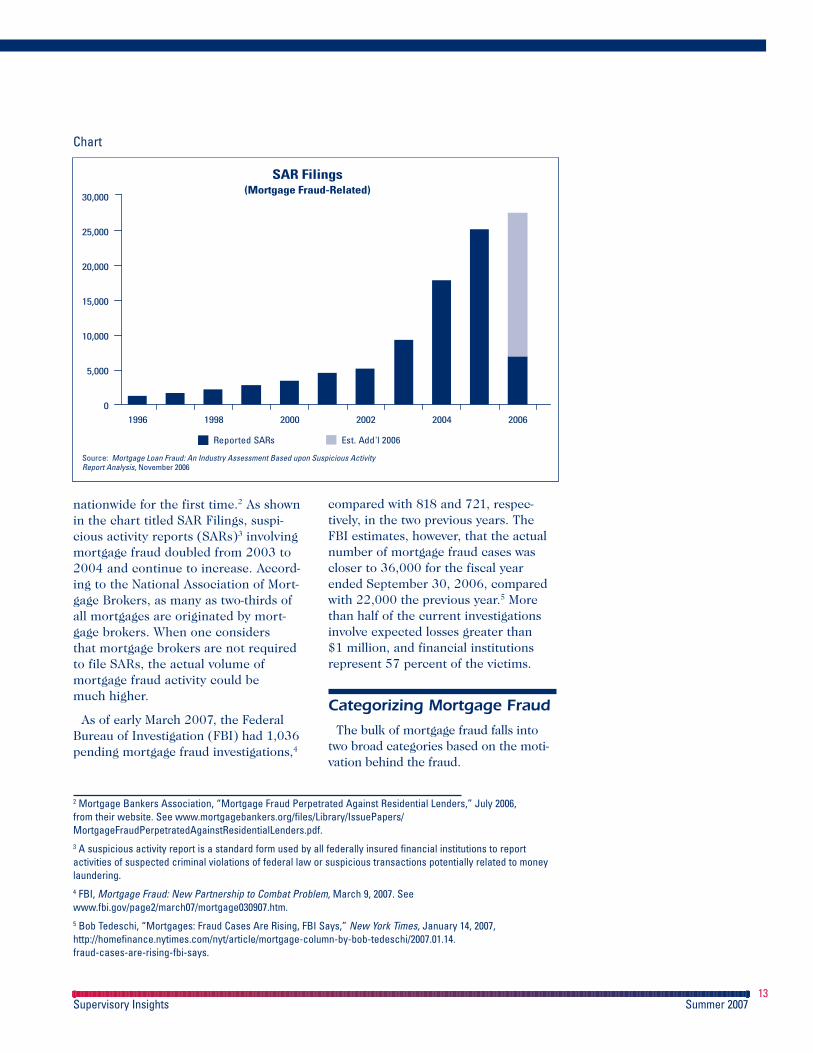

The following example demonstratesthe egregious nature of mortgage fraud.Picture 1 was included in a fraudulentappraisal used to secure a $250,000mortgage loan on this home in Atlanta,Georgia. However, the appraiser failed to

include the second picture, which showsthe rear view of the property! The loanwas granted, and the lender incurred amaterial loss upon subsequent foreclo-sure and disposition of the property.1

This article explores common typesof mortgage fraud, focusing on exam-ples from a recent poll of FDIC examin-ers. The authors also offer suggestionsand links to additional information forfurther support in mitigating the risksof mortgage fraud.

Mortgage Fraud Reaches NewHeights

Mortgage fraud activity has increasedmarkedly in recent years. In 2005,reported losses associated with mort-gage fraud passed the $1 billion mark

1 Ann D. Fulmer, Vice President of Industry Relations, Interthinx™; HUD STOP Conference, June 22, 2006,Savannah, Georgia.

