tiago lopes presentation airdev -...

TRANSCRIPT

AIRDEVAIRDEVAIRDEVAIRDEV conference

Airport PPPs in challenging times Airport PPPs in challenging times Airport PPPs in challenging times Airport PPPs in challenging times –––– transactions and changing business trendstransactions and changing business trendstransactions and changing business trendstransactions and changing business trends

Lisbon, April 2012

2AIRDEV Conference, April 2012 – Tiago Lopes

ALG recent transaction advice projects

Recent airport Due Diligence and Transaction Advic

Portugal and Spain

• Handling Lisboa, Porto e Faro (Aviapartner, 2011)

• Madrid e Barcelona (Ferrovial, 2011)

• Aeroporto privado confidencial (Abu Dhabi Airports Company, 2009)

• BOT Murcia (Aeromur, 2006-2010)

• Lleida ( Catalunha, 2008)

Rest of Europe

• Regionais da França (cliente confidencial, 2011)

• Abertis (fundo privado de infra-estruturas, 2010)

• Roma (fundo de infra-estruturas italiano, 2008)

• Taszár (Hungria, Sedesa Concessões, 2007)

• London City (UK, Consórcio Franco-Espanhol, 2006)

• Bruxelas (Bélgica, Ferrovial Aeropuertos, 2005)

• Bratislava (Eslováquia, Abertis, 2005)

Latin America

• BOT Porto Alegre (Brasil, cliente confidencial, 2011-12)

• concession Viracopos (Brasil, cliente confidencial, 2011)

• concession Aeroporto do Galeão (Brasil, cliente confidencial, 2011)

• BOT Natal (Brasil, cliente confidencial, 2011)

• BOT Cuzco (Peru, Proinversión, 2010-2011)

• concession Manta (Equador, Governo do Equador, 2010)

• Privatização dos do sul do Peru (Proinversión, 2009)

• Cabo Frio (Brasil, cliente confidencial, 2010)

• Regionais de São Paulo (Brasil, cliente confidencial, 2010)

Middle East

• Terminal do Kaia Hajj (Arábia Saudita, TBI, 2006)

Asia

• Aeroporto Internacional de Clark (Filipinas, Metro-Pacific Investments Corp., 2011)

ALG – Europraxis is an Indra Group company

3AIRDEV Conference, April 2012 – Tiago Lopes

Contents Market overview

Private investment in airport infrastructure

Transaction trends

Conclusions

4AIRDEV Conference, April 2012 – Tiago Lopes

Contents Market overview

Private investment in airport infrastructure

Transaction trends

Conclusions

5AIRDEV Conference, April 2012 – Tiago Lopes

Commercial aviation growth is strongly correlated with economic growth

and resilient to successive crises

RPK (trillion)

Source: ICAO, IMF, IATA, analysis ALG

World traffic evolution, 1960-2009

Passengers (RPKs) and Freight (RTKs) vs Economic Drivers

• The aviation industry has historically shown great resilience to crises, having grown consistently for the last 5 decades

• The growth of passenger and freight traffic is highly correlated with GDP growth and with real consumer spending (available income)

• The market has a cyclical behavior, where short periods of crisis are followed by relatively long periods of strong growth

CAGR last years

40 years 4,7%

30 years 6,7%

20 years 3,6%

10 years 3,6%

Emerging countries are the drivers of global economic growth

Cumulative growth 2008-2013 est.

6AIRDEV Conference, April 2012 – Tiago Lopes

Worldwide the air passenger traffic has recovered to pre-crisis levels.

Emerging markets are a key lever in this recovery

• In 2011 the air transport industry showed its resilience to the crisis, although with significant growth differences amongst regions

• The emerging economies are recovering at a much better pace than developed ones

• Latin America showed the highest growth in 2011Source: IATA ‘s Financial Monitor, ALG analysis

Passenger traffic – monthly ASKs Total air freight and passenger volumes

Continuous average growth of 4-5% /p.a. since the deepest point of the crisis in 2009

Approximately 2 years of cumulative losses in Europe and the US

Traffic up 5,4%4,9%

Traffic up 13,7%

Jan 2008Crash of Bear Stearns

Sep 2008Crash of Lehman Brothers

Apr 2010Iceland ash cloud (WE airspace greatly affected for almost one week)

Year on year comparison –2011 vs. 2010

RPK FTK

ASK growth rate

Passenger traffic(RPK)

Freight traffic (RTK)

-0,20%

4,50%

10,10%

14,40%

8,30%

3,50%6,40%

-5,00%

0,00%

5,00%

10,00%

15,00%

20,00%

Africa Asia/Pacific

Europe LatinAmerica

MiddleEast

N.America

TotalMarket

RPK growth rate

Monthly traffic (billions)

7AIRDEV Conference, April 2012 – Tiago Lopes

0,01

0,10

1,00

10,00

0 5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000 45.000

GDP/capita (US$)