Supervisory Insights Summer 2007

Staying Alert to Mortgage Fraud

Picture 1

Picture 2

13

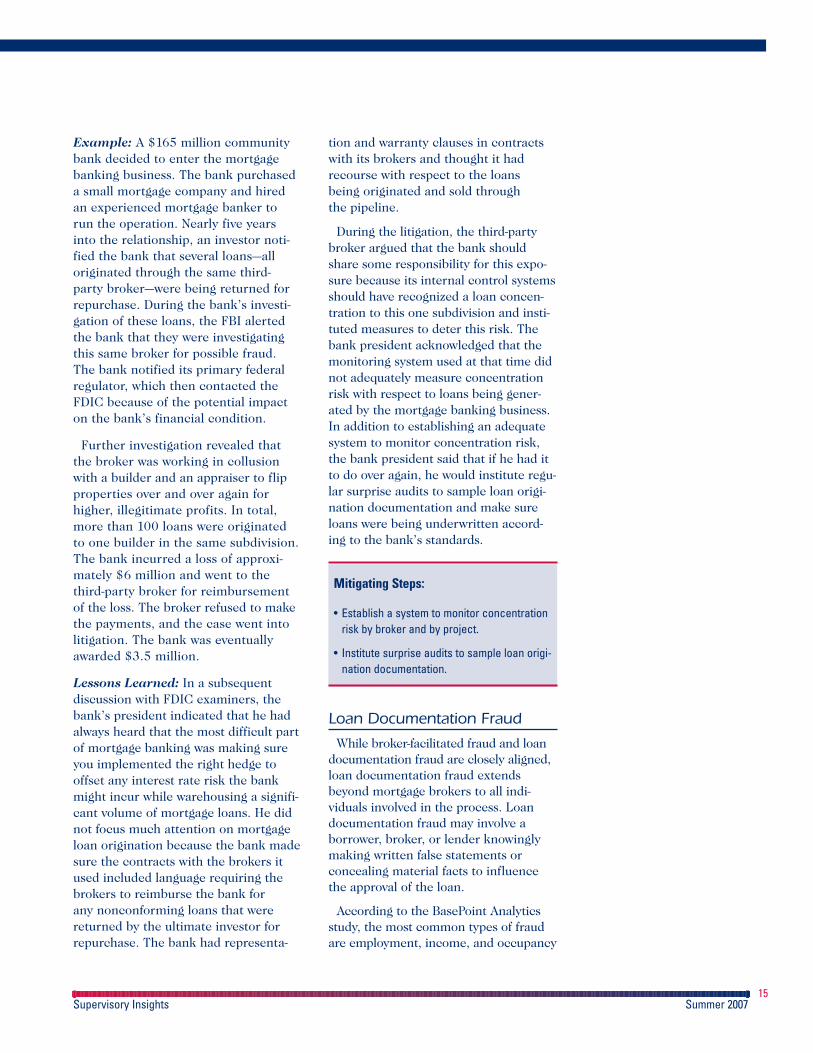

nationwide for the first time.2 As shownin the chart titled SAR Filings, suspi-cious activity reports (SARs)3 involvingmortgage fraud doubled from 2003 to2004 and continue to increase. Accord-ing to the National Association of Mort-gage Brokers, as many as two-thirds ofall mortgages are originated by mort-gage brokers. When one considersthat mortgage brokers are not requiredto file SARs, the actual volume ofmortgage fraud activity could bemuch higher.

As of early March 2007, the FederalBureau of Investigation (FBI) had 1,036pending mortgage fraud investigations,4

compared with 818 and 721, respec-tively, in the two previous years. TheFBI estimates, however, that the actualnumber of mortgage fraud cases wascloser to 36,000 for the fiscal yearended September 30, 2006, comparedwith 22,000 the previous year.5 Morethan half of the current investigationsinvolve expected losses greater than$1 million, and financial institutionsrepresent 57 percent of the victims.

Categorizing Mortgage Fraud

The bulk of mortgage fraud falls intotwo broad categories based on the moti-vation behind the fraud.

Supervisory Insights Summer 2007

2 Mortgage Bankers Association, “Mortgage Fraud Perpetrated Against Residential Lenders,” July 2006,from their website. See www.mortgagebankers.org/files/Library/IssuePapers/MortgageFraudPerpetratedAgainstResidentialLenders.pdf.3 A suspicious activity report is a standard form used by all federally insured financial institutions to reportactivities of suspected criminal violations of federal law or suspicious transactions potentially related to moneylaundering. 4 FBI, Mortgage Fraud: New Partnership to Combat Problem, March 9, 2007. Seewww.fbi.gov/page2/march07/mortgage030907.htm.5 Bob Tedeschi, “Mortgages: Fraud Cases Are Rising, FBI Says,” New York Times, January 14, 2007, http://homefinance.nytimes.com/nyt/article/mortgage-column-by-bob-tedeschi/2007.01.14.fraud-cases-are-rising-fbi-says.

SAR Filings(Mortgage Fraud-Related)

Source: Mortgage Loan Fraud: An Industry Assessment Based upon Suspicious Activity Report Analysis, November 2006

Reported SARs Est. Add'l 2006

30,000

25,000

20,000

15,000

10,000

5,000

01996 1998 2000 2002 2004 2006

Chart

14Supervisory Insights Summer 2007

Staying Alert to Mortgage Fraudcontinued from pg. 13

n Fraud for property typicallyinvolves a borrower who will over-state income or asset values onhis or her financial statement toqualify for a loan to purchase ahome. In many of these cases,expectations are that if the incomedoes not rise to meet the payment,the home will be sold at a profitfrom appreciation.

n Fraud for profit involves morecomplicated schemes and presentsa higher exposure to the market.Fraudulent methods are used toacquire and dispose of property withthe inflated profits going to theperpetrators of the fraudulent trans-action. Participants in these fraudu-lent transactions involve a varietyof insiders and third parties: strawborrowers, sellers, loan originators,brokers, agents, appraisers, builders,and developers. Opportunities forfraud for profit involving insidersare limited only by the perpetrator’simagination.6

Case Studies: Reports fromExaminers

Bearing headlines such as “EightIndicted in Loan Scam” (Dallas Morn-ing News, March 9, 2007) and “Mort-gage Fraud Alleged in 149 Transactions”(Journal Gazette, Fort Wayne, Indiana,April 1, 2007), the media are filled withstories demonstrating the pervasivenessof mortgage fraud. Rarely, however, dothese stories offer insights into whatmight have been done to detect orprevent the fraud or the effect of thefraud on the insured institutionsinvolved.

To get a picture of how mortgagefraud might be affecting insured finan-cial institutions, and to provide somepractical advice, the authors askedexaminers from across the country toprovide examples of the more commontypes of fraud they were encountering.The types of fraud most prevalent inexaminers’ responses were

n Broker-facilitated fraud;

n Loan documentation fraud;

n Appraisal fraud;

n Property flipping; and

n Misapplication of funds fromconstruction or rehabilitation projects.

As illustrated in the examples thatfollow, examiners are often not theones to first discover a case of fraud.The vast majority of fraud instancesare discovered and reported by theinstitutions themselves.

Broker-Facilitated Fraud

According to a study by BasePointAnalytics LLC, broker-facilitated fraudhas surfaced as the most prevalentsegment of mortgage fraud nationwide.7

Broker-facilitated mortgage fraud occurswhen a broker materially misrepresents,misstates, or omits information that aloan officer relies on to make the deci-sion to extend credit.8 Broker-facilitatedfraud can be fraud for property, fraudfor profit, or a combination of both. Forexample, the borrower may be commit-ting the fraud with the primary interestof obtaining a home, while the brokerfacilitating the fraud is motivated byprofit from closing the loan. The follow-ing represents a case of fraud for profit.

6 The Detection, Investigation and Deterrence of Mortgage Loan Fraud Involving Third Parties: A White Paper,Federal Financial Institutions Examination Council (FFIEC) Fraud Investigations Symposium, February 2005,www.ffiec.gov/exam/3P_Mtg_Fraud_wp_oct04.pdf.7 BasePoint Analytics LLC, Broker-Facilitated Fraud—The Impact on Lenders: A White Paper (2006), www.basepointanalytics.com/mortgagewhitepapers.html. 8 Broker-Facilitated Fraud.

15Supervisory Insights Summer 2007

Example: A $165 million communitybank decided to enter the mortgagebanking business. The bank purchaseda small mortgage company and hiredan experienced mortgage banker torun the operation. Nearly five yearsinto the relationship, an investor noti-fied the bank that several loans—alloriginated through the same third-party broker—were being returned forrepurchase. During the bank’s investi-gation of these loans, the FBI alertedthe bank that they were investigatingthis same broker for possible fraud.The bank notified its primary federalregulator, which then contacted theFDIC because of the potential impacton the bank’s financial condition.

Further investigation revealed thatthe broker was working in collusionwith a builder and an appraiser to flipproperties over and over again forhigher, illegitimate profits. In total,more than 100 loans were originatedto one builder in the same subdivision.The bank incurred a loss of approxi-mately $6 million and went to thethird-party broker for reimbursementof the loss. The broker refused to makethe payments, and the case went intolitigation. The bank was eventuallyawarded $3.5 million.

Lessons Learned: In a subsequentdiscussion with FDIC examiners, thebank’s president indicated that he hadalways heard that the most difficult partof mortgage banking was making sureyou implemented the right hedge tooffset any interest rate risk the bankmight incur while warehousing a signifi-cant volume of mortgage loans. He didnot focus much attention on mortgageloan origination because the bank madesure the contracts with the brokers itused included language requiring thebrokers to reimburse the bank forany nonconforming loans that werereturned by the ultimate investor forrepurchase. The bank had representa-

tion and warranty clauses in contractswith its brokers and thought it hadrecourse with respect to the loansbeing originated and sold throughthe pipeline.

During the litigation, the third-partybroker argued that the bank shouldshare some responsibility for this expo-sure because its internal control systemsshould have recognized a loan concen-tration to this one subdivision and insti-tuted measures to deter this risk. Thebank president acknowledged that themonitoring system used at that time didnot adequately measure concentrationrisk with respect to loans being gener-ated by the mortgage banking business.In addition to establishing an adequatesystem to monitor concentration risk,the bank president said that if he had itto do over again, he would institute regu-lar surprise audits to sample loan origi-nation documentation and make sureloans were being underwritten accord-ing to the bank’s standards.

Mitigating Steps:

• Establish a system to monitor concentrationrisk by broker and by project.

• Institute surprise audits to sample loan origi-nation documentation.

Loan Documentation Fraud

While broker-facilitated fraud and loandocumentation fraud are closely aligned,loan documentation fraud extendsbeyond mortgage brokers to all indi-viduals involved in the process. Loandocumentation fraud may involve aborrower, broker, or lender knowinglymaking written false statements orconcealing material facts to influencethe approval of the loan.

According to the BasePoint Analyticsstudy, the most common types of fraudare employment, income, and occupancy

16

misrepresentations—all of which relateto documentation.9 The Mortgage AssetResearch Institute (MARI) reports thatin a sample of loans by one of MARI’sclients, 90 percent of stated incomeswere exaggerated by 5 percent or more,and 60 percent of stated incomes wereinflated by more than 50 percent.10 Theultimate effect of loan documentationfraud on property values and the overalleconomy remains to be seen. Loan docu-mentation fraud is most often fraud forproperty, although if the lender or brokeris aware of the deception, as in the firstexample below, fraud for profit (incomefor the lender or broker) may also beinvolved.