Latin America

Other big markets

World average

New Zealand

USA

China

India

PortugalSpain

Canadá

Brazil

Mexico

Air passengers per inhabitant (propensity to fly) vs. per capita GDP, 2010

The economic growth of developing countries will underpin future air traffic growth…

For example a 50% increase in Brazilian GDP per capita (from the current US$10.000 to 15.000) could potentially result in an additional 120 million air passengers (increase from 0,4 to 1,0 trips per

habitant)

• There is a clear correlation between the per capita income and propensity to fly, although with variations among different countries

• All emerging economies are in the region where small increases in per capita income result in significant improvements in passengers per inhabitant

• Other factors with strong influence in the expansion of aviation are the reduction of fares, the liberalization of air transport and the consequent development of supply

Source: FMI, IATA, ATI, ALG analysis

Air

pax/ in

hab

itan

t (l

og

scale

)

Emerging economies

Mature markets

Brazil 2010: 0,4 trips per inhabitant

8AIRDEV Conference, April 2012 – Tiago Lopes

Which is reflected in industry traffic forecasts showing that passenger

numbers will (still) be increasing fast …

Airbus traffic forecasts to 2029

Source: Airbus

0 500 1.000 1.500 2.000 2.500 3.000 3.500 4.000 4.500

CIS

Africa

Latin America

Middle East

North America

Europe

Asia-Pacific 2009 traffic 2029 traffic

RPK (trilion)

+4.1%

+3.3%

+6.8%

+5.5%

+5.8%

+4.7%

% of 2009World RPK

% of 2029 World RPK

27%

28%

28%

6%

5%

3%

3%

33%

25%

20%

9%

6%

4%

3%

20-year world annual traffic

growth

4.8%

+5.6%

9AIRDEV Conference, April 2012 – Tiago Lopes

Contents Market overview

Private investment in airport infrastructure

Transaction trends

Conclusions

10AIRDEV Conference, April 2012 – Tiago Lopes

Private capital is being attracted to invest in airport infrastructure

development for a number of reasons…

• Major objectives leading governments to search for private partnership in airport

business:

• Funding infrastructure/ capacity needs with private investment

• Finding financial resources in order to fund other government projects / priorities

• Improving airports a economic performance and level of service by involving an highly experienced airport operator

• Transferring airport project development risk to a private party

• Specificity of airport business is that the traffic, construction, operations and financing

risks are usually fully transferred to the private partner within the limits of the risk

mitigation scheme provided by the government

• Private partnership solutions may apply to…

• Full airport infrastructures

• Specific airport infrastructures such as passenger terminals, cargo terminals,

runways, etc…

11AIRDEV Conference, April 2012 – Tiago Lopes

… so who is investing in airport infrastructure?

Financial institutions ContractorsAiport operators

• BAA

• Copenhagen Airport

• Fraport AG

• Schiphol Group

• AENA

• Aéroports de Paris

• YVRAS (Vancouver)