Example: A $43 million communitybank hired a mortgage loan officer fora new loan program designed to benefitminority individuals with poor or nocredit histories. The loan officer begangenerating consistent business, andmanagement did not closely monitorher activities. The loan officer providedcredit to individuals who were using falseor stolen Social Security numbers. Shealso accepted, and in some cases actuallygenerated, false or questionable docu-ments to support the loans, includingfalse rental and utility payment histories.The bank became aware of the problemonly when another institution, whichhad purchased some of these loans,conducted due diligence and discoveredthe falsified information. The bank hadto repurchase these loans, but the bank’stotal exposure has not yet been deter-mined. The FDIC became aware of thisfraud through a routine review of SARsfiled by both institutions.

Lessons Learned: A thorough back-ground check on the loan officer wouldhave disclosed that she used a false SocialSecurity number to obtain her positionwith the bank and falsified other informa-

tion on her employment application. Acall to her former employer would haverevealed that she had been terminatedfrom that financial institution for orches-trating the very same type of fraud. Inaddition, instituting periodic qualitycontrol measures, such as sampling loanfiles, could have identified these practicesearly and limited the bank’s exposure.

Mitigating Steps:

• Establish a “Know Your Employee” program.

• Conduct background checks on newemployees.

• Conduct periodic credit checks on existingemployees.

• Establish clearly defined quality controlrequirements.

• Provide ongoing employee oversight andtraining.

• Structure compensation agreements toinclude loan quality as a contributing factor.

Example: A $1 billion urban financialinstitution became heavily involved inwholesale mortgage lending and beganpressuring employees to increase loanproduction. A disgruntled employeenotified FDIC examiners about wide-spread documentation fraud in thebank’s residential mortgage bankingbusiness. Reportedly, intense pressurefrom senior management to increaseloan production resulted in a practice ofaltering documents by cutting and past-ing customer signatures on differentforms to manufacture false loans. Theseloans were being packaged and sold tothird-party investors, leaving the bankvulnerable to potential buyback claims.The disgruntled employee surrendereddocuments to the FDIC that bankmanagement allegedly told him to

Supervisory Insights Summer 2007

Staying Alert to Mortgage Fraudcontinued from pg. 15

9 Broker-Facilitated Fraud.10 Merle Sharick, Erin E. Omba, Nick Larson, and D. James Croft, “Eighth Periodic Mortgage Fraud Case Reportto Mortgage Bankers Association,” Mortgage Asset Research Institute, Inc. (April 2006), www.mari-inc.com/reports.html.

destroy in an effort to hide the files fromregulators. The FDIC continues to inves-tigate this case, including possible falsestatements by one senior manager thatmay result in a prohibition action, crimi-nal violations, and prosecution.

Lessons Learned: The board of directorsand the audit committee did not establishcomprehensive reporting and monitoringprocedures, largely delegating thisresponsibility to operating management.Information provided to the board wasusually informal and lacked adequate,useful detail. Examiners recommendedthat the board establish clear expecta-tions for the timing and reporting of peri-odic quality control initiatives (e.g., loandocumentation sampling). Examinersalso recommended that managementperform a risk assessment to determineareas of increased exposure and providefraud identification training to staff,including originators, processors, under-writers, and internal audit personnel.Properly trained staff can help identifyred flags such as white outs, squeezed-innames or numbers, and illegible signa-tures with no supporting identification orverification information.

Mitigating Steps:

• Adopt periodic quality control measures,including loan file sampling.

• Train personnel to identify and report redflags.

• Institute adequate internal reporting procedures.

Appraisal Fraud

Appraisal fraud is usually outrightfraud or negligence on the part of theappraiser, often in collusion with otherparties. Some institutions have internalappraisers, but most use outside compa-nies. Manipulating or inflating thecomparable locations, market values,and property characteristics are all

17

tactics of appraisal fraud. Questionablepractices include “windshield appraisals,”where appraisers merely drive by a prop-erty and use inappropriate comparablesthat will get the value where they want itto be. In some cases, appraisers mayfraudulently overstate the benefits of aparticular property to back into the valueneeded for the loan. Appraisal fraud canbe used to qualify an undervalued homefor a higher mortgage amount (usuallyfraud for property) or to inflate the valueof real estate so that the property can beresold or flipped quickly to a straw orduped buyer and the profit retained byperpetrators (fraud for profit). Under thefirst scenario, appraisers may be pres-sured by mortgage brokers or loan offi-cers to falsify an appraisal so that a loantransaction can be approved. Under thesecond scenario, the appraiser actuallyworks in collusion with other conspira-tors to perpetrate the fraud.

Example: A small community bank(total assets less than $250 million)became involved in an inflated appraisalfraud scheme. The bank discoveredinflated appraisals on residential prop-erties securing loans to two borrowerswhen those borrowers defaulted onthe debts. The bank later determinedthat one of the borrowers owned theappraisal firm that prepared the originalappraisals for these properties. Theborrowers allegedly worked in collusionwith bank loan officers to finance theseproperties at inflated values. In total,the bank financed dozens of residentialproperties, with a combined original(fraudulent) appraised value totalingapproximately $2 million. After thedefaults, these properties were reap-praised at less than one-third of theiroriginal appraised value. The banksuffered a significant loss, which hasbeen difficult for it to absorb. The FDICis seeking a removal/prohibition actionagainst the loan officers involved, whohave resigned from the bank. The FDICbecame aware of this fraud by reviewingSARs submitted by the institution.