• Flughafen Zurich AG

• Singapore Changi

• Vienna Airport

• Malaysia Airports Holding

• TAV Airports Holding

• ADC & HAS

• Macquarie

• ABN AMRO Ventures BV

• Caisse des Depots

• Deutsche AssetManagement

• GE Capital

• AXA

• Citigroup

• Global InfrastructurePartners

• Goldman Sachs

• Blackstone Investment

• Advent

• Abertis

• Ferrovial Aeropuertos

• Hochtief

• Vinci Group GTM

• TAV

• Alterra Partners

Many private consortia have members of each of these groups

12AIRDEV Conference, April 2012 – Tiago Lopes

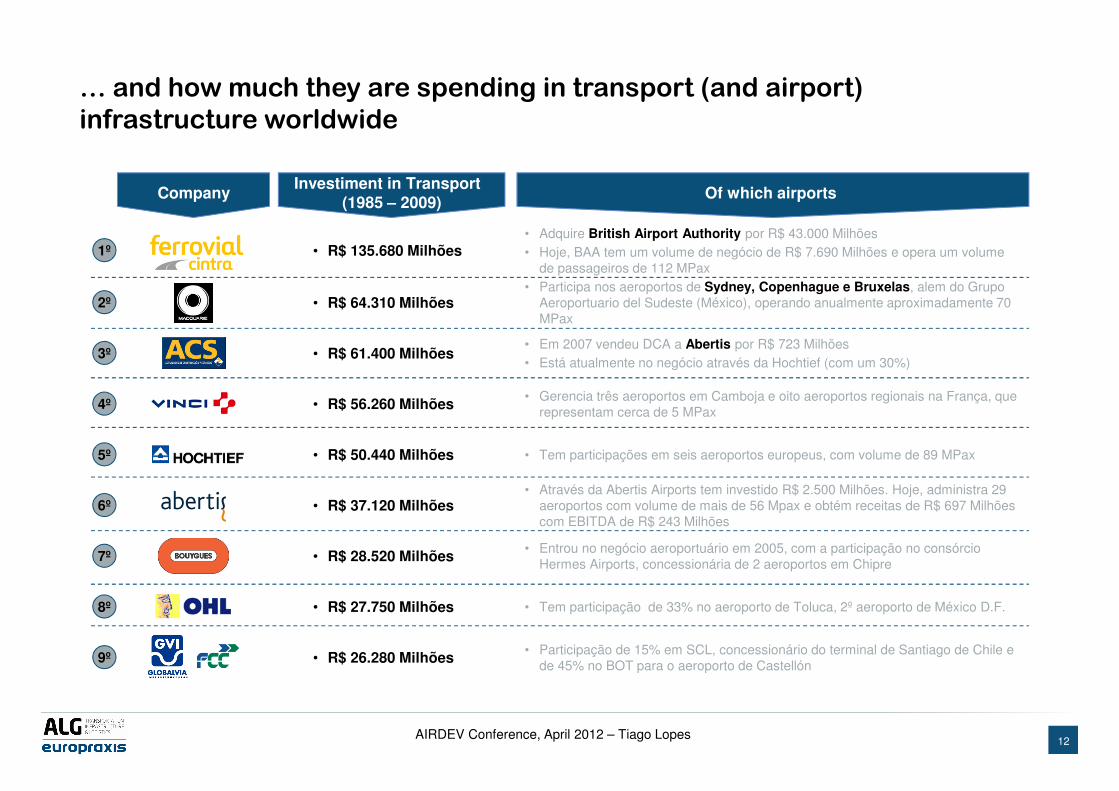

… and how much they are spending in transport (and airport)

infrastructure worldwide

CompanyInvestiment in Transport

(1985 – 2009)Of which airports

1º • R$ 135.680 Milhões• Adquire British Airport Authority por R$ 43.000 Milhões• Hoje, BAA tem um volume de negócio de R$ 7.690 Milhões e opera um volume

de passageiros de 112 MPax

2º • R$ 64.310 Milhões• Participa nos aeroportos de Sydney, Copenhague e Bruxelas, alem do Grupo

Aeroportuario del Sudeste (México), operando anualmente aproximadamente 70 MPax

3º • R$ 61.400 Milhões• Em 2007 vendeu DCA a Abertis por R$ 723 Milhões• Está atualmente no negócio através da Hochtief (com um 30%)

4º • R$ 56.260 Milhões• Gerencia três aeroportos em Camboja e oito aeroportos regionais na França, que

representam cerca de 5 MPax

5º • R$ 50.440 Milhões • Tem participações em seis aeroportos europeus, com volume de 89 MPax

6º • R$ 37.120 Milhões• Através da Abertis Airports tem investido R$ 2.500 Milhões. Hoje, administra 29

aeroportos com volume de mais de 56 Mpax e obtém receitas de R$ 697 Milhões com EBITDA de R$ 243 Milhões

7º • R$ 28.520 Milhões• Entrou no negócio aeroportuário em 2005, com a participação no consórcio

Hermes Airports, concessionária de 2 aeroportos em Chipre

8º • R$ 27.750 Milhões • Tem participação de 33% no aeroporto de Toluca, 2º aeroporto de México D.F.

9º • R$ 26.280 Milhões• Participação de 15% em SCL, concessionário do terminal de Santiago de Chile e

de 45% no BOT para o aeroporto de Castellón

13AIRDEV Conference, April 2012 – Tiago Lopes

How is private investment placed? There are four large types of private

investment vehicles in the airport industry…

Type of involvement

Description Risk profile Duration

Management contract

Private investor runs airport infrastructure or part of it. For

example: terminal or retail area. No ownership of infrastructure

Private operator brings operational and management

knowledge. Can be incentivized for good

performance

short to medium term (4 to 10 years)

BOT/ concession type

Private investor(s) is awarded concession to operate and

manage infrastructure. A number of alternatives are possible:

DBFOT, BOO, BTO,

Private investor hasmandatory investment level in

infrastructure under BOT (Build Operate Transfer)

scheme. Airport reverts to government at end of

concession

long period, usually 20 to 40 years (necessary to

make return on investment in infrastructure)

Trade saleSignificant share (minority or

majority) of airport company sold directly to private investors

Private investors usually bring operational and managerial experience and access to

capital

n.a.

Share flotation/ IPO

Shares sold on stock exchangeRisk transferred to new

shareholders depending on share of equity placed

n.a.