Supervisory Insights Summer 2007

Lessons Learned: Once these activitieswere uncovered, the bank worked aggres-sively to identify all relevant exposure bygetting new appraisals and providingadequate loan loss reserves. However,some improvements to the bank’s loanreview and monitoring procedures couldhave helped the bank identify negativetrends prior to the borrowers defaultingon the debts. First, the bank’s monitor-ing procedures were not sophisticatedenough to establish a connectionbetween either the borrowers or theappraisals supporting these loans. As aresult, this increasing level of exposureremained largely undetected. Second,while each loan was relatively small, thecombined total of these loans was signifi-cant. However, because of the small sizeof each loan, the bank’s internal loanreview did not pick up any of the loans.The bank would have benefited by chang-ing the scope of its loan review to includea sampling of loans from all loan officers,regardless of the loan size. Finally, thebank was not completely familiar withthe appraisal firm used to value thecollateral supporting these loans. If theownership structure of the appraisal firmhad been investigated initially, the bankwould have discovered this apparentconflict of interest, which would havetriggered additional investigation.

Mitigating Steps:

• Develop reports that track problem loans byloan officer, broker, appraiser, underwriter,branch office, settlement agent, and so on.

• Vary the internal loan review scope toinclude a sample from all loan officers.

• Research the background and ownership ofappraisal firms. See 12 CFR 323 of FDIC Rulesand Regulations for additional guidelines onappraisal and appraiser requirements.

18

Property Flipping

Property flipping is the practice ofpurchasing properties and reselling themat artificially inflated prices to straw orduped buyers11 and is strictly fraud forprofit. Flipping schemes typically involvefraudulent appraisals, doctored loandocumentation, or inflated buyerincome. Financial incentives to buyers,investors, brokers, appraisers, and titlecompany employees are also commonand indicate the degree of collusionnecessary to flip a property. Based onexisting investigations and mortgagefraud reports, the FBI estimates that80 percent of all reported fraud lossesinvolve collaboration or collusion byindustry insiders.12 A particularly trou-blesome aspect of property flipping isthat it taints property sale databases andpresents the illusion of rising propertyvalues in neighborhoods where the flip-ping takes place.

Example: During a routine examinationof a $1 billion financial institution, exam-iners became suspicious when theynoticed that one loan officer workedapart from other loan originators andhad processing personnel dedicated tohis loan originations. Bank managementindicated the loan officer was the bank’shighest producer and that “even a badmonth was a good month” for that loanofficer. The loan officer maintained ahigh number of loan originations, eventhough he took no referrals from thephone queue. On further investigation,the FDIC discovered that the loan officerhad an undisclosed relationship with alocal mortgage broker. Examiners’review of the officer’s lending activityrevealed several loans that had been orig-inated, sold, and then quickly fell intoforeclosure. Properties were also refi-nanced rapidly, with an affiliate of the

Supervisory Insights Summer 2007

11 Vernon Martin, “Detection of Mortgage Fraud,” RMA Journal, September 2004, www.findarticles.com/p/articles/mi_m0ITW/is_1_87/ai_n14897572. 12 FBI, “Financial Crimes Report to the Public, Fiscal Year 2006.” Seehttp://www.fbi.gov/publications/financial/fcs_report2006/financial_crime_2006.htm.

Staying Alert to Mortgage Fraudcontinued from pg. 17

broker placing second mortgages on theproperty that would immediately be paidfrom the next refinance. A sample of theofficer’s loan documentation discoveredaltered or falsified account statements,purchase and sale agreements, incomefigures, credit reports, and verification ofdeposit forms. The loan officer has sinceresigned from the institution and is thesubject of an ongoing criminal investiga-tion. Total loss exposure to the bank isstill being determined; however, the bankhas already had to repurchase severalloans as a result of this officer’s actions.

Lessons Learned: Bank managementfocused on income generated by this loanofficer and overlooked or ignored severalkey matters that would normally triggerfurther investigation. First, the isolationof this loan officer from others, includingseparate processing support, allowed himto dominate transactions from start tofinish. The lack of dual control overthese transactions greatly enhanced theloan officer’s ability to perpetrate thefraud. Second, the lack of proper reviewand oversight allowed the relationshipwith the mortgage broker to remainundisclosed to management. Implement-ing periodic quality control audits toverify the accuracy and completeness ofdocumentation would have brought theseactivities to light, including the rapid refi-nancing of properties and falsified loansupport documentation.

Mitigating Steps:

• Verify the quality of business generated byhigh-volume producers.

• Establish dual control over loan processingand fund disbursement.

• Implement periodic audits of loan origina-tions by officers.

• Conduct postmortem reviews of loan lossesand look for common names of participantsin the loan origination or processing areas.