Type of involvement of private sector in airport transactions

Incre

asin

g r

isk level fo

r p

rivate

in

vesto

r

14AIRDEV Conference, April 2012 – Tiago Lopes

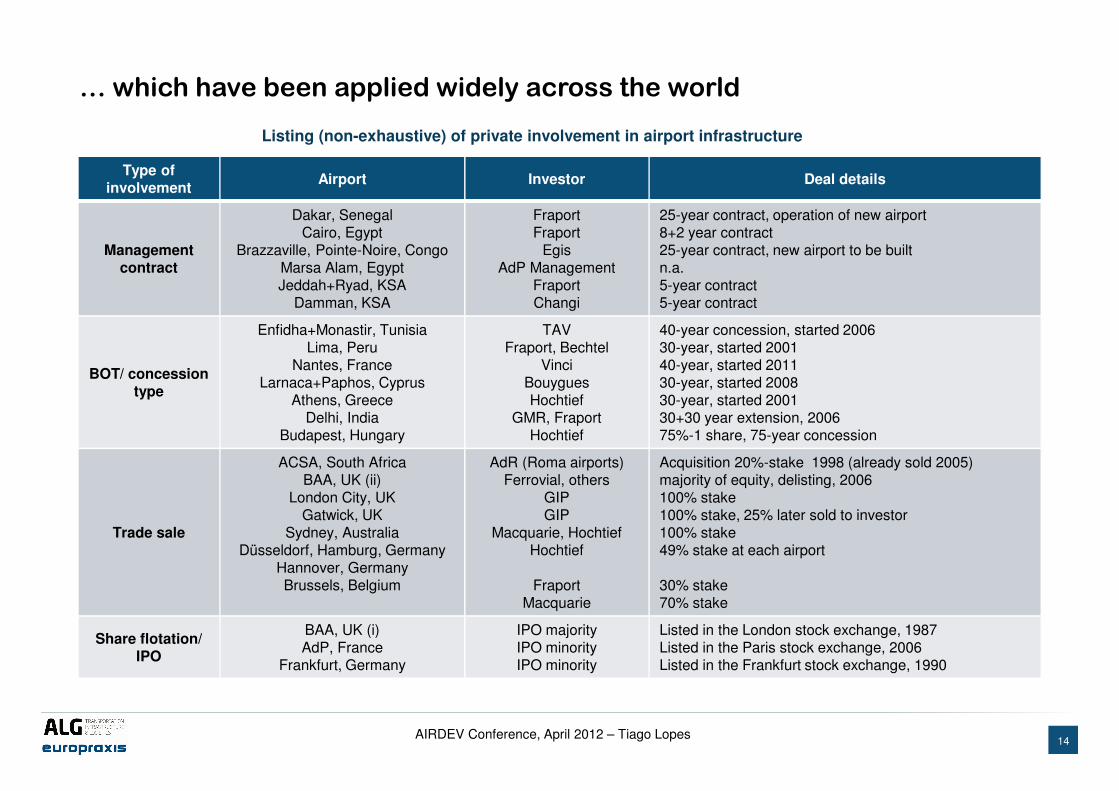

… which have been applied widely across the world

Type of involvement

Airport Investor Deal details

Management contract

Dakar, SenegalCairo, Egypt

Brazzaville, Pointe-Noire, CongoMarsa Alam, EgyptJeddah+Ryad, KSA

Damman, KSA

FraportFraport

EgisAdP Management

FraportChangi

25-year contract, operation of new airport8+2 year contract25-year contract, new airport to be builtn.a.5-year contract5-year contract

BOT/ concession type

Enfidha+Monastir, TunisiaLima, Peru

Nantes, FranceLarnaca+Paphos, Cyprus

Athens, GreeceDelhi, India

Budapest, Hungary

TAVFraport, Bechtel

VinciBouyguesHochtief

GMR, FraportHochtief

40-year concession, started 200630-year, started 200140-year, started 201130-year, started 200830-year, started 200130+30 year extension, 200675%-1 share, 75-year concession

Trade sale

ACSA, South AfricaBAA, UK (ii)

London City, UKGatwick, UK

Sydney, AustraliaDüsseldorf, Hamburg, Germany

Hannover, GermanyBrussels, Belgium

AdR (Roma airports)Ferrovial, others

GIPGIP

Macquarie, HochtiefHochtief

FraportMacquarie

Acquisition 20%-stake 1998 (already sold 2005)majority of equity, delisting, 2006100% stake100% stake, 25% later sold to investor100% stake49% stake at each airport

30% stake70% stake

Share flotation/ IPO

BAA, UK (i)AdP, France

Frankfurt, Germany

IPO majorityIPO minorityIPO minority

Listed in the London stock exchange, 1987Listed in the Paris stock exchange, 2006Listed in the Frankfurt stock exchange, 1990

Listing (non-exhaustive) of private involvement in airport infrastructure

15AIRDEV Conference, April 2012 – Tiago Lopes

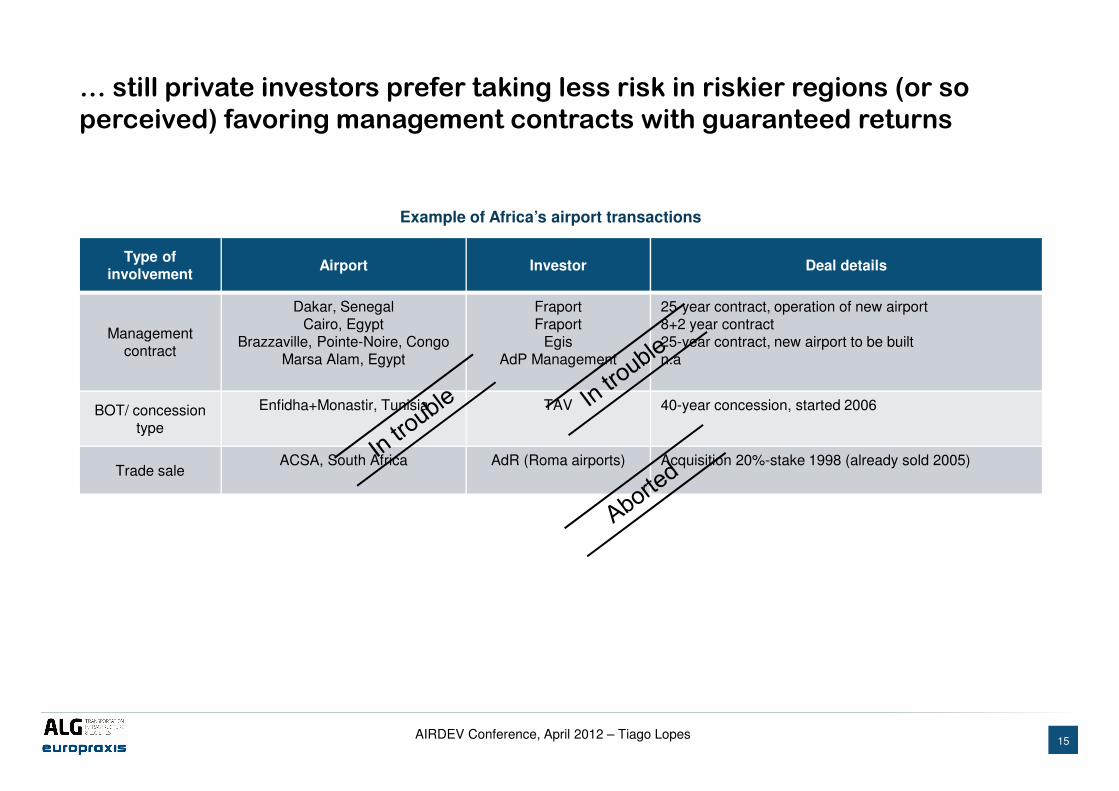

… still private investors prefer taking less risk in riskier regions (or so

perceived) favoring management contracts with guaranteed returns

Type of involvement

Airport Investor Deal details

Management contract

Dakar, SenegalCairo, Egypt

Brazzaville, Pointe-Noire, CongoMarsa Alam, Egypt

FraportFraport

EgisAdP Management

25-year contract, operation of new airport8+2 year contract25-year contract, new airport to be builtn.a

BOT/ concession type

Enfidha+Monastir, Tunisia TAV 40-year concession, started 2006

Trade saleACSA, South Africa AdR (Roma airports) Acquisition 20%-stake 1998 (already sold 2005)

Example of Africa’s airport transactions

16AIRDEV Conference, April 2012 – Tiago Lopes

Contents Market overview

Private investment in airport infrastructure

Transaction trends

Conclusions

17AIRDEV Conference, April 2012 – Tiago Lopes

Airport transactions – PPPs, trade sales, IPOs - as a business solution in

the airport industry only began in the late 80’s…

• Between 1987 and 1995, the number of “privatizations” was limited – only 13 transactions with reduced

transaction values

• Between 1996 and 2001, due to traffic increase, the number of transactions – under various schemes –

increased up to 55 transactions over the period. Transaction values were for the first time above 1 bnUSD,

although dependent on individual transactions

• After 09/11/2001 till 2004, the number of transactions slowed down significantly