19

Misapplication of Funds fromConstruction or RehabilitationProjects

Construction or rehabilitation projectloans are normally established as operat-ing lines of credit. Borrowers make drawsupon these lines of credit and use thesefunds to complete various phases of aproposed construction or rehabilitationproject. Draws are usually matched tothe percentage of the project that iscomplete, with a final percentage heldback as an abundance of caution. Forexample, a builder may ask for a drawthat represents 20 percent of theloan/line total, with verified completionactually totaling around 23–25 percent.The draw is used to pay subcontractorsfor work performed, as well as to provideworking capital for the builder, whosefees are built into the line.

Under fraudulent circumstances,builders may use funds or draws on oneproject to pay for improvements relatedto another project, or may simply divertfunds or draws for their own enrichment—fraud for profit. When this happens,subcontractors do not get paid, and, insome cases, no improvements are madeto the property. In the end, the builderexhausts the line of credit, and the bankis left to dispose of a property with verylittle supporting value.

Example: A $365 million communitybank authorized 13 construction lines ofcredit to a local builder for the construc-tion of speculative houses—those builtwithout a buyer or signed purchase agree-ment. As soon as the lines were approved,the builder began requesting draws. Thebuilder used falsified sales contracts tomislead the loan officer into believingmany of the homes were presold. Theloan officer routinely advanced funds tothe builder and signed off on construc-tion inspection documentation withoutever actually inspecting the constructionsites. After some time had elapsed withno corresponding sales activity, the loan

Supervisory Insights Summer 2007

20

officer began pressing the builder aboutthe status of construction and requestsfor new money. The builder confessedthat no houses had been constructed on11 of the bank’s 13 construction lines.The bank ultimately recorded a loss of $2million on the $2.6 million constructionline. The builder was convicted of fraudand sent to federal prison. The FDICbanned the loan officer from banking.The loss had a significant impact on thebank’s earnings, and the institution’sreputation was tarnished as a result oflocal media coverage. The FDIC becameaware of this fraud by reviewing SARssubmitted by the institution.

Lessons Learned: The monetary rewardand success of attracting and signing aloan client is much more attractive thanthe subsequent job of properly adminis-tering the credit; however, both areequally important to a financial institu-tion. In this instance, the loan officerbecame busy with other responsibilitiesand did not devote the time necessary toproperly monitoring construction drawsand documenting the proper allocationof funds to each project. The institutionhad no established procedures or formsfor conducting and documenting on-siteinspections, except to check the “inspec-tion” box on the disbursement form.Consequently, to authorize a construc-tion draw and deter loan review atten-tion, the loan officer would falselyindicate on loan disbursement forms thatconstruction inspections had beencompleted. Loan oversight was limited toverifying that the “inspection” box waschecked, with no subsequent confirma-tion or review of supporting documenta-tion. In addition, the bank did not reviewor monitor the builder’s deposit accountactivity, which would have revealedconstruction draws being used for amultitude of purposes unrelated to theproject. Verifying the legitimacy of thesales contracts with the proposedpurchasers also would have immediatelyalerted the bank of a possible problem.

Mitigating Steps:

• Monitor construction draws.

• Complete and document on-site inspections.

• Verify sales contracts.

• Monitor builder checking account activity.

Establishing Controls: ACommonsense Approach

Fraud is often compared to a triangle,with the three points of the fraud trianglebeing motive, rationalization, and oppor-tunity. The element of opportunity isparticularly heightened at financial insti-tutions because of the cash and financialtransaction nature of the business. Ascan be seen from the examples and miti-gating steps in this article, developingand implementing a sound internalcontrol environment—including soundlending fundamentals, quality controlprocedures, and audit programs—is a keyfactor in reducing the opportunity for alltypes of mortgage loan fraud. While mostinstitutions are aware of these safeguards,the cost/benefit of internal controlssometimes precludes management frommaking internal controls a top priority.

In addition to the mitigating stepsalready identified, some banks areexploring automated fraud detectionproducts introduced over the past severalyears. These software applications searchbank loan databases and compareborrowers, loan participants, commonnames, addresses, employers, appraisers,and the like, to detect potential red flagsor signs of mortgage fraud. These prod-ucts produce summary ratings or reportsthat serve to identify loans or groups ofloans that may represent an increasedrisk of mortgage fraud and requirefurther investigation. The ultimate deci-sion as to whether these products repre-sent a cost-effective solution remains anindependent choice for each institution.However, it is important that all institu-

Supervisory Insights Summer 2007

Staying Alert to Mortgage Fraudcontinued from pg. 19

21

tions consider the potential impact offraud and establish adequate provisionsfor this risk as part of their normal prof-itability and budgeting process.

Conclusion

Mortgage loan fraud is a large andgrowing problem. It can occur in anyneighborhood and requires that allparties concerned maintain a high levelof vigilance. Bank management shouldkeep alert to fraud triggers, ask ques-tions, review mortgage documentation,perform verifications, and report suspi-cious activity to the appropriate regula-tory and law enforcement authorities in atimely manner. While even the best inter-nal control environment will not preventmortgage fraud in all instances, stronginternal controls, coupled with an alertand knowledgeable staff, are a financialinstitution’s best line of defense.