Deal flow: airport transaction values per year

Source: Credit Suisse, AdPi

bnUSD

18AIRDEV Conference, April 2012 – Tiago Lopes

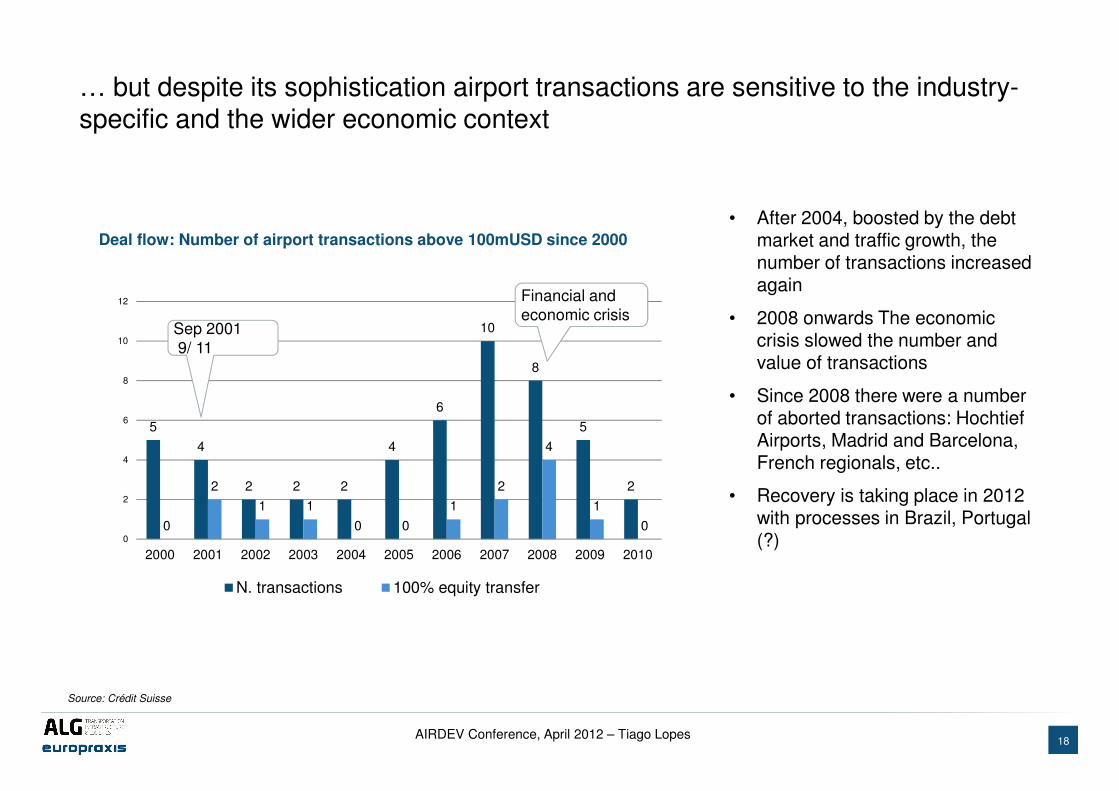

… but despite its sophistication airport transactions are sensitive to the industry-specific and the wider economic context

Deal flow: Number of airport transactions above 100mUSD since 2000

5

4

2 2 2

4

6

10

8

5

2

0

2

1 1

0 0

1

2

4

1

00

2

4

6

8

10

12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

N. transactions 100% equity transfer

Source: Crédit Suisse

Sep 20019/ 11

Financial and economic crisis

• After 2004, boosted by the debt market and traffic growth, the number of transactions increased again

• 2008 onwards The economic crisis slowed the number and value of transactions

• Since 2008 there were a number of aborted transactions: HochtiefAirports, Madrid and Barcelona, French regionals, etc..

• Recovery is taking place in 2012 with processes in Brazil, Portugal (?)

19AIRDEV Conference, April 2012 – Tiago Lopes

The economic crisis also had an impact on airport valuation: EBITDA multiples have decreased significantly after 2008

Transaction valuation in large airport acquisition deals (+100 mUSD): EBITDA multiples and Financial leverage

Source: HSBC, 2010

0

5

10

15

20

25

30

35

Transaction Value /Last Twelve Months EBITDA

Transaction date 2000 2002 2004 2004 2005 2005 2006 2006 2007 2007 2009 2012 (?)

Target AdR Sydney Brussels TBICopen-hagen

Budapest BAA London City Exeter Budapest Gatwick ANA

Buyer Leonardo

Southern Cross

(Macquarie + Hochtief)

MacquarleACDL

(Abertis + AENA)

Macquarle BAA

ADI (Ferrovial +

CDPQ + GIC)

AIG + GIPRegional and city airports

Hochtlef + GIC +

CDPQ + KfW

GIP (?)

Transaction value (€m) 2,700 3,150 1,650 1,050 2,600 2,000 23,400 1,100 100 1,950 1,6502,000 to

2,400

Share (%) 52% 100% 70% 100% 41% 75% 100% 100% 100% 75% 100% 100%

PAX at acquisition (m) 27.1 26.0 15.0 18.0 19.0 7.8 122.7 2.0 1.0 8.2 32.3 30.0 +