Ken A. EdwardsSupervisory Examiner, Albany, GA

Jeffry A. PetruyExaminer,Gainesville, FL

Corbin Harrison Examiner,Atlanta, GA

Rebecca A. BerrymanSenior Capital Markets andSecurities Specialist,Atlanta, GA

Timothy J. HubbyAssistant Regional Director,Atlanta, GA

Acknowledgments: The authors wouldlike to acknowledge the assistanceprovided by Stephen Corona, Office ofFederal Housing Enterprise Oversight;Barbara Nelan, Assistant United StatesAttorney, Northern District of Georgia;Sandra Sheley, Director of MortgageSupervision, Georgia Department ofBanking and Finance; Ed Slagle, SpecialAgent, and Gary L. Sherrill, SeniorSpecial Agent, Office of InspectorGeneral, FDIC.

Supervisory Insights Summer 2007

Community groups, industry-related coali-tions, regulatory authorities, and federal,state, and local governments have volumesof information and resources available toanyone looking for additional informationon mortgage fraud. Many states providewebsites with consumer information andonline access to forms used to reportfraud. The following is a list of a few of themany available resources:

The Detection, Investigation and Preventionof Insider Loan Fraud: A White Paper,FFIEC Fraud Investigations Symposium,May 2003

Mortgage Fraud Perpetrated Against Resi-dential Lenders, Mortgage Bankers Asso-ciation, July 2006

Financial Crimes Report to the Public,Federal Bureau of Investigation andDepartment of Justice, May 2005

Federal Deposit Insurance Corporation, RiskManagement Manual of Examination Poli-cies, Sections 9.1–Fraud, and Section10.1–Suspicious Activity and CriminalViolations

Websites:

www.occ.treas.gov: Office of the Comptrol-ler of the Currency (federal regulator fornational banks)

www.fdic.gov: Federal Deposit InsuranceCorporation (federal regulator for state-chartered nonmember banks)

www.ots.treas.gov: Office of Thrift Supervi-sion (federal regulator for federally char-tered savings institutions)

www.federalreserve.gov: Board of Gover-nors of the Federal Reserve System (regu-lator for state-chartered member banks)

www.hud.gov: Department of Housing andUrban Development

www.fbi.gov: Federal Bureau of Investigation

www.mortgagefraudblog.com: Centralclearinghouse on recent mortgage fraudschemes, indictments, and prevention

www.grefpac.org: Georgia Real EstateFraud Prevention and Awareness Coalition(and similar community groups throughoutthe country)

www.mbafightsfraud.mortgagebankers.com:Mortgage Bankers Association

www.ganet.org/dbf.dbf.html: Georgia Depart-ment of Banking and Finance (and otherappropriate state regulatory authorities)

Resource Links

in coastal areas stretching from southernTexas to the northern tip of Maine.2

Given Florida’s higher risk exposure,even higher increases in Florida wouldnot be unlikely.

Wind insurance premium increasesare having a direct negative effect oncommercial and residential borrowers’overall budgets, including their abilityto service debt. It has also been widelyreported that borrowers and investorsare becoming hesitant to buy propertiesaffected by significantly increasing insur-ance premiums. The reported slowing inreal estate sales activity in Florida maybe exacerbated by insurance issues.

The considerable concern to thebanking industry lies in the fact thatthe risk in much of its lending activity—loans secured by real estate—has histor-ically been mitigated with propertyinsurance, including coverage for winddamage. Prudent bankers will monitorthe effect of this issue on real estatemarkets in their geographic areas oflending, as well as the effect on theoverall economy. Concerned lenderswill also consider the potential effectsof changes in wind hazard insurancecoverage and premiums in underwrit-ing loans and in monitoring their over-all real estate loan portfolios.

Historical and InsuranceIndustry Perspective

After a series of hurricanes hit Floridain the 1940s and 1950s, the state beganpursuing a more consistent statewidebuilding code. In 1974, the state imple-mented a uniform building code systemthat seemed reliable until 1992,3 when

22

The banking industry has long reliedon real estate as collateral for vari-ous types of loans. Hazard insur-

ance has played a big role in mitigatingthe risk of loss of collateral value fromcatastrophic damage. Traditionally,examiners have cited inadequacies incollateral insurance coverage as techni-cal exceptions when reviewing loan files.But in today’s environment, issuesregarding insurance availability andaffordability may soon reach beyondanything considered technical.

In this article, we present an overviewof the impact of the rising cost, and insome cases the lack of availability, ofwind hazard insurance, with a focus onFlorida. Although the issue is not new toFlorida, it has intensified to the pointthat it is often labeled a crisis.

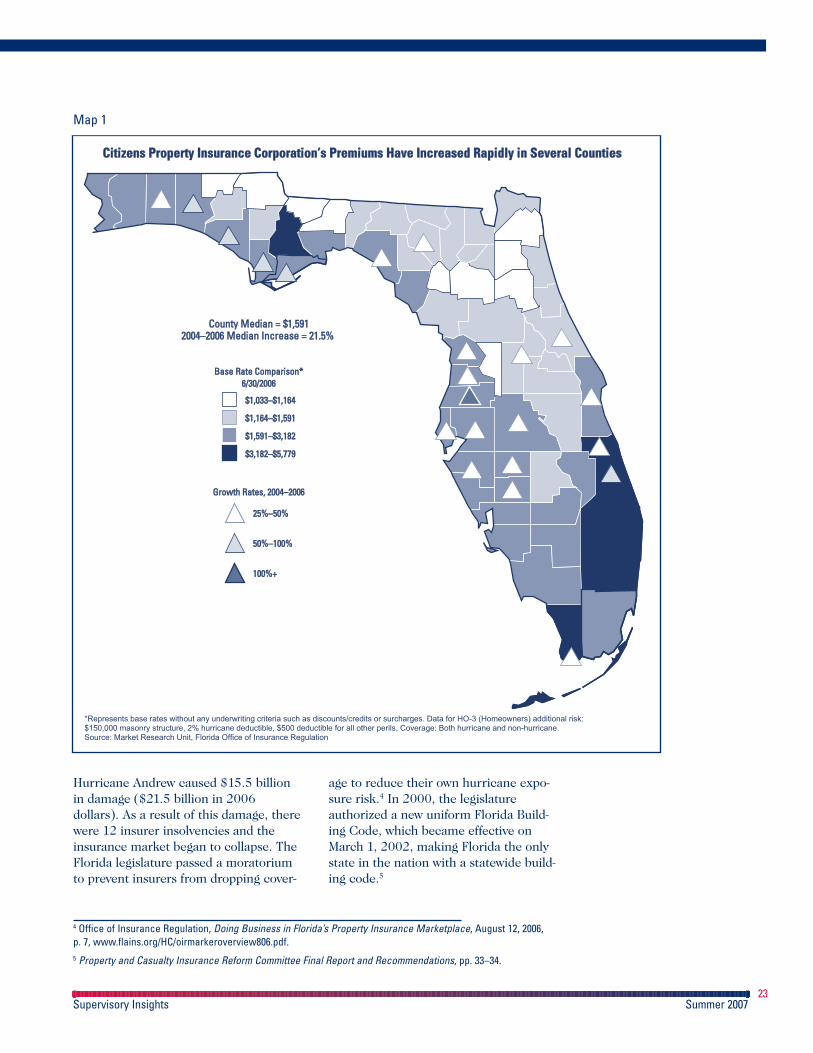

Virtually no part of the eastern andsouthern U.S. coastline is immunefrom the threat of severe storm systems.However, because of the growth inFlorida’s population and infrastructure,national storm modeling firms considerFlorida to have the highest level of riskin the nation for catastrophic stormdamage.1 Insurers that continue to offercoverage in high-risk areas are rapidlyand significantly increasing ratescharged to policyholders to replenishreserves, account for the updated model-ing forecasts, and pay the higher costof reinsurance from the anticipatedincreased risk. Map 1 illustrates howrising rates have already squeezed manyFlorida homeowners in terms of theirbudgets and spending habits. Accordingto the Insurance Information Institute,rates are likely to rise between 20 and100 percent over the next year for the43 percent of the U.S. population living

1 Property and Casualty Insurance Reform Committee, Property and Casualty Insurance Reform Committee FinalReport and Recommendations, November 15, 2006, p. 2, www.myfloridainsurancereform.com/finalrpt.htm.2 John Simmons, “Risky Business: With $58 Billion in Claims to Pay for Last Year Alone, U.S. Insurers Are JackingRates, Canceling Policies and Learning to Cope with Climate Change,” Fortune Magazine (November 2, 2006),retrieved March 26, 2007, from http://money.cnn.com/magazines/fortune/fortune_archive/2006/09/04/8384736/index.htm.3 Property and Casualty Insurance Reform Committee Final Report and Recommendations, p. 33.

Supervisory Insights Summer 2007

Wind Hazard Insurance: No Longer Just a Technical Exception

23Supervisory Insights Summer 2007

Hurricane Andrew caused $15.5 billionin damage ($21.5 billion in 2006dollars). As a result of this damage, therewere 12 insurer insolvencies and theinsurance market began to collapse. TheFlorida legislature passed a moratoriumto prevent insurers from dropping cover-

age to reduce their own hurricane expo-sure risk.4 In 2000, the legislatureauthorized a new uniform Florida Build-ing Code, which became effective onMarch 1, 2002, making Florida the onlystate in the nation with a statewide build-ing code.5

4 Office of Insurance Regulation, Doing Business in Florida’s Property Insurance Marketplace, August 12, 2006,p. 7, www.flains.org/HC/oirmarkeroverview806.pdf.5 Property and Casualty Insurance Reform Committee Final Report and Recommendations, pp. 33–34.

CCiittiizzeennss PPrrooppeerrttyy IInnssuurraannccee CCoorrppoorraattiioon’n’ss PPrreemmiiuummss HHaavvee IInnccrreeaasseedd RRaappiiddllyy iinn SSeevveerraall CCoouunnttiiees

*Represents base rates without any underwriting criteria such as discounts/credits or surcharges. Data for HO-3 (Homeowners) additional risk: $150,000 masonry structure, 2% hurricane deductible, $500 deductible for all other perils, Coverage: Both hurricane and non-hurricane.Source: Market Research Unit, Florida Office of Insurance Regulation

CCoouunnttyy MMeeddiiaann == $$11,,5599112200004–4–22000066 MMeeddiiaann IInnccrreeaassee == 2211..55%%

GGrroowwtthh RRaatteess,, 2200004–4–22000066