10 to 12x

20AIRDEV Conference, April 2012 – Tiago Lopes

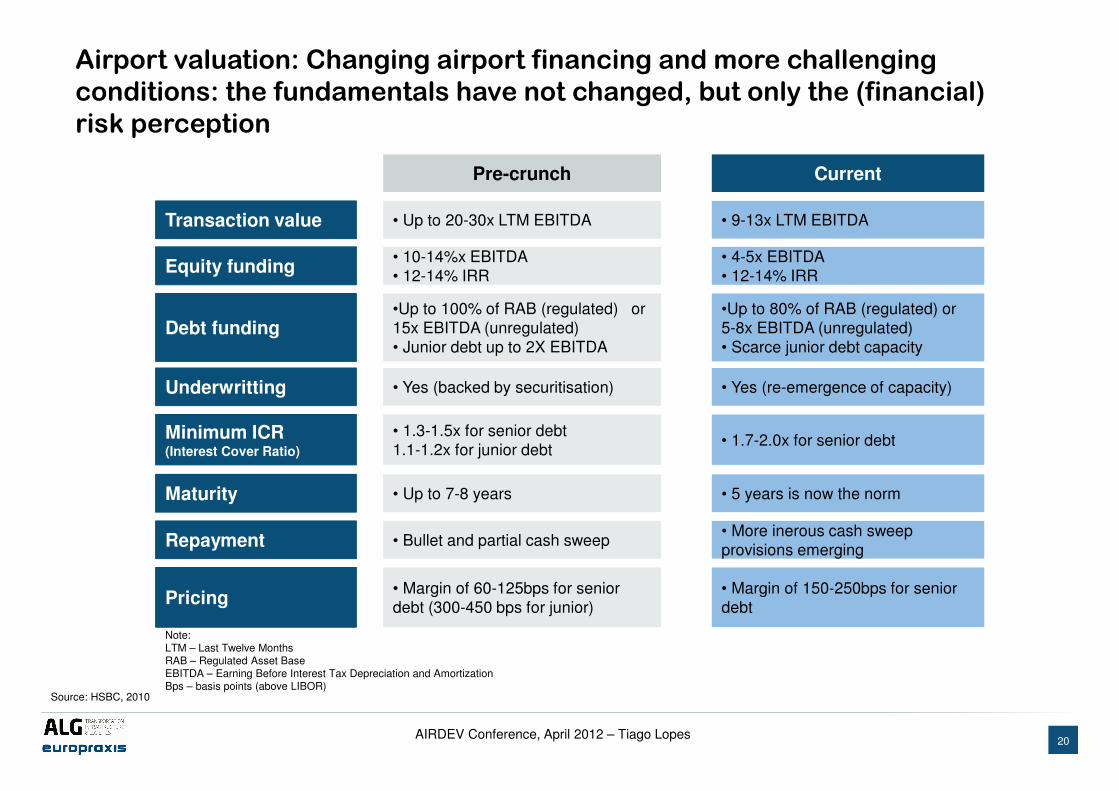

Airport valuation: Changing airport financing and more challenging

conditions: the fundamentals have not changed, but only the (financial)

risk perception

Source: HSBC, 2010

Transaction value

Equity funding

Debt funding

Underwritting

Minimum ICR(Interest Cover Ratio)

Maturity

Repayment

Pricing

Pre-crunch Current

• Up to 20-30x LTM EBITDA • 9-13x LTM EBITDA

• 10-14%x EBITDA• 12-14% IRR

• 4-5x EBITDA• 12-14% IRR

•Up to 100% of RAB (regulated) or 15x EBITDA (unregulated)• Junior debt up to 2X EBITDA

•Up to 80% of RAB (regulated) or 5-8x EBITDA (unregulated)• Scarce junior debt capacity

• Yes (backed by securitisation) • Yes (re-emergence of capacity)

• 1.3-1.5x for senior debt1.1-1.2x for junior debt

• 1.7-2.0x for senior debt

• Up to 7-8 years • 5 years is now the norm

• Bullet and partial cash sweep• More inerous cash sweep provisions emerging

• Margin of 60-125bps for senior debt (300-450 bps for junior)

• Margin of 150-250bps for senior debt

Note: LTM – Last Twelve MonthsRAB – Regulated Asset BaseEBITDA – Earning Before Interest Tax Depreciation and AmortizationBps – basis points (above LIBOR)

21AIRDEV Conference, April 2012 – Tiago Lopes

Long term concessions and trade sales have resulted in higher valuations than IPOs Long term concessions and trade sales have resulted in higher valuations than IPOs

Stock listed airports (IPO)

Recent market valuations

Concessions and direct sales

Unweightedaverage 8,5x

Unweihtedaverage 15x

0

5

10

15

20

Mala

ysia

AIA

VIE

BIA

C

CF

H

BA

A

AD

R

Mala

ysia

AIA

Vie

nn

a

BIA

C

CP

H

BA

A

AD

R

Bir

min

gh

am

East

Mid

lan

ds

Han

no

ver

Belf

ast

Du

sseld

orf

Pre

stw

ick

Lu

ton

Beijin

g (

AD

P)

AC

SA

Bri

sto

l

Ham

bu

rg

Wellin

gto

n

Can

berr

a

Arg

en

tin

a

Melb

ou

rne

Card

iff

Co

llan

gaza

SA

VE

Bri

sb

an

e

Darw

in A

P

Pert

h

Ad

ela

ide

Unweighted average(1) 8,2x

Despite the current negative conditions, the increased competition and the

sector’s inherent conditions (good long-term returns) have pushed

EV/EBITDA in acquisitions to higher values than those currently traded

(1) Unweighted average IPO and concession values(2) LCY: EBITDA estimated by Morgan Stanley in 2006

(EV/EBITDA) multiples

Bu

dap

est

32

LC

Y (

2)

28

Currently accepted EBITDA multiples

22AIRDEV Conference, April 2012 – Tiago Lopes

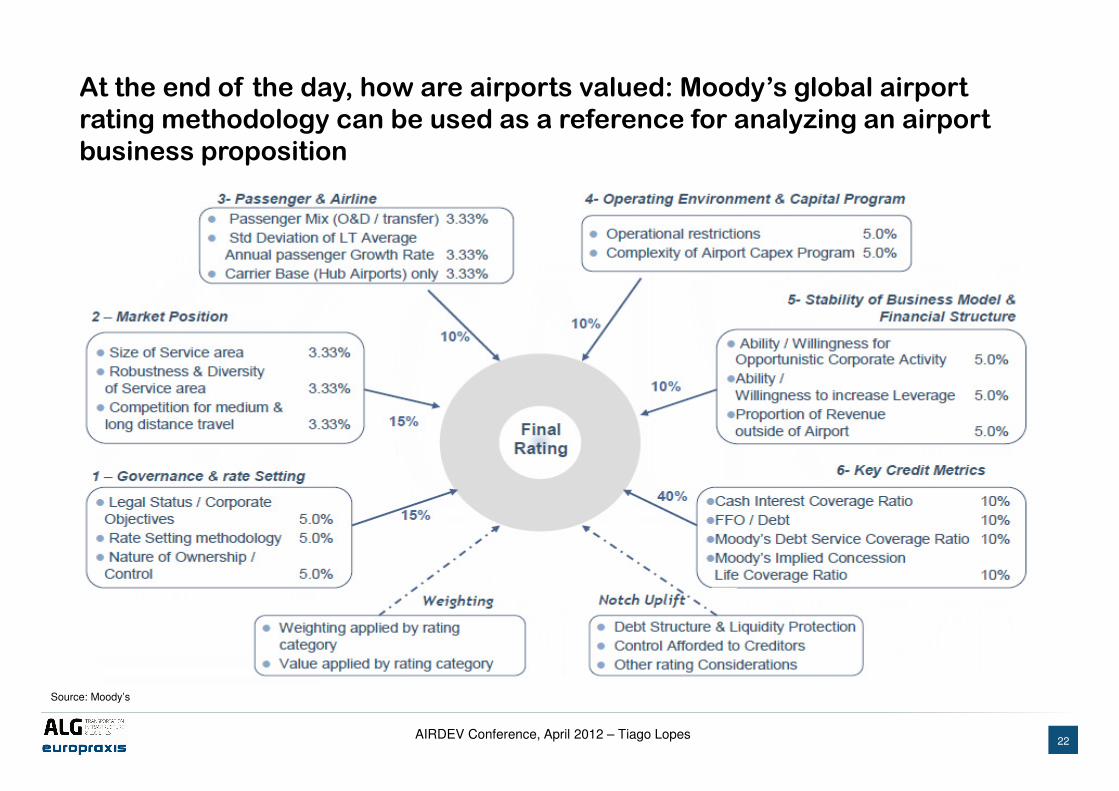

At the end of the day, how are airports valued: Moody’s global airport

rating methodology can be used as a reference for analyzing an airport

business proposition

Source: Moody’s

23AIRDEV Conference, April 2012 – Tiago Lopes

Contents Market overview

Private investment in airport infrastructure

Transaction trends

Conclusions

24AIRDEV Conference, April 2012 – Tiago Lopes

A new paradigm is emerging with the increase of private capital in the

airport industry, the loss of exuberance in the markets and the

• Airports are becoming less of singe prized assets and more like traded commodities

• The increased capital needs and the different types of investment “architecture” and risk profile have attracted new types of investors e.g. contractors, pension funds

• There is a clear separation between airport managers and investors. For the first time in the industry you do NOT need to have expertise to own an airport

• The original goal of attracting private capital to build capacity is now becoming distorted. It is now becoming a cash source for governments in need e.g. Portugal

Source: Credit Suisse, AdPi

25AIRDEV Conference, April 2012 – Tiago Lopes

Tiago Lopes

www.alg-global.comwww.europraxis.com

LISBOATel: (+351) 21 313 90 60Fax (+351) 21 313 90 61 BARCELONA BEIJING BILBAO BUENOS AIRES CARACAS DUBÁI LIMA LONDRES MADRID MÉXICO D.F. MILÁN PARÍS RABAT SAO PAULO